Artificial Intelligence Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

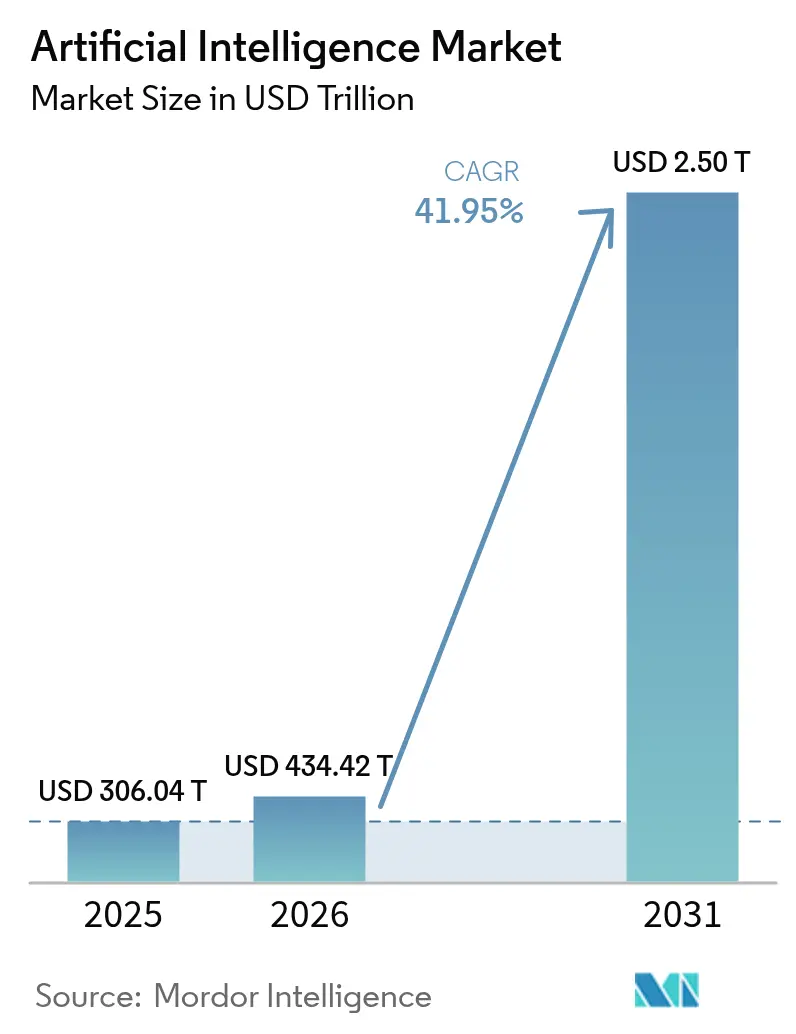

| Market Size (2026) | USD 434.42 Trillion |

| Market Size (2031) | USD 2503.13 Trillion |

| Growth Rate (2026 - 2031) | 41.95% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Artificial Intelligence Market Analysis by Mordor Intelligence

The artificial intelligence market size is expected to grow from USD 306.04 billion in 2025 to USD 434.42 billion in 2026 and is forecast to reach USD 2,503.13 billion by 2031 at 41.95% CAGR over 2026-2031. Sovereign AI programs, enterprise cost-optimization, and rapid hardware innovation are moving the technology from experimental pilots into core production workflows, fuelling sustained demand across every major sector. On-premise deployments are regaining traction because large organisations want direct control over total cost of ownership and data governance. At the same time, cloud hyperscalers are investing heavily in new capacity, ensuring that development environments remain easily accessible. GPU advances, energy-efficient architectures, and tighter integration between hardware and software stacks are shortening time to value and sharpening competitive differentiation.

Key Report Takeaways

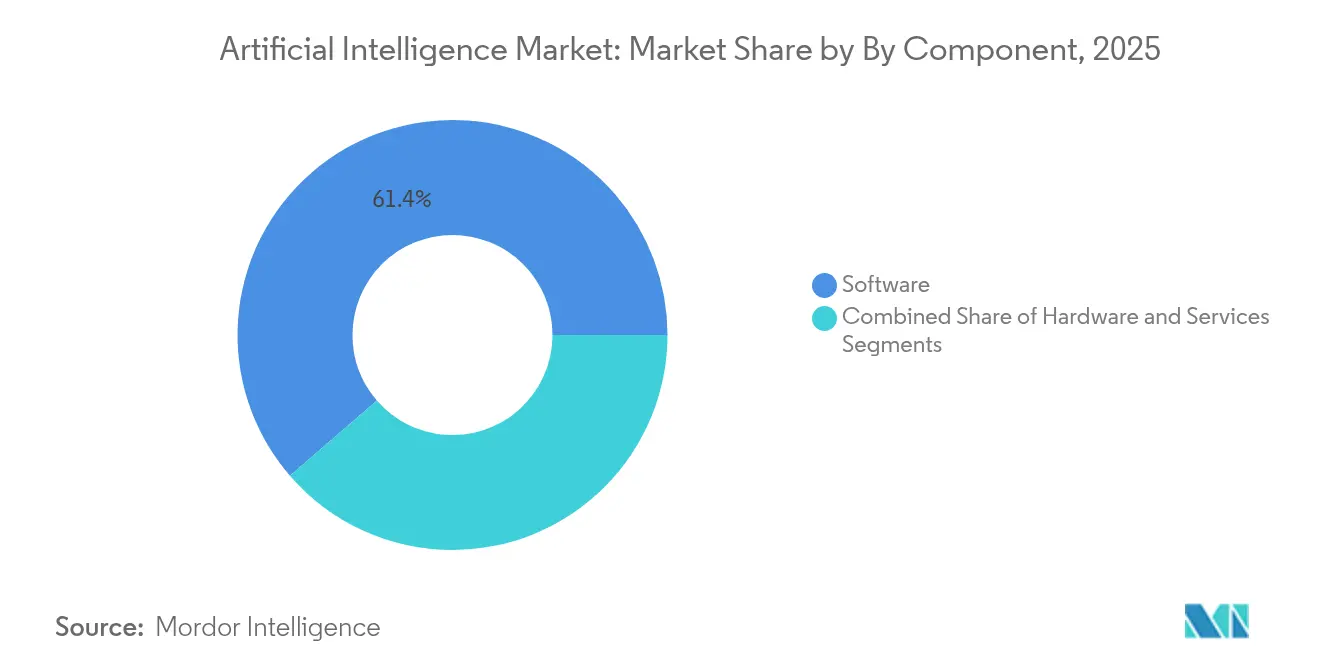

- By component, Software led with 61.35% revenue share in 2025; Services is projected to book the fastest 40.85% CAGR to 2031.

- By deployment mode, Public Cloud held 43.72% share of the artificial intelligence market in 2025, whereas Hybrid models are anticipated to grow at 45.55% CAGR through 2031.

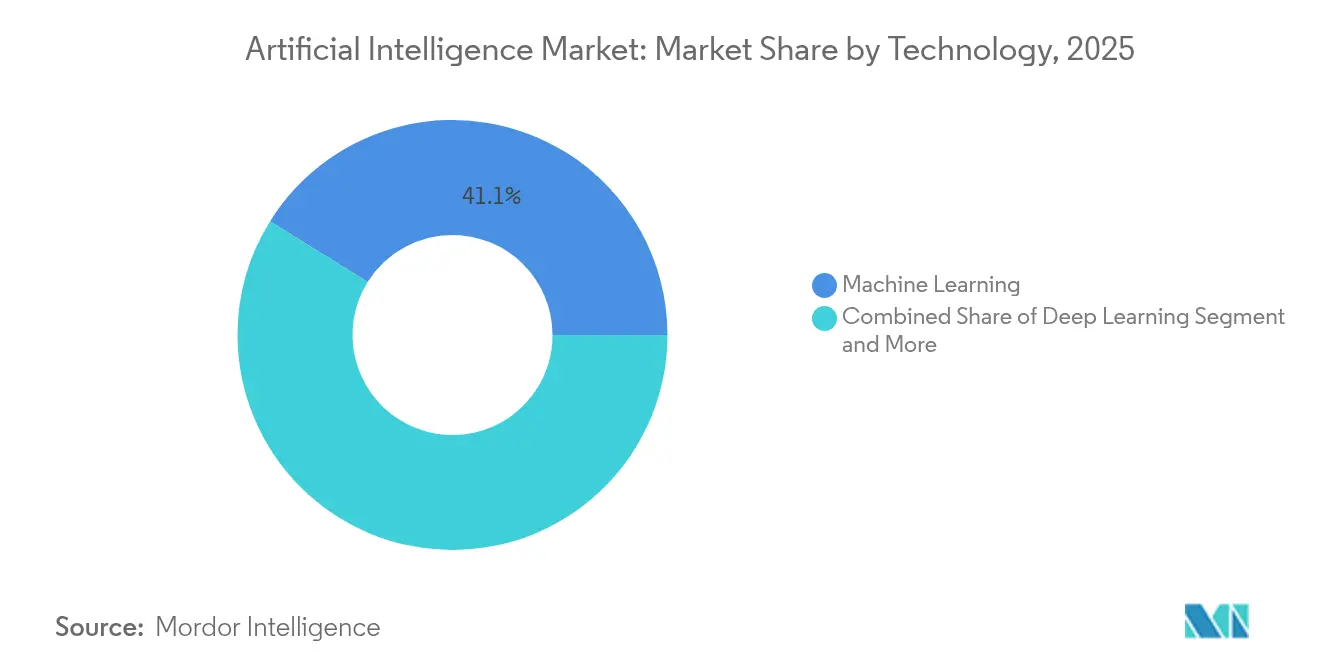

- By technology, Machine Learning controlled 41.12% share in 2025, while Generative AI is forecast to post a 46.25% CAGR through 2031.

- By end-user industry, IT & Telecommunications accounted for 27.02% of the artificial intelligence market share in 2025; Healthcare is set to expand at a 38.35% CAGR to 2031.

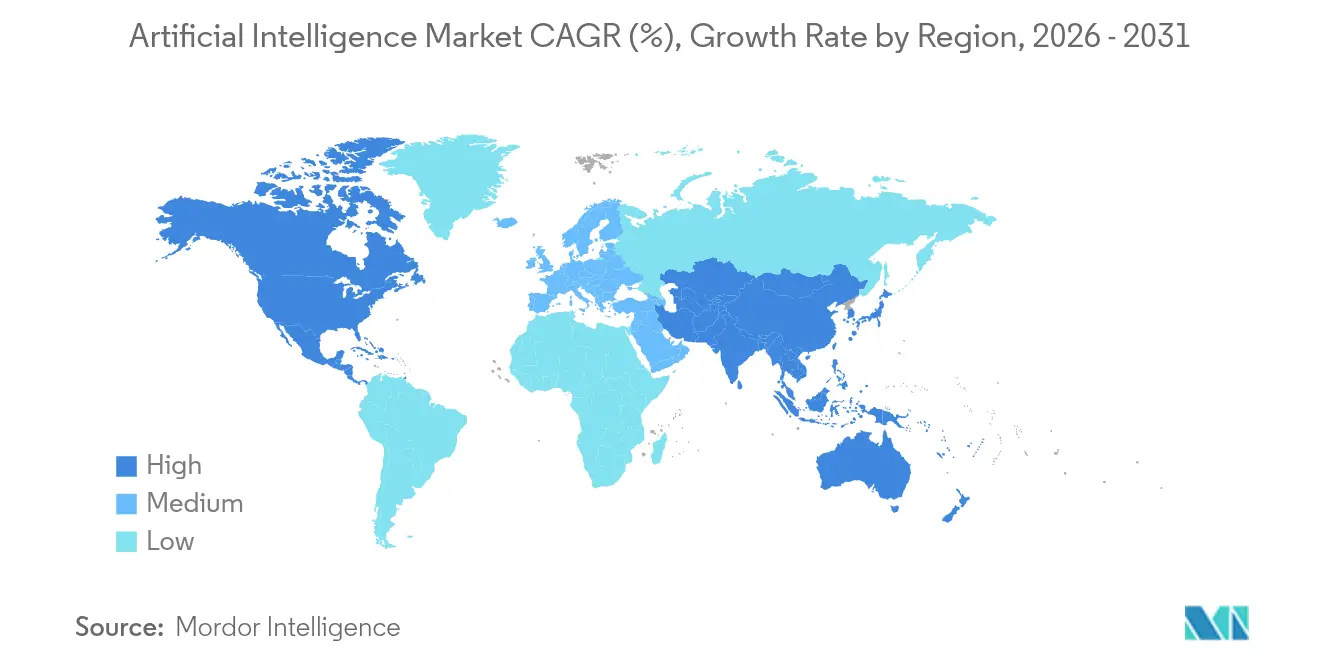

- By geography, North America commanded 37.12% of the artificial intelligence market in 2025, and Asia-Pacific is predicted to register a 40.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Artificial Intelligence Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for predictive analytics | +8.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Explosive growth in data volume/variety | +7.8% | Global, led by Asia-Pacific manufacturing and North America services | Long term (≥ 4 years) |

| Surging adoption of cloud-based AI services | +6.9% | North America and Europe core, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Sovereign AI and national compute initiatives | +5.4% | Asia-Pacific, Europe, selective Middle East markets | Medium term (2-4 years) |

| Shift toward on-prem/private AI for TCO control | +4.1% | Global enterprise markets, strongest in regulated industries | Medium term (2-4 years) |

| Demand for energy-efficient AI hardware | +3.8% | Global, with early adoption in Europe and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sovereign AI and national compute programs

Government funding is shaping local ecosystems. India’s IndiaAI Mission is channeling INR 10,372 crore (USD 124.5 million) into indigenous large language models that meet local language needs[1]Ministry of Electronics and Information Technology, “IndiaAI Mission Cabinet Approval,” indiaai.gov.in. Japan is mobilising JPY 10 trillion for AI and semiconductor capacity, signalling a long-term commitment to self-reliance. Such investments create protected demand for domestic hardware vendors and systems integrators that can comply with localisation rules.

Explosive growth in data volume and variety

Industrial IoT rollouts generate terabytes of sensor data daily, pushing enterprises to adopt AI-driven analytics. Siemens reports 90% touchless invoice processing and USD 5.65 million annual ROI after embedding machine learning into its finance operations. Healthcare imaging, autonomous vehicles, and real-time retail transactions all add to the data deluge, driving up demand for scalable storage, edge processing, and synthetic data generation tools.

Surging adoption of cloud-based AI services

Microsoft’s intelligent-cloud revenue run rate surpassed USD 13 billion in 2025, supported by 31% year-over-year Azure growth. Amazon plans to deploy USD 100 billion in fresh AI capex over the next three years. These investments guarantee enterprises near-instant access to cutting-edge models while shifting upfront costs to consumption-based fees, accelerating proof-of-concept activity.

Shift toward on-prem or private AI for TCO control

Qualcomm’s new on-prem appliance line demonstrates hardware vendors’ response to customers who want predictable cost curves and lower latency for mission-critical workloads. Internal benchmarks show that large enterprises can trim 20% operating costs and cut inference latency by 50% compared with equivalent cloud services when utilization rates are high.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex and talent shortages | -6.7% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Data-privacy and compliance barriers | -4.2% | Europe (GDPR), Asia-Pacific (emerging regulations) | Medium term (2-4 years) |

| GPU / power-grid supply bottlenecks | -5.8% | Global, critical in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Data-center carbon-emission caps | -3.1% | Europe, California, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

GPU and power-grid supply bottlenecks

NVIDIA cited persistent H100 shortages in its FY 2026 outlook, a constraint that has inflated spot prices 30-50% above MSRP and slowed enterprise deployment cycles. Power utilities forecast that data-center electricity demand could hit 1,050 TWh by 2026, exceeding planned capacity additions in several major regions, which in turn pressures project timelines for new AI clusters.

High capex and talent shortages

NVIDIA alone invested USD 1 billion across 50 start-up stakes during 2024, illustrating the capital intensity required to secure differentiation. Meanwhile, experienced MLOps engineers in Silicon Valley command 20-30% salary premiums versus 2023, stretching mid-market budgets and delaying new product launches.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services, acceleration signals, market maturation

Software retained 61.35% revenue share in 2025, reinforcing its foundational role in the artificial intelligence market. Yet the Services segment is forecast to race ahead at 40.85% CAGR through 2031 as enterprises shift focus from experimentation to full-scale implementation. Many regulated industries now require vendors that can interpret compliance mandates and redesign workflows, rather than merely deliver licenses. The scarcity of qualified integrators, therefore, enables service providers to command premium pricing, especially for domain-specific projects in healthcare and financial services.

Across consulting, integration, and managed-services lines, vendors with vertical expertise are preferred. In radiology, service partnerships that combine data-governance, algorithm validation, and clinician workflow redesign are returning 451% ROI for hospital groups over five years. Specialists that package hardware, software, and advisory support into outcome-based contracts are moving up the value chain as customers measure projects against concrete productivity targets rather than abstract model accuracy.

By Deployment Mode: Hybrid models bridge cloud-edge divide

Public Cloud held 43.72% of artificial intelligence market share in 2025, reflecting its role as the default development environment. Hybrid models, however, are projected to compound at 45.55% CAGR to 2031 as organizations seek latency optimization and cost visibility in production. Early adopters run training on hyperscale clusters then push inferencing to on-prem or edge devices for real-time response. Automotive OEMs validate this architecture by executing millisecond-level vision tasks on factory floors while retaining cloud elasticity for model retraining.

Edge rollouts are equally important in resource-constrained settings such as offshore rigs or retail outlets where bandwidth is expensive. On-prem deployments are resurging within finance and public-sector agencies that face strict data-residency mandates. Hardware suppliers now bundle orchestration software that migrates containers across clouds, on-prem racks, and edge devices based on policy rules, ensuring the artificial intelligence market size for hybrid solutions remains on an upward trajectory.

By Technology: Generative AI disrupts traditional hierarchies

Machine Learning captured 41.12% share in 2025, yet Generative AI is forecast to surge at 46.25% CAGR through 2031 as enterprises extend use cases from marketing content to code generation and knowledge-based augmentation. Generative models that pair with retrieval-augmented generation frameworks are displacing rule-based chatbots and manual document processing in customer service centres.

Conversely, Computer Vision adoption continues inside smart factories and diagnostic imaging suites where pixel-level precision drives tangible cost savings. Natural Language Processing gains steady adoption for multilingual support functions. Context-aware computing, which fuses multiple sensing modalities, is moving into smart-city projects. Vendors that combine generative and discriminative techniques within a single platform are capturing cross-sell opportunities, thereby boosting the artificial intelligence market.

By End-user Industry: Healthcare acceleration driven by regulatory clarity

IT and Telecommunications held 27.02% market share in 2025, benefiting from extensive data resources and early cloud alignment. Healthcare is predicted to log the highest 38.35% CAGR through 2031 as regulatory pathways for diagnostic support tools become clearer. The US FDA cleared more than 110 AI-enabled radiology devices between January 2024 and May 2025, reducing reimbursement uncertainty and prompting hospital procurement cycles.

Manufacturing maintains strong demand for predictive-maintenance algorithms that curb unplanned downtime, while Retail and E-commerce invest in dynamic pricing engines that lift basket sizes. BFSI institutions deploy fraud detection platforms that reduce chargebacks and improve customer trust. Autonomous-driving initiatives keep Automotive investment robust, whereas Government and Defense agencies prioritize cyber-threat intelligence solutions that integrate AI-enabled anomaly detection.

Geography Analysis

North America remained the revenue leader with 37.12% share in 2025 thanks to deep venture capital pools, mature cloud ecosystems, and rapid enterprise adoption. Federal programs such as the CHIPS and Science Act funnel additional funding into AI-ready fabs, supporting domestic hardware supply and reinforcing the artificial intelligence market. High-performance computing clusters in Virginia, Texas, and Oregon continue to attract software start-ups that co-locate near cloud availability zones for lower latency.

Europe’s growth profile is shaped by the twin forces of strict data-privacy regulation and sizable sovereign compute budgets. GDPR compliant architectures push vendors to localize inference workloads inside regional borders, creating demand for on-prem GPU appliances. France’s public-private initiative around Mistral AI gained a €2 billion valuation in 2025 and aims to raise USD 1 billion to scale multilingual model training. Similar programs in Germany and the Nordics focus on green-data-center footprints that align with ambitious carbon-reduction targets, sustaining double-digit regional growth for the artificial intelligence market.

Asia-Pacific is projected to register a 40.75% CAGR through 2031, the fastest worldwide. China’s National Semiconductor Mission allocates RMB 1 trillion by 2030 for chips and supporting infrastructure, while India earmarks INR10,372 crore for national AI compute, propelling domestic integrators into global rankings. Japan’s multi-trillion-yen fund fast-tracks fab upgrades and light-touch AI regulation that accelerates time to commercial deployment. Southeast Asian economies, including Singapore and Malaysia, are introducing data-center tax incentives that entice hyperscalers to anchor regional hubs, further enlarging the artificial intelligence market size in the region.

Competitive Landscape

The market is consolidating around a few platform providers while leaving room for highly specialised challengers. NVIDIA captured above 80% share of AI accelerator shipments and posted USD 44.1 billion revenue in Q1 FY 2026, a 69% year-over-year jump. AMD responded with the Instinct MI325X, featuring 256 GB HBM3E and 6 TB/s bandwidth, outperforming NVIDIA’s H200 by 40% on Llama 3.1 inference benchmarks[3]MD, “AI Accelerator Roadmap,” amd.com. Intel, Graphcore, and start-ups such as Etched and Taalas have collectively raised more than USD 4 billion since 2024 to commercialize domain-specific hardware.

On the software side, OpenAI, Anthropic, and Cohere dominate foundation-model APIs. Anthropic tripled annualized revenue from USD 1 billion to USD 3 billion in the twelve months to December 2025 by positioning Claude for enterprise use cases that stress safety and auditability. Perplexity AI seeks to merge with TikTok’s US arm for USD 50 billion to couple real-time conversational search with short-form video engagement, illustrating how consumer platforms view integrated AI capabilities as an essential moat.

Systems integrators and consulting giants are scaling vertical practices. Accenture announced a USD 3 billion investment, including 40 AI studios worldwide, to build repeatable industry solutions. Deloitte, PwC, and Capgemini similarly expanded AI alliances with hyperscalers, targeting regulated industries that require turnkey governance frameworks. The resulting ecosystem competition is measured less by model parameter counts and more by proven cost savings and revenue uplift for end clients.

Artificial Intelligence Industry Leaders

IBM Corporation

Intel Corporation

Microsoft Corporation

Google LLC. (Alphabet Inc.)

Amazon Web Services Inc. (amazon.com Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Elon Musk signals potential Tesla-xAI merger aimed at integrating advanced models into autonomous-driving stacks.

- April 2025: India picks Sarvam AI to build sovereign language models, awarding a ₹220 crore grant.

- March 2025: xAI completes USD 113 billion all-stock acquisition of X to embed Grok AI across social-media surfaces.

- February 2025: AMD unveils Instinct MI325X with 256 GB HBM3E and 6 TB/s bandwidth, beating NVIDIA H200 on inference.

Global Artificial Intelligence Market Report Scope

Artificial intelligence (AI) is a simulation of human intelligence by machines through algorithms to automate and perform tasks commonly done by humans. AI is an interdisciplinary science with multiple approaches, but advancements in machine learning and deep learning create a paradigm shift in virtually every tech industry sector.

The artificial intelligence market is segmented by components (hardware and software and services), by end-user industry (BFSI, fashion and retail, healthcare and life sciences, manufacturing, automotive, aerospace and defense, construction, and other end users), by geography (North America (United States, Canada), Europe (United Kingdom, Germany, France, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Rest of Asia Pacific), Latin America, and Middle East and Africa).

The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| Hardware |

| Software |

| Services |

| Public Cloud |

| On-Premise |

| Hybrid |

| Machine Learning |

| Deep Learning |

| Natural Language Processing |

| Computer Vision |

| Generative AI |

| Context-Aware Computing and Others |

| BFSI |

| IT and Telecommunications |

| Healthcare and Life Sciences |

| Manufacturing |

| Retail and E-commerce |

| Automotive and Transportation |

| Government and Defense |

| Energy and Utilities |

| Media and Entertainment |

| Construction |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics | ||

| Rest of Europe | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Deployment Mode | Public Cloud | ||

| On-Premise | |||

| Hybrid | |||

| By Technology | Machine Learning | ||

| Deep Learning | |||

| Natural Language Processing | |||

| Computer Vision | |||

| Generative AI | |||

| Context-Aware Computing and Others | |||

| By End-user Industry | BFSI | ||

| IT and Telecommunications | |||

| Healthcare and Life Sciences | |||

| Manufacturing | |||

| Retail and E-commerce | |||

| Automotive and Transportation | |||

| Government and Defense | |||

| Energy and Utilities | |||

| Media and Entertainment | |||

| Construction | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Nordics | |||

| Rest of Europe | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

Key Questions Answered in the Report

What is the current size of the artificial intelligence market in 2026?

The artificial intelligence market size reached USD 434.42 billion in 2026 and is projected to climb to USD 2,503.13 billion by 2031.

Which segment is growing the fastest within the artificial intelligence market?

Services is expanding at a 40.85% CAGR through 2031 as enterprises seek integration expertise and ongoing optimisation.

Why are hybrid deployments becoming popular?

Hybrid architectures balance cloud scalability with on-prem cost control and data-sovereignty needs, supporting 45.55% CAGR to 2031.

Which region will register the highest growth in the artificial intelligence market?

Asia-Pacific is on track for a 40.75% CAGR through 2031 owing to sovereign AI funding and manufacturing automation programmes.

Page last updated on: