Butterfly Valve Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 14.62 Billion |

| Market Size (2031) | USD 20.27 Billion |

| Growth Rate (2026 - 2031) | 6.75% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Butterfly Valve Market Analysis by Mordor Intelligence

The butterfly valves market size in 2026 is estimated at USD 14.62 billion, growing from 2025 value of USD 13.7 billion with 2031 projections showing USD 20.27 billion, growing at 6.75% CAGR over 2026-2031. Momentum stems from parallel spending on legacy oil-and-gas projects and new-energy assets such as green-hydrogen plants that specify triple-offset valves for leak-tight service. Supply-side expansion in China, India and Southeast Asia keeps average lead times stable even as demand rises, while aftermarket revenues grow because high-performance designs require specialist maintenance. Digital actuators with predictive diagnostics are lowering ownership costs, reinforcing adoption in municipal water upgrades financed through large public programs in the United States. Although fluoropolymer-lining prices eased late-2024, fresh PFAS-related rules in Europe could re-ignite input cost volatility, pressuring margins during 2025-2026.

Key Report Takeaways

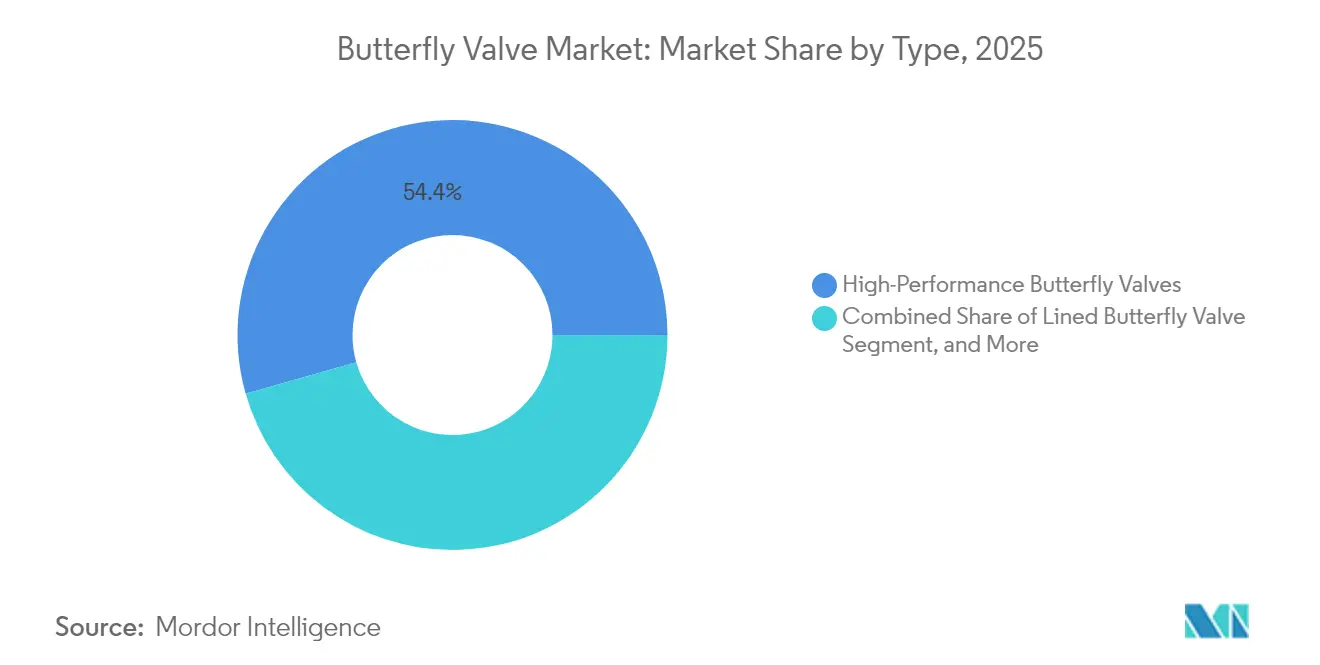

- By valve type, high-performance designs accounted for 54.40% of the butterfly valve market share in 2025, while lined variants are poised for the fastest 7.85% CAGR to 2031.

- By design, double-offset models led with 39.30% revenue in 2025; triple-offset units are projected to grow at 8.10% CAGR through 2031.

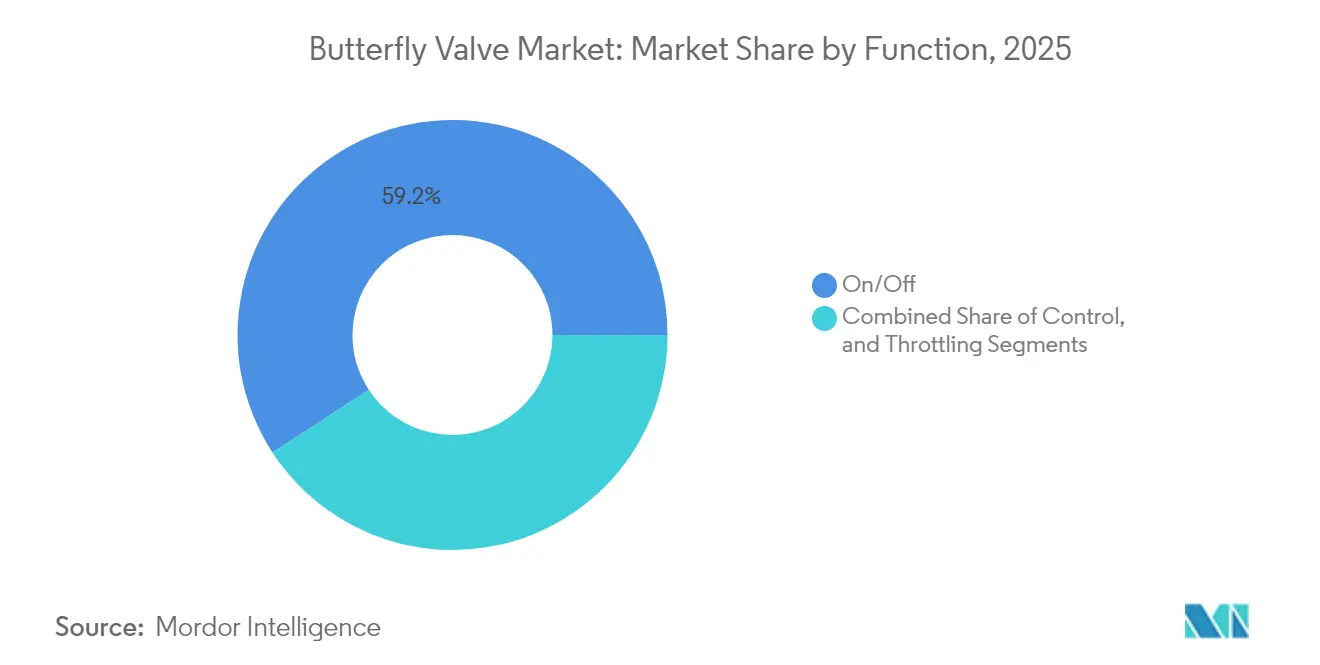

- By function, on/off isolation captured 59.20% of the butterfly valves market size in 2025, whereas control applications advance at a 6.70% CAGR.

- By end user, oil and gas retained a 34.60% share of the butterfly valves market size in 2025; water & wastewater is rising fastest at 7.25% CAGR.

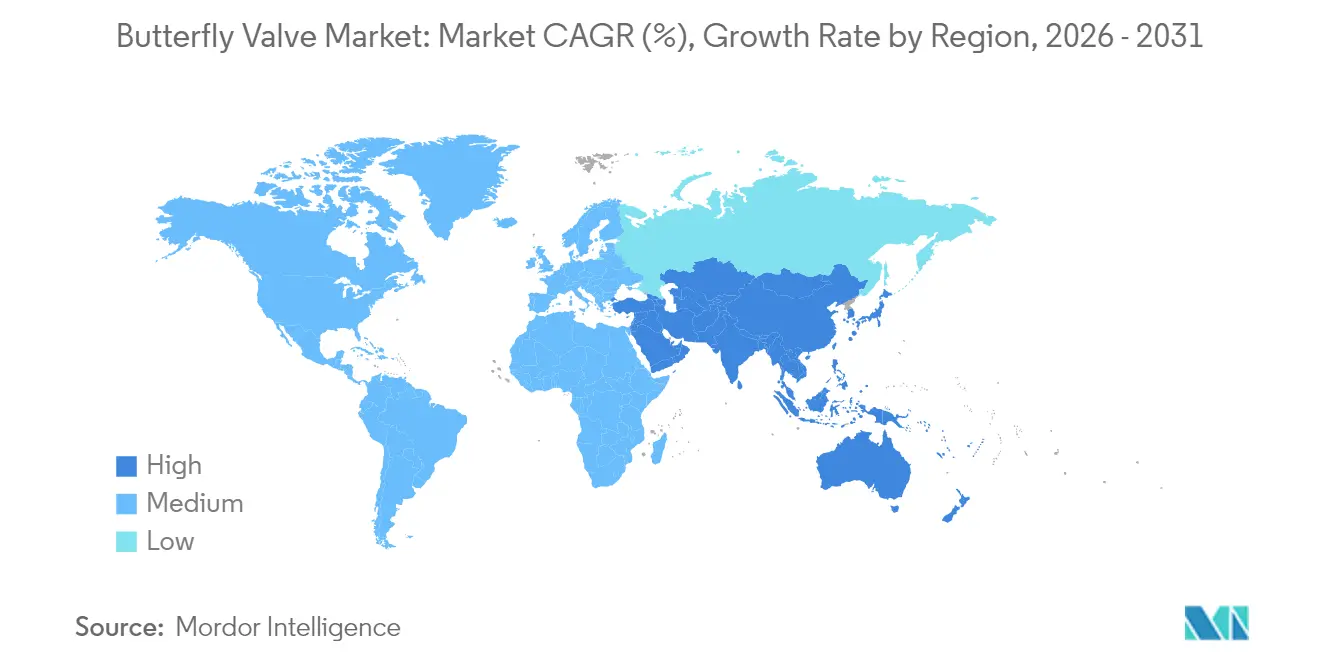

- By geography, Asia-Pacific held 39.50% of 2025 revenue; Middle East and Africa records the top 6.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Butterfly Valve Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cross-border pipeline investments | +1.8% | Middle East, North America, APAC | Medium term (2-4 years) |

| Municipal and industrial water upgrades | +1.5% | North America, Europe | Long term (≥ 4 years) |

| Preference for high-performance shut-off | +1.2% | Global chemical and power sectors | Medium term (2-4 years) |

| Triple-offset valves for green-hydrogen | +0.9% | Europe, North America, expanding APAC | Long term (≥ 4 years) |

| IIoT-ready smart actuators | +0.8% | North America, Europe, Japan | Short term (≤ 2 years) |

| Lightweight thermoplastic valves | +0.6% | Europe, North America, selective APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing investments in oil and gas refineries and cross-border pipelines

Mega-pipelines such as the 1,443 km East African Crude Oil Pipeline require 65 high-pressure block-valve stations, creating sizable orders for 20-40 in butterfly valves. [1]Zawya, “East African Crude Oil Pipeline Set for Completion,” zawya.com PETRONAS plans more than 400 well drills between 2025-2027, sustaining upstream demand for high-pressure valves. Long-distance hydrocarbon transport pushes diameters beyond 48 in, encouraging suppliers to upgrade casting and machining capacity. Material selection is shifting toward duplex stainless and Inconel to resist sour-service corrosion. Concurrent renewables build-outs add cooling-circuit needs, blending traditional and new-energy orders within the butterfly valves market.

Expansion of municipal and industrial water-wastewater infrastructure

The City of Akron earmarked USD 380.9 million for 2025 water projects, including USD 141 million for sewer compliance, placing steady orders for resilient-seated butterfly valves. Middlesex County Utilities Authority’s USD 23.066 million upgrade swaps aging butterfly valves for more efficient plug valves, illustrating the periodic replacement cycle. NSF/ANSI-certified products now dominate potable-water bids, driving R&D toward lead-free alloys. Cities such as Aurora mandate actuator orientation standards that enhance operator safety and asset management. Long-term funding certainty enables valve makers to blueprint capacity additions with lower risk.

Demand for high-performance valves with tight shut-off and high durability

Emerson’s Q1 2025 project funnel reached USD 10.4 billion, much of it tied to decarbonization retrofits that specify fire-safe or zero-leak butterfly valves. Chemical processors target fugitive-emission cuts, elevating triple-offset designs with certified <100 ppm leakage. Flowserve’s purchase of MOGAS bolstered severe-service coverage for erosive slurries. Nuclear builds such as Zhangzhou specify seismic-qualified butterfly valves, lengthening qualification cycles but raising aftermarket annuities. Overall, rising reliability standards lift average selling prices across the butterfly valves market.

Triple-offset valves adopted in green-hydrogen electrolyzers

Electrolyzers require bubble-tight isolation to maintain efficiency; triple-offset geometry avoids seal rubbing, ensuring zero leakage even after thousands of cycles. [2]ADAMS Armaturen GmbH, “Hydrogen Brochure,” adams-armaturen.de ADAMS markets hydrogen-rated valves with metallic sealing that withstand embrittlement. Emerson’s Keystone K-LOK Series 38 supports pressures up to 100 bar in gaseous hydrogen pipelines. Quadax’s 4-offset prototype pushes down to −253 °C for liquid-hydrogen transfer. As national hydrogen roadmaps mature, specialized sealing technology forms a defensible niche within the butterfly valves market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cavitation risk in low-pressure throttling | −0.8% | Global process industries | Short term (≤ 2 years) |

| Price commoditization for low-spec valves | −1.2% | APAC manufacturing hubs, emerging markets | Medium term (2-4 years) |

| Fluoropolymer supply volatility | −0.9% | Global chemical sector | Short term (≤ 2 years) |

| Cyber-security concerns in IoT actuators | −0.5% | Digitally mature regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cavitation/choke risk under low-pressure throttling

When pressure drop exceeds 30-40% of inlet pressure, vapor bubbles implode on the downstream face, eroding discs and seats. Modern plants seek sub-80 dBA noise and low vibration, so engineers increasingly switch to globe valves in critical loops. Bray’s Series 39 adopts silicon-carbide liners to curb erosion, but cost rises by 20-30% versus standard coatings. As advanced control systems proliferate, this inherent design limitation caps deeper penetration of throttling duties for the butterfly valves market.

Volatile supply and cost of fluoropolymer linings (PTFE/PFA)

EU proposals to restrict PFAS could shrink regional fluoropolymer value by EUR 6.2-18 billion between 2025-2030, heightening raw-material risk for lined-valve makers. Although PTFE prices steadied in late-2024, rising EV battery demand is likely to push them higher during 2025, pressuring margins. Valve OEMs debate forward-buying resin inventories versus redesigning with alternative linings, balancing working-capital drag against potential stock-outs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: High-Performance Dominance Meets Lined Growth

High-performance products captured 54.40% of 2025 revenue, underpinning the largest slice of the butterfly valves market share because process plants prioritize zero-leak reliability in hazardous media. Resilient-seated valves still move high volume for HVAC and benign fluids, but price competition from Asian suppliers thins margins. Lined variants expand at 7.85% CAGR, buoyed by chemical, pharmaceutical, and semicon fabs that require PTFE or PFA barriers against aggressive acids. Chinese producers now refine paste-extrusion techniques that improve bond strength, yet field reports cite occasional lining delamination under 10 bar service.

Innovation centers on modular bodies that accept interchangeable seat rings, allowing OEMs to assemble custom configurations from lean inventories. Triple-offset designs, though premium-priced, earn rising traction in hydrogen, LNG and severe-service circuits because metal-to-metal seals endure thermal shock. Such specialization lifts the average selling price and sustains profitability in the butterfly valves market.

By Design: Triple-Offset Innovation Accelerates

Double-offset geometry held 39.30% of 2025 sales, retaining mainstream status for refinery and power-plant isolation. Computational fluid-dynamics optimizes disc profiles, slicing pressure drop by 10-15% versus legacy patterns. Triple-offset units are forecast to post 8.10% CAGR, propelled by green-hydrogen electrolyzers that demand bidirectional, bubble-tight shut-off to safeguard efficiency. Concentric designs still dominate potable-water lines where pressures stay below 16 bar, but growth flattens as municipalities favour higher-performance seats for long-cycle replacement.

Quadax’s 4-offset prototype pushes application envelopes to −253 °C liquid-hydrogen transfer, hinting at a new top-end niche. Tooling complexity and exotic alloys raise entry barriers, lending established patent holders structural advantage. As a result, the butterfly valves market consolidates around a handful of firms that can finance advanced machining and cryogenic test loops.

By Function: Control Applications Drive Sophistication

Isolation service accounted for 59.20% of 2025 demand, underscoring the historical sweet spot for the butterfly valves market size at lower ownership cost. Yet control duty posts a brisk 6.70% CAGR as digital plants embed smart positioners to trim energy use. Modern disc-shaping and cam-profile seats extend linearity over 20-70% opening, enabling butterfly valves to displace costlier globe valves in non-critical loops.

IIoT-ready actuators deliver continuous torque and stem-friction diagnostics, cutting unplanned downtime. However, cavitation and rangeability constraints cap penetration in fine-tune services such as refinery fractionation. Consequently, OEMs bundle hybrid trim inserts or offer anti-cavitation cages to widen performance windows, safeguarding their share of the butterfly valves market even as process accuracy demands tighten.

By End-User Industry: Water Treatment Emerges

Oil and gas kept the largest 34.60% stake in 2025 revenue, powered by upstream drilling and cross-border pipelines . Water and wastewater projects grow fastest at 7.25% CAGR through 2031 as U.S. municipalities deploy federal infrastructure funds for pipe rehabilitation. Chemical processors emphasize PTFE-lined solutions to meet stricter emission caps, pushing a higher mix of premium SKUs. Nuclear plants require ASME-III stamped valves with documented pedigree, adding qualification overhead yet locking in aftermarket revenues.

Food and beverage sites seek hygienic-design, crevice-free discs to support CIP cycles, while HVAC contractors drive volume for economical, resilient seats. This demand spread cushions OEMs against cyclicality, but also multiplies catalog complexity that favours digitally managed configuration platforms within the butterfly valves market.

Geography Analysis

Asia-Pacific generated 39.50% of 2025 revenue, underpinned by China’s CNY 13 billion (USD 1.8 billion) domestic market expanding at 5.86% CAGR. Chemical plants drive 25-30% of local demand, prompting Neway Valve to post 36.59% revenue growth in 2023. Shanghai Electric Power Valve Factory’s CNY 1 billion (USD 0.14 billion) smart-factory build illustrates ongoing regional capacity scale-up. India accelerates refinery and potable-water schemes, while Japan channels stimulus into hydrogen distribution, where KITZ rolls out triple-offset lines.

The Middle East and Africa lead growth at 6.95% CAGR as mega-projects like EACOP and Tanzania LNG proceed to final investment decisions, each specifying hundreds of large-bore butterfly valves. Gulf states promote hydrogen export corridors, demanding 600-lb-rated triple-offset units that few suppliers can certify. Local-content mandates spur joint ventures, altering sourcing strategies across the butterfly valves market.

North America shows replacement-led momentum as shale development stabilizes and municipalities roll out USD 1 billion-plus water programs . The Inflation Reduction Act funnels incentives toward electrolyzer manufacturing, lifting domestic valve orders for green-hydrogen loops. Europe faces PFAS-related cost headwinds but offsets them with aggressive decarbonization grants that require high-performance hydrogen-ready equipment. South America’s outlook hinges on commodity cycles; Brazil’s pre-salt fields and Argentina’s Vaca Muerta basin sustain baseline investment in flow-control hardware.

Competitive Landscape

The butterfly valves market features moderate fragmentation: the top five players command roughly 55-60% combined revenue, leaving material share for regional specialists. Emerson logged USD 17.61 billion 2024 revenue with 52.77% gross margin, leveraging its software-plus-hardware stack to defend pricing. Flowserve’s USD 3.4 billion sales grew 5% in 2024, and its MOGAS acquisition added severe-service capability. The all-stock Chart Industries–Flowserve merger will create a USD 19 billion enterprise value entity with 42% aftermarket revenue, signalling a pivot toward integrated process-technology platforms.

Specialists seize niches: ADAMS excels in hydrogen service with patented metallic seals, while Quadax pioneers 4-offset technology for cryogenic liquid hydrogen. AVK and Bray differentiate on NSF-certified potable-water lines and advanced actuation packages. Asian manufacturers grow export share in resilient-seated commodity SKUs, but often lack documentation depth for nuclear or hydrogen projects.

R&D centres on digital twins, cyber-secure actuators and advanced coatings. Patent filings referencing graphene-enhanced PTFE seats rose 12% year-over-year. Vendors bundle remote diagnostics into service agreements, pushing lifecycle-cost value propositions over initial capex. With large-scale consolidation underway, mid-tier firms may seek alliances or focus on regional specialization to stay relevant within the butterfly valves market.

Butterfly Valve Industry Leaders

-

Emerson Electric Co.

-

Flowserve Corporation

-

AVK Holding A/S

-

Alfa Laval AB

-

L&T Valves Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Chart Industries and Flowserve agreed to merge in an all-stock deal, forming a USD 19 billion process-technology company expected to save USD 300 million annually within three years.

- April 2025: Shanghai Valve Factory secured butterfly-valve supply for Zhangzhou Nuclear Power Plant, while Antwei launched a digital plant capable of 20,000 smart valves annually.

- February 2025: The first integrated E-House main-line block-valve station for EACOP was completed, advancing the USD 5 billion pipeline toward 2026 start-up.

- February 2025: Shanghai Electric Power Valve Factory broke ground on a CNY 1 billion smart facility spanning 150,000 m², slated to go live in Oct 2026.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the butterfly valve market as sales of newly manufactured rotary-motion valves in which a disk rotates ninety degrees to start, regulate, or stop the flow of liquids, gases, or slurries across industrial, municipal, and commercial installations. Materials covered range from cast iron through high-performance alloys and PTFE-lined designs, while actuation manual, electric, pneumatic, or hydraulic is included because it directly affects average selling price and adoption.

Scope Exclusions: Aftermarket spare parts and standalone actuators that are retrofitted onto existing valves are not counted.

Segmentation Overview

-

By Type

- High-Performance Butterfly Valves

- Lined Butterfly Valves

- Resilient-Seated Butterfly Valves

- Triple-Offset Butterfly Valves

- Others

-

By Design

- Concentric

- Double Offset

- Triple Offset

-

By Function

- On/Off (Isolation)

- Control

- Throttling

-

By End-User Industry (Value)

- Oil and Gas

- Water and Wastewater

- Energy and Power

- Chemical

- Pharmaceutical

- Food and Beverage

- HVAC and Building Services

- Pulp and Paper

- Others

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

-

Middle East and Africa

-

Middle East

- South Africa

- Egypt

- Rest of Africa

-

Africa

- Brazil

- Argentina

- Rest of South America

-

Middle East

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted structured interviews with procurement engineers at pipeline EPCs, maintenance managers at municipal utilities, and regional distributors across Asia-Pacific, the Gulf, and North America. These calls validated life-cycle replacement cycles, average lead times, and the current premium commanded by triple-offset variants, while short online surveys with small chemical processors filled data gaps in niche demand pockets.

Desk Research

We began with public datasets that quantify the fluid-handling landscape, such as UN Comtrade trade codes for 848180 and 848130, Energy Information Administration pipeline mileage tables, International Energy Agency refinery capacity statistics, and World Bank municipal water spending series. Trade association briefs from the Water Environment Federation, Valve Manufacturers Association of America, and the International Association of Oil & Gas Producers helped us split demand by end use. Company 10-Ks, investor decks, and project tender portals supplied pricing footprints and backlog clues, which our team placed into D&B Hoovers for comparable revenue checks. The secondary sources named illustrate the wider literature; many additional references were reviewed to ground every assumption.

Market-Sizing & Forecasting

A top-down model converts national production, import, and export quantities into installed units, then layers weighted penetration rates for butterfly valves within each flow-control pool. Supplier revenue roll-ups and sampled ASP × volume checks act as a bottom-up cross-test; any variance beyond five percent triggers a revisit. Key variables like green-field pipeline kilometers, refinery throughput shifts, municipal desalination capacity, average valve diameters, and PTFE resin price swings drive both the historical reconstruction and the 2025-2030 forecast. Multivariate regression links these indicators to annual shipment value, producing a base case that is stress tested under conservative and accelerated investment scenarios.

Data Validation & Update Cycle

Outputs pass a four-layer review: automated anomaly scans, peer comparison, senior analyst sign-off, and final pre-publication refresh. Reports are updated every twelve months, with interim revisions when material events large EPC awards, trade policy changes alter the demand picture.

Why Mordor's Butterfly Valve Baseline Carries Authority

Published estimates often differ because firms choose unique scope boundaries, pricing baskets, and refresh rhythms. Our disciplined variable selection and annual refresh let users trace every figure back to transparent levers.

Key gap drivers include whether concentric low-cost units are lumped with high-performance offsets, if aftermarket sales are folded into totals, the currency conversion rate locked for Asian revenues, and how aggressively future capital expenditure pipelines are assumed.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 13.70 B (2025) | Mordor Intelligence | - |

| USD 12.12 B (2024) | Global Consultancy A | Excludes lined PTFE variants and uses 2022 average prices |

| USD 11.10 B (2024) | Industry Publisher B | Counts only valves <=24 inch bore and omits Middle East green-field projects |

These comparisons show that when scope and pricing are narrowed, totals shrink. By applying full product coverage, recent ASPs, and a live project tracker, Mordor Intelligence provides the balanced, reproducible baseline decision-makers can trust.

Key Questions Answered in the Report

What is the current size of the butterfly valves market?

The butterfly valves market is valued at USD 14.62 billion in 2026.

How fast is the butterfly valves market expected to grow?

It is forecast to expand at a 6.75% CAGR, reaching USD 20.27 billion by 2031.

Which valve type holds the largest revenue share today?

High-performance butterfly valves lead with 54.40% of 2025 revenue.

Which end-user sector is growing the fastest?

Water and wastewater treatment applications are rising at a 7.25% CAGR through 2031.

What region shows the highest growth rate?

Middle East & Africa is the fastest-growing region at a 6.95% CAGR to 2031.

How concentrated is the competitive landscape?

The top five suppliers control roughly 55-60% of sales, reflecting a moderate concentration level.

Page last updated on: