Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 41.43 Billion |

| Market Size (2031) | USD 60.58 Billion |

| Growth Rate (2026 - 2031) | 7.88% CAGR |

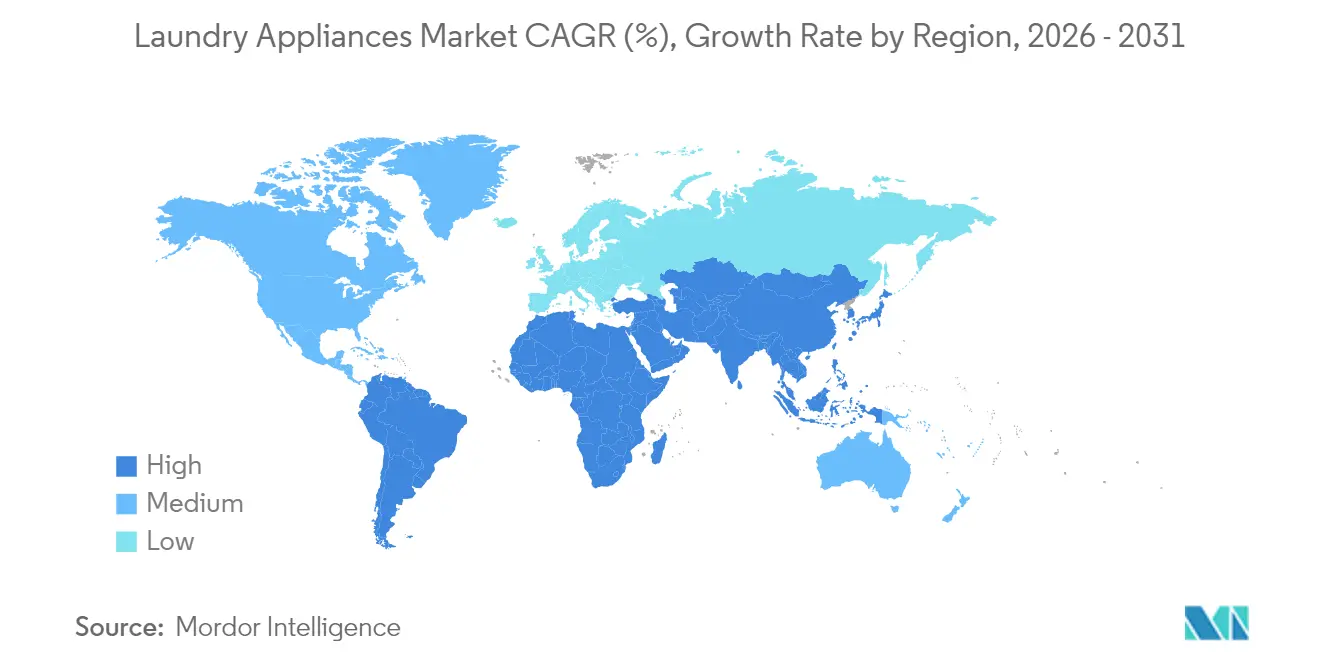

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Laundry Appliances Market Analysis by Mordor Intelligence

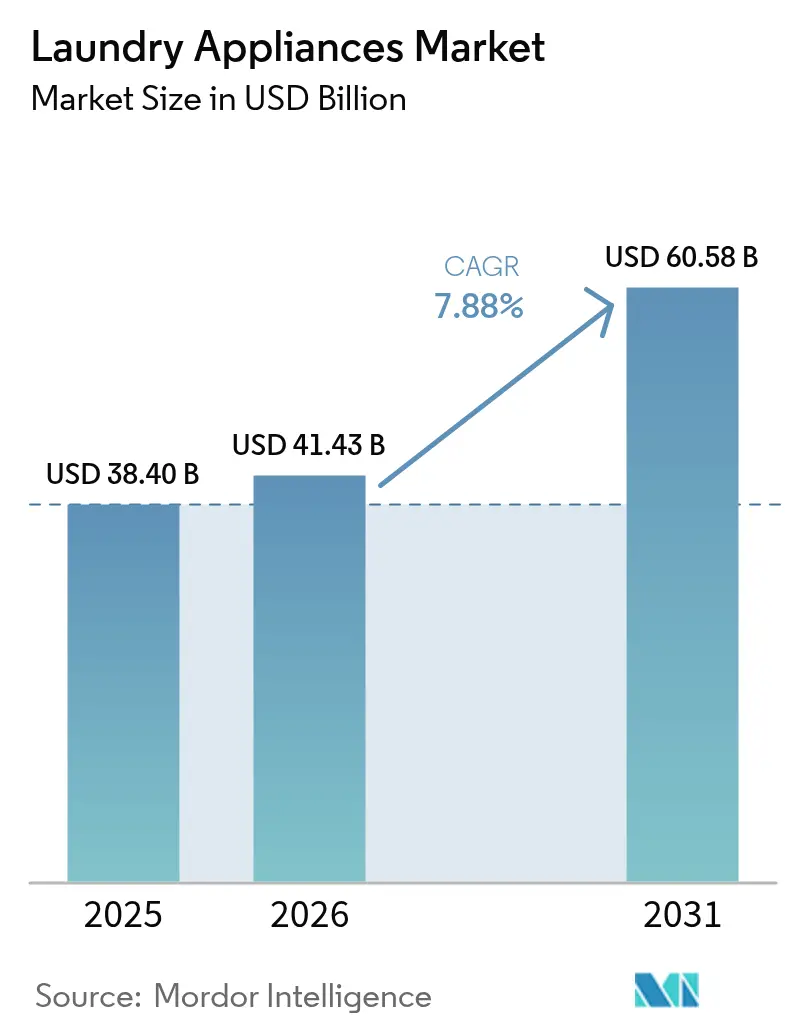

The Laundry Appliances market size is expected to grow from USD 38.40 billion in 2025 to USD 41.43 billion in 2026 and is forecast to reach USD 60.58 billion by 2031 at 7.88% CAGR over 2026-2031.

Urbanization, stricter energy-efficiency mandates, and rapid technological innovation converge to create balanced momentum that blends replacement purchases in mature economies with first-time installations in fast-growing regions. Consumers increasingly favor connected, high-efficiency models that reduce utility costs while delivering convenience gains, prompting manufacturers to speed up product refresh cycles and to expand direct-to-consumer offerings. Heightened raw-material price volatility pressures margins but simultaneously intensifies R&D investment in materials science, modular design, and predictive maintenance that offset cost swings over the product life-cycle. E-commerce adoption accelerates competitive dynamics as online channels give brands granular access to consumer data, enabling agile inventory planning and targeted promotion strategies that amplify the overall growth trajectory of the laundry appliances market.

Key Report Takeaways

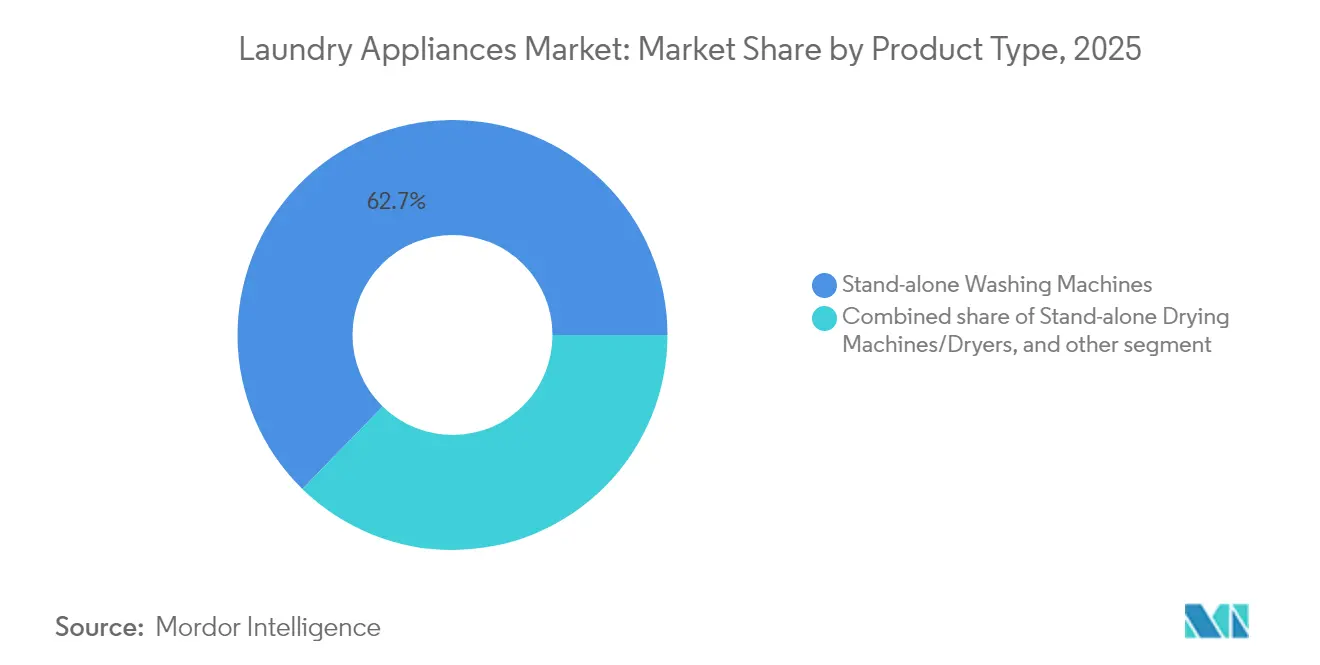

- By product type, stand-alone washing machines captured 62.70% of the laundry appliances market share in 2025, while the laundry appliances market size for combined washer-dryers is projected to grow the fastest at a 10.18% CAGR during 2026-2031.

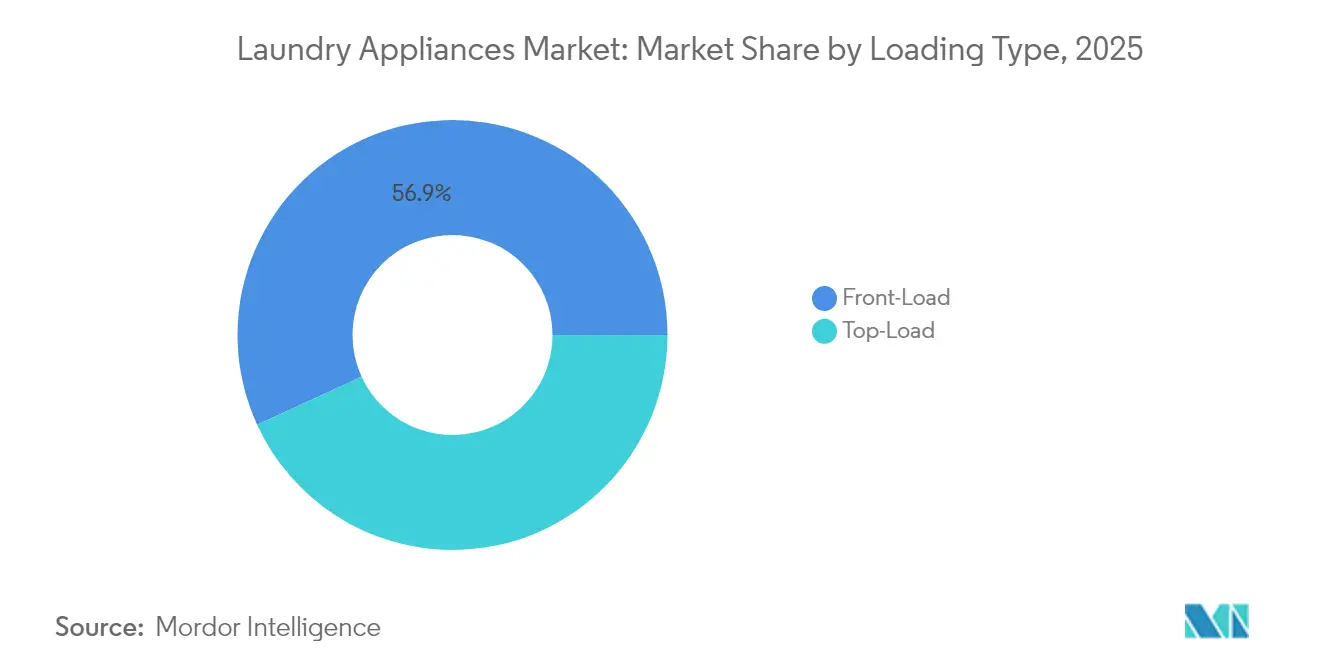

- By loading type, front-load machines accounted for 56.85% of the laundry appliances market share in 2025, and the laundry appliances market size for front-load units is expected to expand at a 8.98% CAGR between 2026 and 2031.

- By capacity, the 6-8 Kg segment held 46.90% of the laundry appliances market share in 2025, while the above 8 Kg segment is projected to be the fastest-growing, with a 9.65% CAGR through 2031.

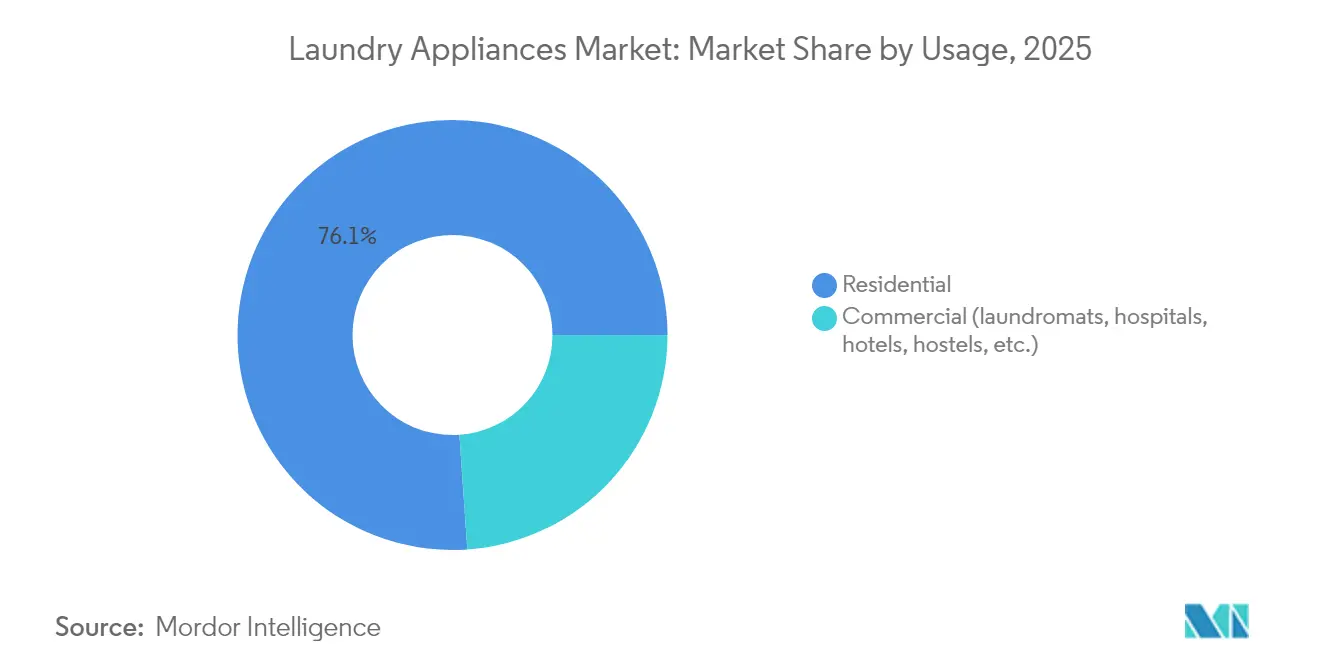

- By usage, the residential category dominated with 76.10% of the laundry appliances market share in 2025, whereas the commercial segment is forecast to grow the quickest, posting a 9.94% CAGR from 2026-2031.

- By distribution channel, the B2C/retail segment represented 70.60% of the laundry appliances market share in 2025, but the B2B/direct channel is expected to expand faster, with a CAGR of 8.11% over 2026-2031.

- By geography, Asia-Pacific led the landscape with 42.95% of the laundry appliances market share in 2025, while the Middle East & Africa region is set to be the fastest-growing, advancing at a 6.32% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Laundry Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising urban middle-class disposable income | +2.1% | Global, strongest in APAC and MEA | Medium term (2-4 years) |

| Proliferation of energy-efficient inverter motors | +1.8% | Global, EU and North America leading adoption | Long term (≥ 4 years) |

| E-commerce penetration in white-goods retail | +1.2% | Global, highest impact in North America and Europe | Short term (≤ 2 years) |

| Government subsidies for high-efficiency appliances | +0.9% | North America, EU, Australia, select APAC markets | Medium term (2-4 years) |

| On-premise laundry demand from co-living spaces | +0.7% | Urban centers globally, concentrated in North America and APAC | Long term (≥ 4 years) |

| AI-powered predictive-maintenance features | +0.5% | Developed markets initially, expanding to emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Urban Middle-Class Disposable Income

Disposable income growth in emerging economies drives first-time appliance purchases, especially in India, where washing-appliance revenue is set to jump significantly.[1]IBEF, “Indian Consumer Market,” Indian Brand Equity Foundation, ibef.org. As households transition from manual to automated washing, time savings enable additional wage-earning activities, reinforcing a virtuous spending cycle that accelerates laundry appliances market penetration. In China, domestic washing-machine sales reached 40.05 million units in 2023, a 3.4% rise year-over-year despite market maturity. African economies present the broadest white-space opportunity: imports of major home appliances totaled USD 3 billion against exports of USD 330 million, spotlighting scope for local assembly and after-sales networks. Urban density boosts collective demand for compact, high-capacity, and energy-efficient models that fit smaller living spaces common in megacities.

Proliferation of Energy-Efficient Inverter Motors

Advanced inverter motors cut electricity usage by up to 40% versus conventional alternatives, aligning with the EU ecodesign rule that bans non-heat-pump dryers from July 2025 to save 15 TWh of energy and slash 1.7 Mt CO₂e by 2040.[2]European Commission, “New Measures for More Energy Efficient Household Tumble Dryers,” energy.europa.eu. Appliances makers leverage this tailwind by positioning higher-margin SKUs with built-in AI energy modes, as seen in Samsung’s Bespoke AI washer that achieves 20% additional savings. Adoption cascades from premium to mass segments, expanding inverter penetration to mid-tier top-load models across Asia-Pacific and Latin America. Emerging regulatory replicas in Australia and Canada hint at global standardization that cements energy efficiency as an indispensable buying criterion. Concurrently, reduced operating costs shorten payback periods, nurturing replacement demand even in price-sensitive markets.

E-Commerce Penetration in White-Goods Retail

Online channels captured nearly 29% of U.S. home-improvement purchases in 2024, with electrical appliances commanding 28.2% share of USD 289 billion in digital electronics sales. Amazon, Apple, and Walmart dominate but specialized marketplaces and direct-to-consumer storefronts gain traction as shoppers seek extensive product detail, reviews, and bundling options. Home Depot’s appliance department vaulted from 12th to 2nd place in revenue contribution between 2012 and 2021, underscoring the omnichannel synergy of click-and-collect models. Direct access to consumer data lets brands refine SKU assortments, personalize promotions, and optimize inventory, compressing product life cycles and stimulating repeat purchases that lift overall laundry appliances market revenue.

Government Subsidies for High-Efficiency Appliances

Public incentives offset upfront price premiums. The U.S. Inflation Reduction Act’s HEAR program offers up to USD 1,680 per heat-pump dryer, with New York pioneering in-store rebates of USD 840.[3]U.S. DOE, “New York First to Launch In-Store Home Energy Rebates,” energy.gov. Queensland’s rebate of AUD 300–1,000 (USD 200–680) on efficient models exhibits policy convergence, accelerating technology shifts across developed and emerging markets alike. Manufacturers often synchronize flagship launches to coincide with funding windows, expanding capture of time-limited demand spikes. Subsidy volatility tied to election cycles demands agile production planning; nonetheless, cumulative uptake advances global decarbonization targets and reinforces energy-savings messaging.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile raw-material (steel & plastics) prices | -1.4% | Global, highest impact in manufacturing hubs | Short term (≤ 2 years) |

| Grid-electricity shortages in emerging nations | -0.8% | MEA, South Asia, select Latin American markets | Medium term (2-4 years) |

| Low penetration of after-sales service networks | -0.7% | Rural Asia, Sub-Saharan Africa | Medium term (2–4 years) |

| Rising import tariffs and trade barriers | -1.0% | North America, EU, ASEAN | Short to medium term |

| Source: Mordor Intelligence | |||

Volatile Raw-Material Prices

Steel and plastic account for roughly half of manufacturing cost, so the 18.8% hike that pushed average washing-machine prices from USD 800 to USD 950 between 2024 and 2025 reduced gross margins until hedging strategies caught up. Producers respond by forward-buying, dual-sourcing, and redesigning chassis to use less metal without sacrificing durability. Hurricane disruptions to high-purity quartz supply chains highlight vulnerabilities that inflate semiconductor prices, raising BOM costs for smart models that integrate multiple chips. While vertical integration shields some risk, inventory buffers strain working capital and threaten profitability in weaker demand cycles. Continuous cost pressure also hastens adoption of recyclable plastics and alternative alloys that balance sustainability goals with economic imperatives.

Grid-Electricity Shortages in Emerging Nations

Intermittent power constrains dryer uptake and dampens washing-machine usage frequency, limiting revenue per household in affected regions. Transformer shortages prolong infrastructure build-outs, with U.S. lead times extending to five years, signaling parallel challenges in markets with thinner capital bases [4]U.S. DOE, “New York First to Launch In-Store Home Energy Rebates,” energy.gov.. Commercial laundromats incur extra capital for generators and UPS systems to maintain service continuity, eroding ROI. In South Africa, load-shedding schedules reshape operating hours and deter investment in large-capacity equipment. Solar-assisted washers and low-power inverter drives offer partial mitigation, yet high capex and limited financing availability hinder rapid diffusion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Combined Units Drive Innovation

Combined washer-dryers accounted for a modest slice of 2025 volume yet are expanding at a 10.18% CAGR through 2031, reflecting consumer pursuit of space savings in compact urban dwellings that dominate new housing stock across Asia-Pacific and Europe. The laundry appliances market size for combination units benefits from premium price positioning and accessory revenue such as stacking kits and smart-detergent dispensers. Stand-alone washers retain 62.70% share thanks to established brand loyalty and price competitiveness, but their growth matures as saturation rises in developed economies. Advanced combo models like Samsung’s Bespoke AI Laundry Vented Combo wash and dry a full load in 68 minutes, leveraging heat-pump technology to trim energy use by 75%. Brand rivalry between LG and Samsung intensifies around cycle speed and AI-driven fabric care, signaling sustained innovation pace that bolsters replacement demand. Stand-alone dryers lag where outdoor line-drying traditions prevail, though policy shifts favoring energy-efficient dryers gradually expand their addressable base.

By Loading Type: Front-Load Technology Expansion

Front-load washers captured 56.85% of 2025 shipments and exhibit a superior 8.98% CAGR, supported by regulatory promotion of water and energy savings. These units use 40% less water per cycle versus top-load models, aligning with municipal conservation targets in drought-prone regions. The laundry appliances market share for top-load models remains sizeable at 43.15% amid North American consumer preference for ergonomic loading and faster cycles. Appliance makers counterbalance by adopting AI Wash routines, self-clean basins, and vibration-damping tech that narrow performance gaps. Hybrid vertical-axis designs featuring impeller plates rather than agitator posts illustrate incremental evolution rather than outright displacement, preserving brand equity among traditionalist buyers. Front-load premiumization opens ancillary revenue for pedestal storage bases and smart dosing accessories that elevate ticket value.

By Capacity: Large-Capacity Segment Acceleration

Models in the 6-8 kg sweet spot represented 46.90% of 2025 shipments, mirroring average household needs worldwide. However, above-8 kg machines are set to outpace at 9.65% CAGR through 2031 as multi-generational living, short-term rental turnovers, and commercial sites prioritize batch processing. Energy-per-kilogram efficiencies improve at larger drum volumes, reinforcing adoption in markets where electricity tariffs continue to rise. The laundry appliances market size for sub-6 kg machines remains niche, catering to urban studios and student housing where footprint trumps capacity. Innovations such as Miele’s InfinityCare honeycomb drum remove traditional ribs, reducing mechanical stress and enabling upsizing without fabric damage. Commercial investors gravitate to 20-30 kg models that shave labor cost per pound of wash, optimizing throughput in high-traffic laundromats.

By Usage: Commercial Segment Momentum

Residential buyers still deliver 76.10% of 2025 revenue, but commercial laundries posting 9.94% CAGR represent a lucrative growth engine. Coin and card laundromats broaden service menus with wash-and-fold, subscription lockers, and textile-rental tie-ins that raise machine utilization rates. The laundry appliances market size linked to commercial channels benefits from shorter five- to seven-year replacement cycles and higher ASPs due to ruggedized build specs. IoT telemetry lowers downtime and feeds predictive algorithms that bundle maintenance contracts into equipment leases, reinforcing manufacturer recurring income. Co-living operators treat laundry amenities as differentiators, integrating digital booking and loyalty integrations that underpin occupancy rates.

By Distribution Channel: Direct Sales Growth

Traditional B2C retail preserved 70.60% share in 2025, yet direct B2B sales log a healthy 8.11% CAGR as brands chase higher margins and unfiltered customer insight. Appliance-specific e-tail exceeds 29% penetration of home-improvement spend, letting consumers compare lifecycle costs and energy ratings in granular fashion. The laundry appliances market expands through virtual showrooms and augmented-reality product visualizers that reduce the need for brick-and-mortar floor space. Manufacturers embed trade-in and financing bundles that accelerate upgrade cycles, especially for smart models requiring connected-home integration consults. Service excellence, including white-glove delivery and installation, becomes a core part of the direct-to-consumer value proposition, reinforcing brand stickiness and post-purchase upsell paths.

Geography Analysis

Asia-Pacific retained 42.95% global share in 2025 as China produced 79.958 million washers, a 16.4% year-on-year surge that cements the region as both a manufacturing super-cluster and consumption juggernaut. India forecasts an 11% CAGR across the broader consumer-durables basket through FY29, supported by government import-duty relief on energy-efficient appliances. The laundry appliances market size in these two economies benefits from urbanization, rising middle-income cohorts, and female labor-force participation that values time-saving devices. Europe, accounting for a 24.30% share, skews toward premium models as the July 2025 ecodesign dryer mandate eradicates inefficient SKUs and catalyzes replacement demand. Consolidation, such as the Whirlpool-Arçelik merger forming Beko Europe, evidences strategic scaling to meet regulatory complexity and product-mix shifts. North America’s replacement-driven market remains resilient, buoyed by smart-appliance adoption and robust home-improvement activity; Home Depot’s record Q4 2024 appliance sales underscore these dynamics. The Middle East & Africa segment, though currently small, posts the fastest 6.32% CAGR, spurred by urban infrastructure investment and rising electrification. Haier’s acquisition of Electrolux’s South Africa water-heater business signals confidence in African expansion, mirroring its double-digit revenue gains across MEA for three consecutive years. South America sees moderate but volatile growth amid currency swings, yet megacity redevelopment keeps baseline demand intact.

Regulatory Landscape

Energy- and water-efficiency regulation is tightening across major markets, affecting product design (inverter motors, heat-pump drying, connected energy modes) and compliance roadmaps. In the United States, the Department of Energy moved to amend energy conservation standards for residential clothes washers in 2024, establishing an updated pathway with a future compliance date (March 2028) that supports multi-year platform redesign and certification planning.

In Europe, ecodesign and energy-labelling requirements for household washing machines and washer-dryers remain anchored to Regulation (EU) 2019/2023. Harmonised standards management was updated in January 2025 through an amendment to Implementing Decision (EU) 2021/936, and the EU adopted the Ecodesign for Sustainable Products Regulation (ESPR) in June 2024 as an umbrella framework for broader ecodesign requirements. A formal review milestone for Regulation (EU) 2019/2023, along with the related energy labelling framework, sits in late 2025, keeping compliance specifications and test standards under active revision.

Value Chain Analysis

Laundry appliances value creation starts with upstream metals and petrochemicals (steel, resins), electronics (controllers, sensors, connectivity modules), and motors and compressors (inverter drives, heat-pump components). It then moves through fabrication and assembly (cabinets, drums, pumps, wiring harnesses, PCB assembly), followed by testing and packaging, and finally multi-node distribution. Channel execution increasingly combines big-box retail and specialist dealers with direct-to-consumer and B2B/direct programs, while service logistics (installation, warranty, parts, and repairs) remain a differentiator given the growing installed base of connected and higher-complexity models.

Recent supply-chain actions point to localization and resilience as key themes. Whirlpool announced a USD 60 million investment (April 2026) to convert a Perrysburg, Ohio site into a production hub for washer and dryer components and subassemblies. It also disclosed a Brazil localization program (May 2026) to raise domestic sourcing for front-load washing machines at Rio Claro, targeting tariff exposure and freight volatility while shortening lead times. On the manufacturing-partnership side, Electrolux Group announced a strategic partnership with Midea Group for Fabric Care production in North America, with operations scheduled to commence in Q3 2026. Separately, it confirmed plans to convert its Anderson County, South Carolina plant for laundry production (restart targeted for 1H 2027), showing how OEMs are reshaping footprints to manage component constraints, platform refresh cadence, and regional demand.

Competitive Landscape

The global laundry appliances market in 2024 was moderately concentrated, with the top companies accounting for a significant share of the total market. Whirlpool remained a key player, reinforcing its presence in the Americas and India following the sale of its European business to Arçelik, which led to the formation of Beko Europe with a production capacity of 24 million units.

Haier Smart Home and LG Electronics also held strong positions, capitalizing on the introduction of AI-enabled features to attract increasingly tech-oriented consumers. Bosch’s exploration of a possible Whirlpool acquisition underscores ongoing realignment aimed at bolstering North American scale. Chinese manufacturers such as Midea exploit cost leadership and aggressive overseas channel build-out to nibble at incumbents’ shares.

Competitive differentiation pivots on AI-enabled washing algorithms, energy-efficiency breakthroughs, and open-standard connectivity such as Matter 1.3 that facilitate cross-brand interoperability. White-space opportunities persist in commercial-laundry management software, subscription-based detergent delivery, and retrofit IoT modules for legacy machines, inviting entrants from adjacent tech domains.

Laundry Appliances Industry Leaders

Whirlpool Corporation

Haier Smart Home Co. Ltd. (incl. GE Appliances)

LG Electronics Inc.

Samsung Electronics Co. Ltd.

AB Electrolux

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Policy-led efficiency upgrades and electrification-oriented product shifts create clear whitespace in premium and mid-tier platforms that can meet tighter test requirements while lowering real-world utility costs. In the U.K., the Ecodesign for Energy-Related Products and Energy Information (Household Tumble Dryers) Regulations 2026 introduce specific requirements applying from April 10, 2026. This reinforces heat-pump and high-efficiency dryer commercialization pathways and aligns with the report’s focus on energy mandates as a purchase driver.

On the supply side, manufacturers are committing capital and updating product roadmaps that expand the opportunity set for combination units and connected energy management. Samsung launched its 2026 Bespoke AI Laundry Combo (May 2026), signaling continued innovation in sensors and automated wash-and-dry optimization for space-constrained households and convenience-led upgrades. North American capacity localization is also becoming a competitive lever: GE Appliances announced a USD 490 million laundry plant investment in Louisville, Kentucky (June 2025) to expand washer production and support newer laundry lines, while Whirlpool announced a USD 60 million Ohio components investment (April 2026) to strengthen domestic subassembly supply. Collectively, these moves support faster platform refresh cycles, improved availability for higher-efficiency SKUs, and higher-value bundling tied to broader home energy management.

Recent Industry Developments

- July 2026: Samsung announced a global rollout of its Bespoke AI Washer and Dryer lineup with SmartThings connectivity and AI-driven fabric care features. The release underscores the shift toward connected, energy-management-oriented laundry platforms, raising the bar for software-enabled differentiation and ecosystem integration across competing brands.

- June 2025: GE Appliances announced a USD 490 million investment at its global headquarters in Louisville, Kentucky to expand laundry appliance production capacity, including support for combo and front-load lines. The commitment strengthens regional manufacturing depth and provides a clearer supply base for feature-rich, higher-efficiency models in a replacement-driven market.

- September 2024: Whirlpool brand launched the FreshFlow vent system on select smart front-load washers, using fan-powered airflow and antimicrobial components to address moisture and odor concerns. The feature-led upgrade targets a common consumer pain point and supports premiumization through hygiene and maintenance-related value propositions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the laundry appliances market is defined as the sales value of household laundry equipment, including washing machines, dryers, electric smoothing irons, and closely related laundry products, tracked across major regions and common retail channels.

Scope exclusions: Excludes spare parts, repair services, extended warranties, and rental or lease revenue that is not part of new-appliance sales.

Segmentation Overview

- By Product Type

- Stand-alone Washing Machines

- Stand-alone Drying Machines/Dryers

- Combined Washer-Dryers

- By Loading Type

- Front-Load

- Top-Load

- By Capacity

- Below 6 Kg

- 6 - 8 Kg

- Above 8 Kg

- By Usage

- Residential

- Commercial (laundromats, hospitals, hotels, hostels, etc.)

- By Distribution Channel

- B2B / Direct from Manufacturers

- B2C / Retail Consumers

- By Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines)

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the outer boundaries of demand and to avoid building the model on assumptions that do not match real world appliance flows. We mainly used public statistics and technical references to understand how many households can buy appliances, how often replacement happens, and what rules shape efficiency and product design.

Sources reviewed included national statistics offices and the UN and World Bank for population, household formation, and income indicators, UN Comtrade and national customs portals for import and export direction, IEA and energy-labeling regulators for efficiency standards and adoption signals, and patent and peer-reviewed engineering journals for technology shifts. We also screened company annual reports, investor decks, and credible press for price positioning and channel mix signals, and then cross-checked a subset of financial and patent details through a paid subscription database used for company intelligence and patent lookups. These desk sources are illustrative, and many other public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test model inputs that are hard to observe in public data, especially price ladders, channel sell-through, and the split between automatic and semi-automatic units in different regions. Interviews and short surveys were completed with a mix of manufacturing, distribution, and retail stakeholders, then repeated with independent experts to confirm the final demand signals across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 12% | APAC: 39% |

| Mid tier: 56% | Functional/Unit leaders: 43% | EMEA: 36% |

| Smaller Players: 18% | Managers: 45% | Americas: 25% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where the demand pool is reconstructed using household base, urbanization, appliance ownership, and replacement cycles, and then filtered by region-specific penetration for washers and dryers. Once the demand pool is formed, value is derived using average selling price bands that reflect mix shifts between automatic and semi-automatic units, capacity preferences (for example, common mid-capacity washer demand), and channel margins.

To keep outputs realistic, we use selective bottom-up checks as guardrails, such as rolling up a sample of supplier and retailer disclosures, comparing implied unit volumes with trade flows, and validating price ladders through channel checks. Key inputs used in the model include household growth, replacement rate, electrification and grid reliability signals, energy and water efficiency regulation intensity, and the online versus offline channel mix, which then feed the forecast engine.

For forecasting, we used a scenario-based approach supported by multivariate regression where demand is linked to household formation, income growth, and urbanization, and then adjusted by expert views on efficiency-driven replacement and smart feature adoption. When data gaps exist for smaller markets, ratios from comparable countries are applied first and then corrected through primary feedback so we avoid over-extending a single regional pattern.

Data Validation & Update Cycle

Validation is done in layers so that one data source does not dictate the final number. Model outputs are compared against independent signals like appliance trade direction, household appliance ownership proxies, and reported channel conditions, and then obvious outliers are reviewed until a reasonable explanation is found.

Before sign-off, the work is reviewed internally with a second analyst pass that checks formulas, currency conversions, and year alignment across all tables. If a variance looks material, respondents are re-contacted and assumptions are updated, and then the market totals are recalculated. Reports are refreshed annually, and interim updates are made when major events change demand, pricing, or regulations, followed by a final freshness check right before delivery.

Mordor Intelligence's Global Laundry Appliances Market Market Estimate Compared With Other Published Estimates

It is normal to see different market values for laundry appliances because publishers do not always count the same product set, the same selling stages, or the same year alignment. Differences also come from how average selling prices are built and whether local currency conversions are held constant or refreshed.

By tracking channel mix, validating ASP bands through interviews, and refreshing currency timing, Mordor Intelligence keeps the total tied to new-appliance sales for washers, dryers, electric smoothing irons, and related products, instead of folding in services or broad laundry-adjacent categories.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 41.43 B (2026) | |

| Industry Publisher A | USD 54.80 B (2024) | Uses a broader base-year construct and a longer-range forecast setup, and the scope language is less specific on which laundry-adjacent items are excluded, which can widen the counted revenue pool. |

| Consultancy B | USD 61.00 B (2024) | Quotes a rounded total for home laundry appliances without a clear product list or pricing build, so washers, dryers, and bundled features may be valued with higher blended ASP assumptions. |

The spread in the table mainly comes down to scope clarity and the way prices and year timing are handled. When scope boundaries and price ladders are stated clearly and then checked with channel feedback, the resulting market size becomes easier to reproduce and to carry into segment and regional planning.

Key Questions Answered in the Report

How large was the laundry appliance market in 2026 and what is its expected size by 2031?

It stood at USD 41.43 billion in 2026 and is forecast to reach USD 60.58 billion by 2031, reflecting a 7.88% CAGR.

Which product category is growing fastest within laundry appliances?

Combined washer-dryers are expanding at a 10.18% CAGR as urban consumers seek space-saving solutions.

Why are front-load washers gaining share against top-load models?

Front-loaders use 40% less water and meet stricter efficiency rules, pushing their share to 56.85% in 2025.

What drives commercial laundry-equipment demand?

The rise of co-living spaces and laundromat modernization is pushing commercial equipment to a 9.94% CAGR.

Which region dominates global sales?

Asia-Pacific leads with 42.95% revenue share thanks to robust production in China and rapid adoption in India.

How concentrated is competition among manufacturers?

The top five companies hold 77% of revenue, placing the sector in a moderately concentrated range.

Page last updated on: