Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

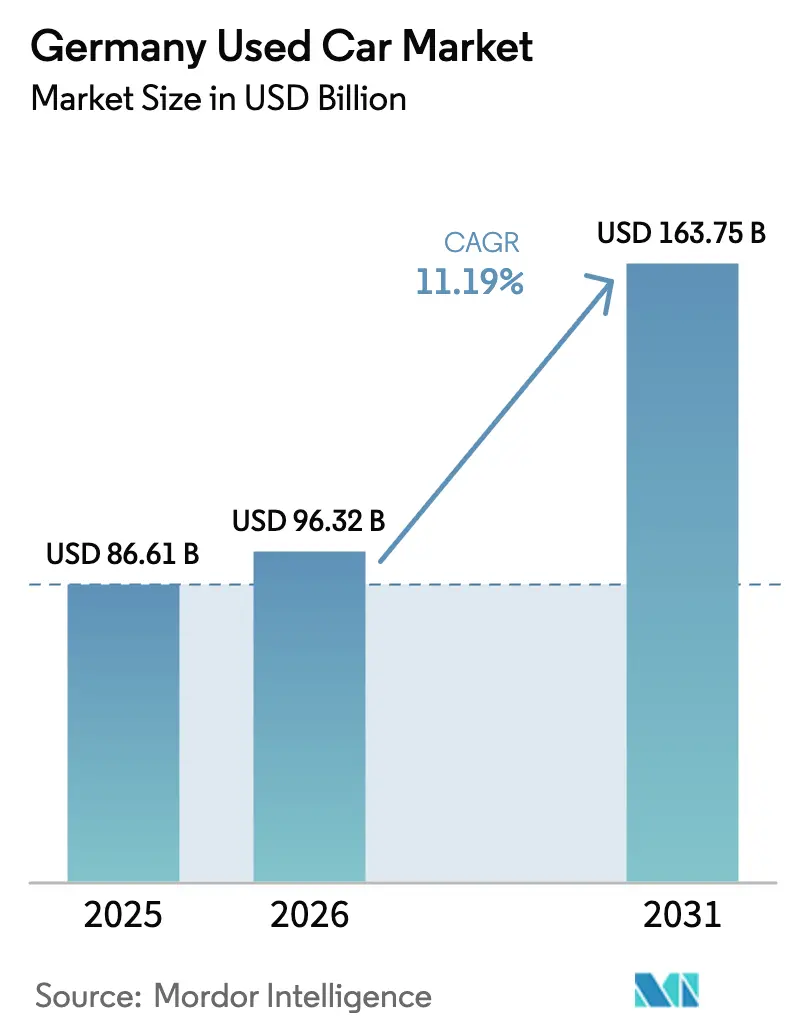

| Base Year Market Size (2025) | USD 86.61 Billion |

| Market Size (2026) | USD 96.32 Billion |

| Market Size (2031) | USD 163.75 Billion |

| Growth Rate (2026 - 2031) | 11.19% CAGR |

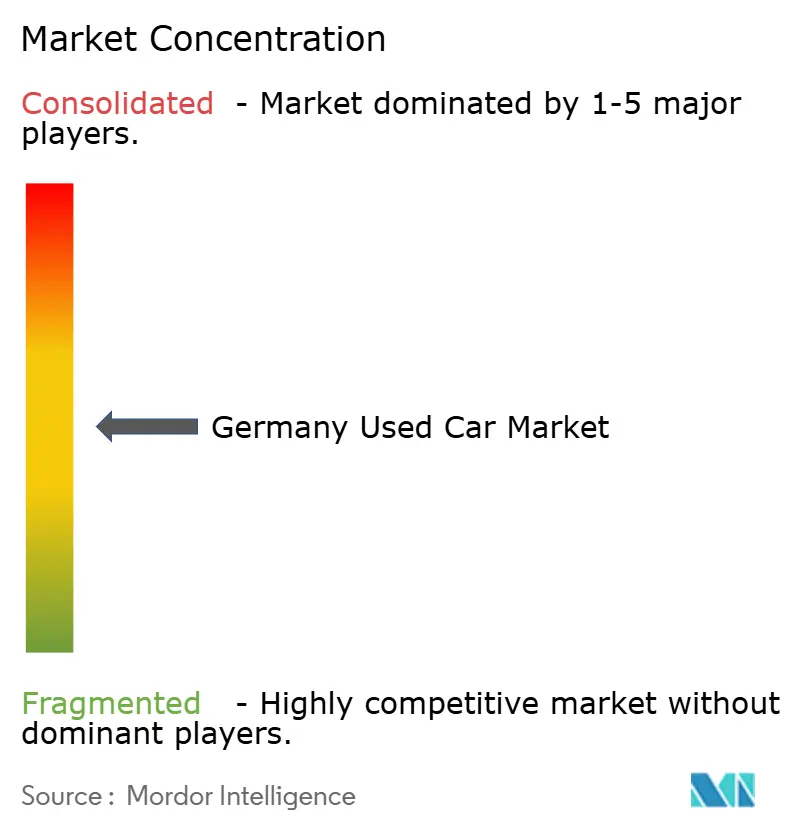

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Germany Used Car Market Analysis by Mordor Intelligence

The German used car market size was valued at USD 86.61 billion in 2025 and estimated to grow from USD 96.32 billion in 2026 to reach USD 163.75 billion by 2031, at a CAGR of 11.19% during the forecast period (2026-2031). Robust demand stems from tight new-car supply, an aging national vehicle fleet, and the rapid uptake of online transaction platforms that reduce friction in vehicle sourcing and sales. Policy drivers such as the European Union Battery Regulation, broader low-emission-zone roll-outs, and OEM-backed certified-pre-owned (CPO) programs are reshaping consumer confidence and shortening replacement cycles. Electric-vehicle (EV) resale activity is accelerating as battery-health transparency improves, while petrol models continue to dominate volumes. Regionally, the southern manufacturing hubs of Baden-Württemberg and Bayern benefit from better vehicle maintenance records, supporting premium residual values. Competitive intensity remains fragmented, leaving room for consolidation as larger digital players leverage scale and data analytics to outpace smaller dealers.

Key Report Takeaways

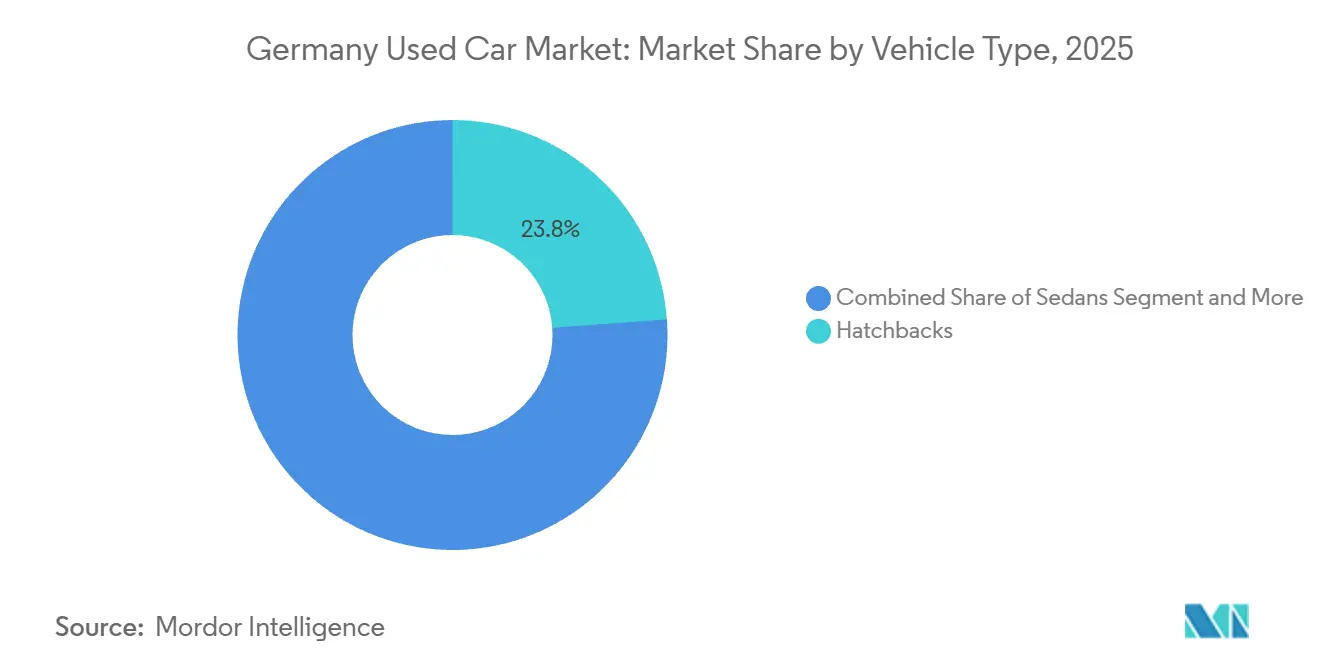

- By vehicle type, hatchbacks led the German used-car market with 23.84% share in 2025, whereas SUVs are projected to post the fastest 14.63% CAGR through 2031.

- By vendor type, organized dealers captured 62.55% of the German used-car market in 2025; the channel is expanding at a 12.29% CAGR through 2031.

- By fuel type, petrol vehicles held a 60.92% share of the German used-car market in 2025, while battery-electric vehicles are forecast to grow at a 21.93% CAGR through 2031.

- By vehicle age, the 9-12-year bracket accounted for 33.68% of the German used-car market share in 2025, but the 0-2-year segment is set to grow at a 14.67% CAGR through 2031.

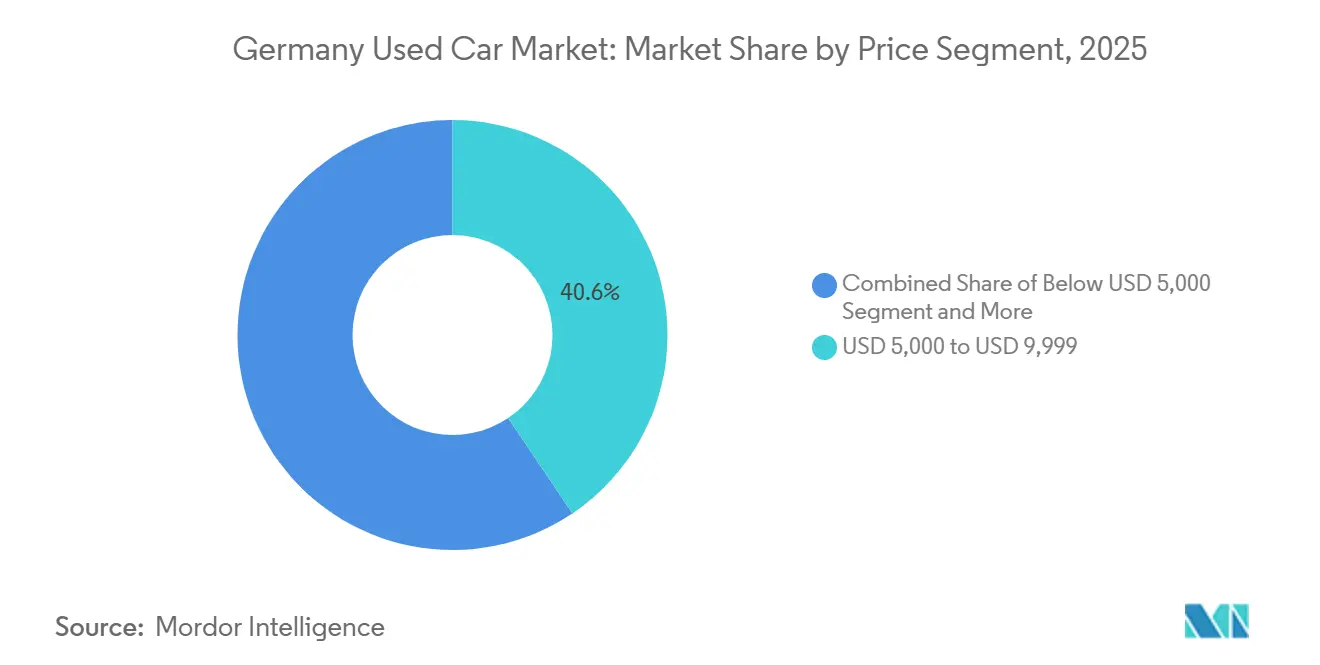

- By price segment, the USD 5,000-9,999 range accounted for 40.58% of the German used-car market in 2025, whereas units priced above USD 30,000 will expand at a 16.21% CAGR through 2031.

- By sales channel, offline transactions retained 76.95% of the German used-car market share in 2025; online channels will register a 15.03% CAGR to 2031.

- By ownership, multi-owner vehicles held 65.41% of the German used-car market share in 2025, yet first-owner resales will grow at a 13.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Used Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Average Vehicle Age Boosts Replacement Demand | +3.2% | Baden-Württemberg, Bayern, Nordrhein-Westfalen | Medium term (2-4 years) |

| Tight Supply of New Cars Elevates Used-Car Prices | +2.8% | Hamburg, Berlin, München, Stuttgart | Short term (≤ 2 years) |

| Proliferation of Online Transaction Platforms | +2.1% | All German states with urban concentration | Medium term (2-4 years) |

| EU Battery Regulation Accelerates BEV Remarketing | +1.9% | Baden-Württemberg, Bayern, Niedersachsen | Long term (≥ 4 years) |

| Subscription Models Spur Demand for Nearly-New Cars | +1.4% | Hamburg, Berlin, München, Frankfurt | Medium term (2-4 years) |

| OEM Certified-Pre-Owned Programs Gain Traction | +1.2% | Baden-Württemberg, Bayern, Nordrhein-Westfalen | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Average Vehicle Age Boosts Replacement Demand

Germany's passenger car fleet has an average age exceeding 10 years, highlighting prolonged ownership cycles and sustained vehicle durability. The rising share of vehicles older than 10 years is driving structural demand in the used-car market. Vehicle owners are increasingly upgrading to relatively newer pre-owned vehicles, which offer improved fuel efficiency, advanced safety systems such as ADAS, and modern infotainment features at lower price points than new vehicles. As maintenance costs escalate with vehicle age and environmental regulations become stricter in urban centers, consumers are shifting from older vehicles to younger used models rather than purchasing new cars. This trend is strengthening trading activity in the used-car market and contributing to higher transaction volumes across organized and digital channels.

Tight Supply of New Cars Elevates Used-Car Prices

Germany's passenger vehicle production has remained below pre-pandemic levels in recent years, resulting in extended delivery times for certain new vehicle models. This has prompted consumers, particularly in the premium and high-specification segments, to consider certified pre-owned (CPO) vehicles as readily available alternatives. This trend has driven demand in the organized used-car market. During periods of constrained new vehicle availability, buyers seeking immediate delivery often shift toward younger used vehicles with comparable specifications. Organized dealers have leveraged this substitution effect by efficiently managing inventory flows across regions to address demand in major urban centers, where purchase urgency is higher.

Proliferation of Online Transaction Platforms

During the period from 2020 to 2024, digital engagement in Germany's used car market experienced substantial growth. Survey findings indicate that approximately 80% of used car buyers in Germany utilized online sources prior to making a purchase. This highlights the critical role of digital platforms in vehicle discovery, price comparison, and benchmarking. Consequently, online classifieds and automotive marketplaces have become essential research channels, significantly influencing dealer visibility and inventory turnover. Leading platforms have enhanced their functionalities by incorporating features such as vehicle history reports, financing calculators, dealer ratings, and secure communication tools. Although fully digital end-to-end transactions remain less prevalent compared to traditional dealership purchases, digital platforms now dominate the research and consideration stages of the buying process.

EU Battery Regulation Accelerates BEV Remarketing

Regulation (EU) 2023/1542 mandates 80% battery state-of-health for vehicles up to five years old, dropping to 70% for those aged five to eight[1]"Regulation (EU) 2023/1542", Official Journal of the European Union, European Union, eur-lex.europa.eu. Greater regulatory clarity around battery health monitoring and performance disclosure supports improved residual value assessment for battery electric vehicles (BEVs). In Germany’s used car market, where BEV penetration has risen steadily in recent years, clearer standards for battery condition reporting reduce uncertainty around long-term degradation risk and ownership costs. As battery condition remains one of the primary concerns for used BEV buyers, structured disclosure frameworks and standardized diagnostics enhance consumer confidence. This is particularly relevant for vehicles transitioning from leasing fleets into the secondary market, where accurate battery performance evaluation directly influences resale pricing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Diesel Demand Falls Amid Urban Low-Emission Zones | -2.3% | Stuttgart, München, Hamburg, Berlin | Short term (≤ 2 years) |

| High Interest Rates Restrict Financing Affordability | -1.8% | All German states | Short term (≤ 2 years) |

| Digital Registration Backlogs Slow Title Transfers | -1.1% | Berlin, Hamburg, Nordrhein-Westfalen | Medium term (2-4 years) |

| Exports Siphon Affordable Stock from Domestic Market | -0.9% | Border regions, port cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Diesel Demand Falls Amid Urban Low-Emission Zones

Low-emission zone (LEZ) policies in several German cities have reduced the operational flexibility of older diesel vehicles that do not meet higher Euro emission standards. Cities such as Stuttgart and Hamburg have implemented diesel-related traffic restrictions targeting certain older Euro 4 and, in specific corridors, early Euro 5 vehicles, particularly in high-pollution areas[2]"Low emission zone Stuttgart," Green Zones, green-zones.eu.. These measures are designed to improve urban air quality and comply with EU nitrogen oxide (NOx) limits. Stuttgart, one of the earliest adopters of stricter diesel controls, has imposed driving bans on selected older diesel passenger cars within designated environmental zones. Such restrictions reduce the practical usability of non-compliant vehicles within city limits, negatively influencing their demand and resale values in affected urban markets.

High Interest Rates Restrict Financing Affordability

In 2024, rising interest rates and higher credit costs led to a noticeable decline in the number of approved auto loans in Germany, disproportionately affecting middle-income buyers. This segment is a key driver of demand for mid-priced vehicles, and tighter financing options constrained their ability to purchase new cars. As a result, many consumers turned to older used vehicles or explored flexible subscription and mobility-as-a-service models, which offered lower upfront costs and adaptable payment structures. These alternatives offered both affordability and flexibility, reinforcing their appeal among cost-conscious buyers and sustaining demand in the used-car market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: SUVs Drive Premium Segment Growth

Hatchbacks currently lead in volume with a 23.84% share, thanks to their maneuverability in dense urban areas. SUVs are projected to record a 14.63% CAGR through 2031, well ahead of any other body style. In Germany, the sedan segment is gradually losing market share as the crossover segment increasingly meets consumer preferences for comfort, practicality, a higher driving position, and perceived safety. The multi-purpose vehicle (MPV) segment continues to target a niche family-oriented demographic. In contrast, the convertible and sports car segments primarily attract enthusiasts and collectors, rather than the broader consumer base.

Regional demand patterns exhibit notable variations: affluent southern states such as Bavaria and Baden-Württemberg report the highest SUV penetration, driven by higher disposable incomes and suburban or semi-rural driving conditions. In contrast, the compact car segment dominates in northern and coastal regions, where narrow streets, dense urban layouts, and constrained parking conditions favor smaller vehicles.

By Vendor Type: Organized Channels Consolidate Market Share

Organized players commanded 62.55% of the German used car market size in 2025 and are growing at a 12.29% CAGR through 2031. German used car buyers increasingly prioritize warranty coverage, financing options, and reliable after-sales service, benefits typically provided by structured and organized dealerships. While independent or unorganized sellers continue to attract price-sensitive buyers, they are losing market share as transaction complexity grows and buyers demand greater transparency and assurance.

Urban and metropolitan areas are seeing accelerated market consolidation, driven in part by rising real estate and operational costs, which encourage smaller independent lots to partner with larger dealer networks or exit the market entirely.

By Fuel Type: Electric Vehicles Accelerate Despite Petrol Dominance

Petrol models retained 60.92% of the German used car market share in 2025. However, BEVs will expand at a striking 21.93% CAGR, aided by clear battery-health standards and the expansion of fast-charging grids. Diesel passenger vehicles in Germany are facing a structural decline, primarily driven by low-emission zone (LEZ) regulations in urban centers that restrict the operation of older Euro 4 and Euro 5 diesel models. Despite this, diesel retains relevance in rural and logistics-intensive areas, where long-distance efficiency and torque advantages remain valuable.

Hybrid vehicles occupy a transitional segment in the market, offering buyers range assurance and familiarity with combustion engines, while enabling compliance with increasingly stringent emissions standards. This makes them a practical choice for cost-conscious consumers navigating tightening urban regulations.

By Vehicle Age: Nearly-New Segments Capture Premium Pricing

Vehicles aged 9-12 years make up the largest slice of the German used-car market, where maintenance costs push owners to sell. Units older than 12 years will gradually become less relevant as safety and emissions regulations tighten. The 0 to 2-year segment is forecast to grow 14.67% annually, driven by subscription fleets and corporate lease returns.

Newer inventory moves more quickly through organized channels that can certify vehicle condition, provide transparent histories, and bundle financing options, enhancing buyer confidence and accelerating turnover. Older vehicle segments will continue to appeal to budget-conscious buyers. Still, their growth is constrained by tightening regulations, particularly low-emission zone restrictions and emissions compliance requirements in urban areas.

By Price Segment: Market Bifurcates Toward Value and Luxury

Vehicles priced USD 5,000 to 9,999 held a 40.58% of the German used car market share in 2025, satisfying mainstream affordability. Above USD 30,000, demand expands at 16.21% CAGR as wealthy buyers shift from delayed new-car orders to nearly-new luxury stock. The mid-tier (USD 10,000 to 29,999) experiences compression, squeezed by budget constraints at one end and aspirational upgrades at the other.

Regional income disparities in Germany further reinforce market segmentation within the used car ecosystem. Dealers serving premium clientele in affluent urban centers such as München and Stuttgart can capture higher margins on luxury and high-specification vehicles, including SUVs, premium sedans, and nearly-new BEVs. Conversely, dealerships in rural or lower-income regions primarily target value-oriented segments, focusing on older, smaller, or economy vehicles where affordability drives demand.

By Sales Channel: Digital Integration Accelerates Omnichannel Evolution

Offline sites still account for 76.95% of transactions, underscoring the need for tactile vehicle assessment. Online channels, scaling at 15.03% CAGR, increasingly serve discovery, financing pre-approval, and paperwork. Dealers adopting omnichannel strategies, combining virtual showrooms, online inventory browsing, and digital financing tools with traditional in-person handovers, are gaining a competitive edge through higher customer retention and satisfaction. Urban, digitally savvy consumers drive the adoption of online platforms, relying on virtual research, price transparency, and home delivery options to streamline purchases.

In contrast, buyers in rural areas continue to emphasize personal relationships with local dealerships, valuing trust, long-standing service history, and hands-on vehicle inspection. This divergence underscores the need for dealers to tailor their sales and engagement models regionally, leveraging digital tools where adoption is high while maintaining a strong local presence in less connected markets.

By Ownership: First-Owner Resales Accelerate Through Subscription Models

Multi-owner vehicles accounted for 65.41% of the German used car market in 2025, reflecting the continued prevalence of vehicles with multiple previous owners in the secondary market. First-owner vehicles are expected to grow at a compound annual growth rate of 13.22%, supported by subscription operators and corporate lease returns that inject well-documented stock into the pipeline. These vehicles allow dealers to offer nearly new cars with lower reconditioning costs, enhancing buyer confidence and supporting faster turnover.

Affluent buyers show a clear preference for single-owner histories, which drives higher resale prices and accelerates movement within organized dealership channels. As warranty-backed first-owner inventory expands, multi-owner vehicles are expected to gradually lose momentum in terms of market share and transaction velocity.

Geography Analysis

Regional differences in vehicle condition and used car demand are evident in Germany’s used car market. According to the TÜV Report, Saxony shows the lowest overall fault rate at about 16.8 percent, followed by Bavaria at around 17.4 percent and Baden‑Württemberg at about 19.6 percent, indicating comparatively better-maintained vehicles in these southern states versus regions such as Hamburg, where defect rates are higher[3]"Regular servicing makes all the difference", TÜV SÜD, tuvsud.com. These lower defect rates support stronger residual values and allow dealers to list vehicles at higher prices in southern markets. Proximity to major automotive manufacturing and leasing hubs in Bavaria and Baden‑Württemberg also contributes to a steady flow of younger lease returns into their secondary markets, aligning with consumer preference for late‑model used vehicles.

Nordrhein-Westfalen, the most populous state, offers scale yet suffers from higher vehicle wear due to urban congestion. Niedersachsen leverages EUR 1.8 million in state support for electric-mobility supply-chain adaptation to accelerate BEV uptake. Eastern regions such as Sachsen, despite improving defect rates, face income constraints that limit penetration of premium segments.

Major cities influence purchasing channels: Berlin and Hamburg lead digital adoption but wrestle with registration backlogs that extend transaction cycles. Stuttgart’s persistent diesel restrictions depress local diesel residuals, whereas surrounding rural zones absorb the displaced stock. Dealers adept at navigating these regulatory nuances optimize sourcing and margin profiles.

Competitive Landscape

The largest platform integrates vehicle acquisition, refurbishment, and direct-to-consumer retailing, achieving robust profitability in 2024. A third digital portal broadens its services to include financing and inspection to defend its position.

Wholesale auction networks scale across multiple European countries, adding liquidity for professional buyers. Technology, particularly data analytics and battery-state reporting, defines competitive edges. Smaller regional dealers must pivot toward specialized services or geographic niches to survive the march of consolidated, tech-rich rivals.

Germany Used Car Industry Leaders

-

AUTO1 Group SE (AutoHero and wirkaufendeinauto.de)

-

mobile.de GmbH

-

AutoScout24 GmbH

-

CarNext.com

-

BCA Autoauktionen GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Barcelona-based Dealcar raised EUR 3 million to digitize used-car dealerships and commence entry into Germany.

- November 2024: Mocean Subscription, part of Hyundai Connected Mobility, launched nationwide access to new and pre-owned Hyundai vehicles for German subscribers.

Germany Used Car Market Report Scope

A used car, often referred to as a pre-owned or secondhand vehicle, is a vehicle that has been previously owned and operated by one or more retail owners. These vehicles are typically sold through various channels, including dealerships, private sellers, and online platforms. The used-car market plays a significant role in the automotive industry, offering cost-effective options for buyers and extending the lifespan of cars.

The German used-car market is segmented by vendor type, fuel type, body type, and sales channel.

By Vendor Type, the market is segmented into Organized and Unorganized. By Fuel Type, the market is segmented into Petrol, Diesel, Electric, and Others. By Body Type, the market is segmented into Hatchback, Sedan, SUVs, and MPVs. By Sales Channel, the market is segmented into Online and Offline. The report covers the market size and forecast in value (USD) for all the above segments.

By Vehicle Type

| Hatchbacks |

| Sedans |

| Sport-Utility Vehicles (SUVs) |

| Multi-Purpose Vehicles (MPVs) |

| Others (convertibles, coupes, crossovers, sports cars) |

By Vendor Type

| Organized |

| Unorganized |

By Fuel Type

| Petrol |

| Diesel |

| Hybrid Vehicles (HEV and PHEV) |

| Battery-Electric Vehicles (BEV) |

| Others (LPG, CNG, etc.) |

By Vehicle Age

| 0 to 2 Years |

| 3 to 5 Years |

| 6 to 8 Years |

| 9 to 12 Years |

| Above 12 Years |

By Price Segment

| Below USD 5,000 |

| USD 5,000 to USD 9,999 |

| USD 10,000 to USD 14,999 |

| USD 15,000 to USD 19,999 |

| USD 20,000 to USD 29,999 |

| USD 30,000 and Above |

By Sales Channel

| Online |

| Offline |

By Ownership

| First-owner Resale |

| Multi-owner |

| By Vehicle Type | Hatchbacks |

| Sedans | |

| Sport-Utility Vehicles (SUVs) | |

| Multi-Purpose Vehicles (MPVs) | |

| Others (convertibles, coupes, crossovers, sports cars) | |

| By Vendor Type | Organized |

| Unorganized | |

| By Fuel Type | Petrol |

| Diesel | |

| Hybrid Vehicles (HEV and PHEV) | |

| Battery-Electric Vehicles (BEV) | |

| Others (LPG, CNG, etc.) | |

| By Vehicle Age | 0 to 2 Years |

| 3 to 5 Years | |

| 6 to 8 Years | |

| 9 to 12 Years | |

| Above 12 Years | |

| By Price Segment | Below USD 5,000 |

| USD 5,000 to USD 9,999 | |

| USD 10,000 to USD 14,999 | |

| USD 15,000 to USD 19,999 | |

| USD 20,000 to USD 29,999 | |

| USD 30,000 and Above | |

| By Sales Channel | Online |

| Offline | |

| By Ownership | First-owner Resale |

| Multi-owner |

Key Questions Answered in the Report

What is the current value of the German used car market in 2026?

The market is worth USD 96.32 billion in 2026.

How fast will the German used car market grow by 2031?

It is projected to reach USD 163.75 billion by 2031, reflecting an 11.19% CAGR during 2026-2031.

Which vehicle type is expanding quickest in German used car sales?

SUVs are set to grow at 14.63% CAGR through 2031.

Why are battery-electric vehicles gaining traction in the German used car market?

Clear battery-health regulations and better charging infrastructure are improving buyer confidence, driving a 21.93% CAGR outlook.

How dominant are online channels in used-car transactions?

Offline dealers still close 76.95% of deals in 2025, but online channels are progressing at 15.03% CAGR as omnichannel models mature through 2031.

What factors suppress diesel demand in Germany?

Expanding low-emission zones in major cities reduce diesel car usability, leading to lower valuations and higher export volumes.

Page last updated on: