Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 30.43 Billion |

| Market Size (2026) | USD 31.06 Billion |

| Market Size (2031) | USD 34.42 Billion |

| Growth Rate (2026 - 2031) | 2.07% CAGR |

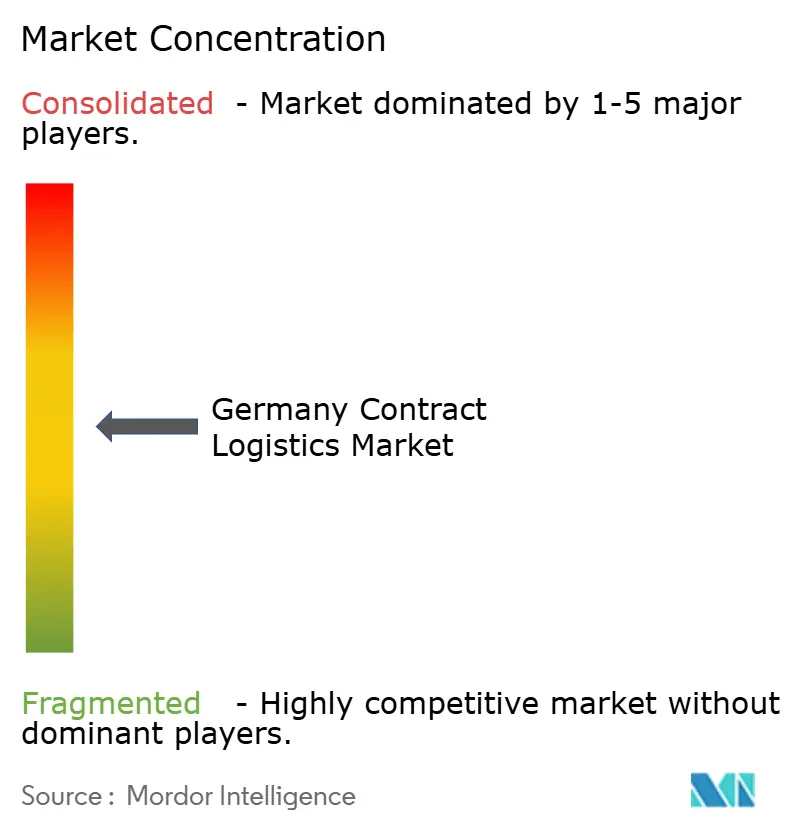

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Contract Logistics Market Analysis by Mordor Intelligence

Germany Contract Logistics Market size in 2026 is estimated at USD 31.06 billion, growing from 2025 value of USD 30.43 billion with 2031 projections showing USD 34.42 billion, growing at 2.07% CAGR over 2026-2031. Growth is underpinned by expanding e-commerce fulfilment volumes, rising complexity in inbound electric-vehicle supply chains, and heightened demand for GDP-compliant cold-chain services. The new Supply Chain Due Diligence Act is prompting manufacturers and retailers to shift logistics activities to compliant third-party providers, while warehouse automation and AI are improving productivity enough to absorb higher wage costs. At the same time, fleet decarbonisation investments and stricter real-estate economics are reshaping operating models, favoring providers with scale, technology depth, and multimodal capabilities. Competitive dynamics are evolving after DSV agreed to acquire DB Schenker, a deal that will reshape bargaining power across the German contract logistics market.

Key Report Takeaways

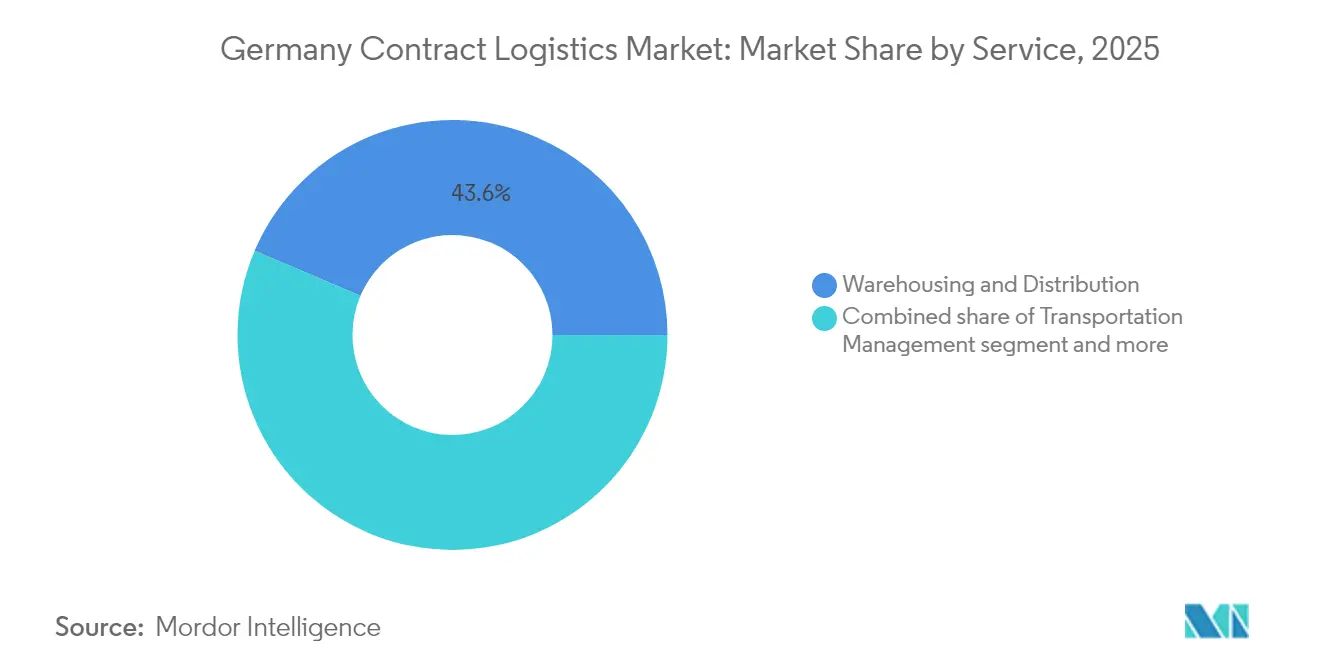

- By service, Warehousing and Distribution held 43.60% of Germany contract logistics market share in 2025. The Germany contract logistics market size for Value-Added Services is projected to compound at 3.92% CAGR between 2026-2031.

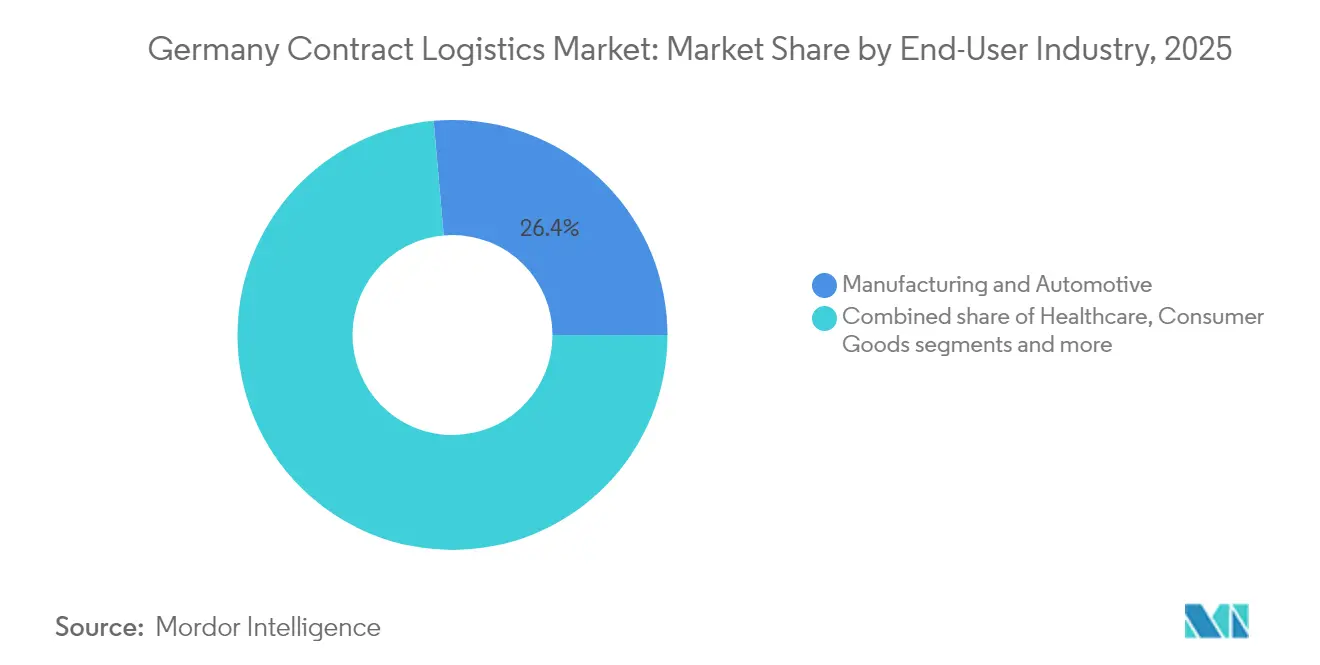

- By end-user industry, Manufacturing and Automotive accounted for 26.40% of the Germany contract logistics market size in 2025. The Germany contract logistics market for Healthcare and Pharmaceuticals is forecast to expand the fastest at 4.65% CAGR between 2026-2031.

- By contract duration, Long-Term (Greater than or equal to 1 Year) held 67.30% of Germany contract logistics market share in 2025, while Short-Term (Less Than 1 Year) post the highest expected CAGR at 3.25% over the forecast period.

- By geography, North Rhine-Westphalia commanded 23.20% of Germany contract logistics market share in 2025. The Germany contract logistics market for Eastern Germany is poised to grow at 3.60% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Contract Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating B2C e-commerce penetration | +2.0% | Nationwide, strongest in large urban areas | Medium term (2-4 years) |

| OEM shift to electric-vehicle and battery production | +1.8% | Bavaria and Baden-Württemberg | Medium term (2-4 years) |

| Supply Chain Due Diligence Act compliance outsourcing | +1.5% | Nationwide | Short term (≤ 2 years) |

| Expansion of domestic pharma and biotech manufacturing | +2.8% | Hesse, Berlin-Brandenburg | Long term (≥ 4 years) |

| Rapid adoption of warehouse robotics and AI | +2.0% | Logistics hubs nationwide | Medium term (2-4 years) |

| Corporate decarbonization targets for transport | +1.0% | Nationwide, urban focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating e-commerce amplifies parcel volumes

B2C e-commerce now reaches 74% of German consumers and pushes fulfilment and last-mile traffic to record highs, raising the attractiveness of outsourcing to 3PLs that can scale automation and omnichannel capabilities. Parcel density, especially inside the Ruhr and Berlin metropolitan areas, enables route optimization that lowers per-unit delivery costs, incentivizing retailers to award multi-year fulfilment mandates within the Germany contract logistics market. Robots and goods-to-person systems shorten order-to-ship cycles, supporting same-day delivery commitments that have become a differentiator for fashion and consumer electronics sellers.

Electric-vehicle transition reshapes inbound flows

Germany remains Europe’s largest vehicle producer, yet platform electrification adds high-value battery modules and hazardous materials handling to inbound JIT and JIS logistics. Dedicated sequencing centers close to assembly plants in Bavaria and Baden-Württemberg are expanding, and providers able to guarantee ISO 45001 and ADR compliance are securing multi-plant contracts. This complexity lifts outsourcing intensity within the Germany contract logistics market as OEMs focus capital on cell production lines rather than warehouse footprints.

Supply Chain Due Diligence Act stimulates compliance-focused outsourcing

Since January 2024, the Act covers firms with at least 1,000 employees and imposes fines of up to 2% of global turnover for violations. Manufacturers have responded by handing over inbound visibility, supplier vetting, and audit-ready documentation to 3PLs with mature ESG platforms. Providers that combine regulatory expertise with blockchain traceability have tripled pipeline enquiries, translating into higher contract values and longer tenures across the Germany contract logistics market.

Domestic pharma expansion escalates cold-chain demand

Germany hosts Europe’s largest pharmaceutical output, and biologics, mRNA vaccines, and cell therapies increasingly require strict 2°C - 8°C or ultra-low-temperature handling down to -196°C. Logistics4Pharma has added dry shippers in Kelsterbach capable of maintaining cryogenic conditions, and UPS Healthcare commissioned a new multi-range cross-dock in Frankfurt. As a result, cold-chain volumes are outpacing the overall Germany contract logistics market by more than two times, supporting premium pricing.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of truck drivers and warehouse labor | −1.2% | Nationwide, acute in rural areas | Medium term (2-4 years) |

| Rising prime logistics real-estate rents and land scarcity | −0.8% | Core urban regions | Long term (≥ 4 years) |

| Strict emission regulations elevate fleet costs | −0.7% | Urban corridors | Short term (≤ 2 years) |

| Inflation-linked input costs under muted industrial output | −0.9% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Labor scarcity inflates operating costs

Vacancies for drivers and warehouse operatives reached about 500,000 in 2024, with the average driver age climbing to 47.2 years, prompting 3.42% statutory wage hikes. Providers in the Germany contract logistics market are investing in academies and flexible rosters, but labor adds volatility to cost bases and limits capacity during peak seasons.

Emission standards trigger fleet spending

Euro VII and CO₂-based tolls add EUR 46,500 (USD 53,737.35) annual charges to diesel heavy-duty vehicles versus less than EUR 2,000 (USD 2,311.28) for zero-emission options[1]Analysis Centre, “CO₂-Based Tolling Adds Cost to Diesel Fleets,” Transport & Environment, transportenvironment.org. The capex gap still deters wholesale electrification for long-haul routes, causing selective deployment and higher depreciation schedules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Warehousing Holds Scale, Value-Added Services Accelerate

Warehousing and distribution generated 43.60% of Germany contract logistics market revenue in 2025 on the back of extensive cross-docking and regional fulfilment centers aligned along the Rhine-Ruhr axis. The segment benefits from dense road, rail, and inland waterway links that shorten lead times to West European consumer markets, yet cost pressures from land scarcity and labor mean automation adoption is climbing steeply. Autonomous mobile robots pick and place small parcels, while automated storage and retrieval systems enhance pallet density, raising throughput by 25% and supporting higher utilization of scarce floor space.

Value-added services ranging from kitting to packaging and end-of-line light assembly are forecast to expand at 3.92% CAGR, outpacing the overall Germany contract logistics market. Clients increasingly require configuration near market to cut inventory risk and accelerate product launches, particularly for consumer electronics and industrial machinery. These specialized tasks command margins of 200–300 basis points above basic warehousing, and providers leverage digital twins to model process flows before committing physical assets. As a result, pressure mounts on smaller operators to invest in skills and technology or partner with larger 3PLs.

By End-User Industry: Healthcare leads growth momentum

Manufacturing and automotive still represent the single largest slice of Germany contract logistics market size at 26.40% in 2025, supported by high-frequency material flows into Bavaria and Baden-Württemberg plants. However, the sector confronts subdued industrial output and an accelerating pivot toward electric vehicles, which shifts layout and inventory profiles. Providers are retrofitting sequencing centers for battery modules, adopting fire-suppression standards, and redesigning transport packaging to mitigate thermal runaway risk.

Healthcare and pharmaceuticals deliver the fastest trajectory at 4.65% CAGR thanks to biologics and cell-and-gene therapies that demand rigorous GDP and GMP handling. Cold-chain volumes grow nearly twice as fast as the overall Germany contract logistics market, and specialized 3PLs have differentiated themselves using real-time temperature visibility, qualified packaging, and end-to-end regulatory documentation. UPS Healthcare, DB Schenker, and Pfenning are enlarging temperature-controlled footprints, triggering further M&A as generalists seek premium vertical exposure. Germany contract logistics industry participants recognize that high-margin healthcare contracts offset the cost drag from standard services.

By Contract Duration: Flexibility Gains Preferential Demand

Long-term agreements of one year or more still cover 67.30% of Germany contract logistics market contracts, offering visibility that underpins asset-heavy investments such as dedicated automation and sustainability upgrades. Automotive and consumer-goods shippers favor multi-year terms to lock in capacity near assembly lines or population centers. Nonetheless, short-term contracts below one year are advancing at a 3.25% CAGR, mirroring heightened macro uncertainty and rapid technological change.

The shift is visible in e-commerce peak season playbooks, where merchants request six-month fulfilment deals that scale both workforce and robot fleets on demand. Providers respond with modular warehousing, variable cost structures, and performance-linked pricing to safeguard profitability while meeting flexibility expectations. Robotics as a Service allows capex avoidance, aligning amortization periods with shorter commitments. These dynamics strengthen competitive rivalry within the Germany contract logistics market as agile mid-tier specialists compete on responsiveness against global incumbents.

Geography Analysis

North Rhine-Westphalia remains the largest regional node, contributing 23.20% of Germany contract logistics market revenue in 2025 on the strength of the Port of Duisburg and dense highway arteries. The Duisburg Gateway Terminal adds 850,000 TEU of annual capacity, enhancing intermodal connectivity that lowers hinterland transport costs for containerized imports. Proximity to Benelux seaports and dense consumer populations underpins robust warehousing demand, with vacancy rates below 3% across the Rhine-Ruhr region, encouraging speculative multilevel developments equipped with renewable energy solutions.

Eastern Germany, encompassing Berlin, Brandenburg, Saxony, Saxony-Anhalt, and Thuringia, is the fastest growing area at 3.60% CAGR, buoyed by Tesla’s gigafactory in Grünheide and Intel’s EUR 30 billion (USD 34.67 billion) semiconductor commitment. Logistics parks near Leipzig/Halle Airport and rail-served sites along the A14 corridor attract electronics, life-sciences, and battery players seeking access to skilled labor and competitively priced land. The German government’s EUR 500 billion (USD 577.82 billion) infrastructure fund prioritizes Eastern corridors, promising motorway upgrades and digital rail enhancements that could further elevate the Germany contract logistics market size in the region.

Hamburg and Schleswig-Holstein benefit from Hamburg’s deep-sea gateway, which handled over 220 million tons of cargo in 2024. Q1 2025 logistics space take-up jumped 89% year on year to 125,000 sqm, reflecting renewed container throughput and rising offshore-wind component staging. Bavaria and Baden-Württemberg, historically automotive strongholds, are reconfiguring supply chains for electric powertrains, creating new inbound flows for battery cells and recyclable materials. The resulting need for hazardous-goods warehousing, just-in-sequence shuttling, and green transport corridors further diversifies service demand across the Germany contract logistics market.

Competitive Landscape

The top tier is populated by DHL Supply Chain, DSV-DB Schenker (post-closing), Kühne + Nagel, and UPS Healthcare, which together control meaningful but not dominant shares, indicating moderate market concentration. DSV’s EUR 14.3 billion (USD 16.53 billion) purchase of DB Schenker adds 60,000 employees and propels pro forma revenue to EUR 39.3 billion (USD 45.42 billion), forging the second-largest global contract logistics provider. The integration strategy focuses on network synergies in Europe and North America, while German operations will absorb capability overlaps and rationalize redundant facilities, reshaping competitive pricing benchmarks across the Germany contract logistics market.

Technological differentiation eclipses pure scale. DHL has deployed more than 7,000 robots and expanded its robotics center of excellence in Troisdorf, enabling rapid cross-site rollout of AMR, vision-picking, and AI-driven labor planning. Hellmann Worldwide Logistics enlarged its global Contract Logistics division in 2025 through new hubs in Osnabrück and mobile automation pilots in Singapore, but the company also added pharmaceutical GDP certifications to bolster healthcare credentials. Mid-tier specialists like Logistics4Pharma focus on ultra-cold capabilities and compliance consulting, allowing them to command high-margin niches despite smaller footprints.

Sustainability commitments shape competitive postures. DB Schenker and DHL target 100% fossil-free line-haul transport in Germany by 2030, driving orders for battery-electric 19-t rigid trucks and piloting hydrogen fuel-cell tractors on hub-to-hub lanes. Providers harness intermodal shifts, especially Duisport-sited rail links, to cut emissions and mitigate Eurovignette CO₂ toll exposure. Customers increasingly evaluate 3PL bids on greenhouse-gas intensity, pushing smaller operators to partner with asset-light green-tech platforms or risk displacement in the Germany contract logistics market.

Germany Contract Logistics Industry Leaders

DHL Supply Chain & Global Forwarding

Dachser SE

Kuehne + Nagel

Rhenus Logistics

DSV Solutions

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: DSV completed its acquisition of DB Schenker for EUR 14.3 billion (USD 16.53 billion), forming a logistics group with approximately 160,000 staff and projected revenue of EUR 41.6 billion (USD 48.07 billion).

- January 2025: Prologis bought a 380,000 sqm logistics portfolio across Hamburg, Rhine-Neckar, Hanover, and Nuremberg, expanding its German footprint by 50% in five years.

- January 2025: Geis Group closed the acquisition of Gras Group and Krüger branches, adding 700 employees and extending IDS network coverage.

- December 2024: Aprojects acquired Futuretrans Logistik, bringing a 20-truck fleet, 24 trailers, and a 16,000 sqm Döbeln site under its European road transport arm.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Germany contract logistics market as all outsourced, multi-year deals in which a specialist 3PL manages domestic or cross-border transportation, warehousing, and value-added tasks (kitting, light assembly, reverse logistics) for goods moving within, into, or out of the country. According to Mordor Intelligence, revenue is captured at full landed value, while purely in-house logistics spend is excluded.

Scope exclusion: one-off spot freight, postal mail, and stand-alone courier or express parcel services lie outside this scope.

Segmentation Overview

- By Service

- Transportation Management

- Road

- Rail

- Air

- Sea

- Warehousing and Distribution

- Cold Chain/Temperature-Controlled

- Non-Cold Chain/Non-Temperature-Controlled

- Value-Added Services (Kitting, Packaging, Assembly, etc.)

- Transportation Management

- By End-User Industry

- Manufacturing and Automotive

- Consumer Goods and Retail (incl. E-commerce)

- High-Tech and Electronics

- Healthcare and Pharmaceuticals

- Oil, Gas and Chemicals

- Other End Users

- By Contract Duration

- Short-Term (Less Than 1 Year)

- Long-Term (Greater than or equal to 1 Year)

- By Geography

- North Rhine-Westphalia

- Hamburg and Schleswig-Holstein

- Lower Saxony and Bremen

- Hesse / Rhine-Main

- Bavaria

- Baden-Württemberg

- Rhineland-Palatinate and Saarland

- Eastern Germany (Berlin, Brandenburg, Saxony, Saxony-Anhalt, Thuringia)

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews with 3PL managers, shipper logistics heads, procurement leads, and regional trade bodies in North Rhine-Westphalia, Bavaria, and Hamburg validated desk findings, adjusted average price-per-pallet, and clarified contract length mix as well as upcoming capacity.

Desk Research

We mapped freight flows, warehouse footprints, and truck utilization with data from the Federal Statistical Office, Federal Motor Transport Authority, Eurostat trade cubes, and the German Logistics Association. Public filings, investor decks, and reputable trade press revealed contract wins and pricing shifts. Our team then tapped D&B Hoovers, Dow Jones Factiva, and Questel patent feeds to refine shipper splits, deal alerts, and automation cues. The sources named illustrate our desk work and are not exhaustive.

Market-Sizing & Forecasting

Mordor's model starts with a top-down rebuild of ton-kilometers and warehouse cubic-meter days, converts them to revenue through respondent-verified averages, and cross-checks totals with selective bottom-up supplier roll-ups. Key variables such as e-commerce share, automotive output, cold-chain space, contract duration mix, and the diesel index feed a multivariate regression that projects the 2024 base year through 2030. Interpolation guided by primary insight closes remaining gaps.

Data Validation & Update Cycle

Outputs face anomaly checks, peer review, and variance thresholds before sign-off. Reports refresh each year, with interim reviews when fuel spikes, major 3PL mergers, or regulatory shifts occur.

Why Mordor's Germany Contract Logistics Baseline Stands Up to Scrutiny

Published values often diverge because firms fold wider service baskets, lock exchange rates on different days, or apply global growth factors untested locally.

Mordor's explicit exclusions, contract-length adjustment, and annual refresh narrow these gaps.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 30.43 B (2025) | Mordor Intelligence | - |

| USD 236.2 B (2024) | Global Consultancy A | Counts whole logistics and in-house spend |

| USD 19.96 B (2024) | Regional Consultancy B | Growth extrapolation; no contract-length split |

| USD 13.14 B (2024) | Trade Journal C | Small-shipper survey; omits value-added work |

These comparisons show that Mordor's disciplined variable selection and regular validation give decision-makers a balanced, transparent baseline they can trust.

Key Questions Answered in the Report

What is the current size of the Germany contract logistics market?

The market is valued at USD 31.06 billion in 2026 and is forecast to climb to USD 34.42 billion by 2031.

Which region leads the Germany contract logistics market?

North Rhine-Westphalia is the largest region, holding 23.20% share in 2025 due to its dense infrastructure and proximity to European consumer hubs.

Which end-user industry is growing the fastest?

Healthcare and pharmaceuticals are expanding at a 4.65% CAGR, driven by strict cold-chain requirements and rising biologics production.

How is the Supply Chain Due Diligence Act affecting logistics outsourcing?

The Act mandates extensive human-rights and environmental checks, prompting firms to outsource logistics to 3PLs with robust compliance systems, thereby increasing contract volumes and values.

What role does automation play in the Germany contract logistics market?

Warehouse robotics and AI boost productivity and mitigate labor shortages, underpinning long-term outsourcing contracts and helping providers maintain margins amid wage inflation.

Page last updated on: