Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

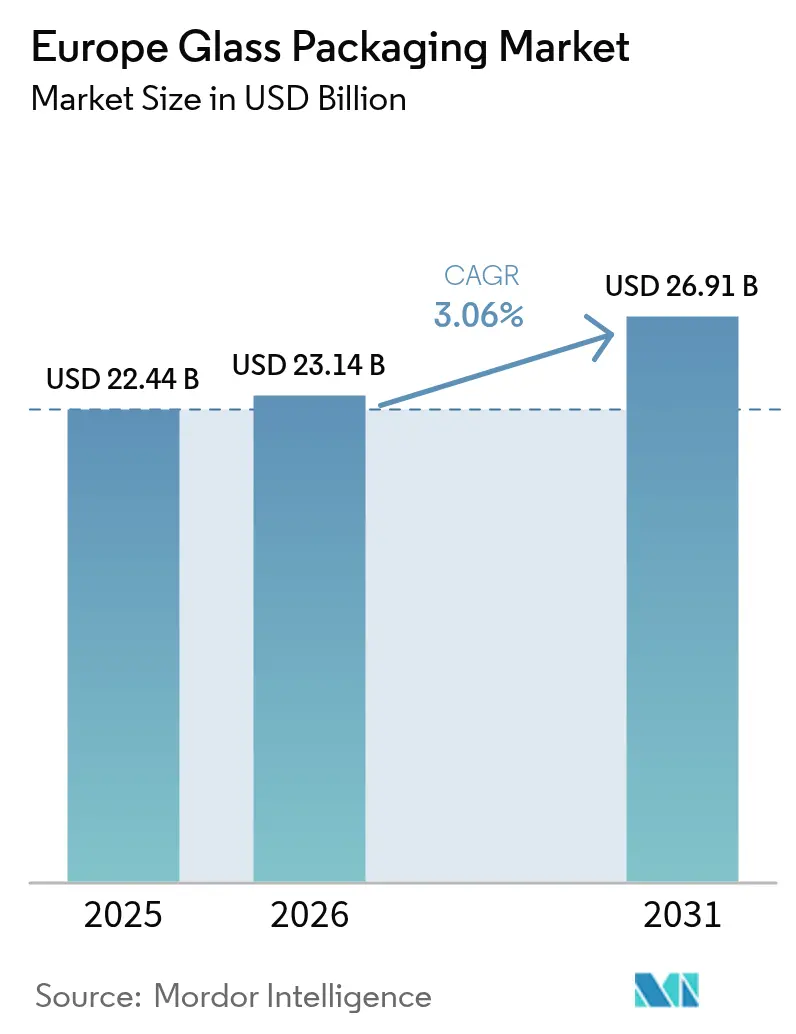

| Base Year Market Size (2025) | USD 22.44 Billion |

| Market Size (2026) | USD 23.14 Billion |

| Market Size (2031) | USD 26.91 Billion |

| Growth Rate (2026 - 2031) | 3.06% CAGR |

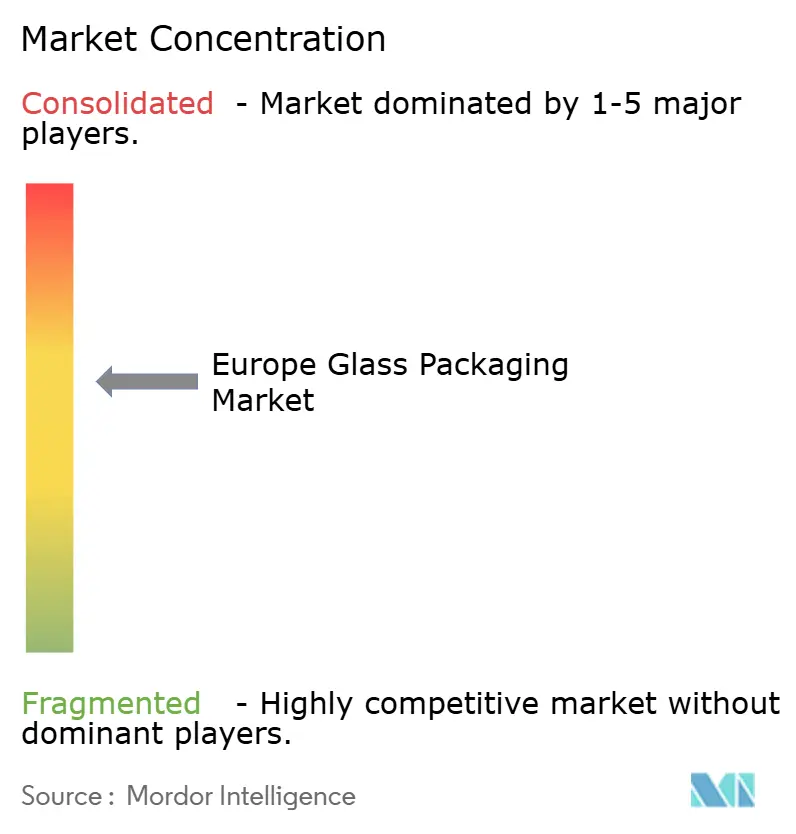

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Glass Packaging Market Analysis by Mordor Intelligence

The Europe glass packaging market size is projected to be USD 22.44 billion in 2025, USD 23.14 billion in 2026, and reach USD 26.91 billion by 2031, growing at a CAGR of 3.06% from 2026 to 2031. Germany continues to anchor demand thanks to its extensive pharmaceutical and beverage clusters, but investment is flowing steadily toward Italy, France, and Spain as converters chase faster-growing premium and pharmaceutical niches. Policy pressure from the European Union’s Packaging and Packaging-Waste Regulation, together with volatile energy prices, is accelerating the adoption of hybrid-electric furnaces and advanced cullet sorting, two enablers that protect margins while supporting climate targets. Brand owners in spirits, cosmetics, and functional beverages are paying double-digit premiums for design-rich, lightweight bottles that reinforce luxury cues and carbon credentials. In parallel, the sustained pivot toward biologics and GLP-1 therapies is lifting demand for borosilicate vials, a shift that offsets volume leakage in commodity soft-drink bottles and jars.

Key Report Takeaways

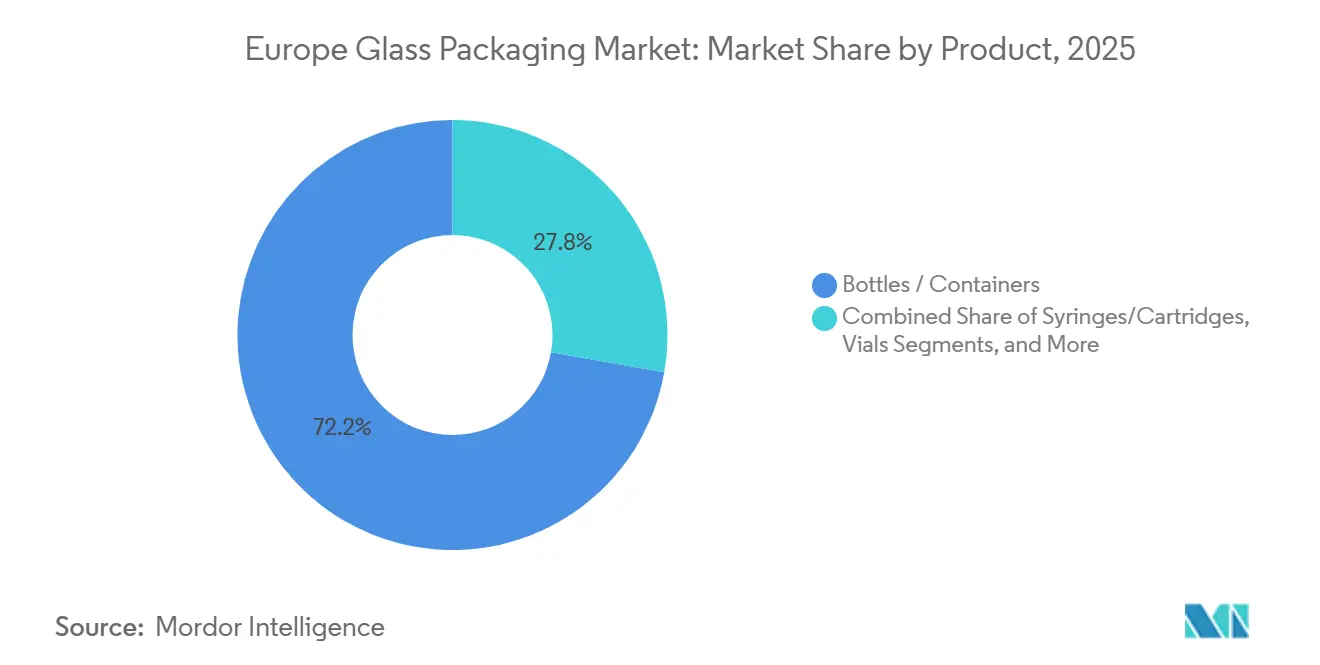

- By product, bottles and containers held 72.23% of the Europe glass packaging market share in 2025, while vials are forecast to expand at a 3.82% CAGR through 2031.

- By glass type, Type III soda-lime glass captured 44.71% share of the Europe glass packaging market size in 2025, whereas Type I borosilicate is advancing at a 3.79% CAGR over 2026-2031.

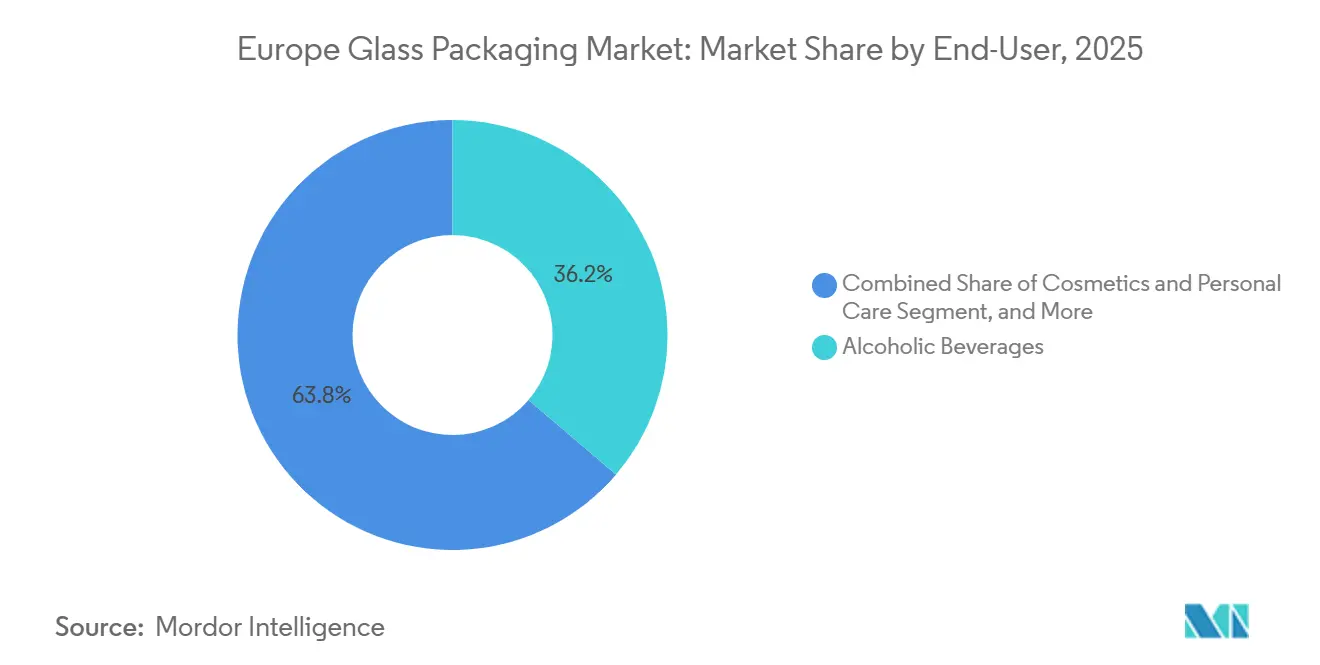

- By end-user, alcoholic beverages led with 36.24% revenue share in 2025; pharmaceutical applications are projected to grow at a 4.03% CAGR to 2031.

- By capacity range, the 100-500 ml segment commanded 41.12% share of the Europe glass packaging market size in 2025, yet formats under 30 ml are set to post a 3.73% CAGR through 2031.

- By country, Germany accounted for 24.12% of the Europe glass packaging market share in 2025, while Italy is expected to record the highest CAGR at 4.18% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Glass Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Packaging and Packaging-Waste Regulation accelerates switch to infinitely recyclable glass | +0.8% | Pan-European, with early enforcement in Germany, France, Netherlands | Medium term (2-4 years) |

| Premiumization in beverages and cosmetics boosts demand for design-rich glass bottles | +0.6% | France, Italy, Spain, United Kingdom | Medium term (2-4 years) |

| Consumer preference for inert, micro-plastic-free containers strengthens brand loyalty | +0.4% | Germany, Nordics, United Kingdom | Long term (≥ 4 years) |

| Industry shift to hybrid- or electric furnaces lowers carbon footprint | +0.5% | Germany, France, Italy, Spain | Long term (≥ 4 years) |

| AI-enabled optical sorting raises cullet quality and glass availability | +0.3% | Pan-European, led by Germany and Netherlands | Short term (≤ 2 years) |

| Rise of refill-on-the-go formats in grocery retail widens glass penetration | +0.4% | France, United Kingdom, Netherlands, Germany, Italy | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU Packaging and Packaging-Waste Regulation Accelerates Switch to Infinitely Recyclable Glass

The regulation that entered force in 2025 stipulates that 10% of beverages must move into reusable packaging by 2030, rising to 40% by 2040, giving glass a structural edge over single-use plastics and metals. Member states are rolling out deposit-return systems, and converters such as Vetropack have announced lightweight refillable lines that cut bottle weight by 30% and emissions by 85%.[1]Vetropack Austria GmbH, “Company News,” vetropack.com French extended-producer-responsibility fees are further steering wine and spirits brands toward soda-lime refillables. With compliance milestones less than four years away, long-term supply contracts for standardized refillable bottles are being signed, adding tangible momentum to the Europe glass packaging market.

Premiumization in Beverages and Cosmetics Boosts Demand for Design-Rich Glass Bottles

Spirits houses and luxury-beauty brands increasingly treat packaging as a centerpiece of product storytelling. O-I’s Contemporary Collection, launched in 2025 with 33% recycled content, targets U.K. gin producers willing to pay 15-20% extra for bespoke embossing.[2]O-I Glass Inc., “Innovation,” o-i.com Verallia’s ECOVA line adds high-definition mold technology that delivers 25% weight reduction without sacrificing shelf impact. French Cognac exporters, despite a dip in 2024 volume, shifted mix toward ultra-premium expressions, sustaining value growth. The upshot is resilient demand for short-run, high-margin bottles, a niche where lead-time agility commands pricing power.

Consumer Preference for Inert, Micro-Plastic-Free Containers Strengthens Brand Loyalty

Glass is chemically inert under ISO 4802-1, eliminating migration concerns that plague PET and coated aluminum.[3]ISO, “Standards Catalogue,” iso.org Retail case studies in Germany show 8-12% repeat-purchase lifts when premium juices switch from plastic to glass. Barrier properties also extend shelf life by up to 30%, supporting the growing functional-beverage segment. Although infrastructure build-out for refill-on-the-go systems remains uneven, early pilots by major retailers demonstrate that consumer willingness to adopt returnable jars rises when product quality and sustainability narratives align.

Industry Shift to Hybrid- or Electric Furnaces Lowers Carbon Footprint

Between 2023 and 2025, more than 100 pilot furnaces cut CO₂ by 55-64% where renewable power is available. Ardagh’s NextGen furnace in Germany, which runs partly on green hydrogen, achieved a 64% emission reduction and now serves as a template for forthcoming builds. Verallia’s fully electric furnace in Cognac operates at similar savings, enabling the company to lock in long-term contracts with spirits houses that face Scope 3 disclosure obligations. Capital outlays of USD 56-169 million per line favor the top five producers, accelerating consolidation within the Europe glass packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lightweight aluminum and PET gaining share on logistics cost advantage | -0.5% | United Kingdom, Germany, Nordics | Short term (≤ 2 years) |

| Volatile energy prices squeeze melting margins | -0.6% | Germany, Italy, Spain | Short term (≤ 2 years) |

| Gen-Z perception that boxed and canned wine is greener than glass | -0.3% | United Kingdom, Netherlands, Germany | Medium term (2-4 years) |

| Growth of concentrated and powder product formats reduces primary-pack volume | -0.2% | Pan-European | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Energy Prices Squeeze Melting Margins

Energy accounts for up to 35% of glass manufacturing costs, and European spot gas prices stayed 40-60% above pre-2022 benchmarks through 2025. Ardagh’s glass EBITDA fell in Q3 2025, and Vetropack posted a 7.2% revenue decline in H1 2025 as overcapacity met inflated utility bills. Converters are responding by signing renewable power-purchase agreements and retrofitting oxy-hybrid melters, yet the typical payback window of five to seven years delays relief, pressuring smaller players to exit or merge.

Lightweight Aluminum and PET Gain Share on Logistics Cost Advantage

In 2024, PET and aluminum accounted for 67.2% of U.K. soft-drink packaging versus glass’s 7.3%, a trend propelled by lighter shipping weights and lower breakage risk. Despite glass’s 76% EU recycling rate, perception gaps around carbon intensity persist, especially among Gen-Z consumers who value convenience and portability. Unless converters succeed in scaling lightweight, single-serve formats and communicating cradle-to-cradle benefits, share erosion in certain beverage segments could accelerate over the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Vials Capture Fastest Growth Momentum

Vials and cartridges, though smaller in volume, are rising rapidly within the Europe glass packaging market. Pharmaceutical demand for Type I borosilicate vials that ensure chemical inertness underpins a 3.82% compound growth trajectory through 2031. Stevanato Group and Gerresheimer each expanded vial capacity during 2025, in part to serve soaring GLP-1 injectable volumes. Bottles and containers retain a commanding 72.23% revenue share, mainly across wine, beer, and soft drinks. However, substitution by PET in mainstream beverages and refill-on-the-go trials in grocery channels are trimming mass-volume growth. Within vials, average unit pricing is two to three times higher than that of beverage bottles, supporting revenue resilience even when macro volumes decelerate. Converters with ISO 15378-certified cleanrooms and automated vision inspection are positioned to secure long-term supply contracts from biopharma majors, reinforcing a premium overlay within the Europe glass packaging market size equation. A second strand of opportunity lies in limited-edition spirits miniatures and fragrance samplers, segments that leverage vial-filling lines during pharmaceutical maintenance windows to diversify revenue without large capital outlays.

The market remains bifurcated between commodity lines optimized for 700 ml or 750 ml bottles and flexible lines that can shift between 2 ml vials and 500 ml flasks within 24 hours. As SKU proliferation intensifies, converters that master quick mold change and digital batch tracking will capture value. Meanwhile, legacy bottle capacity faces downward price pressure, pushing incumbents to accelerate lightweighting beyond the current 10% average and to court refill supply chains that promise higher asset turnover despite lower unit shipments. The interplay of these forces supports a gradual pivot away from volume metrics toward margin per ton, a metric that favors the specialty side of the Europe glass packaging market.

By Glass Type: Borosilicate Extends Value Leadership

Type III soda-lime accounts for 44.71% of 2025 revenue thanks to cost parity, mature recycling loops, and widespread use across alcoholic beverages. Yet borosilicate’s growth path at 3.79% through 2031 signals that the Europe glass packaging market is tilting toward value-added pharma and laboratory use cases. Borosilicate’s low thermal-expansion coefficient and high hydrolytic resistance comply with USP Type I and European Pharmacopoeia 3.2.1, making it indispensable for biologics, cell-and-gene therapies, and mRNA vaccines. Gross margins in borosilicate regularly exceed 40%, nearly double soda-lime averages, an attractive spread for capital allocation even when energy volatility persists. Germany and Italy are expanding borosilicate tubing and vial plants, often backed by long-term contracts with multinational drug producers that require validated secondary sources in Europe. Against this backdrop, soda-lime producers are intensifying lightweighting programs, aiming for 25% average weight reduction by the end of 2027 to offset freight disadvantages versus PET.

Regulatory instruments add nuance. France’s EPR scheme doubles disposal fees on non-soda-lime glass, bolstering soda-lime’s hold on wine bottles even as borosilicate gains in pharma. The net result is a dual-track investment cycle: high-volume lines pivot toward electric melting to cut cost per ton, while specialty operations channel funds into precision tubing, annealing, and cleanroom additions. This divergence underscores why the Europe glass packaging market share calculus is increasingly segmented by end-use compliance requirements rather than by glass chemistry alone.

By End-User: Pharmaceutical Outpaces Beverages in Expansion

Alcoholic beverages contributed 36.24% of 2025 demand, yet the pharmaceutical segment is projected to climb at a 4.03% CAGR, the highest among end-users. Europe’s biopharma output exceeded USD 316 billion in 2024, with biologics, biosimilars, and GLP-1 therapies all demanding superior barrier packaging. Vials, syringes, and cartridges therefore absorb fresh capacity ahead of other segments, and many converters now dedicate furnace blocks exclusively to medical glass. Spirits remain sizable, but headwinds such as Chinese anti-dumping duties on European brandy and rising demand for canned cocktails are shaving baseline growth. Cosmetics, propelled by France’s USD 56 billion beauty complex, holds mid-single-digit momentum as prestige brands elevate glass richness through color gradients and metallized closures. Soft-drink bottlers gravitate toward PET and aluminum for logistics efficiency, leaving glass suppliers to differentiate through low-run specialty SKUs, especially in craft and functional categories.

For converters, the portfolio mix is increasingly strategic. High-margin pharma orders smooth cash flows and fund furnace upgrades, while beverage contracts provide baseline tonnage that keeps melting operations continuous. Firms that orchestrate balanced allocations avoid downtime and improve asset yields, reinforcing competitive positioning across the Europe glass packaging market.

By Capacity Range: Sub-30 ml Segment Delivers Disproportionate Value

Containers between 100 ml and 500 ml generated 41.12% of 2025 sales, anchored by standard wine and spirits bottles plus personal-care formats. Yet the under-30 ml band is expected to expand at 3.73% CAGR, reflecting escalating requirements for injectable vials and luxury perfume miniatures. Each 5 ml pharmaceutical vial can command pricing equivalent to eight or nine 750 ml beverage bottles, highlighting the value density of small formats. Gerresheimer’s new Skopje plant, ramping in 2025, will specialize in 2-20 ml vials, reinforcing Europe’s sovereign supply chain goals. In parallel, fragrance houses in Milan and Paris are commissioning bespoke miniatures to support sampling drives, sometimes ordering runs as small as 10,000 units that require rapid mold change and tight dimensional tolerances.

Formats in the 30-100 ml bracket, used for spirits miniatures and travel-size cosmetics, also benefit from premiumization but face competition from aluminum for ready-to-drink cocktails. Large containers above 1,000 ml, primarily for bulk wine and food service, account for less than 5% of volume and show scant growth. The operational implication is clear: flexible forming machines and quick-cooling molds capable of handling both sub-30 ml vials and mid-range perfume flacons will unlock higher utilization. Such agility shields producers from cyclical swings in mainstream beverages while sustaining exposure to the profitable, innovation-driven niches of the Europe glass packaging industry.

Geography Analysis

Germany remains the largest national market, holding 24.12% share in 2025 thanks to its concentration of pharmaceutical OEMs in Hesse and Baden-Württemberg and strong beverage production in Bavaria and North Rhine-Westphalia. Bundesverband Glasindustrie data showed overall packaging-glass output slipping 1.0% year on year in H1 2025, yet wine and sparkling-wine bottles advanced 5.0% as domestic vintners capitalized on premium cues. Concurrently, Gerresheimer committed USD 113 million to modernize its Lohr facility with an oxy-hybrid furnace capable of cutting CO₂ 40% by 2027. Pharmaceutical glass, propelled by vaccine vial exports and sterile syringe demand, is forecast to grow 4.5% annually, buffering beverage softness.

France sits close behind and is expected to expand at a 3.4% CAGR through 2031. Spirits exports totaled USD 17.6 billion in 2024 despite volume softness, underscoring resilience at the ultra-premium tier. Verallia’s fully electric Cognac furnace, operational since 2024, now supplies lightweight yet high-definition bottles to Rémy Martin, Hennessy, and Martell, demonstrating how decarbonization bolsters competitive advantage. Meanwhile, Eco In Pack’s new refill and cleaning center in Cognac processes up to 7 million bottles per year, giving brand owners a turnkey circular solution.

Italy is on track for the region’s fastest growth at 4.18% CAGR. Stevanato and Bormioli are expanding borosilicate capacity for GLP-1 and insulin therapies, while Saverglass and Verescence tap luxury-perfume programs in Milan and Bologna. Verallia’s USD 260 million acquisition of the Corsico plant in 2024 added 225,000 tonnes of capacity that serves both pharma and beverage clients.

Spain and the United Kingdom show mixed patterns. Spain, home to Rioja and Cava producers, benefits from Verallia’s USD 113 million lightweight-bottle investment in Azuqueca. The United Kingdom struggles with higher energy tariffs, yet the launch of O-I’s Contemporary Collection has preserved glass leadership in craft gin. Rest of Europe—including Poland, Czech Republic, and Austria—grows at 2.8%, buoyed by Vetropack’s upcoming Pöchlarn plant that will supply refillables across Central Europe.

Competitive Landscape

Market concentration is moderate to high, with Ardagh, O-I, Verallia, Vidrala, and BA Glass collectively controlling roughly 60-65% of installed capacity. Each has embarked on multi-hundred-million-dollar furnace decarbonization programs to secure long-term contracts with multinational beverage and pharma companies facing Scope 3 disclosures. Verallia’s 2024 purchase of Vidrala’s Corsico plant and Vidrala’s 2025 move into Chile illustrate the dual strategy of fortifying European strongholds while capturing growth in wine-centric South America. Hybrid-electric furnaces and 50% cullet-content targets are now table-stakes for winning beverage tenders under the EU Packaging and Packaging-Waste Regulation.

Below the top tier, specialty firms such as Gerresheimer, Saverglass, and Verescence leverage ISO 15378 certifications and design studios to win high-margin pharma and cosmetics work. Gerresheimer’s Skopje investment and Verescence’s private-equity recapitalization cement this focus on premium niches. Technology partners add a further competitive layer: TOMRA and Binder+Co supply AI-enabled optical sorters that raise cullet purity, reducing batch defects and energy consumption by up to 20%.

Emergent disruptors, including refill platform MIWA and circular logistics provider zerooo, bypass legacy supply chains by co-developing proprietary bottle geometries and digital tracking, pressing incumbents to accelerate their own reuse offerings. Against this backdrop, securing renewable power-purchase agreements, flex-fuel furnaces, and standardized refillable formats will be decisive for maintaining or expanding Europe glass packaging market share over the next five years.

Europe Glass Packaging Industry Leaders

Gerresheimer AG

Verallia S.A

Vidrala, S.A.

O-I Glass, Inc.

Stoelzle Oberglas GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Vetropack Austria GmbH confirmed summer 2026 start-up of its Pöchlarn plant, producing lightweight refillable bottles that cut weight 30% and emissions 85%.

- December 2025: Vidrala S.A. agreed to acquire Cristalerías Toro in Chile for EUR 77 million (USD 87 million), closing expected early 2026.

- May 2025: Verescence SAS saw ownership changes as Movendo Capital and Draycott took equity stakes.

- May 2025: Verallia S.A. reported EUR 818 million revenue, citing beverage and specialty glass recovery.

Europe Glass Packaging Market Report Scope

Glass packaging refers to containers made from glass that are used to store, protect, and present products. It is widely used in industries such as food and beverages, pharmaceuticals, cosmetics, and chemicals because glass is safe, durable, and preserves product quality.

The Europe Glass Packaging Market Report is Segmented by Product (Bottles/Containers, Vials, Ampoules, Syringes/Cartridges), Glass Type (Type I Borosilicate, Type II Treated Soda-lime, Type III Soda-lime, Amber), End-user (Food, Soft-drink Beverages, Alcoholic Beverages, Cosmetics and Personal Care, Pharmaceutical), Capacity Range (Less Than 30 ml, 30-100 ml, 100-500 ml, 500-1,000 ml), and Country (Germany, France, Italy, Spain, United Kingdom, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

By Product

| Bottles / Containers |

| Vials |

| Ampoules |

| Syringes / Cartridges |

By Glass Type

| Type I (Borosilicate) |

| Type II (Treated Soda-lime) |

| Type III (Soda-lime) |

| Amber |

By End-user

| Food |

| Soft-drink Beverages |

| Alcoholic Beverages |

| Cosmetics and Personal Care |

| Pharmaceutical |

By Capacity Range

| Less Than 30 ml |

| 30 - 100 ml |

| 100 - 500 ml |

| 500 - 1,000 ml |

By Country

| Germany |

| France |

| Italy |

| Spain |

| United Kingdom |

| Rest of Europe |

| By Product | Bottles / Containers |

| Vials | |

| Ampoules | |

| Syringes / Cartridges | |

| By Glass Type | Type I (Borosilicate) |

| Type II (Treated Soda-lime) | |

| Type III (Soda-lime) | |

| Amber | |

| By End-user | Food |

| Soft-drink Beverages | |

| Alcoholic Beverages | |

| Cosmetics and Personal Care | |

| Pharmaceutical | |

| By Capacity Range | Less Than 30 ml |

| 30 - 100 ml | |

| 100 - 500 ml | |

| 500 - 1,000 ml | |

| By Country | Germany |

| France | |

| Italy | |

| Spain | |

| United Kingdom | |

| Rest of Europe |

Key Questions Answered in the Report

How large will the Europe glass packaging market be by 2031?

It is forecast to reach USD 26.91 billion, reflecting a 3.06% CAGR from 2026.

Which product format is growing fastest in Europe?

Pharmaceutical vials are projected to expand at 3.82% annually through 2031.

Why is borosilicate glass gaining share?

Type I borosilicate meets stringent pharma standards, and demand from biologics, vaccines, and GLP-1 therapies supports a 3.79% CAGR.

What regulatory change most affects European converters?

The EU Packaging and Packaging-Waste Regulation mandates 10% reusable beverage packaging by 2030, favoring refillable glass.

How are producers responding to energy price volatility?

Leading firms are installing hybrid-electric or fully electric furnaces and signing long-term renewable power contracts.

Which country will record the fastest market growth?

Italy is expected to lead with a 4.18% CAGR through 2031, supported by pharma and luxury-cosmetics demand.

Page last updated on: