Market Overview

| Study Period | 2021 - 2031 |

|---|---|

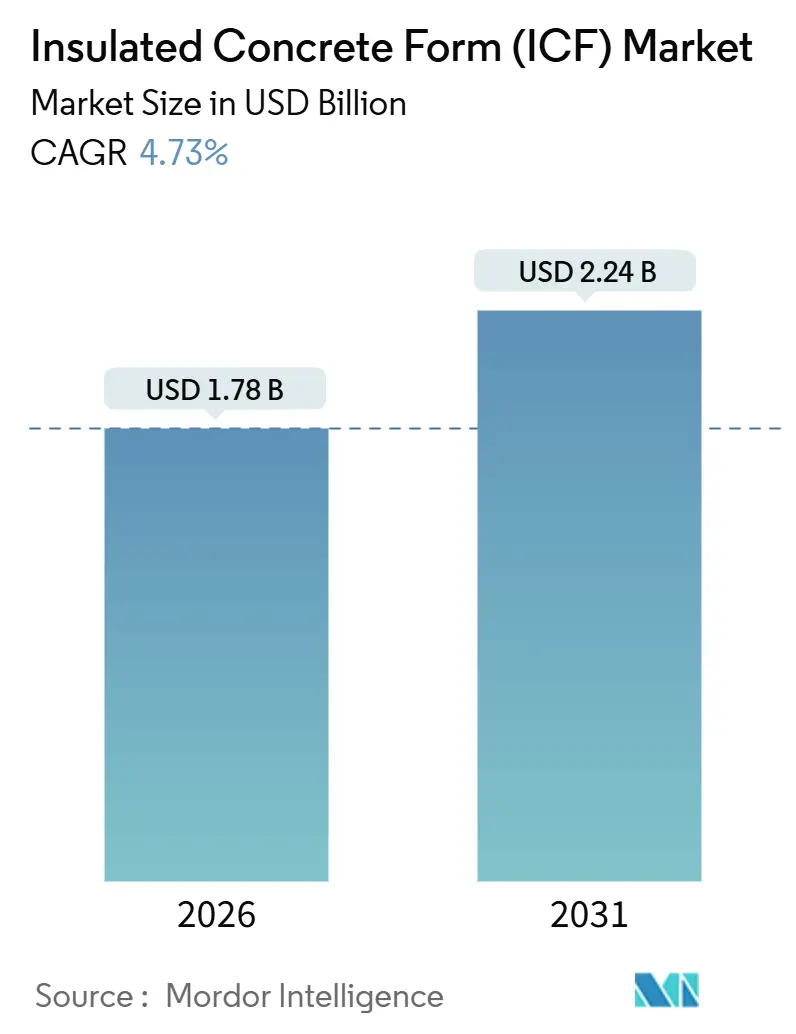

| Market Size (2026) | USD 1.78 Billion |

| Market Size (2031) | USD 2.24 Billion |

| Growth Rate (2026 - 2031) | 4.73% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Insulated Concrete Form (ICF) Market Analysis by Mordor Intelligence

The Insulated Concrete Form (ICF) Market size is estimated at USD 1.78 billion in 2026, and is expected to reach USD 2.24 billion by 2031, at a CAGR of 4.73% during the forecast period (2026-2031). Momentum is building as regulators tighten energy-code compliance, disaster-resilience incentives expand, and designers look for envelope assemblies that curb both operational and embodied carbon. Graphite-enhanced EPS cores now make it possible to raise R-values without increasing wall thickness, a shift that protects rentable floor area in urban projects. Developers are adopting screen-grid systems to streamline rebar placement on multi-story jobs where labor productivity dictates profitability. Meanwhile, styrene-price volatility and limited contractor familiarity temper near-term uptake, yet both headwinds are subsiding as backward-integrated EPS supply and installer-training programs scale. Vertical integration, evidenced by Holcim’s 2024 acquisition of OX Engineered Products, signals that cement majors view the insulated concrete form market as a strategic extension of their building-envelope portfolios.

Key Report Takeaways

- By material type, polystyrene foam accounted for 88.66% of the insulated concrete form market share in 2025 and is anticipated to grow with the fastest CAGR of 4.82 through 2031.

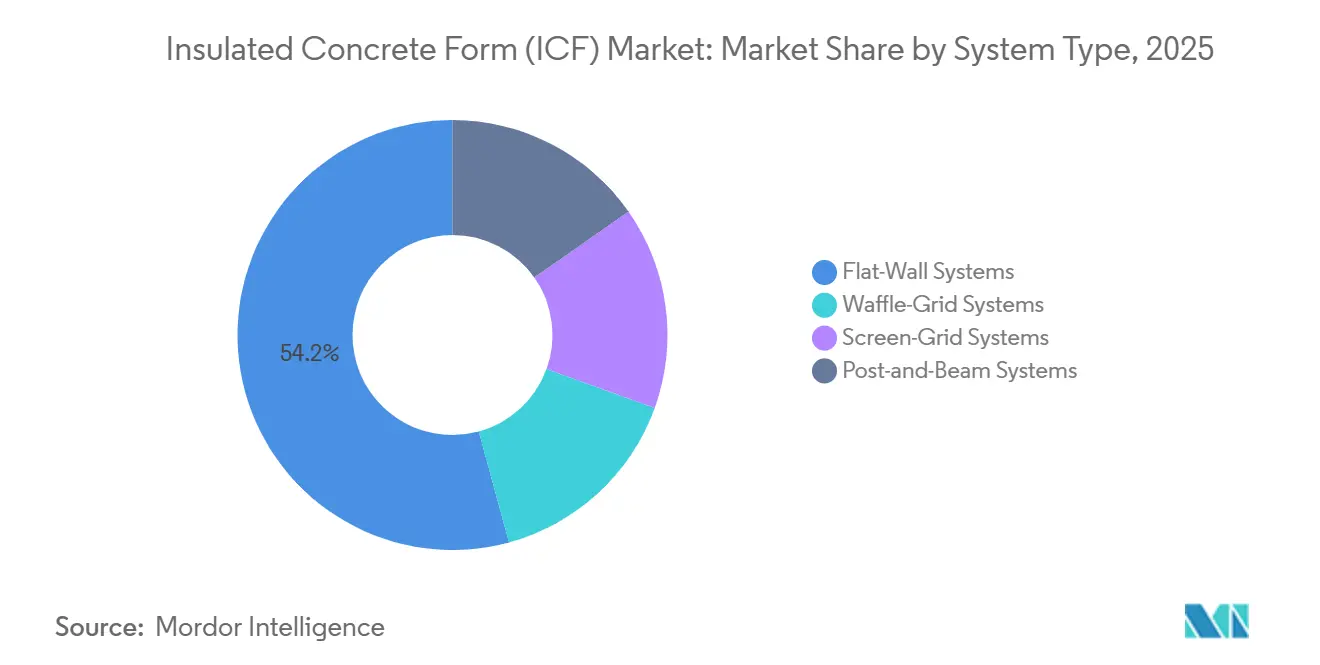

- By system type, flat-wall products accounted for 54.23% of the ICF market size in 2025, while screen-grid units are forecast to expand at a 5.33% CAGR through 2031, the fastest among all configurations.

- By construction type, new-build projects captured 78.34% of the insulated concrete form market size in 2025, while retrofit applications are advancing at a 5.58% CAGR to 2031.

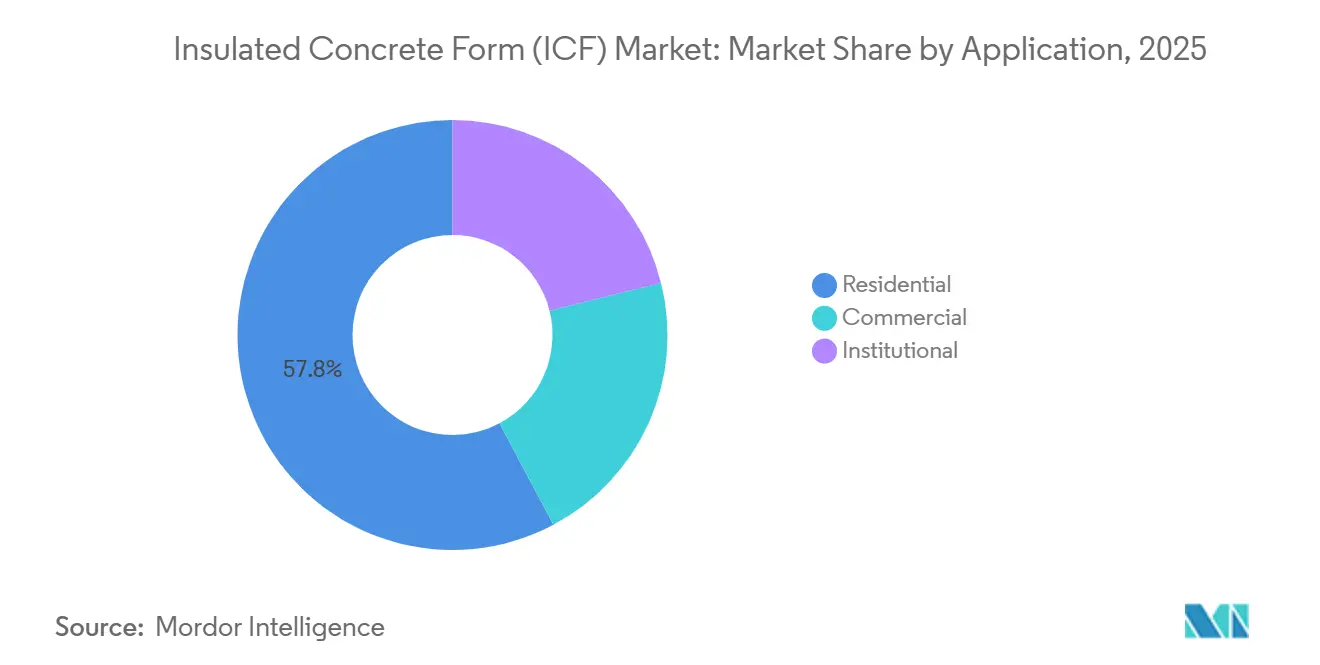

- By application, residential projects held a 57.78% share of the insulated concrete form market in 2025, and commercial projects are progressing at a 4.56% CAGR through 2031.

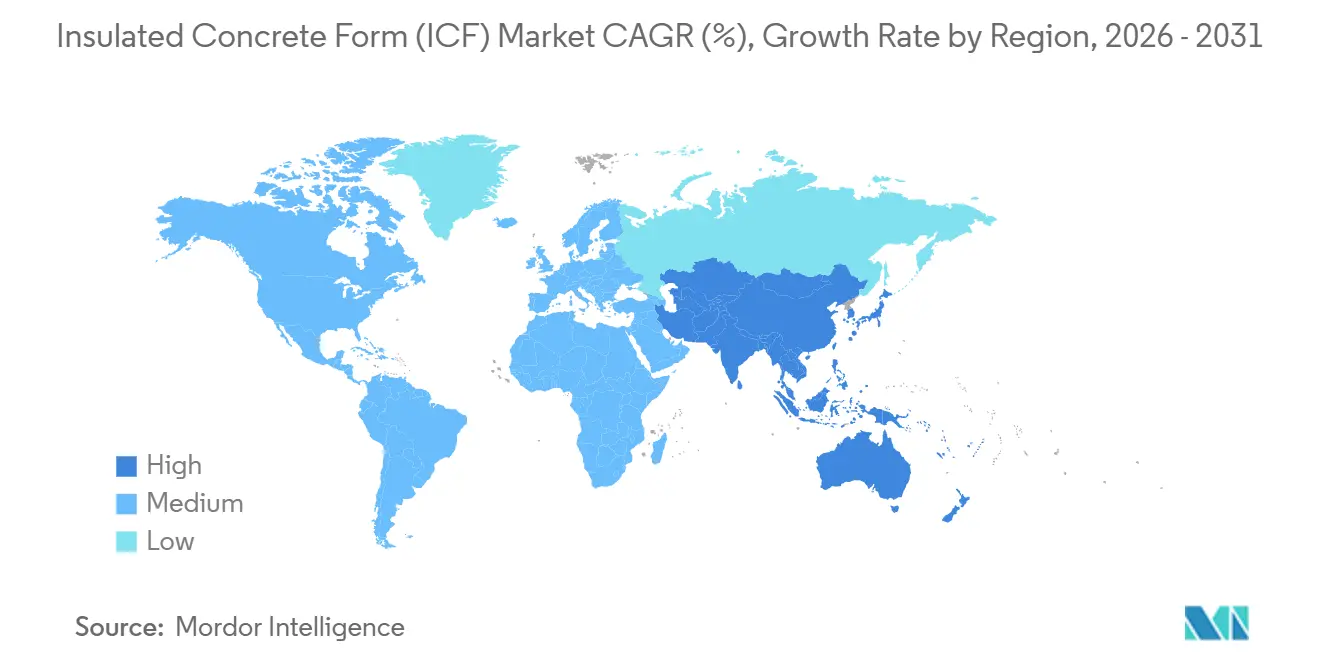

- By geography, North America dominated with 39.67% revenue share in 2025; Asia-Pacific is set to grow the quickest at a 5.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Insulated Concrete Form (ICF) Market*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter green-building codes and incentives | +1.2% | North America, Europe, China, India, Singapore | Medium term (2-4 years) |

| Rising demand for energy-efficient mid/high-rise buildings | +1.0% | Global, concentrated in North America, Europe, China, India | Long term (≥ 4 years) |

| Increased adoption of off-site and modular ICF systems | +0.8% | North America, Europe | Medium term (2-4 years) |

| Expansion of performance-linked green-finance programs | +0.6% | Europe, North America, Brazil, Middle East | Long term (≥ 4 years) |

| FEMA resilience grants favoring ICF construction | +0.9% | United States, Caribbean, Central America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stricter Green-Building Codes And Incentives

The 2024 International Energy Conservation Code lifted prescribed R-value targets for walls across climate zones 3-8, effectively demanding continuous insulation that wood frames struggle to achieve without added layers and labor[1]International Code Council, “2024 IECC,” iccsafe.org. The United Kingdom’s Future Homes Standard, effective in 2025, obliges new dwellings to cut operational carbon by up to 80% compared with 2013 baselines, steering architects toward high-thermal-mass envelopes[2]Government of the United Kingdom, “Future Homes Standard,” gov.uk. China’s 14th Five-Year Plan enforces ultra-low-energy targets for public buildings above 20,000 m², giving ICF an advantage where lifecycle cost analyses justify higher upfront spend. In India, the 2024 Energy Conservation Building Code introduced envelope-performance indices that penalize thermal bridging, a weakness absent from monolithic ICF walls. Finally, Saudi Arabia published 16 thermal-insulation regulations in 2024 that set performance gates for public procurement, establishing a compliance moat around certified ICF suppliers.

Rising Demand For Energy-Efficient Mid/High-Rise Buildings

Hotel chains, student housing developers, and institutional owners value ICF’s average STC rating of 55 over wood-frame’s 38, a difference that lowers tenant turnover and boosts net operating income. Schedule savings are material: the USD 20 million Divi Little Bay Resort in St. Maarten finished 60 days early by staying with ICF forms that combine structure and insulation. Panther Creek High School in Texas cut HVAC tonnage by 30% by leveraging ICF’s continuous R-values, releasing capital for classroom tech upgrades. ASTM C1363 testing shows a 6-inch-core ICF wall needs more than 320 hours to reach steady-state heat transfer at –31 °C, compared with 60 hours for an R-20 wood frame, a lag that trims peak-load charges in extreme climates. Energy rebate models now in 18 U.S. states replicate the performance incentives the Centre Park Holiday Inn secured when it beat ASHRAE standards by 30%.

Increased Adoption Of Off-Site And Modular ICF Systems

Factory-cut wall kits enable contractors to panelize 40-foot sections under cover, then crane them into place, as the Best Western in Georgia showed on a five-story build that even survived a tornado during erection. Logix reduced freight costs up to 40% by shipping knock-down forms flat, allowing distributors to hold deeper inventory in smaller warehouses. Quad-Lock’s 2025 Ultra panel supplies R-28 performance with 20% more compressive strength, letting architects reclaim floor area in high-value infill sites. The Lewis Building in Massachusetts used removable plywood One Series forms to leave exposed concrete on elevator shafts, eliminating finish trades and trimming an eight-week schedule slice. Modular ICF also eases curved façades and acute-angle corners where conventional shoring is labor-intensive, widening design flexibility on tight sites.

Expansion Of Performance-Linked Green-Finance Programs

The EU Taxonomy Regulation, fully operative since 2024, requires real-estate funds to disclose the share of assets meeting mitigation criteria, pushing capital toward envelopes with verifiable performance. Brazil’s December 2024 Law 15.042 introduced a regulated carbon market that monetizes operational-emission cuts, rewarding ICF projects with tradable credits. The International Finance Corporation deployed a USD 2 billion facility that lowers interest rates by 50 bps for assets achieving Energy Star or LEED certification—targets easier to hit with ICF than with post-occupancy retro-commissioning. Saudi Arabia’s Vision 2030 has steered USD 186 billion into sustainability programs that favor heat-resistant, low-maintenance structures, a brief that aligns with ICF’s durability. Brazil’s forthcoming Green Seal will certify low-carbon products by mid-2025, offering procurement advantages to early-approved ICF suppliers.

Restraints Impact Analysis of Insulated Concrete Form (ICF) Market*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher upfront cost versus wood framing | -0.9% | North America, Europe | Short term (≤ 2 years) |

| Limited contractor familiarity and skilled-labor gap | -0.7% | Global, acute in North America and emerging Asia-Pacific | Medium term (2-4 years) |

| Volatile styrene supply and pricing risk for EPS cores | -0.5% | Global, concentrated in Europe and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Higher Upfront Cost Versus Wood Framing

ICF assemblies run 10%–15% above wood frames on a per-square-foot basis, and many speculative residential developers discount future energy savings at more than 8%, stretching payback to a decade. Site-specific soil advantages can offset costs, as seen at the Comfort Inn in Georgia, yet such geotechnical conditions are rare. Contingency mark-ups of 5%–8% persist because contractors fear learning-curve delays and blowouts during concrete pours. Hybrid value-engineering, using ICF only for stair-cores and shafts, saved over 30% at New Hampshire’s Washington Street Office but demands design sophistication many teams lack. Federal tax incentives under Sections 45L and 179D reduce the premium by up to USD 5 per ft², yet uptake is limited because certification steps remain poorly understood.

Limited Contractor Familiarity And Skilled-Labor Gap

Only three in ten U.S. general contractors have crews installing at the 30 ft² per man-hour benchmark that makes ICF labor-competitive with wood, bottlenecking supply and inflating bids. ICFMA certification demands 40 hours of coursework and supervised fieldwork—an investment small firms cannot spare during peak seasons. Of 1,200 installers starting Quad-Lock training in 2024, just 40% reached field certification, showing attrition even in subsidized programs. The Divi Little Bay project demonstrated that untrained crews can still beat schedule targets, yet that outcome remains the exception. Workforce grants in Pennsylvania and Ohio reimbursed fewer than 500 workers in 2024, underscoring the mismatch between training capacity and market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Insulated Concrete Form (ICF) Market Segment Analysis

By Material Type:

Polystyrene Foam Locks In Share Through Graphite InnovationPolystyrene foam controlled 88.66% of the insulated concrete form market share in 2025, and the segment is on track for a 4.82% CAGR to 2031. The insulated concrete form market size for polystyrene products benefits from EPS’s low thermal conductivity, high compressive strength, and abundant global supply. BASF’s Neopor grade raises R-value roughly 20% at equal thickness, permitting code compliance without thicker walls. Polyurethane foam still serves tight-space niches but struggles with concrete consolidation and higher cost. Cement-bonded wood-fiber boards win projects chasing embodied-carbon credits yet hold just 8% share due to limited distribution and a 25% premium.

The polystyrene segment’s competitive edge widened after North American and European suppliers phased out HBCD flame retardants in 2024, removing a regulatory overhang. Backward-integrated EPS producers now hedge styrene swings more effectively, an advantage smaller converters cannot match. Quad-Lock’s Ultra panel, using higher-density Type II EPS, is opening mid-rise markets once limited by compressive-strength constraints. For polyurethane, installer reluctance tied to spray-equipment needs hampers wider use. Cement-bonded mixes carry higher embodied CO₂ because of their cement content, a trade-off that only becomes acceptable when carbon taxation rises sharply.

By System Type:

Screen-Grid Gains On Rebar-Placement EfficiencyFlat-wall configurations held a 54.23% share in 2025, yet screen-grid alternatives are expanding at a 5.33% CAGR, the fastest among system types. Screen-grid’s open geometry lets ironworkers drop horizontal and vertical bars without threading, eliminating a labor choke point on heavily reinforced commercial builds. The insulated concrete form market size for screen-grid products is rising as developers pursue mid-rise structures where rebar density grows. Waffle-grid systems save 10%–15% concrete volume at equal strength but cost more and require meticulous web placement.

Screen-grid’s 8%–12% material premium becomes cost-neutral once labor savings accrue on seismic or blast-resistant designs. Polycrete’s panelized kits, used at the Best Western in Georgia, show how screen-grid forms facilitate crane picks without snagging ties. Flat-wall keeps momentum in single-family builds where simplicity tops labor arithmetic, yet that segment is growing more slowly than commercial demand. Waffle-grid adoption remains North America-centric because ready-mix pricing above USD 150 yd³ makes concrete savings compelling. Post-and-beam ICF serves adaptive-reuse jobs with existing frames but represents only 6% of shipments, leaving the main contest between flat-wall and screen-grid systems.

By Construction Type:

Retrofits Accelerate As Codes TightenNew-builds represented 78.34% of volume in 2025 and will grow steadily on the back of disaster-resistant housing starts. Retrofit work, however, is expanding 5.58% per year to 2031, the quickest pace in the insulated concrete form market. Seismic mandates in California and the Pacific Northwest encourage over-cladding existing masonry with ICF to meet updated lateral-load standards without demolition. Energy-efficiency ordinances in cities such as Berkeley already require envelope upgrades at the point of sale, a policy framework that multiplies retrofit opportunities.

Retrofit growth clusters around seismic, flood, and institutional energy projects. Over-clad techniques need structural-engineering input and custom window bucks, adding 10%–15% labor, yet code avoidance costs are higher. New-build ICF continues to gain share in Midwestern tornado zones where insurers give 15%–30% discounts under the Fortified Homes program. Production builders are piloting ICF in Florida master-planned communities, using scale to pare the cost gap with wood to single digits. As municipal climate policies tighten, the adoption curve for retrofits should converge with new-build uptake.

By Application:

Commercial Projects Close The Gap On ResidentialResidential projects held a 57.78% share in 2025, but commercial builds are advancing at a 4.56% CAGR. The insulated concrete form market size advantage shifts toward hotels, data centers, and cold storage, where thermal mass limits HVAC demand and sound attenuation boosts tenant satisfaction. The Centre Park Holiday Inn cut energy use by 30% and pocketed rebates, enhancing its debt-service coverage ratio by 0.15 points. Institutional builds make up 12% of demand and grow at 4.1%, supported by FEMA grants that refund up to 75% of ICF safe-room costs.

Commercial adoption accelerated after projects like Manitoba’s Souris Hotel demonstrated 20%–25% peak-load savings thanks to ICF’s five-day thermal lag. Production-home pilots hint at broader residential expansion once learning curves flatten. Institutional users, such as Panther Creek High School, cite improved acoustics as a key benefit, raising willingness to pay beyond energy savings. Office and retail builds occasionally need column-free spans that exceed ICF’s load-bearing range, prompting hybrid approaches with steel or mass timber frames. Mixed-use projects like Washington’s ROOST 1B combine ICF shells with exposed wood interiors, signaling a bridge between performance and architectural flexibility.

Geography Analysis

North America Insulated Concrete Form (ICF) Market

North America accounted for 39.67% of 2025 revenue and remains the epicenter of FEMA-backed resilience funding and energy-code stringency. Thirty-five U.S. states adopted the 2024 IECC, driving continuous-insulation requirements that favor ICF construction. Canada’s 2020 National Building Code now factors thermal bridging, disadvantaging steel studs and lifting ICF uptake in multi-family builds like Ontario’s Wellington East Business Centre. Mexico shows early hospitality demand along hurricane-exposed coasts, but installer shortages slow penetration. A strategic swing factor is whether volume homebuilders adopt ICF at scale; pilots by D.R. Horton and Lennar are ongoing yet non-committal.

APAC Insulated Concrete Form (ICF) Market

Asia-Pacific is poised for a 5.12% CAGR, the fastest globally, fueled by China’s ultra-low-energy mandates and India’s 2024 envelope standards. China now requires public buildings above 20,000 m² to meet stringent energy baselines, nudging institutional developers toward high-mass walls. India’s updated code penalizes thermal bridging, opening room for ICF walls that improve U-values by 30% or more. Singapore’s 2024 Green Building Masterplan targets 80% of structures at the Platinum level by 2030, yet high-rise bias limits ICF to podium levels. ASEAN nations such as Vietnam are trialing ICF in refrigerated warehouses where temperature control is mission-critical.

Europe Insulated Concrete Form (ICF) Market

The European market is witnessing growth under the EU Taxonomy and national-level energy laws. The UK’s 2025 Future Homes Standard slashes allowable carbon and privileges high-thermal-mass walls. Germany’s 2024 Gebäudeenergiegesetz raises minimum insulation, and France’s RE 2020 introduces whole-building lifecycle carbon metrics, creating nuanced trade-offs for concrete-intensive solutions. Southern Europe remains slower due to entrenched brick supply chains and lower energy prices.

South America Insulated Concrete Form (ICF) Market

South America ICF market growth is led by Brazil’s carbon-credit scheme under Law 15.042 and the emerging Green Seal certification. Chile’s 2024 wall-insulation mandates open Santiago’s market, though reinforced-concrete frames still dominate.

MEA Insulated Concrete Form (ICF) Market

The Middle East and Africa market growth is anticipated to witness considerable gains in the near future. Saudi Arabia’s Vision 2030 funds sand-storm-resistant projects and sets rigid insulation specs. The UAE’s Estidama and LEED pathways favor high-performance envelopes in commercial builds. Sub-Saharan uptake is nascent but visible in Kenyan pilot homes.

Value Chain Analysis

The ICF value chain starts with upstream petrochemical and polymer inputs that convert into expanded polystyrene (EPS) foam and plastic webs/ties (commonly polypropylene), alongside cement, aggregates, rebar, and admixtures that ultimately form the concrete core. ICF manufacturers then mold or cut foam blocks/panels, cool and stabilize them, and insert plastic connectors to create modular form units; graphite-enhanced EPS (for example, BASF Neopor) is increasingly used where higher R-values are required without thicker walls. Because ICFs ship as bulky, freight-sensitive components, producers such as Fox Blocks, BuildBlock, and Amvic operate multi-site production footprints and rely on regional stocking points to support pour-date reliability and reduce transport cost exposure.

Downstream, distribution runs through direct-to-project delivery for large jobs and a dealer/distributor model for local contractors, with regional players such as Pacific ICF Corporation and service-oriented partners such as UFP Concrete Forming Solutions holding inventory and providing jobsite coordination. Install success depends on technical services (layout, bracing guidance, pour sequencing) and structured training, aligning with the market restraint around limited contractor familiarity noted by ICFMA-style certification pathways. Ready-mix suppliers and placing/finishing crews become critical ecosystem participants on pour days, so manufacturers with tighter supply alliances and stronger field support reduce rework risk and improve contractor productivity, which in turn supports repeat specification by builders and designers.

Competitive Landscape

The insulated concrete form (ICF) market is moderately fragmented. Foam Holdings’ earlier roll-up of Amvic and CBIS centralizes EPS molding, boosting economies of scale but raising systemic risk if outages occur. Competition now hinges on three levers: factory cut-to-length kits that compress site labor, proprietary tie systems that accelerate panel stacking, and supply alliances with ready-mix producers to tweak concrete rheology for narrow cores. Application engineering is a differentiator. Nudura fielded XR35 forms for Ontario’s Wellington East Business Centre to meet beyond-net-zero performance, a consultative model that smaller rivals struggle to replicate. Digital gaps persist, however: fewer than 40% of distributors offer live inventory, obliging contractors to canvass multiple yards before pour dates. Private-equity investors eye regional distributor roll-ups, but capital intensity and the need for local technical services temper straightforward consolidation plays.

Insulated Concrete Form (ICF) Industry Leaders

Nuduara Inc. (RPM International Inc.)

Airlite Plastics Company and Fox Blocks (Fox Blocks)

Amvic Ireland LTD

Logix Brands Ltd.

BASF

- *Disclaimer: Major Players sorted in no particular order

Insulated Concrete Form (ICF) Market Companies Covered in this Report

- Airlite Plastics Company and Fox Blocks (Fox Blocks)

- Alleguard

- Amvic Ireland LTD

- BASF

- Beco Products Ltd

- BuildBlock Building Systems LLC

- Carlisle Construction Materials (Carlisle Companies Inc.)

- Durisol

- Future Foam Inc.

- INTEGRASPEC

- LiteForm

- Logix Brands Ltd.

- Polycrete International

- Quad-Lock Building Systems

- RASTRA

- Nudura Inc. (RPM International Inc.)

- Sismo Building Technology

- SuperForm

- TF System

- Tremco CPG Inc.

Market Opportunities and Future Outlook

Energy-code tightening and compliance clarification create addressable whitespace for ICF suppliers that can document performance and simplify approvals. In the United States, the California Division of the State Architect issued IR 19-6 for the 2025 California Building Code, clarifying requirements and acceptance criteria for flat-wall ICF systems in projects under its jurisdiction, which supports specification in public K-12 and other DSA-regulated work where submittal clarity matters.

In the United Kingdom, the regulatory pathway continues to favor high-performance fabric as the Future Homes Standard framework advances, and 2026 amendments to Building Regulations in England add requirements tied to conservation of fuel and power and renewable electricity generation, reinforcing the role of high-thermal-performance envelope assemblies. Near-term opportunity also sits in scaling ICF beyond bespoke builds into templated, production-style delivery models and more industrialized construction workflows. Digital interoperability standards (buildingSMART International, ISO 16739-1:2024 for Industry Foundation Classes) support embedding wall-assembly and thermal-performance data into BIM and QA routines, reducing coordination friction for multi-trade teams. On the demand side, localized energy-cost pressure is becoming a concrete decision driver for builders pursuing stringent performance targets; for example, commentary around the 2026 Massachusetts Stretch Energy Code highlights HERS 42 requirements alongside high retail electricity pricing (USD 0.32/kWh in Plymouth in April 2026), which raises the economic value of envelope approaches that reduce HVAC loads and improve airtightness without extensive add-on insulation detailing.

Recent Industry Developments in Insulated Concrete Form (ICF) Market

- April 2026: RPM International Inc. released its fiscal 2026 third-quarter update for the period ended February 28, 2026, providing current disclosure around the scale of its building products platform that includes Nudura ICF. The update signals continued corporate-level attention to building-envelope categories where code compliance and resilience are shaping material choices.

- January 2026: Nudura announced a national contractor partnership program to deploy ICF solutions across multiple projects, strengthening installer education and enabling specifier confidence for multi-site builds.

- December 2024: Brazil passed Law 15.042 establishing the Brazilian Greenhouse Gas Emissions Trading System, creating a policy mechanism that monetizes operational-emission reductions in buildings. This regulatory step strengthens the business case for high-performance envelopes, including ICF, in markets where carbon-credit frameworks influence capital allocation and procurement.

Insulated Concrete Form (ICF) Market Report Scope and Research Methodology

Market Definition and Coverage

For this methodology, the insulated concrete form (ICF) market covers the value of factory-made insulated form units (blocks or panels) that stay in place as permanent formwork when concrete is poured. These ICF units are used across new building construction and sized at end-user pricing.

Scope exclusions: The sizing excludes loose insulation boards, repair kits and accessories sold separately, and temporary formwork systems that are removed after the concrete sets.

Segments Covered in This Report

- Material Type

- Polystyrene Foam

- Polyurethane Foam

- Cement-Bonded Wood Fiber

- Cement-Bonded Polystyrene Beads

- System Type

- Flat-Wall Systems

- Waffle-Grid Systems

- Screen-Grid Systems

- Post-and-Beam Systems

- Construction Type

- New-build

- Retrofit / Remodeling

- Application

- Residential

- Commercial

- Institutional

- Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to anchor the model to real construction activity and code-driven demand signals. We referenced public sources such as the US Census Bureau construction spending series, US Energy Information Administration energy price trends, International Energy Agency building energy indicators, and the US Department of Energy building energy codes program materials.

To avoid relying on one data stream, the desk work was cross-checked with items including national building code council updates, customs and trade statistics where relevant for foam and construction material flows, company annual reports and investor presentations, and construction press coverage of project starts. A few paid database subscriptions were used only for company financials and patent checks to confirm who is active and where innovation is concentrated. The sources listed here are illustrative, and other public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was run to pressure-test demand assumptions with people who see ICF specified, purchased, and installed, including manufacturers, distributors, contractors, and building designers. These interviews were used to confirm typical application mix, pricing movement, and how energy codes and resiliency needs change ICF selection by region. The input was then used to triangulate model inputs and close data gaps.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 14% | APAC: 41% |

| Mid tier: 41% | Functional/Unit leaders: 28% | EMEA: 32% |

| Smaller Players: 22% | Managers: 58% | Americas: 27% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs the demand pool from construction activity and ICF adoption, then adjusts it using on-the-ground checks. The model begins from new-build volumes and construction spending by building type, and then applies ICF usage rates validated through installer and distributor feedback, which is where the main market value is derived.

Several practical inputs are tracked because they explain why ICF demand changes year to year. These include building permit and housing start momentum, shifts in energy code stringency and enforcement, insulation and resin price direction that influences ICF pricing, labor availability for forming and concrete work, and the share of projects that prioritize resilience and disaster performance. Forecasts are produced using scenario analysis tied to expected construction cycles and energy-efficiency policy direction, and then sense-checked against selective bottom-up approximations such as sampled average selling prices times estimated unit volumes, plus channel feedback on annual shipment direction. Where bottom-up visibility is thin in smaller countries, gaps are handled using regional proxy adoption rates normalized by climate zone and code maturity, and then re-tested through additional calls.

Data Validation & Update Cycle

Validation is done in steps so the final numbers do not depend on one assumption. Outputs are compared with independent signals such as construction spending trend lines, permit momentum, and input-cost movements, and large swings are investigated before results are finalized.

A second analyst reviews the model logic, calculations, and the final narrative. Any unusual variance triggers a re-check of sources and follow-up with interviewees. The report is refreshed annually, with interim updates if there is a material change, such as a major code shift or a sudden pricing shock in key insulation inputs. Before delivery, a fresh pass is completed so clients receive the latest updated view.

Mordor Intelligence's Insulated Concrete Form Icf Market Estimate Compared With Other Published Estimates

Published market sizes for ICF often do not match because each study draws the boundary in a slightly different way and then uses different construction indicators to convert demand into dollars. The starting year also matters, since construction cycles and resin-linked pricing can move reported revenue quickly.

By tracking permitting and construction spending signals and refreshing inclusion rules for permanent stay-in-place form units, Mordor Intelligence keeps the ICF total tied to new unit sales at end-user prices rather than mixing in adjacent insulation boards or removable formwork revenue. Differences also appear when a source uses a single global price uplift instead of region-specific pricing logic, and when the forecast is built from optimistic code adoption assumptions that are not re-validated with installers and distributors each year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.78 B (2026) | |

| Global Consultancy A | USD 0.96 B (2024) | This estimate appears to use an earlier base year and a narrower revenue capture, which can undercount when ICF penetration is rising and when pricing moved after 2024, and it is not always clear if the value is measured at factory gate or end-user level. |

| Industry Publisher B | USD 2.03 B (2025) | The higher value is consistent with a broader scope choice, where adjacent construction products or wider application revenue may be included, and the pricing and currency timing for 2025 can inflate the headline if regional averages are applied too uniformly. |

Taken together, the spread is mainly explained by scope boundaries, base-year timing, and how price is converted from activity into revenue. Our approach stays repeatable because the build starts from clear construction demand indicators, applies interview-tested adoption and pricing assumptions, and then resolves variances through cross-checks before finalizing totals.

Key Questions Answered in the Report

What is the current value of the insulated concrete form market?

The insulated concrete form market size is estimated at USD 1.78 billion in 2026.

How fast is the insulated concrete form market expected to grow?

It is forecast to expand at a 4.73% CAGR, attaining USD 2.24 billion by 2031.

Which material dominates insulated concrete form production?

Polystyrene foam held 88.66% of the 2025 volume due to ongoing graphite-enhanced EPS innovation.

Why are screen-grid systems gaining popularity?

Their open geometry simplifies rebar placement, lifting productivity on multi-story commercial projects and driving a 5.33% CAGR.

Which region will grow the fastest?

Asia-Pacific is projected to lead with a 5.12% CAGR between 2026 and 2031, spurred by stricter energy codes in China and India.

What is the main barrier to wider adoption?

Higher upfront cost versus wood framing, coupled with limited installer availability, remains the primary restraint.

Page last updated on: