Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

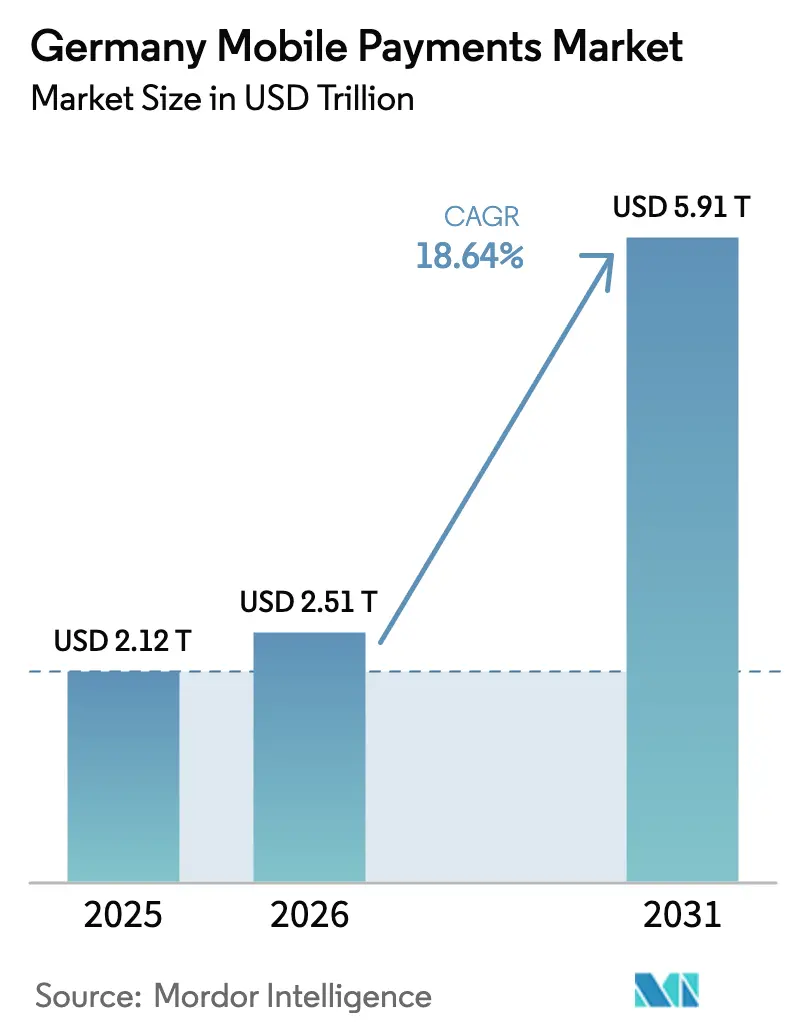

| Base Year Market Size (2025) | USD 2.12 Trillion |

| Market Size (2026) | USD 2.51 Trillion |

| Market Size (2031) | USD 5.91 Trillion |

| Growth Rate (2026 - 2031) | 18.64% CAGR |

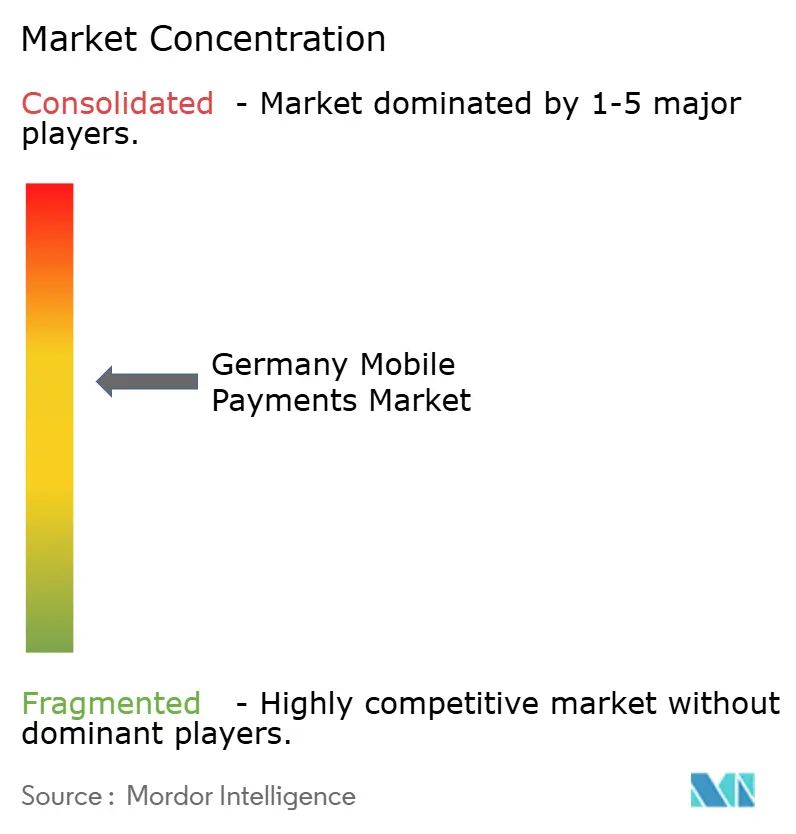

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Mobile Payments Market Analysis by Mordor Intelligence

Germany mobile payments market size in 2026 is estimated at USD 2.51 trillion, growing from 2025 value of USD 2.12 trillion with 2031 projections showing USD 5.91 trillion, growing at 18.64% CAGR over 2026-2031. Rapid infrastructure upgrades, strong regulatory momentum under PSD3 and eIDAS 2.0, and a decisive consumer shift from cash to digital channels underpin this growth.[1]European Central Bank, “Payments statistics: first half of 2024,” ecb.europa.eu Real-time settlement requirements, the nationwide retirement of Giropay, and large-scale retailer investments in contactless terminals create an environment where service reliability now outpaces mere acceptance as the primary competitive differentiator. Intensifying collaboration between banks and fintechs, coupled with record venture financing for payment start-ups, accelerates product innovation despite margin pressure from interchange-fee caps.[2]Global Payments Inc., “Global Payments and Commerzbank Announce Joint Venture in Germany,” investors.globalpayments.com Cybersecurity, demographic resistance among older users, and dependence on US mobile-OS ecosystems temper the upside, yet overall momentum positions Germany as a core test bed for European payment sovereignty initiatives.3Bundeskriminalamt, “Cybercrime,” bka.de

Key Report Takeaways

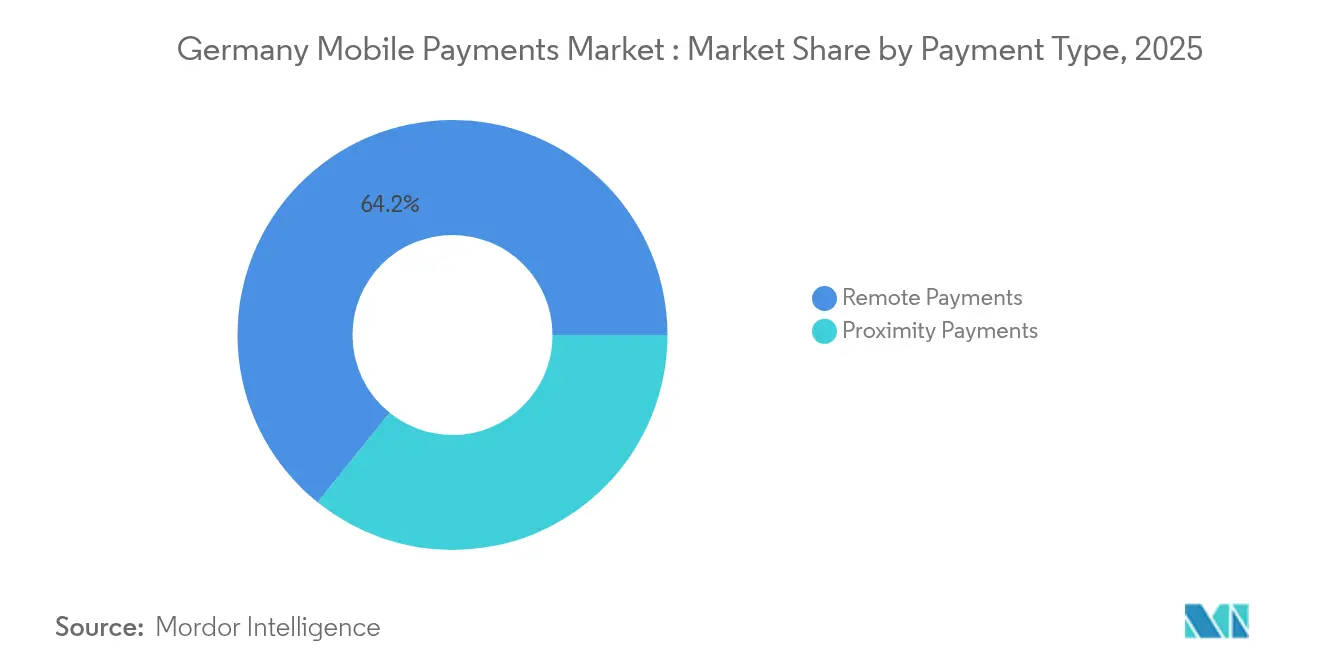

- By payment type, remote payments led with 64.20% of Germany mobile payments market share in 2025; proximity payments are projected to expand at a 20.5% CAGR through 2031.

- By transaction type, point-of-sale transactions accounted for 45.40% of Germany mobile payments market size in 2025, while other transaction categories are forecast to grow at 22.6% CAGR to 2031.

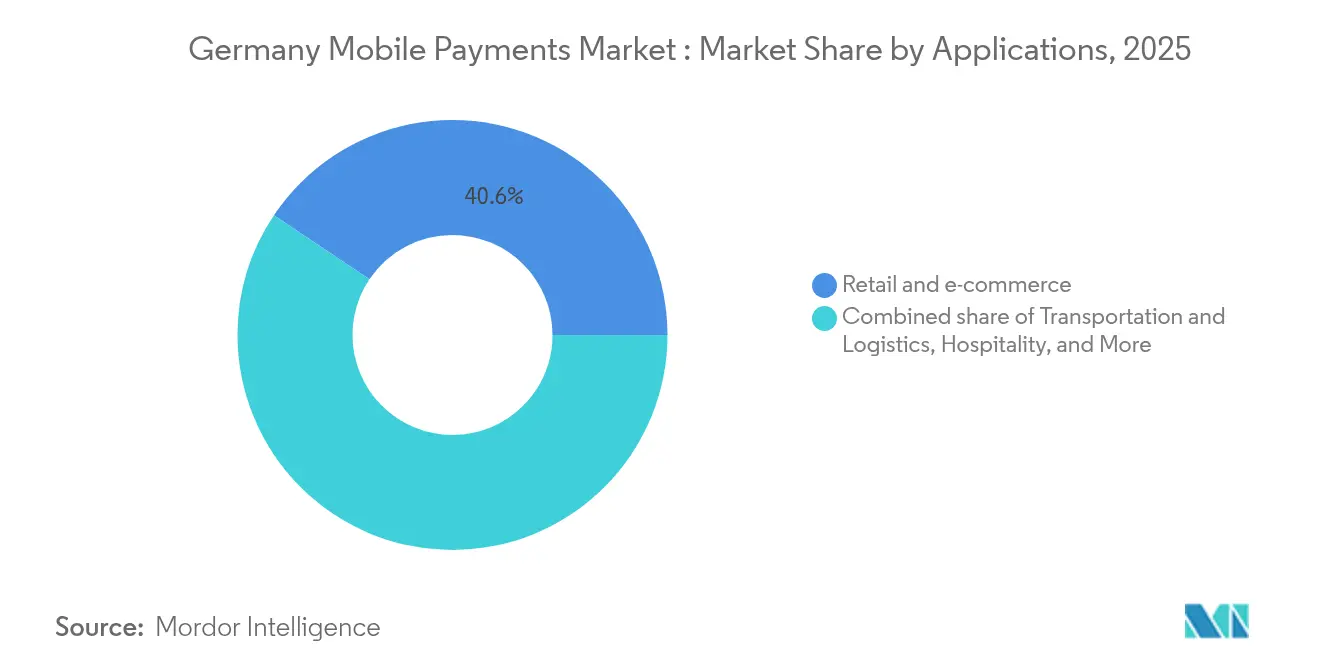

- By application, retail & e-commerce held 40.60% share of the Germany mobile payments market in 2025; transportation & logistics is advancing at a 23.9% CAGR between 2026-2031.

- By end-user, personal users commanded 87.30% of the Germany mobile payments market in 2025, whereas business adoption is rising at a 19.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Mobile Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in contactless POS infrastructure penetration | +4.2% | National, concentrated in urban centers | Medium term (2-4 years) |

| E-commerce expansion among SMEs adopting mobile checkout | +3.8% | National, stronger in Bavaria and North Rhine-Westphalia | Short term (≤ 2 years) |

| Real-time TIPS integration into mobile wallets | +3.1% | EU-wide, early adoption in Germany | Medium term (2-4 years) |

| Digital ID & eIDAS 2.0 wallet enabling frictionless KYC | +2.9% | EU-wide, pilot programs in Germany | Long term (≥ 4 years) |

| Retailer-led closed-loop wallets (e.g., Lidl Pay) | +2.3% | National, retail-concentrated regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Contactless POS Infrastructure Penetration

Nationwide terminal density has reached a point where availability no longer restricts proximity payments. Contactless card transactions rose 13.2% year-on-year during H1 2024, with Germany contributing a notable share of the 25.8 billion payments recorded. Retailers such as REWE use computer-vision formats that combine cashierless checkout with mobile apps, shifting competition toward user-experience optimisation.[4]Retail Technology Innovation Hub, “GenAI, computer vision, and new commerce platforms,” retailtechinnovationhub.com Sparkasse’s Alipay+ integration illustrates how established banks leverage upgraded terminals to capture cross-border flows during large events. Greater confidence in contactless reliability speeds merchant onboarding, strengthening the Germany mobile payments market.

E-commerce Expansion Among SMEs Adopting Mobile Checkout

SMEs account for 99% of German businesses and are central to domestic commerce digitisation. Government “go-digital” subsidies lower adoption barriers, allowing providers such as Stripe and Commerz Globalpay to package mobile checkout with value-added analytics for smaller merchants. Partnerships between incumbent banks and fintechs—exemplified by Commerzbank’s digital card launch—target cost reduction and working-capital optimisation for merchants with limited IT resources. The Germany mobile payments market therefore captures incremental volumes from previously cash-centric micro-merchants.

Real-time TIPS Integration into Mobile Wallets

Mandatory instant euro transfers within 10 seconds make speed and cost permanent differentiators. Wero’s multi-country wallet builds on TIPS rails to challenge US rivals, attracting early adopters among Germany’s digitally active consumers. Deutsche Bundesbank surveys show 80% of residents already have access to instant transfers, validating technical readiness for wallet integration. As execution risk on latency falls, competitive focus turns toward loyalty, budgeting tools, and embedded lending inside wallets.

Digital ID & eIDAS 2.0 Wallet Enabling Frictionless KYC

EU digital-identity pilots allow credential sharing across public and private services. Germany’s 2025 Coalition Agreement endorses EUDI-wallet usage for opening bank accounts and confirming payment authorisation. BaFin’s revised AML rules heighten onboarding diligence, positioning digital IDs as cost-saving compliance utilities. Frictionless KYC reduces abandonment rates during wallet sign-up, raising active-user conversion in the Germany mobile payments market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Security & privacy concerns under PSD3 | -2.8% | EU-wide, heightened in Germany | Short term (≤ 2 years) |

| Interchange-fee caps squeezing provider margins | -2.1% | EU-wide, affecting German operations | Medium term (2-4 years) |

| Ageing demographic's slower adoption | -1.7% | National, rural areas more affected | Long term (≥ 4 years) |

| Dependence on US mobile-OS vendors | -1.4% | National, strategic concern | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Security & Privacy Concerns Under PSD3

Stronger authentication rules add friction if poorly implemented. Emerging social-engineering attacks generate consumer anxiety, especially while reimbursement frameworks remain patchy. Bundeskriminalamt highlights increased malware and phishing aimed at mobile devices, prompting providers to add biometric safeguards that can extend checkout times. Adoption may slow among older consumers who already prefer cash, though sustained education campaigns could soften the impact on the Germany mobile payments market.

Interchange-fee Caps Squeezing Provider Margins

Fee ceilings reduce merchant costs but compress revenue for non-bank payment intermediaries. Ecommerce Europe urges reopening the Interchange Fee Regulation to cover network fees as well as interchange, a move that could further erode provider economics. Smaller fintechs with limited scale may exit unprofitable segments or pursue consolidation, potentially limiting service diversity for merchants in the Germany mobile payments industry

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Payment Type: Remote Dominance Faces Proximity Surge

Remote payments held 64.20% of Germany mobile payments market share in 2025, driven by entrenched e-commerce behaviour and strong digital banking penetration. Proximity transactions are catching up quickly, expanding at 20.5% CAGR as merchants deploy NFC-enabled terminals nationwide. Younger cohorts champion tap-to-pay convenience, while older groups still favour remote channels for online shopping. Contactless reliability, QR-code acceptance, and patent-led innovations that enable low-battery NFC transactions together stimulate proximity uptake. Domestic players integrate reward schemes into in-store apps, while global wallets leverage OS-level enrolment to scale at minimal marginal cost. The dual-track growth amplifies total Germany mobile payments market capacity rather than cannibalising existing remote volumes.

Proximity momentum is also reinforced by mandatory instant settlement, which reduces perceived risk for merchants accepting high-ticket face-to-face payments. Retailers bundle digital-receipt issuance and buy-now-pay-later options at POS, further enhancing perceived value. For remote channels, marketplace platforms focus on stored-credential optimisation and chargeback mitigation to maintain customer trust. Both modalities converge on a unified customer-identity layer, anchored by the eIDAS 2.0 wallet, that could blur distinctions over the long run within the Germany mobile payments market.

By Transaction Type: POS Leadership Amid Diversification

In-store point-of-sale retained 45.40% of Germany mobile payments market size in 2025, underscoring the resilience of physical retail. However, non-POS categories—peer-to-peer, subscription, and embedded-finance flows—are forecast to grow 22.6% CAGR as consumers adopt super-apps that package transfers, loyalty, and micro-investing. Real-time payments infrastructure incentivises billers and utilities to embed instant pay-by-link options, displacing legacy direct-debit norms. The rise of “invisible checkout” in quick-service formats further expands POS definitions to include sensor-based walk-out payments.

Financial-super-app roadmaps from N26 and Revolut target a broader service footprint, integrating salary advances and budgeting. This proliferation increases competitive intensity in adjacent verticals such as insurance and small-ticket credit, thereby enlarging the transaction universe for the Germany mobile payments market. Legacy acquirers respond by exposing API gateways that allow partners to initiate payments straight from bank accounts, avoiding card interchange entirely.

By Application: Transportation Logistics Acceleration

Retail and e-commerce contributed 40.60% of Germany mobile payments market in 2025, reflecting the sector’s mature web-shop ecosystem. Transportation and logistics now leads growth at 23.9% CAGR, catalysed by Deutsche Bahn’s Germany-Ticket, which onboards 11.2 million monthly riders into stored-value subscription models. Public-transport operators integrate real-time fraud screening and open-banking verification for pass renewal, broadening use cases. Logistics giants like DSV allocate USD 15.6 billion (EUR 14.3 billion) to acquisitions that enable cross-border invoice automation, raising B2B payment volumes. Hospitality, food service, and government services follow, benefiting from pandemic-era hygiene priorities and digital-ID pilots for administrative fees.

Clustered urban programmes—such as “Mobility as a Service” platforms that combine ticketing with bike-share credits—drive integrated checkout adoption. Embedded insurance for parcel delivery and on-demand warehousing create additional payment events. These synergies expand overall Germany mobile payments market size across consumer and enterprise spending streams.

By End-user: Business Segment Momentum

Personal users represented 87.30% of Germany mobile payments market in 2025, reflecting transaction-volume dominance from consumer-to-merchant and P2P flows. Business usage is growing 19.8% CAGR as SMEs embrace digital credit cards, softPOS, and embedded-finance invoicing. Corporates seek reconciliation efficiency, liquidity visibility, and real-time settlement to mitigate late-payment exposure revealed by Atradius surveys. Fintech-bank joint ventures deploy cloud-based POS platforms that bundle accounting integrations, accelerating B2B enrolment.

Corporates also adopt mobile wallets for employee travel spend and micro-purchases, reducing petty-cash management overhead. Supply-chain participants leverage tokenised payments for freight insurance disbursements and customs guarantees. These enterprise-grade use cases diversify revenue in the Germany mobile payments industry beyond purely consumer channels.

Geography Analysis

Germany remains the nucleus of the broader European transformation, with 83.8 million inhabitants and the continent’s third-largest e-commerce base delivering constant transaction throughput. Bavaria and North Rhine-Westphalia outperform national averages on SME mobile-checkout adoption, supported by local incubators and high terminal penetration. Urban centres like Berlin act as talent magnets for fintech venture capital, funnelling USD 1.1 billion in funding during 2024 that seeded payment-specific start-ups. Rural regions lag on fibre connectivity and older-age tech acceptance, impeding uniform proximity payment growth; yet government broadband targets aim to narrow this gap within three years.

European Union directives unify technical and compliance standards, allowing German providers to scale regionally with minimal localisation costs. The Instant Payments Regulation imposes a common service baseline across member states, positioning home-grown platforms to compete for cross-border merchant contracts. Germany’s heavy cross-border e-commerce volumes further pressure providers to optimise multi-currency and multi-lingual checkout experiences. The launch of Wero across Germany, France, and Belgium showcases coordinated efforts to build European payment sovereignty, potentially reducing dependency on US wallet ecosystems over time.

External geopolitical tensions highlight strategic vulnerabilities in relying on foreign mobile-OS vendors. Policymakers emphasise digital-euro readiness and secure element access to safeguard domestic transaction data. Overall, geography-driven policy harmonisation and funding flows collectively enlarge Germany mobile payments market potential while raising the bar for compliance agility.

Competitive Landscape

The Germany mobile payments market features a three-tier rivalry among incumbent banks, US tech giants, and European fintech challengers. Banks such as Deutsche Bank and Commerzbank leverage existing deposit relationships, embedding white-label payment processors like Fiserv or Global Payments to accelerate go-to-market for SME offerings. These incumbents retain regulatory credibility and customer trust but must modernise legacy IT to match fintech speed.

Apple, Google, and Samsung harness operating-system integration to secure default wallet positions, yet depend on local issuers for tokenisation and KYC. Their dominance in device ecosystems anchors significant proximity transaction volume, compelling regulators to monitor competitive fairness. European fintechs—Klarna, N26, Revolut—apply asset-light models to scale quickly, adding credit, investing, and budgeting to lock in users. Payment processors such as Adyen, Stripe, and Worldline compete on API flexibility, fraud analytics, and multi-rail routing that minimises interchange cost.

Patent filings in energy-efficient NFC and barcode-based payments signal continuous hardware-software co-innovation aimed at reliability under adverse device conditions. Competitive advantage increasingly resides in ecosystem design that fuses payments with loyalty, identity, and data analytics. Partnerships, rather than outright rivalry, dominate strategic agendas because banks need fintech agility while fintechs require balance-sheet support and licencing breadth. Consequently, the Germany mobile payments market leans toward coopetition, where mutual value creation overrides zero-sum positioning.

Germany Mobile Payments Industry Leaders

Google LLC

Apple Pay

PayPal Holdings, Inc.

Samsung Electronics Co. Ltd

Visa Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: BaFin issued a consultation on safekeeping standards for crypto-asset fund managers, signalling stricter oversight of digital-payment custodians and prompting providers to reassess key-management strategies.

- January 2025: The European Central Bank’s instant-payment mandate took effect, forcing all credit institutions to settle euro transfers in 10 seconds at zero extra cost and reshaping provider pricing structures.

- November 2024: German savings, cooperative, and commercial banks confirmed Wero integration for 2025, unifying 14 million users across three countries and amplifying regional scale economies.

- October 2024: DSV raised EUR 10 billion (USD 10.9 billion) to close its EUR 14.3 billion (USD 15.6 billion) Schenker acquisition, integrating 160,000 staff and upgrading payment platforms to support higher freight volumes.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the German mobile payments market as every transaction that is initiated, authorized, and completed through a mobile device, smartphone, tablet, or wearable, using proximity technologies (NFC, QR) or remote channels (in-app, browser-based) for domestic goods, services, or peer transfers. Values are expressed in U.S. dollars at merchant face value, inclusive of wallet funding charges and payment processor fees where applicable.

Scope exclusion: desktop-originated online payments and international remittances routed outside Germany lie beyond this analysis.

Segmentation Overview

- By Payment Type

- Proximity Payments

- Remote Payments

- By Transaction Type

- Peer-to-Peer (P2P)

- In-store Point-of-Sale (POS)

- Person-to-Merchant (P2M/Checkout)

- Other Transaction Types

- By Application

- Retail and eCommerce

- Transportation and Logistics

- Hospitality and Food-Service

- Government and Public Sector

- Other Applications (Education, Healthcare)

- By End-user

- Personal

- Business

Detailed Research Methodology and Data Validation

Primary Research

In-depth conversations with acquiring banks, wallet providers, and multi-location retailers across Bavaria, NRW, and Berlin helped validate contactless transaction growth, average ticket sizes, and merchant discount rates. Targeted consumer pulse surveys further clarified frequency splits between P2P, in-store tap, and in-app checkout, letting us fine-tune usage coefficients.

Desk Research

Analysts began with macro foundations from the Deutsche Bundesbank's payments statistics, Eurostat's ICT usage surveys, and the Federal Network Agency's telecom reports, which map smartphones, broadband, and POS terminal proliferation. Supplemental context came from the German Retail Federation, European Payments Council guidelines, patent analytics via Questel, and listed payment service providers' 10-K filings. News aggregation through Dow Jones Factiva kept the team updated on regulatory moves such as PSD 3 drafts. This list is illustrative; many other open datasets and filings informed the desk phase.

Market-Sizing & Forecasting

A top-down construct starts with total German non-cash payment value and reconstructs the mobile slice through smartphone penetration, active wallet rate, and incidence of contactless capable POS terminals. Resultant totals are checked against selective bottom-up approximations, sampled issuer volumes multiplied by blended ASPs, to calibrate leakages between channels. Variables that steer the model include: 4G/5G subscriber base, NFC POS installation growth, e-commerce order frequency, average mobile basket value, and regulatory caps on interchange. Multivariate regression with scenario overlays (base, accelerated wallet adoption, and regulatory drag) projects figures to 2030, while gaps in sampled bottom-up data are bridged by indexed growth factors derived from Eurostat household surveys.

Data Validation & Update Cycle

Outputs undergo variance screens versus Bundesbank quarterly data, anonymized gateway feeds, and year-end issuer disclosures. Senior analysts re-check anomalies before sign-off. Our numbers refresh each year; mid-cycle updates trigger if material events, PSD revisions, macro shocks, and wallet launches shift core drivers.

Why Mordor's Germany Mobile Payments Baseline Commands Reliability

Published estimates seldom align, because firms pick different transaction scopes, conversion bases, or refresh cadences.

Key gap drivers stem from whether cross-border volumes are blended in, the aggressiveness of wallet adoption assumptions, and the currency translation approach (constant vs. current). Mordor applies a clean domestic scope, currency adjusted constant 2024 dollars, annual refreshes, and triangulated primary validation, which collectively reduce drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.12 trn (2025) | Mordor Intelligence | - |

| USD 107.6 mn (2024) | Regional Consultancy A | Narrow focus on in-store QR code spend; excludes remote and P2P usage |

| USD 4.5 bn (2023) | Global Consultancy B | Uses merchant revenue only and omits processor and wallet fees |

| USD 84.9 bn (2024) | Industry Association C | Mixes domestic and cross-border flows, applies spot FX without inflation adjustment |

Taken together, the comparison shows that our disciplined scoping, variable selection, and annual recalibration yield a balanced, transparent baseline that decision-makers can trace back to publicly verifiable signals and repeatable steps.

Key Questions Answered in the Report

What is the current size of the Germany mobile payments market?

The market is valued at USD 2.51 trillion in 2026 and is projected to reach USD 5.91 trillion by 2031.

Which payment type leads the Germany mobile payments market?

Remote payments currently lead with 64.20% market share, although proximity payments are the fastest-growing segment at 20.5% CAGR.

How will instant payments regulation affect providers?

From 2025, all euro transfers must settle in 10 seconds at no additional fee, compelling providers to invest in real-time infrastructure and reevaluate pricing.

Why is transportation the fastest-growing application?

The success of Deutsche Bahn’s Germany-Ticket and broader mobility-as-a-service initiatives are integrating digital passes with seamless mobile payments, driving 23.9% CAGR in the segment.

What are the primary risks for the Germany mobile payments industry?

Heightened cybersecurity threats, interchange-margin compression, and slower adoption among older demographics remain key challenges.

Page last updated on: