Brazil OOH And DOOH Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

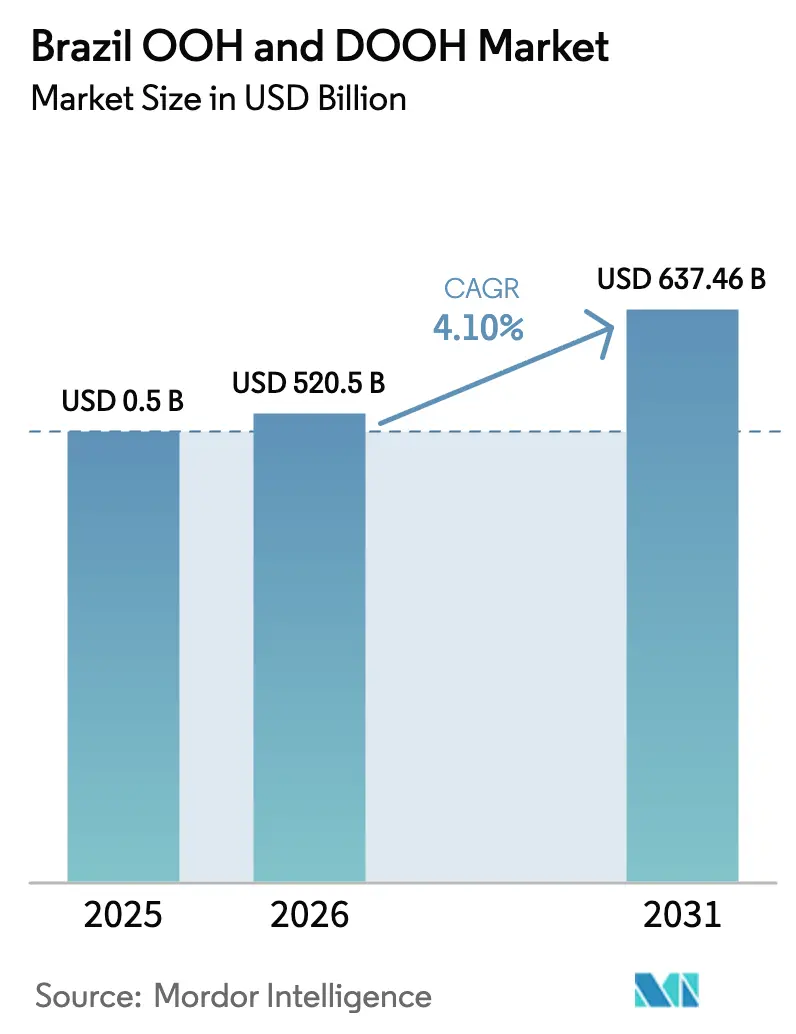

| Base Year Market Size (2025) | USD 0.50 Billion |

| Market Size (2026) | USD 520.5 Billion |

| Market Size (2031) | USD 637.46 Billion |

| Growth Rate (2026 - 2031) | 4.10% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil OOH And DOOH Market Analysis by Mordor Intelligence

Brazil out-of-home and digital out-of-home advertising market size in 2026 is estimated at USD 520.5 million, growing from 2025 value of USD 0.50 billion with 2031 projections showing USD 637.46 million, growing at 4.10% CAGR over 2026-2031. Rising digitization of roadside and place-based inventory, programmatic trading adoption, and smart-city infrastructure projects are the primary engines behind this advance. Digital formats already capture more than half of total spend, and airport, transit, and mall networks accelerate the shift by offering high dwell-time environments that are compatible with data-driven targeting. Integration of programmatic pipes lowers campaign set-up friction and aligns outdoor buys with standard digital metrics, prompting advertisers to reallocate budgets from online display into DOOH. Meanwhile, mega-events such as the 2027 FIFA World Cup and ongoing public–private partnerships in street lighting modernization continue to create premium inventory pockets in host cities. Intensifying consolidation, exemplified by Globo’s acquisition of Eletromidia, broadens cross-channel packages but simultaneously raises competitive stakes for mid-sized networks.

Key Report Takeaways

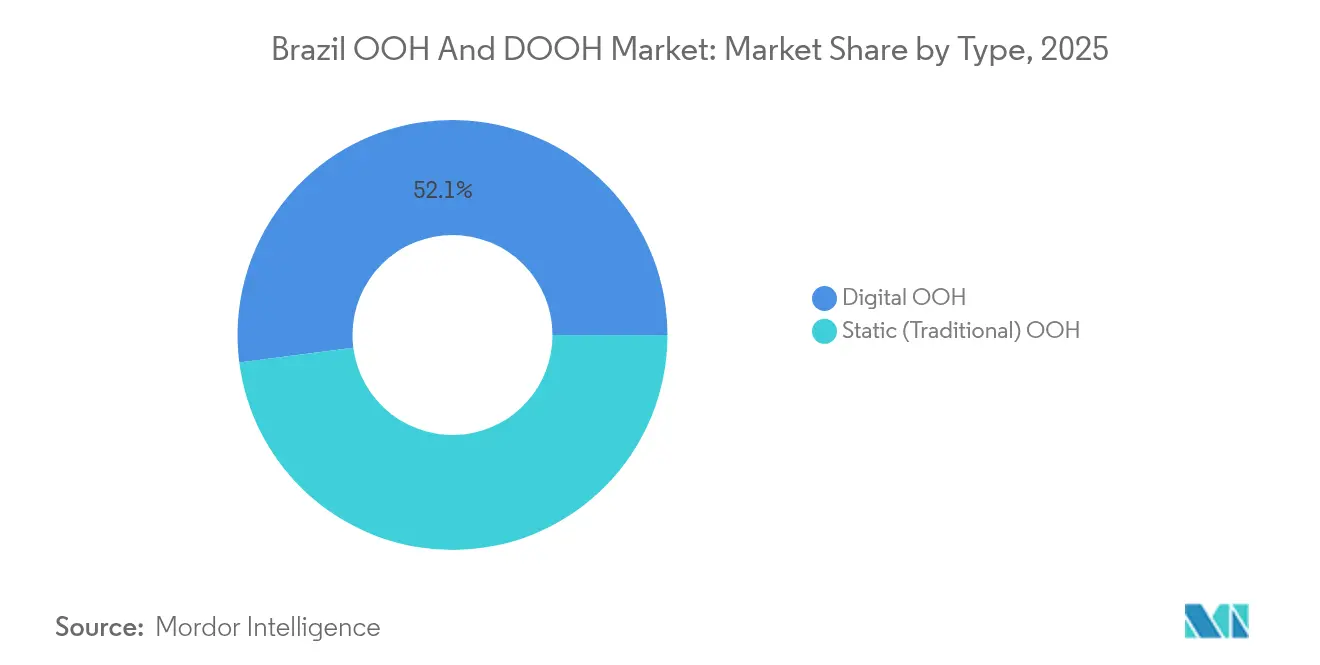

- By type, digital OOH led with 52.05% market share in 2025, programmatic DOOH is forecast to post the fastest 5.97% CAGR through 2031.

- By application, billboards retained the largest application slice at 38.10% in 2025 in the Brazil OOH and DOOH market and transportation is positioned for the strongest 5.45% CAGR to 2031.

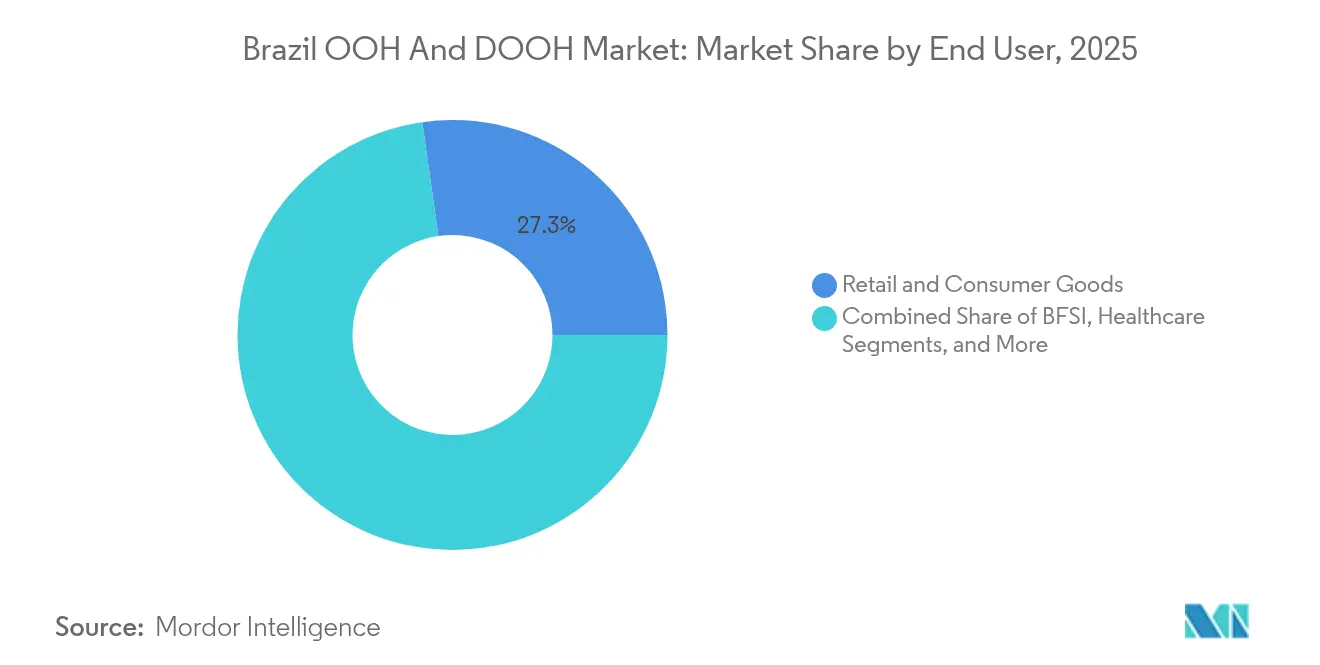

- By end user, retail and consumer goods captured 27.25% of 2025 in the Brazil OOH and DOOH market and healthcare end-users are projected to expand at a 5.26% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil OOH And DOOH Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging smart-city investments catalysing digital street furniture | +1.2% | National, concentrated in São Paulo, Rio de Janeiro, Brasília | Medium term (2-4 years) |

| Programmatic DOOH adoption by national media buyers | +0.8% | National, with São Paulo and Rio leading adoption | Short term (≤ 2 years) |

| Recovery of air-travel fuelling airport media demand | +0.6% | National, focused on major airports (GRU, BSB, Congonhas) | Short term (≤ 2 years) |

| FIFA World Cup 2027 and other mega-events boosting spend | +0.4% | National, with concentration in host cities | Short term (≤ 2 years) |

| Growing retail-media networks inside Brazilian malls | +0.3% | National, concentrated in major metropolitan areas | Medium term (2-4 years) |

| Open-banking data powering audience targeting | +0.2% | National, urban markets primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Smart-City Investments Catalyzing Digital Street Furniture

Brazilian municipalities have committed R$27 billion to public-lighting modernization contracts that bundle LED upgrades with digital signage capabilities, enabling DOOH operators to piggyback on existing poles, power, and fiber.[1]Expolux Editorial, “Investimento de PPP em iluminação urbana chega a R$ 27 bi,” expolux.com.br São Paulo’s Smart Sampa program already links 31,300 connected devices and targets 40,000 by 2026, producing a dense network of addressable street furniture that can deliver context-aware messaging based on traffic speed, ambient light, and weather data.[2]Prefeitura de São Paulo, “Programa Smart Sampa ultrapassa 31,3 mil câmeras,” capital.sp.gov.br Such public–private partnerships lower deployment cost and shorten permitting cycles for DOOH firms while supplying cities with revenue-sharing income and civic-messaging slots. Rapid illumination retrofits in mid-sized municipalities replicate the São Paulo model, signaling scalable nationwide potential. As retrofit projects bundle CMS software within lighting control systems, operators gain the ability to segment creatives down to individual poles, thereby matching audience movement with retailer foot-traffic patterns. This infrastructure foundation is expected to underpin the next wave of hyperlocal, data-infused DOOH campaigns that merge physical reach with digital precision.

Programmatic DOOH Adoption by National Media Buyers

Programmatic buying now accounts for one quarter of all DOOH campaigns, with 51% of those advertisers executing exclusively through automated pipes and the remainder mixing programmatic and direct buys. Global supply-side platforms such as Vistar Media, Hivestack, and VIOOH collectively onboarded more than 46,000 screens during 2024, giving brands real-time access to high-footfall environments from airports to street clocks. National advertisers increasingly value dynamic creative optimization, geo-fencing, and audience-based pricing that mirror online video benchmarks, triggering budget shifts from display and social into DOOH. Agency studies indicate that 43% of marketers reallocated spend from other digital formats to programmatic outdoor in 2024, and they anticipate a further 27% budget lift over the next 18 months. DSP integrations also unlock imported demand from multinational brands buying Brazilian impressions through the same seat used for U.S. or European campaigns. Harmonized measurement APIs, such as OpenRTB extensions for screen attributes, are expected to close remaining data gaps and expand header-bidding style auctions into high-impact roadside units.

Recovery of Air-Travel Fueling Airport Media Demand

Passenger traffic rebounded sharply, with Aena’s 17-airport network alone handling 43 million travelers in 2024. Premium demographics, average household income above 13 minimum wages, make airports a magnet for luxury, fintech, and travel advertisers seeking affluent audiences. Advertiser interaction rates as high as 84% underscore the engagement value of dwell-time environments where travelers actively seek wayfinding and retail information. Aena launched a nationwide tender in February 2025 to standardize media management across its concessions, including upgrades to large-format LEDs, interactive directories, and programmatic ad servers, with new 10-year contracts slated for award by late-2025. The modernization push enhances measurement consistency, unlocks dynamic pricing models, and elevates airport inventory to parity with downtown digital billboards, accelerating campaign deployment ahead of the 2027 World Cup visitor surge.

FIFA World Cup 2027 and Other Mega-Events Boosting Spend

Globo alone targets nearly BRL 2 billion in sponsor commitments around the 2026 World Cup broadcast portfolio, a benchmark that spills over into OOH as brands coordinate cross-channel reach. Historical spending patterns show double-digit uplifts in outdoor budgets during tournament years, particularly in host-city corridors where fan zones and public-viewing arenas demand extensive brand activation. Stadium perimeters, airport arrival halls, and fan-mile routes are earmarked for temporary but high-yield digital installations designed for real-time creative rotations tied to match outcomes. Beyond football, Carnival, Rock in Rio, and election campaigns produce seasonal spikes that validate DOOH’s agility in handling short booking windows and contextual triggers. For networks, these events justify capex in modular, mobile screen formats that can be repurposed after event tear-down, enhancing asset utilization year-round.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented measurement standards across operators | -0.6% | National, affecting programmatic adoption | Medium term (2-4 years) |

| High import tariffs on LED panels inflating capex | -0.4% | National, impacting equipment costs | Short term (≤ 2 years) |

| Municipal permit moratoriums in historic districts | -0.3% | Historic city centers, heritage zones | Long term (≥ 4 years) |

| Rising ad-fraud concerns in programmatic pipes | -0.2% | National, concentrated in digital channels | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Measurement Standards Across Operators

Brazil lacks a unified outdoor currency comparable to Route in the U.K. or Geopath in the U.S., forcing advertisers to reconcile disparate reach calculations, footfall sensors, and impression multipliers. Operators deploy proprietary methodologies, ranging from Wi-Fi probes to computer-vision counts, without standardized audit protocols, complicating cross-network flight optimization. Programmatic buyers, reliant on uniform impression logs, balk at inconsistent confidence intervals that can vary by more than 35% across vendors, limiting spend scalability. Industry bodies such as ABOOH have begun drafting common metrics, yet consensus on accreditation and data privacy safeguards remains two to three years away, dampening near-term growth potential.

High Import Tariffs on LED Panels Inflating Capex

Imported LED modules incur combined duties and federal taxes that can push landed costs 45% above invoice value, squeezing ROI calculations for new roadside and transit screens.[3]International Trade Administration, “Brazil – Import Tariffs,” export.gov The ex-tarifário program temporarily lowers rates to 2% for equipment without local substitutes, but approval probabilities dropped in 2024 after rule revisions tightened local-content evidence requirements.[4]International Trade Administration, “Brazil Customs Tariff Exception,” trade.gov Smaller entrants face steep financing hurdles, widening the competitive moat for incumbents with amortized static assets. Currency volatility adds further risk; a 5% BRL depreciation lifts capex by at least BRL 22,000 per 10-sqm roadside unit, delaying breakeven by up to 12 months. Some operators pivot to local assembly of metal frames and power supplies to qualify for reduced ICMS brackets, though high-precision processing chips still require import.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Digital Dominance Accelerates Programmatic Integration

Digital formats controlled 52.05% of the Brazil out-of-home and digital out-of-home advertising market share in 2025, underpinned by falling hardware costs and municipal concessions that favor multi-use electronic panels. Programmatic sub-formats are projected to clock a 5.97% CAGR, ensuring that the Brazil out-of-home and digital out-of-home advertising market size contribution from addressable screens surpasses USD 0.37 billion by 2031.

Static inventory retains relevance in cost-sensitive secondary markets where electricity or fiber backhaul is scarce, yet advertisers increasingly prioritize the dynamic creative refresh and hourly pricing flexibility of LEDs. Integration deals, such as Eletromidia’s onboarding of 46,000 screens into Hivestack and Vistar ecosystems, signal irreversible momentum toward automated trading. As SSPs roll out predictive-audience modules that combine traffic, weather, and point-of-sale data, digital screens are expected to achieve CPM premiums of 18-23% over static equivalents, accelerating asset conversion roadmaps for tier-two operators.

By Application: Transportation Momentum Builds on Airport Recovery

Billboards remained the largest slice, accounting for 38.10% of 2025 spending within the Brazil out-of-home and digital out-of-home advertising market. Transportation media, however, is slated for a 5.45% CAGR, pushing its Brazil out-of-home and digital out-of-home advertising market size to nearly USD 0.19 billion by 2031.

Airports, metros, and bus fleets provide closed-environment dwell times conducive to sequential storytelling, while integration of QR-code prompts bridges physical screens with mobile commerce. The roll-out of B-Air Digital across 1,000 São Paulo buses by 2026 exemplifies how transit operators monetize passenger journeys through synchronized route-based ad triggers. Street-furniture gains additional traction through smart-pole initiatives that combine LED lighting savings with advertising revenue shares, yielding IRRs above 17% for concessionaires.

By End-User: Healthcare Acceleration Reflects Sector Digitization

Retail and consumer goods dominated advertiser categories with 27.25% share in 2025, aided by omnichannel campaigns that align Black Friday pushes across social, ecommerce, and mall screens. Healthcare’s 5.26% forecast CAGR positions it as the fastest riser, enabling its Brazil out-of-home and digital out-of-home advertising market share to double by 2031.

Pharma brands leverage DOOH for disease-awareness education ahead of teleconsultation links, while hospital chains use directional signage in proximity to clinics to influence appointment bookings. Banks and insurers continue heavy presence to reinforce digital-banking propositions, especially around PIX instant-payment milestones. Automotive spends surge on the back of Chinese EV newcomers that tap highway LEDs for launch teasers synchronized with social video, demonstrating the cross-channel orchestration potential of DOOH creatives.

Geography Analysis

The Southeast region claimed 56.40% of national OOH insertions in 2025, reflecting the economic weight and regulatory maturity of São Paulo and Rio de Janeiro. São Paulo’s combination of the Smart Sampa sensor grid, progressive concession policy, and the Lei Cidade Limpa ban on unlicensed large-formats channels advertising investment into compliant digital street furniture. The city alone hosts more than 1,000 networked street clocks, each capable of delivering location-aware creatives and public notices under a 25-year concession with JCDecaux.

Rio de Janeiro, the second-largest market, faces intermittent infrastructural challenges, illustrated by the Smart Luz concession delays, yet benefits from imminent tourism spikes linked to World Cup fan travel and cruise-ship stopovers. The South region, covering Porto Alegre, Curitiba, and Florianópolis, contributes 16.20% of placements and offers streamlined permitting, encouraging sustained digital conversions of older static sites.

Northeast cities such as Salvador, Recife, and Fortaleza represent 14.10% of placements but register double-digit growth as Carnival and beach tourism reignite advertiser demand. Regional operators expand via mall and airport concessions, enabling brands to cover affluent leisure spenders with high propensity to use mobile wallets for on-the-spot purchases. Center-West accounts for 8.70%, anchored by Brasília’s government communication requirements and premium airport lounges catering to public officials and diplomats. The North trails at 4.60% yet is primed for expansion as fiber-optic corridors along the Manaus Free Trade Zone improve backhaul economics for digital roadside screens.

Competitive Landscape

Brazil’s market shows moderate fragmentation; the top five players control an estimated 63% of gross ad sales, leaving room for regional specialists and retail-media startups. Eletromidia leads with 66,000 panels, having been folded into Globo’s multi-platform portfolio in December 2024 to create bundled TV-digital-OOH packages that command premium CPMs. JCDecaux retains street-furniture supremacy via long-term São Paulo and Rio concessions, while Clear Channel focuses on airport and metro corridors.

Neooh’s March 2025 acquisition of Wide Digital added 12,000 screens and expanded coverage to 700 municipalities, vaulting the firm to third place in mall and grocery environments. International SSPs Vistar Media, Hivestack, and VIOOH embed Brazilian inventory into global buying platforms, exposing domestic networks to multinational demand but also imposing transparency and viewability standards. Smaller independents pursue niche verticals, such as beauty-salon DOOH or favela community screens, to secure localized contracts insulated from big-network pricing pressure.

Strategic moves center on measurement partnerships and data alliances. Eletromidia pilots computer-vision counts with Intelbras to validate impression delivery; Neooh integrates point-of-sale data from Grupo BIG supermarkets to demonstrate in-store sales lift. Hardware innovation also differentiates players: RZK’s large-format LED cube installed in Brasília’s Esplanada offers 360-degree visibility and programmatic lighting sync for festival sponsorships. Ultimately, competitive advantage shifts to operators that can aggregate nationwide inventory, plug into programmatic demand, and comply with evolving privacy and anti-fraud mandates.

Brazil OOH And DOOH Industry Leaders

JCDecaux Brazil

Eletromidia SA

Hivestack Technologies Inc.

Central de Outdoor Associação Brasileira de Mídia Exterior

Clear Channel Outdoor Brasil Ltda.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Neooh acquired Wide Digital, adding 12,000 screens and expanding coverage to 700 municipalities.

- March 2025: Maely OOH and C2R launched B-Air Digital, aiming to outfit 1,000 São Paulo buses with screens by end-2026.

- February 2025: Aena issued a tender to standardize media across 17 airports; contract awards expected H2 2025.

- January 2025: Vistar Media launched programmatic DOOH operations in Brazil, integrating 30,000 screens.

Brazil OOH And DOOH Market Report Scope

The study tracks the advertising spending on various OOH formats, including billboards (city-light boards), street furniture (city-light posters), transit & transportation (advertising in and on vehicles used for public transportation), and place-based media (media at the point of sale). The scope of the study includes digital and static advertisements placed indoors and outdoors at shopping malls, airports, streets, and transit, among others. The commission and production costs of agencies are excluded from the scope of work.

The OOH and DOOH market in Brazil is segmented by type (static [traditional] OOH and digital OOH [programmatic OOH and other DOOH types]), application (billboards, transportation [airports and others (buses, etc.)], street furniture, and other place-based media), and end-user industry (automotive, retail and consumer goods, healthcare, BFSI, and other end users). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Static (Traditional) OOH | |

| Digital OOH (LED Screens) | Programmatic OOH |

| Other Digital Formats |

| Billboard | |

| Transportation (Transit) | Airports |

| Other Transit (Buses, Metro, etc.) | |

| Street Furniture | |

| Other Place-based Media |

| Automotive |

| Retail and Consumer Goods |

| Healthcare and Pharma |

| Banking, Financial Services and Insurance (BFSI) |

| Other End-Users |

| By Type | Static (Traditional) OOH | |

| Digital OOH (LED Screens) | Programmatic OOH | |

| Other Digital Formats | ||

| By Application | Billboard | |

| Transportation (Transit) | Airports | |

| Other Transit (Buses, Metro, etc.) | ||

| Street Furniture | ||

| Other Place-based Media | ||

| By End-User | Automotive | |

| Retail and Consumer Goods | ||

| Healthcare and Pharma | ||

| Banking, Financial Services and Insurance (BFSI) | ||

| Other End-Users | ||

Key Questions Answered in the Report

How large is the Brazil out-of-home and digital out-of-home advertising market in 2026?

The market stands at USD 520.5 million in 2026 and is on track to reach USD 637.46 million by 2031.

Which format leads spending today?

Digital OOH accounts for 52.05% of total spend, reflecting advertisers’ preference for dynamic, measurable screens.

What is the fastest-growing application?

Transportation media, boosted by airport and transit investments, is projected to grow at a 5.45% CAGR through 2031.

Which advertiser vertical is expanding the quickest?

Healthcare campaigns are forecast to rise at a 5.26% CAGR as providers adopt patient-engagement messaging.

How will the 2027 FIFA World Cup influence outdoor advertising?

Host-city inventory is expected to command premium pricing as brands integrate DOOH into multi-channel fan activations.

Page last updated on: