Femtech Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.78 Billion |

| Market Size (2031) | USD 18.98 Billion |

| Growth Rate (2026 - 2031) | 14.20% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Femtech Market Analysis by Mordor Intelligence

The Femtech market size is expected to grow from USD 8.56 billion in 2025 to USD 9.78 billion in 2026 and is forecast to reach USD 18.98 billion by 2031 at 14.20% CAGR over 2026-2031.

The Femtech market size is underscoring the rapid monetization of women-centred healthcare technology. Investment appetite continues to deepen; Silicon Valley Bank tracked USD 2.6 billion of women’s health funding in 2024, a sharp reversal from an era when only 4% of biopharma R&D addressed female-specific conditions. Rising capital flows coincide with the spending clout of female consumers, who direct USD 15 trillion in annual purchasing power and influence 90% of household care decisions, making the Femtech market one of the most attractive growth stories in digital health. Product momentum remains anchored in clinically validated devices, yet software platforms powered by artificial intelligence are setting the pace in user growth and engagement, while service models built on telehealth round out a friction-light ecosystem. Competitive behaviour is evolving in parallel, with large technology firms entering by acquisition and established healthcare brands co-creating solutions to safeguard their relevance.

Key Report Takeaways

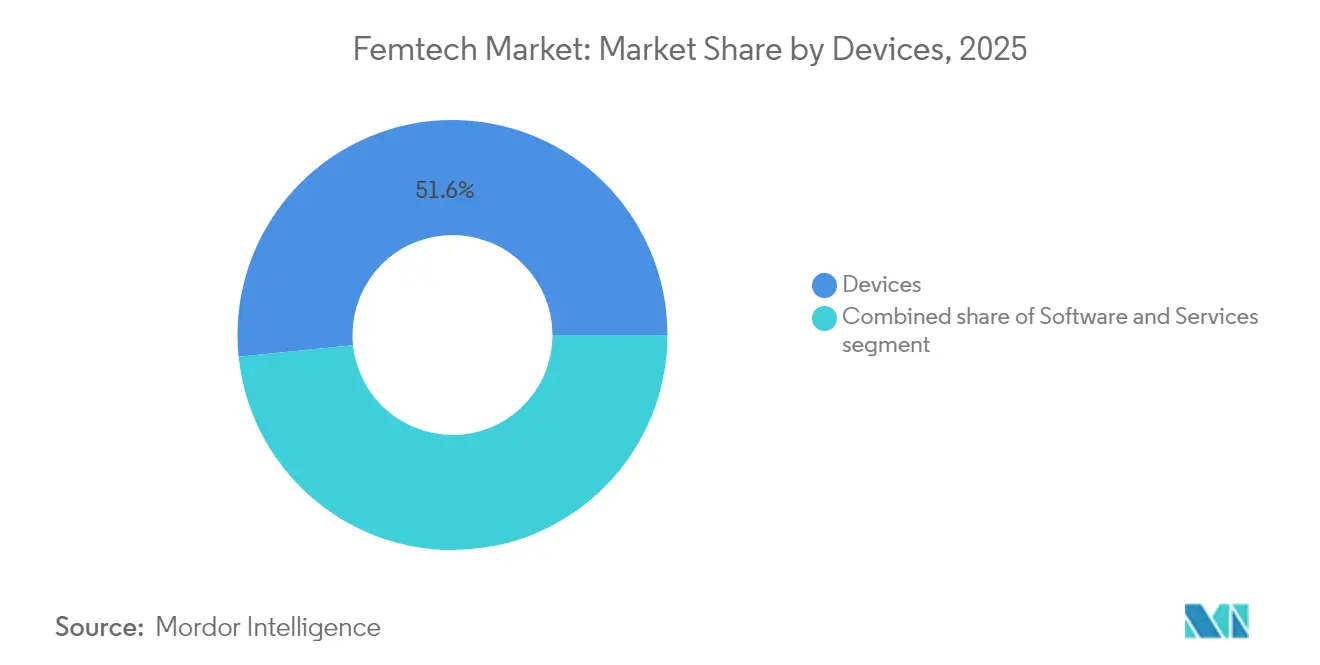

- By type, devices commanded 51.62% of Femtech market share in 2025, while software platforms are poised to expand at a 16.12% CAGR through 2031.

- By application, pregnancy and nursing care held 31.05% of the Femtech market size in 2025, whereas menopause and longevity solutions are projected to grow at a 16.18% CAGR to 2031.

- By end user, hospitals and maternal centres secured 46.10% revenue share in 2025, while specialty women’s health clinics are on track for a 16.73% CAGR through 2031.

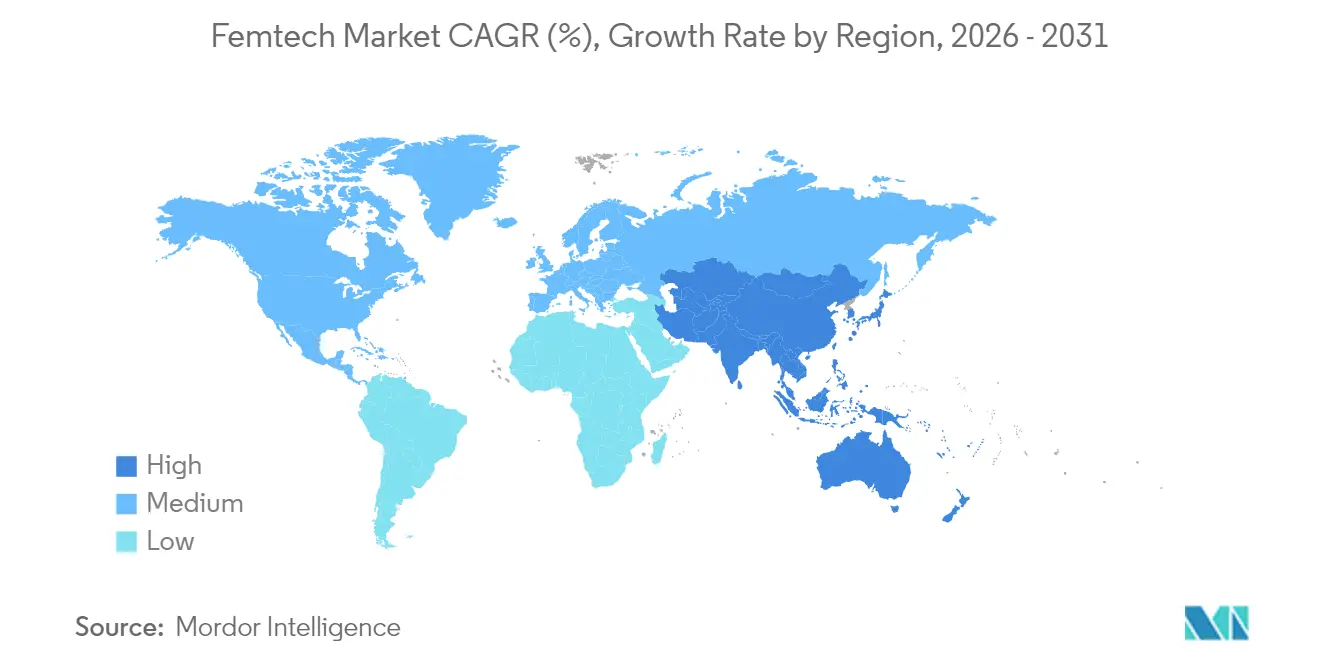

- By geography, North America retained 41.95% of the Femtech market size in 2025; Asia-Pacific is forecast to lead future expansion with a 15.12% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Femtech Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption of digital health technologies | +3.2% | Global, strongest uptake in Asia-Pacific | Medium term (2-4 years) |

| Rising venture capital and corporate funding | +2.8% | North America and Europe, expanding into Asia-Pacific | Short term (≤ 2 years) |

| Increasing incidence of fertility and menstrual disorders | +2.1% | Worldwide, particularly in developed markets | Long term (≥ 4 years) |

| Expanding employer-sponsored women’s health benefits | +1.9% | North America primary, Europe emerging | Medium term (2-4 years) |

| Integration of artificial intelligence across Femtech solutions | +2.5% | Global, led by North America and Europe | Medium term (2-4 years) |

| Regulatory support for fast-track women’s health devices | +1.8% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Digital Health Technologies

Consumers are embracing app-based and connected solutions, helped by worldwide smartphone penetration and normalized telehealth use. Wearable technology revenues are expected to reach USD 380.5 billion by 2028, with women comprising more than 70% of active users[1]PatentPC, “Global Wearables Forecast,” patentpc.com. Hardware innovation improves privacy and usability; the University of Hong Kong’s organic electrochemical transistors enable near-body data processing, removing the need to upload sensitive information to external servers. Clinical-grade accuracy is no longer confined to hospital settings as IoT fetal monitoring systems demonstrate 90% sensitivity and 87.46% precision, allowing continuous in-home prenatal surveillance. Digital therapeutics add a regulatory seal of approval: Curio Digital Therapeutics won FDA clearance for MamaLift Plus, the first prescription app for postpartum depression, highlighting the Femtech market’s capability to deliver evidence-based mental health support. Together these innovations create platform effects that reward integrated ecosystems over point solutions, reinforcing recurring revenue models across the Femtech market.

Rising Venture Capital and Corporate Funding

Capital allocation to women’s health is moving from niche to mainstream as more female investors occupy partner-level roles and identify underpriced opportunities. Flo Health’s USD 200 million raise from General Atlantic produced Europe’s first Femtech unicorn and validated data-driven cycle tracking at scale. Incumbent healthcare companies are also entering via acquisition; LifeMD added women’s health services after purchasing Optimal Human Health MD in 2025. Early-stage money remains active, illustrated by Trellis Health’s USD 1.8 million pre-seed round to build AI-first platforms. Nevertheless, 65% of global Femtech funding still lands in the United States, hinting at untapped capital formation across Europe and Asia.

Increasing Incidence of Fertility and Menstrual Disorders

Delayed childbearing, environmental stressors, and lifestyle shifts are driving higher infertility and menstrual disorder prevalence. High-intensity focused electromagnetic therapy delivers measurable relief from stress urinary incontinence, confirming demand for device-based interventions. Endometriosis remains undertreated despite affecting 10% of reproductive-age women, but a next-generation pain management device (AT-04) has reached Phase III trials. Around 6,000 American women enter menopause each day, supporting a robust pipeline of hormone-free symptom solutions. Meanwhile, ovarian tissue ablation is in clinical investigation at UCSF as an emerging therapy for PCOS. These data points indicate a durable need for personalised, tech-enabled care pathways within the Femtech market.

Expanding Employer-Sponsored Women’s Health Benefits

Corporate benefit plans are widening to capture talent and curb absenteeism. Fertility coverage was offered by 40% of US employers in 2024 compared with 30% in 2020, reflecting a 33% jump. CVS Health research shows that 69% of large employers now view holistic women’s health packages as critical for recruitment, and 75% intend to extend telehealth and clinic access. Maven Clinic partners with more than 2,000 companies and covers 6.7 million lives, demonstrating the scalability of B2B2C Femtech platforms. Financial relief sits at the centre of adoption; 93% of fertility patients incur debt, putting pressure on employers to subsidise care. These benefit dynamics channel steady demand into the Femtech market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data privacy and cybersecurity concerns | –2.3% | Global, most acute in Europe and North America | Short term (≤ 2 years) |

| Limited awareness in emerging economies | –1.8% | Asia-Pacific, Middle East & Africa, Latin America | Long term (≥ 4 years) |

| Fragmented reimbursement and insurance coverage | –2.0% | North America and selected European markets | Medium term (2-4 years) |

| Algorithmic bias and validation challenges in women’s health data | –1.6% | Global, with heightened scrutiny in jurisdictions with strict AI oversight | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Privacy and Cybersecurity Concerns

Trust remains fragile when personal reproductive data are in play. The Financial Times warned in 2024 that privacy woes have slowed several fertility-tech rollouts. A study in Frontiers found many apps still lack robust consent architecture, exposing users in the UK, EU, and Switzerland to data exploitation[2]Frontiers, “Consent Gaps in Femtech Apps,” frontiersin.org. Menstruation-tracking tools are under extra scrutiny because they fall outside traditional HIPAA protections, as noted by the California Law Review. The December 2024 HIPAA amendments add new attestations for data requests, raising compliance complexity for caregivers and platform operators. Cross-border data rules further complicate global scaling, making local partnerships vital for Femtech market entrants.

Limited Awareness in Emerging Economies

Cultural stigmas and resource gaps dampen uptake in developing regions. Southeast Asian research shows sexual-health taboos restr ict product demand, even though smartphone ownership is widespread. Infrastructure shortfalls impede digital health in rural zones, where internet access remains patchy. Higher device prices create affordability hurdles, pressing vendors to design cost-effective models. Educational deficits persist; many women cannot accurately identify fertile windows, restricting interest in advanced cycle-tracking technologies. Government spending on healthcare is climbing, as India’s market crossed USD 372 billion in 2022, yet awareness campaigns are needed to unlock this latent Femtech market opportunity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Devices Lead Through Clinical Validation

Devices generated the largest slice of revenue in 2025 at 51.62%, illustrating how physical products that carry regulatory clearance continue to anchor the Femtech market. Breakthroughs such as Bone Health Technologies’ OsteoBoost translate strong evidence into prescriber confidence and target a USD 30 billion domestic addressable field. The Femtech market size for device-based bone health interventions alone is expected to grow robustly as postmenopausal populations rise. Wearable ultrasound patches developed at MIT permit radiation-free breast screening, while therapy units like Myoovi use TENS currents for drug-free menstrual pain relief, catering to consumers who favour non-pharmacological care.

The software category, buoyed by AI and cloud analytics, is projected to book a 16.12% CAGR through 2031 as digital subscriptions unlock predictable revenue and global reach. Service models, especially telehealth, benefited from FDA recognition of digital therapeutics such as MamaLift Plus, which treats postpartum depression without medication. Integrated ecosystems exemplify future direction, blending sensors, mobile apps, and data dashboards to drive adherence and evidence generation within the Femtech market. Fertility innovations remain vivid; kegg’s cervical-mucus analyser is scaling to Japan after assisting 50,000 US users. Likewise, identifyHer’s Peri wearable debuts in 2025 to quantify hot flash patterns through proprietary algorithms, extending device relevance into menopause care.

By Application: Pregnancy Care Dominance Amid Menopause Acceleration

Pregnancy and nursing care maintained a 31.05% revenue position in 2025, supported by AI models that correctly predict maternal complications in 88.03% of cases. The Femtech market share of pregnancy solutions are reinforced by hospital initiatives such as Cleveland Clinic’s TeamBirth, which lowered Cesarean rates for Black patients by introducing shared-decision protocols. Digital postpartum programmes like MamaLift Plus further reduce readmission risk, keeping payers engaged.

Menopause and longevity applications exhibit the swiftest velocity at 16.18% CAGR as 1.3 billion women are expected to be post-menopausal by 2030. The Femtech market size for menopause solutions is forecast to reach USD 6.35 billion, prompting brands to develop non-hormonal therapies, symptom trackers, and community platforms. Menstrual-health apps thrive in Asia-Pacific, where smartphone density supports a projected 19.67% CAGR to 2033. Sexual-wellness devices gain credibility after the FDA cleared Visby Medical’s home STI test that produces lab-quality results in 30 minutes. Novel male contraceptive pipelines like Plan A point to broader reproductive-equity narratives and open adjacent demand streams.

By End User: Institutional Adoption Drives Specialty Clinic Growth

Hospitals and maternal centres represented 46.10% of total revenue in 2025 as integrated procurement channels facilitate bulk device purchases and EHR integration. Femtech platform uptake accelerated after 82% of health facilities in Latin America and the Caribbean reported ICT usage, highlighting appetite for digital care pathways. Projects such as TeamBirth demonstrate how structured digital workflows can reduce racial disparities, raising adoption incentives among quality-focused institutions.

Specialty women’s health clinics present the fastest trajectory with a 16.73% CAGR through 2031, aided by personalised environments and AI-driven diagnostics like SiD 2.0 sperm assessment. Corporate wellness programmes have become a parallel distribution arm; 40% of US employers cover fertility services, bolstering clinic referrals. Maven Clinic exemplifies the hybrid model, linking virtual care to in-person networks and covering millions of beneficiaries. Consumer trust grows when solutions are both medically endorsed and employer funded, supporting a virtuous cycle of demand in the Femtech industry.

Geography Analysis

North America maintained 41.95% of revenue in 2025, supported by FDA breakthrough pathways, HIPAA data-security amendments, and a USD 500 million federal research allocation for women’s health. Employer benefits amplify market pull: fertility benefits adoption climbed to 40% in 2024, and Progyny’s Q4 2024 revenue reached USD 298.4 million across 473 clients, underscoring corporate appetite for specialised plans. Venture capital remains concentrated in the region, capturing 65% of global Femtech funding, although that concentration also implies competitive intensity and valuation pressure.

Asia-Pacific is projected to register a 15.12% CAGR, the highest globally, thanks to smartphone ubiquity and regulatory receptivity. Menstrual-health apps alone could hit USD 9.37 billion by 2033 at a 19.67% CAGR as rural internet access expands. Japan’s planned launch of kegg in 2025 exemplifies how clinical validation fuels market entry, particularly in countries grappling with rising infertility. Regional investment is climbing; Baker McKenzie notes escalating health-transformation deals likely to push Asia-Pacific healthcare spending to USD 138 billion by 2027. Cultural taboos, however, still restrain penetration in segments like sexual wellness, making education campaigns critical.

Europe combines strong privacy regimes with growing investor attention. Flo Health became the first regional Femtech unicorn in 2024 after a USD 200 million round, highlighting an ecosystem on the brink of scale. Roughly one-fifth of the world’s Femtech firms sit in Europe, but female founders receive only 10% of venture capital, signalling room for funding equity. CE-Mark pathways are smoothing cross-border distribution, as seen with Femasys’ approvals. Compliance costs under GDPR are higher, yet these same standards give European apps a trust dividend, especially for privacy-sensitive use cases within the Femtech market.

Competitive Landscape

About 3,970 companies populate the Femtech market, of which 1,060 are venture funded and together have raised USD 7.61 billion, indicating moderate fragmentation and room for consolidation. Recent takeovers show momentum: Willow bought Elvie’s assets in March 2025, combining two maternal-care stalwarts to form a broader hardware platform. Technology giants are also making strategic moves—Samsung acquired Sonio to enrich its prenatal AI suite, and Lunit purchased Volpara to strengthen AI-enabled breast cancer screening. These plays elevate entry barriers for smaller outfits lacking capital or regulatory heft.

Unmet needs persist, particularly in menopause management where only 25% of symptomatic women receive treatment despite 86.9% having tried a remedy. Competitive differentiation leans on clinical evidence; Teal Health’s FDA-endorsed at-home cervical-cancer screen delivers 96% accuracy and illustrates how rigorous validation converts into market share. Funding inequality still disadvantages female-founded startups, which draw only 10% of venture capital, but those that do secure financing often bring user-centric insights that incumbents struggle to replicate. Overall, strategic depth and data assets are becoming the deciding factors in long-term value capture inside the Femtech market.

Femtech Industry Leaders

Flo Health

Clue by BioWink

Elvie

Maven Clinic

Natural Cycles

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Teal Health received FDA approval for the Teal Wand, the first self-collection cervical-cancer screening device, offering 96% accuracy and California launch plans.

- May 2025: Samsung completed its purchase of French ultrasound-AI specialist Sonio, expanding its maternal diagnostics footprint.

- May 2025: fermata Inc. and Lady Technologies confirmed the Japanese debut of the kegg fertility tracker for summer 2025.

- April 2025: Trellis Health exited stealth with USD 1.8 million to build an AI-first women’s health platform.

- April 2025: LifeMD entered women’s health by acquiring Optimal Human Health MD assets for its telehealth suite.

Global Femtech Market Report Scope

As per the scope of the report, femtech includes the devices and solutions that help empower women's health and well-being. These devices and solutions can be used for various applications related to reproductive systems, fertility disorders, pregnancy, and other women-related healthcare issues. The Femtech Market is segmented by Type (Devices, Software, and Services), Application (Reproductive Health, Pregnancy and Nursing Care, Pelvic and Uterine Healthcare, and General Healthcare and Wellness), End-user (Hospitals, Fertility Clinics, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (USD million) for the above segments.

| Devices |

| Software |

| Services |

| Reproductive Health & Contraception |

| Pregnancy & Nursing Care |

| Menstrual Health Management |

| Pelvic & Uterine Health |

| Menopause & Longevity |

| Sexual Health & Wellness |

| Other Applications |

| Hospitals & Maternal Centers |

| Fertility & IVF Clinics |

| Specialty Women's Health Clinics |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Devices | |

| Software | ||

| Services | ||

| By Application | Reproductive Health & Contraception | |

| Pregnancy & Nursing Care | ||

| Menstrual Health Management | ||

| Pelvic & Uterine Health | ||

| Menopause & Longevity | ||

| Sexual Health & Wellness | ||

| Other Applications | ||

| By End User | Hospitals & Maternal Centers | |

| Fertility & IVF Clinics | ||

| Specialty Women's Health Clinics | ||

| Other End Users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current Femtech market size and how fast is it growing?

The Femtech market size reached USD 9.78 billion in 2026 and is projected to hit USD 18.98 billion by 2031, translating to a 14.20% CAGR.

Which segment leads the Femtech market today?

Devices hold the leading position with a 51.62% share in 2025, underpinned by FDA-cleared wearables and at-home diagnostic tools.

What region shows the quickest Femtech market growth?

Asia-Pacific is forecast to expand at a 15.12% CAGR through 2031 as smartphone penetration drives menstrual-health app adoption.

How are employers influencing Femtech adoption?

In 2024, 40% of US employers provided fertility coverage, and 75% plan to deepen women’s health benefits, steering steady demand toward specialised platforms.

What role does artificial intelligence play in Femtech?

AI improves diagnostic speed and accuracy, such as maternal-risk algorithms that achieve 88.03% precision and sperm-assessment tools that optimise IVF success rates.

Why is data privacy a constraint in Femtech adoption?

Concerns over personal reproductive data misuse, coupled with evolving HIPAA rules, have slowed user uptake and increased compliance costs, especially in North America and Europe.

Page last updated on: