Glass Bonding Adhesives Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.45 Billion |

| Market Size (2031) | USD 5.86 Billion |

| Growth Rate (2026 - 2031) | 5.68% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Glass Bonding Adhesives Market Analysis by Mordor Intelligence

Glass Bonding Adhesives Market size in 2026 is estimated at USD 4.45 billion, growing from 2025 value of USD 4.21 billion with 2031 projections showing USD 5.86 billion, growing at 5.68% CAGR over 2026-2031. Demand resilience stems from the material’s expanding use in laminated automotive glazing, frameless architectural façades, Mini-LED display assembly, and point-of-care medical devices, requiring precise optical clarity, reliable structural strength, and compliance with tightening environmental rules. A continual shift toward UV-curable chemistries, automation-ready dispensing systems, and vertically integrated supply chains allows suppliers to keep pace with tighter takt times in electronics and automotive plants while limiting Volatile Organic Compound (VOC) emissions. Strengthening building codes in Asia-Pacific, adoption of smart glass in premium vehicles, and rising microfluidics use in decentralized diagnostics collectively underpin the market’s medium-term growth trajectory. Nevertheless, volatile energy costs challenge epoxy and silicone feedstock economics, and biocompatibility concerns around traditional cyanoacrylates force healthcare device reform.

Key Report Takeaways

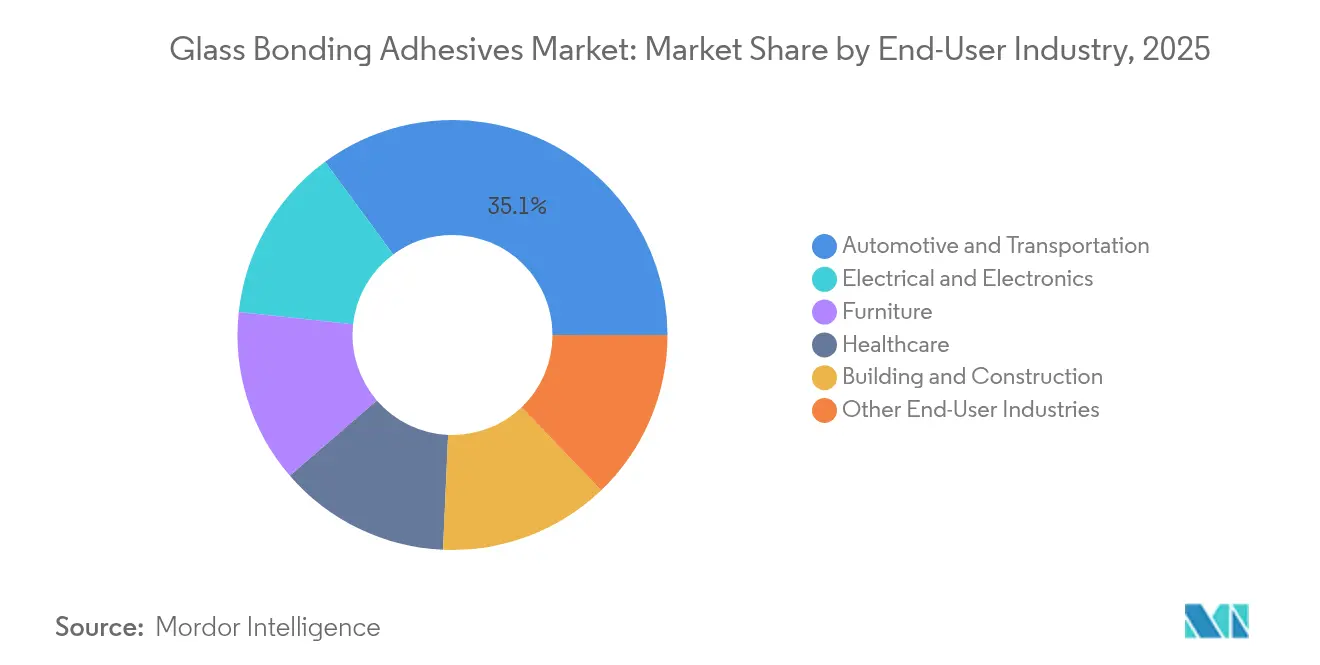

- By end-user industry, Automotive and Transportation led with a 35.10% revenue share in 2025; Electrical and Electronics is projected to expand at a 6.41% CAGR through 2031.

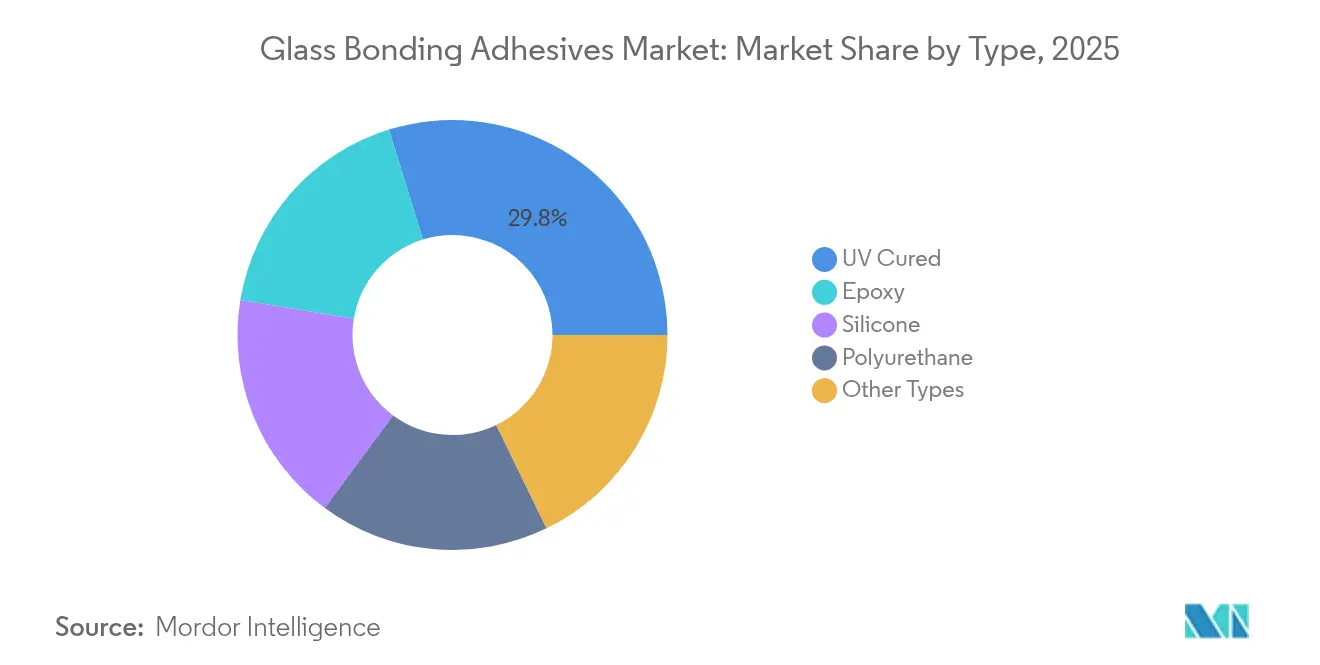

- By product type, UV-Cured formulations captured 29.78% revenue share in 2025; Silicone adhesives are set to grow the fastest at a 6.86% CAGR to 2031.

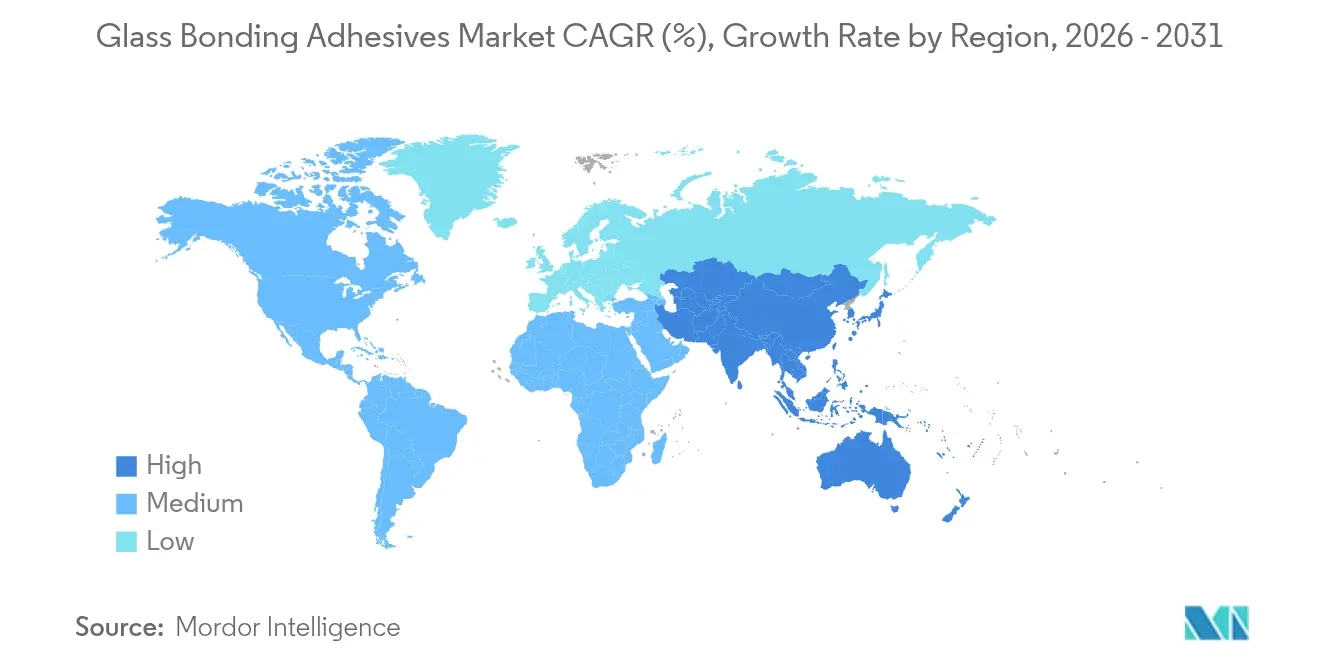

- By geography, Asia-Pacific commanded 41.02% of the 2025 revenue; the same region is forecast to post the highest 6.54% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Glass Bonding Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Laminated and Smart-glass Adoption in Automotive Glazing | +1.2% | Global, led by Asia-Pacific and North America | Medium term (2-4 years) |

| Growing Mini‐LED and Micro-LED Display Assembly Lines | +0.8% | Asia-Pacific core, North America spill-over | Short term (≤ 2 years) |

| Rapid Expansion of Frameless Architectural Façades in Asia-Pacific | +1.1% | Asia-Pacific primary, Middle East emerging | Long term (≥ 4 years) |

| Stringent VOC‐reduction Mandates Driving UV-curable Chemistries | +0.9% | Europe & North America, expanding globally | Medium term (2-4 years) |

| Rising Demand for Point-of-care Medical Diagnostics Devices | +0.6% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Laminated and Smart-glass Adoption in Automotive Glazing

Automakers are embedding heads-up displays, electrochromic layers, and sensor arrays directly into windshields, eliminating brackets and clamps in favor of transparent structural joints. PowerCure technology from Sika trims curing time by 50% relative to legacy urethanes, maintains electromagnetic transparency for Advanced Driver Assistance System (ADAS) radar, and withstands cyclic heat loads between -40°C and +120°C[1]“Structural Silicone SG-500 Data Sheet,” sika.com. Adhesives must absorb differential thermal expansion between glass and metal frames while retaining clarity under continuous UV bombardment. Premium vehicle programs deploy smart glass faster than mass-market models, yet downstream adoption is accelerating as tier-one glazing suppliers standardize on UV-stable silicones. The transition lifts unit consumption per vehicle because each laminated lite now carries more functional layers that must be sealed independently. Combined, these factors add 1.2 percentage points to the projected CAGR in the glass bonding adhesives market.

Growing Mini-LED and Micro-LED Display Assembly Lines

Smartphone, notebook, and in-car infotainment makers are commissioning high-throughput Mini-LED backplane lines that demand sub-millimeter die placement accuracy. UV-curable acrylates with outgassing below 5 ppm protect sensitive junctions, while low-shrink silicone hybrids prevent warpage of ultrathin cover glass during post-cure. X Display Company’s micro-transfer printing patents report 99.99% yield when adhesive fillets remain under 2 μm in height. Integration also extends to industrial Human-Machine Interfaces (HMIs) and avionics, where vibration tolerance and thermal cycling from -55°C to +85°C require elastic moduli in the 0.5–1.2 MPa window. Rapid assembly cycles, often under two seconds of UV exposure, translate into measurable Overall Equipment Effectiveness (OEE) gains for panel makers, supporting an additional 0.8 percentage-point lift in market CAGR.

Rapid Expansion of Frameless Architectural Façades in Asia-Pacific

Asian developers favor point-supported curtain walls and fin-backed glass roofs that rely on structural silicones to transfer wind dead loads directly into steel anchors. Sikasil SG-500 demonstrates a 25-year service life in humid tropical cycles and passes ASTM C1184 structural silicone criteria. The Crystal House case study validates UV-cured bonding of glass brick to glass mortar, achieving ±0.25 mm tolerance and a completely transparent façade. Demand for blast-resistant glazing in transport hubs stimulates hybrid epoxy-silicone tape solutions capable of dissipating peak pressures above 20 kPa without fragmenting. Combined infrastructure outlays in China, India, and Southeast Asia channel sustained double-digit volume growth for façade-grade sealants, contributing a 1.1 percentage-point CAGR uplift.

Stringent VOC-reduction Mandates Driving UV-curable Chemistries

California’s Rule 1168 and the European Green Deal limit VOCs to 50 g/L in many construction and industrial adhesives, steering buyers toward solvent-free UV systems. The United States Environmental Protection Agency (EPA) calculates up to 95% of energy savings versus thermal ovens because UV lamps deliver instantaneous polymerization. Silicone-modified polyacrylates maintain 96% transparency and grade-0 cross-cut adhesion even after 1,000 hours of xenon-arc exposure, meeting Insulated Glass Unit (IGU) durability norms. Adoption cascades into plastics bonding for electronics housings and smoke detector lenses as Original Equipment Manufacturers (OEMs) harmonize material approvals across production sites. The regulatory tailwind adds nearly 0.9 percentage points to forecast CAGR in the glass bonding adhesives market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-Price Volatility Inflating Epoxy and Silicone Feedstock Costs | -0.7% | Global, with acute impact in Europe and Asia | Short term (≤ 2 years) |

| Cytotoxicity Concerns Around Certain Cyanoacrylates in Medical Use | -0.4% | Global, with stricter enforcement in developed markets | Medium term (2-4 years) |

| Skill Gap in Precision Dispensing for Large-format Glass Panels | -0.5% | APAC and North America, with emerging impact in Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Energy-Price Volatility Inflating Epoxy and Silicone Feedstock Costs

Geopolitical tension and refinery downtimes pushed Brent crude toward USD 97 per barrel in late 2024, inflating benzene- and silicon-metal-derived intermediates. Composite resin supplier AOC raised prices by EUR 150–200 per ton in Europe, eroding margins in downstream adhesive lines. Smaller formulators often lack long-term contracts and must hold higher inventory buffers, boosting working capital and delaying innovation projects. The resulting cost pass-through threatens price-sensitive glazing or display applications, paring an estimated 0.7 percentage point from projected CAGR.

Cytotoxicity Concerns Around Certain Cyanoacrylates in Medical Use

Methyl and ethyl cyanoacrylates can trigger ocular and respiratory irritation, prompting stricter labeling and restricted use in surgical settings[2]World Health Organization, “Cyanoacrylate Exposure,” who.int. Food and Drug Administration (FDA) safety reviews document moderate allergic responses, fueling OEM demand for silicone, polyurethane, or UV-cured acrylate replacements in catheter and endoscope bonding. Reformulation cycles lengthen qualification lead times and elevate research and development (R&D) costs, subtracting roughly 0.4 percentage point from forecast CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: UV-Cured Dominance Driven by Manufacturing Efficiency

UV-cured systems accounted for 29.78% revenue in 2025 and hold center stage because one-second flash curing compresses takt times for automotive windshields and television backlight bars. The glass bonding adhesives market size tied to UV products is set to expand at 5.72% annually as OEMs retrofit mercury-free LED lamps and inline inspection sensors. Epoxies still dominate structural joints in rail windows where peel strength above 12 N/mm is mandated, but polyurethane usage is tapering under Europe’s diisocyanate restrictions. Silicone grades are expected to capture 6.86% CAGR on the back of frameless façade projects demanding extreme thermal flexibility. Hot-melt and anaerobic chemistries remain niche yet indispensable in appliance glass panels and compressor sight glasses, where process simplicity trumps optical perfection.

OEMs weigh total cost of ownership: UV rigs use 95% less energy and free valuable floor space once occupied by convection ovens. Shin-Etsu’s UV-cure Liquid Silicone Rubbers (LSRs) show cure shrinkage under 0.1%, enabling ultra-thin camera cover-glass bonding without optical distortion. Suppliers that bundle adhesives with programmable dose-/-dispense robots enlarge switching costs for customers and capture lifecycle service revenue streams.

By End-User Industry: Automotive Leadership Amid Electronics Acceleration

The glass bonding adhesives market share for Automotive and Transportation stood at 35.10% in 2025 as laminated lites, Head-Up Display (HUD) integration, and autonomous-sensor calibration drove higher grams-per-car loading. Regulatory pushes for roof-crush resistance and lighter glazing modules keep structural adhesives in focus. Electrical and Electronics applications are forecast to clock a 6.41% CAGR through 2031, propelled by Mini-LED backplanes in TVs, tablets, and automotive cockpits. Building and Construction remains the third-largest consumer of façade sealants thanks to Asia’s urban skylines, while Healthcare captures premium margins because every syringe pump manifold or single-use cartridge must satisfy biocompatibility protocols. Furniture and specialty industrial applications round out demand, utilizing clear bonds for decorative edges and machine vision enclosures where metal fasteners would obstruct fields of view.

Geography Analysis

Asia-Pacific controlled 41.02% of 2025 revenue and is tracking a 6.54% CAGR through 2031, underpinned by China’s USD 1 Trillion infrastructure program and India’s double-digit automotive output gains. Government mandates for locally sourced electric vehicle (EV) glazing add volume while incentivizing import substitution for sealants. Singapore and Xi’an plants commissioned by Sika shorten lead times and tailor formulations to humid tropical builds. Japan and South Korea provide high-value sales in Micro-LED and semiconductor wafer bonding where defect tolerances are measured in parts per billion.

North America benefits from resilient light-truck demand and a robust aerospace backlog that leverages glass cockpit displays requiring low-modulus silicone encapsulants. California’s VOC limits accelerate UV-curable uptake, prompting retrofits in Midwestern windshield plants. The United States dominates medical device consumption, reflecting stringent FDA oversight and a deep contract-manufacturing ecosystem.

Europe maintains a strong innovation base in Germany’s premium car sector and the UK’s advanced façade design practices, yet profit margins remain compressed by elevated natural-gas costs. The region’s diisocyanate restriction is nudging OEMs toward silicone or UV-modified polyacrylate formulations. South America presents emerging upside, with Brazil’s passenger-car recovery and Colombia’s urban rail projects adding incremental glass bonding adhesives market demand. Middle East & Africa growth hinges on Gulf skyscraper pipelines in Dubai, Doha, and Riyadh, where desert UV load and temperature cycling mandate premium silicone sealants. Gerresheimer’s EUR 1,120.7 million glass packaging revenue in H1 2025 also illustrates vertical synergies for regional medical consumables.

Value Chain Analysis

The value chain begins with upstream feedstocks and additives used to build base chemistries, including epoxy resins and hardeners, polyurethane prepolymers, silicone polymers, and UV-curable acrylate and oligomer systems. It also includes catalysts, fillers, adhesion promoters (such as silanes), and stabilizers that help preserve optical clarity and weathering performance. Formulators then compound these inputs into application-specific grades for automotive glazing, façade structural joints, electronics display bonding, and medical device assembly, where requirements span fast cure, low shrink, low outgassing, and durability under UV exposure and thermal cycling.

In the midstream, adhesive producers increasingly package value with process-enabling equipment and application know-how, pairing light-curable products with UV-LED lamp systems and dispensing solutions to support short takt times and tighter dimensional tolerances. Downstream distribution differs by end use: high-volume or high-reliability programs in automotive, electronics, and medical typically move toward direct supply and technical support at the customer line, while general industrial and replacement channels rely more on distributors and resellers for inventory coverage. Constraints tend to cluster around feedstock and energy cost volatility for epoxy and silicone intermediates, and around application capability gaps such as precision dispensing for large-format panels, which can increase scrap risk and extend qualification timelines.

Competitive Landscape

The Glass Bonding Adhesives market is moderately consolidated with the presence of major players, such as Henkel AG & Co. KGaA, 3M, Sika AG, H.B. Fuller Company, and Dymax Corporation. Sika reported CHF 11.24 Billion sales and used strategic purchases, MBCC Group, Cromar, and Elmich, to secure raw-material backward integration and regional distribution. H.B. Fuller reorganized into Building Adhesive Solutions to expand infrastructure exposure, while 3M deploys its Ceradyne ceramics know-how to co-engineer glass sensor housings. Competition is intensifying around low-energy, mercury-free curing lamps and bio-based raw stocks, best illustrated by Arkema’s Bostik launch of 60% bio-sourced Fast Glue Ultra+ in September 2024. Supplier differentiation ultimately rests on bundle value, advanced rheology modeling, in-line inspection algorithms, and field-service packages that minimize end-user scrap.

Glass Bonding Adhesives Industry Leaders

Henkel AG & Co. KGaA

H.B. Fuller Company

3M

Sika AG

Dymax Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are strongest where glass modules add more functionality and where customers tighten process windows, which supports continued adoption of UV-LED curable and hybrid systems that combine fast curing with high optical performance. Automotive glazing programs that integrate panoramic head-up displays and ADAS sensor content create room for adhesives that retain transparency while handling vibration and thermal cycling. DELO's March 2026 announcement of a light-activatable structural adhesive solution for panoramic HUD series production points directly to commercialization around these requirements. In parallel, bonding demand in shadowed or light-blocking areas within complex assemblies supports further refinement of light-curable platforms, including Dymax's May 2026 launch of a low-viscosity, light-curable medical adhesive aimed at difficult-to-cure geometries.

A second opportunity area is circularity and reworkability, where manufacturers focus on reducing scrap and enabling end-of-life separability without weakening bond strength during service. Henkel indicated this direction in April 2026 with Technomelt PUR hot melt featuring internal debonding capability, which links adhesive choice to repair, rework, and recycling objectives in appliance and industrial assembly that include glass components. On the supply side, regional capacity additions and localization efforts in adhesives and sealants are strengthening resilience and helping shorten lead times near manufacturing clusters; this is reflected in Dow's and SAS Chemicals' insulating glass sealant production start in Turkey (June 2024) and Sonoco's USD 30 million capacity expansion announcement (July 2025), both of which signal investment activity across construction-related and industrial adhesive supply chains.

Recent Industry Developments

- May 2026: Dymax Corporation launched HLC-M-1004, a low-viscosity, light-curable medical adhesive aimed at complex device assembly, including applications with opaque or light-blocking substrates. The release expands where light-curable glass bonding materials can be used by improving processability in difficult-to-cure geometries and supporting higher-reliability assemblies.

- April 2026: Henkel AG & Co. KGaA announced Technomelt PUR 9015 BV/WV, a polyurethane hot melt adhesive designed for appliance assembly that includes internal debonding capability. The product supports waste reduction through in-process debonding and helps enable easier component separation for repair and recycling, reinforcing a shift toward circularity-friendly bonding solutions.

- May 2025: Sika AG launched Sikaflex P2G Premium, a primerless polyurethane auto glass replacement adhesive with a 3-hour minimum drive-away time. By removing a priming step while maintaining rapid return-to-service, the launch targets higher throughput and lower labor intensity in automotive glazing replacement workflows.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers adhesives used to bond glass surfaces to another substrate, where the adhesive is the main joining method and is sold as a formulated product. Revenues are counted for adhesive chemistries that are commonly used for glass bonding across major end-use settings.

Scope exclusions: mechanical fasteners, tapes used as the primary bonding layer, and glass coating materials that do not function as structural or semi-structural adhesives.

Segmentation Overview

- By Type

- Epoxy

- Silicone

- Polyurethane

- UV Cured

- Other Types

- By End-User Industry

- Furniture

- Healthcare

- Electrical and Electronics

- Automotive and Transportation

- Building and Construction

- Other End-User Industries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the basic market boundaries and build the first set of assumptions around demand drivers, pricing direction, and regulatory context. We typically pull public statistics and reference materials such as US Census Bureau construction and manufacturing series, Eurostat industrial production data, UN Comtrade trade flows for relevant chemical categories, and IEA or similar energy and building indicators that help explain construction activity.

To understand adhesive usage patterns, we also review sources such as peer-reviewed materials and polymer journals, standards and guidance notes from recognized standards bodies, and public updates from industry associations linked to adhesives and building materials. Company annual reports, investor presentations, and reputable business press are then used to cross-check capacity moves and end-market exposure. We also use paid subscriptions for company financials and intelligence, patent databases, and shipment-level import or export records where useful. These sources are not exhaustive, and many other public documents were reviewed to collect, validate, and clarify data points.

Primary Interviews and Surveys

Primary work is used to pressure-test model assumptions that desk research cannot confirm cleanly, especially adoption by end-use, typical bonding requirements, and the way pricing moves by chemistry and application. We speak with stakeholders across adhesive producers, raw material suppliers, formulators, distributors, and downstream users in construction glazing, automotive and transportation, and electrical and electronics. We also balance perspectives across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 14% | APAC: 39% |

| Mid tier: 49% | Functional/Unit leaders: 41% | EMEA: 34% |

| Smaller Players: 17% | Managers: 45% | Americas: 27% |

Market-Sizing & Forecasting

Our sizing starts with a top-down build where construction output, automotive glazing activity, and electronics assembly indicators are translated into a realistic demand pool for glass bonding applications. We then filter that demand by penetration rates and typical adhesive intensity. To keep the math practical, we track how demand differs by bonding scenario (glass-to-glass versus glass-to-metal or glass-to-plastic), and we apply representative pricing for key chemistries.

The model is supported with selective bottom-up approximations, where supplier revenue splits, channel checks, and sampled price per kilogram times estimated volumes are used to confirm totals and adjust for undercounting. Inputs that matter in this market include renovation and new-build cycles, vehicle production and glazing trends, display and device assembly momentum, and shifts toward UV-cured and silicone systems for faster processing. We also factor in VOC and safety rules that influence formulation choices. For forecasting, we mainly use scenario analysis with a light multivariate regression check so growth can be tied back to end-market activity and expected chemistry mix shifts. These projections are validated through what interviewees expect to change over the next few years. When bottom-up signals are incomplete for smaller applications, gaps are handled by applying conservative adoption ranges and checking the implied per-unit adhesive usage against engineering norms shared in interviews.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, including demand-side indicators, supply-side movements, and pricing direction, so a single assumption does not drive the total. When the model shows large swings by region or chemistry, the drivers are rechecked and the underlying inputs are reviewed again before sign-off. Follow-up outreach is triggered when a variance cannot be explained by a clear market event.

Reports are refreshed annually. Interim updates are made when material changes occur, such as major capacity additions, regulation changes affecting formulations, or sharp feedstock price shifts that can move average selling prices. Before delivery, an analyst completes a final pass to ensure the latest public updates and interview learnings are reflected in the numbers clients receive.

Mordor Intelligence's Glass Bonding Adhesives Market Size Measured Against Other Published Estimates

Published market numbers for glass bonding adhesives can look different even when the topic name is the same, since teams may not count the same chemistries, end-uses, or bonding scenarios. The base year chosen, the way pricing is converted to USD, and how much of the supply chain is included are also common reasons for spreads.

Key gaps usually come from scope boundaries and modeling choices. Some estimates fold in adjacent adhesive uses that touch glass but are not truly glass bonding. Others assume a faster shift to premium formulations without checking if volumes can scale at that pace. By tracking chemistry mix changes, checking end-use demand signals, and refreshing currency timing, Mordor Intelligence keeps the 2026 total tied to epoxy, silicone, polyurethane, UV cured, and other defined glass bonding products across the covered regions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.45 B (2026) | |

| Global Consultancy A | USD 4.17 B (2024) | Uses a different base year and a faster growth path to 2032, and it also adds application splits (for example, glass-to-ceramic) that can widen scope depending on how specialty uses are classified. |

| Industry Research Group B | USD 3.00 B (2024) | Reports a lower starting point that appears to rely on broader, high-level application coverage with limited detail on chemistry mix and end-use weighting, which can undercount higher value UV-cured and specialty bonding demand. |

The comparison shows that most of the spread can be explained by base-year alignment and what is counted as true glass bonding versus adjacent adhesive demand. In our work, the steps are kept traceable by linking end-market activity to penetration and pricing, and then rechecking the implied totals against supplier and channel feedback before finalizing.

Key Questions Answered in the Report

What is the current value of the Glass Bonding Adhesives market?

The market is valued at USD 4.45 Billion in 2026, and it is projected to reach USD 5.86 Billion by 2031.

Which product type leads the Glass Bonding Adhesives market?

UV-cured formulations held 29.78% revenue share in 2025 thanks to rapid curing and energy-saving advantages.

Which end-user industry accounts for the highest demand?

Automotive and Transportation captured 35.10% of 2025 revenue due to the shift to laminated and smart glass assemblies.

Which region is expected to grow the fastest?

Asia-Pacific is projected to expand at a 6.54% CAGR through 2031, driven by infrastructure spending and vehicle production growth.

How are environmental regulations influencing product development?

Stricter VOC rules in Europe and North America are accelerating the shift toward solvent-free UV-curable chemistries, fostering new product launches and plant retrofits.

Page last updated on: