Newborn Screening Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.52 Billion |

| Market Size (2031) | USD 2.32 Billion |

| Growth Rate (2026 - 2031) | 8.78% CAGR |

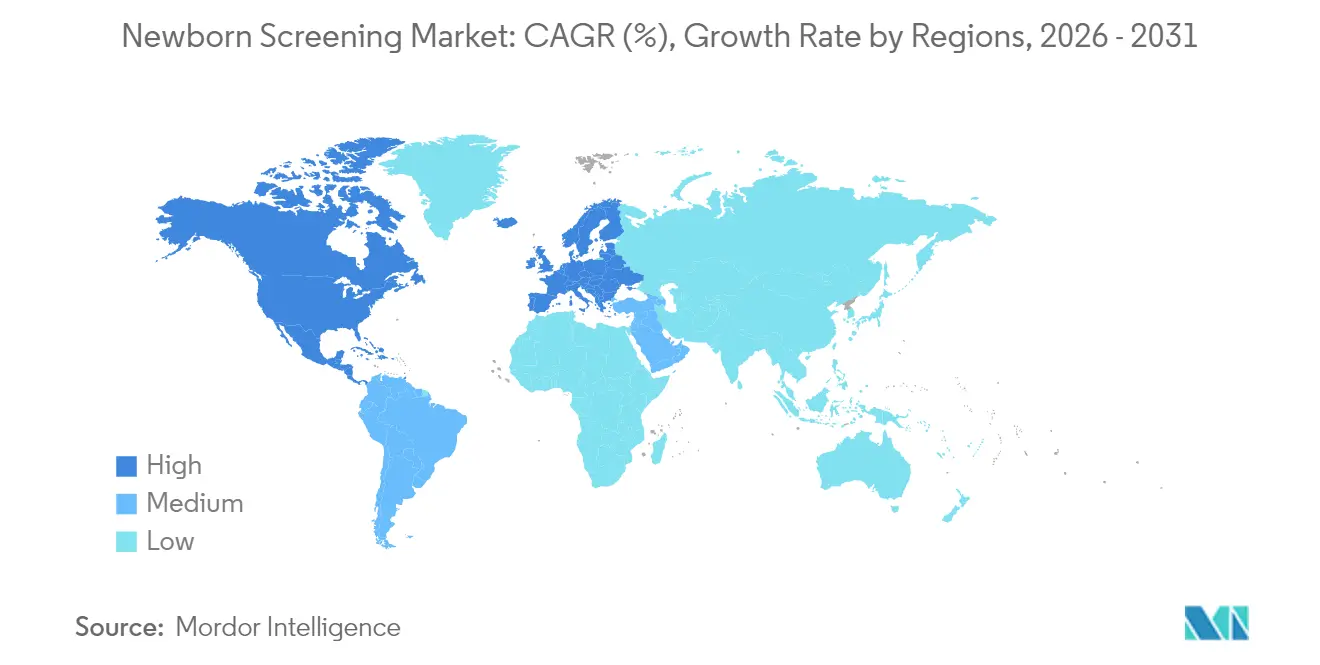

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

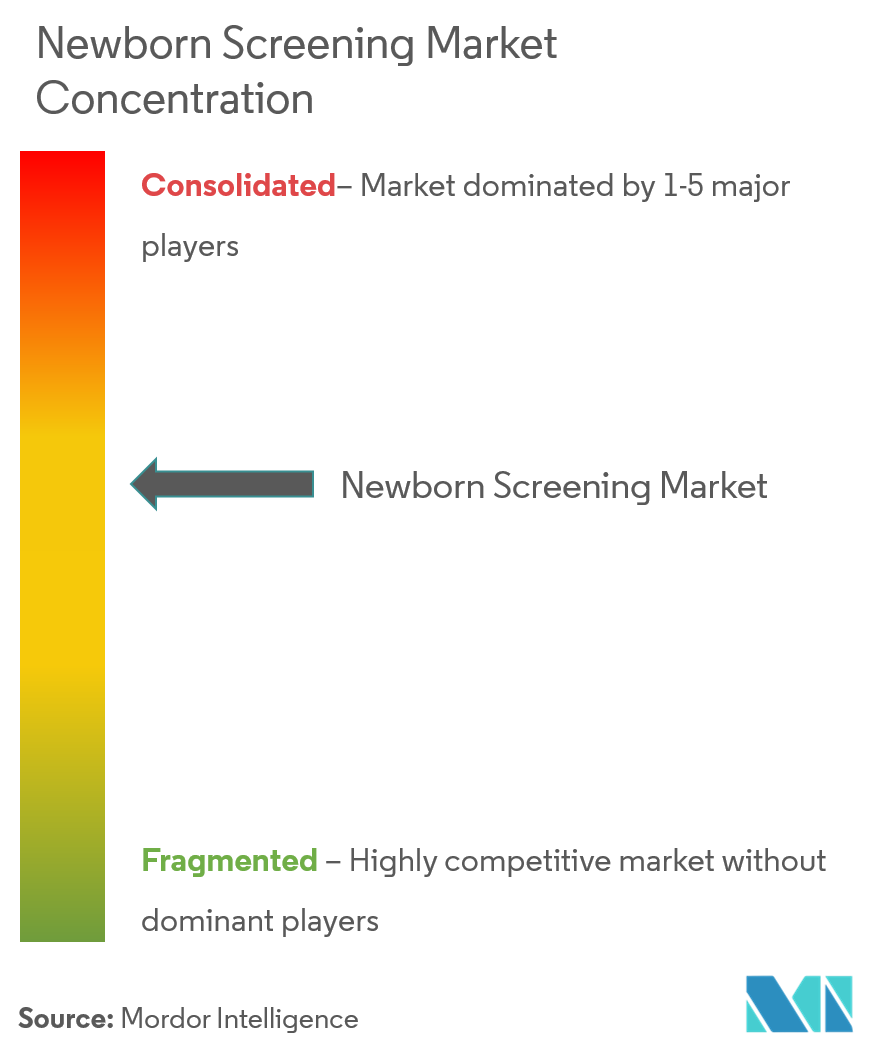

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Newborn Screening Market Analysis by Mordor Intelligence

The newborn screening market size in 2026 is estimated at USD 1.52 billion, growing from 2025 value of USD 1.40 billion with 2031 projections showing USD 2.32 billion, growing at 8.78% CAGR over 2026-2031. Momentum comes from the rapid shift toward genomic platforms that identify hundreds of genetic conditions quicker than conventional assays, alongside artificial-intelligence tools that cut false-positive rates dramatically. Strong government backing, wider reimbursement, and clearer regulatory pathways spur faster technology adoption, while North America retains leadership and Asia-Pacific posts the steepest growth. Robust investment flows, growing pilot programs, and public-health mandates continue to deepen market penetration of tandem mass spectrometry and whole-genome sequencing. Ongoing shortages of biochemical-genetics specialists and data-privacy concerns temper growth but have yet to derail expansion.

Key Report Takeaways

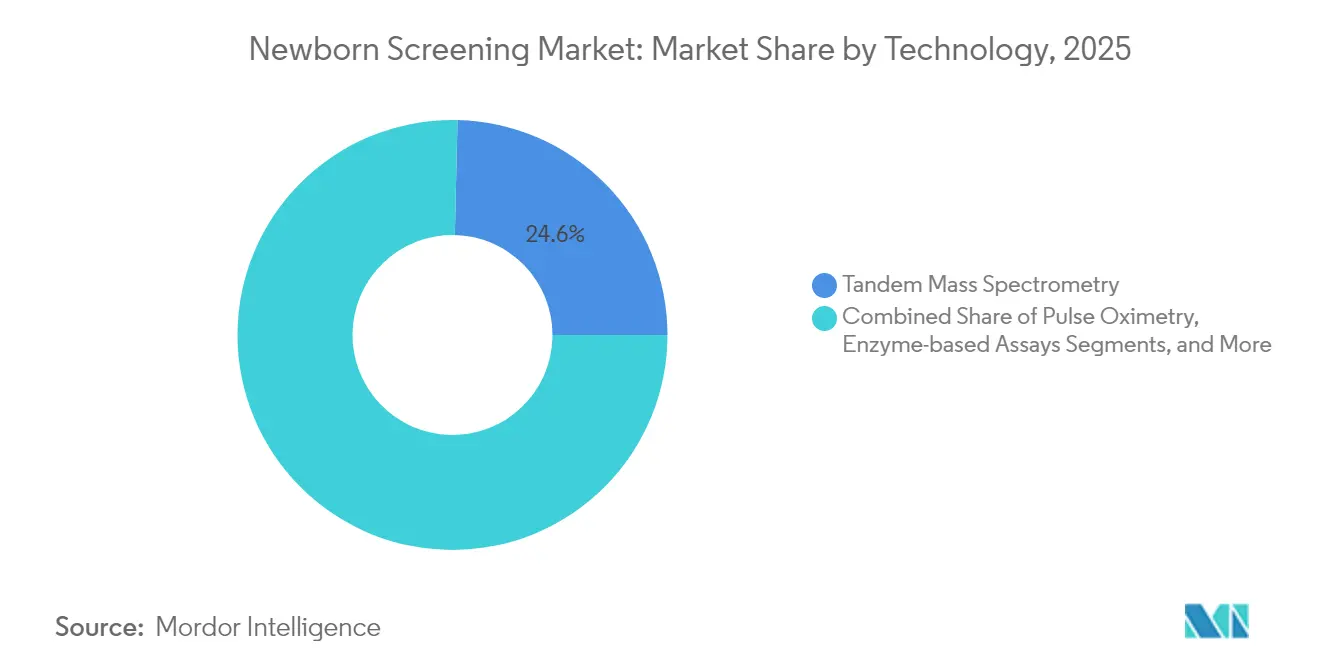

- By technology, tandem mass spectrometry commanded 24.63% of the newborn screening market share in 2025; enzyme-based assays are projected to expand at a 9.21% CAGR through 2031.

- By test type, dried blood spot testing held 45.18% of the newborn screening market size in 2025, while hearing screening is advancing at a 9.61% CAGR to 2031.

- By end user, hospitals accounted for 60.62% revenue share in 2025; diagnostic and reference laboratories exhibit the highest projected CAGR at 9.78% to 2031.

- By geography, North America retained a 42.11% revenue share in 2025, whereas Asia-Pacific leads growth at a 10.09% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Newborn Screening Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of congenital & inherited metabolic disorders | +1.8% | Asia-Pacific; Middle East | Long term (≥ 4 years) |

| Government mandates & funding expansions for national panels | +2.1% | North America; Europe | Medium term (2-4 years) |

| Rapid adoption of tandem-mass-spectrometry platforms | +1.5% | Global | Medium term (2-4 years) |

| AI algorithms reducing false positives | +1.2% | North America; Europe | Short term (≤ 2 years) |

| Roll-out of ultra-rapid whole-genome sequencing in NICUs | +0.9% | North America; pilot Asia-Pacific | Long term (≥ 4 years) |

| Emergence of at-home supplemental DNA newborn kits | +0.5% | North America; developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising burden of congenital & inherited metabolic disorders

Incidence rates for inherited metabolic diseases are climbing, with Iranian data indicating prevalence as high as 1:1,000 births, far above historical averages. High consanguinity in parts of the Middle East magnifies risk, prompting Saudi Arabia to expand its panel to 18 disorders and prepare to add hemoglobinopathies. Demographic shifts toward older maternal age and improved survival of affected infants sustain demand for broader panels. Early-genome initiatives such as BeginNGS have demonstrated a 97% reduction in false positives while preserving >99% sensitivity, lowering lifetime treatment costs by enabling presymptomatic therapy. Health-system economics favor preventive screening as untreated cases drive high downstream expenditures.

Government mandates & funding expansions for national panels

The World Health Organization issued April 2024 guidance promoting universal hearing and hyperbilirubinemia screening, accelerating legislative action across multiple regions [1]World Health Organization, “New guidelines on universal newborn screening,” who.int. In the United States, spinal muscular atrophy reached implementation in 48 programs by late-2024, while the Food and Drug Administration formed the Genetic Metabolic Diseases Advisory Committee to streamline review of new assays. Belgium’s BabyDetect pilot covered 165 disorders with 90% parental uptake, revealing 71 actionable cases, 30 of which conventional panels would miss [2]Nature Medicine, “BabyDetect Pilot Study Identifies Treatable Pediatric Disorders,” nature.com. Funding pools attached to such mandates create predictable procurement cycles that reward suppliers with proven throughput.

Rapid adoption of tandem-mass-spectrometry platforms

Cost-effectiveness evidence from China shows tandem MS/MS outperforms fluorescence assays in diagnostic yield, justifying initial capital outlay. Updated U.S. regulations under 21 CFR 862.1055 clarify pre-market requirements, enabling quicker system upgrades. Laboratories increasingly deploy universal second-tier LC-MS/MS methods that test multiple biomarkers simultaneously, streamlining workflows and curbing false positives. Mature service networks and reagent supply chains further solidify MS/MS as the backbone of many national programs.

AI algorithms reducing false positives

Machine-learning models cut false positives for isovaleric aciduria by 69.9% across a 2 million-newborn German dataset while safeguarding 100% sensitivity. Similar Chinese studies achieved 93.4% sensitivity and 78.6% specificity for multiple metabolic diseases, surpassing manual analytics. AI tools also enhance pulse-oximetry screening for critical congenital heart defects, boosting detection in resource-limited hospitals. Integration into laboratory information systems simplifies interpretation and triage, lessening staffing bottlenecks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of global uniformity in policies & test panels | -1.4% | Global | Long term (≥ 4 years) |

| Persisting false-positive/false-negative follow-ups | -1.8% | Global | Medium term (2-4 years) |

| Acute shortage of biochemical-genetics specialists | -2.2% | Developing nations | Long term (≥ 4 years) |

| Data-privacy & consent concerns around genomic data | -1.1% | North America; Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lack of global uniformity in NBS policies & test panels

Panels vary from fewer than 10 to more than 50 conditions worldwide, complicating cross-border technology deployment and training. The United Kingdom’s updated population-screening pathway highlights ever-shifting protocols that vendors must track. Divergent consent standards for genomic tests slow multinational roll-outs, while inconsistent data formats limit algorithm performance. Suppliers consequently absorb higher customization costs, delaying time-to-market.

Acute shortage of biochemical-genetics specialists

Sixty-two percent of genetics professionals report appointment waits beyond one month, exposing gaps between screening volumes and downstream care capacity. Training pipelines remain thin; the Association of American Medical Colleges notes inadequate fellowship slots for medical biochemical genetics. Rural and low-income regions feel shortages most acutely, constraining follow-up and genetic counseling and thereby capping panel expansion despite technological readiness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Expanding automation in tandem MS/MS

Tandem MS/MS accounted for 24.63% of newborn screening market share in 2025 as the method of choice for high-throughput metabolic testing. Integrated software such as iDIA-QC now automates quality control across dozens of labs, cutting manual oversight and error rates. The newborn screening market size for enzyme-based assays is projected to rise at 9.21% CAGR as regional laboratories search for low-maintenance alternatives. Pulse-oximetry equipment continues stable uptake following universal critical-congenital-heart-defect mandates, with screening costs ranging USD 5–14 per newborn.

Whole-genome sequencing is reshaping long-term growth. Ultra-rapid protocols deliver diagnoses within three hours, positioning genomics to displace multiple standalone assays within one workflow. BeginNGS validations across 255 conditions showcase scalability with near-perfect sensitivity. As instrument prices fall, hybrid models combining MS/MS for metabolites and sequencing for complex genetics are gaining favor among public laboratories.

By Test Type: Dried blood spot holds firm as innovation rises

Dried blood spot (DBS) methods captured 45.18% of the newborn screening market size in 2025 thanks to entrenched logistics and low consumable costs. Two-layer microfiltration cards now mitigate hematocrit interference and enable multiplex protein assays, broadening utility beyond classic metabolic panels. Meanwhile, hearing screening is climbing at a 9.61% CAGR, spurred by WHO recommendations and improved pulse-oximeter precision.

Critical-heart-defect protocols illustrate DBS limitations: dual-index programs in Shanghai that combined pulse-oximetry with auscultation achieved 100% sensitivity among nearly 200,000 infants, showing value beyond blood-based analytics. Genomic assays threaten to upend test-type silos by detecting hundreds of disorders from one sample. Nevertheless, DBS workflows remain indispensable where sequencing budgets and data-privacy frameworks lag.

By End User: Specialized labs accelerate amid hospital dominance

Hospitals retained 60.62% revenue share in 2025 as births and initial tests take place on site. Integration of AI-driven decision support now allows bedside teams to interpret complex reports rapidly, as demonstrated by Rady Children’s Institute NICU genome program. However, diagnostic and reference laboratories are projected to grow 9.78% annually through 2031. GeneDx’s rapid genome-sequencing volume surged 80% year over year after Medicaid expansion across 11 states, highlighting payor willingness to outsource complex analyses.

Public-health labs continue providing confirmatory testing and quality assurance, supported by the CDC’s Newborn Screening Quality Assurance Program that distributes proficiency materials globally. Research institutes add volume via clinical-trial enrollment for novel therapies, but their share remains modest compared with hospitals and commercial labs.

Geography Analysis

North America commanded 42.11% of 2025 revenue, buoyed by comprehensive Recommended Uniform Screening Panel adoption across 53 programs and favorable reimbursement. The newborn screening market benefits from FDA guidance on laboratory-developed tests and the Genetic Metabolic Diseases Advisory Committee, which accelerate assay clearance. GeneDx’s GUARDIAN study of 17,000 infants revealed conditions missed by traditional panels in 3.7% of cases, underscoring latent demand for genomic expansion.

Asia-Pacific exhibits a 10.09% CAGR, fueled by China’s large NBGS pilots that outperformed enzyme assays for lysosomal storage disorders. Taiwan’s five-year spinal muscular atrophy program confirmed 23 presymptomatic cases among 446,966 newborns, illustrating tangible clinical benefits. India’s cystic-fibrosis screening initiatives and Thailand’s 98.6% coverage in rural settings point to mounting public investment.

Europe sustains stable expansion through coordinated projects such as Belgium’s BabyDetect, which screens 165 disorders at EUR 365 per infant with 90% acceptance. The United Kingdom modernized operational agreements to tighten specimen processing times and awarded Revvity a USD 37.8 million contract for rare-disease screening. In emerging regions, sub-Saharan Africa confronts 400,000 annual sickle-cell births, highlighting urgent need for cost-adapted technologies .

Competitive Landscape

Market structure remains moderately fragmented. Revvity leverages its long MS/MS legacy to secure large tenders, exemplified by the 2025 UK contract, and is partnering with Element Biosciences to integrate sequencing into turnkey workflows. GeneDx broadened its footprint by acquiring Fabric Genomics, adding AI interpretation that underpins high-growth rapid sequencing services. LaCAR MDx advanced geographic expansion by purchasing Baebies’ U.S. newborn screening division and developing one-hour fluorescent G6PD tests, addressing gaps in Asia and Africa.

Technology differentiation increasingly centers on AI. Vendors offering machine-learning triage see stronger procurement interest because algorithms slash false positives while preserving sensitivity. Regulatory clarity under updated Laboratory Developed Test rules encourages investment by lowering approval risk. White-space opportunities include point-of-care devices for low-resource settings and mobile data platforms that feed centralized analytics without major infrastructure spend.

Newborn Screening Industry Leaders

Natus Medical Incorporated

Trivitron Healthcare

Medtronic Inc.

Bio-Rad Laboratories Inc.

PerkinElmer

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2023: Trivitron Healthcare began the EkSahiShuruat campaign to raise newborn screening awareness across India.

- January 2023: Masimo launched an advanced baby-monitoring system enabling caregivers to track infant vitals in real time.

- August 2022: Trivitron Healthcare opened a Centre of Excellence at AMTZ Campus, Vishakhapatnam, for metabolomics, genomics, and newborn diagnostics.

- June 2022: Rady Children’s Institute for Genomic Medicine launched the BeginNGS program to screen for 400 treatable genetic diseases using rapid whole-genome sequencing.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the newborn screening testing market as the aggregated annual revenue generated from laboratory assays and allied instrumentation used to screen infants in the first twenty-eight days of life for metabolic, endocrine, hematologic, audiologic, and critical congenital heart conditions. The valuation pools test fees for dried-blood-spot biochemical panels, hearing screens, pulse oximetry, and confirmatory DNA assays that are bundled into public or private newborn programs worldwide, together with associated analyzer and reagent revenues collected at hospital and reference-lab points of care.

Scope exclusion: prenatal carrier tests and post-neonatal genetic diagnostics lie outside this market.

Segmentation Overview

- By Technology

- Tandem Mass Spectrometry

- Pulse Oximetry

- Enzyme-based Assays

- DNA / Genome Sequencing Assays

- Other Technologies

- By Test Type

- Dried Blood Spot (DBS)

- Hearing Screening

- Critical Congenital Heart Defect (CCHD)

- Other Test Types

- By End User

- Hospitals

- Diagnostic & Reference Laboratories

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews with state-run program directors, metabolic-lab supervisors, neonatologists, and instrument distributors across North America, Europe, Asia-Pacific, and Latin America helped us validate coverage ratios, average test prices, panel-expansion timelines, and reagent-use assumptions. The dialogues also probed failure-recall costs and reimbursement lags, enabling us to fine-tune cost inputs and scenario weights.

Desk Research

Mordor analysts began with live-birth statistics and screening policy trackers published by authorities such as the World Health Organization, CDC NewSTEPs, Eurocat, Statistics Canada, and Eurostat, which provided the foundational epidemiological pool. Complementary insights were gathered from peer-reviewed journals like Pediatrics and Molecular Genetics & Metabolism, trade association position papers from ISNS, and open tender databases charting analyzer procurement. Our team extracted company financials through D&B Hoovers and scanned patent-family activity via Questel to benchmark technology adoption curves. These sources are illustrative only, and many additional references informed data gathering, checks, and clarifications.

Market-Sizing & Forecasting

A top-down model first multiplies live-birth cohorts by country-specific screening penetration and weighted average price per test bundle. It then reconciles totals with selective bottom-up checks built from instrument shipments, reagent pull-through volumes, and sampled analyzer ASPs. Key variables include annual live-birth growth, mandated panel size per jurisdiction, reagent cost inflation, reimbursement turnaround, and instrument replacement cycles, each projected through 2030. Forecasts employ multivariate regression plus scenario analysis to reflect birth-rate uncertainty and staged genomic-panel rollouts, while data gaps are bridged by imputation aligned to peer geographies with similar policy profiles.

Data Validation & Update Cycle

Model outputs pass three rounds of variance screening, peer review, and senior-analyst sign-off. We compare our figures with sentinel hospital procurement data and national budget disclosures, and we re-contact industry experts if anomalies exceed preset bands. The study refreshes annually, with interim updates whenever material policy or volume shocks occur. A final consistency sweep is run immediately before delivery to clients.

Why Mordor's Newborn Screening Market Numbers Inspire Confidence

Published estimates often diverge because firms adopt different panel definitions, price blends, and refresh cadences. We acknowledge those gaps upfront, then show how disciplined scope setting and annually renewed variables anchor our baseline.

Key gap drivers include competitors counting only instrument revenue, using older birth-cohort baselines, or excluding DNA assays that several regions already reimburse. Our study, in contrast, captures the full bundled service, adjusts for multi-test discounts, and updates currency conversions at purchasing-power parity.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.40 B (2025) | Mordor Intelligence | - |

| USD 0.84 B (2023) | Regional Consultancy A | Instruments only; narrow technology scope |

| USD 1.16 B (2024) | Global Consultancy B | Omits emerging APAC programs; panel size frozen |

| USD 0.90 B (2021) | Trade Journal C | Older base year; limited currency adjustment |

These comparisons show that when scope breadth, current inputs, and transparent update cycles are applied together, Mordor Intelligence delivers a balanced, reproducible baseline that decision-makers can trust.

Key Questions Answered in the Report

How big is the Newborn Screening Market?

The Newborn Screening Market size is expected to reach USD 1.52 billion in 2026 and grow at a CAGR of 8.78% to reach USD 2.32 billion by 2031.

What is the current Newborn Screening Market size?

The newborn screening market is worth USD 1.52 billion in 2026 and is on track to reach USD 2.32 billion by 2031.

Who are the key players in Newborn Screening Market?

Natus Medical Incorporated, Trivitron Healthcare, Medtronic Inc., Bio-Rad Laboratories Inc. and Revvity are the major companies operating in the Newborn Screening Market.

Which is the fastest growing region in Newborn Screening Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Newborn Screening Market?

North America holds 42.11% market share thanks to universal adoption of the Recommended Uniform Screening Panel and supportive reimbursement.

Page last updated on: