Europe OOH And DOOH Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 10.58 Billion |

| Market Size (2026) | USD 11.03 Billion |

| Market Size (2031) | USD 13.57 Billion |

| Growth Rate (2026 - 2031) | 4.23% CAGR |

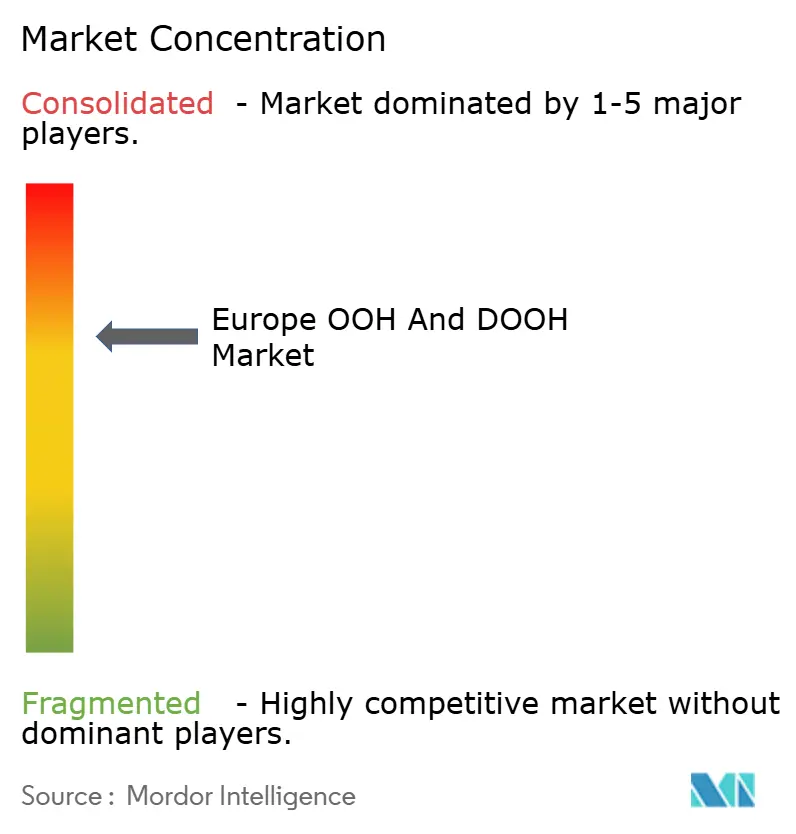

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe OOH And DOOH Market Analysis by Mordor Intelligence

The Europe OOH and DOOH market size in 2026 is estimated at USD 11.03 billion, growing from 2025 value of USD 10.58 billion with 2031 projections showing USD 13.57 billion, growing at 4.23% CAGR over 2026-2031. The upward curve is underpinned by rapid digitization of roadside and transit inventory, rising comfort with programmatic buying, and smart-city investments that position screens as civic infrastructure. Advertisers favor the Europe OOH and DOOH market because it combines mass reach with GDPR-compliant contextual targeting, a feature that gains importance as third-party cookies deprecate across online channels. In addition, mobility rebounds in major rail, metro, and airport hubs restore pre-2020 audience volumes, supporting inventory yields even in slower macroeconomic conditions. Operators deepen competitive moats by pairing large-format LED displays with data layers, weather, traffic, and payment signals, that allow live creative optimization and verifiable incremental lift. Their ability to demonstrate brand outcomes, not just impressions, keeps budgets flowing from retail, automotive, and an expanding cohort of healthcare marketers.

Key Report Takeaways

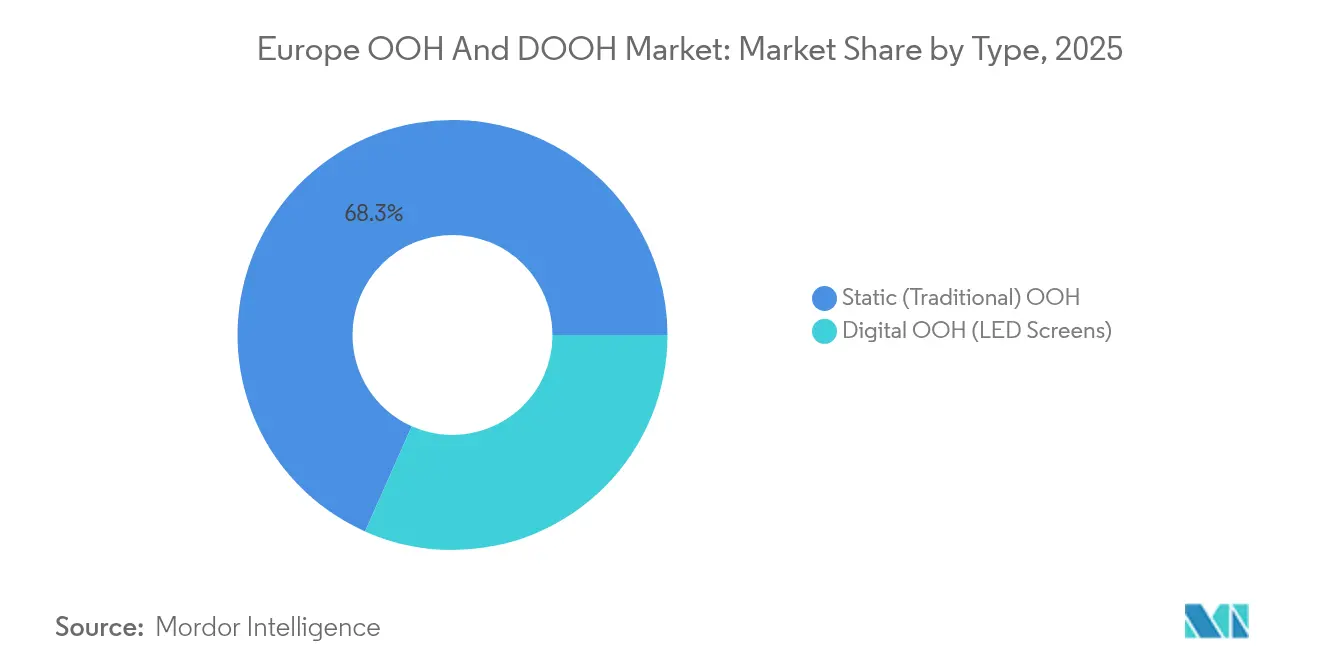

- By type, static traditional formats held 68.33% of Europe OOH and DOOH market share in 2025 while programmatic OOH posted a 6.12% CAGR, the fastest rate among inventory classes.

- By application, billboard media commanded 46.30% of the Europe OOH and DOOH market size in 2025; meanwhile, transportation advertising is forecast to grow at 5.64% CAGR through 2031.

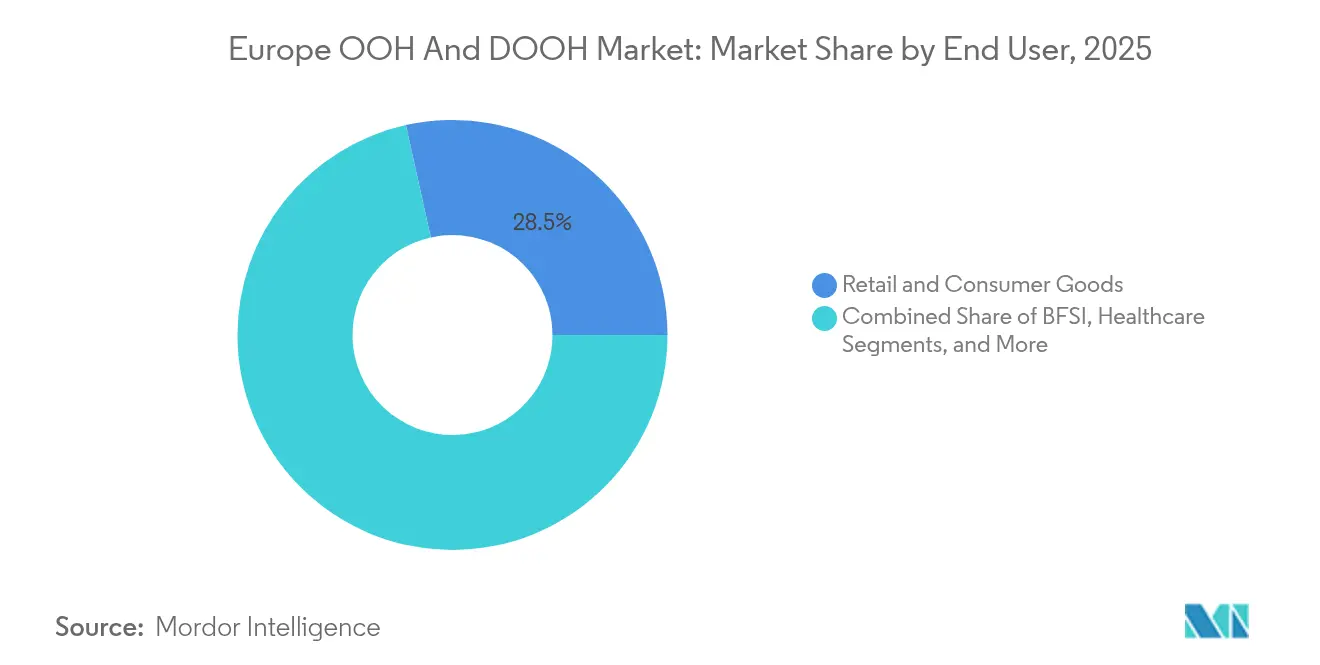

- By end user, retail and consumer goods contributed 28.48% of 2025 spend in the Europe OOH and DOOH market, whereas healthcare campaigns are set to climb at a 5.21% CAGR over the same horizon.

- By country, Germany captured 27.60% revenue in 2025 in the Europe OOH and DOOH market; in contrast, the United Kingdom is on track for a 5.18% CAGR to 2031, the quickest pace among major economies

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe OOH And DOOH Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid digitisation of European OOH inventory | +1.2% | Global, with early gains in UK, Germany, Netherlands | Medium term (2-4 years) |

| Post-pandemic rebound in commuter and tourist footfall | +0.8% | Global, spill-over to major European transit hubs | Short term (≤ 2 years) |

| Programmatic buying unlocks measurability and ROI | +1.5% | North America and EU, with Nordic leadership | Medium term (2-4 years) |

| Smart-city street-furniture deployments | +0.7% | Global, concentrated in major European metropolitan areas | Long term (≥ 4 years) |

| EV-charging-station DOOH networks | +0.5% | APAC core, spill-over to Germany, Netherlands, Nordic markets | Long term (≥ 4 years) |

| AI-driven dynamic creative optimisation | +0.4% | Global, with early adoption in UK, Germany, Switzerland | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Digitization of European OOH Inventory

Operators accelerate LED rollout to monetize programmatic premiums. Ströer enlarged its German screen network by 23% in 2024, pushing digital revenue to EUR 2.05 billion, 37% of which arrived via automated trading.[1]PPC Land, “Ströer Expands Digital Network,” ppc.land JCDecaux will install large cross-track displays across 14 Stockholm subway stations by 2026, while Ocean Outdoor's 3D “DeepScreen” installations bring premium CPMs to landmark sites in London and Amsterdam. Digital upgrades extend beyond large roadside canvases; MOIA equips 530 Hamburg ride-share vehicles with 75-inch in-car panels that reach 200,000 passengers monthly.[2]Moia, “Vehicle Ads,” moia.io These assets allow location-specific trigger-based creatives, accurate impression verification, and instant copy swaps during breaking news or match days, benefits impossible with paste-and-paper static boards.

Post-Pandemic Rebound in Commuter and Tourist Footfall

Passenger flows through metro, bus, and rail corridors now approximate 2019 volumes in Berlin, Paris, and Madrid, restoring dwell-time value for advertisers. Greater Stockholm’s 2.5 million residents funnel 45% of Sweden’s ad spend and attract 4 million annual tourists, boosting demand for transit inventory across the city’s 1,500-plus shelters. Airport media benefits disproportionately: premium LED gateways inside Frankfurt, Heathrow, and Schiphol run full during peak departure windows as airlines reinstate global routes. JCDecaux’s 13-year Rome bus-and-tram renewal underscores operator confidence in mass-mobility economics. Return to office routines revitalizes commuting patterns that underpin Europe OOH and DOOH market revenue forecasts.

Programmatic Buying Unlocks Measurability and ROI

Automated bidding connects digital screens to omnichannel demand-side platforms so brands can unify out-of-home with mobile, CTV, and audio spending. Mercedes-Benz cut cost-per-acquisition by 71% in Spain after layering first-party data into programmatic DOOH deals executed via The Trade Desk. The 2024 merger of Signkick and LiveDOOH produced a unified supply interface supporting Clear Channel, Global, JCDecaux, and Ocean Outdoor, simplifying creative trafficking and AI-driven yield management. Resulting transparency around viewable impressions, venue context, and foot-traffic lift propels the Europe OOH and DOOH market toward performance-based pricing models traditionally associated with digital display.

Smart-City Street-Furniture Deployments

Municipalities reimagine bus shelters, information kiosks, and charging stations as dual-use civic assets. Bauer Media Outdoor added 135 interactive screens that now cover 93% of Brussels metro entrances; these units provide live transit updates beside commercial spots.[3]Bauer Media Outdoor, “2025 Highlights,” bauermediaoutdoor.com Paris, Milan, and Copenhagen embed air-quality sensors inside kiosks, enabling advertisers to trigger content when particulate levels drop below WHO thresholds, framing brands as health allies. Integration of IoT layers also supports citywide emergency alerts that override ad loops, strengthening public acceptance of digital street furniture and enabling longer concessions that underpin operator ROI.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented audience-measurement standards | -0.6% | Global, with particular challenges in multi-market European campaigns | Medium term (2-4 years) |

| Municipal light-pollution and content regulations | -0.4% | National, with early restrictions in France, Zurich, Lisbon | Long term (≥ 4 years) |

| Rising energy-price and carbon-reporting pressures | -0.3% | Global, with heightened impact in Northern Europe and Germany | Medium term (2-4 years) |

| High operator leverage limiting capex | -0.2% | Global, concentrated in leveraged buyout-backed operators | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Audience-Measurement Standards

Measurement diversity complicates cross-border media plans because Germany’s GIMedes, France’s Affimétrie, and the UK’s Route each apply unique exposure models. Bauer Media Outdoor’s proprietary People and Places tool bundles 550+ segments and 66,000 points of interest for Belgium, yet lacks harmonized equivalence with datasets in neighboring markets. For multinational advertisers, trading with inconsistent impression currencies increases reconciliation overhead and clouds ROI assessment, stalling budget fluidity across borders and tempering the growth rate of the Europe OOH and DOOH market.

Municipal Light-Pollution and Content Regulations

To curb energy use and screen brightness, Paris mandates display dimming after 11 p.m., and Zurich restricts dwell-time animations on roadside units. Lisbon capped the number of new digital faces in its historic districts, and France prohibits alcohol advertising on street furniture altogether. The EU Corporate Sustainability Reporting Directive now obliges companies above EUR 150 million turnover to publish environmental KPIs, prompting media owners to justify power consumption per screen. Suppliers such as Sharp respond with zero-watt e-paper surfaces that hold static images without electricity, but capital costs slow immediate large-scale adoption, muting expansion potential in certain precincts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Shift Toward Automated Screens Fuels Monetization

Static faces continued to dominate in 2025, accounting for 68.33% of total spend within the Europe OOH and DOOH market. Yet the Digital OOH (LED Screens) charted the fastest trajectory at 6.12% CAGR, indicating advertisers’ pivot toward impression-level buying and dynamic creative sequencing. Soft-ware advances enable automated day-parting and weather-triggered spots that lift relevance without extra production cost. The Europe OOH and DOOH market size for automated inventory is projected to capture a markedly larger slice of overall revenues by 2031 as DSP integrations mature.

Upgrades rest on platform cooperation: the Signkick-LiveDOOH merger pipes real-time availability from 200,000+ faces into omnichannel bidding environments, slashing manual insertion orders. Simultaneously, GDPR’s privacy guardrails elevate contextual media like programmatic DOOH because it forgoes cookies yet still permits deterministic location targeting. Campaigns such as Helsana’s multilingual Swiss roll-out, which localized branch directions in German, French, and Italian, illustrate how AI-driven templates raise relevance across micro-markets without inflating production budgets.

By Application: Transportation Media Bounces Back Fastest

Billboards retained a 46.30% revenue share in 2025, supported by long life cycles and country road coverage that digital networks have yet to replicate. However, transportation media, metros, buses, trams, and airports, recorded the sharpest growth path at 5.64% CAGR as commuter counts normalized and tourist inflows resurfaced across Schengen markets. The Europe OOH and DOOH market share for transit inventory is buoyed by authorities searching for ancillary revenue streams to fund mobility upgrades.

Inventory innovation is broad: EV-charging hubs combine 65-inch touchscreens with fast chargers, earning sponsorship dollars while meeting EU carbon targets. Street furniture sees smart-city overlays: Brussels’ STIB network delivers way-finding and air-quality dashboards alongside branded messages, raising dwell-time interaction metrics. Airports leverage high dwell times by offering data-triggered creatives that adapt to departure-board changes, ensuring message relevance as passengers advance from security to gate.

By End User: Healthcare Spots Outpace Retail Benchmarks

Retail and FMCG buyers remained the single largest cohort at 28.48% of 2025 billings, leaning on proximity placements to sway in-store decisions. Yet healthcare advertisers, primarily Rx and OTC drugmakers, are scaling fastest at a 5.21% CAGR through 2031, captivated by privacy-compliant audience reach and the credible context of public environments. The Europe OOH and DOOH market size devoted to healthcare already shows above-average CPMs thanks to 3-D anamorphic formats that dramatize product benefits.

Automotive and BFSI also deepen use cases. Mercedes-Benz’s Spanish dealer campaign proved data-enabled DOOH can cut acquisition costs by more than 70%, steering budgets from less measurable channels. Swiss insurer Helsana delivered branch-specific mileage and opening hours to three language groups in real time, registering lift in walk-ins during the four-week flight. Healthcare’s elevated trust scores, 45% of patients deem OOH messages credible and 84% discuss ads with clinicians, cement the vertical’s sustained climb

Geography Analysis

Germany’s strong macro fundamentals and expansive motorways secure its front-runner status, yet new growth orbits around high-impact digital corridors such as Berlin’s Kurfürstendamm and Munich’s Hauptbahnhof where synchronized full-motion takeovers generate headline-grabbing brand events. Meanwhile, the United Kingdom nurtures an ecosystem that combines advanced DSP integrations, 3-D creative standards, and measurement partnerships with tech vendors that validate incremental store visits, positioning the market as Europe’s proving ground for outcome-based.

France balances JCDecaux’s vast street-furniture estate against bright-ness curbs and heritage-site limitations that cap new digital rollouts in central Paris, nudging operators toward energy-efficient reflective panels in compliance with municipal objectives. Italy’s renaissance centers on transport concessions such as Rome’s 13-year bus-and-tram deal that brings high-definition displays into dense tourist corridors, while Spain’s fragmented regional regulations open doors for acquisitive specialists like Wildstone to knit together a cohesive national network.

The Netherlands showcases technical leadership through integrated motorway, filling-station, and mall screens tied into a single planning system, making granular frequency management possible across a country the size of Maryland. Nordic capitals pioneer sustainability KPIs; Stockholm will require screens to prove renewable-energy power sources within concession terms starting 2026, driving investment into low-consumption LEDs and lifecycle carbon audits that may become a blueprint for the wider Europe OOH and DOOH market.

Competitive Landscape

The Europe OOH and DOOH market tilts toward an oligopoly: JCDecaux, Clear Channel, and Ströer collectively steward the lion’s share of premium inventory across top metros. Bauer Media’s pending USD 625 million purchase of Clear Channel Europe consolidates 110,000 faces across 12 nations, expanding reach to 350 million residents while blending print and audio assets for cross-media packages. Although JCDecaux withdrew its EUR 60 million bid for Clear Channel Spain after regulators demanded divestitures, the attempt underscores ongoing jockeying for scale efficiencies.

Technology alliances redraw competitive lines. The Signkick-LiveDOOH platform levels the tech playing field by offering AI-priced spot allocation, marginalizing smaller networks that lack data science resources. Upstarts exploit white-space categories: ChargeEuropa links free fast-charging to 65-inch displays at Polish supermarkets, creating brand safe, dwell-rich environments that incumbent billboard owners cannot replicate quickly. Sustainability differentiation gains currency as the EU CSRD brings transparency to power consumption; Sharp’s zero-watt e-paper debuts earn early adoption credits among municipalities wary of energy-guzzling displays.

Europe OOH And DOOH Industry Leaders

JCDecaux Group

Clear Channel Outdoor Inc.

Ströer SE & Co. KGaA

Ocean Outdoor UK Ltd

Exterion Media (BVI) Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Bauer Media agreed to purchase Clear Channel Europe for USD 625 million, adding 110,000 OOH sites and boosting combined reach to 350 million consumers.

- October 2024: JCDecaux exited its planned EUR 60 million acquisition of Clear Channel Spain after prolonged antitrust review.

- October 2024: JCDecaux Sweden clinched two Greater Stockholm contracts covering 1,500 bus shelters and 14 subway hubs with programmatic-ready screens.

- August 2024: Global Media & Entertainment bought Hillenaar Outdoor’s 66-screen Dutch motorway network, reinforcing Dutch national coverage.

Europe OOH And DOOH Market Report Scope

Out-of-home (OOH) advertising refers to promotions encountered beyond the confines of one's residence. This encompasses billboards, wallscapes, and posters that catch the eye of passersby. Additionally, it encompasses place-based media visible in locales like convenience stores, medical centers, and salons. DOOH advertising, tailored for commercial objectives, predominantly finds its place in public settings, often leveraging screens and interactive digital tools.

The European OOH and DOOH market is segmented by type (static (traditional) OOH and digital OOH (LED screens)), application (billboard, transportation(transit), street furniture, and other place-based media), end-user industry (automotive, retail and consumer goods, healthcare, BFSI, and other end-user industries), and country (United Kingdom, France, Germany, and Italy). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Static (Traditional) OOH | |

| Digital OOH (LED Screens) | Programmatic OOH |

| Others |

| Billboard | |

| Transportation (Transit) | Airports |

| Others (Buses, etc.) | |

| Street Furniture | |

| Other Place-based Media |

| Automotive |

| Retail and Consumer Goods |

| Healthcare |

| BFSI |

| Other End Users |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Netherlands |

| Rest of Europe |

| By Type | Static (Traditional) OOH | |

| Digital OOH (LED Screens) | Programmatic OOH | |

| Others | ||

| By Application | Billboard | |

| Transportation (Transit) | Airports | |

| Others (Buses, etc.) | ||

| Street Furniture | ||

| Other Place-based Media | ||

| By End User | Automotive | |

| Retail and Consumer Goods | ||

| Healthcare | ||

| BFSI | ||

| Other End Users | ||

| By Country | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How large is the Europe OOH and DOOH market in 2026?

The market stands at USD 11.03 billion in 2026 with a forecast to reach USD 13.57 billion by 2031.

What is driving the fastest growth within OOH formats?

Programmatic DOOH is growing the quickest at a 6.12% CAGR thanks to measurable, data-driven buying.

Which country posts the strongest growth outlook?

The United Kingdom leads with a projected 5.18% CAGR through 2031 as digital screens make up two-thirds of national spend.

Which advertiser vertical is expanding fastest?

Healthcare campaigns show a 5.21% CAGR as pharmaceutical and wellness brands leverage privacy-compliant contextual targeting.

How are smart-city projects influencing inventory?

Cities add interactive street furniture that blends transit data, sensors, and ad spots, creating long-term concessions and new revenue.

Page last updated on: