Market Overview

| Study Period | 2019 - 2030 |

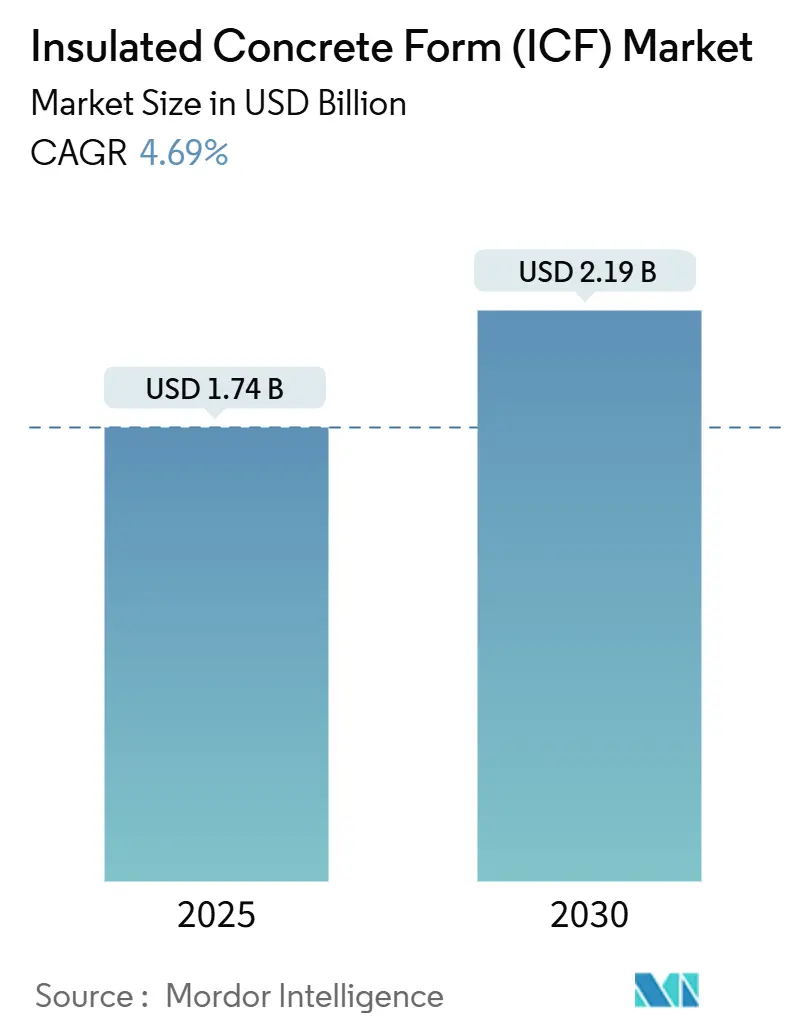

| Market Size (2025) | USD 1.74 Billion |

| Market Size (2030) | USD 2.19 Billion |

| Growth Rate (2025 - 2030) | 4.69% CAGR |

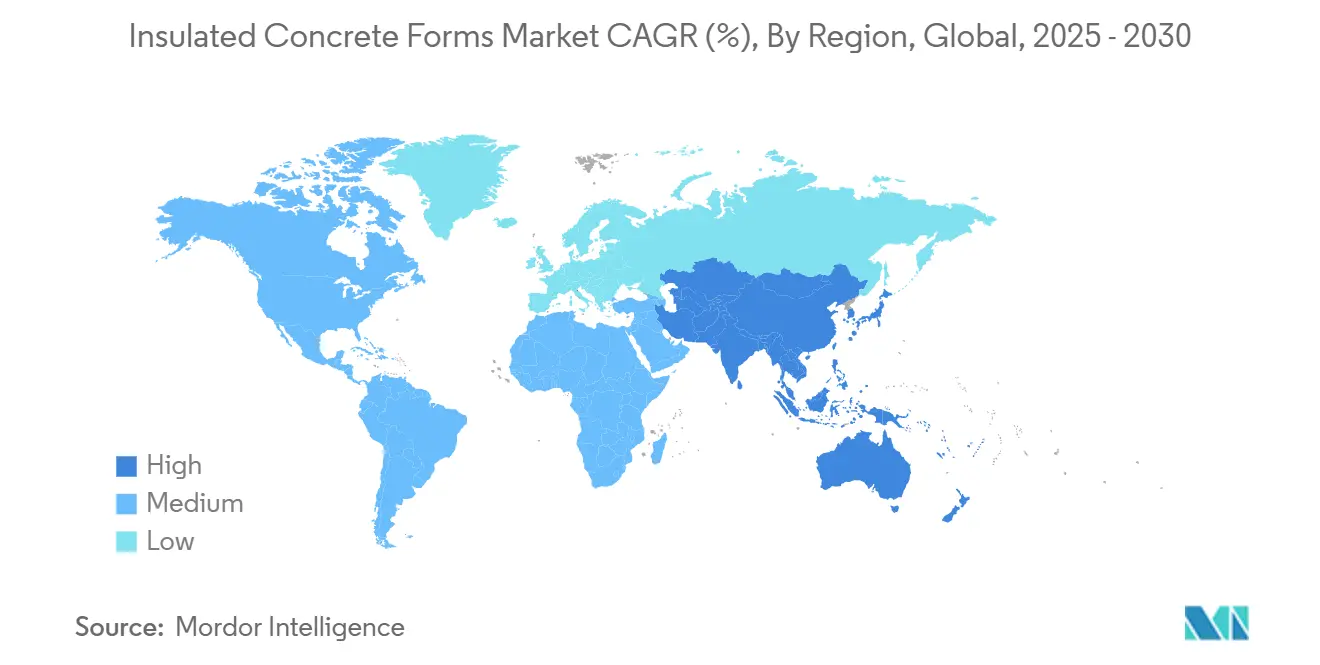

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Insulated Concrete Form (ICF) Market Analysis by Mordor Intelligence

The insulated concrete forms market is valued at USD 1.74 billion in 2025 and is forecast to reach USD 2.19 billion by 2030, advancing at a 4.69% CAGR. The steady expansion reflects the construction sector’s pivot toward energy-efficient building envelopes that satisfy tightening codes while lowering lifetime operating costs. Strong policy support, rising energy prices, and heightened awareness of climate resilience are amplifying adoption, especially where hurricanes, wildfires, or temperature extremes put conventional walls at risk. Residential projects still account for most placements, yet commercial developers and public agencies are scaling up orders to meet net-zero and acoustic targets. North America remains the largest regional buyer, but Asia-Pacific is logging the fastest percentage gains as China and India embed higher insulation levels in national building laws.

Key Report Takeaways

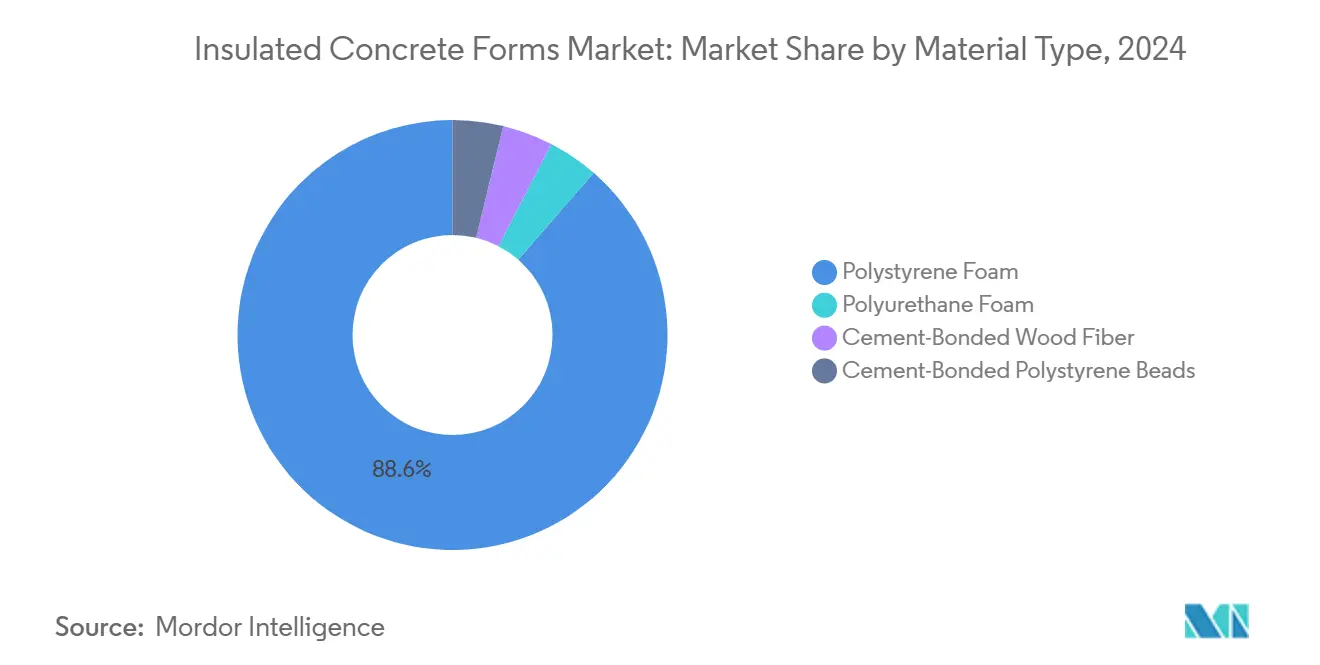

- By material type, polystyrene foam commanded 88.60% of the insulated concrete forms market share in 2024 and is growing at 4.72% through 2030.

- By system type, flat-wall products held 54.17% revenue share in 2024, whereas screen-grid products are projected to expand at a 5.32% CAGR through 2030.

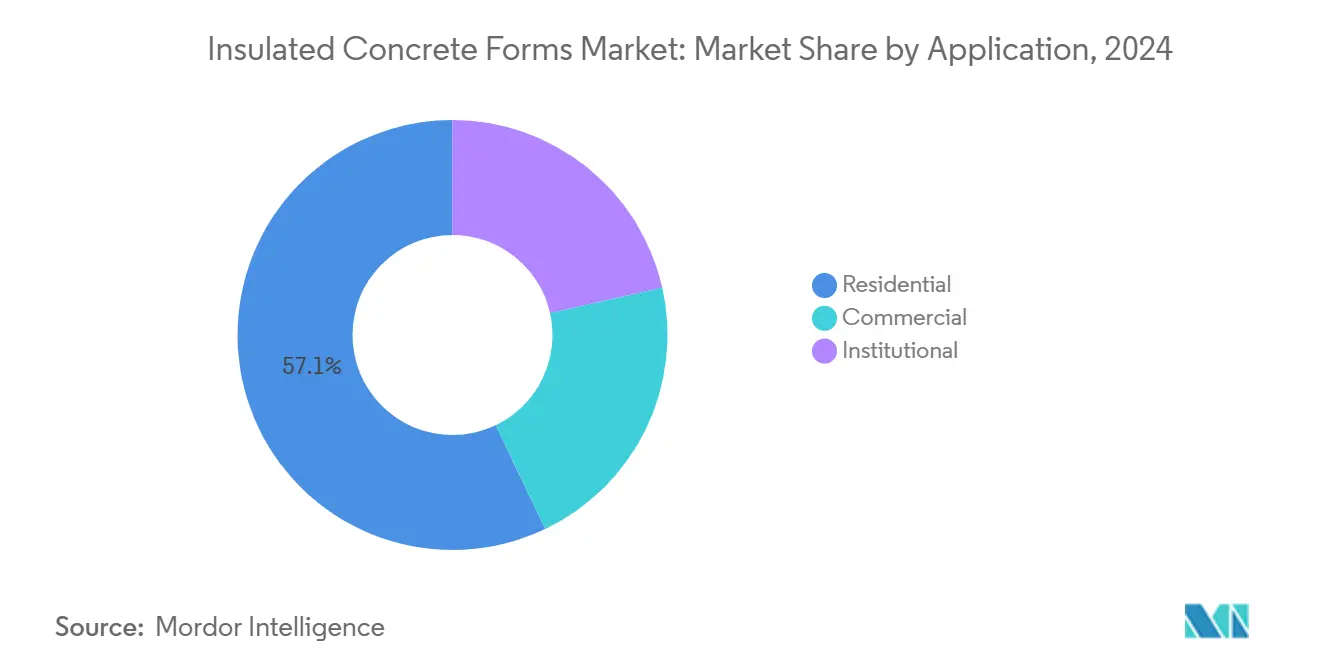

- By application, residential projects captured 57.10% of the insulated concrete forms market size in 2024, while commercial projects are set to grow 4.49% annually to 2030.

- By construction type, new builds contributed 78.21% of 2024 revenues, yet retrofits will climb at a 5.51% CAGR through 2030.

- By geography, North America led with a 39.50% revenue share in 2024; Asia-Pacific is forecast to grow 5.03% annually to 2030.

Global Insulated Concrete Form (ICF) Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Energy-efficient High-rise Buildings | +1.2% | Global, with concentration in North America and EU | Medium term (2-4 years) |

| Increased Adoption of Innovative Construction Procedures | +0.9% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| Stricter Green-building Codes and Incentives | +1.1% | Global, led by developed markets | Short term (≤ 2 years) |

| Growing Demand for Acoustic Insulation in Dense Urban Infill | +0.7% | Global urban centers, particularly APAC | Medium term (2-4 years) |

| Rising Awareness of Sustainable Construction Materials | +0.6% | Global | Long term (≥ 4 years) |

Source: Mordor Intelligence

Rising Demand for Energy-Efficient High-rise Buildings

The 2024 International Energy Conservation Code now mandates exterior continuous insulation in Climate Zones 4 and 5, positioning insulated concrete forms as a compliance solution for multi-story projects. Developers can satisfy code rules and cut thermal bridging within a single step because the concrete core is wrapped by insulation. Higher utility prices further increase the payback value, encouraging owners to select walls that lock in performance for decades. Jurisdictions adopting the code are clustered in metropolitan areas where high-rise construction dominates land-use planning, so demand is likely to intensify.

Increased Adoption of Innovative Construction Procedures

A persistent skilled-labor shortfall is prompting contractors to choose methods that reduce reliance on traditional framing crews. Crews assembling insulated concrete forms report up to 30% schedule savings thanks to simplified stacking and reduced call-backs. The block-like modules lend themselves to prefabrication and repeatable workflows, allowing firms to enlarge their labor pool without sacrificing quality. As the workforce ages and recruitment remains challenging, simplified installation strengthens long-term appeal.

Stricter Green-building Codes and Incentives

US federal legislation, such as the Inflation Reduction Act, has unlocked generous rebates for energy-efficient envelope upgrades, narrowing the cost gap with framed alternatives. Several states have layered on tax credits that reward designs exceeding minimum code levels, which makes insulated concrete forms cost-competitive while delivering superior strength and fire resistance. Similar incentive structures are rolling out in the EU and parts of Asia, combining carbon-reduction, resilience, and energy-savings goals into one push.

Growing Demand for Acoustic Insulation in Dense Urban Infill

Municipal noise ordinances increasingly call for wall assemblies with STC ratings above 50, a threshold easily met by insulated concrete forms that embed dense concrete between dual foam layers. Mixed-use infill projects in congested downtowns benefit because tenants gain quiet interiors without thicker walls that steal rentable floor area. As urban land values rise and buildings stack multiple functions, superior sound control alongside energy performance gives insulated concrete forms a compound advantage.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost versus wood framing | -0.8% | Global, particularly price-sensitive markets | Short term (≤ 2 years) |

| Limited contractor familiarity and skilled labor gap | -0.6% | Global, with regional variations | Medium term (2-4 years) |

| Regulations for VOC Emission | -0.4% | Global, with stricter enforcement in developed markets | Long term (≥ 4 years) |

Source: Mordor Intelligence

High Upfront Cost Versus Wood Framing

Even after lumber price spikes, builders face a 3-8% premium when choosing insulated concrete forms, and smaller firms must rent concrete pumps and pay for structural engineering reviews[1]Iowa Concrete Paving Association, “Cost Comparison of ICF and Wood Framing,” iowaconcretepaving.org. These expenses deter budget-constrained projects despite lower lifetime utility bills. Incentive programs and rising energy tariffs are gradually offsetting the difference, but first-cost sensitivity remains a hurdle.

Limited Contractor Familiarity and Skilled Labor Gap

Builders new to insulated concrete forms often inflate bids to cover perceived schedule risks, which discourages owners from experimenting with the technology. Manufacturers and associations are expanding certification workshops, yet adoption climbs only as fast as training scales. Regions with few reference projects, therefore, move more slowly, perpetuating a cycle of low familiarity.

Segment Analysis

By Material Type: Polystyrene Foam Maintains Dominance

Polystyrene blocks controlled 88.60% of the insulated concrete forms market share in 2024, and the segment is forecast to expand at 4.72% annually to 2030. This command rests on EPS panels that deliver R-22 to R-26 while resisting moisture during concrete placement. Flame-retardant additives help meet code, and recycling programs appeal to municipalities pursuing circular-economy goals.

Polyurethane, cement-bonded wood fiber, and bead-enhanced mixes occupy specialist niches. Polyurethane delivers higher R-values per inch for tight sites, whereas cement, wood fiber blocks satisfy regional code or sourcing preferences. Bio-based polyiso containing 5% bio-circular feedstock debuted in 2024 and signals an emerging green-chemistry direction. As mandates on embodied carbon tighten, alternative foams could gain share, yet polystyrene’s scaling advantages support its leadership.

Note: Segment shares of all individual segments available upon report purchase

By System Type: Screen-grid Systems Drive Innovation

Flat-wall assemblies captured 54.17% of 2024 revenues, confirming their position as the default choice for general contractors. The insulated concrete forms market size for flat-wall solutions is projected to rise steadily, but screen-grid products, growing at 5.32% CAGR, offer compelling economics by trimming concrete volumes without sacrificing load capacity. Contractors appreciate lighter lifts, faster pours, and fewer blow-out risks when stacking hollow-web grids.

Waffle-grid panels serve high-insulation jobs that demand thicker foam, while post-and-beam formats remain popular with architects who want exposed concrete ribs. Connection hardware, utility chases, and alignment bracing continue to evolve, signaling a competitive push toward ease-of-use. As engineering confidence broadens, design teams may specify hybrid grids that merge performance and aesthetic flexibility.

By Construction Type: The Retrofit Market Emerges as a Growth Engine

New builds still account for 78.21% of insulated concrete forms market revenues because walls are simplest to stack on fresh foundations. The insulated concrete forms market size in retrofits, however, will advance 5.51% a year through 2030 as owners pursue deep-energy renovations. Funding under the Inflation Reduction Act helps offset demolition and envelope replacement costs.

Historically, integrating forms within existing frames posed structural and plumbing hurdles. New half-height blocks and tie-in connectors now streamline interior or exterior over-cladding, trimming downtime for occupied buildings. Public housing upgrades, school over-clads, and mixed-use repositions in cold climates illustrate the approach. As cities race toward net-zero stock, retrofit activity could rival new placements in volume.

By Application: Commercial Sector Accelerates Adoption

Residential projects held 57.10% of 2024 sales, making single-family custom builds the largest slice of the insulated concrete forms market. Yet clinics, schools, and hospitality chains now see 4.49% annual growth because energy and acoustic benefits directly reduce operating budgets. Developers also leverage the system’s two-hour fire rating to simplify code compliance.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America generated 39.50% of global revenue in 2024, underpinned by model energy codes that reference insulated concrete forms and a dense network of certified installers. US federal infrastructure funding emphasizes resilient construction that withstands extreme wind and wildfire, benefits that the system delivers without extra layers.

Asia-Pacific is the fastest climber, expected to post a 5.03% CAGR to 2030. India’s Energy Conservation Building Code, targeting 25-50% energy savings, positions forms as a ready path for developers unfamiliar with curtain-wall detailing[2]Bureau of Energy Efficiency, “Energy Conservation Building Code 2024,” beeindia.gov.in.

Europe enforces some of the strictest carbon and energy benchmarks, yet masonry traditions slow adoption. In South America and the Middle East, rising electricity tariffs and urban densification open potential, but limited contractor familiarity and competing low-cost methods keep penetration modest for now.

Competitive Landscape

The insulated concrete forms market remains moderately fragmented. Airlite Plastics Company & Fox Blocks (Fox Blocks), BASF, and BuildBlock Building Systems LLC anchor the global field with multi-plant capacities, while regional firms focus on localized support and climate-specific product tweaks. Leaders invest in field-training academies and digital design libraries to cut learning curves. Technical service rather than price often tips the scales when architects evaluate wall systems.

Insulated Concrete Form (ICF) Industry Leaders

-

Airlite Plastics Company & Fox Blocks (Fox Blocks)

-

BASF

-

Amvic Ireland LTD

-

Tremco CPG Inc.

-

BuildBlock Building Systems LLC

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- August 2024: Carlisle Construction Materials launched bio-based Polyiso Eco rigid foam insulation containing 5% bio-circular content, developed in partnership with Covestro and Stepan.

- May 2024: Fox Blocks released guidance on rebuilding with insulated concrete form walls after wildfire devastation, citing resistance to 1,093 °C exposures for four hours.

Global Insulated Concrete Form (ICF) Market Report Scope

Insulated concrete forms are structures that are used for holding freshly made concrete to provide insulation to the structure they enclose.

The insulated concrete form market is segmented by Material Type (Polystyrene Foam, Polyurethane Foam, Cement-bonded Wood Fiber, Cement-bonded Polystyrene Beads), Application (Residential, Commercial, Institutional), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The report also covers the market sizes and forecasts for the insulated concrete form (ICF) market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done in terms of revenue in USD million.

| Material Type | Polystyrene Foam | ||

| Polyurethane Foam | |||

| Cement-Bonded Wood Fiber | |||

| Cement-Bonded Polystyrene Beads | |||

| System Type | Flat-Wall Systems | ||

| Waffle-Grid Systems | |||

| Screen-Grid Systems | |||

| Post-and-Beam Systems | |||

| Construction Type | New-build | ||

| Retrofit / Remodelling | |||

| Application | Residential | ||

| Commercial | |||

| Institutional | |||

| Geography | Asia-Pacific | China | |

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN Countries | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle-East and Africa | Saudi Arabia | ||

| South Africa | |||

| Rest of Middle-East and Africa | |||

Material Type

| Polystyrene Foam |

| Polyurethane Foam |

| Cement-Bonded Wood Fiber |

| Cement-Bonded Polystyrene Beads |

System Type

| Flat-Wall Systems |

| Waffle-Grid Systems |

| Screen-Grid Systems |

| Post-and-Beam Systems |

Construction Type

| New-build |

| Retrofit / Remodelling |

Application

| Residential |

| Commercial |

| Institutional |

Geography

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the insulated concrete forms market?

The insulated concrete forms market stands at USD 1.74 billion in 2025 and is forecast to reach USD 2.19 billion by 2030.

Which material type leads global demand?

Polystyrene foam blocks hold 88.60% of 2024 revenue, reflecting their balance of cost and performance.

Which region is growing fastest for insulated concrete forms adoption?

Asia-Pacific is projected to expand at a 5.03% CAGR through 2030 on the back of green-building mandates in China and India.

How do insulated concrete forms help meet green-building codes?

They embed continuous insulation that eliminates thermal bridging, allowing projects to exceed IECC and other national efficiency standards without extra layers.

Are insulated concrete forms costlier than wood framing?

Upfront costs are 3-8% higher, but energy savings and resilience advantages often yield favorable lifecycle economics when incentives or rising utility rates are considered.