Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

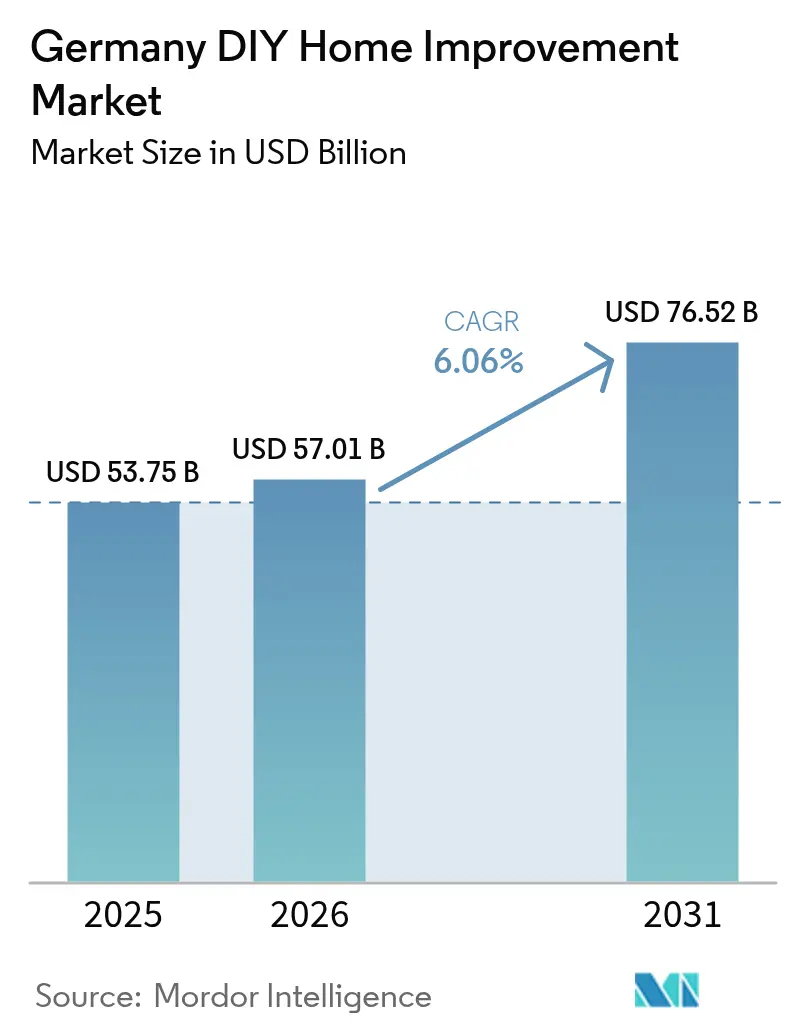

| Base Year Market Size (2025) | USD 53.75 Billion |

| Market Size (2026) | USD 57.01 Billion |

| Market Size (2031) | USD 76.52 Billion |

| Growth Rate (2026 - 2031) | 6.06% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany DIY Home Improvement Market Analysis by Mordor Intelligence

The Germany DIY home improvement market size was valued at USD 53.75 billion in 2025 and estimated to grow from USD 57.01 billion in 2026 to reach USD 76.52 billion by 2031, at a CAGR of 6.06% during the forecast period (2026-2031). Demand is buoyed by structural trends such as an aging housing stock, energy-efficiency mandates, and a nationwide shift toward cost-saving self-help projects. Digital disruption is intensifying competitive pressure because online channels grow faster than stores, despite accounting for only a small revenue share today. Energy retrofits that target heating systems and insulation upgrades contribute steadily to basket sizes, while garden and outdoor lines outperform on the back of lifestyle shifts toward sustainable living. Retailers respond by broadening assortments to include heat-pump kits, solar accessories,s and low-skill installation aids, anchoring future revenue streams on regulatory requirements rather than discretionary décor projects. Regional performance diverges: populous North Rhine-Westphalia supplies the largest revenue base, whereas Bavaria sets the pace on growth thanks to stronger incomes and proactive climate-policy subsidies.

Key Report Takeaways

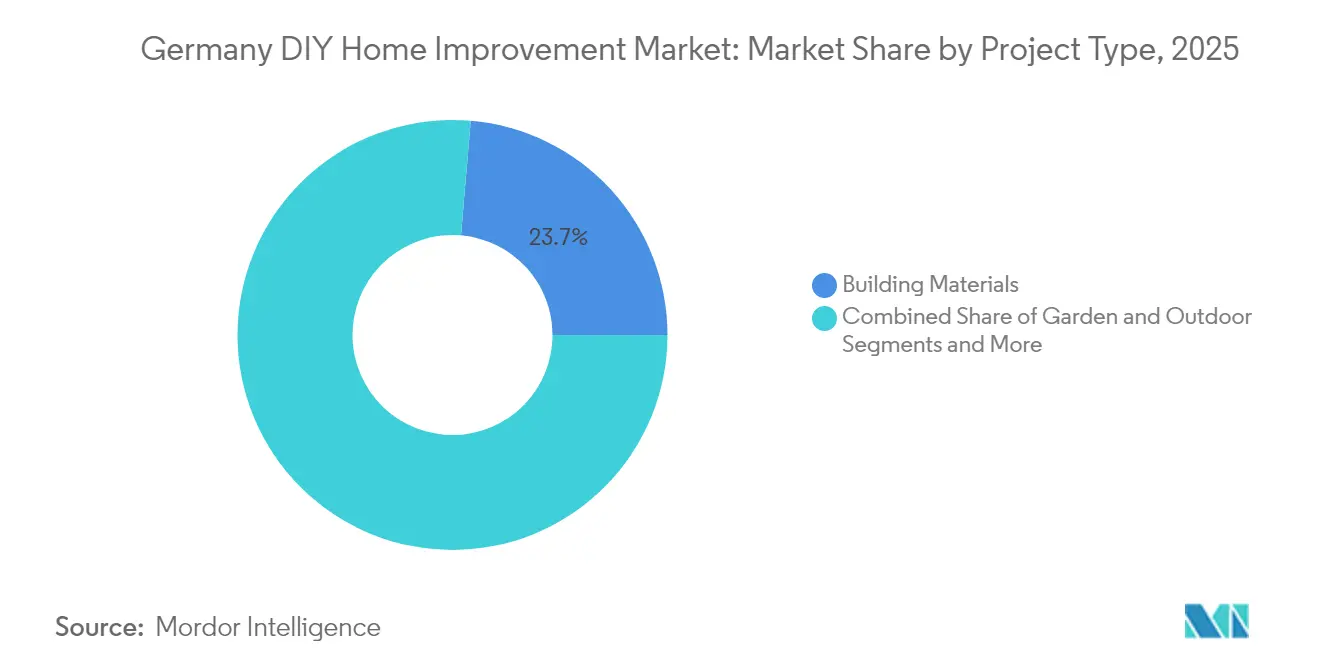

- By product category, Building Materials led with 23.65% of Germany DIY home improvement market share in 2025; Garden and Outdoor products are forecast to expand at a 6.82% CAGR through 2031.

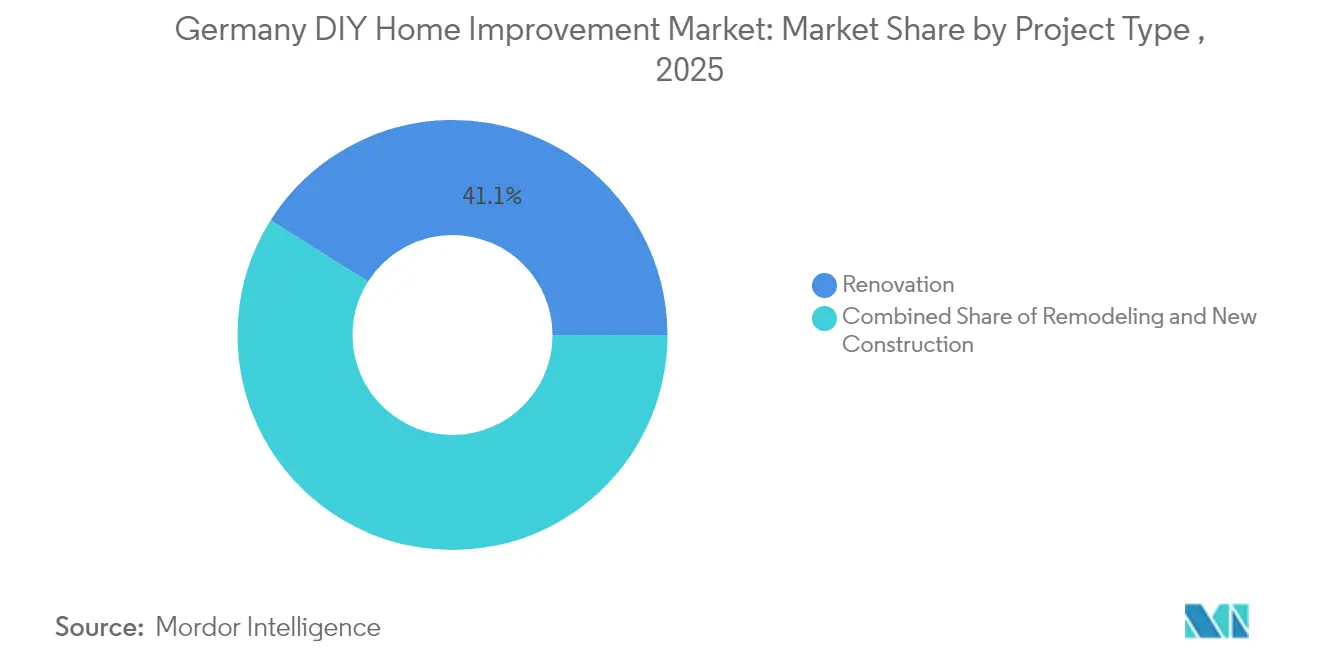

- By project type, Renovation held 41.05% of the Germany DIY home improvement market size in 2025, while Remodeling is advancing at a 6.35% CAGR through 2031.

- By distribution channel, DIY Superstores controlled 48.10% revenue in 2025; Online Pure-Play platforms register the highest projected CAGR at 7.98% to 2031.

- By region, North Rhine-Westphalia commanded 20.05% share of the Germany DIY home improvement market size in 2025 and Bavaria is set to post the fastest CAGR of 6.65% between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany DIY Home Improvement Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging housing stock requiring renovation | +1.8% | National, with concentration in North Rhine-Westphalia, Bavaria | Long term (≥ 4 years) |

| Rising DIY culture among cost-conscious consumers | +1.2% | National, stronger in urban areas | Medium term (2-4 years) |

| Accelerating e-commerce and omnichannel penetration | +0.9% | National, led by metropolitan regions | Short term (≤ 2 years) |

| Sustainability rules driving energy-efficient retrofits | +1.5% | National, EU-wide regulatory alignment | Long term (≥ 4 years) |

| Rental-deposit insurance freeing cash for tenant upgrades | +0.4% | Urban centers, particularly Berlin, Munich, Hamburg | Medium term (2-4 years) |

| Maker-space partnerships with municipalities | +0.2% | Urban municipalities, pilot programs expanding | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Housing Stock Requiring Renovation

About 30% of the country’s 21 million buildings carry poor G or H energy ratings, producing a large backlog of mandatory upgrades that expands the Germany DIY home improvement market. Annual refurbishment targets remain unmet, and cost-constrained owners increasingly opt for self-installation kits to comply with the Gebäudeenergiegesetz. Housing transactions trigger compulsory energy improvements, further lifting demand for insulation boards, roofing membranes, and heat-pump accessories. Rising construction costs of roughly 30% during 2021-2024 amplify the substitution of professional contractors with homeowner efforts. Low home-ownership rates mean landlords, too, are turning to budget DIY approaches to keep dwellings rentable under tighter efficiency rules.

Rising DIY Culture Among Cost-conscious Consumers

A broad shift toward frugal home projects is evident as household budgets tighten yet leisure time preferences favor practical creativity. Tool ownership is rising evenly across genders, and battery-powered devices simplify tasks that once demanded professional skill. Stable inflation forecasts around 2.2% for 2025 give planners confidence to allocate funds to weekend projects rather than postpone maintenance. The household tools segment benefits because cordless innovation makes drilling, sanding and sawing easier within apartments that restrict power outlets. Retailers respond with modular workshops and curated starter bundles, anchoring customer loyalty through instructional content and rental add-ons.

Accelerating E-commerce and Omnichannel Penetration

Digital commerce still represents only the low-teens share of Germany DIY home improvement market turnover, yet it is the fastest mover. Amazon.de illustrates the scale of opportunity with USD 1.3 billion in category sales. Brick-and-mortar leaders integrate click-and-collect, dynamic pricing, and artificial-intelligence inventory tools to protect their share. Hornbach’s real-time stock visibility system exemplifies this change and reduces out-of-stock rates, boosting both online conversion and in-store traffic. Current shopper behavior combines in-store advice with online research, so winning propositions blend wide assortments, transparent availability, and convenient fulfilment rather than pure online intensity.

Sustainability Rules Driving Energy-efficient Retrofits

The updated Gebäudeenergiegesetz obliges new heating systems to source 65% renewable energy from 2024, catalyzing sales of insulation materials, smart thermostats and solar kits[1]Source: Bundesministerium für Wohnen, Stadtentwicklung und Bauwesen, “Gebäudeenergiegesetz 2024,” bmwsb.bund.de. Heat pumps already appear in 76% of newly approved residential buildings. Federal and state subsidy schemes refund up to 70% of qualifying upgrade costs, turning energy retrofits from discretionary to economically compulsory. Two-thirds of homeowners plan photovoltaic installs by 2029, feeding demand for mounting hardware, inverters and wiring solutions. Retailers allocate extra aisle space to eco lines and supply QR-code tutorials that help customers navigate eligibility paperwork.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-labour shortages inflating input prices | -0.7% | National, acute in construction-heavy regions | Medium term (2-4 years) |

| High interest rates suppressing big-ticket remodels | -1.0% | National, stronger impact in high-cost regions | Short term (≤ 2 years) |

| Inflation in building-material costs | -0.6% | National, with regional variations in supply chains | Short term (≤ 2 years) |

| EU product-safety revisions raising sourcing overheads | -0.3% | EU-wide, with compliance costs varying by product category | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skilled-labour Shortages Inflating Input Prices

One-quarter of construction firms report that limited worker availability constrains order intake, pushing up wages and delaying projects[2]Source: Hauptverband der Deutschen Bauindustrie, “Krise im Wohnungsbau,” bauindustrie.de. Scarcity spills into retail channels because manufacturers ration supply to higher-margin professional outlets, sending price lists upward for items like specialty insulation foams. Prefabricated panels and plug-and-play retrofit kits appear as partial solutions because they shorten installation time and reduce skill needs. Municipal pilot programs test maker-spaces where citizens can borrow tools and attend workshops, easing reliance on trade professionals and sustaining the Germany DIY home improvement market despite capacity bottlenecks.

High Interest Rates Suppressing Big-ticket Remodels

Elevated financing costs weigh on new mortgages and equity-financed renovations, as reflected in a construction PMI trough of 36.3 during 2024. Consumers shift toward phased projects below EUR 5,000 that can be cash-funded, stretching improvement cycles but preserving volume in core ranges such as paint, sealants and fittings. Retailers adjust marketing to emphasize cost-splitting, modular tool hire and energy-savings calculators that translate upfront spending into lower utility bills. While the drag on the Germany DIY home improvement market persists through 2026, policy signals pointing to rate stability gradually restore confidence for larger undertakings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Building Materials Lead as Garden and Outdoor Accelerate

Building Materials captured 23.65% of the Germany DIY home improvement market in 2025, reflecting the dominance of insulation boards, roofing membranes and structural lumber in energy-driven retrofits. Garden and Outdoor ranges post the quickest climb at 6.82% CAGR through 2031 as households seek self-sufficiency and curb-appeal upgrades. The tools segment continues to benefit from cordless innovation, while decorative paints hold resilient because cosmetic refreshes remain affordable entry points for novice do-it-yourselfers.

Many Building Material purchases connect directly to subsidy-qualified projects, lifting average basket values and reinforcing loyalty to full-line superstores offering certified product assortments. Garden demand thrives on a cultural turn toward balcony vegetable patches and pollinator-friendly landscaping kits. Tools enjoy cross-category pull-through because consumers value versatilities such as drilling anchor holes for photovoltaic brackets. Décor and Furniture feel budget pressure, yet specialty lighting tied to smart-home integration partially offsets softness in impulse furnishings.

By Project Type: Renovation Dominance with Remodeling Momentum

Renovations retained 41.05% of the Germany DIY home improvement market size in 2025 as households tackled essential maintenance and incremental energy upgrades. Remodeling shows a faster 6.35% CAGR to 2031 because regulatory changes push simple fixes toward comprehensive system overhauls that integrate insulation, heat pumps, and solar power.

Subsidy programs enable homeowners to pursue larger scopes in single projects, and retailers curate bundled material lists that match funding criteria to ease compliance. The incremental migration from renovation to remodeling also stems from improved access to how-to content, encouraging confident multitasking rather than isolated repairs. While new-construction demand remains soft amid broader building sector weakness, self-build and prefabricated cabin kits offer a niche that retailers exploit through value-added logistics and on-site consultation services.

By Distribution Channel: Superstores Hold Share as Online Gains Momentum

DIY Superstores accounted for 48.10% revenue in 2025, preserving their leadership through immediate product availability, advisory services, and showroom displays. Online pure-play platforms grow at an 7.98% CAGR, helped by marketplace breadth and fast last-mile delivery that attracts digitally native customers.

Store-based players are doubling down on omnichannel capabilities: click-and-collect orders, AI-driven demand planning, and augmented-reality store navigation. Autonomous micro-stores piloted in commuter locations extend opening hours with minimal staffing and may help counter labor scarcity in retail operations. Specialty hardware outlets face squeeze pressures but defend niches through expert guidance in plumbing or electrical lines that remain trust-critical for safety compliance.

Geography Analysis

Regional performance highlights the heterogeneous nature of the Germany DIY home improvement market. North Rhine-Westphalia generated 20.05% of national revenue in 2025 thanks to its dense urban corridors, mature logistics networks, and concentration of large-format outlets. However, operating costs and softer consumer sentiment caused selected store closures, underlining the importance of efficiency upgrades and inventory rationalization.

Bavaria leads growth at a 6.65% CAGR through 2031. Higher disposable incomes, strong technology industry employment, and proactive state subsidy programs foster willingness to invest in premium insulation solutions, smart-home integrations, and garden upgrades. Rural Bavarian districts amplify potential because detached housing stock is larger, giving scope for exterior improvements and rooftop solar arrays.

Baden-Württemberg confronts GDP contraction and a 5.5% fall in construction output, but its engineering culture sustains demand for technically advanced DIY kits as households look to self-install efficiency measures. Lower Saxony, Hesse, and the remaining Bundesländer offer expansion possibilities where digital infrastructure enables retailers to reach scattered communities with tailored omnichannel services. Rental market diversity also shapes spending: urban tenancy dominates Berlin and Hamburg, creating demand for reversible décor products and portable solar balconies, whereas higher ownership ratios in eastern regions support more extensive structural renovations.

Competitive Landscape

Market concentration is moderate: Bauhaus captured EUR 4.31 billion sales in 2024, edging past OBI at EUR 4.19 billion and consolidating top-line leadership. Hornbach maintains strong positions in central and southern states and differentiates through technology investments that deliver real-time inventory accuracy. Amazon.de’s USD 1.3 billion DIY turnover signals a structural digital competitor able to scale assortments rapidly without fixed-store capital.

Strategic responses emphasize ecosystem building. Bauhaus operates a marketplace that hosts 2,000+ categories and draws more than 150 million annual visits, creating platform-fee revenue in addition to product margin. OBI’s April 2025 purchase of Migros’ Swiss chain broadens geographic presence and procurement leverage[3]Source: OBI Group, “OBI Expands into Switzerland,” obi-group.com. Category specialists step into white-space opportunities such as heat-pump accessories, EV-charging kits and smart-watering systems, partnering with utilities and municipalities for co-marketing campaigns.

Competitive intensity is further shaped by supply chain digitization. Leaders deploy predictive analytics to minimize stock-outs in subsidy-relevant products, an edge when homeowners face regulatory deadlines. Smaller regional chains cooperate through joint buying groups yet still grapple with technology capital needs. Overall success hinges on blending physical experience, digital convenience and value-added service packages that support complex installation projects without inflating total cost of ownership for customers.

Germany DIY Home Improvement Industry Leaders

OBI

Bauhaus

Hornbach

Toom Baumarkt

Hagebau

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: OBI Group completed the acquisition of Migros’ OBI stores in Switzerland along with two Do it + Garden outlets, strengthening its European footprint in the home and garden sector.

- September 2024: Hornbach Baumarkt selected Blue Yonder software to enhance real-time inventory visibility in support of its interconnected retail strategy.

- July 2024: Bosch agreed to purchase Johnson Controls’ global HVAC solutions business for USD 8 billion, adding EUR 4 billion in annual sales to its Home Comfort Group.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Germany DIY home-improvement market as all products, tools, and ancillary materials bought by end-users who personally plan and execute repair, maintenance, minor construction, or aesthetic upgrade projects within residential premises. Spending tracked covers in-store and online purchases of building materials, paints and coatings, hardware, garden inputs, electrical and plumbing fittings, and portable power tools, expressed in nominal US dollars.

Scope exclusions include labor services performed by professional contractors, wholesale-only building material flows, and large appliances, which are kept outside the value pool.

Segmentation Overview

- By Product Category

- Building Materials

- Tools and Equipment

- Paints, Coatings and Adhesives

- Lighting and Electrical

- Decor and Furniture

- Garden and Outdoor

- Plumbing Materials

- Flooring

- By Project Type

- Renovation

- Remodeling

- New Construction

- By Distribution Channel

- DIY Superstores

- Specialty Hardware Stores

- Online Pure-Play

- Retailer Click-and-Collect

- By Region - Germany

- Bavaria

- Baden-Wurttemberg

- North Rhine-Westphalia

- Lower Saxony

- Hesse

- Remaining Bundeslander

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed store managers in five Bundeslaender, online marketplace category heads, buying groups, and insulation-system suppliers. These conversations helped us verify average ticket sizes, peak spring-summer seasonality, do-it-yourself skill penetration among tenants, and the pass-through of raw-material inflation into shelf prices. Insights also shaped model assumptions for online share and project-type mix.

Desk Research

We started with public macro-series from Destatis, Eurostat, and the German Federal Environment Agency to size housing stock, renovation cycles, and energy-efficiency retrofit grants. Trade association yearbooks from BHB and Hagebau supplied DIY retail turnover splits, while customs data (Volza) clarified import penetration for hand tools and fittings. Company filings, investor decks, and selected articles harvested through Dow Jones Factiva mapped pricing shifts and promotional intensity. Paid resources such as D&B Hoovers filled revenue gaps for unlisted retailers. This list is illustrative; many other databases and journals supported cross-checks and clarification throughout the build.

Market-Sizing & Forecasting

A top-down construct begins with retail sales reported by DIY superstores and specialty chains, rebuilt into a national value pool using coverage ratios for independents and e-commerce. Selective bottom-up tests sampled average selling price multiplied by unit volumes for key categories, providing a reasonableness lens before finalization. Key variables include housing turnover, renovation subsidy uptake, average project basket value, online channel penetration, price indices for lumber and decorative paints, and consumer confidence trends. A multivariate regression projects each driver through 2030, and an ARIMA overlay captures cyclical shocks. Gaps in category data are bridged with weighted moving-average imputation anchored to the most reliable adjacent series.

Data Validation & Update Cycle

Outputs undergo variance checks versus government retail statistics, retailer guidance, and ECDB e-commerce panels. Senior analysts review anomalies, and numbers are updated annually or sooner if energy-renovation incentives, VAT shifts, or retailer mergers materially alter baselines. A fresh validation pass is performed just before report release.

Why Our Germany DIY Home Improvement Baseline Earns Trust

Published estimates often differ because firms pick dissimilar scopes, exchange-rate cut-offs, and refresh cadences.

Key gap drivers include whether online pure-play sales are counted, how gift-card breakage is treated, and how aggressively future subsidy uptake is assumed. Our study aligns to full-channel spending in 2025 US dollars and refreshes each year, which are then reinforced by German-specific primary checks.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 53.75 Bn (2025) | Mordor Intelligence | - |

| USD 46.20 Bn (2024) | Global Consultancy A | Omits online-only platforms and applies conservative housing-turnover elasticity |

| USD 68.50 Bn (2024) | Industry Association B | Includes contractor-assisted DIY kits and bundles trade-only categories, inflating totals |

The comparison shows that figures sway when scope or variable choices shift. By grounding the baseline in clearly stated inclusions, audited data streams, and an annually renewed forecast logic, Mordor Intelligence delivers a dependable, decision-ready reference for stakeholders.

Key Questions Answered in the Report

What is the current size of the Germany DIY home improvement market?

The market stands at USD 57.01 billion in 2026 and is projected to reach USD 76.52 billion by 2031.

Which product category leads sales in Germany’s DIY sector?

Building Materials leads with 23.65% revenue share in 2025, reflecting strong demand for insulation, roofing and structural upgrades.

How fast are online DIY sales growing in Germany?

Online pure-play channels grow at an 7.98% CAGR through 2031, faster than any other distribution format.

Why is Bavaria the fastest-growing region?

Higher disposable incomes, strong employment and generous energy-efficiency subsidies propel Bavarian growth at a 6.65% CAGR.

Who is the largest DIY retailer in Germany?

Bauhaus became the market leader in 2024 with EUR 4.31 billion in sales, surpassing OBI.

Page last updated on: