Market Overview

| Study Period | 2019 - 2030 |

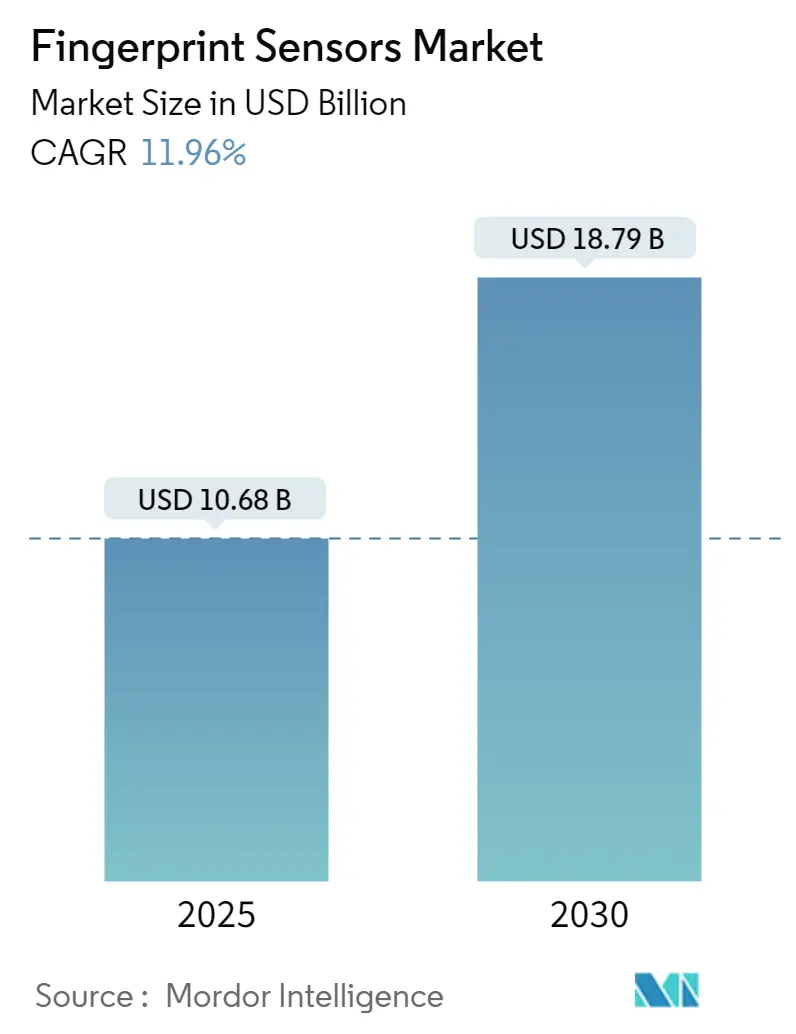

| Market Size (2025) | USD 10.68 Billion |

| Market Size (2030) | USD 18.79 Billion |

| Growth Rate (2025 - 2030) | 11.96% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

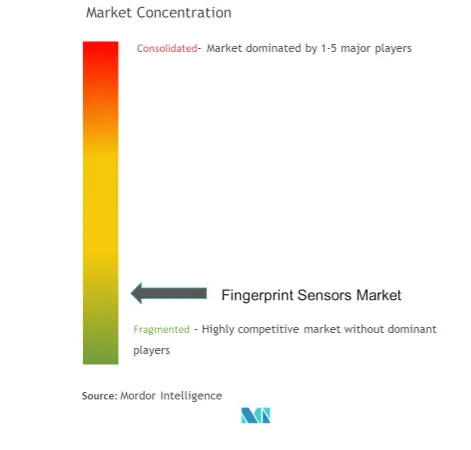

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Fingerprint Sensors Market Analysis

The Fingerprint Sensors Market size is estimated at USD 10.68 billion in 2025, and is expected to reach USD 18.79 billion by 2030, at a CAGR of 11.96% during the forecast period (2025-2030).

The fingerprint sensor industry is experiencing a profound transformation driven by the convergence of digital technologies and an increasing emphasis on secure authentication methods. According to GSMA, the global smartphone penetration rate reached 68% in 2022, marking the first increase since 2018, based on an estimated 6.3 billion smartphone subscriptions globally. This digital revolution has catalyzed innovations in fingerprint sensor technologies, particularly in areas such as ultrasonic sensors, optical sensors, and capacitive sensing solutions. The integration of artificial intelligence and machine learning algorithms has further enhanced the accuracy and reliability of fingerprint recognition systems, with the Biometrics Institute reporting that interest in AI applications for biometric sensors more than doubled from 8% in 2022 to 19% in 2023.

The industry is witnessing a significant shift toward more sophisticated and versatile fingerprint sensor solutions, particularly in the realm of in-display sensors and multi-modal biometric systems. Major technological advancements include the development of ultrasonic sensors capable of reading fingerprints through various materials, including glass and metal, enabling more flexible device designs. The emergence of transparent sensors has opened new possibilities for seamless integration into displays, while improvements in processing capabilities have reduced recognition times and enhanced security features. These innovations are particularly evident in the latest smartphone releases, where manufacturers are incorporating advanced fingerprint sensor technologies beneath the display glass.

The convergence of payment technologies and biometric authentication has created new opportunities for fingerprint sensor market applications, particularly in the financial sector. Banks and financial institutions are increasingly adopting biometric payment cards that incorporate fingerprint scanners, enabling secure and convenient transactions without PIN entry. The integration of fingerprint authentication in automotive applications has also gained traction, with manufacturers implementing biometric access systems for vehicle entry and ignition. This trend extends to smart home security systems, where fingerprint recognition is becoming a standard feature for access control.

The market is experiencing a notable shift in authentication preferences, with organizations increasingly adopting multi-factor authentication systems that combine fingerprint recognition with other biometric sensor modalities. According to GSMA projections, Europe is positioned to lead in digital adoption with an estimated 88% smartphone penetration rate and 82% internet penetration by 2025, creating a robust foundation for advanced biometric applications. The industry has also witnessed significant developments in standardization efforts, with various stakeholders collaborating to establish unified protocols for fingerprint sensor market integration and interoperability, ensuring consistent performance and security across different platforms and applications.

Fingerprint Sensors Market Trends

Increasing Usage of Fingerprint Sensors for Smart Wearable Devices and Smartphones

The proliferation of smartphones and smart wearable devices has become a primary driver for fingerprint sensor adoption, with smartphones representing the largest application segment for user authentication. The technology has evolved significantly since Toshiba's first smartphone implementation in 2011, with Apple's Touch ID revolutionizing the mobile biometrics landscape through its accurate and user-friendly capacitive technology. This breakthrough has led to widespread adoption across major manufacturers, with companies like Samsung, Lenovo, and Asus incorporating fingerprint sensors into their devices. According to the latest Ericsson Mobility Report from June 2023, smartphone subscriptions have reached an impressive 6.71 billion, indicating the massive potential market for fingerprint sensor integration.

The technological landscape is witnessing a significant shift from traditional capacitive sensors to more advanced solutions, particularly in premium smartphones. Manufacturers are increasingly adopting ultrasonic fingerprint scanners for high-end devices while implementing optical sensors in mid-range products, driven by the growing demand for in-display sensor integration and bezel-less designs. This evolution is complemented by the rising adoption of smart wearables, where fingerprint authentication is becoming a crucial feature for securing personal data and enabling seamless user experiences. The integration of these sensors in various form factors, from smartphones to tablets and wearables, demonstrates the versatility and growing importance of fingerprint authentication in modern consumer electronics.

Understand The Key Trends Shaping This Market

Download PDF

Need for Security in Business Applications

The escalating frequency and sophistication of cyber threats and data breaches have made robust security measures imperative across enterprises and government organizations. Financial institutions and businesses are particularly vulnerable, as evidenced by significant data breaches affecting hundreds of thousands of records containing sensitive information like phone numbers, email addresses, and payment details. The integration of fingerprint readers provides an additional layer of security for various business applications, from secure access control to financial transactions, helping organizations protect sensitive data and maintain customer trust.

The growing prevalence of online shopping and digital transactions has created an urgent need for enhanced security measures in financial applications. Banks and financial institutions are increasingly adopting fingerprint authentication for secure transactions, with many implementing biometric payment cards that incorporate fingerprint sensors for user verification. This trend is particularly evident in mobile payment systems, where fingerprint authentication has become a standard security feature. For instance, in China alone, the China Internet Network Information Center (CNNIC) reported that as of June 2023, approximately 943.19 million people were using mobile payments, highlighting the massive scale of transactions that require secure authentication methods.

Government Initiatives to Adopt Biometrics in Various Fields

Government initiatives worldwide are driving the adoption of fingerprint sensors across various applications, from civil identity systems to border security and law enforcement. Many countries are implementing large-scale biometric identification programs that require fingerprint authentication as a core component. These initiatives range from national ID programs to border control systems, with governments investing significantly in fingerprint recognition technology to enhance security and streamline citizen services. The implementation of these programs has created a substantial demand for fingerprint sensors and related technologies, as governments seek to modernize their identification and security infrastructure.

The automotive sector is also witnessing increased government support for biometric integration, with various countries promoting advanced security features in vehicles. This is exemplified by Nissan's introduction of the Xmotion concept car featuring fingerprint biometric authentication for enhanced vehicle security, demonstrating how government initiatives are influencing innovation across different sectors. Additionally, government organizations are implementing fingerprint authentication in various public services, from healthcare to social welfare programs, creating a comprehensive ecosystem that relies on secure biometric identification. These initiatives are complemented by regulations and standards that mandate the use of biometric authentication in certain applications, further driving the adoption of fingerprint sensor technology.

Segment Analysis: By Type

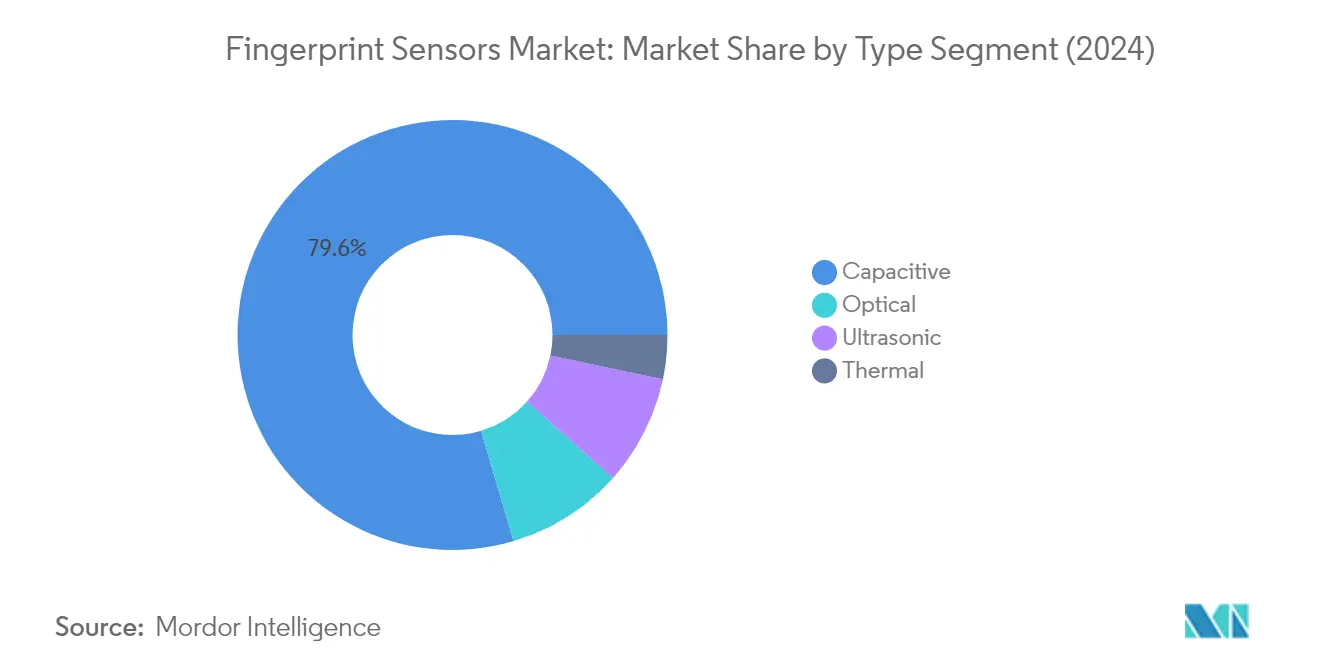

Capacitive Segment in Fingerprint Sensors Market

The capacitive segment continues to dominate the global fingerprint sensors market, commanding approximately 80% market share in 2024. This significant market position is driven by the widespread adoption of capacitive fingerprint scanners in smartphones, laptops, and other consumer electronic devices. The technology's reliability, cost-effectiveness, and superior performance characteristics have made it the preferred choice for manufacturers. Major smartphone vendors are actively incorporating advanced capacitive sensors, with companies like Fingerprint Cards developing curved capacitive sensors specifically designed for modern smartphone designs. The segment's strength is further reinforced by its ability to provide high levels of security and performance while maintaining relatively low power consumption, making it ideal for battery-powered devices.

Ultrasonic Segment in Fingerprint Sensors Market

The ultrasonic fingerprint sensors market is emerging as the fastest-growing technology in the fingerprint sensors market, with an expected growth rate of approximately 15% during 2024-2029. This rapid growth is attributed to the technology's superior capabilities in reading fingerprints through various materials and its ability to provide enhanced security features. Ultrasonic sensors are gaining particular traction in premium smartphones and high-security applications due to their ability to capture three-dimensional fingerprint details, making them more secure against spoofing attempts. The technology's capability to function effectively even with wet or dirty fingers, coupled with its increasing adoption in under-display implementations, is driving its rapid market expansion. Major technology providers are investing heavily in ultrasonic sensor development, focusing on improving scanning speed and reducing production costs to make the technology more accessible across different price segments.

Remaining Segments in Fingerprint Sensors Market by Type

The optical fingerprint sensor market and thermal segments continue to play important roles in the fingerprint sensors market, each serving specific application needs. Optical sensors, known for their cost-effectiveness and reliability in certain applications, are finding renewed interest in under-display fingerprint reader solutions for smartphones. The technology's ability to capture high-resolution fingerprint images makes it particularly suitable for government and security applications. Meanwhile, thermal sensors, while occupying a smaller market share, maintain their importance in specialized applications where temperature-based sensing offers unique advantages. These segments are experiencing ongoing technological improvements, with manufacturers focusing on enhancing resolution, reducing form factors, and improving overall performance to meet evolving market demands.

Segment Analysis: By Application

Smartphones/Tablets Segment in Fingerprint Sensors Market

The smartphones and tablets segment continues to dominate the fingerprint sensors market, commanding approximately 63% market share in 2024. This significant market position is driven by the widespread integration of fingerprint readers in mobile devices across all price segments. The increasing focus on security in mobile payments and app authentication has made fingerprint scanners a standard feature in smartphones. Major smartphone manufacturers are continuously innovating in this space, with many adopting advanced technologies like in-display screen fingerprint sensor market and ultrasonic sensors for enhanced security and user experience. The segment's growth is further supported by the rising smartphone penetration rates globally and the increasing adoption of mobile banking and payment applications that require secure biometric authentication.

Smartcards Segment in Fingerprint Sensors Market

The smartcards segment is emerging as the fastest-growing application area in the fingerprint sensors market, with an expected growth rate of approximately 13% during 2024-2029. This rapid growth is primarily driven by the increasing adoption of biometric payment cards by major financial institutions worldwide. The integration of fingerprint sensors in smartcards is revolutionizing the payment industry by offering enhanced security and convenience for contactless transactions. Financial institutions are increasingly partnering with technology providers to develop and deploy biometric payment cards, while government agencies are incorporating fingerprint sensor authentication in identity cards and access control systems. The segment's growth is further accelerated by the rising demand for secure payment solutions and the increasing focus on reducing payment fraud.

Remaining Segments in Application Market Segmentation

The laptops and IoT & Other Applications segments represent significant opportunities in the fingerprint sensors market. The laptops segment is witnessing steady growth due to the increasing integration of fingerprint sensors in business and consumer laptops for secure login and authentication purposes. Meanwhile, the IoT & Other Applications segment is expanding rapidly as fingerprint authentication becomes increasingly important in connected devices, automotive applications, and smart home solutions. These segments are benefiting from the growing emphasis on security in enterprise environments and the rising adoption of IoT devices across various industries. The integration of fingerprint sensors in these applications is driven by the need for secure access control and user authentication in an increasingly connected world.

Segment Analysis: By End User

Consumer Electronics Segment in Fingerprint Sensors Market

The consumer electronics segment dominates the global fingerprint sensors market, holding approximately 36% market share in 2024. This significant market position is primarily driven by the widespread adoption of fingerprint sensors in smartphones, tablets, laptops, and other consumer electronic devices. The integration of in-display fingerprint sensors in premium smartphones and the growing trend of bezel-less displays have further strengthened this segment's dominance. Major smartphone manufacturers are increasingly incorporating advanced fingerprint sensing technologies, with many devices now featuring ultrasonic and optical sensors for enhanced security and user experience. The segment's growth is also supported by the rising demand for smart wearables and IoT devices that utilize fingerprint authentication for secure access and personalization features.

BFSI Segment in Fingerprint Sensors Market

The Banking, Financial Services, and Insurance (BFSI) segment is emerging as the fastest-growing segment in the fingerprint sensors market, with a projected growth rate of approximately 13% during 2024-2029. This rapid growth is driven by the increasing adoption of biometric authentication in banking applications, particularly in payment cards and ATM security systems. Financial institutions are actively implementing fingerprint authentication solutions to enhance transaction security and combat financial fraud. The integration of fingerprint sensors in biometric payment cards is gaining significant traction, with several major banks worldwide launching pilot programs for fingerprint-authenticated payment cards. The segment's growth is further accelerated by the rising demand for contactless payment solutions and the increasing focus on secure digital banking services.

Remaining Segments in End User Segmentation

The military and defense segment continues to be a crucial market for fingerprint sensors, with applications ranging from secure access control to personnel identification systems. The government sector utilizes fingerprint sensors for various applications including national ID programs, border control, and law enforcement. These segments benefit from the high reliability and security features of fingerprint authentication systems. The other end-user industries segment, which includes automotive and healthcare sectors, is witnessing increased adoption of fingerprint sensors for applications such as vehicle access control and patient identification systems. Each of these segments contributes uniquely to the market's growth, driven by their specific security requirements and authentication needs.

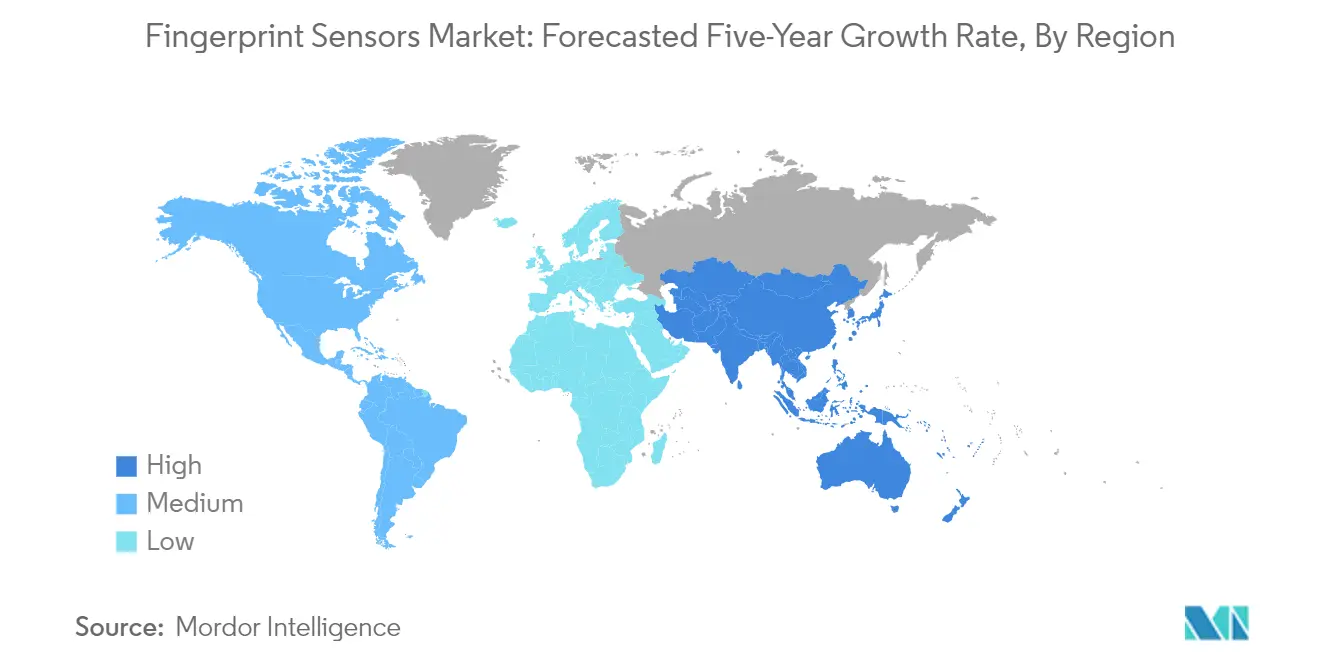

Fingerprint Sensors Market Geography Segment Analysis

Fingerprint Sensors Market in North America

North America represents a mature fingerprint sensor market, driven by extensive adoption across various sectors, including consumer electronics, government, and defense applications. The United States and Canada are the key markets in this region, with a strong presence of major technology companies and increasing implementation of biometric solutions in security systems. The region's growth is supported by robust technological infrastructure, a growing emphasis on cybersecurity, and increasing adoption of fingerprint sensors in smartphones and other electronic devices.

Fingerprint Sensors Market in United States

The United States dominates the North American fingerprint sensors market, holding approximately 88% market share in 2024. The country's market leadership is attributed to its advanced technological ecosystem and strong presence of key market players. The widespread adoption of fingerprint sensors in smartphones, growing implementation in government applications, and increasing focus on secure payment solutions are driving market growth. The country has also witnessed significant adoption in law enforcement and border control applications, with various government agencies implementing fingerprint-based authentication systems.

Fingerprint Sensors Market in Canada

Canada demonstrates steady growth in the fingerprint sensor market, with a projected growth rate of approximately 10% during 2024-2029. The country's market is primarily driven by increasing adoption of biometric solutions in banking and financial institutions, government initiatives for enhanced security measures, and growing implementation in consumer electronics. Canadian airports and border security agencies are increasingly deploying fingerprint scanning technologies, contributing to market expansion. The country's focus on digital identity verification and secure payment solutions is expected to further boost market growth in the coming years.

Fingerprint Sensors Market in Europe

The European fingerprint sensors market is characterized by strong technological innovation and widespread adoption across multiple sectors. The region's market is primarily driven by countries like the United Kingdom, Germany, and France, with each contributing significantly to market growth. The implementation of stringent security regulations, increasing focus on contactless payments, and growing adoption of biometric solutions in various industries are key factors shaping the market landscape in Europe.

Fingerprint Sensors Market in United Kingdom

The United Kingdom leads the European fingerprint sensor market, commanding approximately 35% market share in 2024. The country's dominant position is supported by extensive implementation of biometric solutions in banking and financial services, government applications, and consumer electronics. The UK has witnessed significant adoption of fingerprint authentication in law enforcement and security applications, with police forces increasingly utilizing mobile fingerprint scanning systems for rapid identification.

Fingerprint Sensors Market in Germany

Germany exhibits strong growth potential in the fingerprint sensor market, with a projected growth rate of approximately 12% during 2024-2029. The country's automotive sector is increasingly incorporating fingerprint sensors in vehicles for enhanced security and personalization features. German manufacturers are actively developing innovative fingerprint sensor solutions, particularly for payment cards and access control systems. The country's strong focus on technological advancement and digital security is expected to drive continued market expansion.

Fingerprint Sensors Market in Asia-Pacific

The Asia-Pacific region represents a dynamic fingerprint sensors market, characterized by rapid technological adoption and increasing implementation across various sectors. Countries like China, Japan, India, and South Korea are driving significant growth in the region. The market is benefiting from the growing smartphone penetration, increasing focus on secure payment solutions, and government initiatives for digital identity verification systems.

Fingerprint Sensors Market in China

China maintains its position as the largest market for fingerprint sensors in the Asia-Pacific region. The country's dominance is driven by its massive smartphone manufacturing industry, extensive implementation of biometric identification systems, and strong government support for security technologies. Chinese manufacturers are actively developing innovative fingerprint sensor solutions, particularly focusing on in-display sensors for smartphones and other mobile devices.

Fingerprint Sensors Market in India

India emerges as the fastest-growing market for fingerprint sensors in the Asia-Pacific region. The country's growth is primarily driven by government initiatives promoting biometric identification systems, increasing smartphone adoption, and growing implementation in banking and financial services. The success of the Aadhaar program, which uses fingerprint authentication for citizen identification, has created a strong foundation for market expansion.

Fingerprint Sensors Market in Latin America

The Latin American fingerprint sensor market is experiencing steady growth, driven by increasing adoption of biometric solutions in banking and financial services, government applications, and consumer electronics. The region is witnessing growing implementation of fingerprint authentication in payment cards and mobile devices. Brazil emerges as the largest market in the region, while Mexico shows the fastest growth potential, supported by increasing adoption of secure payment solutions and government initiatives for digital identification systems.

Fingerprint Sensors Market in Middle East and Africa

The Middle East and Africa region demonstrates growing adoption of fingerprint sensor technologies, particularly in banking, government, and security applications. The market is driven by increasing focus on secure payment solutions and growing implementation of biometric identification systems. The United Arab Emirates leads the market in terms of size, while Saudi Arabia shows the fastest growth potential, supported by various government initiatives and increasing adoption of digital payment solutions.

Get Analysis on Important Geographic Markets

Download PDF

Fingerprint Sensors Industry Overview

Top Companies in Fingerprint Sensors Market

The fingerprint scanner companies market features prominent players like Qualcomm Technologies, TDK Corporation, Fingerprint Cards AB, Synaptics, NEC Corporation, and IDEX Biometrics ASA, leading innovation and market development. These companies are heavily investing in research and development to advance fingerprint sensor technologies, particularly focusing on ultrasonic, capacitive, and optical sensing solutions. Strategic partnerships with smartphone manufacturers, payment card providers, and automotive companies have become increasingly common to expand application scope. Companies are prioritizing the miniaturization of sensors while improving accuracy and security features, with a notable trend toward developing in-display fingerprint solutions. The industry is witnessing an increased focus on developing cost-effective solutions for mass-market adoption while maintaining high-security standards. Market leaders are also expanding their geographical presence through regional offices and distribution networks, particularly in high-growth markets across Asia-Pacific and emerging economies.

Consolidated Market with Strong Regional Players

The fingerprint sensor market exhibits a moderately consolidated structure with a mix of global technology conglomerates and specialized biometric solution providers. Global players like Qualcomm and NEC Corporation leverage their extensive technological capabilities and cross-industry presence to maintain market leadership, while specialized firms like Fingerprint Cards AB and IDEX Biometrics focus on developing cutting-edge fingerprint recognition solutions. The market has witnessed significant consolidation through strategic acquisitions, such as Thales Group's acquisition of Gemalto NV, which has reshaped the competitive landscape and enhanced technological capabilities in the biometric authentication space.

The industry is characterized by strong regional dynamics, particularly in Asia-Pacific, where local players have established significant market presence through partnerships with regional smartphone manufacturers and government agencies. Market participants are increasingly pursuing vertical integration strategies to strengthen their position in the value chain, from sensor manufacturing to solution deployment. The competitive environment is further intensified by the emergence of new entrants bringing innovative technologies, although high entry barriers in terms of technological expertise and capital requirements limit widespread market entry.

Innovation and Adaptability Drive Market Success

Success in the fingerprint scanner market increasingly depends on companies' ability to innovate while maintaining cost competitiveness and security standards. Incumbent players are focusing on developing comprehensive biometric solutions that integrate multiple authentication methods while expanding their presence in emerging applications such as automotive security and IoT devices. The ability to adapt to changing end-user requirements, particularly in the smartphone and payment card segments, while maintaining strong relationships with device manufacturers and system integrators, has become crucial for market success. Companies are also investing in developing proprietary algorithms and security features to differentiate their offerings and create barriers to entry.

For new entrants and challenger companies, success lies in identifying and capitalizing on niche market segments while building strategic partnerships with established players in the value chain. The fingerprint module market presents opportunities for companies that can offer innovative solutions addressing specific industry challenges, such as power consumption in mobile devices or durability in harsh environments. Regulatory compliance, particularly regarding data privacy and security standards, has become a critical success factor, with companies needing to demonstrate robust security measures and compliance with regional regulations. The ability to scale operations while maintaining product quality and meeting increasingly stringent customer requirements will determine long-term success in this evolving market.

Fingerprint Sensors Market Leaders

-

Qualcomm Incorporated

-

TDK Corporation

-

Vkansee Technology Inc.

-

Egis Technology Inc.

-

Fingerprint Cards AB

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Fingerprint Sensors Market News

- September 2023 - Mastercard launched an in-car payment partnership aimed at Mercedes drivers in Germany. The collaboration will allow customers to use a fingerprint sensor in their car to make digital payments at more than 3,600 service stations in Germany.

- May 2023 - Samsung Display revealed an advancement in biometric technology at the SID Display Week 2023 in Los Angeles. The Sensor OLED Display depends on an embedded light-sensing organic photodiode within the panel structure, eliminating the need for separate sensor modules beneath the display.

Fingerprint Sensors Industry Segmentation

A fingerprint sensor is an electronic security system that uses fingerprints for biometric authentication to grant users access to a device or information or to approve transactions.

The fingerprint sensor market is segmented by type (optical, capacitive, thermal, and ultrasonic), application (smartphones/tablets, laptops, smartcards, IoT, and other applications), end-user industry (military and defense, consumer electronics, BFSI, government, and other end-user industries), and geography (North America [United States and Canada], Europe [Germany, United Kingdom, France, and the Rest of Europe], Asia-Pacific [China, Japan, India, South Korea, and the Rest of Asia-Pacific], Latin America, and Middle East and Africa). The market size and forecast are provided in terms of value (USD) for all the segments.

| By Type | Optical | ||

| Capacitive | |||

| Thermal | |||

| Ultrasonic | |||

| By Application | Smartphones/Tablets | ||

| Laptops | |||

| Smartcards | |||

| IoT and Other Applications | |||

| By End-user Industries | Military and Defense | ||

| Consumer Electronics | |||

| BFSI | |||

| Government | |||

| Other End-user Industries | |||

| By Geography*** | North America | United States | |

| Canada | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Asia | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Latin America | |||

| Middle East and Africa | |||

By Type

| Optical |

| Capacitive |

| Thermal |

| Ultrasonic |

By Application

| Smartphones/Tablets |

| Laptops |

| Smartcards |

| IoT and Other Applications |

By End-user Industries

| Military and Defense |

| Consumer Electronics |

| BFSI |

| Government |

| Other End-user Industries |

By Geography***

| North America | United States |

| Canada | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Asia | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Latin America | |

| Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Fingerprint Sensors Market Research FAQs

How big is the Fingerprint Sensors Market?

The Fingerprint Sensors Market size is expected to reach USD 10.68 billion in 2025 and grow at a CAGR of 11.96% to reach USD 18.79 billion by 2030.

What is the current Fingerprint Sensors Market size?

In 2025, the Fingerprint Sensors Market size is expected to reach USD 10.68 billion.

Who are the key players in Fingerprint Sensors Market?

Qualcomm Incorporated, TDK Corporation, Vkansee Technology Inc., Egis Technology Inc. and Fingerprint Cards AB are the major companies operating in the Fingerprint Sensors Market.

Which is the fastest growing region in Fingerprint Sensors Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Fingerprint Sensors Market?

In 2025, the Asia-Pacific accounts for the largest market share in Fingerprint Sensors Market.

What years does this Fingerprint Sensors Market cover, and what was the market size in 2024?

In 2024, the Fingerprint Sensors Market size was estimated at USD 9.40 billion. The report covers the Fingerprint Sensors Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Fingerprint Sensors Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.