Germany OOH And DOOH Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

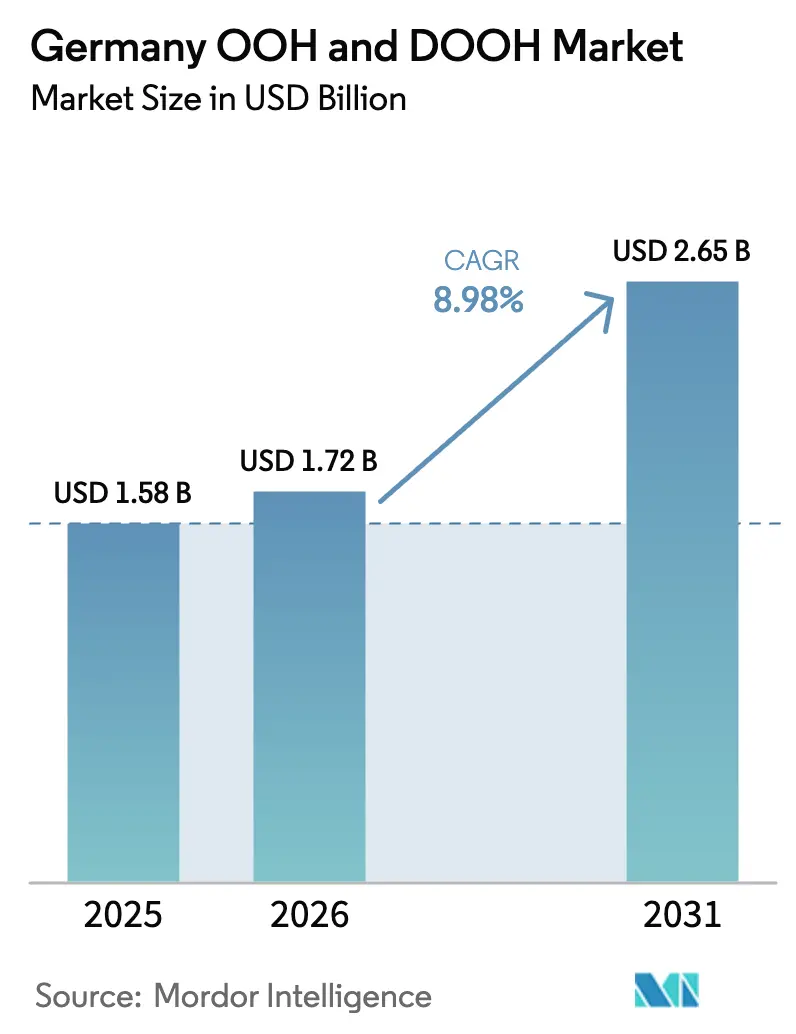

| Base Year Market Size (2025) | USD 1.58 Billion |

| Market Size (2026) | USD 1.72 Billion |

| Market Size (2031) | USD 2.65 Billion |

| Growth Rate (2026 - 2031) | 8.98% CAGR |

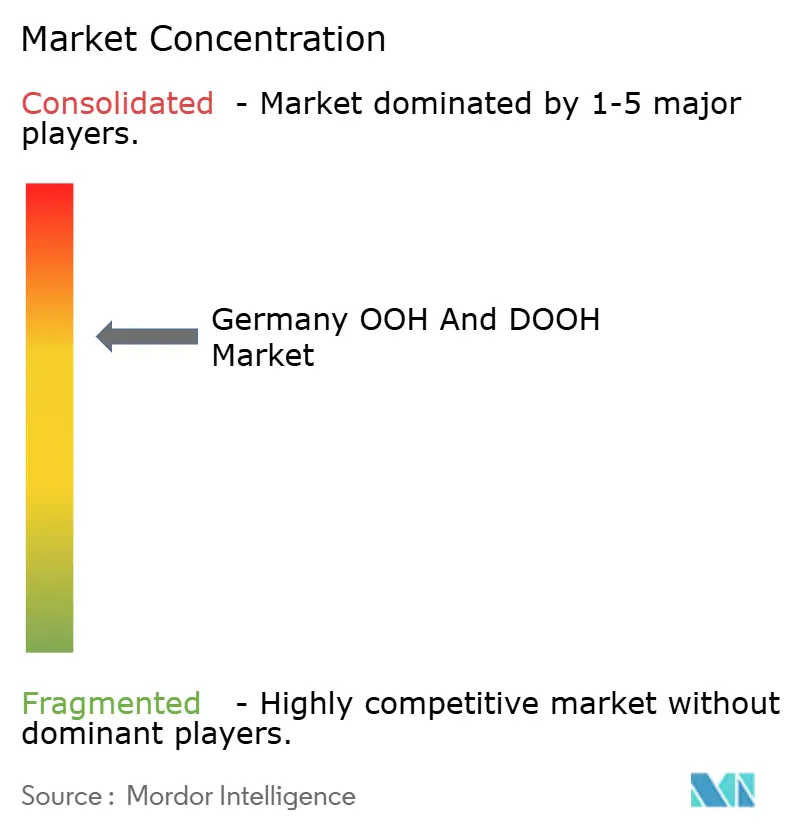

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany OOH And DOOH Market Analysis by Mordor Intelligence

The German OOH And DOOH advertising market size is expected to grow from USD 1.58 billion in 2025 to USD 1.72 billion in 2026 and is forecast to reach USD 2.65 billion by 2031 at 8.98% CAGR over 2026-2031. Growth rests on four mutually reinforcing levers: smart-city concessions that embed digital street furniture inside public-service programs, rail and airport digitisation that unlocks premium commuter impressions, programmatic retail-media networks that mimic online buying logic, and mobile geo-targeting that closes the attribution gap. Together these forces attract brand budgets shifting from cookie-constrained digital channels and reinforce inventory monetisation without diluting civic value. While digitisation widens inventory, municipal caps on luminance and rising power prices moderate rollout speed, prompting operators to prioritise energy-efficient LCD kiosks and renewable-power sourcing. Competitive intensity remains high as telecom and private-equity entrants chase predictable cash flows, yet heritage operators keep their edge through long-dated concessions, large estates and proprietary programmatic pipes that defend margins across the German OOH & DOOH advertising market.

Key Report Takeaways

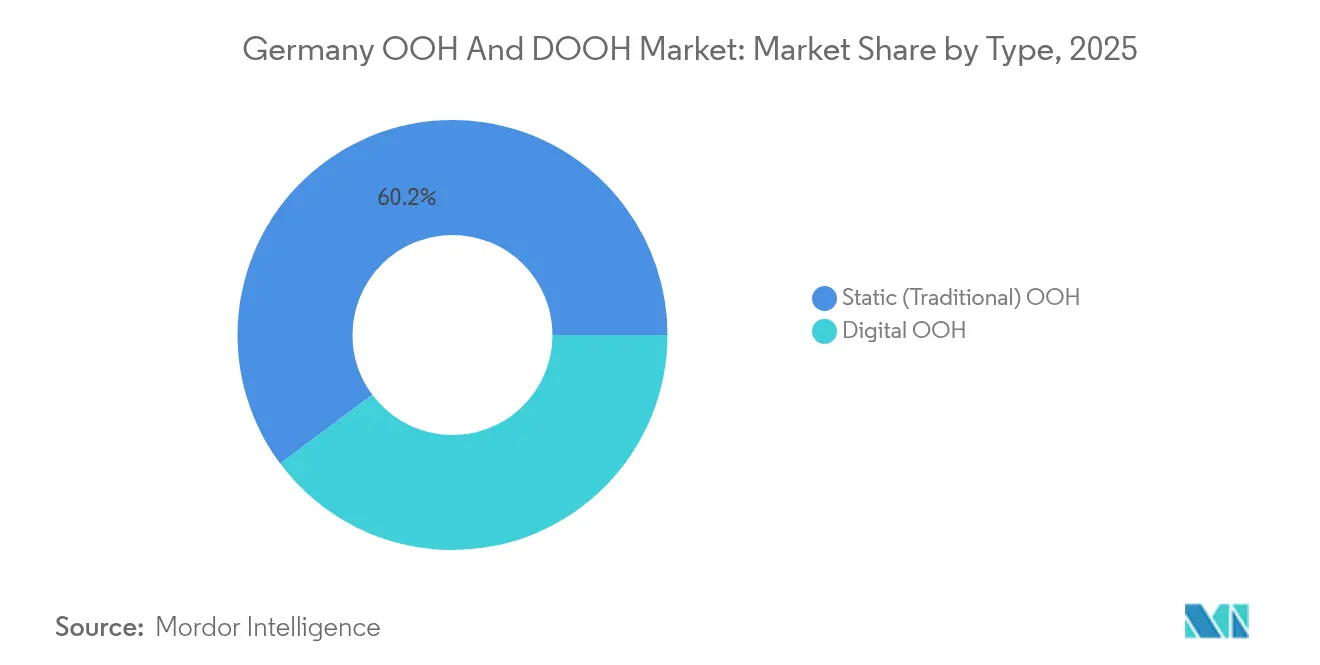

- By type, static posters led with 60.20% revenue share in 2025, while digital OOH is forecast to expand at a 12.62% CAGR through 2031.

- By format, billboards commanded 37.40% of German OOH & DOOH advertising market share in 2025; transportation media is projected to grow at 10.85% CAGR to 2031.

- By location environment, outdoor assets retained 87.50% spend in 2025, but indoor placements are advancing at 10.72% CAGR to 2031.

- By end-user industry, retail & consumer goods captured 27.60% of the 2025 billings, whereas healthcare & pharmaceuticals posts the fastest 11.28% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany OOH And DOOH Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smart-city DOOH pilots in tier-1 cities | +1.8% | Berlin, Hamburg, Munich, Cologne, Frankfurt | Medium term (2–4 years) |

| Digital screen deployment across Deutsche Bahn | +1.5% | National rail hubs | Medium term (2–4 years) |

| Retail-media DOOH in shopping malls | +1.2% | Urban and suburban retail corridors | Short term (≤ 2 years) |

| Mobile geo-targeting integration | +1.7% | Data-rich metropolitan areas | Medium term (2–4 years) |

| Programmatic OOH adoption across SSP/ DSP pipes | +1.3% | Nationwide, strongest in large metros | Medium term (2–4 years) |

| Telco data partnerships powering addressable OOH | +1.1% | National, initial focus on high-traffic transport hubs | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Sponsorship of smart-city DOOH pilots in tier-1 German cities

Digital street furniture placed inside municipal smart-city programs delivers premium inventory that combines way-finding, transit updates and brand content in one unit stroeer. Screens at pedestrian eye level record high dwell without appearing intrusive and enjoy automated context switching through city-owned data feeds that trigger weather or event messages. Councils bundle long concessions with carbon-reduction clauses, giving media owners predictable cash flows to fund LED investment. This alignment between civic utility and private revenue keeps the German OOH & DOOH advertising market on a steep digital adoption path over the coming four years.

Rapid digital screen deployment across the Deutsche Bahn network

Deutsche Bahn’s “Zukunft Bahn” modernisation replaces static posters with full-motion 16:9 displays in rail concourses, pushing daily views at Frankfurt Hauptbahnhof to over 40,000 and average dwell to 8–12 minutes bahn. Repeat commuter visits allow frequency-based scheduling that approaches digital-video reach, while live passenger APIs trigger creative changes such as weather-adaptive offers, placing the German OOH & DOOH advertising market on par with mobile display in dynamism.

Retail-media DOOH roll-out in shopping malls

Mall operators such as ECE Group transform corridors, food courts and car-park entrances into programmatic networks that monetise foot traffic beyond rent. [1]ECE Group, “Future Forward ECE 2024/25,” ece.com Screens near escalators accumulate up to 45–120 minutes of cumulative dwell, and demand-side platforms let FMCG and fashion brands buy loops in near real time. Programmatic OOH is set to reach 28.7% of German DOOH revenue in 2025, up from 3.7% in 2020.[2]WallDecaux GmbH, “Media Guide 2025,” walldecaux.de Layering Wi-Fi data enables shopper segments such as “grocery regulars,” supporting the attractiveness of the German OOH & DOOH advertising market for agencies reallocating budgets from online display.

Integration of mobile geo-targeting with OOH

The fusion of Adsquare analytics into WallDecaux’s OOH-Planner helps planners overlay device movement on every poster panel nationwide horizont. Advertisers can expose a consumer on Monday morning and retarget the same device in-app on Tuesday, lifting store-visit rates by 25–35%. Deterministic measurement fills the attribution gap and protects outdoor budgets, while GDPR-compliant triggers such as “screen on when stadium exits surge” will soon be routine, cementing the German OOH & DOOH advertising market as an accountable channel.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban-planning restrictions on illumination | -1.4% | Historic city centers nationwide | Medium term (2–4 years) |

| Rising electricity costs for large LEDs | -1.2% | National, strongest where energy-intensive formats dominate | Short term (≤ 2 years) |

| Regulatory fragmentation among Bundesländer | -1.0% | Nationwide, higher complexity in heritage districts | Medium term (2–4 years) |

| Heritage-district vetoes on digital screens | -0.9% | Dresden, Bamberg, other UNESCO-listed zones | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Tight restrictions on illuminated displays under urban-planning ordinances

City bylaws in Düsseldorf, Cologne and Leipzig cap luminance, limit sequential animations and set minimum wall distances, stretching permit processes from six to 18 months in listed areas tagesschau. Slower rollout reduces digital yield per site and forces brands to concentrate spend on fewer screens, curbing campaign flexibility across the German OOH & DOOH advertising market. Without federal harmonisation, programmatic bookings that rely on uniform specs will remain constrained.

Rising electricity costs undermining large-format LED profitability

Wholesale power prices climbed 24% between Q1 2024 and Q1 2025, adding EUR 1,300 annual cost to every 10 m² screen and pushing network consumption to 113,000 MWh, equal to 40,000 households tagesschau. Margin compression drives operators to dim screens after hours and shift capex toward smaller LCD kiosks, slowing expansion of German OOH & DOOH advertising market inventory along suburban arterials.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Digital transformation accelerates despite static dominance

Static posters delivered USD 951.16 million in 2025, equal to 60.20% of the German OOH & DOOH advertising market size, as advertisers value cost efficiency and nationwide reach stroeer. Yet inventory saturation limits growth to 3.32% CAGR. Digital OOH is forecast to rise at 12.62% CAGR to 2031, powered by animated creative, flexible daypart selling and data-targeting engines. Digital’s share of the German OOH & DOOH advertising market climbed from 24.00% in 2020 to 39.80% in 2025 tagesschau. Operators such as Ströer convert legacy posters into LED street furniture to lift yield per square metre and attract direct-to-consumer brands needing fast creative swaps. Councils now award concessions to proposals featuring energy-efficient screens and public-service widgets, ensuring sustained momentum for the German OOH and DOOH advertising industry.

By Format: Transportation media captures premium audiences

Billboards held 37.40% of German OOH & DOOH advertising market share and generated USD 590.92 million spend in 2025 walldecaux. Their roadside ubiquity secures broad frequency for FMCG and telco advertisers. Transportation media - rail, airports, bus shelters - is positioned to grow at 10.85% CAGR through 2031. Deutsche Bahn concourse digitisation funnels commuters toward 1080p displays, while Stuttgart Airport’s Digital Departure Network reaches 40,000 passengers weekly stuttgart-airport. Dwell up to 110 minutes supports long-form storytelling and justifies premium CPMs, lifting transportation’s future share of German OOH and DOOH advertising market size.

By Location Environment: Indoor formats gain momentum

Outdoor assets still attract 87.50% of spend in 2025, yet indoor environments will expand at 10.72% CAGR. Controlled lighting, ambient comfort and Wi-Fi analytics let advertisers personalise content and close the performance gap with mobile display ece. ECE’s network layers point-of-sale data onto scheduling to push real-time promotions, giving retailers closed-loop attribution. Landlord ownership removes permit hurdles, allowing quick screen deployment and securing new budget flows into the German OOH and DOOH advertising market from e-commerce players reaching shoppers offline.

By End-User Industry: Healthcare sector embraces visual impact

Retail & consumer goods led spend with 27.60% of 2025 billings by pairing roadside six-sheets with mall LEDs to intercept shoppers near purchase. Healthcare & pharmaceuticals is projected to record the fastest 11.28% CAGR, supported by over-the-counter brands and hospital groups building trust at scale. Contextual triggers link pollen counts to antihistamine ads and temperature spikes to sun-cream messages, elevating brand quality inside the German OOH and DOOH advertising market and encouraging medical advertisers to boost share-of-voice.

Geography Analysis

Germany’s four largest metros - Berlin, Hamburg, Munich and Frankfurt - host 60% of deployable digital street furniture, anchoring 2024 revenue growth for the German OOH & DOOH advertising market walldecaux. WallDecaux’s DigitalCityNet spans 40,000 surfaces across these cities, giving planners national reach with local nuance. Regulatory fragmentation complicates nationwide rollouts; Bavaria allows 24-hour illumination on transport property while North Rhine-Westphalia caps brightness after 22:00 in residential zones, forcing creative adaptation. Heritage districts in Dresden and Bamberg often veto digital screens outright, funnelling spend into static posters and limiting market depth. Nonetheless, councils increasingly bundle public Wi-Fi, air-quality sensors and emergency call points into advertising kiosks, aligning civic and commercial interests across the German OOH and DOOH advertising market.

Transport hubs provide nationwide reach. Frankfurt Airport handles 59 million passengers yearly, with baggage-hall LEDs commanding CPMs 160% above roadside six-sheets. Deutsche Bahn stations extend digital coverage into mid-size cities such as Kassel and Saarbrücken, broadening advertiser access to regional audiences. This distribution sustains consistent inventory growth within the German OOH and DOOH advertising market.

Rural and suburban corridors remain largely static but offer cost-efficient frequency. Operators focus on energy-efficient LCD kiosks to meet municipal sustainability goals and contain power costs, balancing coverage expansion with profitability. As fibre backhaul improves, remote areas will gain programmatic capabilities, incrementally lifting the national penetration of digital inventory across the German OOH and DOOH advertising market.

Competitive Landscape

Four heritage operators - Ströer, JCDecaux (WallDecaux), Clear Channel and Media Frankfurt - dominate, with Ströer alone managing 300,000 media carriers and posting 17.4% organic revenue expansion in early 2025 stroeer. Their combined scale delivers bargaining power with municipalities and brands, streamlining concession renewals and enabling network-wide rollouts.

Private-equity appetite intensifies. Indicative bids above Ströer’s market capitalisation highlight investor hunger for cash-generative estates backed by long concessions finanzwire. Telecom groups are also active.[3]JCDecaux SE, “Half-Year Results 2024,” jcdecaux.com USD 600 million purchase of programmatic specialist Vistar Media merges telco data with out-of-home supply to enrich targeting t-mobile. These new entrants accelerate digitisation, while incumbents defend share through estate upgrades and data partnerships.

Product innovation centres on programmatic pipes. JCDecaux recorded 61.8% YoY programmatic revenue growth in H1 2024.[4]T-Mobile US Inc., “Vistar Media Acquisition Press Release 2025,” t-mobile.com Ströer’s proprietary SSP “Public Video” integrates carbon-footprint calculators, enabling brands to offset emissions at booking and maintain price premiums. Such differentiation supports pricing power even as trading models shift from tenancy contracts to impression-based auctions across the German OOH & DOOH advertising market.

Germany OOH And DOOH Industry Leaders

Ströer SE & Co. KGaA

JCDecaux SA (incl. WallDecaux)

Clear Channel Outdoor Deutschland

blowUP media GmbH

Goldbach Group AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Ströer reported 22% organic revenue growth in out-of-home advertising, underscoring sustained German expansion

- February 2025: Ströer’s share price jumped 15% on strong outdoor results, reflecting investor confidence

- January 2025: Ströer confirmed talks to divest core assets after private-equity offers topped book value

- January 2025: T-Mobile agreed to acquire Vistar Media for USD 600 million, deepening telco-adtech convergence

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the German out-of-home (OOH) advertising market as paid brand messages that reach audiences outside their homes across static displays such as billboards, street furniture, and transit posters, plus digital out-of-home (DOOH) screens that deliver dynamic or programmatic content in similar environments. According to Mordor Intelligence, the scope tracks net advertiser spend generated within Germany and excludes agency commissions.

Scope exclusion: indoor point-of-sale screens located inside retail stores and shopping malls are not counted.

Segmentation Overview

- By Type

- Static (Traditional) OOH

- Digital OOH

- Programmatic DOOH

- Other Digital Formats

- By Format

- Billboard

- Transportation (Transit)

- Airports

- Rail and Metro

- Roadside Bus Shelters

- Street Furniture

- Place-Based Media

- By Location Environment

- Outdoor

- Indoor

- By End-User Industry

- Automotive

- Retail and Consumer Goods

- Healthcare and Pharmaceuticals

- BFSI

- Media and Entertainment

- Other End Users

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted structured conversations with media planners, outdoor network operators, programmatic tech providers, and brand advertisers across Berlin, Hamburg, Munich, and Cologne. These interviews validated share-of-spend splits, fill-rate assumptions, and screen utilization ranges, which were then reconciled with the desk findings.

Desk Research

We mapped the demand pool through public sources such as the Federal Statistical Office, the German Outdoor Advertising Association, Eurostat mobility dashboards, IAB Europe ad-spend trackers, and Digital Signage Federation white papers. Company filings, investor decks, and reputable press helped us benchmark screen roll-outs and CPM trends. Select paid databases, D&B Hoovers for financials and Dow Jones Factiva for deal news, filled corporate data gaps. This list is illustrative; many additional references informed our estimates and narrative.

Market-Sizing & Forecasting

A top-down model begins with Germany's total advertising spend, applies the historical OOH share, and then reconstructs DOOH revenue using screen counts, average ad load factors, and prevailing CPMs. Supplier roll-ups and sampled average selling price multiplied by impression volumes provide the needed bottom-up cross-check. Key inputs include urban footfall indices, fleet expansion of digital panels, screen brightness hour regulations, programmatic buying penetration, and euro-to-dollar exchange trajectories. Forecasts employ a multivariate regression blended with ARIMA to capture cyclical ad-budget swings, with scenario adjustments vetted by our primary research participants. Data voids in supplier roll-ups are bridged using weighted averages drawn from similar-sized municipalities.

Data Validation & Update Cycle

Outputs pass variance checks against independent spend trackers, then enter a two-tier analyst review before sign-off. The report refreshes annually, and interim revisions are triggered by material events such as regulatory shifts or double-digit revenue surprises; a last-mile validation is performed just before client delivery.

German OOH And DOOH Baseline Numbers You Can Trust

Published estimates often diverge because firms adopt different platform scopes, currency conversions, and refresh cadences.

The comparison shows that values swing when scope or input rigor changes.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.58 B (2025) | Mordor Intelligence | - |

| USD 2.04 B (2024) | Global Consultancy A | Focuses mainly on static billboard and outdoor formats and projects forward without validating DOOH share shifts |

| €1.3 B (2025) | Data Analytics Firm B | Aggregates OOH and DOOH but relies on extrapolated growth factors instead of verified screen inventories |

By combining clear market boundaries, audited variables, and a documented update cycle, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can rely on.

Key Questions Answered in the Report

What is the current size of the German OOH And DOOH advertising market?

The German OOH And DOOH advertising market size is USD 1.72 billion in 2026 and is projected to reach USD 2.65 billion by 2031 at a 8.98% CAGR.

Which segment is growing fastest within the market?

Digital OOH is the fastest-expanding type, forecast to rise at 12.62% CAGR from 2026 to 2031 as advertisers shift toward dynamic, data-driven formats.

How significant is programmatic buying in German DOOH?

Programmatic spending is expected to reach EUR 553 million in 2025, equal to 28.7% of total DOOH revenue, up from 3.7% share in 2020.

Why are transportation hubs important for advertisers?

Train stations and airports deliver long dwell times, 8-12 minutes on rail platforms and up to 110 minutes in departure lounges, giving brands ample opportunity to engage high-spending travellers.

Page last updated on: