Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Hybrid Valve Market is Segmented by Valve Type (Globe Hybrid Valves, Ball Hybrid Valves, and More), Material (Stainless Steel, Duplex/Super-Duplex Steel, and More), Pressure Class (≤1500 Psi, 1501–4500 Psi, and >4500 Psi), Actuation Method (Pneumatic, Hydraulic, and More), End-User Industry (Oil and Gas, Power Generation and Hydrogen/CCUS, and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

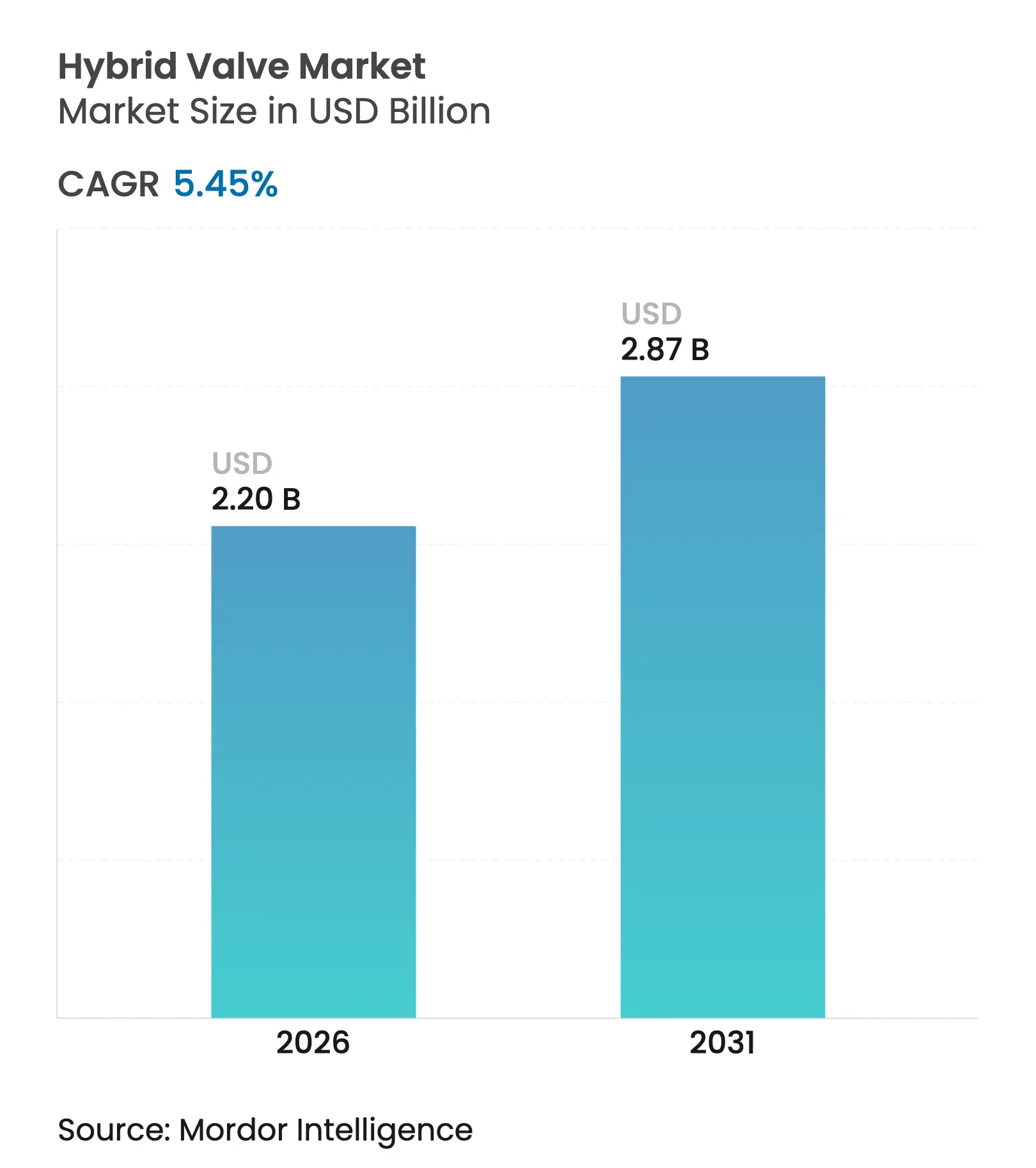

| Market Size (2026) | USD 2.2 Billion |

| Market Size (2031) | USD 2.87 Billion |

| Growth Rate (2026 - 2031) | 5.45 % CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Hybrid Valve Market size is expected to grow from USD 2.09 billion in 2025 to USD 2.2 billion in 2026 and is forecast to reach USD 2.87 billion by 2031 at 5.45% CAGR over 2026-2031. Expansion is anchored in refinery and petrochemical megaprojects across Asia-Pacific and the Middle East, where more than 60% of global capacity additions are scheduled before 2028.[1]U.S. Energy Information Administration, “Outlook on Global Refining to 2028,” eia.gov Adoption also benefits from smart actuation retrofits that improve uptime and energy efficiency, a decisive factor for operators targeting tighter emissions requirements. Material advances, notably specialty alloys for hydrogen service, open higher-margin niches as energy transition projects multiply. Finally, rising digital-twin deployments reduce maintenance downtime by double-digit percentages, reinforcing long-term demand for connected valves.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Expansion of

petro-refining capacity

Expansion of

petro-refining capacity

| +1.2% | Asia-Pacific, Middle East | Medium term (2–4 years) |

(~) % Impact on

CAGR Forecast

:

+1.2%

|

Geographic

Relevance

:

Asia-Pacific, Middle

East

|

Impact Timeline

:

Medium term (2–4

years)

|

Stricter noise and

emissions rules

Stricter noise and

emissions rules

| +0.8% | North America, EU | Short term (≤ 2 years) | |||

Water-wastewater

rehabilitation

Water-wastewater

rehabilitation

| +0.6% | North America, Europe | Long term (≥ 4 years) | |||

Digital-twin

adoption

Digital-twin

adoption

| +0.7% | Global | Medium term (2–4 years) | |||

Green-hydrogen

electrolyzers

Green-hydrogen

electrolyzers

| +0.9% | EU, North America, select APAC | Long term (≥ 4 years) | |||

Floating LNG and

FPSO uptake

Floating LNG and

FPSO uptake

| +0.5% | Offshore Asia-Pacific | Medium term (2–4 years) | |||

| Source: Mordor Intelligence | ||||||

Expansion of Petro-Refining Capacity in Asia-Pacific and Middle East

Planned additions of 4.9 million barrels per day by 2028 ensure steady orders for 50-100 hybrid valves per new processing unit. Saudi Aramco’s USD 25 billion gas program alone will require thousands of high-pressure valves capable of tight fugitive-emission control.[2]Saudi Aramco, “Aramco’s Strategic Gas Expansion Progresses,” aramco.com Indonesia’s USD 12.5 billion refinery upgrades and ExxonMobil’s Singapore revamp further widen the regional installed base. The ChemOne aromatics complex in Malaysia illustrates the scale, processing 6.5 million tpa of condensate that demands corrosion-resistant trims. Across all projects, design specifications prioritize smart diagnostics, tilting procurement toward next-generation hybrid solutions.

Digital-Twin Adoption Driving Demand for Smart Hybrid Valves

Early adopters achieve 15.8% quality gains and shave 66 hours from average downtime within 18 months of roll-out. Azbil’s 700 Series positioner drops auto-setup time from 120 seconds to 45 seconds while adding stick-slip analytics. Wanhua Chemical’s 500,000 I/O points demonstrate the scale at which digital twins now operate, cutting configuration labor by 60%. Coupling AI with condition data generates prescriptive alerts, which makes smart hybrid valves an operational necessity rather than a discretionary upgrade.

Green-Hydrogen Electrolyzer Build-Outs Need High-Cycle Hybrid Trims

Proton Exchange Membrane systems cycle thousands of times per year at 350-700 bar, posing hydrogen embrittlement risks that conventional valves cannot tackle. Bürkert’s hydrogen lineup specifies explosion-proof seals, while Pall’s Seprasol LG coalescers protect downstream purity. Testing uses helium trace gas due to hydrogen’s molecular size, adding cost but ensuring leak-tight service.[4]Valve Magazine, “Testing of Hydrogen Valves,” valvemagazine.com Material science breakthroughs in titanium and duplex alloys supply the reliability profile investors demand for multi-gigawatt electrolyzer parks.

Stricter Noise/Emissions Regulations in Critical Process Industries

Emerson’s zero-emission electric dump valves cut vented gas while boosting production efficiency by 98.75% at Laramie Energy.[3]Emerson Electric Co., “Emerson Helps Oil and Gas Company Meet Emissions Standards with New Electric Dump Valves,” emerson.com Utilities likewise retrofit nuclear units with bellows-sealed hybrids that meet demanding noise codes under radiation exposure. Carbon-capture schemes mandate −89 °C service, as seen in Mokveld’s Joule Thomson valves, further validating the hybrid concept for severe low-temperature duty.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High upfront cost vs

conventional valves

High upfront cost vs

conventional valves

| -1.1% | Global | Short term (≤ 2 years) |

(~) % Impact on

CAGR Forecast

:

-1.1%

|

Geographic

Relevance

:

Global

|

Impact Timeline

:

Short term (≤ 2

years)

|

Volatile duplex and

alloy steel prices

Volatile duplex and

alloy steel prices

| -0.7% | Europe, North America | Medium term (2–4 years) | |||

Limited machining

capacity for custom trims

Limited machining

capacity for custom trims

| -0.5% | Specialized hubs | Long term (≥ 4 years) | |||

Cyber-security risks

in IIoT valves

Cyber-security risks

in IIoT valves

| -0.4% | Digitalized markets | Medium term (2–4 years) | |||

| Source: Mordor Intelligence | ||||||

High Upfront Cost Versus Conventional Control Valves

Hybrid alternatives command 40-60% price premiums because of smart positioners and additive-manufactured internals. Velan’s 3D-printed Hexashield sleeves exemplify performance advantages but extend payback periods for budget-sensitive projects. Procurement teams in the USD 52.6 billion industrial PVF sector are therefore slow to green-light retrofits despite lifecycle savings. Retrofit installations also face piping modifications that further dilute short-term ROI.

Volatile Duplex and Alloy Steel Prices

Nickel cost swings disrupt duplex supply, prompting frequent design recalculations and bid revisions. Damstahl’s late-2024 survey flagged shrinking order books amid energy-price inflation in Europe. Valve makers evaluate lean duplex grades like Forta LDX 2101 to cushion volatility. Labor shortages complicate scheduling, with 75% of manufacturers citing skilled-trade gaps that delay delivery windows.

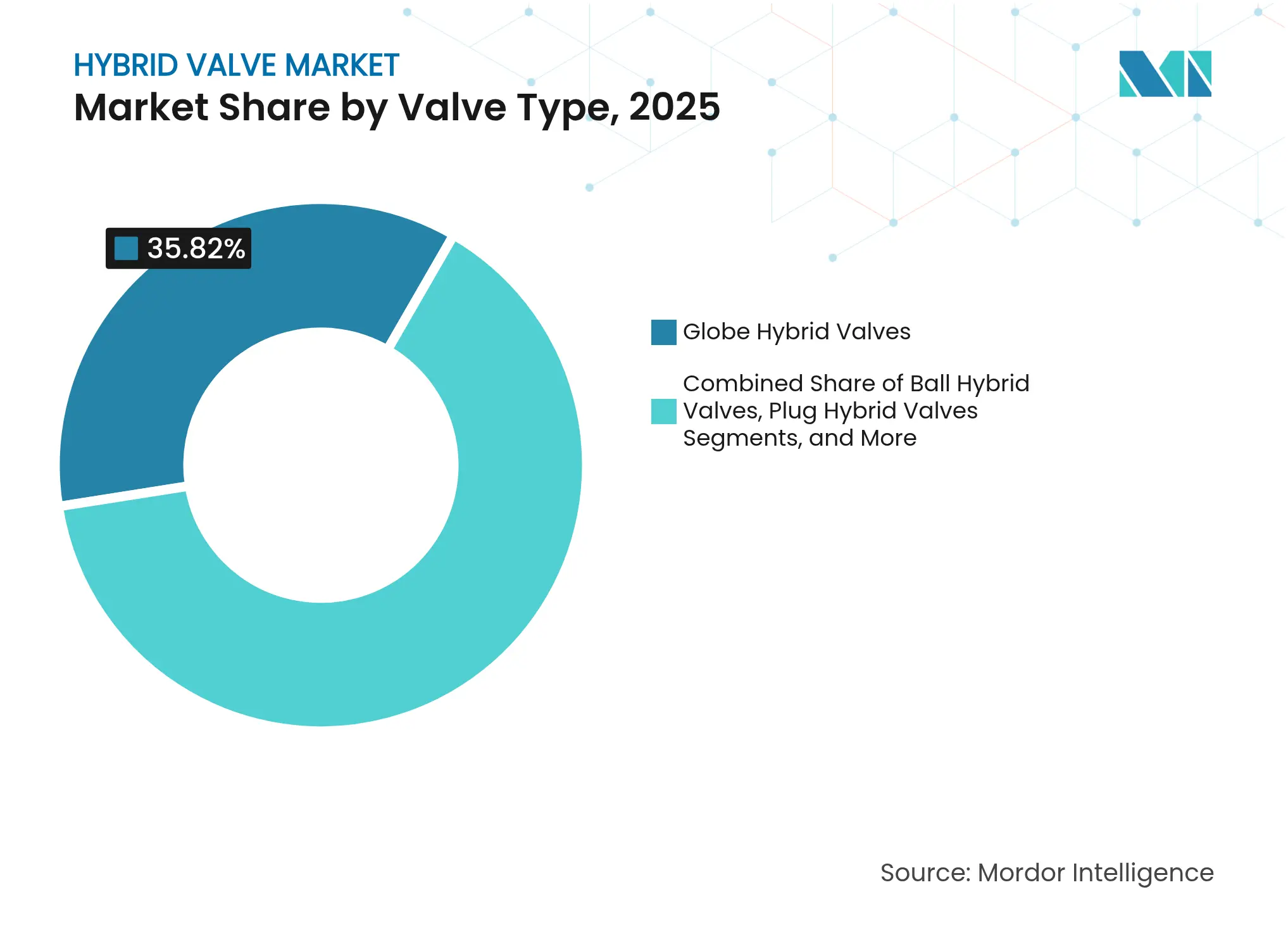

By Valve Type: Performance Needs Redefine Selection

Globe hybrids commanded 35.82% of 2025 revenue owing to their linear motion and fine throttling accuracy, which remain vital in critical refining loops. Ball designs now outpace at 6.45% CAGR as operators prefer their compact envelope and quarter-turn actuation that eases offshore maintenance in tight modules. The hybrid valve market favors ball variants in new FPSO topsides, where reduced weight cuts mooring loads. Plug, butterfly, and diaphragm formats carve smaller domains, largely where multi-port control or sanitary standards dictate unique geometries.

Technological refinements extend across all formats. KDV Flow’s PTFE-sleeved plug valve highlights chemical-resistant sealing that reduces flushing cycles. Computational fluid dynamics tools optimize port contours to slash turbulence, lowering energy draw across pump trains. Integrated diagnostics, once optional, now ship standard, confirming that digital readiness is a baseline requirement across the entire hybrid valve market.

Note: Segment shares of all individual segments available upon report purchase

By Material: Specialty Alloys Win High-Value Niches

Stainless grades retained a 40.08% share in 2025 on the strength of proven corrosion resistance versus cost. The hybrid valve market size for titanium and composite alloys is smaller today but rising 6.23% annually because electrolyzer and aerospace users pay for ultra-light, hydrogen-proof designs. Duplex and super-duplex remain essential in subsea tie-backs where chloride stress cracking is a life-of-field threat. Alloy and carbon steel linger in utility water lines, yet their share slides as operators demand longer asset life and fewer shutdowns.

Material strategies now focus on balancing price volatility with performance. Lean duplex options deliver nickel-like attributes without severe input-cost exposure, sheltering bids from supply shocks. Composite housings emerge in high-temperature flue-gas recycle loops, saving weight and attenuating vibration. The trend signals that the hybrid valve industry is evolving from single-alloy paradigms toward application-specific metallurgy.

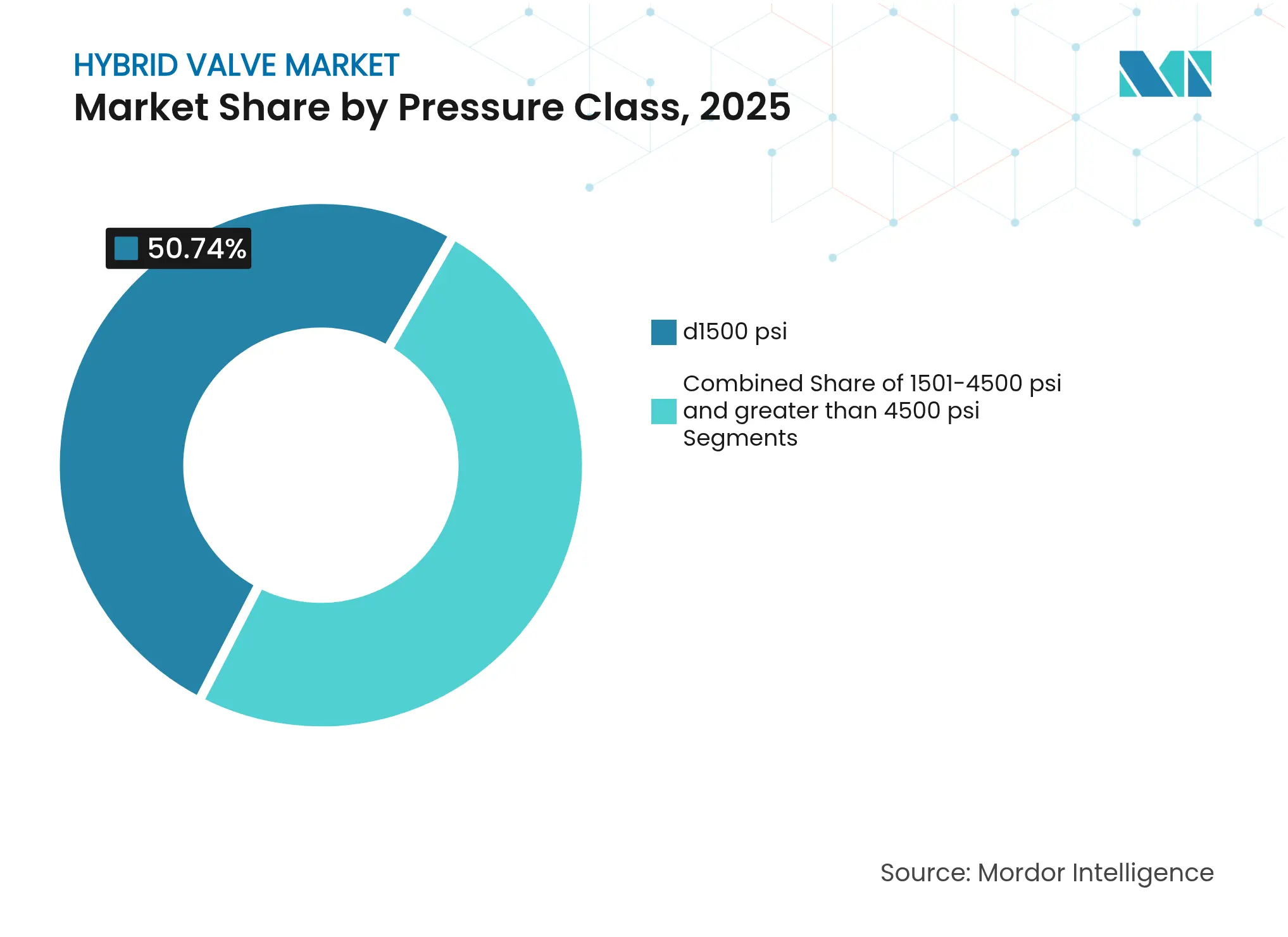

By Pressure Class: Extreme Service Drives Innovation

Valves rated ≤1500 psi form the commercial backbone with 50.74% 2025 share, standard for midstream lines and chemical reactors. Yet >4500 psi units are advancing at a 6.72% CAGR as CO₂ sequestration, EOR, and supercritical water oxidation move mainstream. The hybrid valve market size for intermediate 1501-4500 psi designs grows steadily, where flexible plastics and petrochemical reactors operate in moderate but fluctuating pressure realms.

Engineering for ultra-high ratings spurs additive manufacturing and finite-element validation. Baker Hughes qualified an HPHT injection model capable of surviving 20,000 psi cycles without seat wear, foreshadowing wider adoption in deepwater manifolds. Subsea assemblies demand not only internal pressure proof but also external hydrostatic resistance, adding complexity that favors digitally monitored hybrids for early leak detection.

Note: Segment shares of all individual segments available upon report purchase

By Actuation Method: Smart Platforms Surpass Legacy Pneumatics

Pneumatic drives held a 45.63% share in 2025, due to inherent explosion safety and rapid stroke speeds. However, electric, electro-hydraulic, and fully smart packages are gaining at 6.55% CAGR as plants digitize asset health and hunt for compressed-air savings. Hydraulic cylinders remain indispensable for very large-bore choke valves, yet their maintenance intensity pushes designers toward electrically assisted hybrids when feasible.

Emerson’s AVENTICS XV raises flow by 40% while supporting multiple fieldbus protocols. IFM’s MVQ sensors halve retrofit labor by clipping onto legacy actuators and streaming health metrics. Machine-learning layers adjust stroke profiles in real time to mitigate cavitation and seat erosion, proving that intelligence, not force alone, defines next-generation hybrid valve platforms.

By End-user Industry: Energy Transition Reshapes Demand

Oil and gas still consume 43.12% of shipments, driven by brownfield reliability projects and offshore greenfield builds. Yet the hybrid valve market grows fastest in power generation and emerging hydrogen value chains at 6.88% CAGR. Nuclear life-extension projects specify N-stamp qualified hybrids with 40-year design life, while combined-cycle plants adopt electric actuation to meet zero-bleed rules. Chemicals and petrochemicals demand high-cycle values as feedstocks diversify; water utility managers focus on leak-loss reduction through digital-ready isolation valves.

Curtiss-Wright’s AP1000 contracts underscore nuclear’s appetite for ultra-reliable flow control. Green hydrogen start-ups specify SIL-2 switches and titanium alloys despite cost premiums because safety lawsuits would dwarf the savings from cheaper metals. Across sectors, lifecycle analytics and predictive maintenance drive procurement more than unit price, a pivot that strengthens the smart segment of the hybrid valve market.

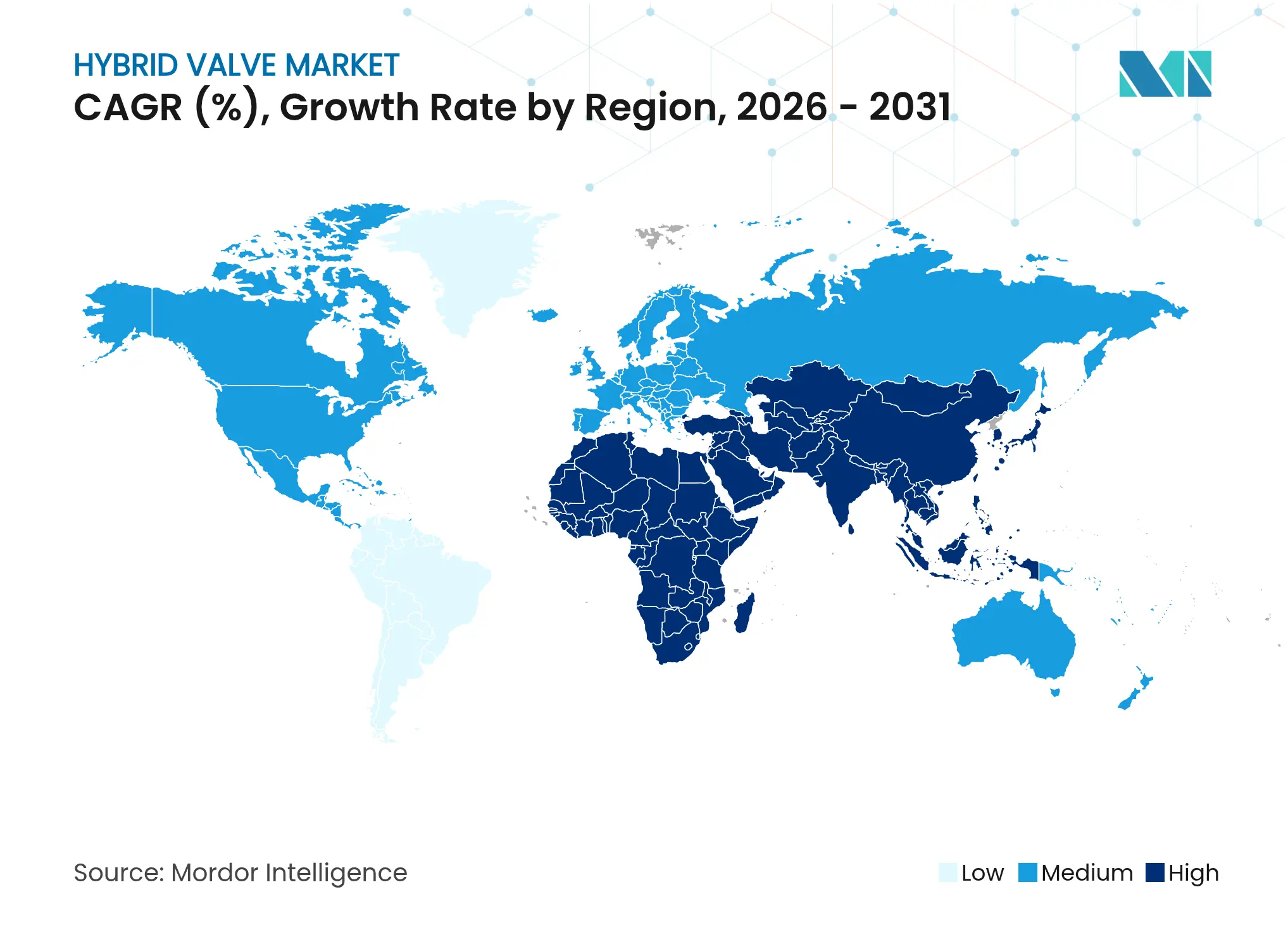

Asia-Pacific maintained a dominant 36.74% share in 2025 on the back of refinery expansions, including China’s record 14.8 million bpd throughput and Indonesia’s USD 12.5 billion upgrade push. Large petrochemical builds like ChemOne’s USD 3.5 billion complex in Malaysia intensify demand for corrosion-proof hybrid trims. Digital-twin pilots proliferate in Japanese and Korean plants, raising order volumes for connected actuation platforms. Policy shifts nudging Chinese refiners toward chemicals over transport fuels will tilt specifications toward high-temperature, high-purity variants during the forecast horizon.

The Middle East and Africa region posts a 6.79% CAGR as Saudi Aramco leverages a USD 25 billion gas build-out and offshore Safaniyah expansion to lift valve spending. The integrated Baosteel complex promises regional alloy supply, easing import bottlenecks and lowering landed cost for local assembly. African opportunities center on Nigeria’s gas monetization and South Africa’s refinery modernizations, though political risk tempers immediate capital inflows.

North America profits from shale gas debottlenecking, nuclear uprates, and USD 42.5 billion in forecast PVF spending by 2025. The region champions zero-emission actuation, illustrated by Laramie Energy’s retrofit that paired electric dumps with SCADA-enabled analytics. Europe pursues decarbonization, directing funds to hydrogen corridors and CCUS hubs. Valves that verify fugitive-emission performance in real time thus command premium bids despite austere capital budgets.

Market Concentration

The hybrid valve market is moderately concentrated. Flowserve, Emerson, and IMI leverage aftermarket networks, generating 42-45% of their revenue, hedging cyclical project risk. The all-stock merger between Chart Industries and Flowserve will create a USD 8.8 billion sales platform, pooling cryogenic know-how with severe-service valve lines. Innovation pivots on digital integration and additive manufacturing; Velan’s 3D-printed sleeves illustrate bespoke solutions priced at a premium [additivemanufacturing.media]. Patent filings increasingly cover AI-assisted diagnostics, underlining the tilt from mechanical differentiation to data analytics.

Regional challengers compete on cost and local content, particularly in Asia, yet lack the installed base to rival global service networks. Suppliers embedding machine-learning edge devices into actuators win specification priority as operators phase out unconnected valves during plant turnarounds. Market entrants specializing in hydrogen-ready materials secure early positions in electrolyzer megaprojects, showing that niche expertise can capture volume before incumbents adapt.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUES)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Market Definitions and Key Coverage

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

Desk Research

Market-Sizing & Forecasting

Data Validation & Update Cycle

Why Mordor's Hybrid Valve Baseline Is Widely Trusted

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 2.09 B (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 1.31 B (2024) | Regional Consultancy A | excludes high-pressure classes >4500 psi and uses limited Asia trade data | ||

USD 1.40 B (2024) | Trade Journal B | combines hybrid with digital smart valves; base year five years old | ||

USD 1.47 B (2024) | Global Consultancy C | applies flat ASP escalation and omits Middle East refinery additions |

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.