Elastic Bonding Adhesive And Sealant Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

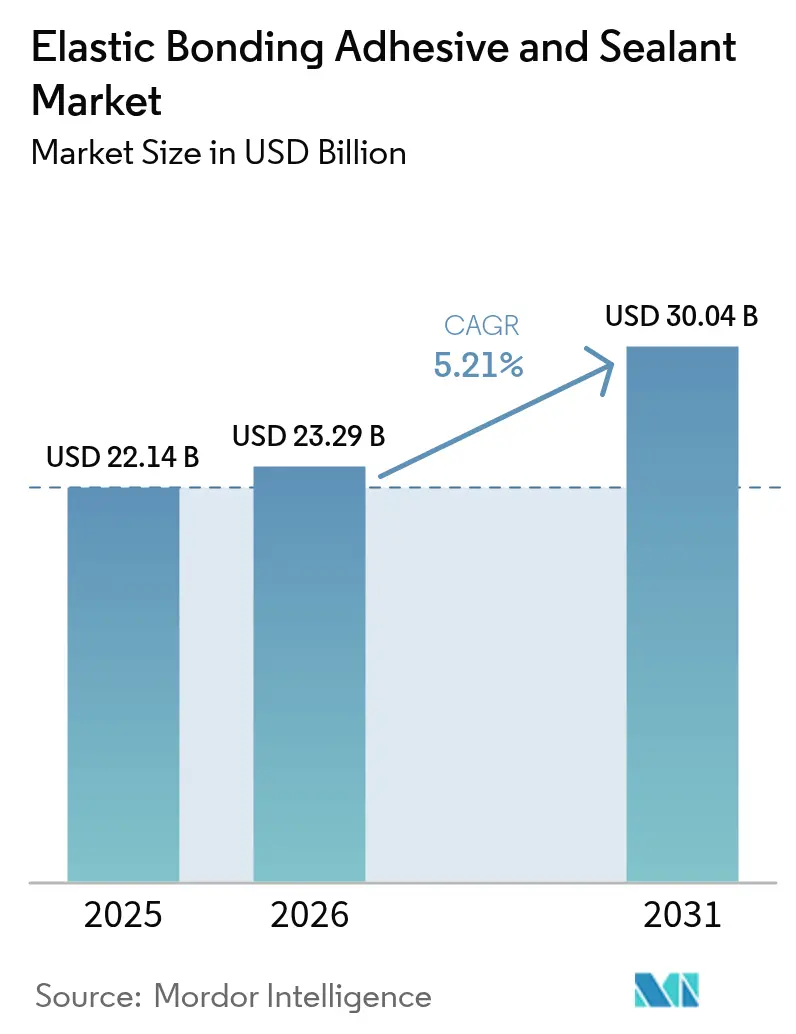

| Market Size (2026) | USD 23.29 Billion |

| Market Size (2031) | USD 30.04 Billion |

| Growth Rate (2026 - 2031) | 5.21% CAGR |

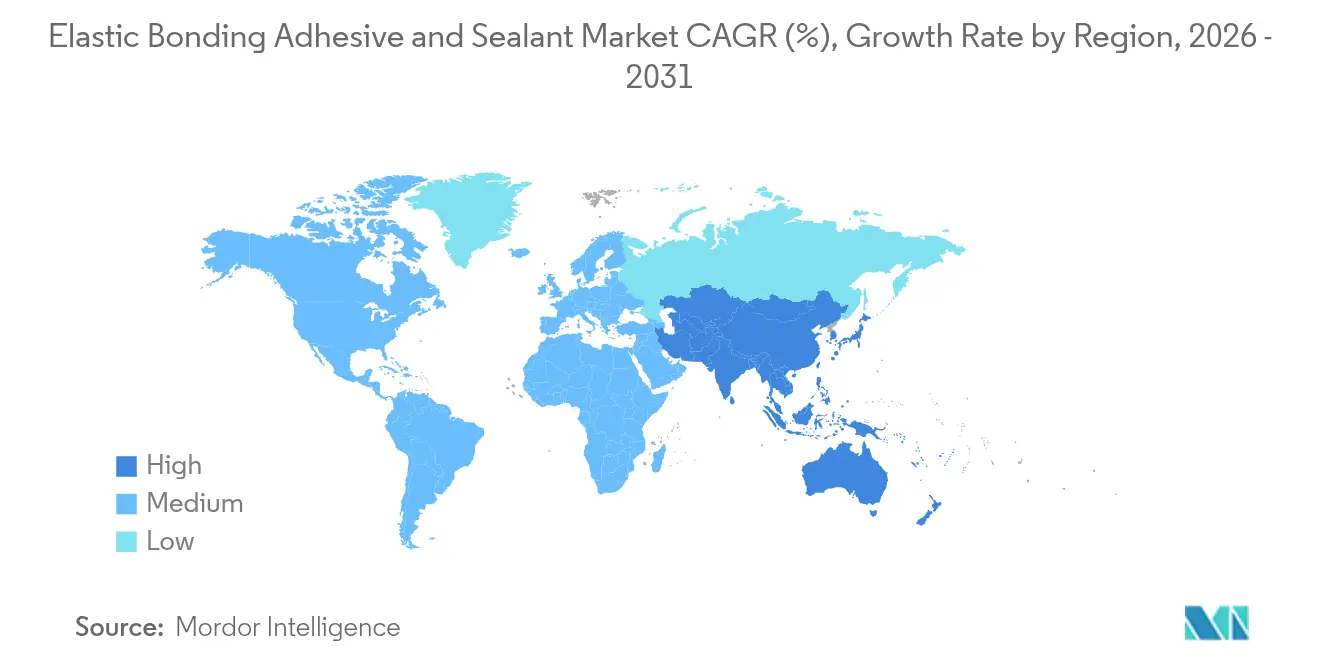

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Elastic Bonding Adhesive And Sealant Market Analysis by Mordor Intelligence

The Elastic Bonding Adhesive And Sealant market size is expected to grow from USD 22.14 billion in 2025 to USD 23.29 billion in 2026 and is forecast to reach USD 30.04 billion by 2031 at 5.21% CAGR over 2026-2031. Growing reliance on lightweight multi-material assemblies, tighter environmental rules, and demand for faster manufacturing cycles continue to steer this growth. Within automotive production, modern vehicles incorporate more than 400 linear feet of adhesive, displacing mechanical fasteners and driving repeat orders from global OEM lines. Construction firms are also shifting toward curtain walls and modular façades that need weather-resistant bonding systems able to tolerate thermal stress and UV exposure. Polyurethane grades remain the most widely specified chemistry, yet silyl-modified hybrids are rising quickly on class-leading VOC performance. Regionally, Asia-Pacific anchors supply chains, attracts fresh capacity for electric-vehicle (EV) battery pack assembly, and delivers the fastest incremental demand for the Elastic Bonding Adhesive and Sealant market. Consolidation among tier-one manufacturers persists, but scores of regional specialists still compete on niche chemistries and custom packaging formats.

Key Report Takeaways

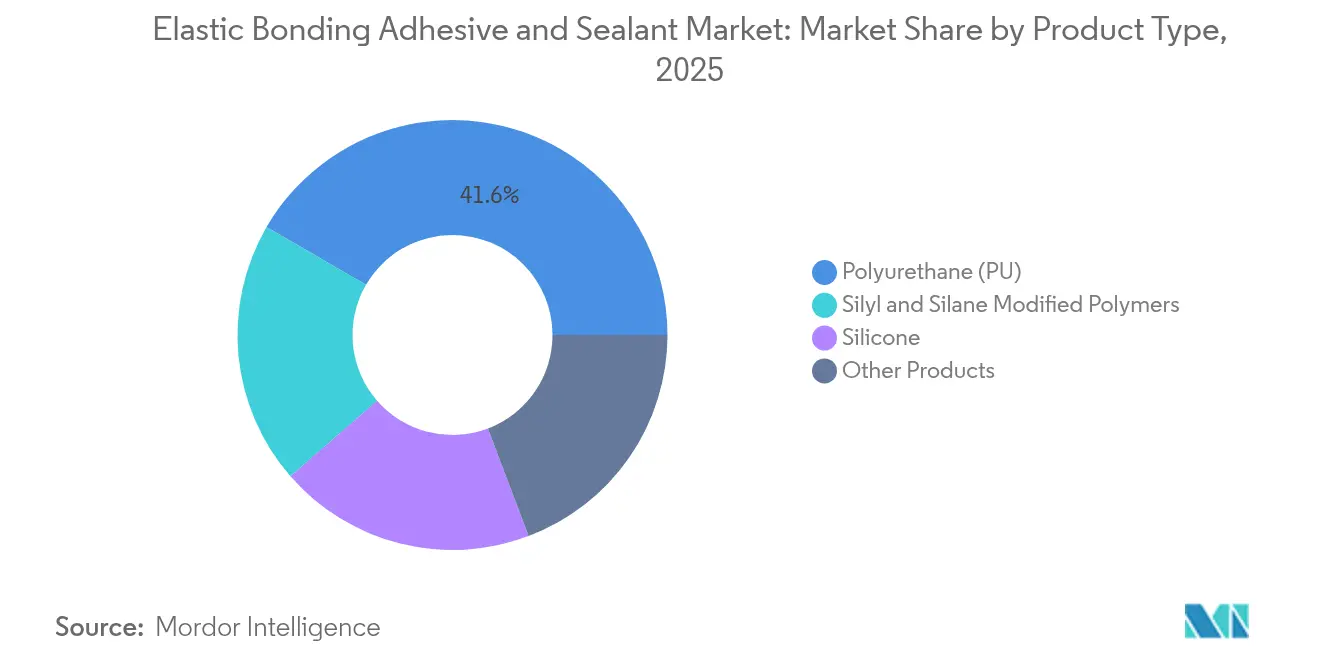

- By product type, polyurethane held 41.63% of the Elastic Bonding Adhesive and Sealant market share in 2025 while silyl and silane-modified polymers are projected to register a 7.01% CAGR to 2031.

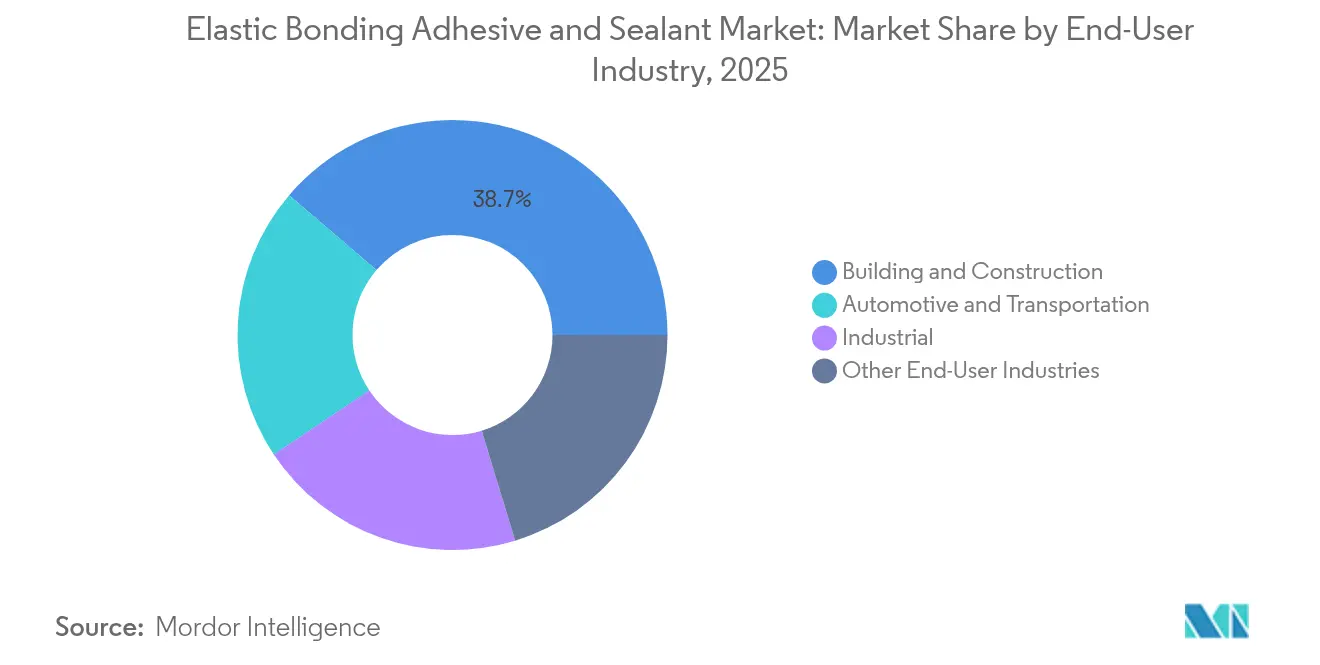

- By end-user industry, building and construction accounted for 38.74% of the Elastic Bonding Adhesive and Sealant market size in 2025 while automotive and transportation is forecast to expand at a 6.44% CAGR through 2031.

- By geography, Asia-Pacific commanded 42.88% revenue in 2025, while also advancing at a 6.67% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Elastic Bonding Adhesive And Sealant Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift to lightweight multi-material vehicle structures | +1.2% | Global, with concentration in APAC and Europe | Medium term (2-4 years) |

| Rising adoption of modular façade and curtain wall systems | +0.8% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| Stricter VOC regulations driving solvent-free chemistries | +0.6% | Global, led by California and EU regulations | Short term (≤ 2 years) |

| Wind-turbine blade fatigue mitigation needs | +0.4% | Global, concentrated in offshore wind markets | Medium term (2-4 years) |

| EV battery pack gap-filling for thermal shock control | +0.3% | APAC core, spill-over to North America and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shift to Lightweight Multi-Material Vehicle Structures

Automakers are replacing welds and rivets with high-strength bonding to shave vehicle weight, meet CO₂ targets, and improve NVH. Mixed-material bodies that combine steel, aluminum, CFRP, and bio-composites demand adhesives able to bridge wide differences in thermal expansion. Adoption grew from 30 linear feet of adhesive per car in 2001 to more than 400 feet in current models. Battery-electric vehicles deepen this dependence because cell-to-pack designs require structural bonding that also channels heat away from cells. Suppliers such as Parker LORD have released acrylic and epoxy grades tuned for peel resistance and crash energy absorption. As every tenth of a kilogram saved translates into longer driving range, the Elastic Bonding Adhesive and Sealant market captures recurring volume per new vehicle platform.

Rising Adoption of Modular Façade and Curtain Wall Systems

Architects favor prefabricated façade units to accelerate schedules, lower labor risk, and achieve sleek glass exteriors. These systems rely on structural silicone glazing that must resist hurricane-force winds, seismic sway, and UV degradation for 30 years or more. Momentive UltraGlaze sealants are already specified on landmark towers from Shanghai to Chicago[1]Momentive Performance Materials, “UltraGlaze™ Structural Silicone Glazing,” momentive.com . Ködiglaze hybrids from H.B. Fuller let designers slim frame profiles, enlarge pane area, and integrate IoT sensors without drilling hardware through the envelope. As green-building codes tighten air-leakage rates, builders opt for continuous bead bonding, which raises unit demand for the Elastic Bonding Adhesive and Sealant market.

Stricter VOC Regulations Driving Solvent-Free Chemistries

California’s Air Resources Board targets a 21-ton-per-day cut in VOC emissions from consumer and industrial sealants, forcing global adoption of solvent-free and water-borne systems. Henkel launched Loctite Liofol LA 7837/LA 6265 in July 2025 as a zero-solvent laminate adhesive that eliminates drying ovens and associated CO₂. Hybrid silyl technologies comply with EU REACH limits on diisocyanates above 0.1%, allowing applicators to avoid costly training mandates. Manufacturers racing to certify low-VOC products unlock premium pricing and higher tender eligibility, reinforcing revenue momentum across the Elastic Bonding Adhesive and Sealant market.

Wind-Turbine Blade Fatigue Mitigation Needs

Average rotor diameter already exceeds 150 meters offshore, magnifying cyclic shear on trailing-edge bonds. Delft University observed that damping in adhesive joints can rise 45% before failure, providing predictive maintenance windows. Epoxy formulations enriched with toughening agents now dominate root-joint bonding, while urethane-acrylic hybrids fill spars and shear webs to stall crack propagation. Blade makers turn to bondline-thickness optimization via FEA, spurring consultancy demand and additional liters per blade. Larger nacelle factories in China, Denmark, and the United States therefore elevate regional consumption in the Elastic Bonding Adhesive and Sealant market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility (isocyanates, silicone) | -0.7% | Global, with acute impact in Asia-Pacific | Short term (≤ 2 years) |

| Limited durability data for new hybrid chemistries | -0.5% | Global, affecting premium applications | Medium term (2-4 years) |

| Smart mechanical fasteners as substitute solutions | -0.3% | North America and EU, early adoption markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility (Isocyanates, Silicone)

Isocyanate costs surged in early 2025 after refinery outages in East Asia forced force-majeure at MDI suppliers. Silicone feedstock values swung week-to-week due to quartz shortages and freight spikes. Epoxy supply rebounded in Europe when construction demand softened, but the lack of long-term price visibility squeezes formulators’ margins. Such unpredictability delays product launches and prompts converters to carry higher inventory, weighing on near-term growth for the Elastic Bonding Adhesive and Sealant market.

Limited Durability Data for New Hybrid Chemistries

Silane-terminated polyether blends promise VOC-free curing and primer-less adhesion, yet field exposure data beyond five years remains limited. Certification bodies in façade engineering still favor legacy polyurethane or structural silicone systems because failure risk carries large liability. Universities accelerate weather-ing cycles with UV-humidity chambers, but real-world acid-rain and freeze-thaw patterns differ. Until long-term datasets mature, conservative specifiers slow mass adoption, capping highest-value gains for the Elastic Bonding Adhesive and Sealant market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Polyurethane Dominance Faces Chemistry Evolution

Polyurethane commanded 41.63% of Elastic Bonding Adhesive and Sealant market share in 2025, underlining its versatility in vehicle bodies, window frames, and wind blades. Toughness, low-temperature cure, and broad substrate compatibility keep polyurethane entrenched, yet regulatory scrutiny of free isocyanate levels creates reformulation urgency. Silyl-modified polymer demand is climbing at a 7.01% CAGR as processors seek VOC-free dispensing without secondary moisture-barrier paints. Hybrid grades blend polyurethane backbone strength with silane end-groups, extending shelf life and ensuring bubble-free cures even in humid climates. Henkel, Sika, and Bostik now supply pre-polymer blends shipped in foil packs that cut packaging waste and aid robotic application. Silicone and epoxy chemistries still serve aerospace interiors, electronics potting, and high-temperature gasketing where heat resistance above 180 °C is critical. Within these niche use-cases, premium pricing and lower volume still lift revenue per kilogram, cushioning margin pressure across the Elastic Bonding Adhesive and Sealant market.

Second-generation bio-based polyurethane pulls polyols from soybean oil and castor beans, lowering CO₂-equivalent by up to 40% against petroleum analogues. Pilot housing projects in Germany report primer-less adhesion to cross-laminated timber, opening fresh volumes in mass-timber construction. Nanotube-reinforced epoxies deliver 30% higher fracture toughness, appealing to wind-blade makers fighting edge erosion. As product portfolios diversify, distributors carry smaller lot sizes but wider SKU counts, fostering bespoke selection and advisory services that strengthen the Elastic Bonding Adhesive and Sealant market.

By End-User Industry: Construction Leadership Challenged by Automotive Acceleration

Building and construction contributed 38.74% of Elastic Bonding Adhesive and Sealant market size in 2025. Curtain wall contractors, window fabricators, and flooring installers all depend on structural bonding that resists moisture, UV, and cyclic wind load. Infrastructure stimulus packages in India and the United States fund bridge bearing pads, expansion joint sealing, and precast panel assembly that leverage high-elongation grades. Yet automotive and transportation is growing faster, with a 6.44% CAGR projected through 2031. Electric-vehicle makers bond aluminum roof panels, carbon-fiber spoilers, and battery housings in single pass robotic cells, raising unit adhesive consumption per car. Tier-1 suppliers are qualifying flame-retardant epoxies that meet UN 38.3 battery shipping rules, expanding procurement budgets. Rail carriage producers in China and Europe adopt flexible silane systems to cut vibration, reduce noise, and speed final assembly, redirecting spend toward the Elastic Bonding Adhesive and Sealant market.

Industrial machinery, marine vessel, and electronics segments offer steady baseline demand. Food-grade silicone sealants keep conveyors hygienic, while two-part acrylics bond composite boat hulls and withstand salt-spray fatigue. These applications need niche certifications, allowing formulators to defend premium margins even as mainstream prices align with lower-cost Asian imports. Cross-sector synergies- such as the same toughened epoxy serving both rotor blade spars and high-speed rail noses- highlight how innovations cascade across segments, bolstering resilience of the Elastic Bonding Adhesive and Sealant market.

Geography Analysis

Asia-Pacific generated 42.88% of global revenue in 2025 and is projected to post a 6.67% CAGR to 2031, the highest regional pace. China’s dominant battery supply chain pulls in thermally conductive gap fillers and polyurethane gasketing at double-digit growth. India’s adhesive demand surges on public-sector housing and the Make-in-India automotive push, reinforced by Henkel’s LEED-Gold Kurkumbh facility ramp-up, which shortens lead times and trims imports. Japan and South Korea focus on precision electronics and next-generation mobility, requiring ultra-low outgassing formulas for camera modules and ADAS sensors. ASEAN economies invest in mass-rapid-transit lines and data centers, both reliant on fire-retardant sealants, therefore extending the regional pull on the Elastic Bonding Adhesive and Sealant market.

North America remains the second-largest market. California’s VOC cap accelerates zero-solvent adoption, while the Inflation Reduction Act channels billions into wind-power and EV factories, each consuming kilogram-scale adhesive lines. Aerospace primes in Washington and Quebec specify high-temperature bismaleimide pastes for composite nacelles. Mexico’s export-oriented auto clusters integrate robotic bead systems that improve cycle-time predictability and cut rework, contributing new demand nodes to the Elastic Bonding Adhesive and Sealant market.

Europe blends mature demand with regulatory leadership. The August 2023 REACH limit on diisocyanates above 0.1% spurs accelerated substitution toward hybrids, pushing R&D centers in Germany, Austria, and Italy to pilot catalyst-free cure routes. Automotive assembly plants in Central Europe hunger for bonding that tolerates e-coat ovens and provides crash energy absorption. Offshore wind farms in the North Sea rely on fatigue-resistant epoxies for blade bonding, safeguarding replacement intervals. South America and the Middle East and Africa collectively hold smaller shares, yet infrastructure builds such as Brazil’s BR-163 upgrades and Saudi giga-projects open localized production incentives, pointing to future participation in the Elastic Bonding Adhesive and Sealant market.

Competitive Landscape

Market leadership is shared among global multinationals distinguished by R&D scale, application engineering teams, and vertically integrated raw-material chains. Sika posted CHF 11.24 billion sales in 2023, using profits to expand admixture-ready silane lines[2]Sika AG, “Annual Report 2024,” sika.com . Henkel’s Adhesive Technologies logged EUR 5.475 billion in H1 2024 and recently agreed to co-develop CO₂-based methanol routes with Celanese, targeting cradle-to-gate carbon cuts. 3M continues to restructure toward higher-growth safety and industrial businesses and authorized a USD 7.5 billion share buyback in February 2025, signaling balance-sheet strength.

Saint-Gobain’s USD 1.025 billion purchase of FOSROC in July 2024 extends reach in Middle Eastern construction bonding. Parker Hannifin scales CoolTherm production at its Ohio plant, supplying EV battery customers in the United States and Korea. Regional specialists, such as Wacker and Shin-Etsu, defend silicone niches through backward-integrated monomer capacity. Despite moderate concentration, new entrants supplying bio-based chemistries and nano-reinforced hybrids keep pricing competitive, capping gross margins at midsized formulators. Technical service, digital dispensing analytics, and in-line visualization of cure profiles become differentiators rather than mere product specification, shaping competitive tactics within the Elastic Bonding Adhesive and Sealant market.

Elastic Bonding Adhesive And Sealant Industry Leaders

Henkel AG & CO. KGaA

Sika AG

3M

H.B. Fuller Company

Arkema (Bostik)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Henkel introduced Loctite Liofol LA 7837/LA 6265, a solvent-free elastic adhesive system for sustainable packaging applications. The system eliminates energy-intensive drying processes while maintaining high-speed processing capabilities for pet food and ready meal packaging. It addresses the increasing demand for environmentally friendly packaging solutions and reduces CO2 emissions throughout the production cycle.

- April 2024: MAPEI S.p.A introduces Mapeflex MS 55, a hybrid elastic adhesive and sealant with a high modulus of elasticity. The product, suitable for both professional and domestic applications, combines silicone and polyurethane systems. Its features include straightforward application and smoothing capabilities, compatibility with damp or wet surfaces, and extended durability.

Global Elastic Bonding Adhesive And Sealant Market Report Scope

The elastic bonding adhesive and sealant market report includes:

| Polyurethane (PU) |

| Silyl and Silane Modified Polymers |

| Silicone |

| Other Products |

| Building and Construction |

| Automotive and Transportation |

| Industrial |

| Other End-User Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product Type | Polyurethane (PU) | |

| Silyl and Silane Modified Polymers | ||

| Silicone | ||

| Other Products | ||

| By End-User Industry | Building and Construction | |

| Automotive and Transportation | ||

| Industrial | ||

| Other End-User Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the Elastic Bonding Adhesive and Sealant market?

The Elastic Bonding Adhesive and Sealant market size reached USD 23.29 billion in 2026.

Which region leads demand for elastic bonding products?

Asia-Pacific holds the largest revenue share at 42.88% thanks to strong automotive, construction, and battery manufacturing bases.

Which end-user segment is growing the fastest?

Automotive and transportation is expanding at a 6.44% CAGR through 2031 as EV production accelerates.

Why are silyl-modified polymers gaining popularity?

They cure without emitting VOCs and avoid diisocyanate restrictions, resulting in a projected 7.01% CAGR to 2031.

How do VOC regulations affect adhesive formulation?

Stricter limits in California and the EU push formulators toward solvent-free systems, boosting demand for hybrid chemistries.

Page last updated on: