Lung Cancer Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

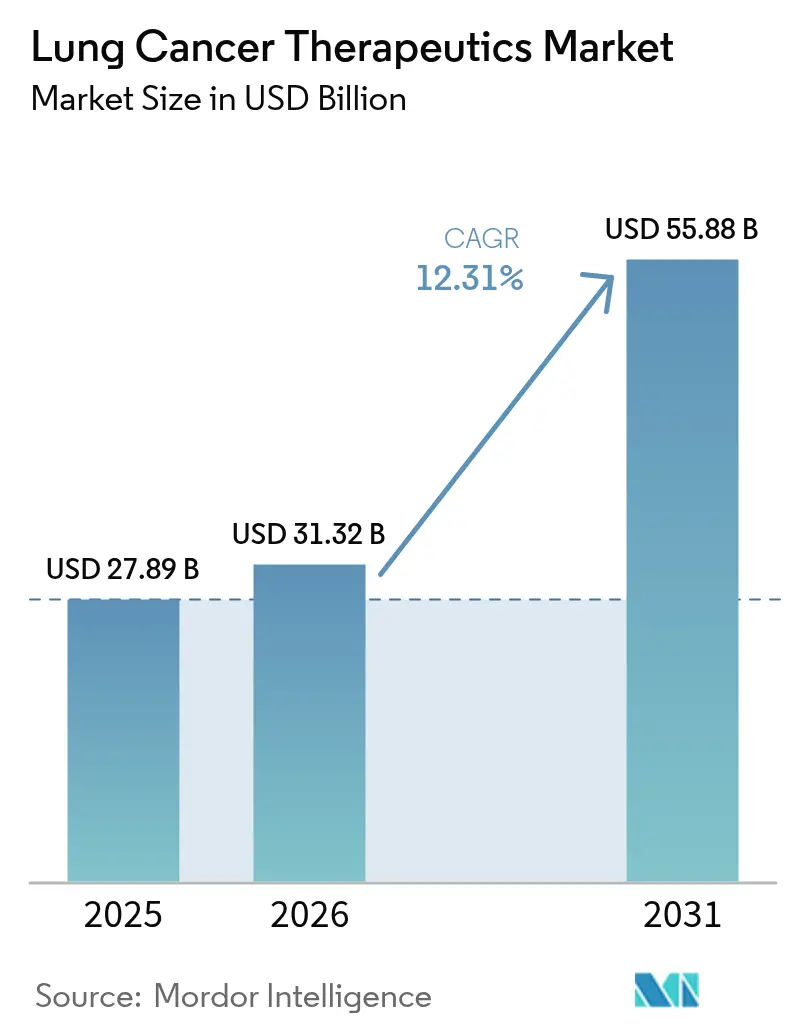

| Market Size (2026) | USD 31.32 Billion |

| Market Size (2031) | USD 55.88 Billion |

| Growth Rate (2026 - 2031) | 12.31% CAGR |

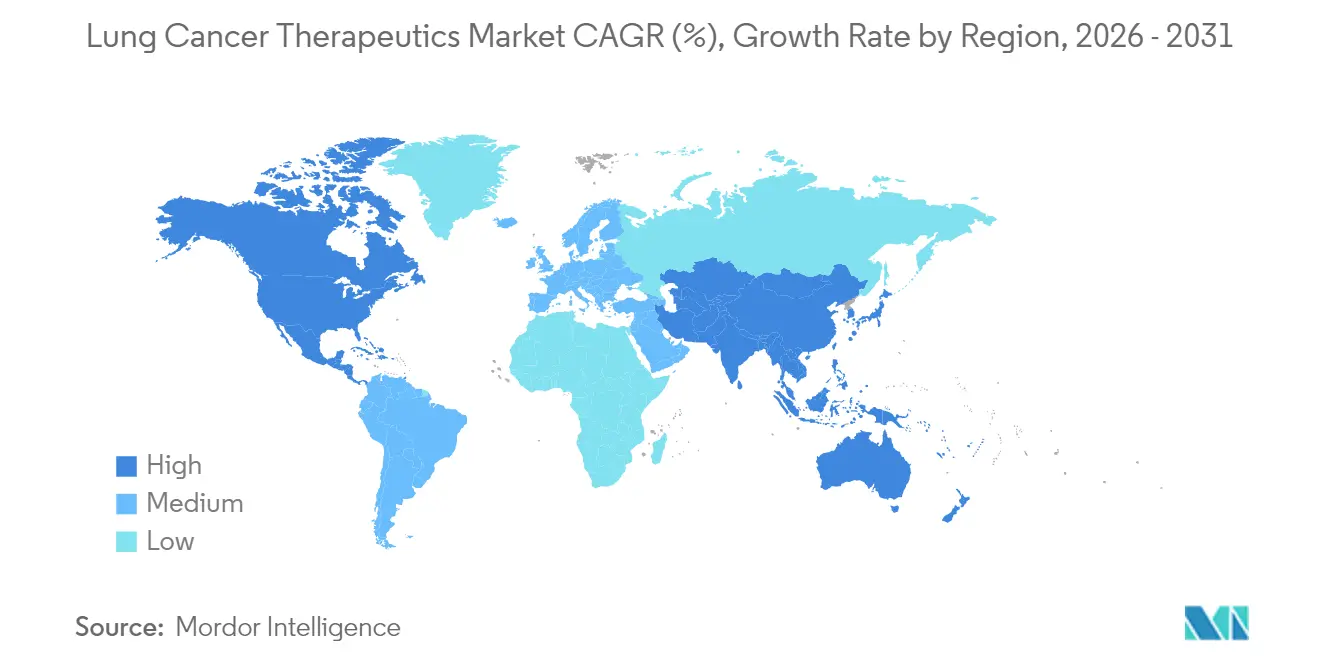

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

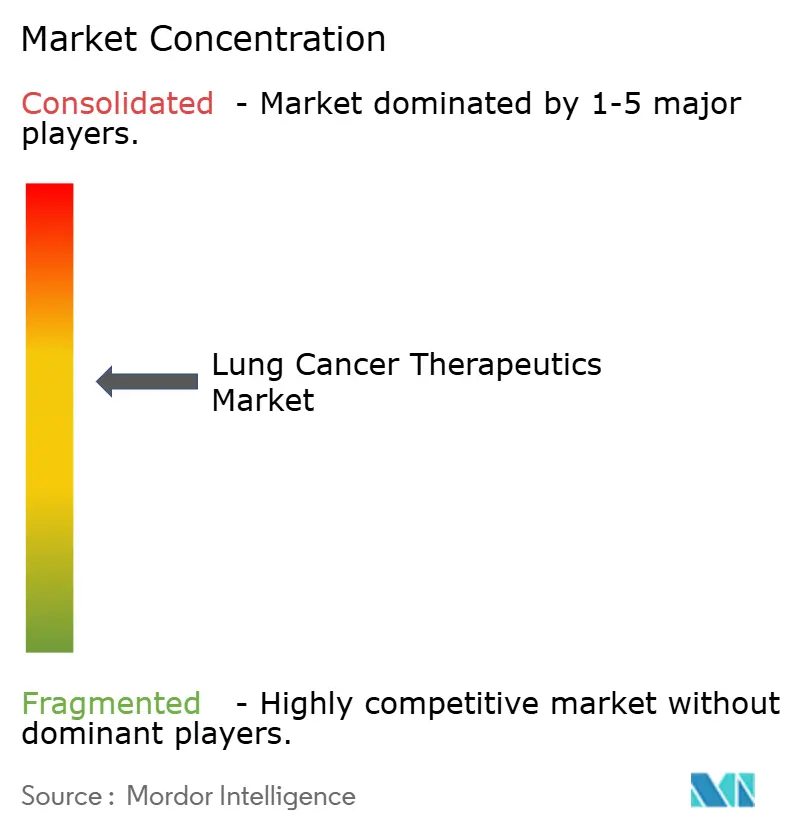

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Lung Cancer Therapeutics Market Analysis by Mordor Intelligence

The lung cancer therapeutics market size is expected to grow from USD 27.89 billion in 2025 to USD 31.32 billion in 2026 and is forecast to reach USD 55.88 billion by 2031 at 12.31% CAGR over 2026-2031. Rapid gains stem from immuno-oncology breakthroughs, bispecific antibodies, and wider global reimbursement adoption that collectively lift treatment volumes. Regulatory agencies expedited 11 new non-small cell approvals after 2024, underscoring an innovation cycle that compresses development timelines and intensifies competition. Precision biomarker testing has moved from specialist to mainstream practice, enabling mutation-matched drug selection and pushing response rates higher for previously hard-to-treat patients. Wider insurance coverage across Asia-Pacific and Latin America improves affordability, while price pressure in mature markets continues to nudge manufacturers toward value-based agreements. Strategic consolidation around combination platforms is accelerating as companies seek to defend positions before major patent cliffs arrive.

Key Report Takeaways

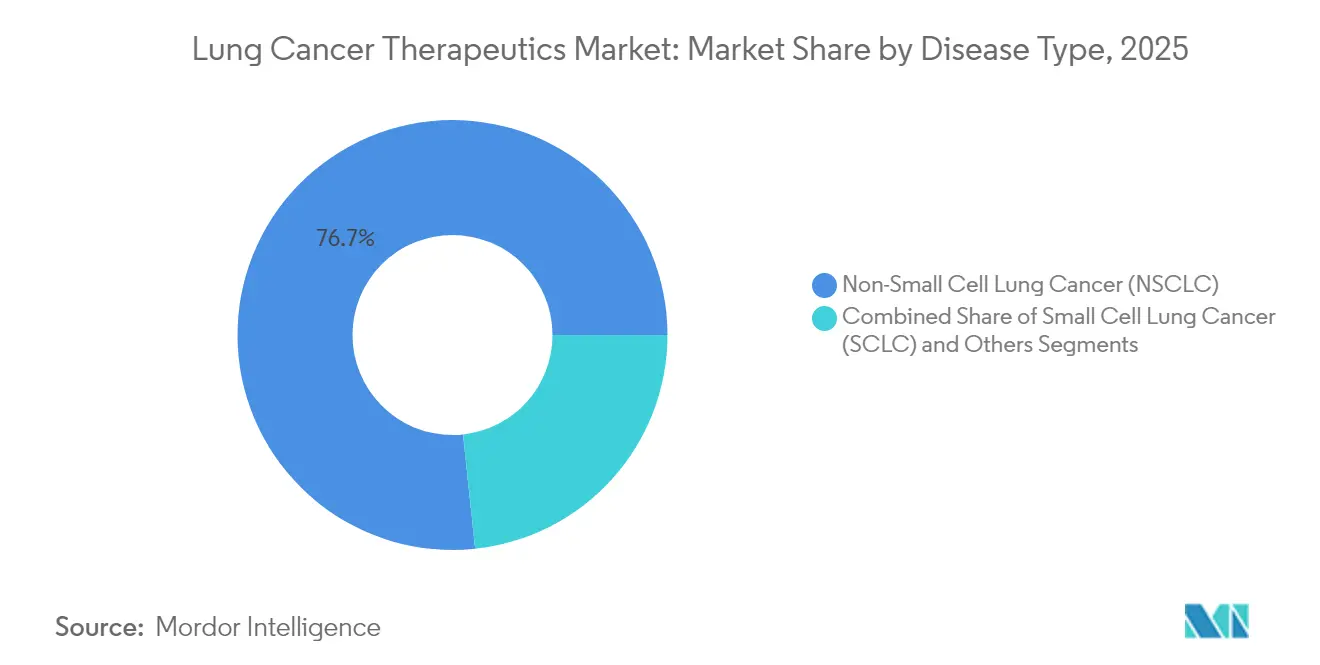

- By disease type, non-small cell lung cancer led with 76.68% revenue share in 2025; small-cell lung cancer is advancing at a 13.05% CAGR through 2031.

- By treatment modality, chemotherapy held 42.74% share of the lung cancer therapeutics market in 2025, while immunotherapy is projected to expand at 13.02% CAGR to 2031.

- By drug class, small-molecule agents accounted for 63.95% share in 2025, whereas biologics and biosimilars are rising at a 13.12% CAGR over the same horizon.

- By distribution channel, hospital pharmacies captured 69.21% share in 2025; retail pharmacies show the fastest trajectory at 13.01% CAGR through 2031.

- By line of therapy, first-line regimens commanded 54.88% share in 2025; third-line and later therapies record the highest projected CAGR at 13.18% to 2031.

- By geography, North America contributed 38.62% of 2025 revenue, yet Asia-Pacific is on track for a 13.34% CAGR to the end of the decade.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Lung Cancer Therapeutics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing prevalence of lung cancer | +3.1% | Global, strongest in Asia-Pacific and emerging economies | Long term (≥ 4 years) |

| Rising pollution and smoking rates | +1.9% | Asia-Pacific core, spill-over to Middle East and urban centers worldwide | Medium term (2-4 years) |

| Rapid adoption of immuno-oncology therapies | +3.8% | North America and Europe lead, swift Asia-Pacific uptake | Short term (≤ 2 years) |

| Expanding healthcare reimbursement coverage | +2.5% | Global, highest acceleration in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Precision-medicine biomarker testing uptake | +2.3% | North America and Europe mature, emerging Asia-Pacific markets | Short term (≤ 2 years) |

| Emerging cell and RNA-based therapy pipeline | +2.8% | North America and Europe early adoption, selective Asia-Pacific entry | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Immuno-Oncology & Targeted Therapies

Checkpoint inhibitors combined with novel targets lift survival beyond legacy chemotherapy. Bispecific T-cell engagers such as tarlatamab post 40% objective responses in heavily pre-treated small-cell cases, while antibody-drug conjugates like datopotamab deruxtecan reach 45% responses in EGFR-mutated non-small-cell disease [1]U.S. Food and Drug Administration, "FDA grants accelerated approval to datopotamab deruxtecan-dlnk for EGFR-mutated non-small cell lung cancer," fda.gov. Thirteen lung cancer indications cleared the FDA’s accelerated pathway during 2024 alone, compressing launch cycles and intensifying rivalry [2]U.S. Food and Drug Administration, "Oncology Regulatory Review 2023," fda.gov. Combination regimens dominate pipelines as developers marry immune activation with mutation-specific blockade to blunt escape mechanisms. Biomarker-driven selection now guides most first-line decisions, enabling higher response depths and longer progression-free intervals. As new modalities gain first-line status, chemotherapy shifts toward a backbone role within multi-agent protocols rather than standalone therapy.

Precision-Medicine Biomarker Testing Uptake

Comprehensive molecular profiling is replacing histology-based selection. Next-generation sequencing panels, supported by FDA-cleared diagnostics such as the Oncomine Dx Express Test, are becoming standard for community oncologists [3]U.S. Food and Drug Administration," FDA grants accelerated approval to sunvozertinib for metastatic non-small cell lung cancer with EGFR exon 20 insertion mutations," fda.gov. Actionable alterations cover EGFR, ALK, ROS1, KRAS, HER2, MET, and BRAF, now informing choices for more than 60% of non-small-cell cases. Liquid biopsy expands real-time resistance monitoring, allowing therapy switches before clinical progression. Declining sequencing costs, along with payer reimbursement, embed biomarker testing into routine care across higher-income Asia-Pacific markets. Wider panels create additional commercial niches for targeted agents, reinforcing a virtuous cycle of test adoption and drug development.

Emerging Cell & RNA-Based Therapy Pipeline

Cellular immunotherapies and RNA constructs extend options beyond small molecules and antibodies. DLL3-targeted CAR-T cells report meaningful activity in small-cell disease, while CEACAM5-directed constructs enter non-small-cell trials. Individualized mRNA vaccines combined with checkpoint inhibition are advancing toward Phase III, capitalizing on patient-specific neoantigen signatures. TCR-T therapies widen the antigen universe by addressing intracellular targets. Radioligand candidates such as FXX489, which binds FAP, open a fresh class of precision payloads. Manufacturing scale-up and cost control remain hurdles, yet early efficacy signals energize investment and create merger targets for large manufacturers.

Expanding Healthcare Reimbursement Coverage

Governments and insurers broaden access as survival gains justify budget allocation. China’s National Healthcare Security Administration has listed multiple new lung agents, sharply lowering patient co-pays. The United States extended Medicare coverage to additional biomarker tests and breakthrough treatments, while Latin American payers negotiate risk-sharing contracts that tie payment to real-world outcomes. Value-based arrangements become common as dual and triple regimens prompt affordability debates. International reference pricing pressures high-income markets, yet also levels global prices, supporting adoption in lower-income countries. Real-world evidence collected through registries underpins these agreements and shapes formulary status.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High therapy costs and pricing pressures | -1.9% | Global, pronounced in emerging markets and uninsured populations | Short term (≤ 2 years) |

| Severe immune-related adverse events | -1.5% | Global, higher in elderly cohorts and multi-agent regimens | Medium term (2-4 years) |

| Looming patent cliffs for blockbuster drugs | -2.3% | North America and Europe primary, ripple effects in Asia-Pacific | Short term (≤ 2 years) |

| Limited biopsy access in low-resource areas | -1.0% | Emerging markets and rural settings worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Therapy Costs & Pricing Pressures

Annual courses often exceed USD 200,000, straining payers and patients. Durvalumab’s acquisition price slowed global uptake despite survival benefit, with cost-effectiveness analyses finding unfavorable ratios in resource-constrained regions. Biosimilar pipelines for pembrolizumab and nivolumab are expected to erode pricing power, forcing originators into value-based deals. Combination regimens compound cost, and multi-year therapy durations magnify budget impact. Reference pricing frameworks in Europe and Latin America intensify discount expectations. Manufacturers respond by offering outcome guarantees and tiered pricing, yet access gaps persist in low-income countries.

Looming Patent Cliffs for Blockbuster Drugs

Keytruda’s core patents expire in 2028, exposing over USD 20 billion annual sales to biosimilar erosion. Bristol Myers Squibb and Roche confront similar timelines across their checkpoint portfolios. Generic entrants line up dossiers as regulatory pathways for complex biologics mature. Innovators prioritize lifecycle extensions, including novel combinations, subcutaneous formulations, and new tumor sites. M&A activity targets early-stage assets that can replenish revenue streams. Market volatility is expected as payers leverage competitive bids to slash prices, potentially expanding access but squeezing margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease Type: NSCLC Dominance Faces SCLC Innovation

Non-small cell disease generated 76.68% of 2025 revenue within the lung cancer therapeutics market share, benefiting from broad biomarker-driven options and high incidence. The small-cell segment holds a smaller base yet is forecast to outpace at 13.05% CAGR through 2031, fueled by the first-in-class bispecific tarlatamab and checkpoint additions. The lung cancer therapeutics market size for small-cell therapy is therefore projected to climb swiftly from a low anchor point. Precision approaches in NSCLC, such as EGFR and KRAS inhibitors, keep that segment sizeable, but pipeline momentum is visibly shifting SCLC from neglect to opportunity.

Continued SCLC innovation narrows historic survival gaps. Tarlatamab reached 40% objective responses in heavily pre-treated cohorts, and durvalumab pushed median overall survival to 55.9 months in limited-stage settings. NSCLC pipelines add HER2 and MET inhibitors plus antibody-drug conjugates to re-intercept resistance, keeping volume leadership intact. Together, both segments illustrate a diversification that attracts specialized players while pushing incumbents to broaden portfolios.

By Treatment Modality: Immunotherapy Disrupts Chemotherapy Hegemony

Chemotherapy still accounted for 42.74% of 2025 revenue, yet immunotherapy is projected to climb at 13.02% CAGR, eroding monotherapy chemo reliance. Checkpoint inhibitors moved into first-line PD-L1-positive care, and bispecifics headline second-line SCLC protocols. The lung cancer therapeutics market size allocated to immunotherapy is forecast to double over the decade. Targeted agents add steady mid-single-digit growth by focusing on well-defined biomarkers.

Combination regimens are rising. Durvalumab plus chemotherapy extended survival in limited-stage SCLC, while chemo-IO combos dominate non-small cell first-line practice. As pipelines fill with T-cell engagers and antibody-drug conjugates, immunotherapy’s reach broadens into biomarker-low populations, enlarging addressable demand while reshaping safety management norms.

By Drug Class: Biologics Challenge Small-Molecule Dominance

Small molecules retained 63.95% revenue in 2025, helped by oral dosing and cost-efficient manufacture. Biologics and biosimilars, however, are predicted to advance 13.12% per year, trimming the gap by 2031. The lung cancer therapeutics market size for biologics will grow sharply as monoclonal antibodies, bispecifics, and radioligand conjugates gain ground. Hybrid formats like antibody-drug conjugates mix biologic targeting with potent small-molecule payloads, illustrating convergence.

Patent cliffs heighten change. Pembrolizumab biosimilars threaten incumbent biologics’ price premium, while oral small-molecule brands chase ever-smaller niches to escape generic assault. As manufacturing technology for antibodies scales, cost barriers decline, tilting favor toward biologics for difficult targets with limited small-molecule tractability.

By Distribution Channel: Retail Expansion Challenges Hospital Dominance

Hospital pharmacies dominated distribution with 69.21% revenue in 2025 because infusion-based regimens demand specialized oversight. Retail outlets, including specialty chains, are forecast for a 13.01% CAGR due to oral targeted therapies and supportive drugs that patients can manage at home. The lung cancer therapeutics market share routed through retail remains smaller but is expanding steadily.

Growth reflects healthcare decentralization. Oral EGFR, ALK, and KRAS inhibitors shift dispensing to the community, lowering patient travel burden. Specialty pharmacy programs supply adherence monitoring and cold-chain logistics, matching hospital standards. Hospitals maintain a critical role for complex infusions and acute-care rescue, preserving their lead.

By Line of Therapy: Sequential Treatment Drives Later-Line Growth

First-line protocols delivered 54.88% of 2025 sales, yet third-line and beyond treatments are set for the fastest growth at 13.18% CAGR. The lung cancer therapeutics market size in later lines benefits from extended survival that enlarges eligible cohorts. Second-line growth is moderate, sustained by agents designed to overcome specific resistance mutations.

Recent approvals illustrate momentum. Tarlatamab improved overall survival in second-line SCLC versus chemo and is expected to migrate earlier as data mature. A richer therapy arsenal compels oncologists to strategize sequences that conserve options for eventual resistance, reinforcing continual demand across all lines.

Geography Analysis

North America generated 38.62% of global revenue in 2025. Advanced trial infrastructure enables rapid translation from study to practice. Insurance systems fund high-cost regimens, though price negotiations tighten as biosimilars loom. Academic centers accelerate guideline updates, keeping adoption curves steep. Canada and Mexico participate through cross-border trials, widening patient access.

Asia-Pacific is the chief growth engine at 13.34% CAGR. China’s reimbursement expansion and local innovation double-team to unlock suppressed demand. Japan’s accelerated programs shorten review to 6 months for priority therapies, while Australia leverages expedited pathways for unmet-need cancers. India and Southeast Asia scale diagnostic capacity, installing NGS panels in tertiary hospitals. Economic development and urban pollution jointly increase lung burden, sustaining volume growth.

Europe exhibits steady mid-single-digit gains. Centralized EMA approvals speed simultaneous market launches, but reimbursement decisions remain country specific. Health technology assessment bodies focus on value thresholds, nudging manufacturers toward managed-entry agreements. Eastern European markets catch up through EU cohesion funding for oncology infrastructure. Brexit triggered parallel pathways in the United Kingdom, yet mutual recognition maintains most supply routes.

Regulatory Landscape

Regulatory oversight in lung cancer therapeutics is increasingly shaped by expedited review mechanisms for biomarker-defined populations across major agencies, including the US FDA, the European Medicines Agency (EMA), and China’s National Medical Products Administration (NMPA). The FDA continued to use accelerated approval and related oncology pathways to bring targeted agents and combinations to market, alongside ongoing post-approval confirmatory trial requirements. Meanwhile, the EMA advanced centralized approvals and label updates through CHMP opinions and marketing authorisations, including Aumseqa for EGFR-mutated NSCLC in 2026.

In China, the NMPA reinforced speed-to-trial and speed-to-market dynamics, including a stated 30-day clinical trial review and approval pathway (announced in October 2025) for national key R&D products, along with regulatory actions supporting both new authorizations and priority reviews for lung cancer therapies. Overall, regulatory direction across the United States, the EU, and China continues to favor mutation-directed claims (EGFR, HER2, RET, ROS1) and combination regimens, which increases the importance of companion diagnostics, real-world evidence collection, and pharmacovigilance for immune-related adverse events in multi-agent protocols.

Value Chain Analysis

The lung cancer therapeutics value chain spans target discovery and translational biology, clinical development with biomarker-driven trial recruitment, regulator-aligned companion diagnostics, and scaled manufacturing of small molecules and complex biologics, including antibody formats and ADCs. Commercial execution is closely tied to reimbursement and access workflows, with hospital pharmacies remaining central for infused immunotherapies and ADCs, while specialty and retail pharmacy networks expand for oral targeted therapies as dispensing shifts closer to community settings.

Manufacturing and supply continuity increasingly depend on external partners, with CDMOs and specialized fill-finish providers supporting both launch readiness and geographic redundancy. For example, Nuvation Bio completed process technology transfer and product introduction to Thermo Fisher Scientific for US-based drug product manufacturing of taletrectinib (IBTROZI) in 2026, reflecting the role of contracted capacity for precision-oncology assets. On the innovation-to-market bridge, large pharma licensing and collaboration models are used to secure late-stage targeted therapies and combination options, including AstraZeneca’s 2026 exclusive global license with Dizal for sunvozertinib (Zegfrovy) and related efforts to broaden combination regimens in NSCLC.

Competitive Landscape

Sixteen major firms share the market, producing moderate fragmentation. F. Hoffmann-La Roche, AstraZeneca, and Merck anchor checkpoint franchises, while Bristol Myers Squibb and Pfizer span multiple modalities. Patent expiries, notably Keytruda’s in 2028, invite biosimilar entries that threaten entrenched share. Developers respond by bundling assets: AstraZeneca couples durvalumab with antibody-drug conjugates, and Johnson & Johnson combines amivantamab with lazertinib to counter osimertinib resistance.

Emergent Asian biotechs such as BeiGene and Innovent gain global profiles through PD-1 antibodies priced 30–40% below Western peers, adding cost competition. Technology convergence shapes future positioning. AI-driven screening cuts hit-to-lead timelines, while in-house diagnostic units secure companion tests. Radioligand and cell therapy capabilities are acquisition priorities, illustrated by recent tie-ups between large pharma and nuclear-medicine specialists. The race favors platforms that supply combination flexibility, cost-disciplined manufacturing, and global supply chain reach.

Lung Cancer Therapeutics Industry Leaders

-

AstraZeneca

-

Boehringer Ingelheim

-

Bristol-Myers Squibb Company

-

Novartis AG

-

Eli Lilly and Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Whitespace in lung cancer therapeutics increasingly centers on earlier-line precision targeting and on combination strategies designed to address resistance and heterogeneous tumor biology in both NSCLC and SCLC. One clear opportunity is first-line targeted therapy expansion beyond established EGFR and ALK settings into additional molecular subsets, supported by recent regulatory momentum such as the FDA action in February 2026 for Boehringer Ingelheim’s zongertinib (HERNEXEOS) in HER2-mutant advanced NSCLC. That momentum increases demand for routine, broad-panel molecular profiling and creates additional commercial room for companion diagnostics and integrated clinic-to-pharmacy pathways that shorten time from test result to treatment initiation.

Combination-led development also offers a visible differentiation route, including ADC plus PD-1/PD-L1 regimens that aim to extend benefit to both biomarker-defined and biomarker-low populations. Published Phase 3 evidence in 2026 (OptiTROP-Lung05) reporting progression-free survival improvement with sacituzumab tirumotecan plus pembrolizumab in PD-L1-positive advanced NSCLC highlights how combination protocols can reshape sequencing and formulary evaluations. Regulatory designations reinforce this active development environment, including the FDA Breakthrough Therapy Designation granted in May 2026 for Merck’s investigational KRAS G12C inhibitor calderasib (MK-1084) with pembrolizumab for first-line KRAS G12C-mutant NSCLC, as well as EMA validation in 2026 for taletrectinib in ROS1-positive NSCLC, which points to continued competitive entry in smaller, high-value molecular niches.

Recent Industry Developments

- July 2026: AstraZeneca entered an exclusive global license agreement with Dizal Pharmaceutical to develop and commercialize Zegfrovy (sunvozertinib), an oral EGFR inhibitor for lung cancer with exon 20 insertion mutations. The deal added a late-stage targeted asset to AstraZeneca’s lung cancer franchise and reinforced its positioning in oral precision oncology alongside established EGFR therapy platforms.

- July 2025: The US FDA granted accelerated approval to sunvozertinib (Zegfrovy) for adults with locally advanced or metastatic EGFR exon 20 insertion NSCLC. The approval expanded the set of targeted options for a historically difficult-to-treat subgroup and highlighted the role of expedited FDA pathways in speeding NSCLC launches.

- April 2024: The US FDA cleared durvalumab for limited-stage small-cell lung cancer. The decision broadened immunotherapy use into an earlier SCLC setting and supported increased adoption of multi-modality regimens that combine immunotherapy with existing standards of care.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenue generated from therapeutic treatment used to manage lung cancer in patients, counted at the global level across major regions and key countries, for the defined study period.

Scope exclusions: We exclude screening, diagnostics, surgical procedures, and supportive care that is not a therapeutic treatment for lung cancer.

Segmentation Overview

-

By Disease Type

- Non-Small Cell Lung Cancer (NSCLC)

- Small Cell Lung Cancer (SCLC)

- Others

-

By Treatment Modality

- Chemotherapy

- Immunotherapy

- Targeted Therapy

-

By Drug Class

- Small-Molecule Drugs

- Biologics and Biosimilars

-

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

-

By Line of Therapy

- First-Line

- Second-Line

- Third-Line and Beyond

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to define the demand pool and set market context before any sizing was finalized. We relied on public epidemiology and health system signals to map where treatment volumes can realistically occur, then linked this to therapy use patterns by line of care where possible.

Typical inputs came from sources such as the World Health Organization, International Agency for Research on Cancer (GLOBOCAN), national cancer registries and health agencies such as the US CDC, peer reviewed oncology journals, and clinical trial registries such as ClinicalTrials.gov. We also reviewed annual reports, investor presentations, and press releases to understand portfolio mix and reported oncology performance, supported by paid subscriptions for company financials and another for patents to track therapy launches and exclusivity timelines. These sources listed are illustrative only, and many other public references were also used for data collection, cross-checking, and clarifying assumptions.

Primary Interviews and Surveys

Primary work was done to validate treatment mix, uptake timing, and pricing logic across regions, since these can shift quickly with guideline updates and new approvals. We spoke with a mix of clinicians, hospital pharmacy stakeholders, and payor or reimbursement experts, along with other industry participants across APAC, EMEA, and the Americas. The goal was to close gaps from desk research and pressure-test the final assumptions used in the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 13% | APAC: 53% |

| Mid tier: 48% | Functional/Unit leaders: 38% | EMEA: 29% |

| Smaller Players: 15% | Managers: 49% | Americas: 18% |

Market-Sizing & Forecasting

Sizing started with a top-down build where incidence and prevalence signals were translated into a treated patient pool, then adjusted using diagnosis rates, biomarker testing penetration, and therapy eligibility by cancer type. After the demand pool was framed, value was modeled using therapy mix shares and average annual treatment cost, and then aligned to region-level reimbursement and access realities.

To keep the model grounded, we tracked a small set of market fingerprints as core inputs. These included the NSCLC versus SCLC split, the shares of targeted therapy and immunotherapy in treated patients, line-of-therapy movement toward earlier use, and the timing of new approvals that can shift regimen selection. Because price is not a single global number, ASP progression was handled with region-level currency timing and expected net-price direction based on contracting and loss of exclusivity. Results were corroborated through selective bottom-up checks using supplier revenue cues, sampled price points, and volume reasonableness by key countries. Where information gaps existed, we used conservative interpolation based on adjacent markets with similar access patterns.

For forecasting, scenario analysis was applied so the base case reflected expected uptake of newer regimens, while still allowing sensitivity around approval timing, payer restrictions, and guideline changes. Assumptions were reviewed with primary experts by region, and any step-change forecast was only kept when it matched clinical adoption logic and observable policy signals.

Data Validation & Update Cycle

Validation was done in multiple passes so the final number did not depend on a single assumption. Outputs were checked against independent signals such as epidemiology trend direction, regional treatment access, and therapy mix consistency. When a country or region moved outside a realistic band, we investigated the driver and revised where needed.

Before sign-off, the model and key drivers go through an analyst review step, followed by targeted re-contacts when inputs looked inconsistent or when a new approval changed treatment patterns. Reports are refreshed annually, and interim updates are triggered for material events such as major label expansions, reimbursement changes, or loss of exclusivity. Right before delivery, we do a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Global Lung Cancer Therapeutics Market Market Size Measured Against Other Published Estimates

Published market sizes for lung cancer therapeutics can differ even when the topic name sounds the same, because the counted year, therapy inclusions, and pricing logic are not always aligned. The spread is usually explained by how each study treats radiation and other non-drug treatments, how it handles net pricing versus list pricing, and how quickly it assumes newer classes move into earlier lines of therapy.

Key gaps also come from timing choices. Some sources anchor on 2025 while others start at 2026, and they then apply different currency conversion points. In addition, some estimates blend broader oncology revenue proxies into the total when patient-level demand indicators are not rebuilt, which can make the total look higher even if treated volumes are not explicitly validated.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 31.32 B (2026) | |

| Industry Publisher A | USD 32.50 B (2025) | Uses a different base year and a shorter forecast window, and the demand build appears more anchored to a 2025 starting point, which can change adoption timing for newer regimens versus a 2026 start. |

| Industry Publisher B | USD 35.37 B (2025) | Likely captures a broader therapy value pool and applies a higher 2025 price level, which can lift totals when net pricing and therapy mix shifts are not normalized consistently across regions. |

The table shows a clear year and scope effect behind the size differences, and in Mordor Intelligence's model the 2026 value is tied to a treated-patient demand build and includes chemotherapy, radiation therapy, immunotherapy, targeted therapy, and other treatments, which are then priced with region-level currency timing rather than a single global price assumption. When the same demand signals and timing rules are applied consistently, the result is a more traceable number that can be updated step by step as approvals, access, and regimen mix change.

Key Questions Answered in the Report

What is the projected value of the lung cancer therapeutics market by 2031?

The market is forecast to reach USD 55.88 billion by 2031, supported by a 12.31% CAGR.

Which disease segment is expanding fastest within lung cancer treatment?

Small-cell lung cancer therapies are expected to grow 13.05% annually through 2031, outpacing non-small-cell treatments.

How will Keytrudas 2028 patent expiry influence competition?

Biosimilar entries are set to erode premium pricing and open a USD 20 billion revenue gap, prompting originators to launch next-generation drugs.

Why is Asia-Pacific the most attractive growth region for lung cancer treatments?

Expanding reimbursement, large patient populations, and streamlined regulatory pathways drive a 13.34% CAGR in the region.

Which drug class will gain the most share against small molecules over the decade?

Biologics, including monoclonal antibodies and bispecifics, are projected to climb at 13.12% CAGR, narrowing the gap with small molecules.

What role do retail pharmacies play in future lung cancer drug distribution?

Oral targeted therapies and specialty support programs are moving more dispensing to retail outlets, which are set for a 13.01% CAGR.

Page last updated on: