Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 35.68 Billion |

| Market Size (2031) | USD 42.86 Billion |

| Growth Rate (2026 - 2031) | 3.74% CAGR |

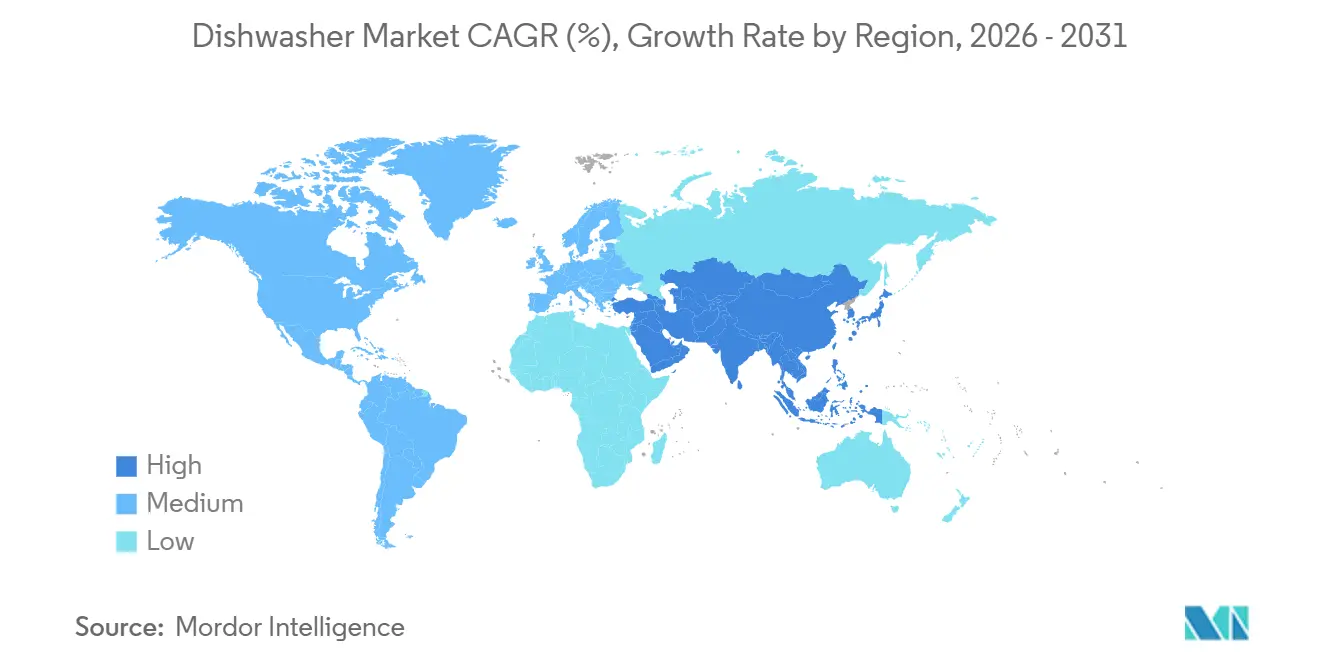

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

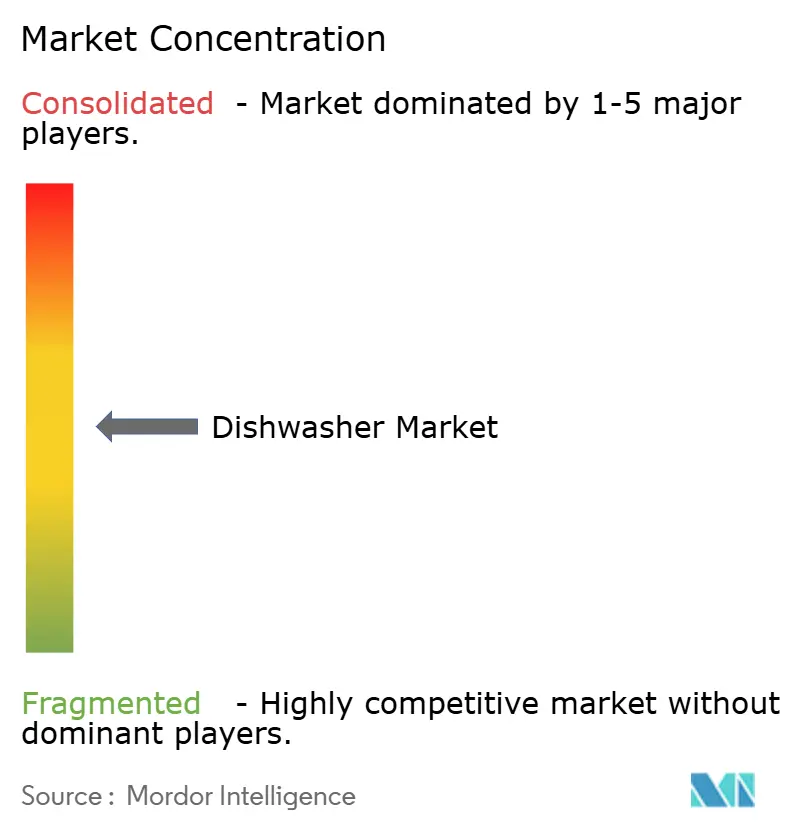

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dishwasher Market Analysis by Mordor Intelligence

The global dishwasher market size was USD 34.39 billion in 2025, is set to reach USD 35.68 billion in 2026, and is forecast to rise to USD 42.86 billion by 2031, reflecting a 3.74% CAGR during 2026-2031. Efficiency rules and labels in major markets continue to move designs toward lower energy and water consumption, and those rules are tightening, redirecting R&D toward hydraulics, motors, and drying methods. The adoption of smart-home ecosystems further supports the dishwasher market by offering remote diagnostics, predictive maintenance, and voice-controlled convenience. These features enhance the perceived value of appliances and accelerate upgrade decisions. Manufacturers are leveraging scale efficiencies in electronic components to gradually lower average selling prices without compromising margins, thereby expanding the customer base in emerging regions.

Key Report Takeaways

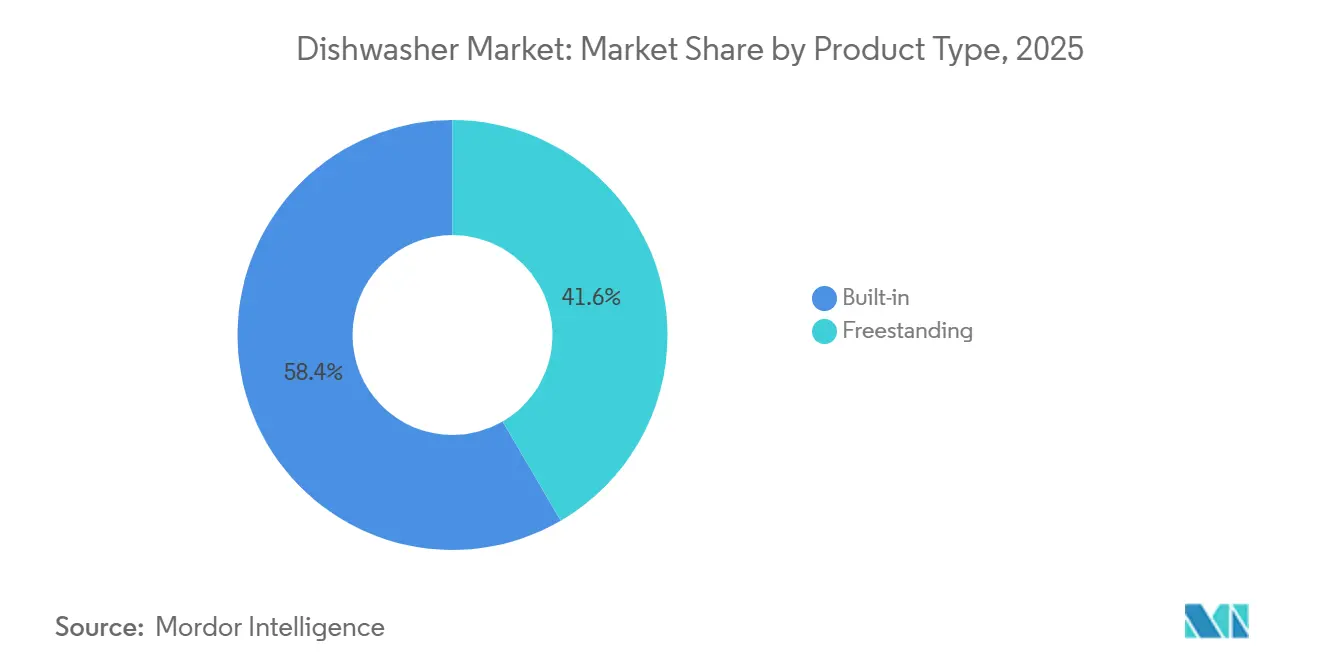

- By product type, built-in dishwashers led with 58.40% of the global dishwasher market share in 2025, and the same segment is projected to expand at a 5.09% CAGR through 2031.

- By application, the residential segment accounted for 82.15% of the global dishwasher market share in 2025, while the commercial segment is forecast to grow at a 6.76% CAGR to 2031.

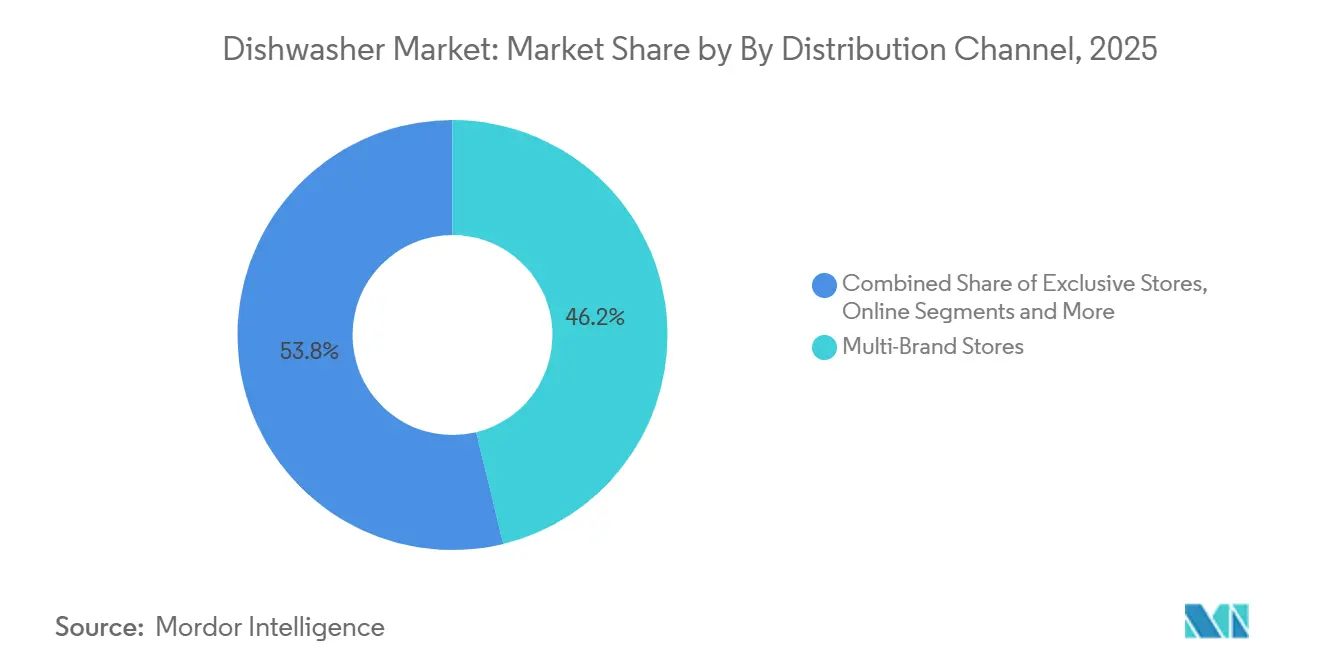

- By distribution channel, multi-brand stores held 46.25% of the global dishwasher market share in 2025, while online channels are projected to advance at a 6.94% CAGR through 2031.

- By geography, Asia-Pacific commanded 36.20% of the global dishwasher market share in 2025, and the Middle East & Africa is expected to record the highest regional growth at a 6.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dishwasher Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory push for higher energy- and water-efficiency standards | +0.6% | Global, with stricter enforcement in the European Union, North America, and China | Medium term (2-4 years) |

| Kitchen remodeling and built-in adoption in mature markets | +0.5% | North America, Europe, Australia | Short term (≤ 2 years) |

| Rising household penetration in underpenetrated urban markets | +1.2% | Asia-Pacific core (China, India), spill-over to MEA | Long term (≥ 4 years) |

| E-commerce enablement and omnichannel retail execution | +0.7% | Global, led by North America, Europe, and urban Asia-Pacific | Short term (≤ 2 years) |

| In-sink/compact formats unlocking first-time ownership in micro-kitchens | +0.4% | Asia-Pacific urban (China, Japan, South Korea, Singapore) | Medium term (2-4 years) |

| Smart features driving premium replacement | +0.5% | North America, Western Europe, urban Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Push for Higher Energy- and Water-Efficiency Standards

Policy makers in the European Union, the United States, and other large markets have tightened energy and water thresholds, which pulls dishwasher engineering toward more efficient hydraulics, heat management, and motors [1]European Commission, “Commission Delegated Regulation (EU) 2019/2017 on Energy Labeling of Dishwashers,” EUR-Lex, eur-lex.europa.eu . Clear labeling requirements such as the European Union energy label and the United States ENERGY STAR Version 8.0 specification make operating-cost differences visible at the point of sale, and this steers many purchases in the global dishwasher market toward models with stronger lifecycle performance. Meeting divergent regional test methods and compliance checks often requires re-engineering or, at a minimum, re-testing, which raises per-unit costs for smaller brands that lack platform scale. Companies that operate R&D to surpass coming thresholds earn more time between redesigning and avoid access risks at rule-change milestones. This regulatory cadence increases the strategic weight of component commonality and global platforms while preserving the flexibility to adapt to local rules in the global dishwasher market.

Kitchen Remodeling and Built-In Adoption in Mature Markets

In North America and Western Europe, kitchen renovations often specify integrated appliance suites, which keep built-in dishwashers high on the consideration list during remodels. Builder and contractor ecosystems influence brand selection and pricing, and they elevate products that align with cabinetry and ventilation plans that are common in mid to high-end projects. These channels deliver steady volume but can compress margins due to volume pricing and coordinated installation schedules that reward predictable suppliers in the global dishwasher market. Lead times for panel-ready units tend to be longer than for freestanding units because of cabinetry coordination and trade scheduling, which can slow first-time adoption outside planned projects. New home construction trends also matter because many builders pre-install dishwashers, which brings decisions upstream and concentrates bargaining power with national builders that negotiate at scale in the global dishwasher market.

Rising Household Penetration in Underpenetrated Urban Markets

Urbanization tailwinds and rising disposable incomes in China, India, and other Asian economies support first-time purchases where penetration is still low relative to developed regions. As more dual-income households seek time savings, dishwashers shift from discretionary to essential among early adopters, particularly in tier-one and tier-two cities in the global dishwasher market. Infrastructure gaps slow progress in older apartments without dedicated electrical circuits, hot-water lines, or drain standards that align with standard appliance installation. Developers are adding provisions for dishwashers in new towers, which reduces installation complexity and raises take-up among buyers who want move-in-ready kitchens in the global dishwasher market. Compact and faucet-connected formats help early households cross the threshold, although their smaller capacity makes them a bridge category rather than the endpoint for larger families.

E-Commerce Enablement and Omnichannel Retail Execution

More consumers now research and purchase large appliances online, where they can compare features, energy labels, and pricing, and then add scheduled delivery and installation during checkout. This shift trims the dependence on showrooms and nudges manufacturers to invest in digital content, visualization tools, and direct-to-consumer logistics that match white-glove service benchmarks in the global dishwasher market. Marketplaces provide scale but press on pricing, which favors brands that can balance sponsored placements with margin protection. Economics reward incumbents that can absorb fulfillment costs and maintain dense service networks for warranty and repairs, while smaller brands face delivery-time and service-coverage gaps online. The net effect is a faster discovery-to-purchase loop and marketing budget reallocation from storefronts to search and media in the global dishwasher market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost and installation complexity for built-in models | -0.3% | Global, acute in price-sensitive Asia-Pacific, MEA, Latin America | Short term (≤ 2 years) |

| Cultural habits and low awareness are limiting adoption in parts of the Asia-Pacific & Africa | -0.5% | India, Indonesia, Sub-Saharan Africa, parts of the Middle East | Long term (≥ 4 years) |

| Space/plumbing/electrical retrofit constraints in emerging markets | -0.4% | Urban Asia-Pacific, MEA, Latin America | Medium term (2-4 years) |

| Leasing/rental models in HoReCa are delaying outright purchases | -0.2% | Global commercial segment, pronounced in North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost and Installation Complexity for Built-In Models

Built-in models usually carry higher purchase prices than equivalent freestanding units, and they also require paid installation for electrical, plumbing, and cabinetry alignment. The need to coordinate multiple trades can extend timelines, which adds friction for first-time buyers in the global dishwasher market. In price-sensitive regions and rental-heavy markets, the mix of product cost and installation labor makes freestanding units more attractive [2]World Bank Data Team, “Urban Population (% of Total Population),” World Bank, worldbank.org . The scarcity of skilled trades in some countries also pushes labor costs higher and increases wait times. These hurdles reduce impulse purchases and push many buyers toward simpler formats in the global dishwasher market.

Cultural Habits and Low Awareness Limiting Adoption in Parts of Asia-Pacific & Africa

Manual dishwashing remains the default in many South Asian and African households, and this leads to misconceptions about machine water and energy use. Peer-reviewed research has shown that efficient dishwashers can use less water and energy than typical manual washing, but awareness is limited in many markets. Cookware that is not dishwasher-safe further reduces the perceived benefit when many items would still be washed by hand in the global dishwasher market. In-store and influencer demonstrations can help close knowledge gaps, but habit change is gradual. Localization of racks, spray patterns, and cycles can improve outcomes with regional dishes and speed adoption in the global dishwasher market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Built-In Models Command Share, But Freestanding Units Enable Market Entry

Built-in dishwashers held 58.40% of the dishwasher market size in 2025, and they are projected to grow at 5.09% CAGR through 2031 as remodeling and new-build installations sustain demand in mature markets. These products match integrated kitchen designs and offer premium features that lift average selling prices in the global dishwasher market. Installation complexity limits adoption in rental-heavy and price-sensitive settings, which keeps freestanding formats relevant for first-time buyers. Builder programs concentrate volume and increase negotiating leverage on price and service-level agreements across the global dishwasher market.

Freestanding units remain an important gateway, as they require only a standard outlet and a water connection, allowing same-day delivery and simpler setup. Compact and countertop variants address micro-kitchen constraints and can connect to a faucet, which reduces the need for cabinet changes in the global dishwasher market. Panel-ready built-ins command the highest prices and rely on tight coordination with designers and cabinet makers. Portable models serve temporary or space-constrained applications and provide a stable niche that supports channel breadth in the dishwasher industry.

By Application: Residential Dominates, But Commercial Segment’s Leasing Shift Alters Revenue Models

Residential accounted for 82.15% of the dishwasher market size in 2025, which reflects the large installed base in single-family homes, condos, and apartments across leading regions. Replacement cycles of 10 to 12 years in mature markets and the appeal of energy-efficient upgrades sustain steady volumes in the global dishwasher market [3]World Bank Data Team, “Urban Population (% of Total Population),” World Bank, worldbank.org . First-time purchases in urban Asia add incremental demand, though infrastructure and awareness remain constraints. Multi-unit developers increasingly specify dishwashers to meet renter expectations, which channels more volume through bulk procurement in the global dishwasher market.

Commercial is forecast to grow at 6.76% CAGR through 2031 on the back of labor-tight conditions and health-code compliance in hospitality and food service. Leasing and equipment-as-a-service packages expand access, spread payments over time, and bundle maintenance, but they shift asset risk to OEMs or financing partners in the global dishwasher market. High-temperature sanitizing and throughput needs drive specification in foodservice, and certified machines can carry price premiums where compliance is critical. As models add connected monitoring and predictive maintenance, service revenue opportunities grow alongside the installed base in the dishwasher industry.

By Distribution Channel: Multi-Brand Stores Under Margin Pressure as Online CAGR Accelerates

Multi-brand stores held 46.25% of the dishwasher market size in 2025, supported by expert sales support, live displays, and bundled delivery-install services. These retailers benefit from adjacent categories in showrooms, although cost structures and price-matching behavior pressure margins in the global dishwasher market. Exclusive SKU strategies reduce direct price comparisons, which helps preserve store economics at the cost of greater supply complexity. Builder and designer channels aggregate volume for specification-driven sales, especially on built-ins in the global dishwasher market.

Online is set to grow at 6.94% CAGR through 2031 as consumers trust large-appliance purchases on the web, aided by transparent pricing and installation scheduling. Direct-to-consumer platforms let brands reclaim margin and control post-sale experience, while marketplaces trade margin for reach in the global dishwasher market. Investments in augmented reality, energy-cost calculators, and delivery slot selection narrow the gap with in-store consultation. Scale advantages in fulfillment and after-sales support favor incumbents online, reinforcing share where delivery and service networks are dense in the dishwasher industry.

Geography Analysis

Asia-Pacific held 36.20% of the global dishwasher market in 2025, led by China, Japan, and South Korea, where rising incomes and smaller households support adoption. Penetration remains low relative to developed regions, and infrastructure gaps in older buildings slow conversion to built-ins in the global dishwasher market. Local brands lead to compact and sink-integrated formats suited to micro-kitchens, while global brands lean into premium features in tier-one cities. India’s category is in early stages, given limited awareness and household help dynamics, although dual-income households are starting to shift attitudes in the global dishwasher market.

North America shows mature dynamics where growth depends on replacement and new-home construction, and penetration in single-family homes exceeded 70% in recent surveys [4]U.S. EIA Survey Team, “Residential Energy Consumption Survey,” EIA, eia.gov . Europe follows a similar path with built-ins as the standard in countries like Germany, France, and the United Kingdom, with room to grow in parts of Southern and Eastern Europe. The Middle East and Africa are projected to post the fastest regional growth at 6.86% through 2031, supported by infrastructure investment in the Gulf, a rising middle class in select African markets, and urban-tower projects that pre-install appliances in the global dishwasher market. South America’s progress is more variable due to macro volatility and currency depreciation, which weigh on appliance affordability and long-term planning for manufacturers in the global dishwasher market. Oceania shows mature replacement patterns with renovation-driven built-in adoption and ongoing focus on energy efficiency supported by national programs.

Competitive Landscape

The global dishwasher market shows moderate concentration, with the top five brands accounting for 56.4% of revenue in 2025 and leaving meaningful room for regional players and private-label suppliers. Competition emphasizes maintaining margins by pairing feature upgrades, such as quieter operation, faster cycles, and connected functions, with operational levers, such as local production and supplier diversification in the global dishwasher market. Incumbents standardize components where it is feasible to gain scale while tailoring control panels, racks, and cycles to regional preferences. Companies that link connected diagnostics to service operations can lower warranty costs and lift customer satisfaction in the global dishwasher market.

Compact-format specialists and direct-to-consumer challengers target dense urban markets with space-aware designs and social-first marketing, but their service coverage and distribution depth remain limited. Global leaders respond by expanding compact lines while keeping focus on built-ins for core volume in the global dishwasher market. Strategic moves since 2025 include capacity expansions, supply-chain verticalization, and software-driven product differentiation that seek to harden moats without relying on price-only tactics. Collaborations between appliance makers and detergent brands to co-develop auto-dosing systems aim to create recurring revenue, though buyers can resist proprietary cartridge models in the global dishwasher market.

Recent product news underscores the role of speed and connectivity in premium tiers, as well as regional capacity plays to defend share. Builders and hospitality buyers continue to influence specification, which encourages manufacturers to align roadmaps with compliance standards and installation requirements in the global dishwasher market. The direction of travel favors brands that pair hardware improvements with digital tooling and service models, while managing channel conflict as online sales grow in the global dishwasher market.

Dishwasher Industry Leaders

BSH Hausgeräte GmbH (Bosch-Siemens)

Whirlpool Corporation

Electrolux AB

Haier Smart Home Co.

Midea Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: BSH Hausgeräte announced a EUR 150 million (USD 165 million) investment in its manufacturing facility in Nauen, Germany, to expand production of built-in dishwashers with heat-pump drying technology, targeting a 20% capacity increase by Q4 2026. The expansion responds to rising demand for energy-efficient models compliant with the European Union's updated ecodesign regulations, taking effect in 2027, positioning BSH to meet stricter water and electricity consumption thresholds ahead of competitors.

- December 2025: Whirlpool Corporation completed its acquisition of a 35% stake in a Turkish appliance component supplier for USD 48 million, securing access to spray-arm assemblies and pump motors. The investment vertically integrates Whirlpool's supply chain in Europe and reduces reliance on Asian imports subject to tariff volatility, a strategic hedge against trade-policy uncertainty.

- November 2025: LG Electronics launched its ThinQ-enabled dishwasher line across South Korea and Japan, featuring AI-powered cycle optimization, remote diagnostics via smartphone app, and integration with LG's smart-home platform. The premium models are priced 18-22% above baseline units, target replacement buyers seeking connectivity, and the company's data indicates early adopters run 15% fewer service calls due to predictive maintenance alerts.

- October 2025: Haier Smart Home opened a 120,000-square-meter dishwasher manufacturing plant in Hefei, China, with an annual capacity of 2.5 million units. The facility incorporates automated assembly lines and IoT-enabled quality-control systems, reducing per-unit production costs by an estimated 8-10% and supporting Haier's strategy to defend share in China's fast-growing mid-tier segment against Midea and local challengers.

Global Dishwasher Market Report Scope

A dishwasher is a mechanical device that performs the function of cleaning cutlery and dishware by spraying hot water on the dishes to remove the soiling. The increasing expenditure involved in hiring manual cleaners is the primary factor responsible for the inclination of consumers toward the installation of automated dishwashers across various residential and commercial sectors.

The Global Dishwasher Market Report is segmented by Product Type (Freestanding and Built-in), Application (Residential and Commercial), Distribution Channel (Multi-Brand Stores, Exclusive Stores, Online, and Other Distribution Channels), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East & Africa). The market forecasts are provided in terms of value in USD.

By Product Type

| Freestanding |

| Built-in |

By Application

| Residential |

| Commercial |

By Distribution Channel

| Multi-Brand Stores |

| Exclusive Stores |

| Online |

| Other Distribution Channels |

By Geography

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Product Type | Freestanding | |

| Built-in | ||

| By Application | Residential | |

| Commercial | ||

| By Distribution Channel | Multi-Brand Stores | |

| Exclusive Stores | ||

| Online | ||

| Other Distribution Channels | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the size of the global dishwasher market, and how fast is it growing to 2031?

The global dishwasher market size is expected to increase from USD 34.39 billion in 2025 to USD 35.68 billion in 2026 and reach USD 42.86 billion by 2031, at a 3.74% CAGR over 2026-2031.

Which product type leads and which channels are growing fastest?

Built-in models led with 58.40% share in 2025, while online channels are projected to grow at a 6.94% CAGR to 2031.

Which application will expand the most through 2031?

Residential dominated with 82.15% in 2025, but commercials are forecast to grow faster at 6.76% CAGR as operators address labor and hygiene requirements.

Which regions matter most for growth and scale in the next five years?

Asia-Pacific held 36.20% in 2025, offering the largest base, while the Middle East and Africa are projected to grow at 6.86% through 2031.

What features and standards are shaping product development right now?

Efficiency rules and labels like European Union ecodesign and ENERGY STAR Version 8.0, plus connected diagnostics and auto-dosing, are shaping designs and upgrading cycles.

How concentrated is competition among leading brands?

The top five companies controlled 56.4% of global revenue in 2025, which indicates a moderately concentrated competitive landscape.

Page last updated on: