Glioblastoma Multiforme Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

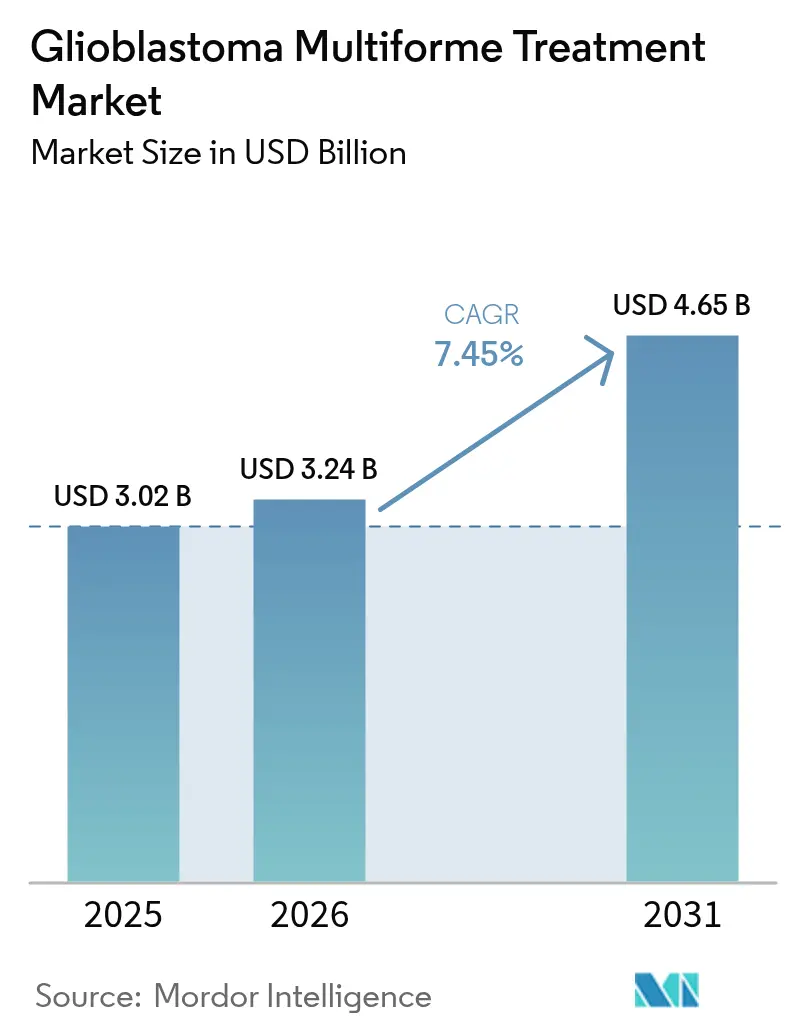

| Market Size (2026) | USD 3.24 Billion |

| Market Size (2031) | USD 4.65 Billion |

| Growth Rate (2026 - 2031) | 7.45% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Glioblastoma Multiforme Treatment Market Analysis by Mordor Intelligence

Glioblastoma multiforme treatment market size in 2026 is estimated at USD 3.24 billion, growing from 2025 value of USD 3.02 billion with 2031 projections showing USD 4.65 billion, growing at 7.45% CAGR over 2026-2031. Growing demand for therapies that prolong survival, rapid adoption of Tumor-Treating Fields (TTFields) devices, orphan-drug incentives that accelerate approvals, and steady venture funding for blood-brain-barrier (BBB)‐penetrating platforms underpin this trajectory. Investment is also spurred by the first major U.S. Food and Drug Administration (FDA) breakthrough in decades [1]U.S. Food and Drug Administration, “FDA Approvals for Oncology Drugs,” fda.gov —vorasidenib for Grade 2 IDH-mutant glioma—which has renewed confidence in multimodal development strategies. Meanwhile, physicians are shifting toward combination regimens because monotherapies deliver only incremental benefit, reinforcing the need for integrated device-drug approaches. Ongoing clinical trials that combine TTFields with immune checkpoint inhibition illustrate how developers intend to capture durable survival gains while mitigating toxicity.

Key Report Takeaways

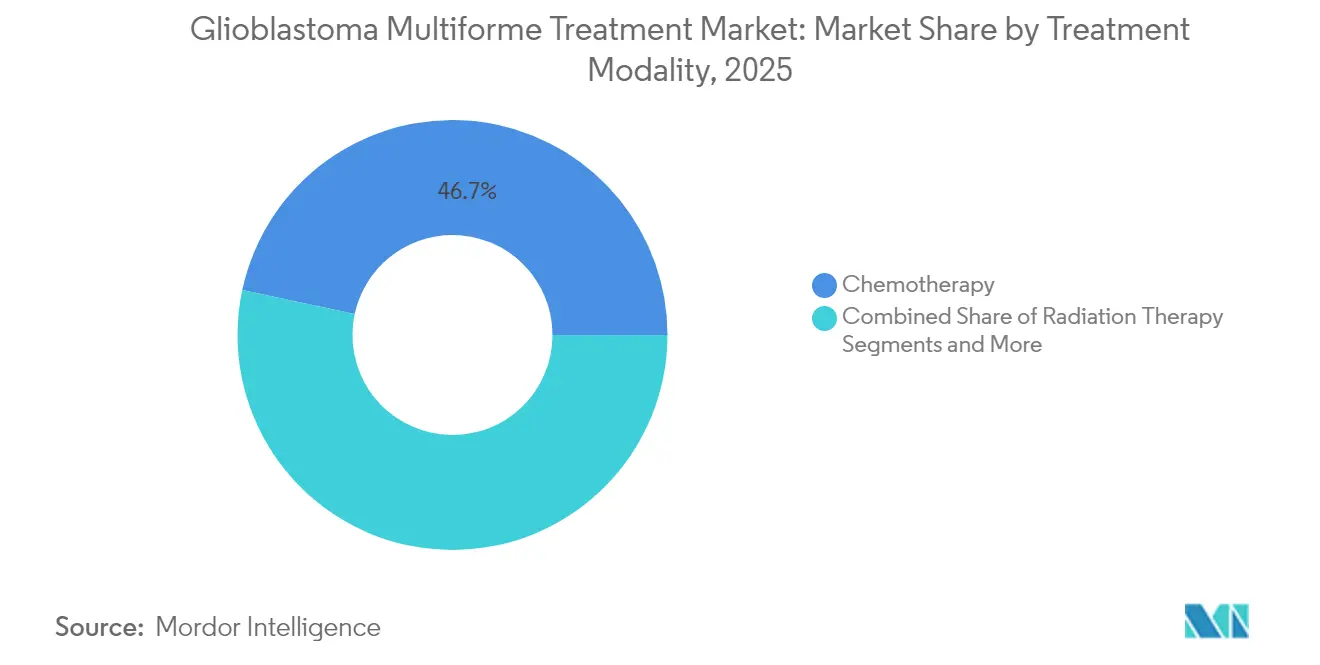

- By treatment modality, chemotherapy led with 46.65% revenue share in 2025, whereas TTFields therapy is expanding at an 8.62% CAGR through 2031.

- By patient type, newly diagnosed cases accounted for 67.92% of the glioblastoma multiforme market share in 2025, while therapies for recurrent disease are advancing at an 8.55% CAGR to 2031.

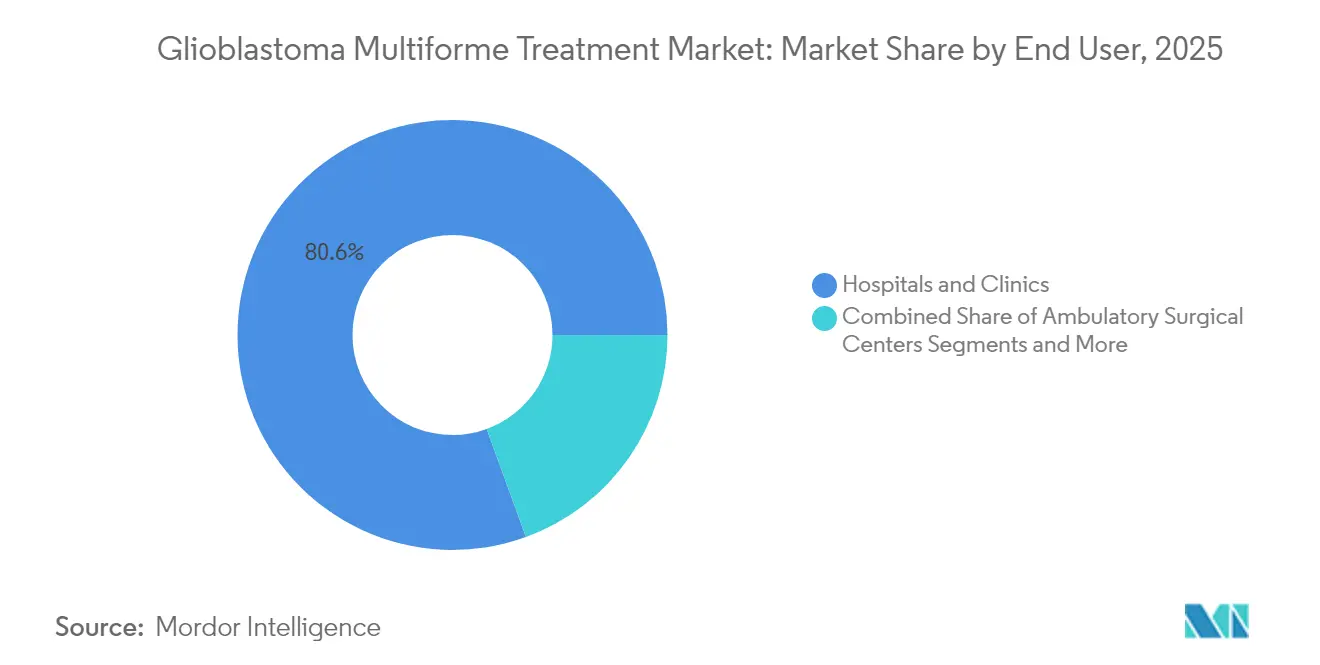

- By end user, hospitals and clinics commanded 80.55% share in 2025, and ambulatory surgical centers are projected to grow at 8.66% CAGR as outpatient pathways gain traction.

- By age group, adults commanded 67.12% share in 2025, and pediatric are projected to grow at 8.71% CAGR through 2031.

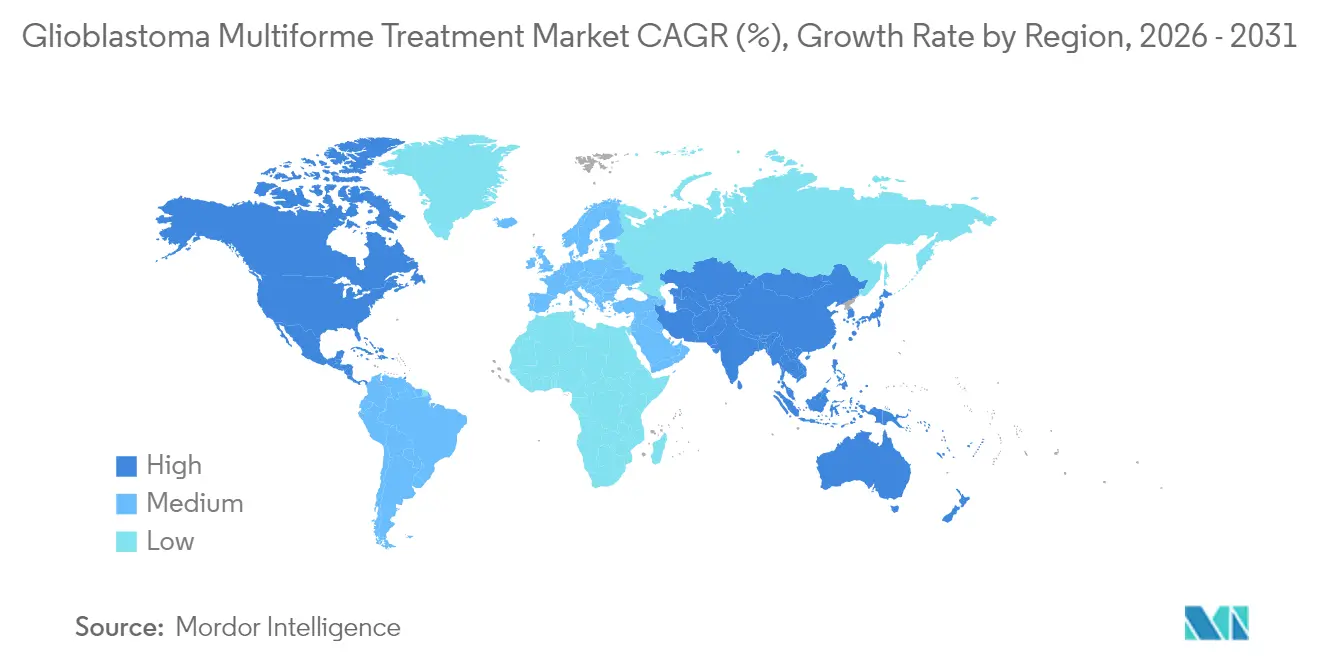

- By geography, North America retained 39.75% share in 2025, but Asia-Pacific is the fastest-growing region with a 8.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Glioblastoma Multiforme Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Incidence of High-Grade Gliomas | +1.2% | Global, with highest impact in North America & Europe | Medium term (2-4 years) |

| Age-Associated Rise in GBM Cases | +0.9% | Global, particularly developed markets with aging populations | Long term (≥ 4 years) |

| Expanding R&D Pipelines & Orphan-Drug Incentives | +1.8% | North America & EU regulatory frameworks | Medium term (2-4 years) |

| Growing Adoption of Tumor-Treating Fields (TTFields) Devices | +1.5% | North America, expanding to Europe & APAC | Short term (≤ 2 years) |

| AI-Enabled Radiogenomics Improving Early Detection | +0.7% | Advanced healthcare systems in developed markets | Long term (≥ 4 years) |

| Venture Funding Surge For BBB-Penetrating Nanocarriers | +1.1% | Global, with concentration in biotech hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Incidence of High-Grade Gliomas

Incidence trends keep the glioblastoma multiforme treatment market on a firm growth footing. Glioblastoma already represents nearly half of all malignant primary brain tumors worldwide, and rising diagnostic awareness is bringing more patients into care pathways earlier in their disease course. Neuro-oncology units at major academic centers are scaling to meet these volumes, creating predictable demand for approved drugs, TTFields devices, and related diagnostics. Higher case numbers also accelerate clinical-trial enrollment, shortening development cycles for next-generation therapies. Manufacturers leverage the larger addressable population to justify premium pricing strategies that fund further innovation.

Expanding R&D Pipelines and Orphan-Drug Incentives

Fast-track and orphan designations under U.S. and EU regulations reduce both cost and time-to-market, transforming glioblastoma from a historically unattractive niche into a commercial priority. The FDA’s orphan approval of ERAS-801 for malignant glioma and the swift clearance pathway for vorasidenib demonstrate regulators’ willingness to accept surrogate endpoints when unmet need is high. Exclusivity periods that follow such designations provide companies with revenue protection that offsets the risks associated with small patient populations. The environment is catalyzing cross-border licensing deals and big-pharma acquisitions, such as Merck’s purchase of Modifi Biosciences, targeted at overcoming temozolomide resistance [2]Merck, and Co. Inc. "Modifi Biosciences Acquired by Merck," merck.com.

Growing Adoption of Tumor-Treating Fields (TTFields) Devices

TTFields therapy is a physics-based modality that interrupts mitosis without systemic toxicity. U.S. reimbursement coverage now spans more than 600 cancer centers, enabling rapid physician uptake. Clinical data show comparable survival to chemotherapy with fewer side effects, a profile that appeals to elderly patients and payers concerned with hospitalization costs. The system’s home-use design supports outpatient management, reducing pressure on inpatient resources and creating a recurring consumable revenue stream for manufacturers. Momentum in Europe and Japan is rising as health agencies review real-world evidence packages submitted post-approval.

Venture Funding Surge for BBB-Penetrating Nanocarriers

Crossing the BBB remains the field’s central pharmacological challenge. Venture investors are channeling capital toward nanoparticle, exosome, and radiopharmaceutical platforms engineered for deep brain delivery. Eli Lilly’s USD 140 million upfront alliance with Radionetics underscores big-pharma belief that delivery breakthroughs may unlock latent efficacy in existing drug classes. Securing these funds helps small innovators advance IND-stage candidates into mid-phase trials, enriching the pipeline and broadening combination-therapy options for future regimens.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Reimbursement Hurdles for Novel Devices | -1.3% | Global, particularly in cost-conscious healthcare systems | Short term (≤ 2 years) |

| High Therapy Cost Burden & Limited Cost-Effectiveness in LMICs | -0.8% | Low and middle-income countries, emerging markets | Medium term (2-4 years) |

| Temozolomide Resistance & MGMT Heterogeneity | -1.1% | Global clinical challenge across all markets | Long term (≥ 4 years) |

| Low Real-World Compliance with TTFields Therapy | -0.6% | Markets with TTFields adoption, primarily developed countries | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Reimbursement Hurdles for Novel Devices

Health-technology assessment bodies increasingly demand real-world cost–benefit evidence before granting coverage. For TTFields, payers often require post-market studies showing reductions in hospitalizations and adverse-event management costs. Delays of 12–24 months between regulatory clearance and final reimbursement decisions prolong the path to revenue, testing the liquidity of device firms. Outcome-based contracts that shift financial risk to manufacturers are becoming standard in Europe, raising hurdles for smaller entrants.

Temozolomide Resistance and MGMT Heterogeneity

Around half of glioblastoma patients harbor MGMT promoter activity that renders temozolomide less effective, undermining the drug backbone of many current regimens. Molecular heterogeneity complicates trial design and forces developers to stratify studies, inflating costs. Resistance also shortens progression-free intervals, pushing patients rapidly into the recurrent setting where therapeutic options remain limited. The clinical community is therefore watching emerging MGMT-targeted agents closely, but until new standards emerge, this biological barrier will temper outcome gains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Modality: Device-Driven Transition Gains Pace

Chemotherapy generated 46.65% of total revenue in 2025 as generic temozolomide continues to anchor frontline protocols. TTFields therapy’s 8.62% CAGR to 2031 signals accelerating clinician confidence in a device-centric approach that avoids systemic side effects. Radiation, including proton techniques, remains critical for local control, while a growing “others” basket contains vaccine, radiopharmaceutical, and immunotherapy combinations that are moving through mid-phase trials. Market participants increasingly bundle modalities: Novocure and MSD are evaluating TTFields plus pembrolizumab in registrational studies, reflecting consensus that multimodal attack is necessary for durable survival.

The treatment‐mix shift influences supply chains and reimbursement models. TTFields systems create subscription-style consumables demand, distinct from one-time drug infusions. As new combinations reach approval, clinical pathways will feature sequential or concurrent regimens, adding complexity but enlarging the addressable spend. Developers that prove cost-effective integration of devices with drugs will capture outsized share.

By Patient Type: Recurrent Segment Catalyzes Innovation

Newly diagnosed cases dominated with 67.92% revenue in 2025, driven by the larger incident population and accepted Stupp protocol adoption. Yet the recurrent segment’s 8.55% CAGR to 2031 illustrates where the innovation frontier lies. Alpha DaRT’s FDA-supported pilot trial of radium-224 therapy and RRx-001 combination protocols are early examples of aggressive experimentation in salvage settings.

The recurrent focus encourages smaller, adaptive study designs, shortening timelines and reducing capital requirements. These features attract biotech venture funding and big-pharma option deals, as demonstrated by Merck’s acquisition of Modifi Biosciences to tackle temozolomide resistance. Success here will likely ripple into frontline standards through combination expansion, closing the loop between recurrent and newly diagnosed care algorithms.

By End User: Outpatient Care Reshapes Delivery

Hospitals and clinics captured 80.55% of spending in 2025 owing to the multidisciplinary nature of glioblastoma management. However, ambulatory surgical centers are projected to grow at 8.66% CAGR as minimally invasive resections and same-day discharge protocols proliferate. Portable TTFields systems further enable home-based treatment segments, lowering inpatient occupancy and aligning with value-based purchasing incentives.

The shift demands that technology developers design products fit for community settings, supported by tele-oncology platforms that guide treatment adherence. Health systems that move infusion and monitoring into outpatient suites will realize cost savings and throughput gains, reinforcing the trend toward decentralized neuro-oncology care.

By Age Group: Pediatric Pipeline Accelerates

Adults accounted for 67.12% of revenue in 2025, but pediatric treatments are expanding at 8.71% CAGR through 2031, stimulated by CAR-T programs targeting GD2, B7-H3, and IL-13Rα2 antigens. Orphan-drug incentives and pediatric investigation plans extend exclusivity, improving commercial viability.

At the other end of the spectrum, geriatric management emphasizes tolerability; TTFields produces fewer systemic toxicities, making it attractive in this cohort. Age-tailored regimens and dosing schedules are evolving, guided by molecular profiling that reveals biological distinctions between pediatric, adult, and elderly tumors.

Geography Analysis

North America holds 39.75% of revenue because Medicare and private insurers reimburse TTFields and the latest chemotherapeutic agents, while more than 600 clinical centers provide trial infrastructure. Regulatory clarity and orphan-drug benefits encourage rapid launch of pipeline assets, and the region’s dense venture-capital ecosystem funds early-stage innovation. Comprehensive neuro-oncology programs combine surgery, radiation, devices, and drug trials, positioning the United States as the reference market for new therapy rollouts.

Europe represents the second-largest regional opportunity but employs cost-effectiveness thresholds that mandate rigorous health-technology assessments. Germany has pioneered dendritic-cell therapy reimbursement for difficult-to-treat cancers, signaling selective openness to premium interventions. The European Medicines Agency’s centralized procedure expedites marketing authorization, yet reimbursement remains country specific, lengthening time to broad uptake. Developers must navigate outcome-based agreements that align payment with survival or quality-of-life metrics.

Asia-Pacific is the fastest-growing territory at 8.8% CAGR. Governments are investing in precision-medicine infrastructures, and major oncology hospitals are equipping operating suites for advanced neurosurgery. Japan’s universal coverage system increasingly funds high-cost therapies when domestic clinical data demonstrate benefit, and China’s centralized volume-based procurement initiatives are beginning to include neuro-oncology devices. Local manufacturers are entering the TTFields and nanoparticle spaces, thereby driving competitive pricing and broader access. Multinational firms partner with regional contract research organizations to run adaptive trials that expedite approval in key Asian markets.

Competitive Landscape

Competition spans diversified pharmaceutical companies, pure-play device manufacturers, and venture-backed biotechs. Barriers to entry stem from trial design complexity and the regulatory evidence threshold rather than scale manufacturing economies. Novocure remains the TTFields leader and is leveraging combination studies to extend its platform defensively, recently commencing a registrational program with pembrolizumab [3]Novocure Investor Relations, “Strategic Collaboration with MSD,” novocure.com . Large-cap pharma focus on molecular targets governing temozolomide resistance, illustrated by Merck’s Modifi acquisition and Eli Lilly’s radiopharmaceutical alliance with Radionetics.

Biotech entrants such as Alpha Tau Medical and companies advancing BBB-penetrating nanoparticles broaden modality diversity, often pairing assets with companion diagnostics that refine patient selection. Strategic collaborations dominate, enabling device developers to access immunotherapy pipelines and drug makers to secure delivery platforms. Real-world evidence generation is a competitive differentiator; firms that publish robust post-launch cost-utility data gain faster reimbursement approvals, expanding installed base or prescription volumes ahead of rivals.

Looking forward, market leadership will be determined by success in three arenas: cross-BBB delivery, adaptive-immunotherapy combinations, and health-economics validation. Companies that orchestrate all three will cement durable positions within the glioblastoma multiforme treatment market.

Glioblastoma Multiforme Treatment Industry Leaders

-

Arbor Pharmaceuticals, LLC

-

F. Hoffmann-La Roche Ltd

-

Merck & Co. Inc.

-

Sun Pharmaceutical Industries Ltd.

-

Teva Pharmaceutical Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Novocure received FDA approval for its Head Flexible Electrode transducer arrays for Optune Gio in adult glioblastoma patients.

- October 2024: Merck acquired Modifi Biosciences for USD 30 million upfront with milestones up to USD 1.3 billion to develop MOD-246 against temozolomide resistance.

- October 2024: Alpha Tau Medical entered the FDA TAP pilot to speed Alpha DaRT access for recurrent glioblastoma.

- July 2024: Eli Lilly paid USD 140 million upfront to partner with Radionetics Oncology on GPCR-targeted radiopharmaceuticals, retaining an option to acquire the company for USD 1 billion.

Global Glioblastoma Multiforme Treatment Market Report Scope

Glioblastoma multiforme (GBM), also known as glioblastoma, is the most common type of malignant brain tumor. A brain tumor arises from the abnormal growth of cancerous cells in the brain. The glioblastoma multiforme treatment market was segmented by treatment (chemotherapy, radiation therapy, and other treatments), end-user (hospitals/clinics and ambulatory surgical centers), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (USD) for the above segments.

| Chemotherapy |

| Radiation Therapy |

| Tumor-Treating Fields |

| Others |

| Newly Diagnosed GBM |

| Recurrent GBM |

| Hospitals and Clinics |

| Ambulatory Surgical Centers |

| Others |

| Adults |

| Pediatric |

| Geriatric |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Modality | Chemotherapy | |

| Radiation Therapy | ||

| Tumor-Treating Fields | ||

| Others | ||

| By Patient Type | Newly Diagnosed GBM | |

| Recurrent GBM | ||

| By End User | Hospitals and Clinics | |

| Ambulatory Surgical Centers | ||

| Others | ||

| By Age Group | Adults | |

| Pediatric | ||

| Geriatric | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the glioblastoma multiforme treatment market?

The market is valued at USD 3.24 billion in 2026 and is projected to reach USD 4.65 billion by 2031.

Which treatment modality is growing fastest?

Tumor-Treating Fields therapy is the fastest-growing modality with an 8.62% CAGR through 2031.

Why is North America the largest regional market?

North America benefits from broad reimbursement coverage for novel devices, established clinical-trial networks, and clear orphan-drug incentives that accelerate product launches.

What drives investment in BBB-penetrating technologies?

The blood-brain barrier limits drug efficacy; solving this challenge offers significant clinical and commercial upside, prompting deals like Eli Lilly’s USD 140 million partnership with Radionetics.

How are reimbursement hurdles impacting new devices?

Payers increasingly require outcome-based evidence and may delay coverage decisions by up to two years, pressing device firms to fund extensive post-market studies.

Which patient segment attracts the most innovation?

Therapies for recurrent glioblastoma draw intense R&D focus because current options deliver limited benefit and regulatory pathways can be shorter than for newly diagnosed disease.

Page last updated on: