Fiber Optic Pressure Sensors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

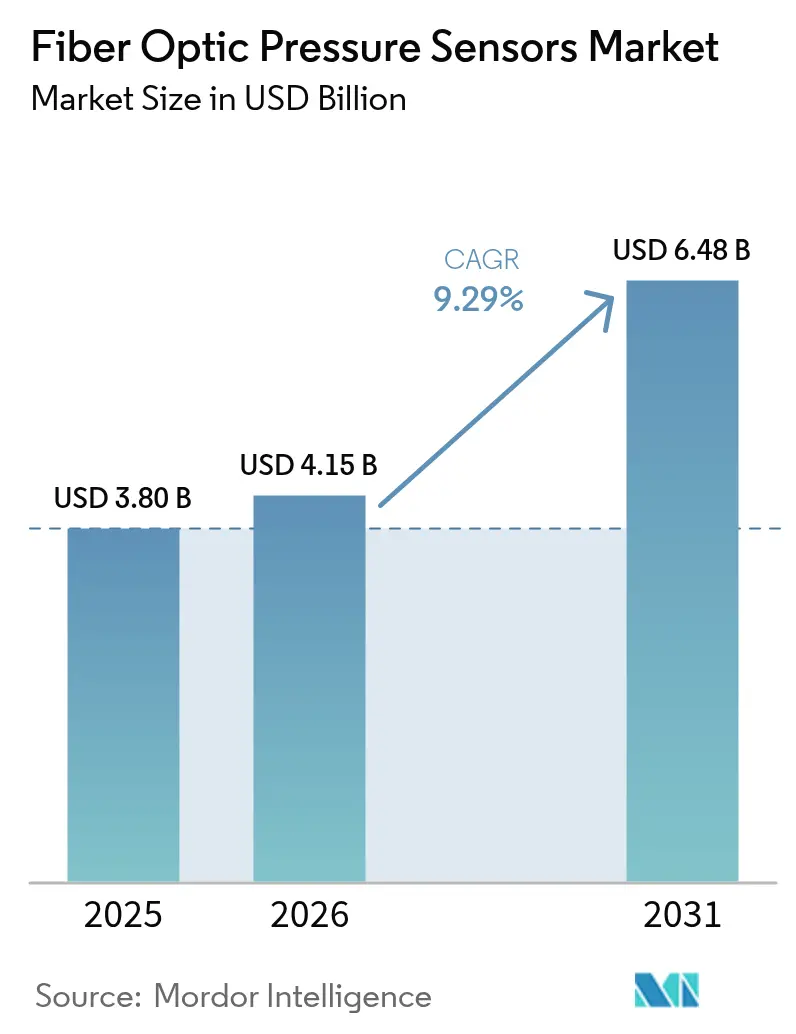

| Market Size (2026) | USD 4.15 Billion |

| Market Size (2031) | USD 6.48 Billion |

| Growth Rate (2026 - 2031) | 9.29% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fiber Optic Pressure Sensors Market Analysis by Mordor Intelligence

The fiber optic pressure sensors market size was valued at USD 3.8 billion in 2025 and estimated to grow from USD 4.15 billion in 2026 to reach USD 6.48 billion by 2031, at a CAGR of 9.29% during the forecast period (2026-2031). Robust demand stems from the technology’s suitability for real-time monitoring in harsh environments such as downhole oil wells and electric-vehicle battery packs. Ongoing miniaturization of Fabry–Perot micro-cavities and a 60% fall in interrogation-unit costs since 2020 have broadened adoption across industrial automation, healthcare, and mobility. Multiplexing gains have lifted Fiber Bragg Grating (FBG) uptake, while edge analytics integration in smart factories and implantable devices underscores new avenues of growth. Despite a 2–3 × cost premium over piezo-resistive sensors, rising total-cost-of-ownership advantages, workforce upskilling, and connector standardization initiatives continue to mitigate adoption barriers.

Key Report Takeaways

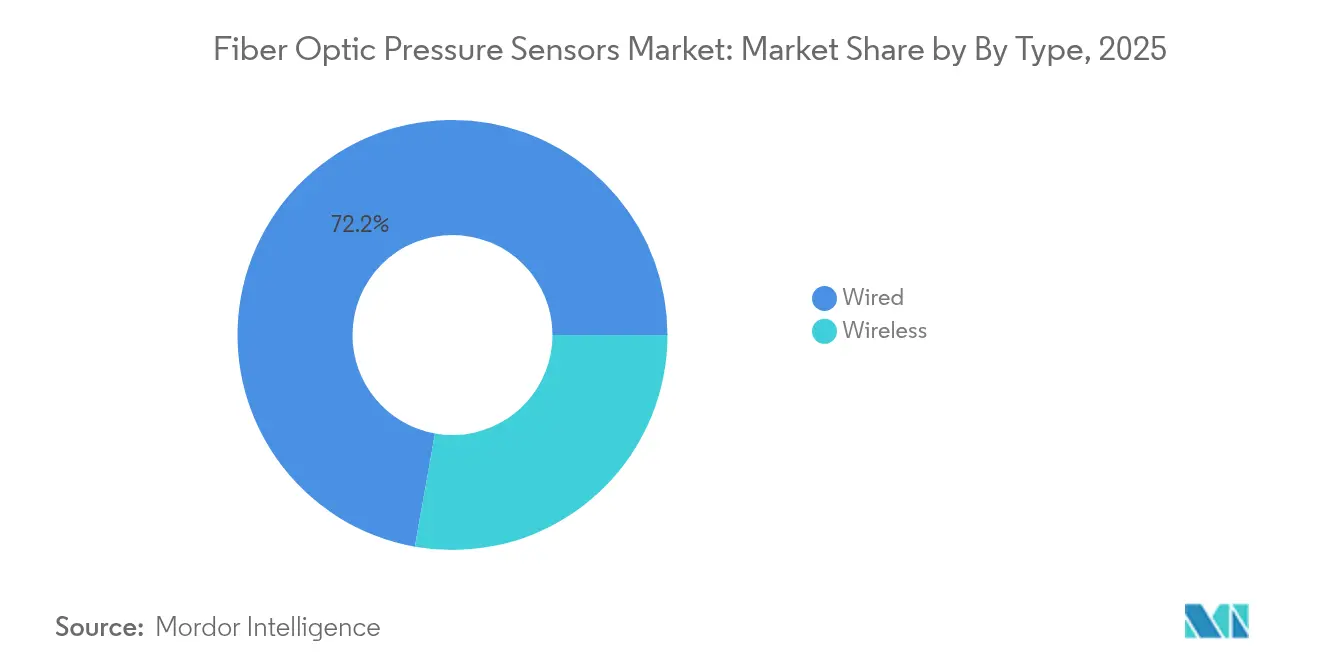

- By type, wired sensors held 72.20% of fiber optic pressure sensors market share in 2025, whereas wireless variants are projected to expand at a 11.6% CAGR through 2031.

- By technology, Fabry–Perot sensors led with 46.40% revenue share in 2025, while FBG technology is poised for the fastest 12.9% CAGR through 2031.

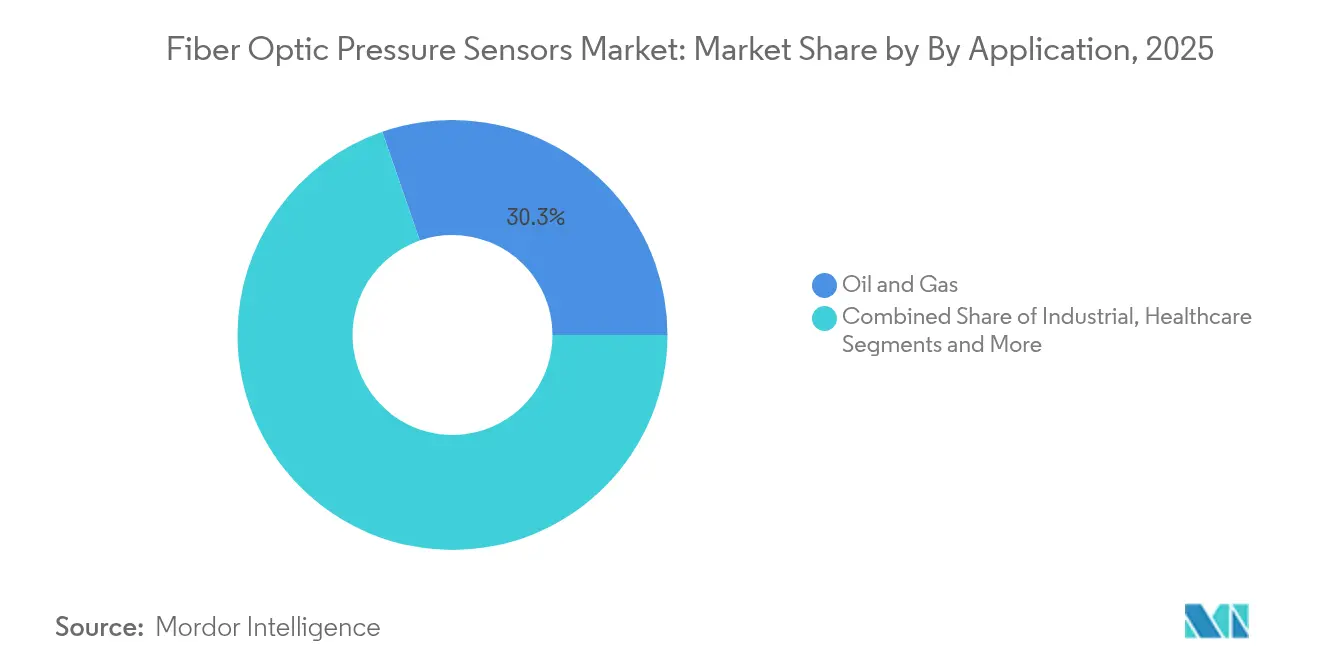

- By application, oil and gas accounted for 30.30% of the fiber optic pressure sensors market size in 2025; healthcare and medical devices are advancing at a 13.8% CAGR to 2031.

- By installation environment, down-hole and subsurface deployments captured 34.40% share of the fiber optic pressure sensors market size in 2025, whereas in-vivo biomedical use is set for a 14.2% CAGR through 2031.

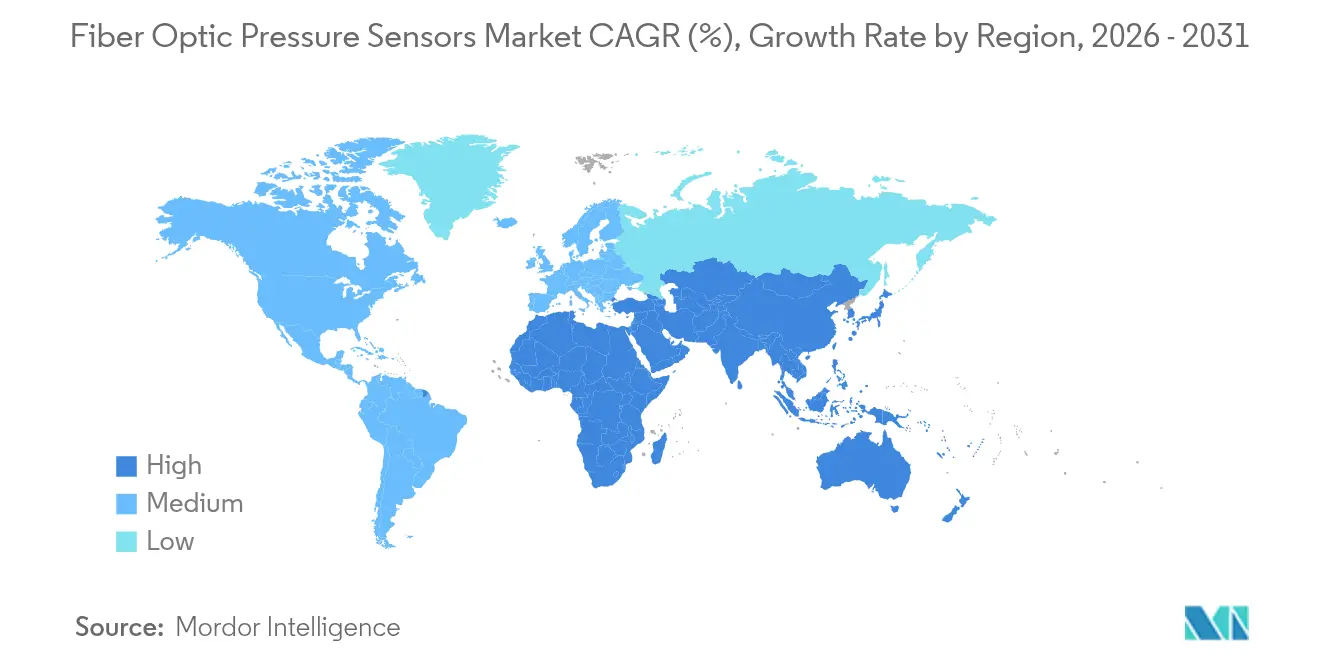

- By geography, North America dominated with 37.50% market share in 2025, yet Asia–Pacific is projected to grow the fastest at a 11.7% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fiber Optic Pressure Sensors Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rapid miniaturisation of Fabry-Perot MEMS cavities | 2.1% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Cost–down of distributed fiber-optic interrogation units | 1.8% | Global, accelerated in APAC manufacturing hubs | Short term (≤ 2 years) |

| OEM integration in EV battery-pack thermal-runaway safety | 1.5% | North America, EU, China EV manufacturing centers | Medium term (2-4 years) |

| Mandatory down-hole digitalisation targets (O&G) | 1.2% | Global O&G regions, concentrated in North America & Middle East | Long term (≥ 4 years) |

| Edge-analytics in smart factories (under-reported) | 0.9% | APAC industrial corridors, expanding to EU & North America | Medium term (2-4 years) |

| Implantable smart-catheter R&D funding spike (under-reported) | 0.7% | North America & EU medical device hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Miniaturization of Fabry-Perot MEMS Cavities

Mass-production lithography now delivers cavity dimensions below 10 µm while preserving ±0.01% full-scale accuracy. This leap enables pressure detection as low as 2 kPa in space-constrained medical devices, outperforming conventional polymer sensors by 80% sensitivity. Smaller cavities shorten response times and lower unit cost through wafer-level integration that follows silicon-photonics process flows. Miniature sensors now support catheter-based cardiovascular monitoring, high-speed aerospace actuation feedback, and embedded battery-cell diagnostics without compromising structural integrity. As production volumes climb, the wired and wireless segments of the fiber optic pressure sensors market both benefit from higher performance at reduced price per channel.[1]Photonics Media, “Tiny Pressure Sensor Measures Minute Changes Within the Body,” photonics.com

Cost-Down of Distributed Fiber-Optic Interrogation Units

The integration of silicon photonics has trimmed interrogation-unit pricing by roughly 60% since 2020, placing sub-nanometer wavelength resolution within reach of routine industrial budgets. Low-cost units now achieve 2.5 µε accuracy and sub-1 s response time, accelerating structural-health-monitoring adoption in bridges, tunnels, and pipelines. China leads global deployments with 11.3% share, validating cost competitiveness in large-scale smart-factory rollouts. Edge-analytics firmware further reduces data-backhaul needs, strengthening the value proposition in remote assets and boosting overall uptake of the fiber optic pressure sensors market.[2]Yandong Gong, “Investigation on Low Cost Optical Fiber Sensor Interrogator,” SpringerLink, link.springer.com

OEM Integration in EV Battery-Pack Thermal-Runaway Safety

Lab-on-fiber probes just 12 mm long and 125 µm in diameter track internal cell pressure and temperature during thermal runaway, offering advance warnings well before venting events. Their immunity to electromagnetic interference and corrosive electrolytes suits next-generation battery-management systems seeking improved safety compliance. Major automakers in North America, Europe, and China now trial embedded optical networks inside 18650 and pouch cells, pushing the fiber optic pressure sensors market deeper into the mobility ecosystem.

Mandatory Down-Hole Digitalization Targets in Oil & Gas

Baker Hughes’ SureCONNECT FE system links optical gauges to electric completions without intervention, reducing rig time while withstanding 200 °C and 15,000 psi conditions. Bragg-grating arrays measure pressure, temperature, and multiphase flow in real time, supporting production optimization mandates across tight reservoirs. As Middle-East producers pursue reservoir-management targets, adoption underpins long-term growth for the fiber optic pressure sensors market.[3]Baker Hughes, “Distributed Temperature Sensing (DTS),” bakerhughes.com

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High ASP vs piezo-resistive sensors | -1.4% | Global, particularly pronounced in price-sensitive APAC markets | Short term (≤ 2 years) |

| Connector standard-isation lag in subsea systems | -0.8% | Offshore regions, concentrated in North Sea & Gulf of Mexico | Medium term (2-4 years) |

| Scarcity of opto-qualified technicians (under-reported) | -0.6% | Global, acute in emerging markets and specialized applications | Long term (≥ 4 years) |

| IP fragmentation around micro-cavity designs (under-reported) | -0.4% | Global, affecting innovation-driven markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High ASP Versus Piezo-Resistive Sensors

A 2–3 × unit-price premium persists, particularly in multi-sensor industrial automation projects where budget ceilings remain strict. Specialized interrogation hardware inflates capital cost compared to simple strain-gauge conditioners. Yet maintenance savings in corrosive or high-temperature sites offset initial spend over asset life cycles, encouraging gradual substitution. Silicon-photonics scale-up is expected to shrink the gap to near parity in high-volume lines by 2028, easing this restraint on the fiber optic pressure sensors market.

Connector Standardization Lag in Subsea Systems

Proprietary wet-mate connectors hinder interoperability and raise qualification expenses in deepwater fields. Each bespoke design demands exhaustive testing to assure leak-proof performance at depth, delaying deployments and discouraging multi-vendor integration. Industry consortia now draft common interface guidelines, while suppliers such as Baker Hughes promote modular wet-connect platforms that remove multiple penetrations and improve reliability. As standards mature, subsea adoption barriers will ease, lifting prospects for the fiber optic pressure sensors market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Wired Dominance Drives Infrastructure Reliability

Wired devices represented 72.20% of revenue in 2025, cementing their role in high-integrity assets such as downhole completions, pipeline corridors, and industrial furnaces. The fiber optic pressure sensors market size for wired units is projected to rise steadily alongside refinery upgrades and LNG terminal expansions. Physical connectivity guarantees signal integrity across kilometers of fiber in environments where wireless propagation is unreliable.

Wireless nodes, growing at a 11.6% CAGR, address installations where cabling adds weight, complexity, or safety risk. Implantable medical devices, battery cells, and rotating machinery capitalize on battery-free passive tags interrogated asynchronously. Continuous cost declines in ultra-low-power optical interrogators widen the addressable base beyond early adopters, lifting overall demand within the broader fiber optic pressure sensors market. [3]Baker Hughes, “Distributed Temperature Sensing (DTS),” bakerhughes.com.

By Technology: Fabry–Perot Leadership Faces FBG Challenge

Fabry–Perot sensors held 46.40% revenue share thanks to sub-milli-bar resolution and robustness at 200 °C. Their micro-cavity designs, now below 10 µm, allow integration in hypodermic needles and narrow geological perforations, reinforcing leadership within the fiber optic pressure sensors market share.

FBG arrays, however, will expand the fastest at 12.9% CAGR. A single fiber multiplexes hundreds of gratings, trimming per-point cost for structural-health-monitoring and long-haul pipeline projects. High-speed demodulators achieve ±1 pm stability, enhancing earthquake-resilient building surveillance and high-rise wind-load analysis. As interrogation costs fall, FBG uptake moderates Fabry–Perot dominance while enlarging total addressable revenue for the fiber optic pressure sensors market.

By Application: Oil & Gas Dominance Challenged by Healthcare Growth

Oil and gas operations controlled 30.30% of 2025 revenue, driven by mandatory downhole sensing in unconventional wells and mature offshore fields. Systems logging pressure and temperature at 10,000 ft depth underpin dynamic reservoir models, anchoring the fiber optic pressure sensors market size to energy-sector budgets.

Healthcare grows at 13.8% CAGR, pulling optical sensors into minimally invasive surgeries, smart catheters, and continuous cardiac monitoring. Biocompatible coatings and EMI immunity allow safe in-body deployment where electronics would pose rejection risks. Advanced cardiac mapping catheters rely on 80% higher sensitivity than polymer sensors, underscoring new frontiers for the fiber optic pressure sensors market.

By Installation Environment: Down-Hole Applications Lead Specialized Deployments

Down-hole installations delivered 34.40% of 2025 revenue due to stringent reliability requirements in wells hotter than 200 °C and pressures beyond 15,000 psi. The wired architecture remains preferred for its immunity to electromagnetic disturbances from drilling operations. Real-time analytics optimize artificial-lift settings and fracture-stimulation schedules, sustaining the core of the fiber optic pressure sensors market.

In-vivo biomedical settings record the fastest 14.2% CAGR. Ultra-thin probes inform surgeons of localized pressure changes during endovascular repairs, enhancing procedural outcomes. Similarly, aerospace and UAV sectors embed optical gauges to measure cabin pressure and fuel-line transients under high vibration, exploiting low mass and EMI immunity advantages. These diverse environments collectively extend the reach of the fiber optic pressure sensors market.

Geography Analysis

North America led with 37.50% revenue in 2025, supported by rigorous safety codes across shale plays and expanding EV battery plants. Federal incentives for advanced manufacturing and the presence of oilfield service majors foster rapid prototyping and early commercial launches. Aerospace programs also adopt optical gauges for flight-critical systems, reinforcing the region’s innovation edge within the fiber optic pressure sensors market.

Asia–Pacific posts the strongest 11.7% CAGR to 2031. China’s 11.3% share of global distributed sensing deployments evidences government-driven smart-factory rollouts. Japan’s precision automotive giants integrate optical sensors in battery cooling loops, while India’s refinery expansions demand high-temperature gauging. Regional cost advantages in silicon photonics accelerate interrogation-unit output, broadening domestic availability and stimulating overall growth in the fiber optic pressure sensors market.

Europe records stable uptake anchored in automotive manufacturing, petrochemical processing, and offshore wind. Germany’s 9.4% share of global optical deployments reflects long-standing leadership in industrial automation. United Kingdom subsea operators embrace wet-mate optical connectors for a new wave of North Sea life-extension projects. France’s aerospace sector increasingly favors optical arrays for real-time structural diagnostics, adding to steady momentum across the fiber optic pressure sensors market.

Competitive Landscape

The market remains moderately fragmented, with no player exceeding a one-third share. Broad-portfolio service giants such as Baker Hughes, Halliburton, and Schlumberger bundle downhole optical gauges with integrated reservoir management, leveraging global fleets and high-pressure qualification laboratories. Specialized firms Luna Innovations and Opsens capitalize on high-precision medical and aerospace niches where sub-millibar resolution is essential.

Recent shifts indicate sharpening focus. Luna Innovations divested non-core assets to center on optical technology and expanded capacity in Atlanta to fulfill rising EV battery orders. Baker Hughes unveiled SureCONNECT FE, blending fiber arrays with intelligent completions to cut intervention costs. Nokia’s acquisition of Infinera extended silicon-photonics depth, promising lower interrogation costs for industrial-grade deployments.

Standard-interface momentum could reshape vendor dynamics. Providers offering interoperable wet-connect solutions and modular interrogation firmware may capture platform leadership as customers seek vendor-agnostic ecosystems. Conversely, IP fragmentation around micro-cavity designs could segment the fiber optic pressure sensors market into application-specific silos, sustaining price premiums in specialized medical and aerospace domains.

Fiber Optic Pressure Sensors Industry Leaders

Schlumberger Limited (SLB)

AP Sensing GmbH

Opsens Inc.

Luna Innovations Incorporated (incl. FISO Technologies)

Halliburton Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Baker Hughes launched SureCONNECT FE, the first commercially available downhole fiber-optic wet-connect system designed to optimize reservoir performance with real-time data insights. The system enables fiber-optic monitoring and electric intelligent completion systems without intervention, reducing rig time and maintenance costs while enhancing safety in complex wells and subsea operations.

- January 2025: Luna Innovations announced significant growth in bookings and revenue, particularly in the second half of 2024, driven by advancements in their fiber optic sensing products. The company's Atlas Interrogation Unit, utilizing Distributed Acoustic Sensing Technology, gained traction in critical infrastructure projects.

- January 2025: Luna Innovations completed the divestiture of Luna Labs division to concentrate on fiber optic-based technologies, with CEO Scott Graeff emphasizing the move simplifies their portfolio and allows focus on core fiber optics markets.

- January 2025: Luna Innovations secured a major order for THz sensing solutions used in electric vehicle battery production, transferring production to its Atlanta facility and increasing capacity by four times to meet growing demand.

Global Fiber Optic Pressure Sensors Market Report Scope

Fiber optic pressure sensors are used to provide accurate pressure measurement in harsh environments. Over the past few years, optical fibers have seen significant inroads across various sensor applications, owing to their small size and ability to transmit huge amounts of data. The market report offers insights into the application segment, such as automotive, consumer electronics, healthcare, industrial, oil and gas, petrochemical, etc.

| Wired |

| Wireless |

| Fabry-Perot |

| Fiber Bragg Grating |

| Intensity-Based |

| Other Technologies |

| Oil and Gas |

| Industrial Automation |

| Healthcare and Medical Devices |

| Automotive and Mobility |

| Consumer Electronics |

| Petrochemical |

| Other Applications |

| Down-hole / Sub-surface |

| Industrial Surface Plants |

| In-vivo / Biomedical |

| Aerospace and UAV |

| Marine and Subsea Structures |

| North America | United States |

| Canada | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC Countries |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Wired | |

| Wireless | ||

| By Technology | Fabry-Perot | |

| Fiber Bragg Grating | ||

| Intensity-Based | ||

| Other Technologies | ||

| By Application | Oil and Gas | |

| Industrial Automation | ||

| Healthcare and Medical Devices | ||

| Automotive and Mobility | ||

| Consumer Electronics | ||

| Petrochemical | ||

| Other Applications | ||

| By Installation Environment | Down-hole / Sub-surface | |

| Industrial Surface Plants | ||

| In-vivo / Biomedical | ||

| Aerospace and UAV | ||

| Marine and Subsea Structures | ||

| By Geography | North America | United States |

| Canada | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC Countries | |

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the fiber optic pressure sensors market?

The market stood at USD 4.15 billion in 2026 and is projected to reach USD 6.48 billion by 2031.

Which technology segment will grow the fastest?

Fiber Bragg Grating sensors are expected to record a 12.9% CAGR, outpacing other technologies thanks to multiplexing advantages.

Why are wireless optical pressure sensors gaining traction?

Wireless variants enable non-invasive monitoring in implantable medical devices and EV battery cells, supporting a 11.6% CAGR through 2031.

Which application dominates revenue today?

Oil and gas downhole monitoring leads with 30.30% revenue share because of mandatory digitalization targets.

Which region offers the highest growth potential?

Asia–Pacific is forecast to expand at a 11.7% CAGR through 2031, propelled by Chinese smart-factory and Japanese mobility initiatives.

What is the main hurdle to broader adoption?

A 2–3 × cost premium over piezo-resistive sensors remains the primary restraint, though the gap is narrowing as silicon-photonics scaling progresses.

Page last updated on: