Microbial Seed Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

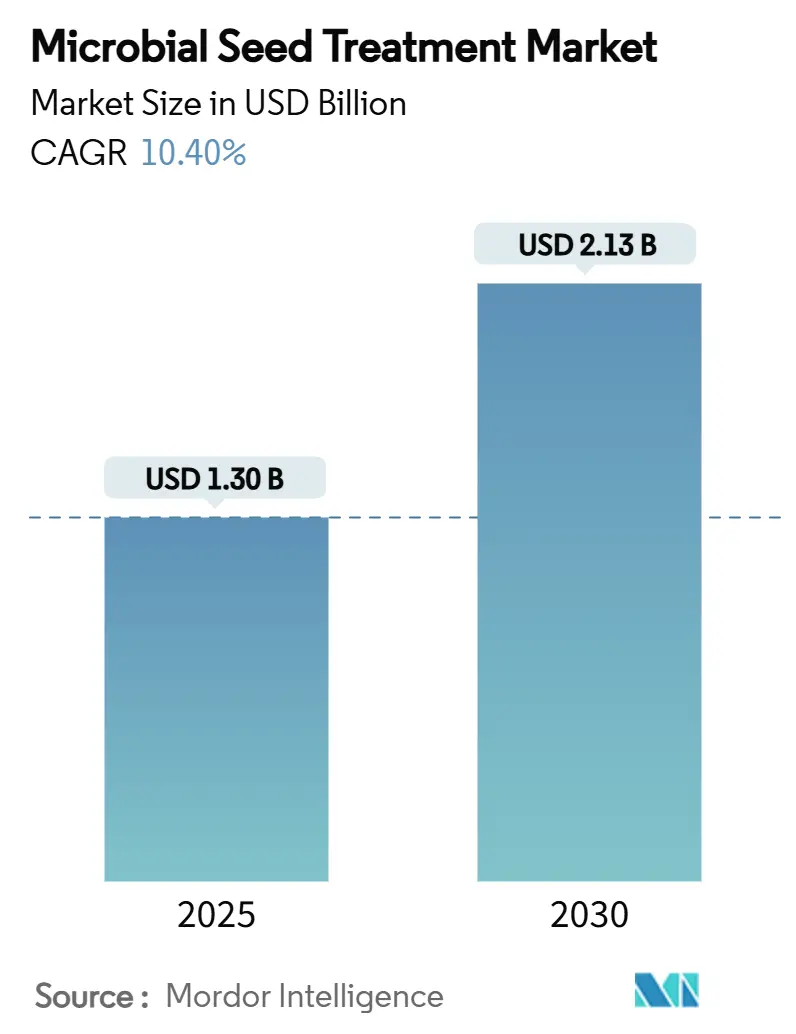

| Market Size (2025) | USD 1.30 Billion |

| Market Size (2030) | USD 2.13 Billion |

| Growth Rate (2025 - 2030) | 10.40% CAGR |

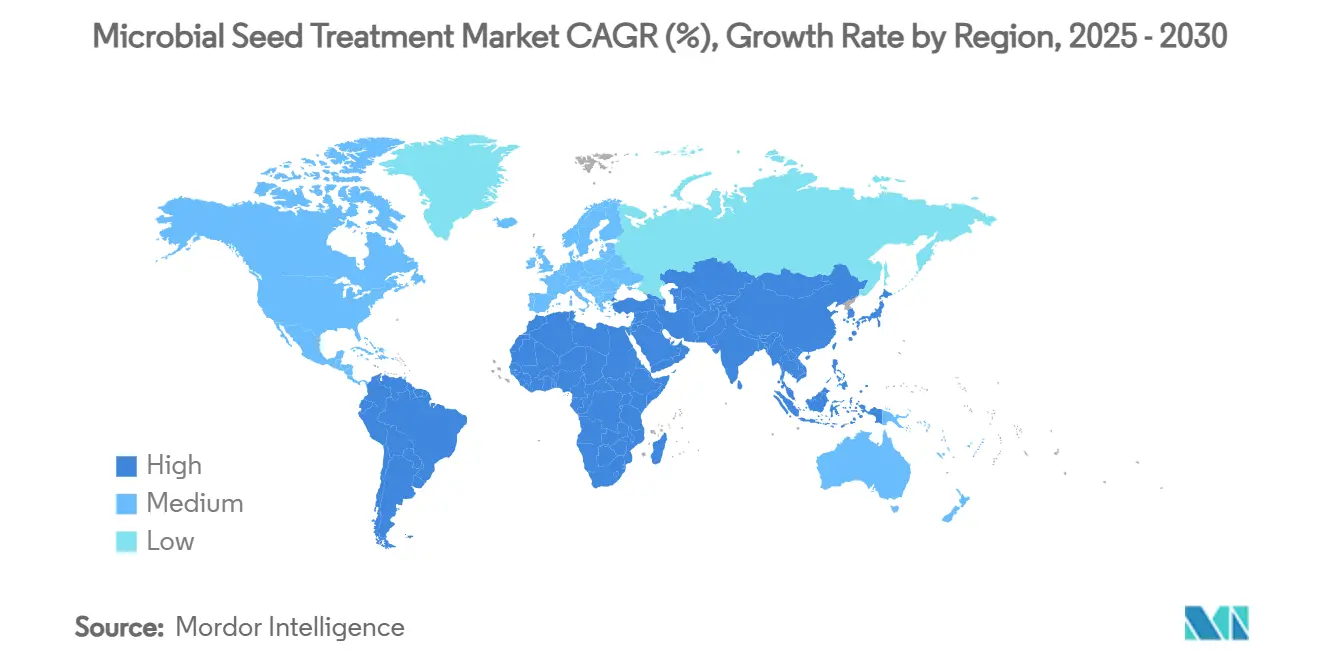

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Microbial Seed Treatment Market Analysis by Mordor Intelligence

The microbial seed treatment market size reached USD 1.30 billion in 2025 and is projected to reach USD 2.13 billion by 2030, advancing at a 10.4% CAGR from 2025 to 2030. Growing regulatory restrictions on synthetic crop-protection chemicals, consumer preference for residue-free food, and technology improvements in microbial formulation continue to accelerate adoption. Established players are broadening biological portfolios to hedge against tightening residue limits, while regional governments finance bio-input programs that reduce reliance on chemical pesticides. Expansion is further reinforced by rising genetically modified (GM) seed prices, which heighten growers’ interest in treatments that safeguard high-value seed lots. North America maintains the largest share due to its mature seed treatment infrastructure. However, the Asia-Pacific region is posting the strongest growth, driven by policy initiatives and the rapid commercial adoption of biological inputs.

Key Report Takeaways

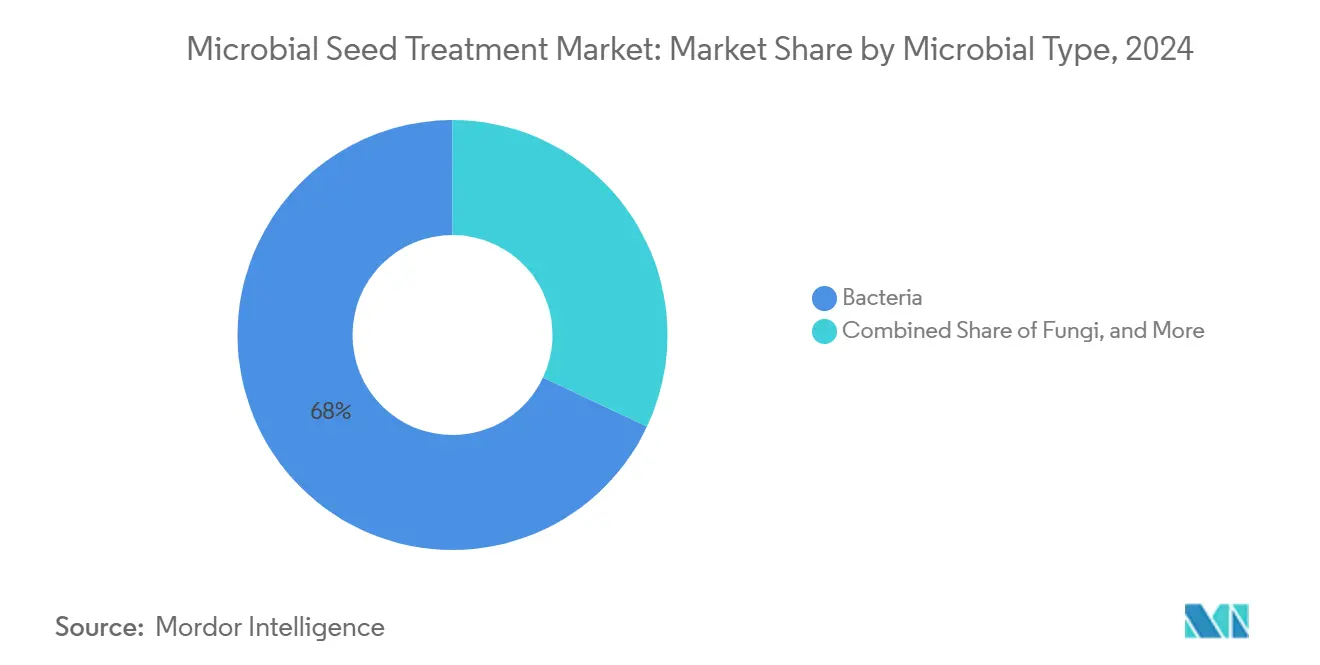

- By microbial type, bacteria led with 68% of the microbial seed treatment market share in 2024, and the fungi segment is forecast to expand at an 11.2% CAGR through 2030.

- By crop type, cereals and grains commanded a 43% share of the microbial seed treatment market size in 2024, and fruits and vegetables represent the fastest-growing crop segment with a 12% CAGR to 2030.

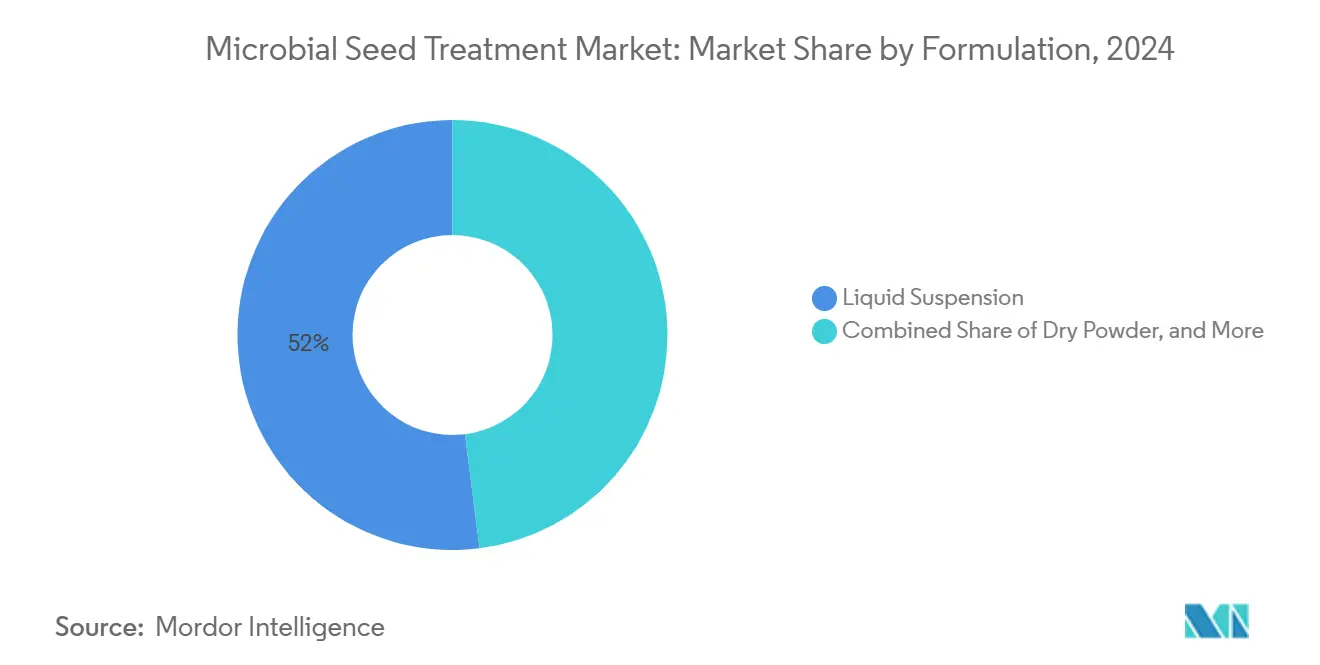

- By formulation, liquid suspensions held 52% of the microbial seed treatment market share in 2024, while encapsulated granules posted the highest projected growth at an 11.5% CAGR through 2030.

- By geography, North America captured 34% of the microbial seed treatment market size in 2024, and Asia-Pacific is advancing at a 12.1% CAGR over 2025-2030.

Global Microbial Seed Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for sustainable agriculture | +3.2% | North America and Europe strongest, and global adoption is broadening | Medium term (2-4 years) |

| Escalating genetically modified seed prices | +2.8% | Pronounced in North and South America | Short term (≤ 2 years) |

| Stricter regulations on chemical residues | +2.5% | Europe and North America are leading, and Asia-Pacific is catching up. | Long term (≥ 4 years) |

| Mainstream adoption of biological seed coatings | +2.1% | North America and Europe's core emerging markets are rising. | Medium term (2-4 years) |

| Carbon-credit incentives for biologically treated seeds | +1.8% | Pilot programs in North America and Europe, global expansion projected. | Long term (≥ 4 years) |

| AI-enabled microbial strain discovery | +1.4% | Technology hubs across North America, Europe, and the Asia-Pacific. | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Sustainable Agriculture

The demand for sustainable agriculture is driving rapid adoption of microbial seed treatments as growers, retailers, and processors aim to align with regenerative farming goals. Retail chains and food processors increasingly require verified biological treatment protocols to ensure environmental compliance, traceability, and adherence to residue standards. This has encouraged growers to integrate microbial seed treatments that support soil health while improving crop performance. Research-backed trials show that fungal endophytes and other microbial inoculants enhance soil organic carbon and root-zone biodiversity, contributing to both yield stability and long-term land productivity. Certification programs and traceability systems are further institutionalizing biological seed treatments, especially in premium produce supply chains.

Escalating Genetically Modified Seed Prices

The rising cost of genetically modified (GM) seeds, often priced at three to four times higher than conventional alternatives, has significantly heightened the importance of yield protection strategies. Growers are increasingly turning to microbial seed treatments to safeguard these high-value inputs from early-season losses caused by abiotic stress and soil pathogens. Nitrogen-fixing microbial inoculants, for example, are gaining traction due to their ability to provide nutrient support while stabilizing seedling emergence. Two-year on-seed stability offered by some modern microbial products helps reduce stand losses, especially in variable field conditions. This cost-benefit dynamic makes microbial protection an economically viable choice for safeguarding premium seed lots.

Stricter Regulations on Chemical Residues

Tighter global regulations on agrochemical residues are accelerating the transition to biological seed treatments. In the European Union, recent environmental directives have restricted the use of microplastics and synthetic seed coatings, pushing the industry toward biodegradable and nutrient-enriched alternatives. Seed treatment manufacturers are now developing biologically compatible coatings that comply with evolving standards while delivering essential micronutrients and beneficial microbes. Similar policy shifts are occurring in North America, where multiple microbial strains such as Bacillus and Trichoderma have received regulatory exemptions, reflecting their environmental safety and low residue impact[1]Source: Environmental Protection Agency, “Bacillus Subtilis Strain CH4000; Exemption From the Requirement of a Tolerance,” Federal Register, federalregister.gov. These changes are reinforcing microbial adoption in commercial seed treatment protocols.

Mainstream Adoption of Biological Seed Coatings

Biological seed treatments are becoming mainstream as major seed producers integrate microbial solutions directly into film-coat formulations. This shift eliminates the need for additional on-farm application, improving ease of use for growers while ensuring consistent product performance. Seed companies are now embedding nitrogen-fixing bacteria and other beneficial microbes within polymer matrices, enabling controlled release and uniform coverage. Industrial-scale processing reduces per-unit treatment costs and enhances shelf life, making biologically enhanced seeds viable for large-scale distribution. As a result, microbial seed treatments are evolving from niche inputs into standard components of commercial seed systems across a range of high-value crops.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low farmer awareness in emerging economies | -2.1% | Asia-Pacific, Africa, parts of South America | Medium term (2-4 years) |

| Inconsistent field performance across geographies | -1.8% | Global, variable climates most affected | Short term (≤ 2 years) |

| Cold-chain gaps for liquid microbial formulations | -1.5% | Emerging markets with limited infrastructure | Medium term (2-4 years) |

| Regulatory ambiguity on living modified microbes | -1.2% | Worldwide, differing regional rules | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Low Farmer Awareness in Emerging Economies

Limited awareness and technical knowledge continue to restrict the adoption of microbial seed treatments among smallholder farmers in emerging economies. Many growers remain unfamiliar with the specific benefits of microbial strains, optimal application timing, and the importance of on-seed microbial stability. Although some growth in biopesticide and biofertilizer usage is evident, adoption is still largely confined to larger or more commercially connected farms. To close this gap, localized agricultural extension programs that showcase the economic benefits of staple crops are vital for building trust and encouraging widespread usage across rural regions.

Inconsistent Field Performance Across Geographies

Microbial seed treatments often show variable results across different geographic and climatic conditions due to the influence of local soil pH, moisture levels, and native microbial populations. While certain strains, such as Trichoderma harzianum, demonstrate proven stress-mitigation properties, their impact on yield may fluctuate significantly based on environmental conditions. These inconsistencies can deter farmer confidence and limit repeat adoption. To overcome this, ongoing innovations focus on strain optimization, predictive field modelling, and the development of region-specific advisory tools to ensure more consistent and reliable field performance in diverse agroecological zones.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Microbial Type: Bacillus Dominance Drives Innovation

Bacteria held a 68% market share in the microbial seed treatment market in 2024, and fungi are forecasted to grow at the fastest rate, with a 11.2% CAGR through 2030. Multiple 2024 and 2025 Environmental Protection Agency (EPA) exemptions confirm regulatory confidence in Bacillus spores’ safety[2]Source: Environmental Protection Agency, “40 CFR 180.1383 — Bacillus velezensis Strain RTI301; Exemption,” ecfr.gov. The microbial seed treatment market is witnessing rapid growth in Bacillus-based formulations, primarily due to their exceptional stability, long shelf life, and broad-spectrum activity against a wide range of soil-borne pathogens. These traits make Bacillus strains particularly well-suited for large-scale commercial agriculture, where consistent performance and logistics are crucial. Their ability to thrive across diverse environmental conditions further supports the widespread deployment of this technology across major crop categories. As a result, Bacillus species are emerging as a foundational component in many next-generation biological seed treatments.

Fungi represent the fastest-growing segment in microbial seed treatments, supported by their unique biocontrol properties, particularly in suppressing fungal pathogens such as Fusarium, Rhizoctonia, and Pythium. Species like Trichoderma are increasingly integrated into seed treatment protocols for high-value crops due to their ability to promote root development and stress resilience. Although currently smaller in scale, other microbial categories, including viruses, actinomycetes, and protozoa, are being explored for future use, primarily in specialized formulations. These emerging subsegments offer novel mechanisms of action and are likely to complement bacteria and fungi in multi-strain consortia designed to enhance field consistency and crop performance.

By Crop Type: Cereals and Grains Lead Volume While Specialty Crops Drive Value

Cereals and grains dominated 43% of the microbial seed treatment market size in 2024, benefiting from extensive acreage and accepted seed treatment routines. Fruits and vegetables, while smaller, post the fastest 12% CAGR to 2030, leveraging premium price points and strict residue limits. The widespread adoption of conventional seed treatment practices in these crops creates a natural entry point for microbial products, particularly those that offer enhanced stress tolerance and nutrient uptake. Large-scale growers and seed companies increasingly view microbial inoculants as a sustainable complement to existing chemical treatments, especially in regions facing tightening residue regulations.

Specialty crops such as fruits and vegetables, though cultivated on comparatively smaller acreage, are emerging as high-value drivers of microbial seed treatment adoption. Their premium market prices, coupled with stringent maximum residue limits and consumer demand for clean-label produce, make biological solutions particularly attractive. Microbial treatments in these crops support early root development, disease resistance, and resilience against abiotic stress. Oilseeds and pulses are also gaining traction, with dual-inoculation techniques in legumes like faba bean showing significant yield improvements in field trials. In rice-based systems, particularly across the Asia-Pacific region, microbiome engineering efforts are opening new frontiers by reducing reliance on synthetic inputs and improving climate adaptability through targeted microbial interventions.

By Formulation: Liquid Suspension Dominance Faces Encapsulation Challenge

Liquid suspensions captured 52% of the microbial seed treatment market share in 2024, supported by compatibility with commercial application lines. Encapsulated granules, however, are projected to grow at an 11.5% CAGR through 2030 as they protect microbes from heat and ultraviolet degradation, critical in markets with weak cold-chain infrastructure. Dry powders maintain a significant share, valued in regions with ambient storage. Novel film-coat systems embed microbes in polymer matrices, endorsed by Evonik's silica carrier technology that shelters Gram-negative strains.

The growing diversity of formulation types reflects regional adaptation needs and advancements in microbial stabilization technologies. Liquid suspensions remain popular due to ease of mixing, even coverage on seeds, and integration with automated seed treatment equipment. However, in tropical and remote regions, where microbial viability is threatened by high temperatures and poor storage conditions, encapsulated granules and film-coated systems are gaining favor. These innovations not only extend shelf life but also improve microbial activation timing in the soil. The development of carrier systems that protect more sensitive microbial classes, such as Gram-negative bacteria, marks a significant leap in formulation science, paving the way for broader adoption across variable supply chains and climatic zones.

Geography Analysis

North America accounted for about 34% of the microbial seed treatment market size in 2024, supported by advanced seed treatment lines, strong extension services, and rapid regulatory clearance for new strains. Environmental Protection Agency (EPA) tolerance exemptions in 2024 and 2025 lowered barriers for commercial launches. Uptake in the United States and Canada focuses on corn, soybean, and canola, where biological solutions complement Genetically Modified (GM) traits. Nevertheless, growth cools slightly as market maturity approaches.

Asia-Pacific posts the highest CAGR of 12.1% through 2030, propelled by policy programs converting growers to biological inputs. China’s green channel speeds approvals, and local manufacturers scale domestic strains, especially Bacillus[3]Source: CIRS Group, “China Microbial Pesticide Registration,” cirs-group.com. India’s National Bio-inputs Program funds demonstration farms that showcase yield gains, narrowing awareness gaps. Australia and Japan advance through research collaborations that integrate microbial solutions with precision planting. Europe’s stringent residue legislation stimulates demand. The upcoming 2027 microplastics ban drives investment in biodegradable coatings, giving European suppliers a formulation edge. Germany and France allocate research budgets to accelerate biological efficacy validation, while Eastern Europe represents an emerging frontier for microbial seed treatment market penetration.

South America, led by Brazil and Argentina, steadily increases adoption as integrated pest management gains trust. Brazil’s bio-input growth reflects cost savings in soybean and corn production, where microbial nitrogen fixation offsets fertilizer spending. The region seeks cold-chain-free formulations to overcome distribution challenges across vast agricultural frontiers. Africa and the Middle East remain nascent but show long-term potential. Pilot programs in Kenya and South Africa evaluate consortia that improve drought tolerance in maize, linking microbial adoption to food-security goals. Middle East greenhouse horticulture offers a niche early-adopter segment seeking residue-free solutions for export compliance.

Competitive Landscape

The microbial seed treatment market shows a moderately concentrated structure in 2024, with the top five leading players accounting for about 54% of the microbial seed treatment market. Bayer AG remains a dominant force, leveraging its proprietary seed brands and extensive supply networks. BASF SE integrates microbial seed treatments into its expansive crop protection and biologicals portfolio. Syngenta Group has expanded its presence through strategic partnerships, including a recent collaboration with Intrinsyx Bio focused on enhancing nitrogen-use efficiency. Corteva Agriscience and Valent BioSciences also hold strong positions, supported by active R&D pipelines and global crop-specific initiatives.

Competitive dynamics are intensifying as major firms refine their microbial portfolios and pursue targeted partnerships. Syngenta Group's divestment of its FarMore vegetable seed treatment platform to Gowan SeedTech allows greater focus on advanced coating technologies and microbial integration. Indigo Ag has continued expanding its biotrinsic line, pairing seed-applied microbes with digital decision tools.

Innovation in the market is shaped by microbial strain libraries, proprietary formulation techniques, and seed delivery mechanisms. Novonesis Group, building on Novozymes’ legacy, focuses on long-shelf-life inoculants with proven compatibility across seed types. Koppert continues to scale solutions targeting disease suppression through competitive exclusion. Evogene is working at the frontier of microbial discovery, using genomics and synthetic biology to enhance performance. Companies that develop robust, multi-strain products with consistent field efficacy across diverse geographies are best positioned to lead as microbial seed treatment solutions become more mainstream.

Microbial Seed Treatment Industry Leaders

BASF SE

Corteva Agriscience

Bayer AG

Syngenta Group

Novonesis Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: BioConsortia partnered with Hodder & Taylor to introduce its nitrogen‑fixing microbial seed treatment FixiN 33 for corn, cereals, and brassicas in New Zealand. The product offers enhanced shelf life (~2+ years) and reduced reliance on synthetic nitrogen, demonstrating performance across global field trials.

- December 2024: Syngenta Group divested its FarMore vegetable seed treatment platform to Gowan SeedTech LLC. The move allows Syngenta Group to focus on next-gen biological coatings, while Gowan expands its presence in precision vegetable seed treatments. This reflects ongoing specialization in the microbial seed treatment market.

- July 2024: Evonik launched a biobased carrier system that improves the shelf life of Gram-negative bacteria in liquid microbial seed treatments. This advancement enhances formulation stability, enabling wider use of sensitive strains. It supports market growth by improving product reliability across diverse storage conditions.

Global Microbial Seed Treatment Market Report Scope

| Bacteria | Bacillus spp. |

| Rhizobium spp. | |

| Pseudomonas spp. | |

| Paenibacillus spp. | |

| Streptomyces spp. | |

| Fungi | Trichoderma spp. |

| Penicillium spp. | |

| Aspergillus spp. | |

| Others (Viruses and Protozoa) |

| Cereals and Grains | Wheat |

| Corn | |

| Rice | |

| Oilseeds and Pulses | Soybean |

| Canola | |

| Fruits and Vegetables | Tomatoes |

| Potatoes | |

| Others (Forage, Turf, Ornamentals) |

| Liquid Suspension |

| Dry Powder |

| Encapsulated Granule |

| Others |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Microbial Type | Bacteria | Bacillus spp. |

| Rhizobium spp. | ||

| Pseudomonas spp. | ||

| Paenibacillus spp. | ||

| Streptomyces spp. | ||

| Fungi | Trichoderma spp. | |

| Penicillium spp. | ||

| Aspergillus spp. | ||

| Others (Viruses and Protozoa) | ||

| By Crop Type | Cereals and Grains | Wheat |

| Corn | ||

| Rice | ||

| Oilseeds and Pulses | Soybean | |

| Canola | ||

| Fruits and Vegetables | Tomatoes | |

| Potatoes | ||

| Others (Forage, Turf, Ornamentals) | ||

| By Formulation | Liquid Suspension | |

| Dry Powder | ||

| Encapsulated Granule | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the microbial seed treatment market in 2025?

The microbial seed treatment market size is USD 1.30 billion in 2025.

What CAGR is anticipated for microbial seed treatments through 2030?

The market is projected to expand at a 10.4% CAGR from 2025 to 2030.

Which region is growing fastest for microbial seed treatments?

Asia-Pacific shows the highest growth, advancing at 12.1% CAGR on policy support and rapid adoption in China and India.

What key factor drives farmers to adopt microbial seed treatments?

Rising GM seed prices encourage growers to protect high-value seed lots with biological treatments that enhance germination and vigor.

Page last updated on: