Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2017 - 2023 |

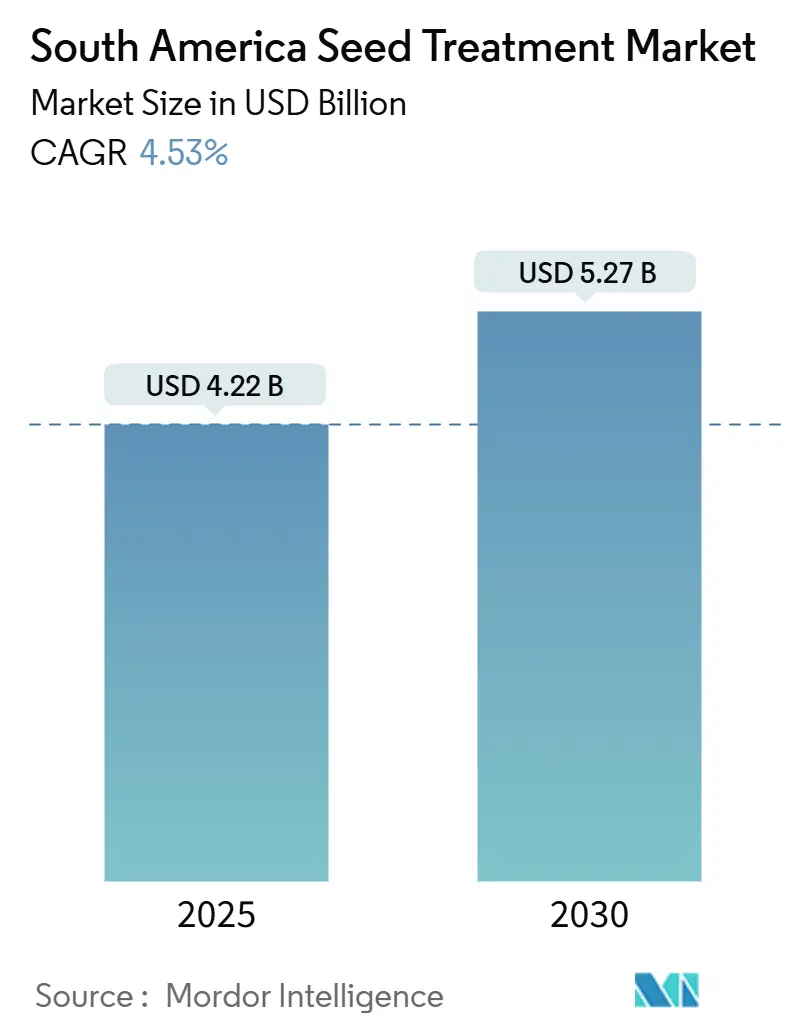

| Market Size (2025) | USD 4.22 Billion |

| Market Size (2030) | USD 5.27 Billion |

| Growth Rate (2025 - 2030) | 4.53% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Seed Treatment Market Analysis by Mordor Intelligence

The South America seed treatment market size reached USD 4.22 billion in 2025 and is forecast to hit USD 5.27 billion by 2030, expanding at a 4.53% CAGR. Expanding soybean cultivation, stringent sustainability mandates, and steady technology upgrades combine to lift demand for premium seed coatings across Brazil, Argentina, Chile, and neighboring producers. Growing adoption of drought-tolerant biotech seeds, wider IPM use, and the rise of crop protectants all reinforce the upward path for the South America seed treatment market. Government policies that restrict neonicotinoids are steering buyers toward selective chemistries, a trend anticipated to gather pace through the forecast horizon.

Key Report Takeaways

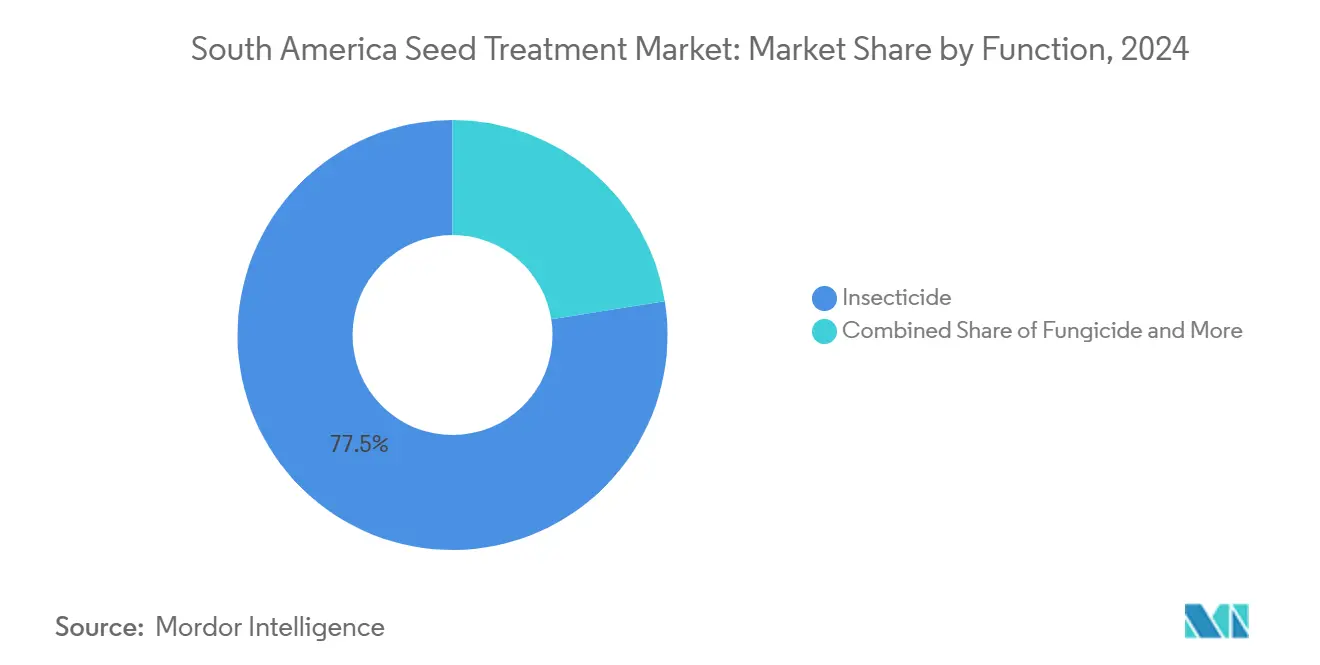

- By function, insecticide coatings led with 77.5% of the South America seed treatment market share in 2024, while the same segment is projected to post the fastest 4.61% CAGR through 2030.

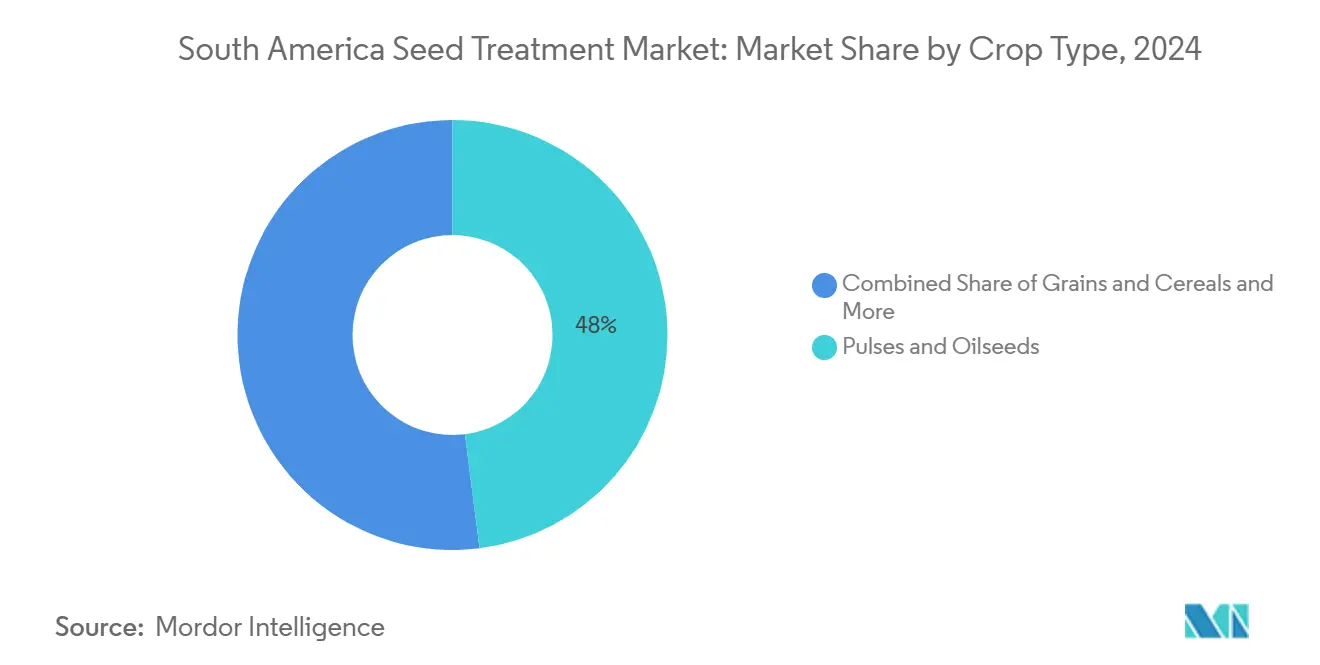

- By crop type, pulses and oilseeds captured 48.0% of revenue in 2024, while the segment is set to expand at a 4.71% CAGR through 2030.

- By geography, Brazil accounted for 91.5% of the South America seed treatment market size in 2024, whereas Chile is advancing at the fastest 5.44% CAGR through 2030.

South America Seed Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Widespread adoption of biotech drought-tolerant seeds | +0.8% | Brazil, Argentina, and Chile | Medium term (2-4 years) |

| Rising soybean acreage in Brazil and Argentina | +1.2% | Brazil, and Argentina | Short term (≤ 2 years) |

| Shift toward integrated pest-management programs | +0.9% | Global, strongest in Brazil and Argentina | Medium term (2-4 years) |

| Expansion of contract farming in South America | +0.6% | Brazil, Argentina, and Chile | Long term (≥ 4 years) |

| Emergence of biological seed coatings with nano-delivery systems | +0.7% | Brazil, Chile, spill-over to Argentina | Long term (≥ 4 years) |

| Digital agriculture platforms enabling prescription seed treatment | +0.5% | Brazil, Argentina, emerging in Chile | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Widespread Adoption of Biotech Drought-Tolerant Seeds

Drought-tolerant seed varieties require specialized protective coatings to maintain viability under water stress conditions, creating sustained demand for advanced seed treatment formulations. Brazil's adoption of drought-resistant soybean varieties increased by 23% in 2024, with these seeds requiring enhanced fungicidal and insecticidal protection during germination phases when plants are most vulnerable. The integration of biotechnology traits with precision seed treatments enables farmers to maintain productivity even during irregular rainfall patterns, which have become more frequent due to climate variability. Regulatory frameworks in Argentina now mandate specific seed treatment protocols for genetically modified drought-tolerant varieties, ensuring consistent field performance across diverse growing conditions. This trend is particularly pronounced in marginal growing areas where traditional varieties struggle, expanding the addressable market for premium seed treatment solutions.

Rising Soybean Acreage in Brazil and Argentina

Soybean cultivation expansion drives proportional increases in seed treatment demand, particularly for broad-spectrum insecticidal coatings that protect against early-season pests. Brazil planted 45.2 million hectares of soybeans in the 2024-2025 growing season, representing a 3.1% increase from the previous year, while Argentina expanded soybean area by 2.8% to 16.8 million hectares.[1]Source: National Supply Company, “Crop Production Estimates,” conab.gov.brEach hectare of soybean production typically requires 150-200 grams of seed treatment products, creating direct market expansion opportunities for manufacturers. The shift toward higher-yielding soybean varieties necessitates more sophisticated treatment protocols, including multi-active formulations that address region-specific pest complexes. Export-oriented production systems increasingly adopt standardized seed treatment protocols to meet international quality standards, particularly for shipments to European and Asian markets with strict residue tolerance levels.

Shift Toward Integrated Pest-Management Programs

Integrated pest management (IPM) adoption positions seed treatments as the foundational defense layer, reducing reliance on foliar applications while maintaining crop protection efficacy. Brazilian soybean producers implementing IPM protocols report 18% lower overall pesticide usage while maintaining equivalent yield protection, with seed treatments accounting for 35% of total crop protection value. This approach aligns with sustainability mandates from major commodity buyers, including Cargill and ADM, who require IPM compliance for premium contract pricing. Argentina's National Agricultural Technology Institute promotes IPM adoption through subsidized seed treatment programs, particularly targeting smallholder producers who previously relied heavily on calendar-based foliar spraying.[2]Argentine Ministry of Agriculture, “Agricultural Statistics,” magyp.gob.ar The regulatory environment increasingly favors IPM approaches, with tax incentives available for producers demonstrating reduced synthetic pesticide usage through enhanced seed treatment protocols.

Expansion of Contract Farming in South America

Contract farming arrangements standardize seed treatment protocols across consolidated production areas, creating predictable demand patterns for manufacturers while ensuring consistent crop protection outcomes. Large agribusiness companies like Amaggi and SLC Agricola now specify seed treatment requirements in their production contracts, covering over 2.3 million hectares in Brazil during 2024. These arrangements enable bulk purchasing of specialized treatment formulations, reducing per-unit costs while improving application consistency across contracted areas. Contract farming expansion is particularly pronounced in frontier agricultural regions where infrastructure development requires coordinated investment in seed treatment facilities and cold-chain logistics. The model facilitates technology transfer to smaller producers who gain access to premium seed treatment products through cooperative purchasing arrangements, expanding market penetration beyond traditional large-scale operations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing regulatory scrutiny on neonicotinoids | -0.9% | Brazil, Argentina, and Chile | Short term (≤ 2 years) |

| Volatility in active-ingredient prices | -0.6% | Global, strongest impact in Brazil and Argentina | Short term (≤ 2 years) |

| Limited cold-chain infrastructure for biological products | -0.4% | Chile, and Rest of South America | Medium term (2-4 years) |

| Farmer skepticism toward seed-treatment ROI in smallholder segments | -0.3% | Argentina, and Rest of South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Regulatory Scrutiny on Neonicotinoids

Regulatory restrictions on neonicotinoid insecticides are constraining seed treatment options, particularly for high-value crops where these actives historically provided reliable pest control. Brazil's Agência Nacional de Vigilância Sanitária(ANVISA) implemented usage limitations on clothianidin and thiamethoxam seed treatments in 2024, requiring mandatory buffer zones near pollinator habitats and restricting application rates on flowering crops. Chile's environmental ministry banned imidacloprid seed treatments for sunflower and canola production, affecting approximately 180,000 hectares of cultivation area. These restrictions create market opportunities for alternative chemistries and biological products, but transition periods often result in temporary yield losses while farmers adapt to new treatment protocols. The regulatory trend toward pollinator protection is accelerating across the region, with Argentina considering similar restrictions following European Union guidelines on neonicotinoid usage.

Volatility in Active-Ingredient Prices

Fluctuating costs of key active ingredients disrupt treatment formulation economics and create pricing uncertainty for both manufacturers and end-users. Global supply chain disruptions in 2024 increased prices for fungicidal actives like fludioxonil and metalaxyl by 15-25%, forcing seed treatment manufacturers to reformulate products or absorb margin pressure. Currency fluctuations compound price volatility, with the Brazilian real's depreciation against the US dollar increasing import costs for specialized active ingredients not produced domestically. Energy-intensive manufacturing processes for synthetic actives are particularly sensitive to petroleum price fluctuations, creating additional cost pressures that ultimately affect farmer adoption rates. Long-term supply contracts between manufacturers and active ingredient suppliers are becoming more common as a risk mitigation strategy, but these arrangements can limit flexibility in product formulation optimization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function: Insecticides Lead Amid Regulatory Transitions

Insecticide treatments dominate the South America seed treatment market with 77.5% market share in 2024, driven by increasing pest pressure from climate variability and expanding cultivation into marginal areas. This segment is projected to maintain the fastest growth at 4.6% CAGR through 2030, despite regulatory challenges affecting neonicotinoid actives. Fungicide treatments with steady demand from high-humidity growing regions where seed-borne diseases pose significant yield risks. Nematicide applications concentrated in areas with persistent soil-dwelling pest populations.

The regulatory landscape is reshaping functional segment dynamics, with Brazil's ANVISA implementing stricter guidelines for neonicotinoid seed treatments in 2024, particularly affecting clothianidin and thiamethoxam applications. [3]Source: ANVISA, “Pesticide Registration Guidelines,” gov.br/anvisa In response to mounting regulatory pressures, companies are ramping up investments in alternative insecticidal chemistries. The shift toward integrated pest management approaches is creating demand for multi-functional seed treatment formulations that combine insecticidal, fungicidal, and plant growth-promoting properties in single applications, improving cost-effectiveness for producers while maintaining comprehensive crop protection.

By Crop Type: Pulses and Oilseeds Drive Market Expansion

Pulses and oilseeds represent the largest crop segment with 48.0% market share in 2024, reflecting South America's position as the global center for soybean production and export. The segment acceleration indicates market expansion driven by increasing global demand for plant-based proteins and sustainable agricultural practices. This segment maintains the fastest growth rate at 4.7% CAGR through 2030, supported by the continued expansion of soybean cultivation in Brazil and Argentina. Grains and cereals, with corn and wheat production, are driving demand for broad-spectrum seed treatments that address region-specific pest complexes. Fruits and vegetables are concentrated in Chile and specialized production areas where high-value crops justify premium treatment costs.

Commercial crops, including sugarcane, cotton, and tobacco, are driven by export-oriented production systems that require standardized treatment protocols to meet international quality standards. Turf and ornamentals primarily serve urban landscaping and recreational facility markets in major metropolitan areas. Brazil's National Supply Company projects soybean area expansion of 2.5% annually through 2030, directly supporting seed treatment market growth in the dominant crop segment.

Geography Analysis

Brazil dominates the South America seed treatment market with 91.5% share in 2024, reflecting its position as the world's largest soybean producer and a major corn cultivation region. Chile demonstrates the fastest growth at 5.4% CAGR through 2030, reflecting government initiatives promoting sustainable agriculture and export diversification. Brazil's market is supported by continued agricultural expansion into the Cerrado region and increasing adoption of precision farming technologies. Brazil's regulatory framework, managed by ANVISA and the Ministry of Agriculture, provides clear approval pathways for both synthetic seed treatments, encouraging innovation investment by multinational companies.

Argentina is driven by soybean area recovery following favorable policy changes and improved export infrastructure. The country's seed treatment market benefits from established agricultural extension services and high farmer education levels, facilitating adoption of advanced treatment technologies.

Chile's distinct climate and regulatory landscape position it as a global hub for high-value seed multiplication, both GM and non-GM, necessitating sophisticated seed treatments. Chile's seed treatment market benefits from advanced cold-chain infrastructure and proximity to export ports, supporting adoption of temperature-sensitive products. The Rest of South America, including Uruguay, Paraguay, and smaller agricultural economies, accounts for the minimal market share, with growth driven by increasing mechanization and integration with regional agricultural value chains.

Competitive Landscape

The South America seed treatment market is moderately concentrated, with Syngenta Group, Bayer AG, Corteva Agriscience, UPL Limited, and BASF SE securing nearly 37.2% combined revenue in 2024, an oligopolistic setup that funds aggressive R&D while leaving room for specialized challengers. Syngenta is leveraging broad chemistry access and deep distribution of its products. Bayer and Corteva integrate digital agronomy platforms, linking seed genetics, coating prescriptions, and field analytics to lock in customer loyalty.

In UPL, ProNutiva melds natural biosolutions with traditional crop protection methods, striving to boost crop safety, achieve elevated yields, and improve quality. BASF received ANVISA clearance for a tropical fungicidal active in late 2024, underscoring a pivot toward region-specific chemistry. Smaller innovators target white-space niches, notably micro-encapsulation and localized microbes, where speed and agility offset the giants’ scale.

Strategic focus now centers on bundled offerings that marry premium coatings, data analytics, and sustainability verification, satisfying commodity traders that reward traceable low-residue produce. Cross-licensing deals appear likely as leading firms try to blend proprietary microbes with proven chemistries, spreading regulatory risk and capturing premium demand from global buyers.

South America Seed Treatment Industry Leaders

BASF SE

Bayer AG

Corteva Agriscience

Syngenta Group

UPL Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Syngenta Group launched TYMIRIUM technology in Paraguay; field trials in soybean showed 10–12% yield improvement while controlling nematodes and early foliar diseases.

- August 2025: Corteva Agriscience introduced Lumidapt Valta LS, a nutritional, naturally-derived seed treatment aimed at enhancing corn emergence. This product is designed to support healthy seedling development and improve early plant vigor.

South America Seed Treatment Market Report Scope

Function

| Fungicide |

| Insecticide |

| Nematicide |

Crop Type

| Commercial Crops |

| Fruits & Vegetables |

| Grains & Cereals |

| Pulses & Oilseeds |

| Turf & Ornamental |

Country

| Argentina |

| Brazil |

| Chile |

| Rest of South America |

| Function | Fungicide |

| Insecticide | |

| Nematicide | |

| Crop Type | Commercial Crops |

| Fruits & Vegetables | |

| Grains & Cereals | |

| Pulses & Oilseeds | |

| Turf & Ornamental | |

| Country | Argentina |

| Brazil | |

| Chile | |

| Rest of South America |

Market Definition

- Function - Insecticides, fungicides, and nematicides are the crop protection chemicals used to treat seeds or seedlings.

- Application Mode - Seed treatment is a method of applying crop protection chemicals to the seeds before sowing or the seedlings before transplanting to the main field.

- Crop Type - This represents the consumption of crop protection chemicals by Cereals, Pulses, Oilseeds, Fruits, Vegetables, Turf, and Ornamental crops.

| Keyword | Definition |

|---|---|

| IWM | Integrated weed management (IWM) is an approach to incorporate multiple weed control techniques throughout the growing season to give producers the best opportunity to control problematic weeds. |

| Host | Hosts are the plants that form relationships with beneficial microorganisms and help them colonize. |

| Pathogen | A disease-causing organism. |

| Herbigation | Herbigation is an effective method of applying herbicides through irrigation systems. |

| Maximum residue levels (MRL) | Maximum Residue Limit (MRL) is the maximum allowed limit of pesticide residue in food or feed obtained from plants and animals. |

| IoT | The Internet of Things (IoT) is a network of interconnected devices that connect and exchange data with other IoT devices and the cloud. |

| Herbicide-tolerant varieties (HTVs) | Herbicide-tolerant varieties are plant species that have been genetically engineered to be resistant to herbicides used on crops. |

| Chemigation | Chemigation is a method of applying pesticides to crops through an irrigation system. |

| Crop Protection | Crop protection is a method of protecting crop yields from different pests, including insects, weeds, plant diseases, and others that cause damage to agricultural crops. |

| Seed Treatment | Seed treatment helps to disinfect seeds or seedlings from seed-borne or soil-borne pests. Crop protection chemicals, such as fungicides, insecticides, or nematicides, are commonly used for seed treatment. |

| Fumigation | Fumigation is the application of crop protection chemicals in gaseous form to control pests. |

| Bait | A bait is a food or other material used to lure a pest and kill it through various methods, including poisoning. |

| Contact Fungicide | Contact pesticides prevent crop contamination and combat fungal pathogens. They act on pests (fungi) only when they come in contact with the pests. |

| Systemic Fungicide | A systemic fungicide is a compound taken up by a plant and then translocated within the plant, thus protecting the plant from attack by pathogens. |

| Mass Drug Administration (MDA) | Mass drug administration is the strategy to control or eliminate many neglected tropical diseases. |

| Mollusks | Mollusks are pests that feed on crops, causing crop damage and yield loss. Mollusks include octopi, squid, snails, and slugs. |

| Pre-emergence Herbicide | Preemergence herbicides are a form of chemical weed control that prevents germinated weed seedlings from becoming established. |

| Post-emergence Herbicide | Postemergence herbicides are applied to the agricultural field to control weeds after emergence (germination) of seeds or seedlings. |

| Active Ingredients | Active ingredients are the chemicals in pesticide products that kill, control, or repel pests. |

| United States Department of Agriculture (USDA) | The Department of Agriculture provides leadership on food, agriculture, natural resources, and related issues. |

| Weed Science Society of America (WSSA) | The WSSA, a non-profit professional society, promotes research, education, and extension outreach activities related to weeds. |

| Suspension concentrate | Suspension concentrate (SC) is one of the formulations of crop protection chemicals with solid active ingredients dispersed in water. |

| Wettable powder | A wettable powder (WP) is a powder formulation that forms a suspension when mixed with water prior to spraying. |

| Emulsifiable concentrate | Emulsifiable concentrate (EC) is a concentrated liquid formulation of pesticide that needs to be diluted with water to create a spray solution. |

| Plant-parasitic nematodes | Parasitic Nematodes feed on the roots of crops, causing damage to the roots. These damages allow for easy plant infestation by soil-borne pathogens, which results in crop or yield loss. |

| Australian Weeds Strategy (AWS) | The Australian Weeds Strategy, owned by the Environment and Invasives Committee, provides national guidance on weed management. |

| Weed Science Society of Japan (WSSJ) | WSSJ aims to contribute to the prevention of weed damage and the utilization of weed value by providing the chance for research presentation and information exchange. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms