Metaverse In Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

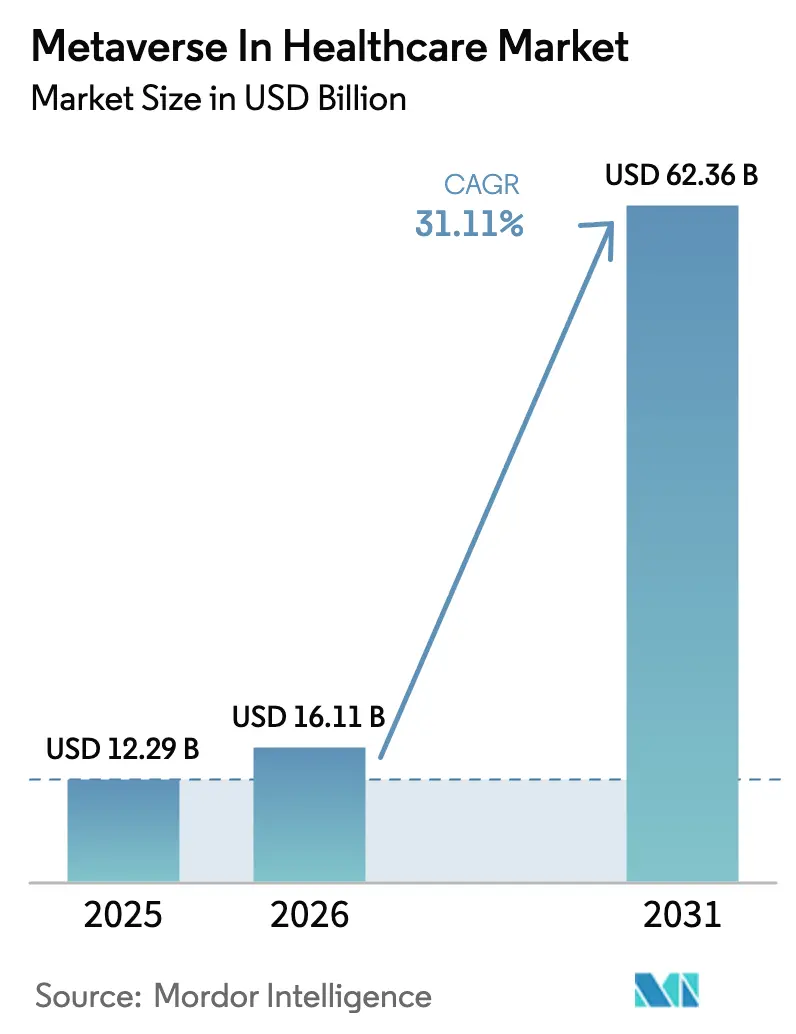

| Market Size (2026) | USD 16.11 Billion |

| Market Size (2031) | USD 62.36 Billion |

| Growth Rate (2026 - 2031) | 31.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Metaverse In Healthcare Market Analysis by Mordor Intelligence

The Metaverse in healthcare market size was valued at USD 12.29 billion in 2025 and estimated to grow from USD 16.11 billion in 2026 to reach USD 62.36 billion by 2031, at a CAGR of 31.11% during the forecast period (2026-2031). Immersive technologies are moving from pilot projects to enterprise-wide deployment as hospitals look for digital-first patient engagement models that offset clinical staffing gaps and rising costs. Post-pandemic normalization of telehealth, rapid declines in AR/VR hardware prices, and clearer reimbursement pathways for extended-reality therapeutics are accelerating procurement cycles. At the same time, strategic alliances between health systems and cloud-AI leaders give providers access to the computing power needed for complex digital twins without large upfront investment. Regulatory bodies are also formalizing guidelines that treat certain XR therapies as durable medical equipment, improving payer confidence and shortening time to revenue.[1]U.S. Food and Drug Administration, “Artificial Intelligence-Enabled Device Software Functions: Lifecycle Management and Marketing Submission Recommendations,” FDA, fda.gov

Key Report Takeaways

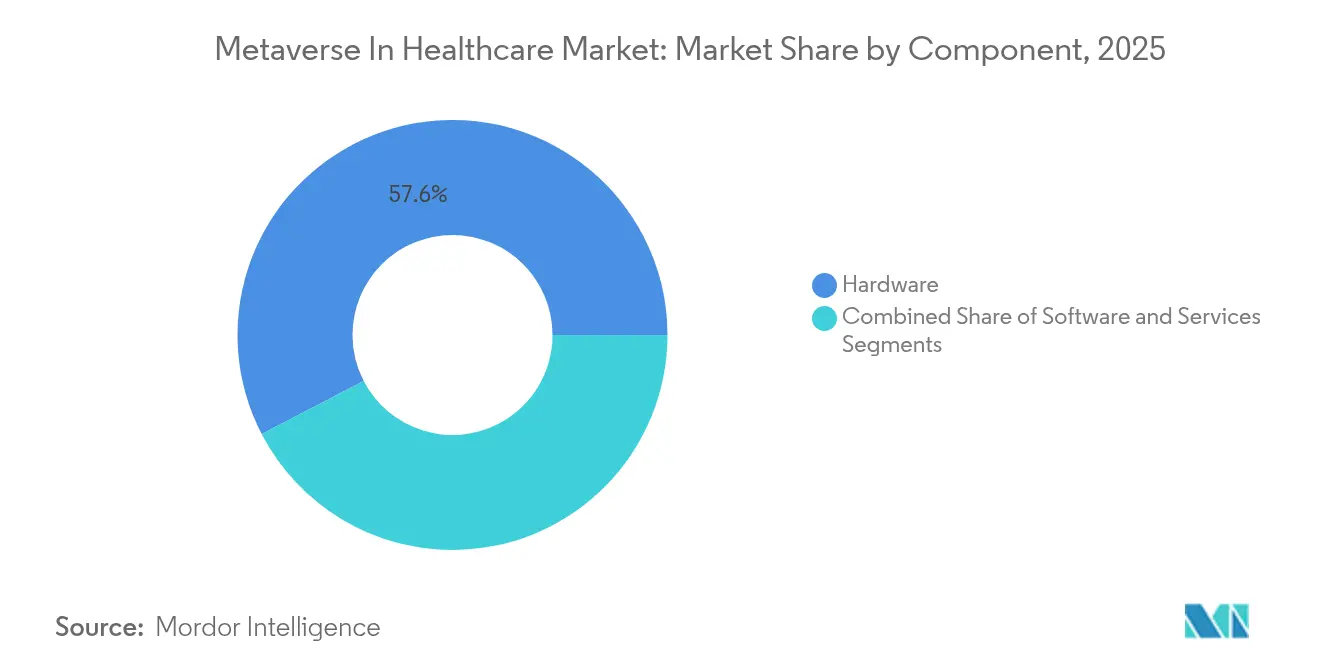

- By component, hardware led with 57.62% of the Metaverse in healthcare market share in 2025, while services are projected to post the fastest 34.20% CAGR through 2031.

- By technology, augmented reality held 58.65% revenue share in 2025; digital twins are set to expand at a 35.10% CAGR.

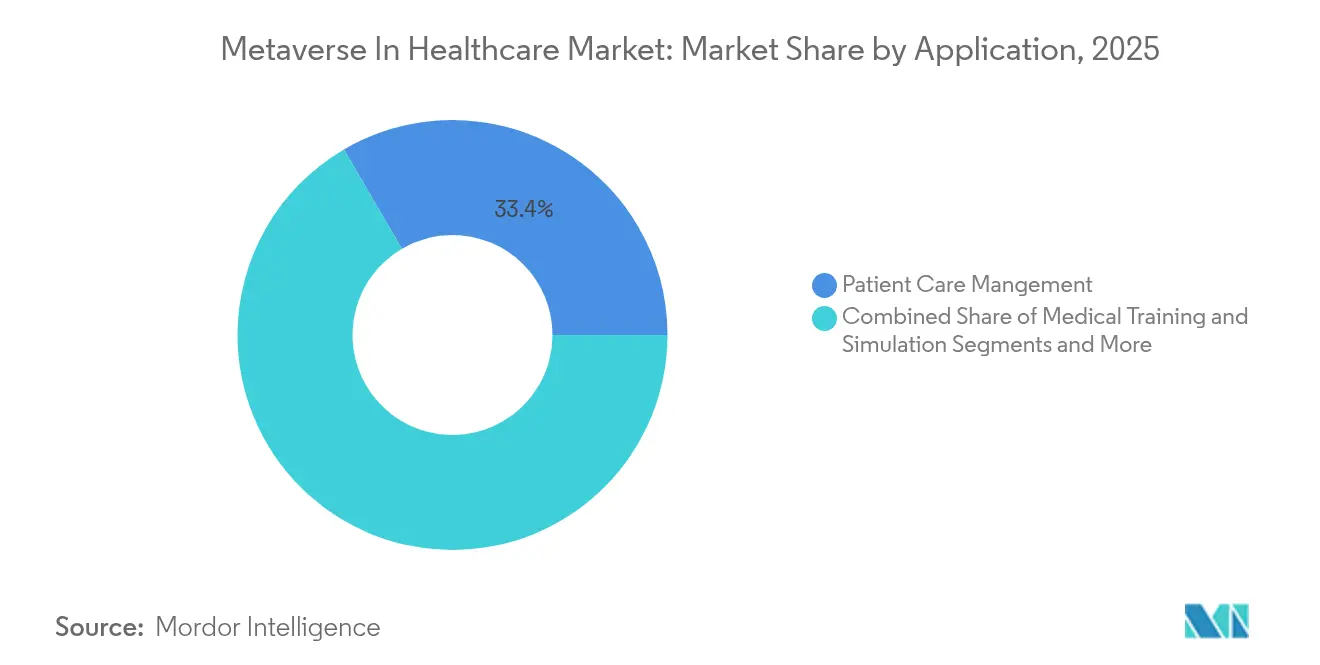

- By application, patient care management accounted for 33.42% of the Metaverse in healthcare market size in 2025, yet mental health VR therapy is advancing at a 33.90% CAGR.

- By end user, hospitals and clinics captured 57.80% of 2025 demand, whereas payers and insurers record the highest 33.10% CAGR to 2031.

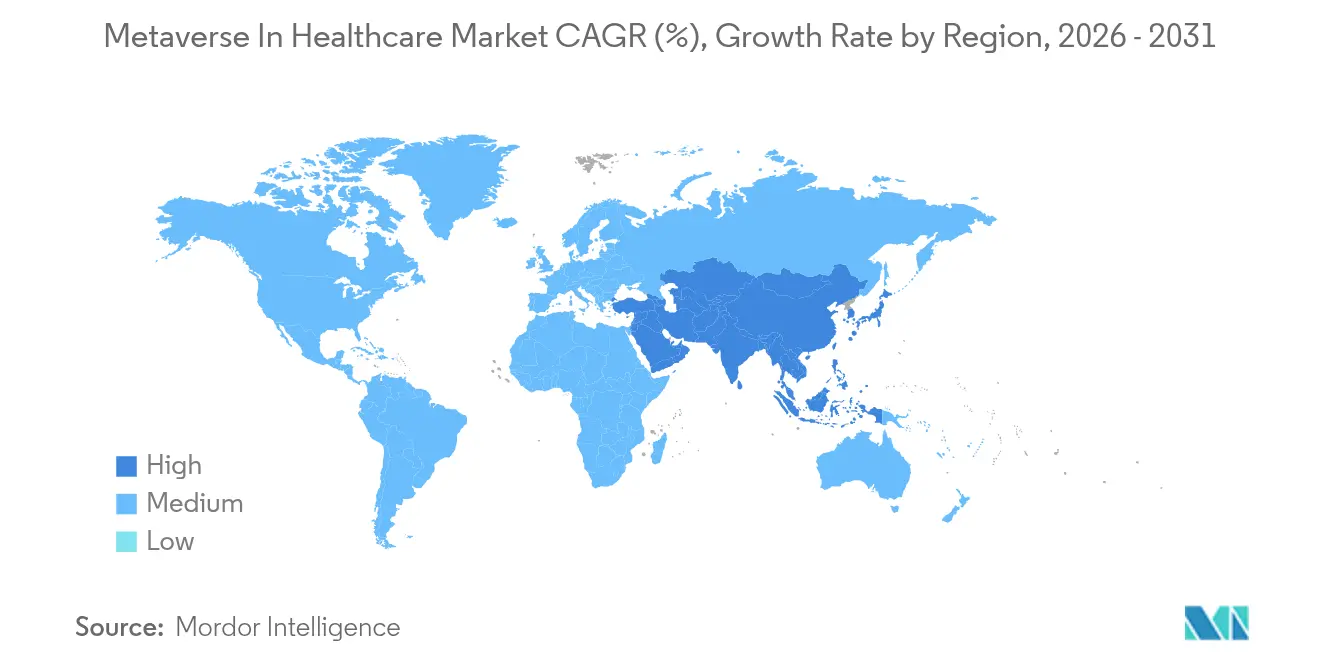

- By geography, North America commanded 42.05% of 2025 revenue; Asia-Pacific is the fastest-growing region with a 32.90% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Metaverse In Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge In Telehealth & Virtual-Care Adoption Post-COVID-19 | +8.2% | Global, with strongest impact in North America & Europe | Medium term (2-4 years) |

| Falling AR/VR Device ASPs Expand Hospital Adoption | +6.8% | Global, with accelerated adoption in APAC markets | Short term (≤ 2 years) |

| Big-Tech & Provider Partnerships Unlock Capex Budgets | +5.4% | North America & EU core, spill-over to APAC | Medium term (2-4 years) |

| FDA Draft XR/DTx Guidance Accelerates Reimbursement | +4.9% | North America primary, EU secondary adoption | Long term (≥ 4 years) |

| Digital-Twin Surgical Planning Cuts Malpractice Premiums | +3.7% | North America & EU, emerging in APAC | Long term (≥ 4 years) |

| Metaverse Medical-Tourism Hubs Open New Patient Pools | +2.8% | APAC core, MEA emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Telehealth & Virtual-Care Adoption Post-COVID-19

Virtual care volumes remain elevated, and analyst projections suggest that 30% of all US medical visits will be delivered remotely by 2026. Health systems are now layering immersive environments on top of video calls to deliver richer patient engagement. Psychiatric consultations already show 38.3% virtual penetration, spurring demand for purpose-built VR therapy rooms that improve adherence and outcomes. The European Health Data Space, effective March 2025, further supports cross-border virtual care by standardizing data exchange. Providers are piloting “virtual hospitals” staffed by multidisciplinary teams that monitor patients around the clock through metaverse dashboards. These programs relieve brick-and-mortar capacity constraints while extending specialist access to rural communities.

Falling AR/VR Device ASPs Expand Hospital Adoption

Aggressive component cost declines have lowered entry-level headset prices below USD 400, making clinical trials economically viable for mid-sized hospitals. Mixed-reality use in dental surgery now shows positive five-year ROI because fewer treatment errors offset hardware costs. Apple Vision Pro’s clearance for surgical imaging, supported by Siemens Healthineers’ Cinematic Reality app, demonstrates how consumer-grade devices can meet clinical fidelity requirements. Surveys reveal that 99% of clinicians believe VR has clinical value, yet 95% have never used it in practice, highlighting the need for turnkey implementation partners. Vendors that combine hardware leasing, software subscriptions, and clinical-workflow training are gaining early traction.

Big-Tech & Provider Partnerships Unlock Capex Budgets

Joint ventures with hyperscale cloud providers are reducing the risk and cost of adopting advanced XR. Microsoft’s alliance with NVIDIA gives hospitals pay-as-you-go access to accelerated computing that powers photorealistic digital twins. CVS Health is investing USD 20 billion over the next decade to modernize digital front doors, creating multi-year revenue opportunities for metaverse platform suppliers. Pharmaceutical firms such as Novo Nordisk are using NVIDIA’s Gefion supercomputer to speed up drug discovery by running in-silico clinical trials. Shared investment models allow smaller providers to tap enterprise-grade infrastructure without owning the assets, which in turn accelerates ecosystem network effects.

FDA Draft XR/DTx Guidance Accelerates Reimbursement

The FDA’s pending guidance on AI-enabled device software functions outlines how developers can secure marketing clearance for adaptive XR therapeutics. The agency’s Home as a Health Care Hub program positions AR/VR as a tool to address diabetes-related health inequities. Medicare has proposed new HCPCS codes that cover immersive digital mental-health therapies, signalling to private payers that reimbursement is clinically and economically justifiable. AppliedVR’s RelieVRx became the first VR therapy to receive a durable-medical-equipment code, establishing a vital precedent. Clearer policy removes a major financing barrier for hospitals evaluating large-scale deployments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Infrastructure & Integration Costs | -7.3% | Global, with acute impact in emerging markets | Short term (≤ 2 years) |

| Cyber-Security & Patient-Data-Sovereignty Risks | -5.8% | Global, with stricter EU regulations under GDPR | Medium term (2-4 years) |

| Sparse Clinical-Outcome Proof Slows Payer Coverage | -4.2% | North America & EU insurance markets | Long term (≥ 4 years) |

| Shortage Of HIPAA-Literate XR Content Developers | -3.1% | North America primary, global secondary impact | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Infrastructure & Integration Costs

Deploying enterprise-grade XR requires network upgrades, hardened cybersecurity, and integration with electronic medical records. Smaller clinics struggle to amortize device purchases and staff training over limited patient volumes. A mixed-reality cost-benefit study in dentistry showed positive ROI only after three years, underlining early cash-flow pressure. Hospitals also face bidding wars for systems integrators who understand both HL7 data standards and real-time 3D engines, which inflates project budgets. Financing mechanisms that wrap hardware, software, and services into operating-expense subscriptions can soften the barrier but are still emerging in many markets.[2]Christine T. Shiner, “Perspectives on the Use of Virtual Reality Within a Public Hospital Setting,” BMC Digital Health, bmcdigitalhealth.biomedcentral.com

Cyber-Security & Patient-Data-Sovereignty Risks

VR headsets collect detailed biometric signals such as gaze patterns and gait, which are considered highly sensitive under GDPR. Threat-modelling studies identify tampering and user profiling as major attack vectors. Homomorphic encryption and zero-trust architectures promise mitigation, yet they add latency and cost.[3]Vasilis Xynogalas, “The Metaverse: Searching for Compliance with the General Data Protection Regulation,” International Data Privacy Law, academic.oup.com Multinational health systems must also navigate conflicting data-localization rules that complicate cloud deployment strategies. Cyber-insurance premiums are rising in response to high-profile breaches involving XR devices, impacting total cost of ownership.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Dominance Shifts to Service Models

Hardware accounted for 57.62% of the Metaverse in healthcare market in 2025, underscoring the capital intensity of head-mounted displays, haptic gloves, and spatial sensors. Hospitals procure these assets mainly for surgical rehearsal and high-fidelity simulation labs. However, services are forecast to grow at a 34.20% CAGR, reflecting provider preference for subscription platforms that include software updates, managed hosting, and clinical support. Metaverse-as-a-service offerings bundle compliance monitoring and performance analytics, helping chief information officers justify operating-budget allocations.

The transition toward service contracts also addresses refresh-cycle risk. Hardware lifespans are shortening as headset resolutions and processor requirements climb. Service vendors absorb obsolescence and spread cost across a broader client base, which appeals to public hospitals facing procurement scrutiny. Integration and training services enjoy strong demand because 95% of clinicians have limited XR experience. Vendors that combine regulatory-grade content libraries with single-sign-on workflows reduce administrative burden and speed clinician adoption.

By Technology: Digital Twins Disrupt AR Leadership

Augmented reality retained 58.65% share in 2025 thanks to its ability to overlay guidance without occluding the real surgical field. Orthopedic and cardiovascular procedures are early beneficiaries, with wafer-thin smart glasses displaying CT-derived holograms that improve screw placement accuracy. Yet digital twin technology is forecast to outpace all other modalities at a 35.10% CAGR, fundamentally changing precision medicine. Real-time biometric feeds update the twin, allowing physicians to simulate medication titrations before applying them to the patient.

AI integration magnifies the twin’s predictive power by correlating historical outcomes with live sensor data. Blockchain adds tamper-proof audit trails, which is crucial for medico-legal acceptance. IoT wearables extend the model outside the clinic, enabling continuous postoperative tracking. As these capabilities mature, the Metaverse in healthcare market size for digital-twin-enabled services is set to rise sharply, particularly in pre-operative oncology planning where malpractice premiums remain high.

By Application: Mental Health VR Therapy Accelerates Beyond Patient Care

Patient care management held the largest 33.42% slice of the Metaverse in healthcare market in 2025, covering virtual consultations, remote monitoring, and care-coordination dashboards. Providers deploy immersive waiting rooms that collect previsit vitals and health literacy assessments, shortening in-clinic encounters. Mental-health VR therapy, however, is growing fastest at a 33.90% CAGR. Controlled exposure environments treat phobias, anxiety, and post-traumatic stress with outcome metrics that rival traditional cognitive behavioral therapy.

Reimbursement momentum followed Medicare’s draft codes for digital therapeutics, which private insurers often benchmark. Start-ups supply turnkey kits mailed to patients, complete with headsets and preloaded therapy modules. Clinicians receive adherence dashboards and can adjust scenarios in real time, improving personalization. Outcome data feed into payer dashboards that track avoided inpatient admissions, reinforcing value-based-care contracts.

By End User: Payers Drive Adoption Through Cost Recognition

Hospitals and surgical centers commanded 57.80% of end-user revenue in 2025 as they integrate XR across surgical, nursing, and rehabilitation workflows. Teaching hospitals rely on VR cadavers that lower recurring expenses in anatomy programs. Diagnostic centers employ AR overlays to speed image interpretation. Despite this dominance, payers and insurers exhibit the highest 33.10% CAGR because they directly capture savings from reduced emergency visits and shorter recovery times.

Early adopter insurers now reimburse VR pain-management programs for musculoskeletal disorders, which lowers opioid prescription costs. Actuarial teams use digital twins to refine underwriting models that factor real-time behavior. Provider-payer joint ventures are piloting home-based stroke rehabilitation using gamified XR, linking reimbursement to functional-mobility milestones. As these pilots scale, the Metaverse in healthcare market share held by risk-bearing entities will rise.

Geography Analysis

North America held 42.05% of 2025 revenue, supported by mature telehealth norms, sizable capital budgets, and clear FDA oversight. The region’s hospitals act as global reference sites for XR best practices, attracting international trainees. Medicare’s nascent reimbursement codes for immersive mental-health therapies strengthen the commercial case for vendors that can show clinical utility. Canada funds cross-provincial licensing pilots that permit XR specialists to treat patients nationwide, while Mexico’s Seguro Popular program explores low-cost headset leasing for rural clinics. Large technology ecosystems in Boston, Seattle, and Silicon Valley foster rapid prototyping and clinical validation cycles.

Asia-Pacific is the fastest-expanding territory with a 32.90% CAGR through 2031, driven by government incentives and lower labor costs that stretch investment budgets. China’s Healthy China 2030 roadmap earmarks grants for digital-twin hospitals. India’s Ayushman Bharat Digital Mission provides national patient identifiers, simplifying data interoperability for immersive teleconsultations. Japan subsidizes XR-based geriatric therapy to address an aging society, and South Korea offers 5G reimbursement that supports high-bandwidth holographic streams. Multinationals partner with local cloud providers to comply with data-residency mandates while retaining global software stacks. As these projects mature, the Metaverse in healthcare market size captured by Asia-Pacific providers will narrow the gap with North America.

Europe maintains steady momentum anchored by the European Health Data Space regulation, which allocates EUR 810 million to interoperable infrastructure. Germany’s Digital Care Act accelerates inclusion of DTx applications in statutory insurance formularies. The United Kingdom pilot-tests XR triage suites within its NHS 111 tele-advice service. France invests in immersive cadaver alternatives to cope with donor shortages. Southern European countries focus on medical-tourism hubs leveraging mixed-reality language interpretation. However, stricter GDPR compliance requirements extend procurement cycles as vendors add privacy-by-design features. Despite the regulatory load, coordinated funding ensures that the region remains pivotal in shaping ethical standards for the Metaverse in healthcare market.

Competitive Landscape

The market remains fragmented, with top device makers, hyperscalers, and pure-play start-ups jostling for contracts. Siemens Healthineers, Medtronic, and Philips embed XR modules into imaging and navigation systems, leveraging installed bases for upselling. Microsoft, NVIDIA, and Meta Platforms provide toolchains and GPU-cloud credits that lower development barriers, positioning themselves as indispensable infrastructure partners. Apple’s entry via Vision Pro supplies a high-acuity display option, prompting clinical-grade accessory ecosystems.

Strategic partnerships dominate go-to-market models. Microsoft and NVIDIA co-developed real-time inference services that enable photorealistic surgical twins on Azure. CVS Health’s USD 20 billion modernization fund secures multiyear procurement pipelines for XR workflow vendors. AppliedVR works with payers to validate economic outcomes, securing the first enduring reimbursement code for immersive pain relief. These alliances allow risk sharing, accelerating adoption while diversifying revenue streams across hardware, software, and services.

Niche innovators exploit white space in content, compliance, and cyber-defense. XRHealth offers HIPAA-compliant teletherapy rooms that integrate with EHRs. Veyond Metaverse focuses on intraoperative collaboration platforms that connect remote surgeons in real time. Cyber-security specialists deploy zero-trust device agents tailored to biometric data streams, answering insurer concerns. As clinical proof accumulates and reimbursement stabilizes, consolidation is likely, with infrastructure giants seeking to deepen vertical integration.

Metaverse In Healthcare Industry Leaders

Medtronic

NVIDIA Corporation

Pfizer Inc.

Koninklijke Philips N.V.

Siemens Healthineers

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: NVIDIA partnered with IQVIA, Illumina, Mayo Clinic, and Arc Institute to apply AI agents and accelerated computing across clinical trials and genomics.

- June 2025: CVS Health unveiled a USD 20 billion plan to modernize US consumer healthcare, emphasizing interoperability and immersive patient engagement.

- March 2025: The European Health Data Space regulation was published, allocating EUR 810 million to cross-border health-data infrastructure across EU member states.

Global Metaverse In Healthcare Market Report Scope

As per the scope of the report, metaverse in healthcare is the incorporation of virtual and augmented reality technologies into medical practices, training, and patient care. This integration fosters immersive and interactive environments, enabling healthcare professionals and patients to participate in a range of activities.

The metaverse in healthcare market is segmented into component, technology, application, end user, and geography. By component, the market is segmented into hardware, software, and services. By technology, the market is segmented into augmented reality and virtual reality, IoT and wearable health devices, artificial intelligence, and other technologies. By application, the market is segmented into telemedicine, medical training and simulation, patient engagement and remote monitoring, robot-assisted surgery, mental health and rehabilitation, data management, and other applications. By end user, the market is segmented into medical and diagnostic centers, medical device manufacturers, biotechnology and pharmaceutical companies, and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. For each segment, the market sizes and forecasts have been done based on value (USD).

| Hardware | Head-Mounted Displays |

| Haptic & Holo-haptics Devices | |

| Wearable Sensors & Smart Glasses | |

| Software | Application Software |

| Middleware / SDK | |

| Metaverse-as-a-Service Platforms | |

| Services | Integration & Deployment |

| Training & Consulting | |

| Support & Maintenance |

| Augmented Reality (AR) |

| Virtual Reality (VR) |

| Mixed Reality (MR) |

| Artificial Intelligence |

| IoT & Wearable Health Devices |

| Blockchain |

| Digital Twins |

| Telemedicine & Virtual Consultations |

| Medical Training & Simulation |

| Patient Engagement & Remote Monitoring |

| Robot-Assisted & Remote Surgery |

| Mental Health & Neuro-rehabilitation |

| Data Management & Digital-twin Analytics |

| Other Applications (Drug Discovery, Supply-Chain) |

| Hospitals & Surgical Centers |

| Diagnostic & Imaging Centers |

| Medical-Device Manufacturers |

| Biotechnology & Pharmaceutical Firms |

| Academic & Research Institutes |

| Payers & Insurers |

| Other Healthcare Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Hardware | Head-Mounted Displays |

| Haptic & Holo-haptics Devices | ||

| Wearable Sensors & Smart Glasses | ||

| Software | Application Software | |

| Middleware / SDK | ||

| Metaverse-as-a-Service Platforms | ||

| Services | Integration & Deployment | |

| Training & Consulting | ||

| Support & Maintenance | ||

| By Technology | Augmented Reality (AR) | |

| Virtual Reality (VR) | ||

| Mixed Reality (MR) | ||

| Artificial Intelligence | ||

| IoT & Wearable Health Devices | ||

| Blockchain | ||

| Digital Twins | ||

| By Application | Telemedicine & Virtual Consultations | |

| Medical Training & Simulation | ||

| Patient Engagement & Remote Monitoring | ||

| Robot-Assisted & Remote Surgery | ||

| Mental Health & Neuro-rehabilitation | ||

| Data Management & Digital-twin Analytics | ||

| Other Applications (Drug Discovery, Supply-Chain) | ||

| By End User | Hospitals & Surgical Centers | |

| Diagnostic & Imaging Centers | ||

| Medical-Device Manufacturers | ||

| Biotechnology & Pharmaceutical Firms | ||

| Academic & Research Institutes | ||

| Payers & Insurers | ||

| Other Healthcare Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the Metaverse In Healthcare Market?

The Metaverse In Healthcare Market size is expected to reach USD 16.11 billion in 2026 and grow at a CAGR of 31.11% to reach USD 62.36 billion by 2031.

What is the current value of the Metaverse in healthcare market?

The market is valued at USD 16.11 billion in 2026 and is projected to reach USD 62.36 billion by 2031.

Which component segment is growing fastest?

Services are expanding at a 34.20% CAGR as providers shift from hardware ownership to subscription platforms.

Why are digital twins gaining traction in healthcare?

Digital twins enable patient-specific surgical planning that can reduce malpractice premiums and improve outcomes, driving a 35.10% CAGR within this technology segment.

How are payers adopting metaverse applications?

Payers and insurers are integrating immersive digital therapeutics into coverage policies, seeking to cut claims costs through preventive care and remote monitoring.

Which region shows the highest growth potential?

Asia-Pacific leads with a forecast 32.90% CAGR due to supportive government programs and cost-efficient implementation models.

Page last updated on: