Online Casual Games Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 22.68 Billion |

| Market Size (2031) | USD 29.51 Billion |

| Growth Rate (2026 - 2031) | 5.41% CAGR |

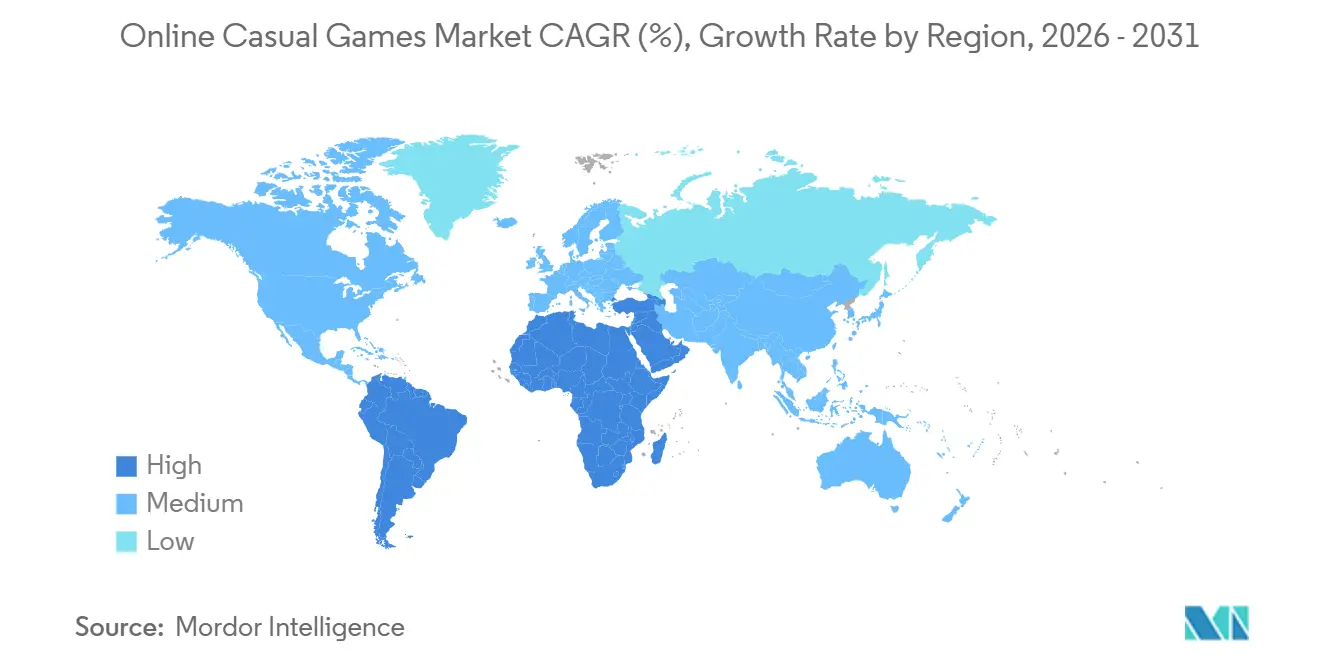

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Online Casual Games Market Analysis by Mordor Intelligence

The online casual games market was valued at USD 22.68 billion in 2026 and is projected to reach USD 29.51 billion in 2031, translating into a 5.41% CAGR over the forecast period. This expansion underscores a strategic pivot from single-channel monetization toward hybrid models that blend in-app purchases with rewarded advertising, a mix that captures discretionary micro-spends while preserving free access for price-sensitive users. Rising 5G coverage, sovereign investment funds that underwrite local studio formation, and privacy rules that push publishers toward first-party data loops collectively reinforce the sector’s resilience. Regulatory pressure on loot-box mechanics is steering design toward transparent battle-pass systems that stabilize lifetime value, while direct-to-consumer web shops in Europe are compressing platform fees and boosting average revenue per paying user. Competitive dynamics remain fluid because cross-platform engines have reduced development costs to the point where teams of three or four can launch globally polished titles.

Key Report Takeaways

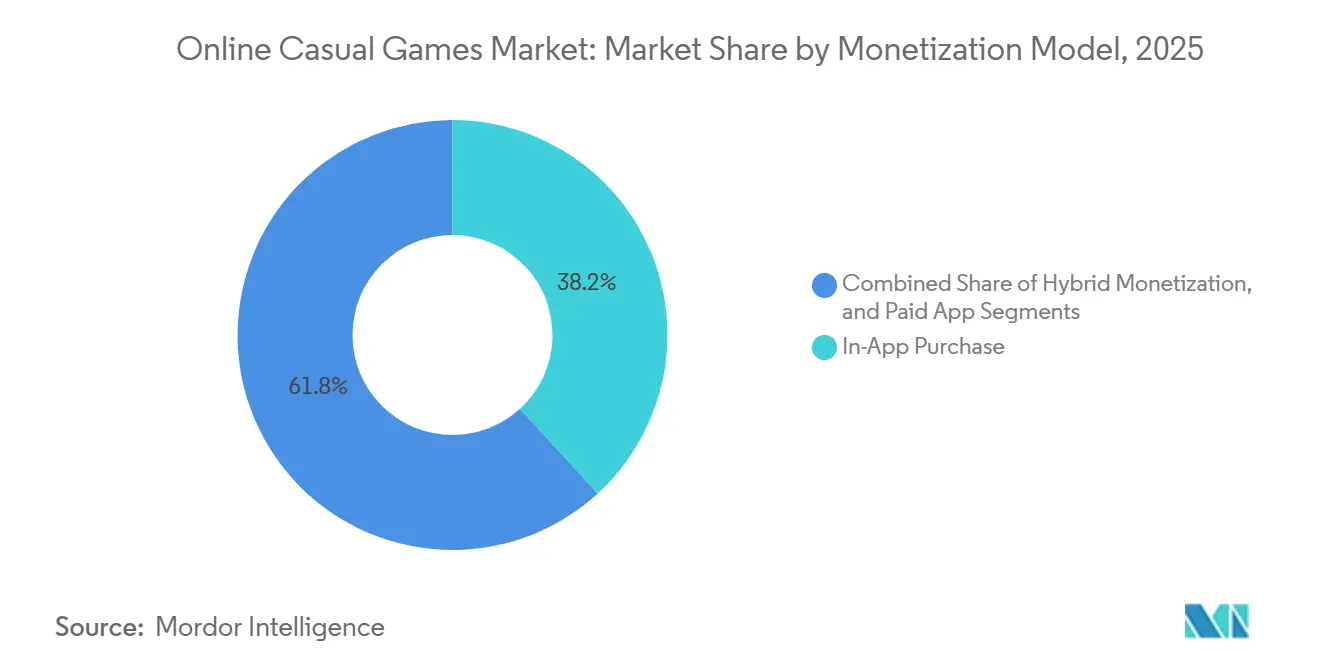

- By monetization model, in-app purchases led with 38.19% of revenue in 2025, while hybrid monetization is projected to advance at a 5.89% CAGR to 2031.

- By platform, smartphones accounted for 72.11% of the online casual games market share in 2025 and are forecast to grow at a 6.16% CAGR through 2031.

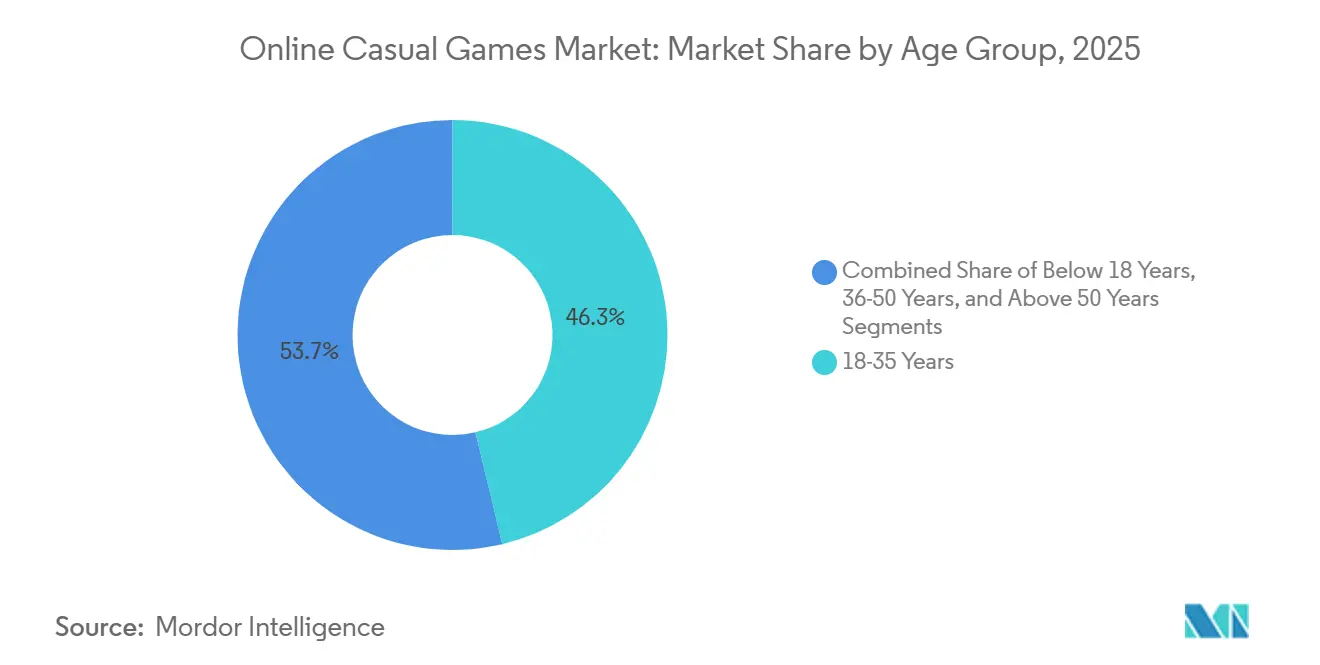

- By age group, the 18-35 cohort accounted for 46.29% of revenue in 2025, while the under-18 segment is set to expand at a 5.58% CAGR during the outlook period.

- By geography, Asia Pacific accounted for 35.48% of revenue in 2025, while the Middle East is expected to post the fastest CAGR of 5.92% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Online Casual Games Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing 5G smartphone penetration is accelerating mobile gaming adoption | +0.8% | Asia Pacific, Middle East, South America | Medium term (2-4 years) |

| Expansion of reward-based advertising networks is boosting casual title monetization | +0.9% | North America and Europe, spreading worldwide | Short term (≤ 2 years) |

| Cloud-streaming integration lowers hardware barriers in Southeast Asia | +0.6% | Core Southeast Asia, spill-over to South Asia | Medium term (2-4 years) |

| Cross-platform engines are slashing development costs for indie studios | +0.7% | Emerging markets in South America and Africa, global reach | Short term (≤ 2 years) |

| Direct-to-consumer web shops are reducing platform fees in Europe | +0.5% | Europe, early adoption in North America | Medium term (2-4 years) |

| AI-powered creative optimization is lowering CPI for hyper-casual titles | +0.4% | Middle East and North Africa, expanding into the Asia Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing 5G Smartphone Penetration Accelerating Mobile Gaming Adoption

Low-latency radio networks enable real-time multiplayer on handsets priced under USD 200, allowing publishers to port PC-quality assets without alienating budget buyers. Indonesia alone counts 155 million gamers who rely almost exclusively on mobile access, and sub-20-millisecond latency enables cloud-rendered experiences previously locked behind discrete GPUs. Tencent’s Dungeon and Fighter Mobile demonstrated the commercial upside by surpassing CNY 10 billion (USD 1.4 billion) in its first two post-launch months. As edge nodes extend into tier-2 cities, the performance gap between premium and entry-level devices narrows, democratizing access to content and expanding the online casual games market.

Expansion of Reward-Based Advertising Networks Boosting Casual Titles Monetization

Opt-in video ads have matured into the highest-yield format for casual games, with click-through rates averaging 8.2% in Q4 2024 compared with 1.1% for static banners. Completion rates exceed 90% because users receive guaranteed in-game value, a tradeoff that resonates with 18-35-year-olds who typically budget USD 5-15 a month for virtual goods. Server-side bidding by Google AdMob and Unity Ads now auctions impressions in real time, lifting average revenue per daily active user by up to 25% as higher-yield networks compete for each view.[1]Unity Technologies, “AI-Powered Creative Optimization,” unity.com European publishers are layering rewarded ads beneath optional USD 4.99 subscriptions, creating three-tier models that capture spend across income bands without eroding free-to-play reach.

Cloud-Streaming Integration Lowering Hardware Barriers in Southeast Asia

Tencent Cloud Gaming surpassed 500 million registered users in 2024, and 60% of sessions originate from devices with less than 4 GB of RAM. In Indonesia, the Philippines, Vietnam, and Thailand, mobile game downloads totaled 1.93 billion and generated USD 625 million in Q1 2025, with cloud-streamed titles already accounting for 12-15% of playtime. Streaming trims the USD 2-5 per-gigabyte data expense tied to asset downloads in prepaid markets, but rural latency, still 45-60 milliseconds in parts of the Philippines, pushes studios to release downloadable lite editions to preserve retention.

Cross-Platform Engines Slashing Development Costs for Indie Studios

Unity’s September 2024 rollback to a seat-based subscription at USD 2,040 per Unity Pro seat removed variable per-install charges that rattled small studios. Epic Games complements this pivot through its USD 100 million Unreal Engine Mega Grants program, which supports casual and hyper-casual teams without taking equity. A three-person outfit can now bring a polished prototype to market for USD 8,000-12,000 annually, roughly half the pre-2024 total cost of ownership. Cross-platform export shrinks production cycles from 9-12 months to 4-6 months, a tempo advantage in genres where engagement peaks within 90 days.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent loot-box regulations in Germany and Belgium | -0.3% | Europe, monitoring in North America, and the Asia Pacific | Long term (≥ 4 years) |

| Latency issues in rural India are hindering cloud-casual adoption | -0.2% | South Asia, similar gaps in rural Africa and Latin America | Medium term (2-4 years) |

| Rising energy costs are increasing server opex for ad-supported web casual games | -0.3% | Global, most acute in Europe and parts of the Asia Pacific | Medium term (2-4 years) |

| ATT privacy changes are compressing attribution data for mid-tier publishers | -0.4% | Global, strongly felt in iOS-first markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

ATT Privacy Changes Compressing Attribution Data for Mid-Tier Publishers

Apple’s AdAttributionKit replaces device-level identifiers with aggregated cohorts, reducing post-install event visibility for advertisers by up to 60%. Casual titles with many purchasable SKUs lose the precision needed to bid aggressively for high-value users, prompting a 25-35% budget shift toward organic tactics such as influencer collaborations and in-app cross-promotion. Larger publishers mitigate the data gap by pooling events across multiple franchises, a scale benefit unavailable to single-game studios. The restraint weighs most heavily on puzzle and hyper-casual teams that rely on granular optimization to keep CPI below USD 1 in saturated Western markets.

Rising Energy Costs Increasing Server Opex for Ad-Supported Web Casual Games

Data-center electricity demand is forecast to double between 2025 and 2030, driven by AI workloads that power real-time ad auctions. Publishers of web-based casual titles report that server expenses per thousand impressions rose 12-18% since 2024 in Ireland, Amsterdam, and Singapore. Higher rack densities raise cooling requirements and expose smaller studios to quarter-over-quarter cost swings exceeding 20%. Some publishers relocate workloads to renewable-heavy regions such as Scandinavia or negotiate fixed-rate power contracts, but many indie teams lack the volume to secure favorable terms, pressuring margins on titles that already depend on high-frequency ad inventory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Monetization Model: Hybrid Adoption Leads Growth

Hybrid frameworks now sit at the vanguard of the online casual games market, expanding at a 5.89% CAGR through 2031. In-app purchases maintained a 38.19% share of 2025 revenue, sustained by franchises like Candy Crush Saga, yet their share is gradually ceding ground to approaches that combine micro-transactions, rewarded ads, and optional USD 4.99 monthly passes. Roblox’s USD 919 million Q3 2024 revenue illustrates how layered models can monetize both free users and high spenders.[2]Roblox Corporation, “Q3 2024 Earnings,” roblox.com Rewarded videos act as a safety valve, letting non-payers progress without hard locks and keeping retention high enough to convert a minority into payers. The online casual games market for subscription-driven word and puzzle titles is modest today, but is projected to expand as players seek ad-free convenience.

Hybrid design also buffers developers against privacy-related swings in user acquisition efficiency. When attribution visibility narrows, teams lean on engagement loops rather than precision targeting, a hedge that has gained salience since Apple’s privacy changes. Small starter packs priced at USD 0.99 amplify initial conversion by reducing sticker shock, while battle passes introduce predictable revenue arcs over four-week cycles. Paid-only apps are relegated to niche board-game adaptations because free alternatives and rapid content inflation discourage upfront fees.

By Platform: Smartphones Remain the Center of Gravity

Smartphones generated 72.11% of 2025 spending and are forecast to grow at 6.16% annually, ensuring mobile remains the backbone of the online casual games market. Sensor Tower logged 1.93 billion Southeast Asian downloads in Q1 2025, underscoring mobile’s gravitational pull. Tablets appeal to younger learners, especially under-18s, who use 10-inch screens for gamified lessons, yet replacement cycles stretch well beyond those of smartphones. Browser-based experiences are re-emerging because WebGL enables near-native performance without installing apps, and Europe’s Digital Markets Act removed distribution friction by forcing Apple and Google to tolerate alternative app stores.

Cross-platform engines further soften platform boundaries by letting studios export a single build to iOS, Android, and WebGL. Roblox’s October 2024 PlayStation launch raised quarterly engagement hours to 18.7 billion, proving that device-agnostic inventories deepen networks and extend play sessions. The online casual games market on PCs and browsers is smaller but growing steadily in idle genres, where players keep tabs open during work hours. Carrier billing and e-wallets, dominant in Indonesia and other emerging economies, cement the smartphone’s lead by simplifying micro-payments unavailable on desktop storefronts.

By Age Group: Under-18s Accelerate, Adults Still Monetize Most

The under-18 cohort is poised for a 5.58% CAGR, driven by parental acceptance of gaming as an educational tool and a screen-time management tool. Age-gated storefronts and family-sharing functions reduce purchase friction, making it easier for minors to secure permissioned access to USD 0.99 booster packs. Adults aged 18-35 retained 46.29% of 2025 revenue, leveraging higher disposable income and mobile immersion during commutes. As this group continues to dominate in engagement minutes, it shapes update cadences and live-ops calendars across the online casual games market.

Players aged 36-50 gravitate toward asynchronous puzzle loops, valuing pause-friendly mechanics that fit around work obligations. Those above 50 represent the smallest but highest-spending slice, averaging more than USD 20 per paying user each month in social casino formats, a segment that often surpasses youthful cohorts in monetization density. Upcoming European rules requiring real-money equivalents for virtual currencies may alter the offerings for minors, but developers are already piloting separate cosmetic-only stores to pre-empt compliance mandates. Overall, demographic diversification cushions revenue volatility and ensures steady gains for the online casual games industry.

Geography Analysis

Asia Pacific commanded 35.48% of spending in 2025, anchored by China’s partial regulatory thaw that cleared NetEase to launch Marvel Rivals and helped Tencent post CNY 51.8 billion (USD 7.3 billion) in Q3 2024 gaming revenue. Southeast Asia’s 1.93 billion Q1 2025 downloads and USD 625 million in receipts highlight the potential unlocked by inexpensive Android devices and carrier billing integrations. India’s rural teledensity is 58.8%, compared with 125.3% in urban areas, so metropolitan gamers stream high-fidelity titles, while villagers gravitate toward lightweight downloadable games that cache assets locally. Japan and South Korea remain revenue-dense but slower-growing, the latter setting a template for alternative payment models after passing its in-app billing choice legislation in 2024.

The Middle East is on course for a 5.92% CAGR, powered by Saudi Arabia’s USD 38 billion gaming investment program and its USD 4.9 billion Scopely acquisition. Vision 2030 targets USD 13.3 billion in gaming GDP contribution, supported by the Qiddiya Gaming District and Dubai’s 10-year Gaming Visa. With 420 million Arabic speakers worldwide, the addressable pool for localized titles is vast, and AI-driven asset generation now compresses translation costs enough for mid-tier studios to pursue the opportunity. Africa’s emerging markets lag due to smartphone affordability and fragmented payment rails, but mobile money services such as M-Pesa are widening the funnel in East Africa.

North America and Europe collectively delivered roughly 45% of 2025 revenue. The United States still leads on absolute spend, though growth tapers as CPI inflation meets Apple’s privacy policy constraints. Canada and Mexico expand faster, with Mexico’s 50 million gamers serving as a gateway into Spanish-speaking South America. Europe’s Digital Markets Act is already shifting spend to web shops that bypass 30% platform fees, boosting average revenue per paying user by as much as 18% without raising prices.[3]European Commission, “Digital Markets Act Gatekeeper Designations,” ec.europa.eu Germany and Belgium’s loot-box prohibitions accelerate cosmetic-only monetization, forcing studios to maintain region-specific builds but also smoothing retention by removing perceived pay-to-win features.

Competitive Landscape

Roughly 40% of global revenue resides with the top 10 publishers, confirming moderate concentration that still leaves room for breakout hits. Tencent’s Honor of Kings now clears 100 million daily actives, yet the publisher wrestles with mounting acquisition costs and Chinese regulatory oversight. NetEase leverages Marvel Rivals to court Western audiences while offsetting domestic license bottlenecks. Microsoft integrated King into the Xbox Game Pass framework after finalizing its USD 68.7 billion Activision Blizzard deal, but Candy Crush revenue, while sturdy at USD 727 million in Q3 2024, grows only in single digits.

Voodoo, having surpassed 7 billion lifetime downloads, pivots toward hybrid-casual models that extend 30-day retention by layering meta-progression loops on traditionally throwaway mechanics. White-space opportunities cluster around older demographics, underserved languages, and fragmented payment terrains. The over-50 cohort’s willingness to pay USD 20 per month for social casino titles remains largely unmet by mainstream publishers. The 420 million-strong Arabic audience still has limited catalogue depth, and Latin America’s mélange of carrier billing, e-wallets, and cash vouchers rewards studios that localize checkout flows for Mercado Pago or OXXO.

AI-powered creative pipelines compress cost-per-install by up to 35%, allowing nimble indie teams to iterate 50-100 ad variants a week and outmaneuver slower, committee-bound corporations. Roblox’s user-generated economy, which paid developers USD 1.2 billion over the year to Q3 2024, redefines competition by turning players into creators and lowering the platform owner's content acquisition risk.

Online Casual Games Industry Leaders

Zynga Inc.

Microsoft Corporation

Konami Digital Entertainment

Apple Inc.

Ubisoft Entertainment SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Roblox unveiled its 4D Generative AI at RDC, allowing creators to generate fully functional, scripted, interactive objects and to translate real-time voice into natural language.

- September 2025: Savvy Games Group’s subsidiary Scopely acquired Niantic’s game business for USD 3.5 billion, integrating AR and geolocation expertise to expand its global mobile presence.

- June 2025: Epic Games launched mobile "Webshops" and a 0% store fee for the first USD 1 million in annual revenue to help developers bypass mobile platform commissions.

- February 2025: Qualcomm enabled Snapdragon “Game Super Resolution” for WebGL, cutting average frame times 18% in browser sessions.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the online casual games market as all gross revenue earned from browser-based or downloadable games that feature simple mechanics, short session loops, and wide age appeal, played on smartphones, tablets, PCs, or lightweight web portals. Revenue streams counted include in-app purchases, reward or display advertising, and one-time paid downloads; regional taxes and platform fees are netted out to keep figures comparable.

Scope Exclusion: Esports tournaments, premium console titles, hardcore PC client games, and gaming hardware are intentionally left outside the sizing.

Segmentation Overview

- By Monetization Model

- Advertising

- In-App Purchase

- Paid App

- By Platform

- Smartphone

- Tablet

- PC / Web

- By Age Group

- Below 18 Years

- 18-35 Years

- 36-50 Years

- Above 50 Years

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed casual-game developers, ad-tech network managers, user-acquisition specialists, and regionally diverse players to verify average revenue per daily active user, seasonality impact, and regulation risk. These conversations filled data gaps and helped refine assumptions before totals were frozen.

Desk Research

Analysts collected baseline inputs from high-integrity public domains such as ITU mobile-subscriber data, GSMA Intelligence 5G coverage maps, national telecom regulators, and app-economy trade groups. Storefront leader boards from Google Play and the Apple App Store, Sensor Tower public dashboards, and press releases supplied indicative install counts and monetization patterns. Paid databases, including D&B Hoovers for publisher financials and Questel for patent filings, clarified revenue splits, launch pipelines, and platform fee structures. This list is illustrative; many other open and subscription sources supported the desk work.

Second-round validation tapped company filings, investor presentations, and technology journalism to catch product pivots, privacy-policy changes, and ad-pricing swings, ensuring no early signal was missed.

Market-Sizing & Forecasting

The top-down build starts with each country's active-smartphone base, multiplies it by casual-gamer penetration and monetized ARPU to generate a gross demand pool, which is then reconciled with sampled publisher revenue and ad-impression volumes for a directional bottom-up check. Key variables include smartphone installed base, daily playtime minutes, ad fill rates, IAP conversion, regional GDP per capita, and platform commission. Five-year forecasts employ multivariate regression that links ARPU and penetration to those drivers, followed by scenario stress tests our experts discussed during interviews.

Data Validation & Update Cycle

Every model passes peer review, variance thresholds are flagged, and outliers trigger a re-contact with sources. Reports refresh yearly, with interim patches when platform policy, taxation, or privacy shifts materially alter revenue pathways.

Why Mordor's Online Casual Games Baseline Earns Trust

Published estimates often differ because firms select unique scope boundaries, revenue filters, and refresh cadences. Understanding these levers helps buyers judge credibility.

Key gap drivers include whether advertising revenue is included, if hyper-casual downloads are blended with casual, and the currency year used for conversion. Some studies rely on questionnaire extrapolations or narrow geography, while Mordor's model ties directly to observable device counts and cross-checked publisher take-rates.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 20.57 B (2025) | Mordor Intelligence | - |

| USD 24.80 B (2024) | Global Consultancy A | Includes mobile ads plus casual casino, limited publisher validation |

| USD 19.48 B (2023) | Regional Consultancy B | Rolls forward historic growth, excludes browser play |

| USD 3.22 B (2024) | Trade Journal C | Covers only IAP for puzzle and card genres |

These comparisons show that by aligning scope to genuine monetization streams and by testing inputs against both public statistics and direct stakeholder insight, our baseline offers decision-makers a balanced, transparent reference point.

Key Questions Answered in the Report

How large is the online casual games market today, and what CAGR is expected?

The online casual games market stands at USD 22.68 billion in 2026 and is projected to grow at a 5.41% CAGR, reaching USD 29.51 billion by 2031.

Which platform contributes most to spending on online casual titles?

Smartphones generate 72.11% of 2025 revenue and are projected to expand at a 6.16% CAGR, keeping mobile firmly in the lead.

What monetization mix is gaining the most traction with players?

Hybrid frameworks that blend in-app purchases, rewarded ads, and optional subscriptions are advancing at a 5.89% CAGR, outpacing single-stream models.

Which region is forecast to grow fastest in casual gaming through 2031?

The Middle East is expected to post a 5.92% CAGR, fueled by Saudi Arabia’s USD 38 billion commitment to gaming infrastructure and studio investment.

How are privacy changes on iOS affecting user-acquisition strategy?

Apple’s aggregated attribution reduces post-install visibility by up to 60%, prompting mid-tier publishers to reallocate 25-35% of their budgets to organic growth channels.

What demographic shows the highest spend per user in casual games?

Players over 50 years old, especially in social casino formats, spend an average of more than USD 20 per paying user per month, the highest among age groups.

Page last updated on: