Russia OOH And DOOH Market Size and Share

Market Overview

| Study Period | 2015 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

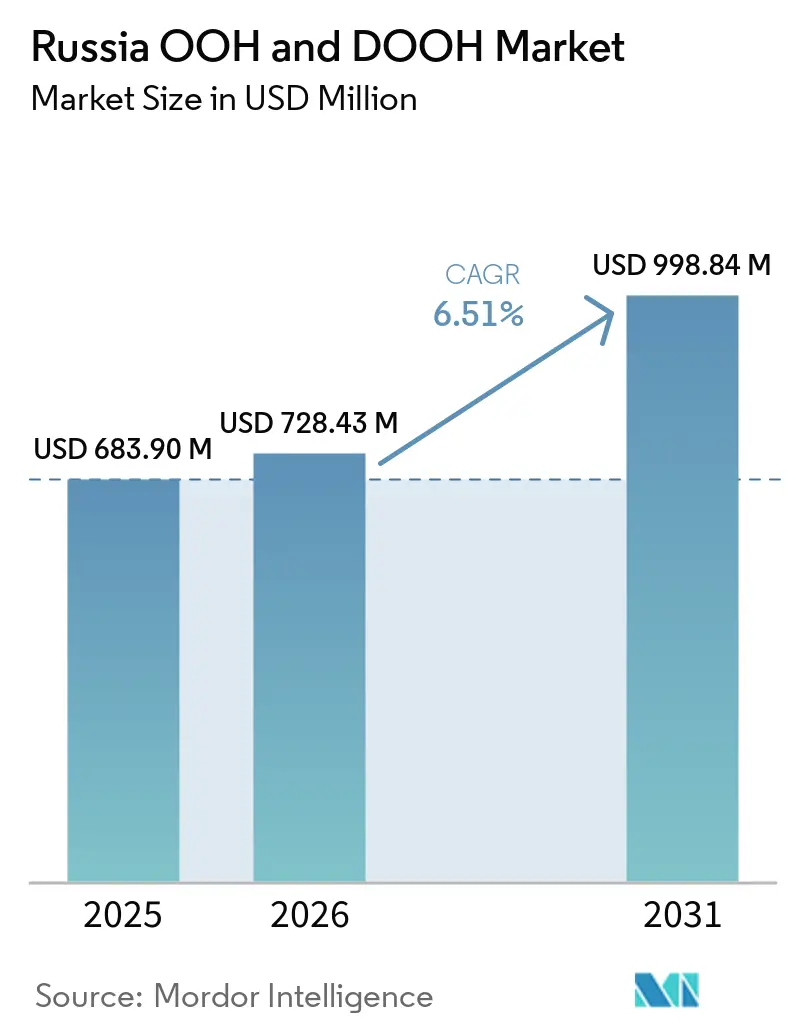

| Base Year Market Size (2025) | USD 683.90 Million |

| Market Size (2026) | USD 728.43 Million |

| Market Size (2031) | USD 998.84 Million |

| Growth Rate (2026 - 2031) | 6.51% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia OOH And DOOH Market Analysis by Mordor Intelligence

The Russian OOH and DOOH market size was valued at USD 683.90 million in 2025 and estimated to grow from USD 728.43 million in 2026 to reach USD 998.84 million by 2031, at a CAGR of 6.51% during the forecast period (2026-2031). Growth momentum is driven by three interconnected forces: rapid digitization of static inventory, aggressive rollout of 5G-enabled programmatic trading, and renewed capital spending on premium airport concessions. Digital out-of-home (DOOH) remains the standout, advancing at 11.4% annually, yet static formats still command 60% of total spend because of their cost advantage in tier-2 and tier-3 cities. Government-backed initiatives such as “Safe Highways” and Moscow’s Smart City program are unlocking new digital street furniture and LED gantry inventory, while amended advertising regulations that tighten content controls for “foreign agents” are tilting demand toward domestic media owners. At the same time, currency volatility is complicating CPM budgeting for multinational advertisers, prompting flexible rate cards and risk-sharing contracts with media partners.

Key Report Takeaways

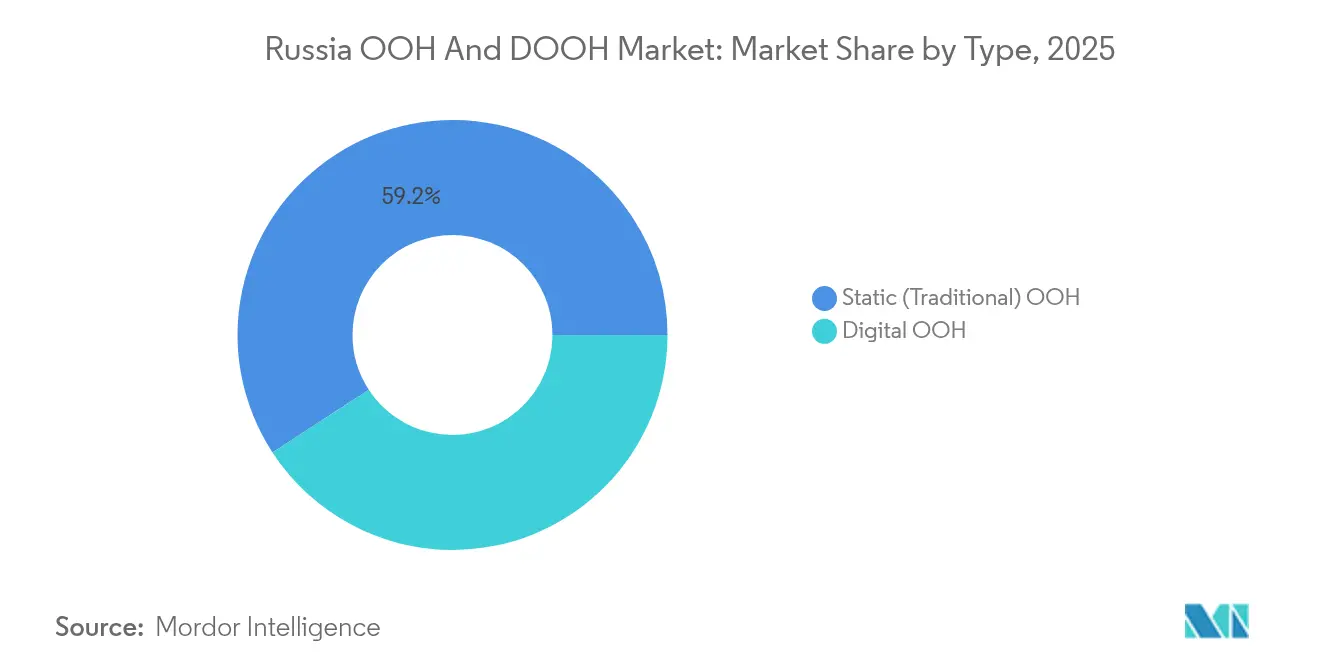

- By type, static formats led with 59.20% of the Russian OOH and DOOH market share in 2025, while DOOH is on track for an 11.18% CAGR through 2031.

- By format, billboards captured 44.60% revenue share of the Russian OOH and DOOH market size in 2025; airport advertising is set to grow fastest at 12.42% CAGR to 2031.

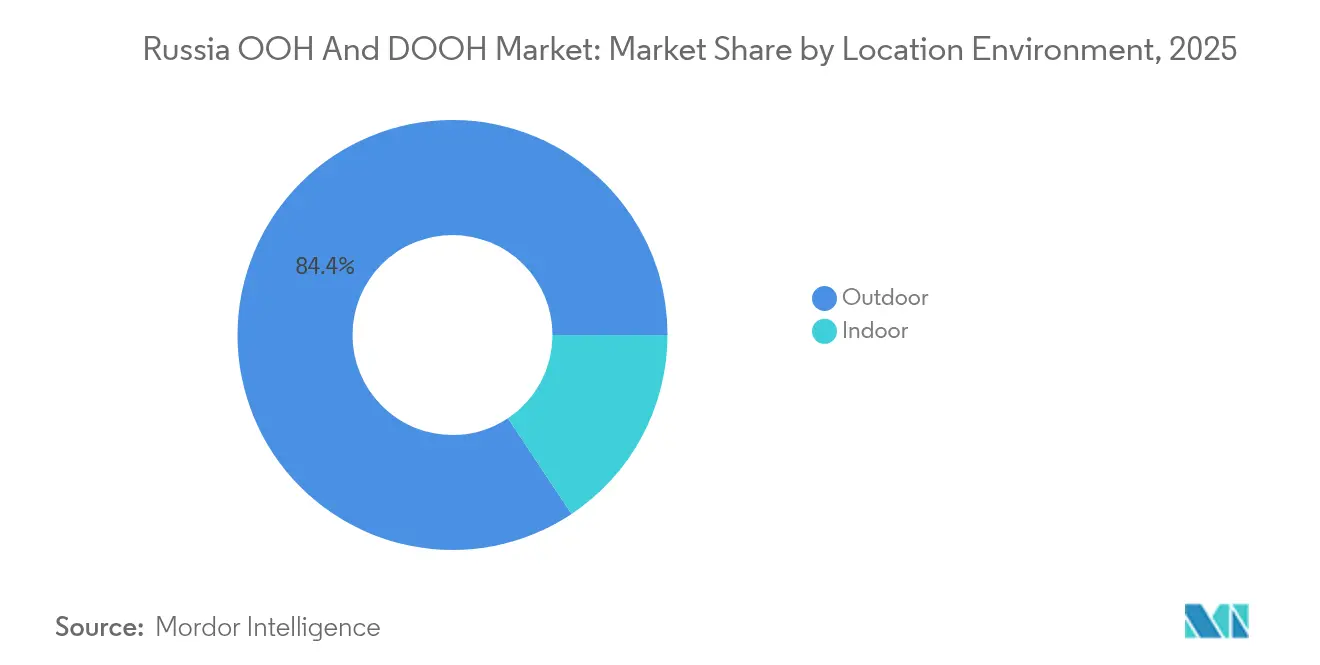

- By location environment, outdoor placements held an 84.35% share in 2025, whereas indoor venues are poised to advance at a 9.65% CAGR over the forecast period.

- By end-user, retail and consumer goods accounted for 24.70% of spending in 2025; the BFSI segment is projected to accelerate at an 8.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Russia OOH And DOOH Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smart-city roll-outs | +1.8% | Moscow, St. Petersburg, spillover to regional centers | Medium term (2-4 years) |

| Airport concession upgrades | +1.5% | Sheremetyevo, Domodedovo, other tier-1 airports | Short term (≤2 years) |

| 5G-backed programmatic trading | +1.2% | Major urban zones with 5G coverage | Medium term (2-4 years) |

| Retail chain expansion into tier-2 cities | +0.9% | Nationwide tier-2 urban clusters | Medium term (2-4 years) |

| “Safe Highways” LED gantry installations | +0.8% | Federal intercity corridors | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Smart-city roll-outs catalyzing digital street furniture uptake

Moscow’s Smart City roadmap earmarks large-scale deployment of interactive bus pavilions, sensor-equipped information boards, and augmented reality wayfinding pillars that double as advertising inventory. Media owners exploit these public-private assets to deliver weather-adaptive or traffic-triggered creatives, producing 37% higher engagement and 42-second longer dwell times versus static panels. Capital-intensive upgrades are co-financed through multi-year concession contracts, aligning municipal service improvements with incremental advertising revenue.

Airport concession upgrades enabling high-ROI DOOH networks

Sheremetyevo and Domodedovo completed terminal refurbishments that include full-motion LED walls, holographic portals, and programmatic selling pipes. Brands leverage these premium positions to capture affluent business travelers, achieving conversion rates that exceed other OOH environments according to operator case studies. Performance accountability and high CPMs help offset lower passenger throughput caused by route rationalizations.

5G-backed programmatic trading accelerating real-time audience targeting

Nationwide 5G coverage now supports millisecond bidding and edge-based creative swaps. Computer-vision sensors feed anonymized audience counts directly into demand-side platforms, delivering a 64% uplift in targeting accuracy and shortening campaign setup cycles by 28%. AI frameworks such as SOMONITOR enrich this loop with competitive content intelligence, further driving spend re-allocation from static to dynamic panels.

Retail chain expansion into tier-2 cities boosting static poster demand

Hypermarket operators extending their footprint beyond Moscow and St. Petersburg rely on localized billboards to drive grand-opening traffic. Sberbank’s “Neighborhoods” pilot underscored the strategy’s potency, generating ninefold higher responses and tripling new customer sign-ups when creatives were geotailored to residential catchments. Traditional posters remain favored in these markets because digital infrastructure is less mature and printing costs are low.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency volatility | -1.2% | National, heavier for import-dependent campaigns | Short term (≤2 years) |

| Municipal permit moratoriums | -1.0% | Historic districts in Moscow & St. Petersburg | Long term (≥4 years) |

| Lack of unified DOOH audit | -0.7% | Nationwide, affects DOOH bookings | Medium term (2-4 years) |

| Rising energy tariffs | -0.6% | Regions with elevated power costs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Currency-linked media-buying volatility raising CPM uncertainty

A widening ruble-to-dollar band inflates CPM calculations for foreign brands that book budgets in hard currency but settle in local tender. Resulting rate clauses can swing campaign cost by double digits mid-flight, reducing appetite for long-term commitments. Agencies are adopting indexation models and shorter insertion orders to hedge risk.

Municipal permit moratoriums in historic centers limiting new installations

Strict preservation codes cap new large-format builds in downtown Moscow and St. Petersburg. Scarcity lifts rental costs for existing inventory and shifts capital toward digital retrofits of legally grandfathered sites. Media companies diversify into street furniture and transit hubs where approval barriers are lower.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Digital acceleration amid static dominance

The Russian OOH and DOOH market size for static formats represented 59.20% of total spend in 2025. Budget-constrained local advertisers favor these proven assets, especially near retail openings in tier-2 municipalities. Nevertheless, DOOH is scaling at 11.18% CAGR and is forecast to absorb a growing slice of the Russian OOH and DOOH market by 2031 as programmatic pipes mature. In this migration, sensor arrays and AI-driven scheduling ensure smarter audience delivery than static posters can achieve.

Cost-to-benefit parity is inching closer because LED panel prices have fallen and energy efficiency has improved. Brands also value real-time content swaps, which static infrastructure cannot support. While rollout pace remains highest in Moscow and other tier-1 agglomerations, provincial operators are piloting solar-powered digital kiosks to offset grid cost escalation.

By Format: Billboards hold sway while airports surge

Traditional roadside billboards retained a 44.60% Russian OOH and DOOH market share in 2025, thanks to entrenched locations on arterial roads and suburban ring-roads. Upgrades to high-resolution LED are injecting dynamic capability without losing the footprint advantage. Airport DOOH, representing 8.35% of 2025 spend, is on course to log a 12.42% CAGR - outpacing any other sub-segment and lifting its contribution to the Russian OOH and DOOH market size through 2031.

Airports deliver affluent, time-rich travelers, and newly overhauled terminals like Sheremetyevo’s Terminal C now support holographic showcases that command premium CPMs. Beyond air hubs, rail stations, and metro concourses, scrolling LED and large-format LCD tunnels are being integrated, broadening transit media diversity and enabling omnichannel flighting.

By Location Environment: Outdoor dominance, indoor momentum

Outdoor installations accounted for 84.35% of 2025 spending, fortified by the “Safe Highways” gantry program and flourishing roadside inventory. Yet indoor placements in malls, airports, and convention venues are projected to compound at 9.65% annually, elevating their slice of the Russian OOH and DOOH market by the end of the decade. Prolonged dwell times and climate-controlled settings make these venues ideal for immersive activations and interactive screens.

Sophisticated audience analytics, such as foot-traffic heat-maps, guide media planners toward high-value concourses. New smart-bus pavilions in Moscow blend shelter functionality with climate control, blurring the delineation between indoor and outdoor while opening up hybrid creative.

By End-User: Retail scale, BFSI velocity

Retail and consumer goods groups consumed 24.70% of the 2025 spend, using geographically targeted billboards to funnel shoppers into physical outlets. Their consistent volumes solidify base demand across urban tiers. The BFSI cohort, however, is registering an 8.62% CAGR - fastest among all verticals - and is gradually enlarging its share of the Russian OOH and DOOH market. Campaigns like Sberbank’s geo-customized panels illustrate how data-driven creatives can triple lead generation and remodel brand perception.

Automotive, telecom, and entertainment advertisers continue to utilize full-motion billboards for product launches, while healthcare brands lean on proximity-based displays around pharmacies. Cross-screen retargeting, enabled by device-ID matching, is further enticing new verticals to allocate a higher slice of omnichannel budgets to OOH.

Geography Analysis

Moscow and St. Petersburg controlled more than 59% of the Russian OOH and DOOH market in 2025 as their dense commuter flows and rich digital infrastructure enabled premium pricing. Smart City investments in the capital city alone are spawning interactive street furniture corridors that offer advertisers granular day-part targeting and QR-enabled engagement options. Permit constraints in St. Petersburg incentivize media owners to retrofit existing structures with high-definition LED rather than erect new footprints, sustaining a seller-favored inventory dynamic.

Tier-2 conurbations such as Kazan, Yekaterinburg, and Novosibirsk are the fastest-growing pockets of demand. Retail chains expanding into these locales rely heavily on static billboards and posters adjacent to hypermarket entrances, fueling localized spend and gradually expanding the Russian OOH and DOOH market beyond the two prime cities. Municipal authorities in cities with populations above 300,000 are rolling out intelligent transport systems with federal subsidies, installing new digital boards along bus corridors and at arterial intersections.

Federal highways that interlink major metros are transforming into high-impact OOH corridors, courtesy of the “Safe Highways” investment pool. LED gantries deliver dual safety messages and paid advertising, unlocking a novel canvas for automotive, logistics, and insurance brands targeting intercity travelers. Over the forecast horizon, digital saturation is expected to permeate secondary highways, gradually narrowing the urban–rural inventory quality gap.

Competitive Landscape

Russia’s OOH arena is moderately fragmented, with domestic stalwart Russ Outdoor, international specialists such as JCDecaux, and diversified conglomerates like Gazprom-Media vying for contracts. April 2025 saw e-commerce giant Wildberries finalize its acquisition of Russ Group, combining online shopper data with nationwide billboard assets to craft closed-loop attribution models.[2]bne IntelliNews, “Wildberries-Russ Outdoor Deal Closes,” bne.eu JCDecaux, for its part, installed 50 premium screens at Moscow intersections in March 2025, bolstering its programmatic supply and underscoring a 28.3% global DOOH revenue surge in H1 2024. [3]JCDecaux, “H1 2024 Results,” jcdecaux.com

Domestic policy continues to reshape the rivalry. Decree No. 1875, enacted in December 2024, bars foreign vendors from state-funded advertising tenders, inherently favoring local incumbents. Gazprom-Media OOH used the window to roll out an AI-based audience measurement layer across its digital billboard estate, claiming real-time demographic detection accuracy above 90%.[4]Gazprom-Media, “AI-Driven Audience Measurement Launch,” gazprom-media.com Smaller regional outfits like SetlCity Media and Vera-Olimp secure relevance through entrenched municipal relationships and niche regional portfolios.

Technology is the primary arms race. Media owners that combine automated bidding rails, third-party verification, and dynamic creative optimization win disproportionate share of wallet from data-hungry advertisers. Conversely, operators reliant on legacy static fleets face tightening margins amid climbing electricity tariffs and stricter content regulations.

Russia OOH And DOOH Industry Leaders

Russ Outdoor

Prime Group

JCDecaux Russia

Gallery

SetlCity Media

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Wildberries completed the acquisition of Russ Group, forging Russia’s largest integrated retail media network.

- April 2025: JCDecaux added 50 premium digital screens at high-traffic Moscow crossings, enhancing programmatic reach.

- February 2025: Sheremetyevo International Airport launched a holographic advertising platform in Terminal D, opening immersive 3D opportunities.

- December 2024: Russian government issued Decree No. 1875, banning foreign entities from state and municipal advertising contracts.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Russian out-of-home advertising market as every paid communication that appears on static or digital media faces visible in public spaces, including billboards, street furniture, transit shelters, airports, shopping malls, and place-based screens. Spend tied to in-store retail media, cinema, or personal mobile devices stays outside this lens.

Scope Exclusion: Indoor retail digital signage that is owned and sold by retailers for on-premise promotion is excluded.

Segmentation Overview

- By Type

- Static (Traditional) OOH

- Digital OOH (LED Screens)

- Programmatic OOH

- Other Digital Formats

- By Format

- Billboards

- Transportation (Transit)

- Airports

- Other Transit (Bus, Rail, Taxi)

- Street Furniture

- Place-Based Media

- By Location Environment

- Outdoor

- Indoor

- By End-User Industry

- Retail and Consumer Goods

- Automotive

- BFSI

- Healthcare and Pharma

- Other Industries

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview media owners, buying-unit leads at agencies, municipal tender officials, and ad-tech vendors across Moscow, Saint Petersburg, Novosibirsk, and Kazan. Conversations verify inventory digitalization rates, average selling prices, and post-sanction demand shifts, filling the gaps left by public data.

Desk Research

We start with publicly available cornerstones such as Rosstat outdoor ad revenue filings, Federal Antimonopoly Service contract bulletins, and customs import codes for LED modules. Trade bodies like the Association of Communication Agencies of Russia, UITP transit statistics, and airport concession disclosures supply placement counts, while peer-reviewed journals on programmatic DOOH adoption add behavioral context. Company 10-Ks and investor decks complement these threads. Paid feeds from D&B Hoovers and Dow Jones Factiva help us benchmark operator revenues and flag one-off events. This list illustrates our source mix and is not exhaustive.

Market-Sizing & Forecasting

A top-down reconstruction begins with gross media spend reported by Rosstat, which is then split by OOH share and digital share using audited operator disclosures. Select bottom-up checks, sampled screen counts multiplied by typical sell-out ratios, calibrate totals. Key variables in our model include the digital conversion pace of static faces, the ruble-to-USD exchange path, airport passenger flows, urban GDP growth, regulatory quota changes, and seasonality of national campaigns. Forecasts rely on multivariate regression that links spend to GDP, retail turnover, and passenger kilometers. Scenario analysis captures sanction risk. Where operator data are missing, we bridge gaps with averaged ASPs sourced during interviews.

Data Validation & Update Cycle

Outputs pass variance tests against historical spend, inter-modal advertising ratios, and peer signals. Senior reviewers examine anomalies before sign-off. Reports refresh each year, with interim tweaks when policy shifts or large mergers, like the 2025 Wildberries-Russ deal, materially alter baselines.

Why Our Russia OOH And DOOH Baseline Commands Reliability

Published estimates rarely align because firms pick different media formats, coverage cities, deflator methods, and refresh cadences.

Key gap drivers include whether indoor retail screens are folded in, how quickly digital faces are assumed to replace static panels, the ruble conversion month chosen, and if war-related ad bans are baked into 2025 forecasts. Mordor Intelligence reports only outdoor screens sold on an open market, applies real 2024 exchange averages, and updates after every material decree, while others sometimes project once every three years or pool indoor networks.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 642.84 M (2024) | Mordor Intelligence | - |

| USD 621.80 M (2025) | Global Consultancy A | Includes certain indoor retail networks and assumes slower ruble depreciation |

| ~USD 600 M (2024) | Trade Journal B | Uses nine-month operator revenue extrapolation and omits small regional cities |

In sum, because our analysts anchor the model to audited spend, cross-check with bottom-up samples, and refresh after every policy change, decision-makers receive a balanced, transparent baseline they can trace to clear variables and repeat with confidence.

Key Questions Answered in the Report

What is the current size of the Russian OOH and DOOH market?

It is valued at USD 683.90 million in 2025 and is estimated at USD 728.43 million in 2026, and is projected to reach USD 998.84 million by 2031.

Which segment is growing fastest within the market?

Digital out-of-home (DOOH) leads growth with an 11.18% CAGR forecast for 2026-2031.

How significant are airport advertising formats?

Airports account for about 8.35% of spend and are forecast to grow at 12.42% CAGR, making them the fastest-expanding format cluster.

How do smart-city projects influence OOH advertising?

Smart-city investments in Moscow and beyond provide new digital street furniture that boosts engagement by up to 37% and lengthens dwell time.

Page last updated on: