ASEAN Roadside Safety Barriers Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

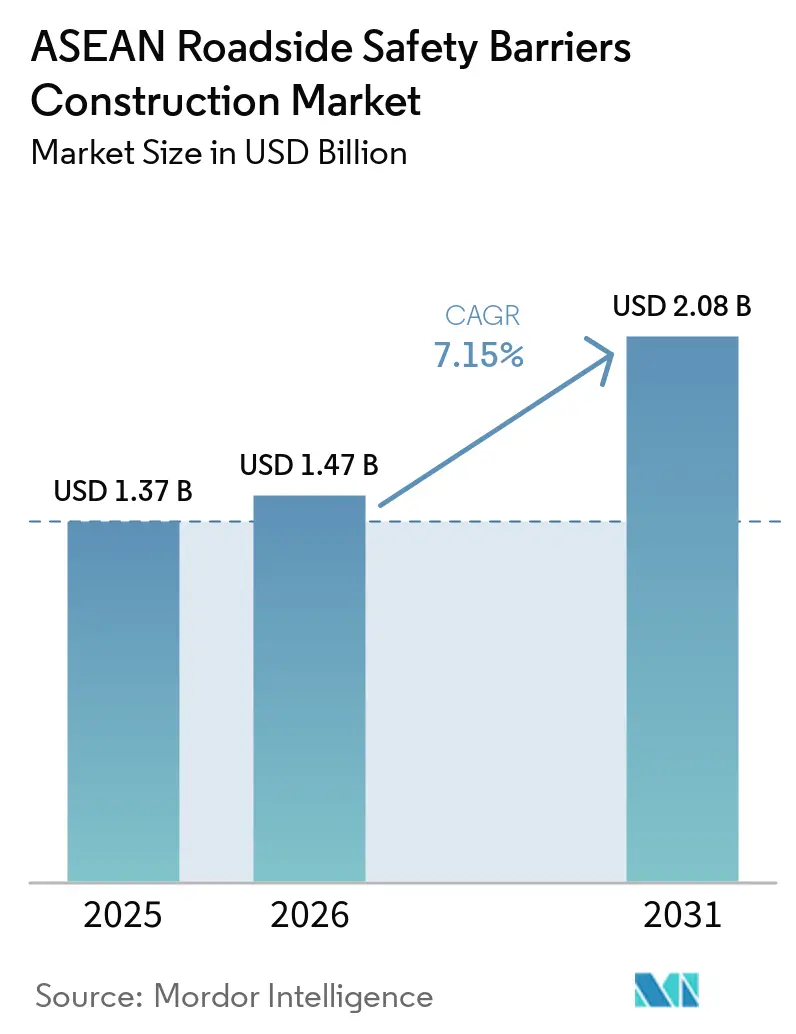

| Base Year Market Size (2025) | USD 1.37 Billion |

| Market Size (2026) | USD 1.47 Billion |

| Market Size (2031) | USD 2.08 Billion |

| Growth Rate (2026 - 2031) | 7.15% CAGR |

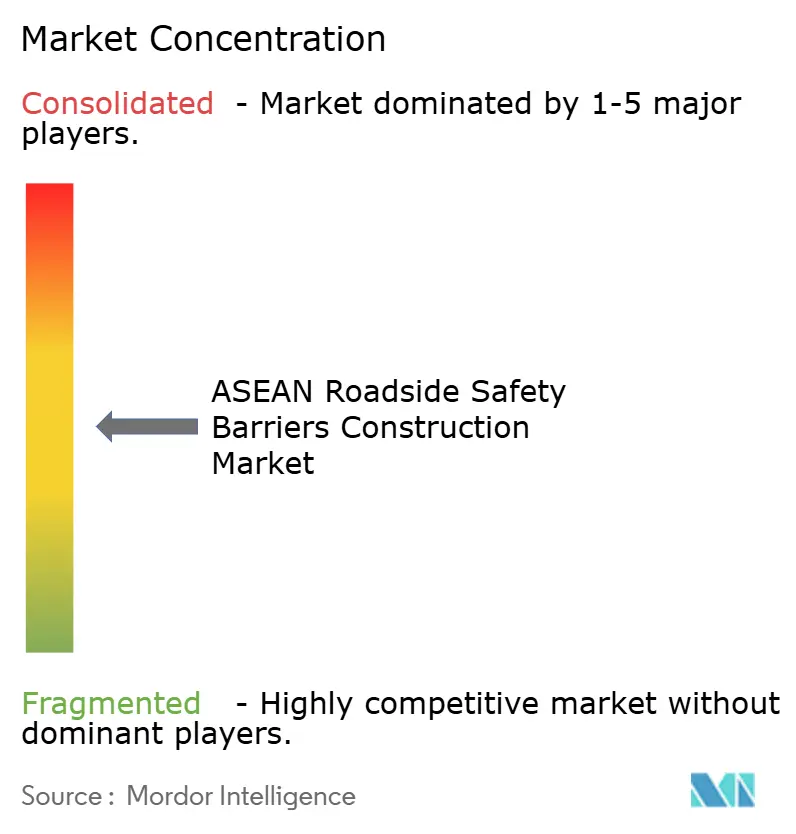

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN Roadside Safety Barriers Construction Market Analysis by Mordor Intelligence

The ASEAN Roadside Safety Barriers Construction Market size is projected to be USD 1.37 billion in 2025 and is estimated to be USD 1.47 billion in 2026, and expected to reach USD 2.08 billion by 2031, growing at a CAGR of 7.15% from 2026 to 2031. Highway construction programs, stricter crash-test regulations, and increased public attention on motorcycle fatalities are driving growth in procurement budgets, despite the impact of raw-steel price volatility on contractor margins. High-grade steel guardrails continue to dominate the market; however, plastic and composite alternatives are gaining traction, particularly in humid and coastal regions. While new toll road construction accounts for the majority of spending, retrofit projects on first-generation expressways in Thailand, Malaysia, and Vietnam are accelerating to comply with Manual for Assessing Safety Hardware (MASH) Test Level-3 standards. Competitive intensity remains moderate due to decentralized tenders, diverse certification requirements, and varying material preferences, which prevent regional suppliers from capturing significant market shares. This environment creates opportunities for cross-border joint ventures and niche innovators to expand their presence.

Key Report Takeaways

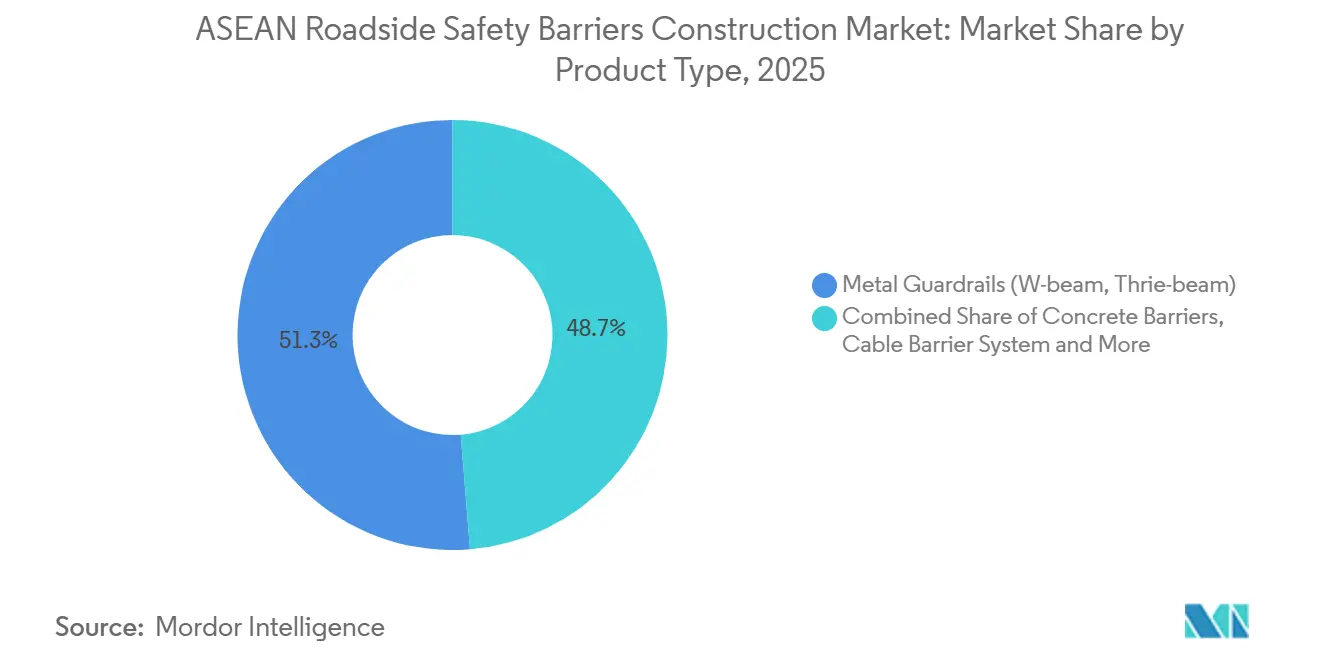

- By product type, metal guardrails led with 51.3% of the ASEAN roadside safety barriers construction market share in 2025, while cable systems are projected to advance at 7.98% CAGR between 2026 and 2031.

- By material, steel commanded 67.8% of the ASEAN roadside safety barriers construction market size in 2025; plastics and composites represent the fastest-growing material class at 8.07% CAGR between 2026 and 2031.

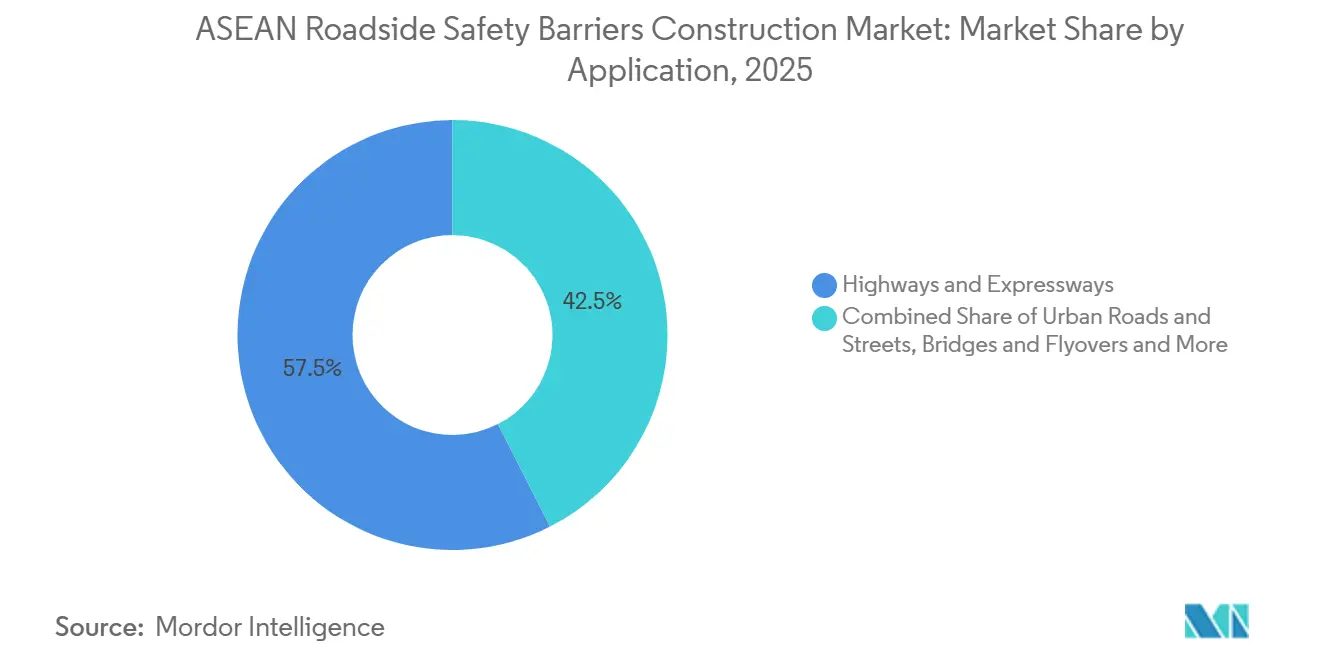

- By application, highways and expressways accounted for 57.5% of the ASEAN roadside safety barriers construction market size in 2025, whereas bridges and flyovers are set to expand at 8.11% CAGR between 2026 and 2031.

- By installation type, new projects represented 71.2% of the ASEAN roadside safety barriers construction market in 2025; renovation and retrofit work is the fastest-growing sub-segment at 7.59% CAGR between 2026 and 2031.

- By country, Indonesia held 34.9% of ASEAN roadside safety barriers construction market share in 2025, and the Philippines is forecast to record the highest national growth at 8.34% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

ASEAN Roadside Safety Barriers Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing ASEAN highway connectivity and cross-border corridor upgrades are accelerating roadside safety barrier installation | +2.1% | Indonesia, Thailand, Vietnam, Malaysia, Cambodia | Medium term (2–4 years) |

| Regional road safety action plans are driving the adoption of median and edge protection systems | +1.8% | Thailand, Vietnam, Philippines | Short term (≤ 2 years) |

| High accident exposure on intercity and mountainous roads is increasing the demand for crash barriers | +1.5% | Vietnam, Philippines, Indonesia, Thailand | Short term (≤ 2 years) |

| Expansion of freight corridors and logistics routes is boosting the need for barriers on strategic highways | +1.2% | Indonesia, Vietnam, Thailand | Medium term (2–4 years) |

| Rising policy support for motorcycle-specific protection systems is encouraging targeted barrier deployment | +0.9% | Vietnam, Thailand, Indonesia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing ASEAN highway connectivity and cross-border corridor upgrades are accelerating roadside safety barrier installation.

Multi-country corridors, such as the Greater Mekong Sub-region Highway and the India-Myanmar-Thailand Trilateral Highway, require harmonized safety hardware that surpasses outdated national minimum standards. Thailand’s proposed Southern Economic Corridor, with an estimated value of THB 990 billion (USD 27.5 billion), is expected to add hundreds of kilometers of guardrails along landslide-prone coastal areas. Similarly, Vietnam’s USD 3.2 billion Ha Tien-Rach Gia-Bac Lieu Expressway and Indonesia’s Bogor-Serpong toll road will drive significant demand for W-beam and cable-barrier systems. As major corridors implement modern safety barriers, provincial agencies are under public pressure to retrofit adjacent feeder roads, thereby expanding the ASEAN roadside safety barriers construction market[1]Department of Highways Thailand, “Southern Economic Corridor Project Brief 2026,” doh.go.th. Suppliers capable of meeting both AASHTO M180 and local certification standards are well-positioned to capitalize on this growing demand.

Regional road safety action plans are driving the adoption of median and edge protection systems.

ASEAN governments have allocated barrier spending in their 2026-2030 budgets as part of the United Nations Decade of Action for Road Safety. Projects such as Cambodia’s National Road 4 upgrade and the Philippines’ Maharlika Highway rehabilitation include guardrails as key deliverables linked to multilateral loan disbursements. Thailand’s Toyota TRUST project uses data analytics to identify high-risk areas and implement rapid barrier installations, demonstrating how public-private collaboration enhances crash hotspot mitigation. These initiatives increasingly emphasize motorcycle-friendly barrier designs, creating a niche market for smooth-surfaced, low-beam products. This collective effort positions barrier procurement as a fundamental safety investment rather than an optional expense.[2]United Nations, “Decade of Action for Road Safety 2021-2030 Plan,” un.org .

High accident exposure on intercity and mountainous roads is increasing the demand for crash barriers.

Fatality rates on steep rural highways in Indonesia, Vietnam, and the Philippines are two to three times higher than urban averages. Infrastructure projects, such as Vietnam’s Thu Thiem 4 bridge and Indonesia’s Probolinggo-Banyuwangi segment on the Trans-Java highway, require concrete parapets and TL-4 steel rails capable of containing 36-tonne trucks. Additionally, retrofit programs are significant, as first-generation expressways built before 2005 used lighter-gauge steel that no longer complies with MASH standards, necessitating systematic replacement efforts. This dual demand—new construction and retrofitting—drives growth in the ASEAN roadside safety barriers construction market, alongside routine maintenance budgets. Manufacturers providing quick-install modular kits are favored, as prolonged lane closures are politically undesirable.[3]Japan International Cooperation Agency, “Indonesia Road Safety Enhancement Program 2025,” jica.go.jp.

Expansion of freight corridors and logistics routes is boosting the need for barriers on strategic highways.

Freight-intensive corridors, such as Malaysia's upcoming North-South Expressway 2 and Singapore's Changi Viaduct upgrade, require high-containment Thrie-beam barriers, concrete F-shape medians, and tensioned cable systems designed to accommodate articulated lorries. In 2024, the ASEAN Single Window processed 1.4 billion electronic certificates, streamlining cross-border truck movement but increasing crash risks near border checkpoints. Toll operators are increasingly adopting movable concrete barriers for work-zone safety and flood control, as demonstrated on Indonesia's Tangerang-Merak route in 2026. This trend connects logistics modernization with rising demand for safety barriers, driving growth in the ASEAN roadside safety barriers construction market beyond passenger vehicle considerations.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budget constraints in lower-income ASEAN markets are delaying large-scale roadside safety upgrades | -1.1% | Cambodia, Myanmar, Lao PDR | Short term (≤ 2 years) |

| Uneven road safety enforcement across member countries is limiting consistent barrier adoption | -0.8% | Cambodia, Lao PDR, Myanmar | Medium term (2–4 years) |

| Variations in standards and procurement practices are slowing the regional deployment of barrier systems | -0.6% | All member states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Budget constraints in lower-income ASEAN markets are delaying large-scale roadside safety upgrades.

Fiscal space has tightened following an 82% decline in international project finance to ASEAN, dropping to USD 17 billion in 2024. In the absence of concessional loans, provinces are compelled to make difficult decisions between maintaining fiscal guardrails and addressing urgent needs such as flood-control measures or school construction projects. The rise in steel prices to USD 515 per ton in 2026 has further reduced fixed-price tender margins, leading some fabricators to withdraw from bids and delaying projects to the next fiscal year. These deferred procurements result in kilometer-long backlogs, increasing crash exposure. While donor-co-financed road safety components address part of the issue, they only mitigate a small portion of the gap. As a result, near-term growth in the ASEAN roadside safety barriers construction market remains below potential, particularly in Cambodia and Myanmar.

Uneven road safety enforcement across member countries is limiting consistent barrier adoption.

Central inspectorates with the legal authority to enforce barrier upgrades remain underdeveloped in Cambodia, Lao PDR, and Myanmar. Provincial works offices often prioritize road resurfacing over implementing passive safety infrastructure, leaving newly paved roads unprotected on embankments and curves. In Indonesia, only 32% of surveyed rural road segments had continuous guardrails, despite national guidelines recommending full coverage for roads with speeds exceeding 80 km/h. Inconsistent enforcement hinders suppliers' ability to accurately forecast demand, leading to higher inventory costs and slower product innovation. Until unified oversight bodies are established, this lack of consistency will limit the growth potential of the ASEAN roadside safety barriers construction market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Metal Guardrails Anchor Market, Cable Systems Surge

Metal guardrails accounted for 51.3% of the ASEAN roadside safety barriers construction market share in 2025. W-beam rails are predominantly used on rural expressways, meeting Test Level-3 containment standards, while Thrie-beam profiles are preferred for freight corridors that accommodate heavier trucks. Cable barriers, although representing a smaller market share, are projected to grow at a CAGR of 7.98%, the fastest within the category. Agencies report up to a 90% reduction in fatal crashes on divided highways where cable barriers are implemented. In Malaysia, products like ArmorWire and Muar Cathay’s Ezy-Guard series, both certified to MASH TL-3 standards, illustrate the increasing adoption of tensioned systems for narrow medians. Concrete Jersey and F-shape barriers maintain niche applications on bridges, toll plazas, and urban work zones, where permanent high-containment solutions are critical. Companies like WIKA Beton leverage their fourteen Indonesian plants to secure rapid-turnaround supply contracts in these areas.

Cable barriers also offer advantages in terms of easier and faster repairs after high-speed collisions, reducing lane-closure times by half compared to concrete alternatives. Crash cushions and impact attenuators occupy a premium segment, primarily used for protecting bridge piers and gore points. For instance, Safe Direction’s TAU-M units in Singapore demonstrate a willingness to invest in controlled-deformation technology, particularly in areas with limited land availability. The "others" segment includes hybrid steel-concrete barriers and motorcycle-specific rails, where innovation is advancing faster than volume growth. Collectively, these trends indicate that the ASEAN roadside safety barriers construction market is diversifying beyond the traditional dominance of W-beam barriers over the forecast period.

By Material: Steel Dominates, Composites Gain Ground

In 2025, steel accounted for 67.8% of the total material demand in the ASEAN roadside safety barriers construction market. Locally produced coils from mills in Indonesia and Vietnam help maintain competitive pricing. Galvaco’s integrated roll-form-plus-galvanizing line consistently exceeds AASHTO M180 coating standards, providing a 20-year corrosion resistance even in humid climates. High-strength grades like HR700F enable the use of thinner-gauge guardrails without compromising crash energy absorption, reducing freight costs on routes such as those in Sulawesi. Concrete ranks as the second most used material, primarily for parapets and medians on elevated expressways. Precast concrete units from Samwoh’s Singapore plant have been specified for projects like the USD 387 million Changi viaduct, demonstrating their performance under seismic and typhoon conditions.

Composites, while currently holding a single-digit market share, are experiencing the fastest growth with a CAGR of 8.07%. Glass-fiber reinforced polyethylene rails from Boplan and GFRP-reinforced parapets, which are undergoing laboratory trials in Malaysia, offer advantages such as lighter weight and zero corrosion. These materials are particularly favored by toll operators for flood-prone areas where maintenance access is challenging. Recycled-plastic blends are also gaining traction, aligning with emerging circular-economy regulations in Thailand and Vietnam. Additionally, aluminum rails, though more expensive, are in demand for weight-restricted viaducts in the Mekong Delta. The diversification of materials positions suppliers with multi-substrate portfolios to outperform competitors relying on single-metal solutions as the ASEAN roadside safety barriers construction market continues to evolve.

By Application: Highways Lead, Bridges Accelerate

Highways and expressways are projected to account for 57.5% of the ASEAN roadside safety barriers construction market size in 2025. Indonesia's auction of seven new toll roads, valued at USD 8.3 billion, ensures multi-year demand for W-beam and concrete medians. In Vietnam, upgrades to Ho Chi Minh City's gateway include barrier-free tolling systems, necessitating uninterrupted safety rails. Urban arterial projects in Kuala Lumpur and Manila are increasingly incorporating guardrails alongside pedestrian fencing and noise screens, broadening the range of specifications. Contractors offering blended steel-and-composite packages are now scoring higher in technical evaluations, reflecting the growing emphasis on aesthetics and sustainability.

Although starting from a smaller base, bridges and flyovers are expected to grow at a CAGR of 8.11% through 2031. Large-scale projects, such as the Philippines' USD 3.9 billion Bataan-Cavite span and Vietnam's USD 950 million Thuận An sea bridge, require TL-4 concrete parapets and cable-reinforced edges to prevent truck water entry. Singapore's North-South Corridor viaducts integrate crash-tested parapets with LED lighting, highlighting advancements in multifunctional barrier design. These projects often specify ultra-high-performance concrete modules for quick replacement after impacts, minimizing traffic disruptions and supporting higher service-level targets for toll operators. This steady pipeline of projects is expected to increase the market share of bridges within the ASEAN roadside safety barriers construction market.

By Installation Type: New Projects Prevail, Retrofits Rise

New installations are projected to account for 71.2% of the expenditure in 2025 within the ASEAN roadside safety barriers construction market. Key projects, such as Indonesia’s Bogor-Serpong and Bali’s Gilimanuk-Mengwi toll roads, incorporate barriers into design-build contracts. This approach enables contractors to secure bulk steel pricing and coordinate guardrail installation alongside pavement works. Similar turnkey models are anticipated for Thailand’s THB 990 billion Southern Economic Corridor, which is expected to open for tender in 2027. Meanwhile, retrofit requirements are increasing as expressways built in the 1990s fail to meet MASH TL-3 standards, particularly in areas where corrosion has compromised post embedment.

The retrofit and repair segment is forecasted to grow at a CAGR of 7.59%. For instance, Malaysia’s East-West Highway has allocated RM 2.7 million (USD 0.6 million) for spot repairs in 2026, reflecting the widespread need for short-segment repairs across ASEAN. Quick-install UHPC precast rails are gaining popularity, as lane closures exceeding six hours often result in contractual penalties on heavily trafficked toll roads. Additionally, multi-year rehabilitation frameworks, such as those for the Philippines’ Maharlika Highway, provide suppliers with consistent demand beyond large-scale projects, contributing to the overall growth of the ASEAN roadside safety barriers construction market.

Geography Analysis

Indonesia accounted for 34.9% of the ASEAN roadside safety barriers construction market share in 2025, driven by ongoing toll-road privatization and the 1,150 km Trans-Java backbone, which mandates continuous median and edge protection. The USD 1.6 billion Probolinggo-Banyuwangi segment, completed in 2025, utilized over 10,000 tons of galvanized steel rails. Additionally, seven concessions auctioned in 2025, valued at USD 8.3 billion, support a rolling five-year order book for domestic manufacturers such as PT Inter Nusa Kreasindo. Concrete specialist WIKA Beton, with its fourteen plants, ensures a timely parapet supply. Further demand was bolstered by Ministry guidelines issued in February 2026, recommending movable concrete barriers for flood mitigation on low-lying routes like Tangerang-Merak.

Vietnam, Thailand, and Malaysia collectively generate over 40% of the market's revenue. Vietnam’s bridge construction projects, including the USD 950 million Thu Thiem 4 and USD 920 million Phu My 2 river crossings, require TL-4 parapets and GFRP-enhanced edges to address seismic and typhoon design requirements. Thailand’s Southern Economic Corridor, with a budget of USD 27.5 billion, is expected to tender multi-year guardrail packages favoring suppliers certified in both Bangkok and Kuala Lumpur. Malaysia’s USD 380 million North-South Expressway 2, designed to accommodate elevated truck volumes, incorporates high-tension cable barriers in its final design. Meanwhile, Singapore, though limited in road kilometers, invests in premium aesthetic concrete systems with noise-mitigation features, as demonstrated in the USD 707 million North-South Corridor viaduct.

The Philippines is projected to achieve the fastest growth in the market, with a CAGR of 8.34% through 2031. The Build Better More program allocates USD 7.8 billion for expressways and bridges, including the 32 km Bataan-Cavite span and the 450 km Central Mindanao Highway, which traverses landslide-prone areas. Multilateral lenders now require International Road Assessment Program upgrades as a condition for funding, ensuring sustained investment in safety barriers.

Cambodia, Lao PDR, and Myanmar represent smaller but growing markets, supported by India-Myanmar-Thailand corridor extensions and donor-funded projects such as Cambodia’s USD 110 million National Road 4 upgrade. New partnerships, such as the Projek Garuda-Shindo joint venture established in February 2026, aim to integrate roller-barrier technology into these emerging markets. This development signals the formation of a pan-ASEAN supply network, which is expected to gradually enhance the region’s overall safety standards.

Competitive Landscape

Competition in the ASEAN roadside safety barriers construction market is moderate due to fragmented purchasing patterns among national highway agencies, toll operators, and provincial public works departments, each requiring customized specifications. Muar Cathay Industries has established a strong position by securing approvals from Jabatan Kerja Raya (JKR) and the Malaysian Highway Authority (LLM), while maintaining inventory along the PLUS corridor, enabling a 48-hour response time for emergency repairs. Galvaco Industries differentiates itself by offering full-line galvanizing and on-site beam punching, reducing lead times by up to 20%. In Thailand, Thai Solid and Siam Traffic dominate domestic tenders by bundling guardrails with signage and delineator packages, simplifying procurement for provincial clients through single-invoice solutions.

International companies are intensifying competition by leveraging their certification capabilities. Valmont Industries, through Ingal Malaysia, utilizes U.S. crash-test credentials to secure quick approvals in markets like Singapore and Thailand. Samwoh Corporation capitalizes on its USD 387 million Changi viaduct contracts to promote concrete-steel hybrid parapets. PT Wijaya Karya Beton has secured USD 280 million in orders for barriers, parapets, and retaining walls in 2025 by integrating road products with metro rail sleepers under a single precast supply agreement, increasing its share with key contractors. Cross-border collaborations, such as the Projek Garuda-Shindo partnership established in February 2026, aim to achieve economies of scale in roller-barrier manufacturing and distribution, signaling potential regional consolidation.

Innovation is a key differentiator for emerging competitors. Muar Cathay’s MZ-Guard Z-Post reduces installation time by 50% through supercomputer-optimized crash geometry and the elimination of C-packers, a feature highlighted at Malaysia’s Hari Profesion Teknikal Negara expo. Composite material specialists are conducting MASH TL-3 trials for glass-fiber reinforced polyethylene rails, which are 40% lighter than steel, offering reduced freight costs for archipelago nations. Webforge Group’s extensive regional presence and triple ISO certification provide a competitive advantage in donor-funded tenders with strict timeline requirements. While selective mergers and acquisitions may occur, entrenched provincial preferences and regulatory approval challenges suggest that the ASEAN roadside safety barriers construction market will remain moderately fragmented through 2031.

ASEAN Roadside Safety Barriers Construction Industry Leaders

Galvaco Industries Sdn Bhd

Thai Solid Co., Ltd.

Colform Group Berhad (RoadMaster)

PT Inter Nusa Kreasindo

Muar Cathay Industries Sdn Bhd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: PT Wijaya Karya Beton (WIKA Beton) introduced the Concrete Level Crossing (CLC) system, a modular knock-down precast solution designed for at-grade railway-road crossings. The first installation was completed at KM 166+500 on the Gedebage-Haurpugur double-track segment in Bandung, West Java. This product aims to mitigate issues such as asphalt deformation and structural damage caused by train vibrations, heavy vehicle loads, and extreme weather conditions. It is intended to enhance national construction industry self-reliance and improve transportation safety.

- February 2026: Projek Garuda and Shindo Industry signed a memorandum of understanding to develop roller barriers and guardrails targeting Malaysia, Thailand, Indonesia, Singapore, Vietnam, and Cambodia. This joint venture pools technical expertise and distribution networks to create a pan-ASEAN supply platform capable of navigating multiple certification regimes and offering localized inventory across six markets.

- February 2026: Indonesia's Ministry of Public Works promoted movable concrete barriers (MCB) for flood-prone toll roads, citing their dual function as traffic separators and temporary flood-containment structures; MCBs were deployed on the Tangerang-Merak toll to retain floodwater and prevent re-flooding of the carriageway, with technical guidance issued for use on national roads and tolls requiring compliance with Indonesian National Standards (SNI)

ASEAN Roadside Safety Barriers Construction Market Report Scope

| Metal Guardrails (W-beam, Thrie-beam) |

| Concrete Barriers (Jersey, F-shape) |

| Cable Barrier Systems |

| Crash Cushions & Impact Attenuators |

| Others (Motorcyclist protection, hybrid, emerging) |

| Steel |

| Concrete |

| Plastic & Composite |

| Others (Aluminum, rubber, recycled blends) |

| Highways & Expressways |

| Urban Roads & Streets |

| Bridges & Flyovers |

| Others (Rural, industrial/private, parking, tunnels, temp zones) |

| New Installation |

| Renovation / Retrofit / Repair |

| Indonesia |

| Vietnam |

| Thailand |

| Philippines |

| Malaysia |

| Singapore |

| Rest of ASEAN |

| By Product Type | Metal Guardrails (W-beam, Thrie-beam) |

| Concrete Barriers (Jersey, F-shape) | |

| Cable Barrier Systems | |

| Crash Cushions & Impact Attenuators | |

| Others (Motorcyclist protection, hybrid, emerging) | |

| By Material | Steel |

| Concrete | |

| Plastic & Composite | |

| Others (Aluminum, rubber, recycled blends) | |

| By Application | Highways & Expressways |

| Urban Roads & Streets | |

| Bridges & Flyovers | |

| Others (Rural, industrial/private, parking, tunnels, temp zones) | |

| By Installation Type | New Installation |

| Renovation / Retrofit / Repair | |

| By Country | Indonesia |

| Vietnam | |

| Thailand | |

| Philippines | |

| Malaysia | |

| Singapore | |

| Rest of ASEAN |

Key Questions Answered in the Report

How large is the ASEAN roadside safety barrier construction market today?

The market stood at USD 1.47 billion in 2026 and is projected to reach USD 2.08 billion by 2031.

Which product type leads current demand?

Metal guardrails—primarily W-beam and Thrie-beam systems—held a 51.3% share in 2025, driven by cost-effective compliance with AASHTO M180 standards.

What is the fastest-growing product segment through 2031?

Cable barrier systems are forecast to expand at a CAGR of 7.98%, as agencies prioritize higher containment performance with easier post-crash repairs.

Which country is the strongest growth engine?

The Philippines is expected to grow at a CAGR of 8.34% through 2031, supported by its Build Better More expressway and bridge development pipeline.

How are rising steel prices affecting contractors?

Steel coil prices, at approximately USD 515 per ton in 2026, have tightened margins on fixed-price government tenders, increasing demand for modular precast and composite alternatives that reduce steel usage.

Are motorcycle-specific safety barriers becoming mandatory?

Several ASEAN regulators are incorporating smooth-post, low-rail designs into 2026–2030 standards, signaling a steady scale-up of motorcycle-friendly barrier systems across both new and retrofit projects.

Page last updated on: