Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

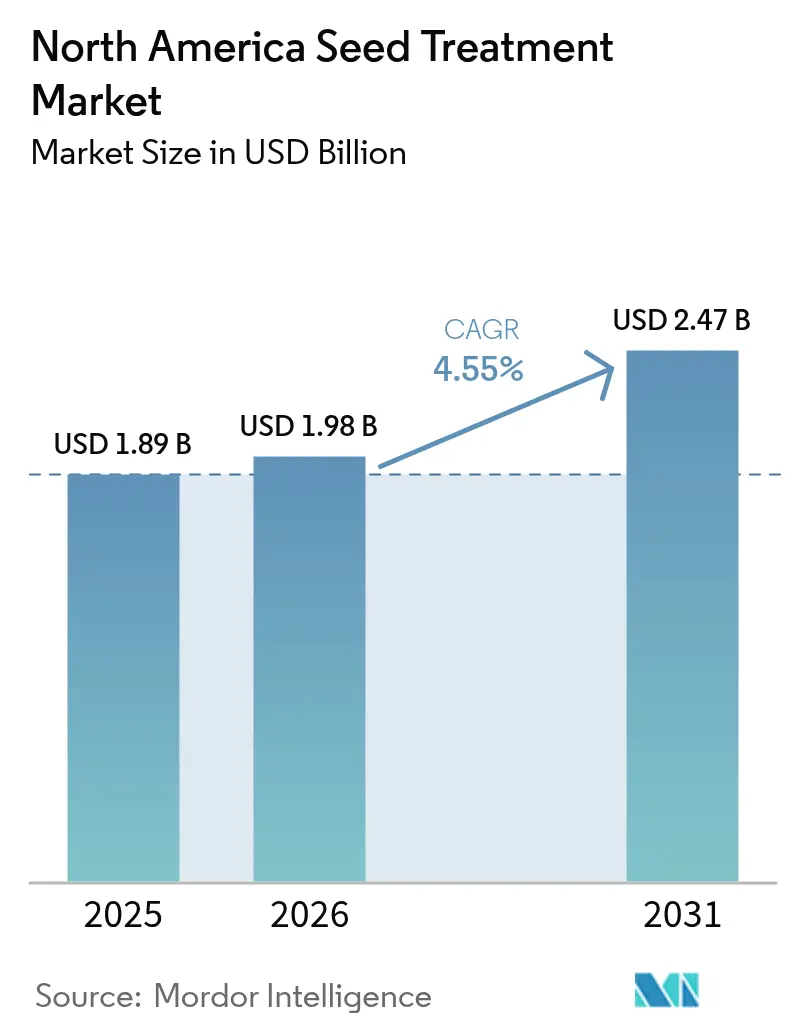

| Base Year Market Size (2025) | USD 1.89 Billion |

| Market Size (2026) | USD 1.98 Billion |

| Market Size (2031) | USD 2.47 Billion |

| Growth Rate (2026 - 2031) | 4.55% CAGR |

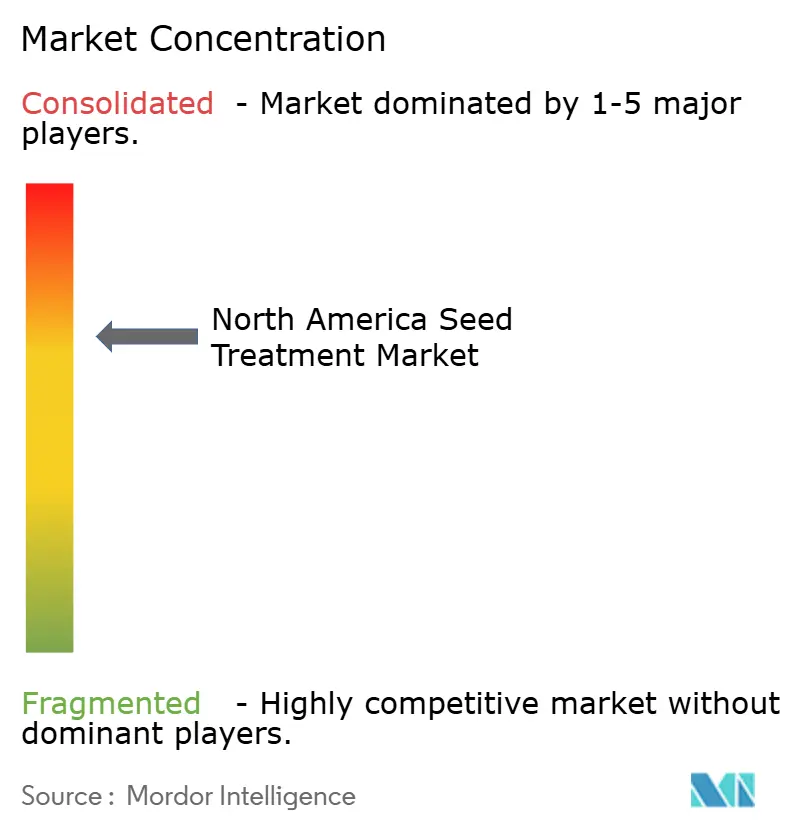

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Seed Treatment Market Analysis by Mordor Intelligence

The North America Seed Treatment market size is expected to grow from USD 1.89 billion in 2025 to USD 1.98 billion in 2026 and is forecast to reach USD 2.47 billion by 2031 at 4.55% CAGR over 2026-2031. This steady progression reflects producer demand for preventive crop protection, regulatory shifts that favor treated seed over foliar sprays, and continuous improvements in precision application technologies. The adoption of GPS-guided planters and farmer participation in carbon programs strengthen and enhance revenue visibility, while stringent Environmental Protection Agency (EPA) re-registration reviews and distributor consolidation temper limit pricing flexibility. The functional mix continues to favor insecticides. Companies with integrated seed genetics, treatment chemistries, and data services sustain a competitive advantage by bundling agronomic value into a single purchase decision for growers.

Key Report Takeaways

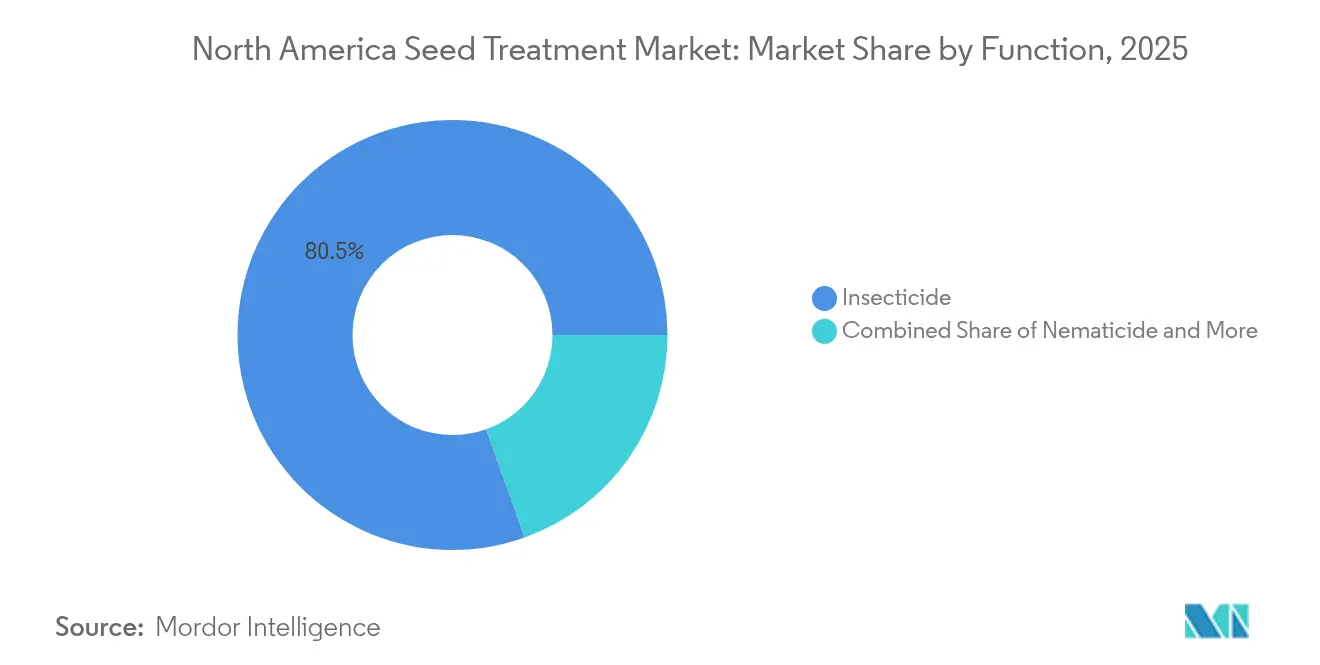

- By Function, insecticide treatments held 80.45% of the North America Seed Treatment market share in 2025 and are anticipated to advance at a 4.72% CAGR through 2031.

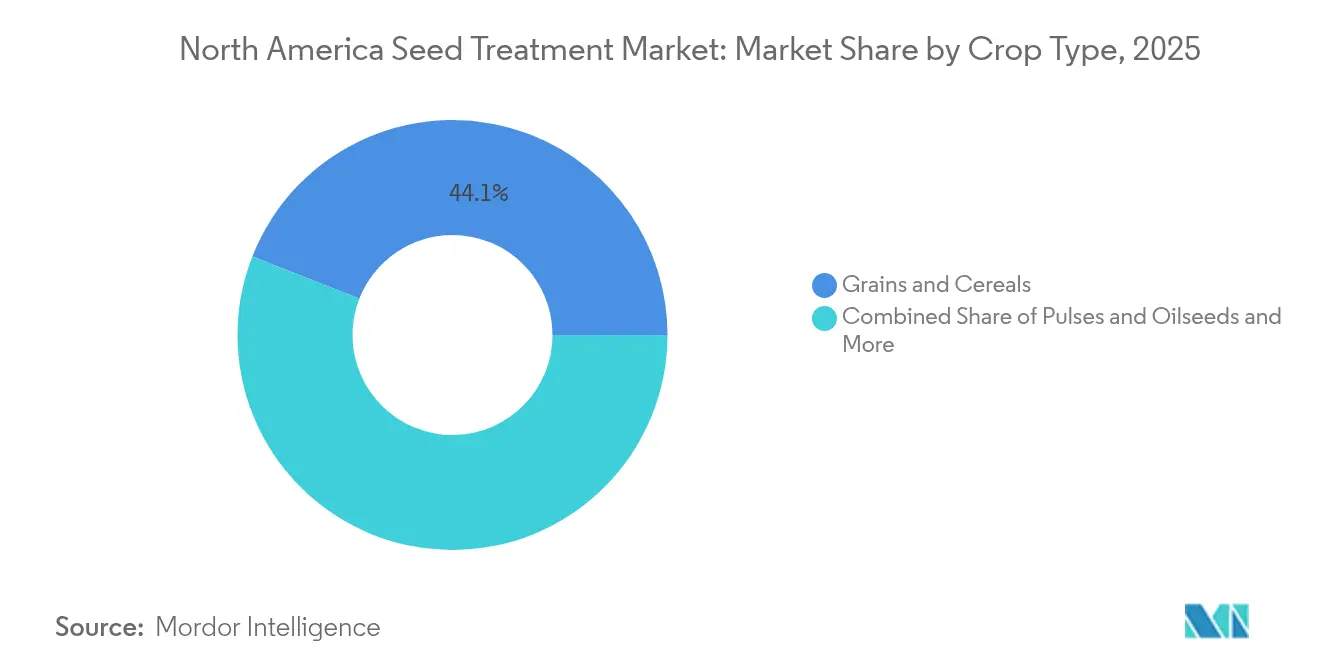

- By Crop Type, grains and cereals accounted for 44.05% of the North America Seed Treatment market size in 2025, and this segment is projected to expand at a 4.78% CAGR through 2031.

- By Country, the United States accounted for 83.10% revenue share of the North America Seed Treatment Market in 2025, while Mexico records the highest projected to record CAGR at 5.55% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Seed Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of seed-borne diseases | +1.2% | North America, with acute pressure in Great Plains wheat belt | Medium term (2-4 years) |

| Regulatory pressure on field spraying driving seed-applied alternatives | +0.9% | United States and Canada, limited Mexico impact | Short term (≤ 2 years) |

| Adoption of precision planting equipment enabling targeted seed dosing | +0.7% | United States core, expanding to Canada and Mexico | Long term (≥ 4 years) |

| Higher per-kernel value of GMO and traited seeds is pushing growers to use seed-treatment coatings to protect that larger seed investment. | +0.8% | United States Corn Belt and Canada | Medium term (2-4 years) |

| Carbon-credit programs rewarding treated cover-crop seeds | +0.4% | United States Midwest, expanding to Canadian prairies | Long term (≥ 4 years) |

| Seed-applied RNA-interference technologies moving from pilots to acres | +0.6% | United States and Canada, limited Mexico deployment | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Seed-Borne Diseases

Pathogen pressure has intensified across corn, wheat, and soybean systems, resulting in a USD 2.9 billion loss in yield for wheat growers in 2024 alone.[1]Source: USDA Economic Research Service, “Crop Production Costs and Returns,” United States Department of Agriculture, ers.usda.gov Climate variability enables pathogens to overwinter farther north, prompting the use of fungicide seed treatment in Canadian provinces that were previously rarely affected a decade ago. Preventive applications deliver higher returns than rescue sprays because they establish stand yield potential early in the season. Fungal threats, such as Fusarium head blight, continue to expand their geographic range, leading growers to adopt multi-mode treatment stacks. The economic urgency of disease management is most acute in high-value hybrid seed sectors, reinforcing premium demand for broad-spectrum products.

Regulatory Pressure on Field Spraying Driving Seed-Applied Alternatives

The Environmental Protection Agency (EPA) strengthened pollinator protection guidelines in 2024, restricting several foliar neonicotinoid uses while leaving seed-applied products largely intact.[2]Source: EPA Biopesticides and Pollution Prevention Division, “Biopesticides,” EPA, epa.gov State watershed regulations have also curtailed aerial applications in sensitive zones. As a result, retailers report a swing toward treatments that provide season-long protection without requiring in-season spraying. The differential regulatory burden effectively redirects chemical budgets from the foliar to the seed channel.

Adoption of Precision Planting Equipment Enabling Targeted Seed Dosing

United States Department of Agriculture (USDA) surveys show 68% of corn acres planted with GPS-guided planters in 2024, up from 61% in 2023.[3]Source: USDA National Agricultural Statistics Service, “Farm Computer Usage and Ownership,” USDA, nass.usda.gov These machines synchronize with on-planter treatment injectors, delivering site-specific rates that stretch active ingredient over more acres while improving efficacy. Software links diagnostics from soil maps, past yields, and disease history to prescription files, helping growers fine-tune their treatment spending. Equipment vendors bundle support packages that shorten learning curves, accelerating adoption across Canada and Mexico. As hardware lifecycles average seven years, each planter upgrade cycle deepens compatibility for advanced seed protection.

Higher Per-Kernel Value of GMO and Traited Seeds Driving Protective Coatings

Genetically modified (GMO) and other traited hybrids now command seed prices that are 18-25% higher than conventional varieties, raising the financial risk of stand loss for growers. This premium motivates farmers to invest in multi-component seed-treatment coatings that safeguard every kernel from early-season pests, pathogens, and abiotic stress. Trait developers bundle proprietary treatments with seed sales, turning protection into an embedded cost that growers rarely forgo. The trend is strongest in corn and soybean systems where stacked traits deliver yield advantages valued at USD 35-55 per acre. Seed companies enhance coatings with colorants and polymers that verify trait authenticity while reducing dust-off during planting, further justifying the added expense. As trait packages expand to include herbicide tolerance, insect resistance, and drought resilience, the imperative to shield that genetic value sustains demand growth for robust seed-treatment solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening U.S. EPA re-registration reviews on key actives | -0.8% | United States primarily, spillover to Canada | Short term (≤ 2 years) |

| In-furrow nutrition products cannibalizing seed treatment spend | -0.5% | United States Corn Belt, expanding to Canada | Medium term (2-4 years) |

| Consolidation of distributors squeezing price premiums | -0.4% | North America-wide, acute in United States | Short term (≤ 2 years) |

| Cold-plasma seed sanitation reducing chemical load requirements | -0.3% | United States and Canada, limited commercial deployment | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening U.S. EPA Re-registration Reviews on Key Actives

The EPA intensified data calls during the 2024 interim decisions for clothianidin and thiamethoxam, extending timelines and raising compliance costs. Required pollinator and aquatic toxicity studies lengthen relabeling processes by up to two years. Smaller registrants struggle to finance the expanded dossiers, consolidating shares toward incumbent leaders. Farmers remain wary of purchasing treatments that could face mid-season restrictions, leading to cautious stocking and delayed procurement.

In-Furrow Nutrition Products Cannibalizing Seed Treatment Spend

High-speed planters now house dual delivery systems that place fertilizer beside the seed. Growers allocate their limited budgets to nutrients that show an immediate visual response, occasionally trimming spending on preventive fungicides when disease forecasts appear mild. Precision Planting research indicates a 6% yield lift from optimized in-furrow micronutrient packages, strengthening the value proposition. Seed treatment suppliers counter the shift toward in-furrow inputs by rolling out volume rebates, extended payment terms, and on-farm technical support packages to defend wallet share, yet price competition intensifies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function: Insecticides Sustain Leadership While Chemistry Portfolios Evolve

Insecticide coatings valued about USD 1.52 billion, equal to 80.45% of the North America Seed Treatment market size in 2025, and the segment is forecast to advance at a 4.72% CAGR through 2031. Growers rely on seed-applied insecticides to protect high-value traited corn and soybean seed from early-season wireworm and rootworm attack, an insurance cost they view as essential after investing in expensive genetic packages. Regulatory tightening on foliar neonicotinoid sprays keeps demand anchored in the seed channel, where exposure is lower, and permitting is simpler. Polymer coaters improve active-ingredient adhesion, limiting dust-off during high-speed planting and ensuring label compliance. Early-order discount programs from leading suppliers encourage retailers to secure insecticide volumes months ahead of planting, smoothing production planning and reinforcing market concentration among the top players. Competitive intensity centers on dose efficiency, with major brands claiming equal control at 10-15% lower application rates versus older formulations. The result is stable volume growth combined with incremental price appreciation that underpins overall market expansion.

Fungicide treatments form the second-largest functional category, propelled by the northward spread of Fusarium, Pythium, and Rhizoctonia pathogens that jeopardize stand establishment in cool, wet soils. Combination fungicide packages now integrate dual or triple modes of action to mitigate resistance and extend residual activity to four weeks, covering the most vulnerable growth stages. Nematicide coatings remain a smaller niche but prove indispensable in vegetable, cotton, and sugar beet rotations where soil-borne nematodes can slash yields by more than 20%. Suppliers promote ready-to-plant blends that unite insecticide, fungicide, and nematicide actives in a single coating, reducing on-farm mixing steps and lowering the risk of application error. Across all functions, formulators target thinner, more uniform films that reduce kernel weight variation and maintain planter singulation accuracy at speeds exceeding 8 miles per hour. The continued dominance of insecticides, coupled with steady uptake of broad-spectrum fungicides and selective nematicides, positions chemistry-based seed protection as the linchpin of acreage defense for the remainder of the decade.

By Crop Type: Grains and Cereals Leverage Acreage Scale

Grains and cereals commanded 44.05% of the North America Seed Treatment market share in 2025, equivalent to USD 0.83 billion. The segment benefits from a 4.78% CAGR outlook as precision planters lower per-bushel treatment costs and enable variable-rate dosing that aligns chemistry with localized pest pressure. Corn and wheat producers integrate predictive analytics to refine treatment spend, while soybean growers layer insecticidal coatings to protect high-value trait stacks. Pulses and oilseeds trail grains but gain momentum from Canada’s expanding canola acreage and double-cropping of soybeans in the southern United States. Turf and ornamental uses occupy a specialist niche because aesthetic loss cannot be recovered after germination, reinforcing premium demand for color-stable coatings that verify treatment integrity.

Fruit and vegetable growers pay the highest per-seed treatment rate, yet represent a smaller overall volume. Their export orientation exposes them to strict maximum residue limits set by overseas buyers, pushing demand toward low-dose synthetic actives and advanced polymer encapsulation that minimizes detectable residues at harvest. These coatings extend protection against early-season pathogens while keeping chemical load within tight tolerances that satisfy importer audits. High crop value per acre allows growers to absorb the added cost of premium coatings, especially in lettuce, tomato, and bell pepper supply chains destined for North America and Europe. The same residue-driven discipline influences grape and berry sectors where cosmetic quality dictates marketability, ensuring sustained uptake of precision-metered seed treatment packages that pair efficacy with compliance. Specialty crop dealers further reinforce adoption by offering price premiums for lots documented under verifiable residue management protocols.

Geography Analysis

The United States contributed USD 1.57 billion, accounting for 83.10% of the North American seed treatment market size in 2025. The United States dominates the North America Seed Treatment Market, supported by 310 million planted row-crop acres and the highest precision planter penetration in the region. Federal crop insurance rules recognize seed treatment as a legitimate risk-mitigation practice, thereby encouraging its use among corn and soybean growers.

Mexico, by contrast, supplied USD 0.18 billion but posts a 5.55% CAGR, driven by government-backed credit lines for modern inputs. Mexico offers the fastest absolute growth, assisted by Secretaría de Agricultura y Desarrollo Rural (SADER) incentives that co-finance precision equipment, which in turn widens the addressable market for variable-rate seed dressings. Multinationals establish toll manufacturing arrangements to localize production, thereby reducing logistics costs and navigating import duties more effectively.

Canada mirrors U.S. agronomic practice but faces distinct climatic challenges. Warming trends extend disease ranges northward, prompting the use of fungicides on wheat and barley that were rarely required a decade ago. The Pest Management Regulatory Agency (PMRA) harmonizes many EPA decisions while retaining the authority to demand cold-climate efficacy data, which adds to launch timelines. Prairie growers adopt rainfast polymers that secure fungicide adhesion during unpredictable spring rains.

Competitive Landscape

The market is dominated by a few global agrochemical companies that control the majority of commercial seed-treatment products and integrated seed and trait bundles. These agrochemical companies lead in research and development (R&D), formulation scale-up, and maintaining strong channel relationships with seed companies and cooperatives. North America is identified as a key region, with significant market value driven by large-scale commercial seed-coating operations and robust supplier margins.

Regulatory and technical pressures are influencing the product mix. Ongoing regulatory reviews of neonicotinoids and increased scrutiny on pollinator and environmental impacts in the United States and Canada are prompting companies to reformulate products, implement mitigation measures, and accelerate the development of alternatives. Concurrently, growers demand treatments that align with integrated pest management practices and meet residue or traceability requirements, leading to increased investment in lower-residue active ingredients.

Competition in the market includes large-scale players and specialized formulators. Structural changes, such as mergers and acquisitions (M&A), carve-outs, and strategic restructurings, are reshaping industry capabilities. As a result, differentiation is increasingly driven by integrated services and the rapid development of niche chemistries rather than price competition alone. This dynamic creates challenges for new entrants focused solely on single offerings but provides opportunities for agile innovators and contract treaters to carve out specialized niches.

North America Seed Treatment Industry Leaders

BASF SE

Bayer AG

Corteva Agriscience

Syngenta Group

Nufarm

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Bayer Crop Science Canada has introduced Raxil Rise, a cereal seed treatment designed to provide broad-spectrum protection against seed- and soil-borne diseases. Building on 25 years of Raxil’s established performance, it incorporates penflufen and advanced micro-dispersion technology to enhance seed coverage and disease control.

- February 2024: Syngenta announced Victrato as a new seed treatment for soybeans and cotton in the United States. The product is designed to target nematodes and soil diseases, and secured EPA approval before the 2025 planting season.

North America Seed Treatment Market Report Scope

The North America Seed Treatment Market Report is Segmented by Function (Fungicide, Insecticide, and Nematicide), Crop Type (Commercial Crops, Fruits and Vegetables, Grains and Cereals, Pulses and Oilseeds, and Turf and Ornamental), and Geography (Canada, Mexico, and United States). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Function

| Fungicide |

| Insecticide |

| Nematicide |

Crop Type

| Commercial Crops |

| Fruits and Vegetables |

| Grains and Cereals |

| Pulses and Oilseeds |

| Turf and Ornamental |

Country

| Canada |

| Mexico |

| United States |

| Rest of North America |

| Function | Fungicide |

| Insecticide | |

| Nematicide | |

| Crop Type | Commercial Crops |

| Fruits and Vegetables | |

| Grains and Cereals | |

| Pulses and Oilseeds | |

| Turf and Ornamental | |

| Country | Canada |

| Mexico | |

| United States | |

| Rest of North America |

Market Definition

- Function - Insecticides, fungicides, and nematicides are the crop protection chemicals used to treat seeds or seedlings.

- Application Mode - Seed treatment is a method of applying crop protection chemicals to the seeds before sowing or the seedlings before transplanting to the main field.

- Crop Type - This represents the consumption of crop protection chemicals by Cereals, Pulses, Oilseeds, Fruits, Vegetables, Turf, and Ornamental crops.

| Keyword | Definition |

|---|---|

| IWM | Integrated weed management (IWM) is an approach to incorporate multiple weed control techniques throughout the growing season to give producers the best opportunity to control problematic weeds. |

| Host | Hosts are the plants that form relationships with beneficial microorganisms and help them colonize. |

| Pathogen | A disease-causing organism. |

| Herbigation | Herbigation is an effective method of applying herbicides through irrigation systems. |

| Maximum residue levels (MRL) | Maximum Residue Limit (MRL) is the maximum allowed limit of pesticide residue in food or feed obtained from plants and animals. |

| IoT | The Internet of Things (IoT) is a network of interconnected devices that connect and exchange data with other IoT devices and the cloud. |

| Herbicide-tolerant varieties (HTVs) | Herbicide-tolerant varieties are plant species that have been genetically engineered to be resistant to herbicides used on crops. |

| Chemigation | Chemigation is a method of applying pesticides to crops through an irrigation system. |

| Crop Protection | Crop protection is a method of protecting crop yields from different pests, including insects, weeds, plant diseases, and others that cause damage to agricultural crops. |

| Seed Treatment | Seed treatment helps to disinfect seeds or seedlings from seed-borne or soil-borne pests. Crop protection chemicals, such as fungicides, insecticides, or nematicides, are commonly used for seed treatment. |

| Fumigation | Fumigation is the application of crop protection chemicals in gaseous form to control pests. |

| Bait | A bait is a food or other material used to lure a pest and kill it through various methods, including poisoning. |

| Contact Fungicide | Contact pesticides prevent crop contamination and combat fungal pathogens. They act on pests (fungi) only when they come in contact with the pests. |

| Systemic Fungicide | A systemic fungicide is a compound taken up by a plant and then translocated within the plant, thus protecting the plant from attack by pathogens. |

| Mass Drug Administration (MDA) | Mass drug administration is the strategy to control or eliminate many neglected tropical diseases. |

| Mollusks | Mollusks are pests that feed on crops, causing crop damage and yield loss. Mollusks include octopi, squid, snails, and slugs. |

| Pre-emergence Herbicide | Preemergence herbicides are a form of chemical weed control that prevents germinated weed seedlings from becoming established. |

| Post-emergence Herbicide | Postemergence herbicides are applied to the agricultural field to control weeds after emergence (germination) of seeds or seedlings. |

| Active Ingredients | Active ingredients are the chemicals in pesticide products that kill, control, or repel pests. |

| United States Department of Agriculture (USDA) | The Department of Agriculture provides leadership on food, agriculture, natural resources, and related issues. |

| Weed Science Society of America (WSSA) | The WSSA, a non-profit professional society, promotes research, education, and extension outreach activities related to weeds. |

| Suspension concentrate | Suspension concentrate (SC) is one of the formulations of crop protection chemicals with solid active ingredients dispersed in water. |

| Wettable powder | A wettable powder (WP) is a powder formulation that forms a suspension when mixed with water prior to spraying. |

| Emulsifiable concentrate | Emulsifiable concentrate (EC) is a concentrated liquid formulation of pesticide that needs to be diluted with water to create a spray solution. |

| Plant-parasitic nematodes | Parasitic Nematodes feed on the roots of crops, causing damage to the roots. These damages allow for easy plant infestation by soil-borne pathogens, which results in crop or yield loss. |

| Australian Weeds Strategy (AWS) | The Australian Weeds Strategy, owned by the Environment and Invasives Committee, provides national guidance on weed management. |

| Weed Science Society of Japan (WSSJ) | WSSJ aims to contribute to the prevention of weed damage and the utilization of weed value by providing the chance for research presentation and information exchange. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms