Adult Malignant Glioma Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

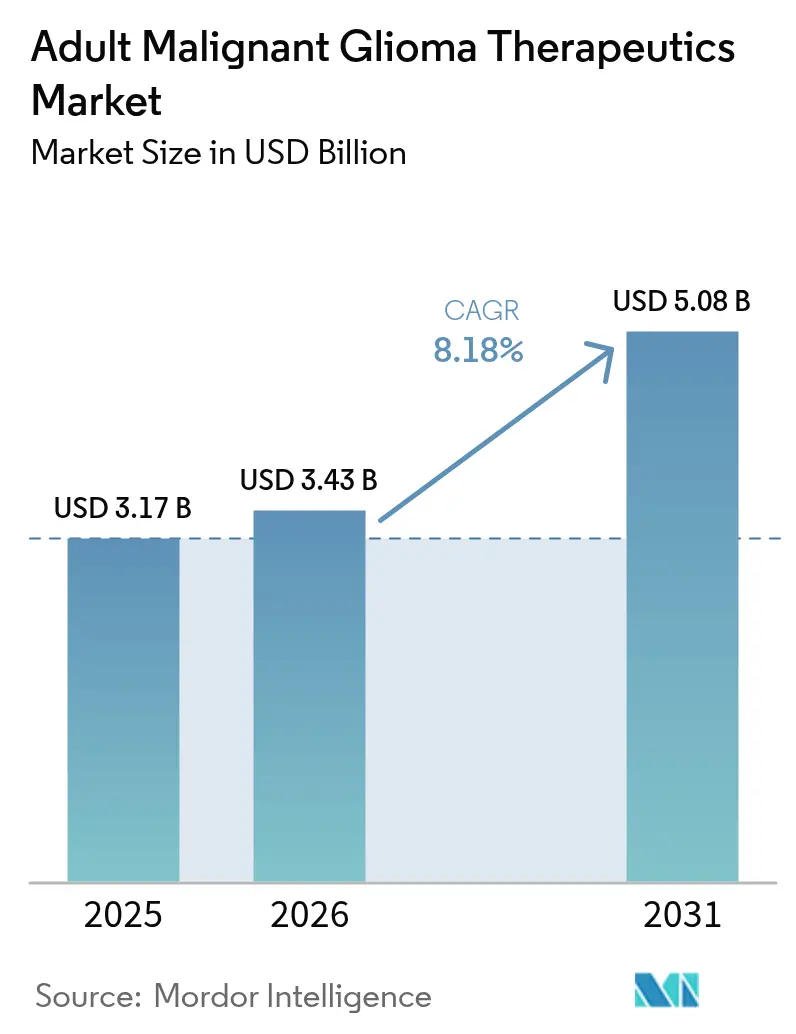

| Market Size (2026) | USD 3.43 Billion |

| Market Size (2031) | USD 5.08 Billion |

| Growth Rate (2026 - 2031) | 8.18% CAGR |

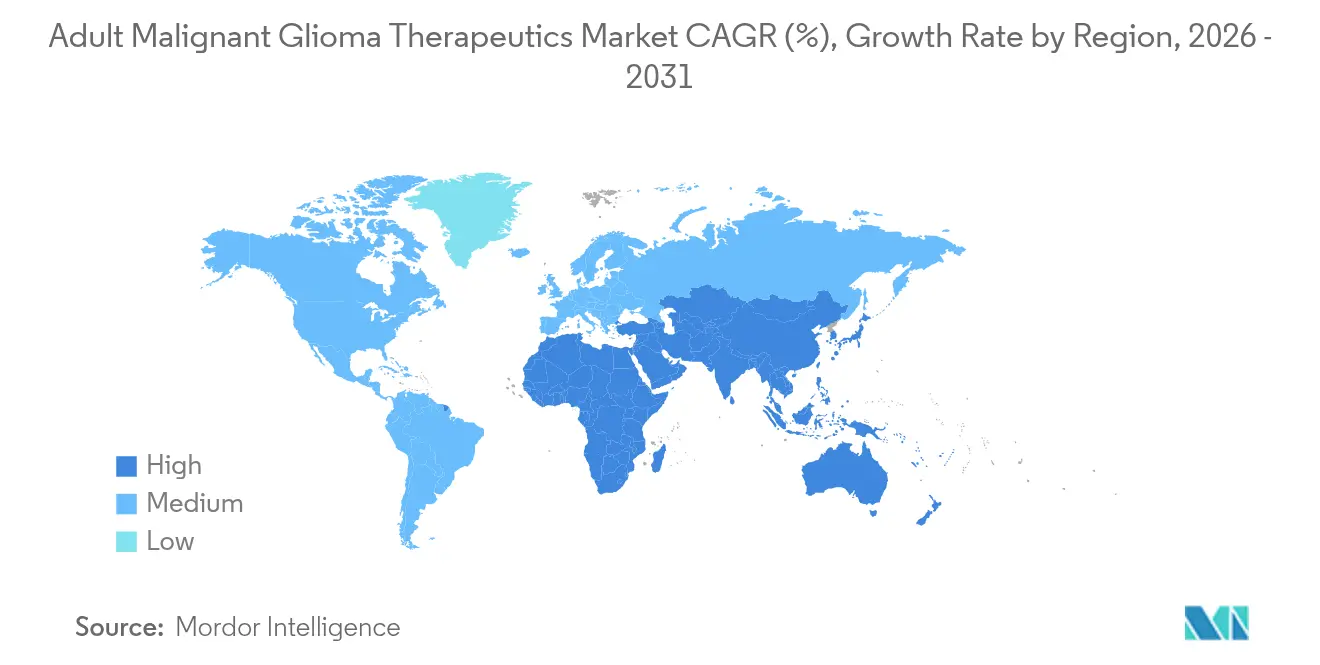

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

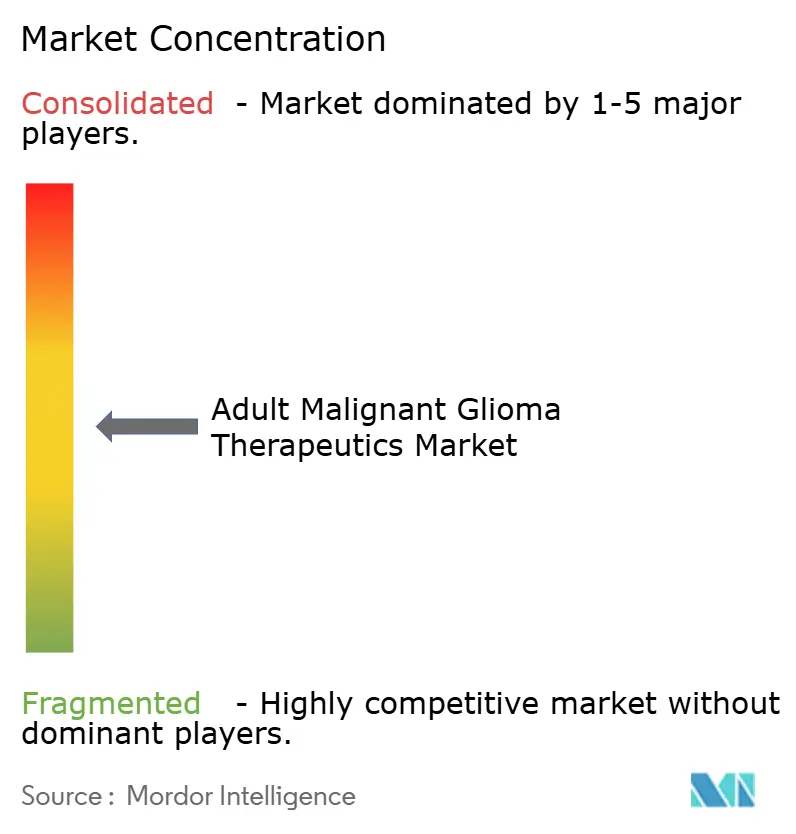

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Adult Malignant Glioma Therapeutics Market Analysis by Mordor Intelligence

The Adult Malignant Glioma Therapeutics Market size was valued at USD 3.17 billion in 2025 and estimated to grow from USD 3.43 billion in 2026 to reach USD 5.08 billion by 2031, at a CAGR of 8.18% during the forecast period (2026-2031).

Pipeline momentum stems from the FDA’s fast-track and breakthrough programs, which shorten review timelines for first-in-class assets such as LP-184, and from AI-driven diagnostic tools that improve tumor characterization and treatment matching. Venture capital continues to flow into precision platforms, while large pharmaceutical firms consolidate targeted portfolios to offset temozolomide resistance and the blood-brain-barrier delivery challenge. Regionally, North America anchors commercial uptake through reimbursement support, yet hospital network expansion and regulatory harmonization in Asia Pacific are catalyzing the next demand wave. Parallel growth opportunities arise in device-based modalities like Tumor Treating Fields (TTFields), biosimilar bevacizumab launches, and cell-based therapies that register favorable stable-disease rates in early studies.

Key Report Takeaways

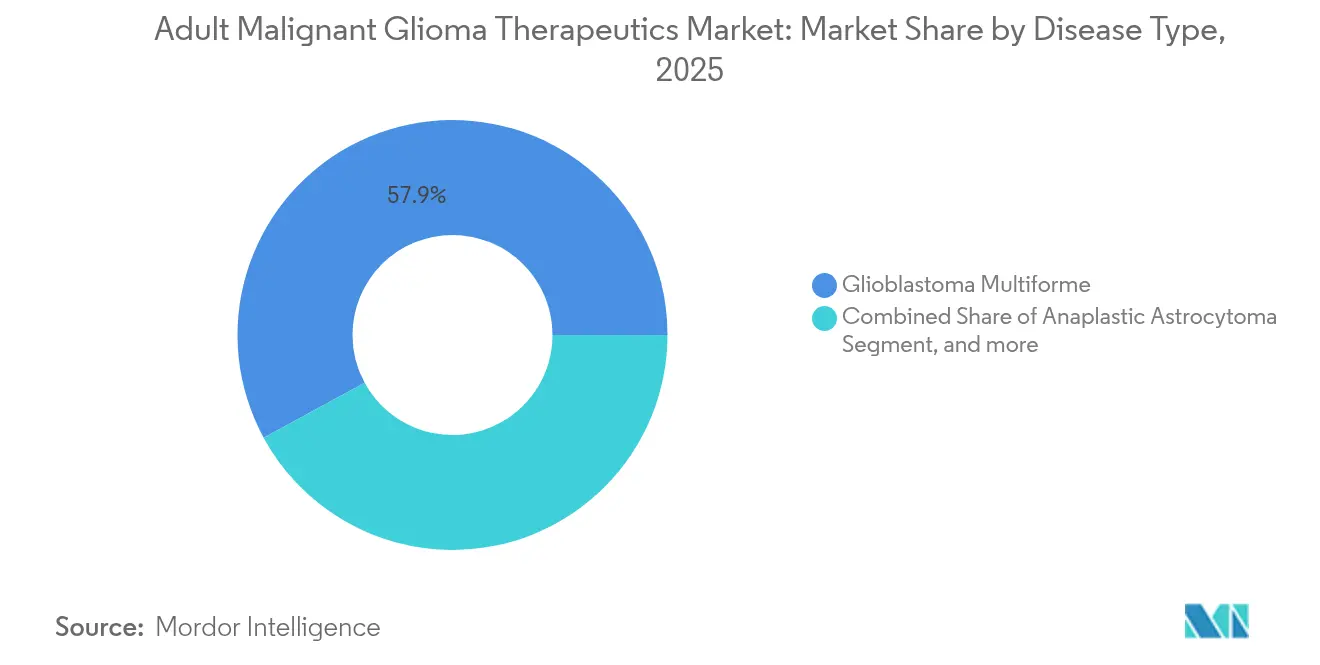

- By disease type, glioblastoma multiforme held 57.92% of the adult malignant glioma therapeutics market share in 2025, whereas anaplastic oligodendroglioma is poised for the fastest 9.12% CAGR through 2031.

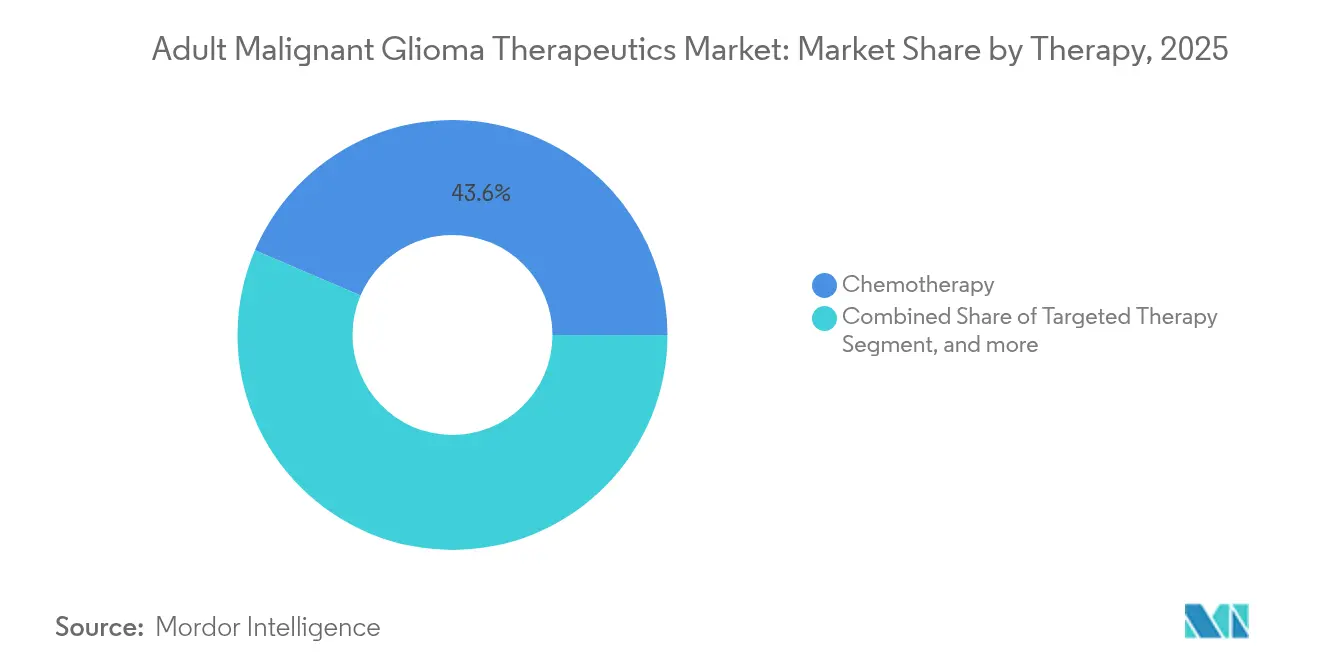

- By therapy, chemotherapy commanded 43.55% of the adult malignant glioma therapeutics market size in 2025, while immunotherapy leads growth at a 12.41% CAGR for 2026-2031.

- By geography, North America maintained 41.32% share of the adult malignant glioma therapeutics market in 2025; Asia Pacific is positioned as the fastest-growing region at an 11.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Adult Malignant Glioma Therapeutics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of malignant gliomas | +1.8% | Global, higher rates in North America & Europe | Long term (≥ 4 years) |

| Sustained public-sector R&D funding | +1.2% | North America & EU primary, spillover to APAC | Medium term (2-4 years) |

| Fast-track & breakthrough designations | +1.5% | Global, FDA-led with EMA harmonization | Short term (≤ 2 years) |

| AI-enabled early diagnosis & treatment plans | +0.9% | North America & APAC core, expanding to EU | Medium term (2-4 years) |

| Venture capital surge into BNCT platforms | +0.7% | Global, concentrated in biotech hubs | Long term (≥ 4 years) |

| Availability of bevacizumab biosimilars | +0.4% | Global, strongest in price-sensitive markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Malignant Gliomas

Epidemiological projections indicate that Asian glioma cases will jump 39.3% by 2040, fundamentally shifting the Adult malignant glioma therapeutics market toward emerging economies.[1]Clinical Trials Arena, “Asia’s Glioma Incidence Forecast to Rise 39.3% by 2040,” clinicaltrialsarena.com Improved imaging infrastructure now detects tumors earlier, adding previously undocumented patients to national registries. Younger Asian cohorts also present higher treatment tolerance, encouraging localized clinical trials and region-specific protocol adjustments. Survival rates from leading Chinese centers already surpass many Western benchmarks, implying potential biological or care-pathway differences. Drug developers therefore increase trial footprints in China, India, and South Korea to validate molecularly targeted regimens in genetically diverse populations.

Sustained Public-Sector R&D Funding

The adult malignant glioma therapeutics market benefits from government spending that offsets early-stage risk. The California Institute for Regenerative Medicine has allocated USD 11 million to UCSF’s CAR-T glioblastoma program, complementing NIH and DoD line items aimed at brain cancer.[2]UCSF News Team, “CIRM Awards USD 11 Million for CAR-T Glioblastoma Trial,” ucsfmedconnection.org Europe mirrors this trajectory through Horizon Europe grants that underpin the LEGATO study, which enrolls 411 patients at 43 sites across 11 countries. Public co-funding stretches beyond direct grants to include tax incentives and academic-industry incubators, thereby lowering capital barriers for first-in-class concepts such as synNotch cell therapies and nanoparticle delivery vehicles.

Fast-Track & Breakthrough Designations for Novel Devices

Regulators have accepted that standard 12-15-month median survival requires urgent reform, translating into unprecedented use of expedited pathways. The FDA has awarded breakthrough device designation to TTFields for brain metastases and has simultaneously fast-tracked CAN-3110, TLX101-CDx, and other assets.[3]Novocure, “FDA Grants Breakthrough Device Designation for TTFields,” novocure.com EMA’s participation in Project Orbis enables coordinated dossier reviews, compressing Europe-US launch gaps to months rather than years. Accelerated programs also unlock rolling submissions and increased agency feedback, letting small biotechs allocate resources more efficiently. Commercially, priority review vouchers linked to rare pediatric extensions provide additional monetization options, reinforcing innovation velocity across the Adult malignant glioma therapeutics market.

AI-Enabled Early Diagnosis & Treatment Planning

Machine-learning systems now translate radiological, genomic, and intraoperative data into actionable guidance. FastGlioma software offers real-time tumor segmentation during surgery, while DeepGlioma algorithms deliver IDH mutation probability scores that inform immediate therapeutic decisions. Predictive models project individual response curves for temozolomide and CAR-T candidates, improving trial stratification and resource allocation. Hospitals integrating AI workflows report shorter diagnosis-to-treatment cycles, driving better progression-free outcomes that ripple across payer evaluations. Vendors bundling AI-driven decision support with drug or device portfolios secure a competitive edge as clinical teams demand turnkey solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low late-stage trial success rates | -1.4% | Global, particularly affecting biotech sector | Medium term (2-4 years) |

| Rapid emergence of temozolomide resistance | -0.8% | Global, most pronounced in recurrent cases | Short term (≤ 2 years) |

| Boron-10 isotope supply-chain bottlenecks | -0.6% | Global, concentrated in BNCT development regions | Long term (≥ 4 years) |

| Oncology R&D capital diverted elsewhere | -0.9% | North America & Europe, spillover globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Low Late-Stage Trial Success Rates

Success rates in phase 3 glioblastoma programs remain below 5%, eroding investor confidence and inflating capital requirements. The Adult malignant glioma therapeutics market therefore witnesses portfolio diversification as companies balance high-risk CNS assets with solid-tumor franchises. Failures often stem from off-target toxicity, insufficient blood-brain-barrier penetration, or control-arm outperformance. Each setback can wipe USD 500 million in sunk costs, driving partnerships that share financial exposure. Venture syndicates react by inserting stringent milestone-based tranched financing, prolonging timelines for smaller entrants.

Rapid Emergence of Temozolomide Resistance

Within 6-12 months of therapy initiation, MGMT promoter demethylation like clusters trigger clinical relapse across many glioblastoma patients. Oncologists then pivot to bevacizumab, TTFields, or off-label checkpoint inhibitors, yet durable responses remain elusive. The Adult malignant glioma therapeutics market thus accelerates investment in resistance-overcoming strategies such as PARP inhibitor combinations and polymer-encapsulated temozolomide formulations. Regulators demand robust proof of superiority, increasing trial complexity and prolonging data accrual.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease Type: Molecular precision reorders therapeutic priorities

Glioblastoma multiforme led with 57.92% of the adult malignant glioma therapeutics market share in 2025, a level that steered sponsor focus toward blood-brain-barrier penetration chemistry and adaptive trial designs. Anaplastic oligodendroglioma, aided by IDH-targeted breakthroughs such as vorasidenib, is registering a 9.12% CAGR to 2031 and is on course to raise its contribution to the Adult malignant glioma therapeutics market size in absolute terms. Anaplastic astrocytoma garners steady funding for combination regimens, while anaplastic oligoastrocytoma benefits from refined WHO re-classification that funnels patients into mutation-specific protocols.

The success of vorasidenib, which delivered 27.7-month median progression-free survival against 11.1 months for placebo, illustrates how genotype-guided design outperforms histology-centric approaches. As panel sequencing becomes routine, developers can match small-molecule libraries to well-defined subpopulations, improving statistical power in trials and facilitating conditional approvals. The Adult malignant glioma therapeutics market therefore shifts toward smaller, faster studies that direct capital efficiency toward high-response cohorts.

By Therapy: Next-wave modalities escalate competitive churn

Chemotherapy retained 43.55% of Adult malignant glioma therapeutics market size in 2025, reflecting the entrenched use of temozolomide in newly diagnosed cases. Immunotherapy, led by early CAR-T and PD-1 combination signals, is expanding at a 12.41% CAGR and threatens to capture meaningful share once registrational trials mature. Device-based approaches such as TTFields continue to grow through label expansions and payer adoption, while gene and cell therapies advance rapidly from a small base.

Checkpoint inhibitors and CAR-T platforms now dominate conference abstracts, indicating a pipeline pivot away from monotherapy cytotoxics. The Adult malignant glioma therapeutics market responds with cooperative studies that blend TTFields electric-field disruption with immune activation or DNA-repair inhibition. Pricing flexibility for biosimilar bevacizumab further intensifies competition by freeing hospital budgets for premium novel agents, elevating barriers for follow-on chemotherapy entrants.

Geography Analysis

North America contributed 41.32% of the Adult malignant glioma therapeutics market size in 2025, supported by robust reimbursement schemes, NCI-designated trial networks, and high diagnosis rates. The United States leads in fast-track designations, enabling products like vorasidenib to move from pivotal data to approval within a year. Canada integrates provincial health technology assessments that expedite reimbursement once Health Canada decisions align with FDA precedents.

Asia Pacific is the fastest-growing theatre at an 11.55% CAGR, adding modern radiotherapy suites and accelerating inclusion of Chinese, Japanese, and South Korean centers in global protocols. Superior survival metrics reported by large tertiary hospitals in Beijing and Shanghai have triggered comparative-effectiveness collaborations to decode protocol differences. Harmonized rules under the ASEAN Mutual Recognition Arrangement further reduce barriers for device-based therapies, positioning the region as a volume and innovation hub.

Europe posts stable momentum as EMA’s Project Orbis shortens market entry gaps. Germany, France, and the United Kingdom dominate trial starts, while Southern and Eastern European countries benefit from pan-regional ethical-review alignment. Horizon Europe grants finance multi-national datasets such as LEGATO, reinforcing investigator-initiated evidence generation that feeds directly into NICE and G-BA decisions. The Adult malignant glioma therapeutics market thus enjoys continent-wide platform harmonization, improving sponsor ROI on pivotal enrollment.

Competitive Landscape

The adult malignant glioma therapeutics market is moderately concentrated, with top companies controlling meaningful revenue but leaving room for nimble biotechs that exploit niche molecular targets. Big-pharma players strengthen pipelines through buy-and-build tactics; Jazz Pharmaceuticals’ USD 935 million takeover of Chimerix for dordaviprone underscores appetite for H3 K27M-mutant assets. Novocure maintains first-mover advantage in TTFields across both adult and pediatric indications, partnering with MSD to explore checkpoint synergies.

Strategic alliances are proliferating as blood-brain-barrier delivery chemistry remains a universal hurdle. Biotechs with liposomal, polymer-conjugate, or focused-ultrasound platforms increasingly license technology rather than push full-cycle development. Intellectual-property jockeying around CAR-T engineering and neoantigen personalization intensifies, prompting cross-licensing to avoid mutual blocking worldwide.

Pricing dynamics evolve as biosimilars pressure legacy monoclonal antibodies, while orphan-drug exclusivity sustains premium positioning for mutation-specific therapies. Companies therefore embed value-based reimbursement models that tie payment to real-world outcomes, aligning economic incentives with clinical endpoints. This shift reinforces demand for AI analytics that track progression-free survival and quality-of-life metrics in near real time.

Adult Malignant Glioma Therapeutics Industry Leaders

Merck & Co. Inc.

Bristol-Myers Squibb Company

F. Hoffmann-La Roche Ltd

Bio-Rad Laboratories

Azurity Pharmaceuticals, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: FDA approved Biocon Biologics' Jobevne (bevacizumab-nwgd) biosimilar for multiple cancer indications including recurrent glioblastoma, expanding affordable treatment access and intensifying biosimilar competition.

- February 2025: FDA granted priority review to dordaviprone for H3K27M-mutant diffuse glioma with PDUFA date of August 18, 2025, representing potential first approval for this rare pediatric indication.

- August 2024: FDA approved Servier's vorasidenib (Voranigo) as first targeted therapy for Grade 2 IDH-mutant glioma, establishing new treatment standard for molecularly defined patient population.

Global Adult Malignant Glioma Therapeutics Market Report Scope

As per the scope of the report, malignant brain tumors strike deep into the psyche of those receiving and those delivering the diagnosis. Malignant gliomas, the most common subtype of primary brain tumors, are aggressive, highly invasive, and neurologically destructive tumors considered to be among the deadliest of human cancers. The Adult Malignant Glioma Therapeutics Market is Segmented by Type of Disease (Glioblastoma Multiforme, Anaplastic Astrocytoma, Anaplastic Oligodendroglioma, Anaplastic Oligoastrocytoma, and Other Types of Diseases), Therapy (Chemotherapy, Targeted Drug Therapy, and Radiation Therapy) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report offers the value (in USD million) for the above segments. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Glioblastoma Multiforme |

| Anaplastic Astrocytoma |

| Anaplastic Oligodendroglioma |

| Anaplastic Oligoastrocytoma |

| Other High-Grade Gliomas |

| Chemotherapy | Temozolomide |

| Lomustine | |

| Carmustine | |

| Bevacizumab | |

| Other Alkylating Agents | |

| Targeted Therapy | EGFR Inhibitors |

| VEGF/VEGFR Inhibitors | |

| IDH Inhibitors | |

| Immunotherapy | Checkpoint Inhibitors |

| CAR-T/NK Cell Therapy | |

| Oncolytic Viruses | |

| Device-Based Therapy | |

| Radiation Therapy | |

| Gene & Cell Therapy |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Disease Type | Glioblastoma Multiforme | |

| Anaplastic Astrocytoma | ||

| Anaplastic Oligodendroglioma | ||

| Anaplastic Oligoastrocytoma | ||

| Other High-Grade Gliomas | ||

| By Therapy | Chemotherapy | Temozolomide |

| Lomustine | ||

| Carmustine | ||

| Bevacizumab | ||

| Other Alkylating Agents | ||

| Targeted Therapy | EGFR Inhibitors | |

| VEGF/VEGFR Inhibitors | ||

| IDH Inhibitors | ||

| Immunotherapy | Checkpoint Inhibitors | |

| CAR-T/NK Cell Therapy | ||

| Oncolytic Viruses | ||

| Device-Based Therapy | ||

| Radiation Therapy | ||

| Gene & Cell Therapy | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is global spending on adult malignant glioma therapeutics in 2026?

Worldwide spending stands at USD 3.43 billion in 2026.

What compound annual growth rate is projected for this segment through 2031?

The forecast calls for an 8.18% CAGR, lifting revenue to USD 5.08 billion by 2031.

Which treatment approach currently generates the highest revenue?

Chemotherapy leads with 43.55% share, owing to the entrenched use of temozolomide.

Which disease subtype is expanding the quickest?

Anaplastic oligodendroglioma is advancing at a 9.12% CAGR on the back of IDH-targeted breakthroughs such as vorasidenib.

Which region is growing fastest in therapeutic uptake?

Asia Pacific records the highest pace, rising at an 11.55% CAGR as clinical infrastructure and regulatory harmonization improve.

What primary factor is accelerating the adoption of immunotherapy options?

Early-phase CAR-T studies demonstrating 50% stable-disease rates are encouraging clinicians to add immunotherapy to treatment plans.

Page last updated on: