Germany Data Center Water Consumption Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

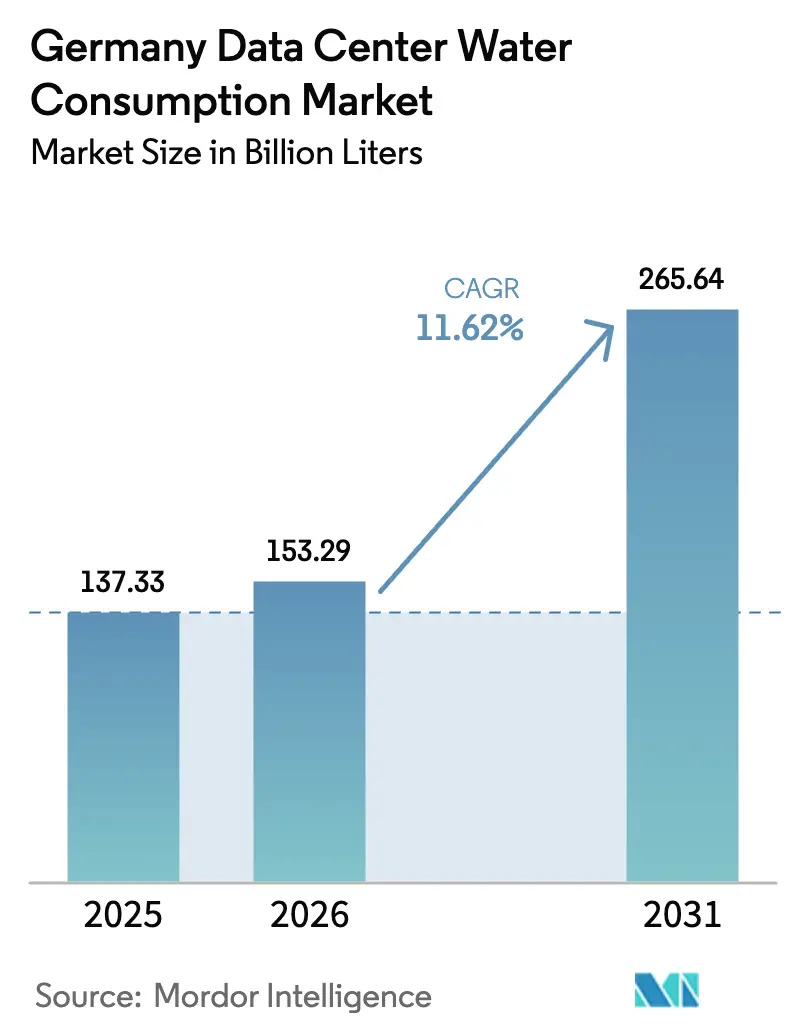

| Base Year Market Size (2025) | 137.33 Billion liters |

| Market Volume (2026) | 153.29 Billion liters |

| Market Volume (2031) | 265.64 Billion liters |

| Growth Rate (2026 - 2031) | 11.62% CAGR |

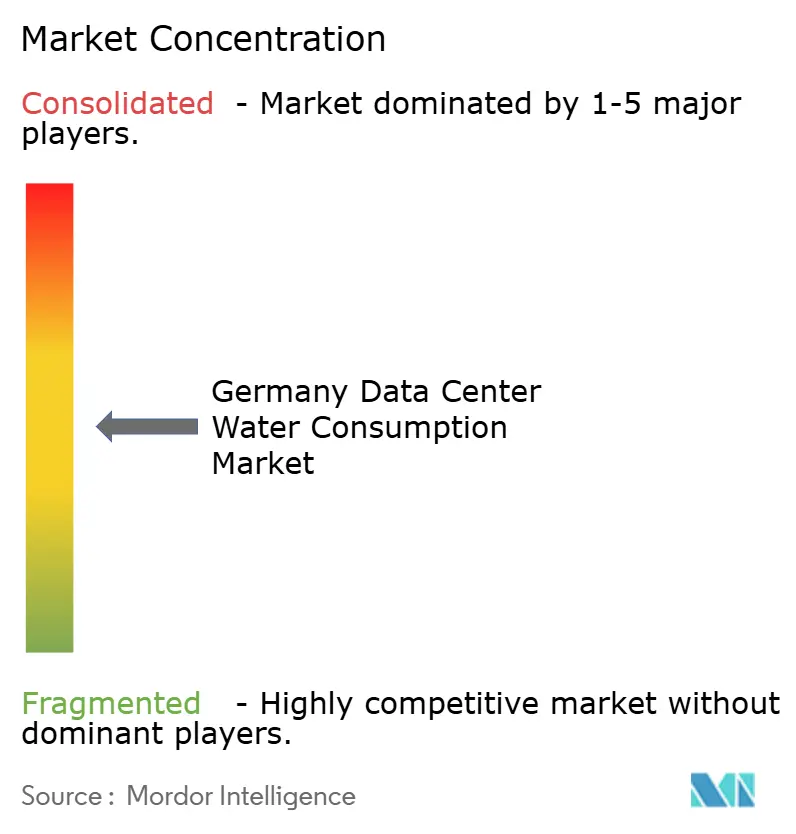

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Data Center Water Consumption Market Analysis by Mordor Intelligence

The Germany Data Center Water Consumption Market size is expected to grow from 137.33 Billion liters in 2025 to 153.29 Billion liters in 2026 and is forecast to reach 265.64 Billion liters by 2031 at 11.62% CAGR over 2026-2031. This expansion reflects simultaneous growth in hyperscale capacity, tighter efficiency mandates, and heightened public scrutiny over water withdrawals. Demand is rising fastest in Frankfurt and Berlin, where new cloud regions require high-density racks that favor liquid cooling, a shift that increases per-megawatt water draw despite efficiency gains. Operators are responding with closed-loop designs, reclaimed water sourcing, and waste heat reuse agreements that offset freshwater demand. Capital spending is being re-allocated toward on-site treatment plants and AI-based control software, which together lower operating costs and improve compliance with Germany’s Energy Efficiency Act. Competitive intensity is rising as cooling-equipment majors and immersion specialists race to deliver turnkey solutions that simultaneously satisfy energy, water, and heat-reuse metrics.

Key Report Takeaways

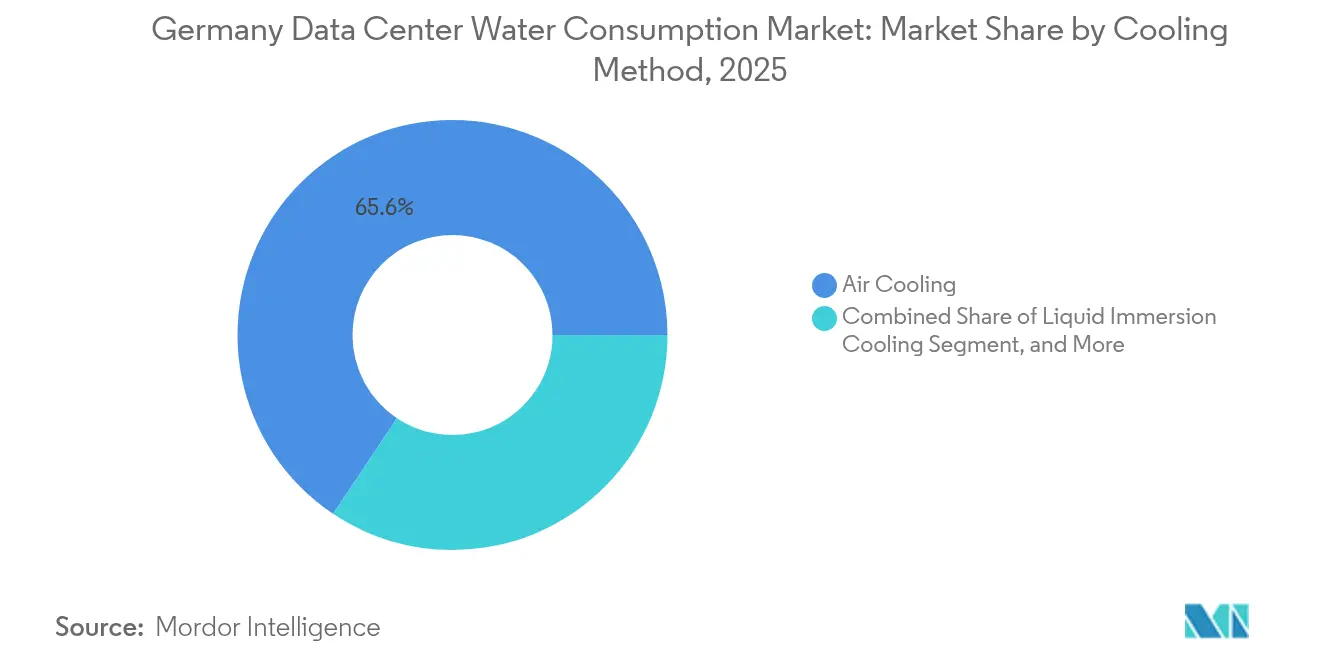

- By cooling method, air cooling led with 65.62% of the Germany data center water consumption market share in 2025; liquid immersion is projected to grow at a 12.21% CAGR through 2031.

- By facility size, medium installations captured 41.12% of the Germany data center water consumption market share in 2025, while hyperscale sites above 50 MW are expanding at a 12.08% CAGR to 2031.

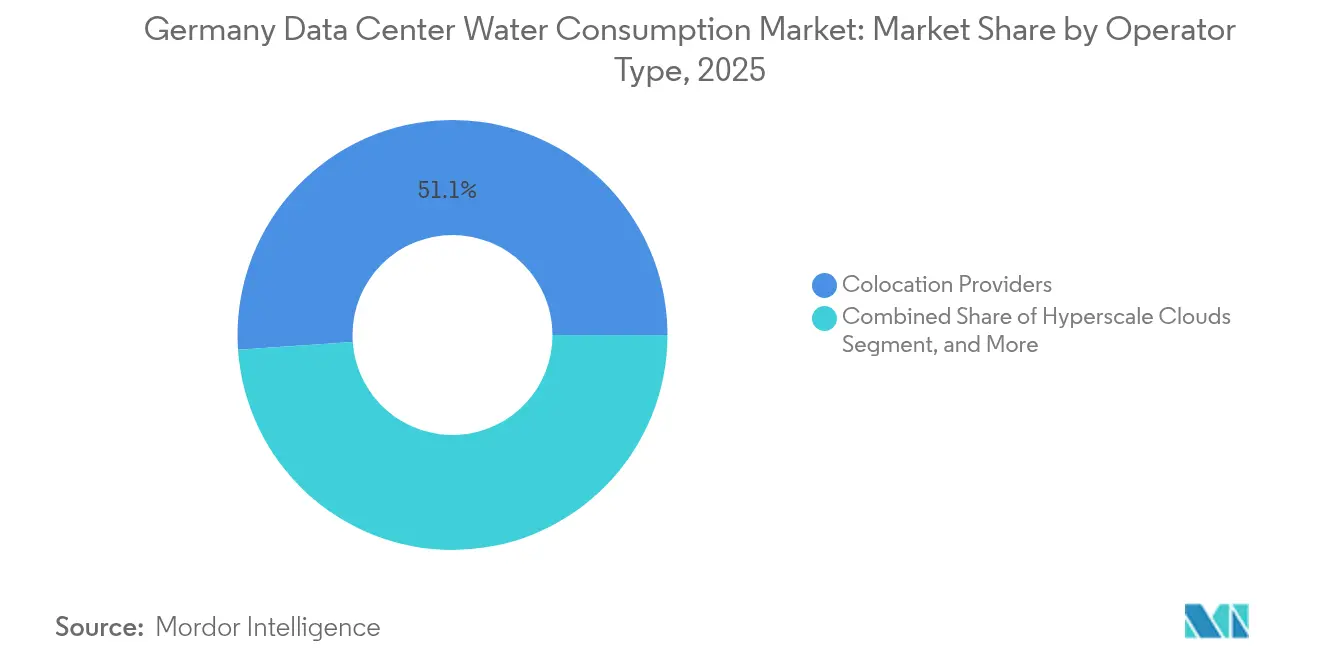

- By operator type, colocation providers held a 51.10% of the Germany data center water consumption market share in 2025, and hyperscale clouds are projected to record the highest CAGR at 12.32% through 2031.

- By water source, municipal potable water accounted for 70.88% of the Germany data center water consumption market size in 2025; reclaimed and wastewater sources are projected to grow at a 12.36% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Competitive positioning in Germany includes both locally based firms and those operating across multiple regions. The market landscape in the global data center water consumption industry research shows how these players are arranged internationally.

Germany Data Center Water Consumption Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter Government Targets on Data Center Water Usage Effectiveness | +2.1% | National (Frankfurt, Berlin, Munich) | Medium term (2-4 years) |

| Expansion of Hyperscale Facilities in Frankfurt and Berlin Regions | +2.8% | Frankfurt Rhine-Main, Berlin-Brandenburg | Short term (≤ 2 years) |

| Adoption of Closed-Loop Liquid Cooling to Lower Operating Costs | +2.3% | National (AI/HPC clusters) | Medium term (2-4 years) |

| Incentives for Greywater and Reclaimed Water Use in Industrial Facilities | +1.4% | Water-stressed regions | Long term (≥ 4 years) |

| Rising Electricity Prices Driving Demand for Water-Efficient Cooling | +1.9% | National | Short term (≤ 2 years) |

| Advancements in AI-Based Cooling Control Systems Reducing Water Waste | +1.5% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter Government Targets On Data Center Water Usage Effectiveness

Germany’s Energy Efficiency Act requires annual Water Usage Effectiveness (WUE) reporting for every facility above 300 kW connection capacity, applying DIN EN 50600-4-9 methodology and imposing lower PUE ceilings over time.[1]Umweltbundesamt, “Aufbau eines Registers für Rechenzentren in Deutschland und Entwicklung eines Bewertungssystems für energieeffiziente Rechenzentren,” umweltbundesamt.de Operators must therefore optimize energy and water performance in tandem, favoring liquid cooling that supports heat-reuse mandates. Inland sites lacking reclaimed supplies face a higher compliance risk and must invest in closed-loop systems or on-site treatment to avoid relying on potable water withdrawals. Larger operators are already securing wastewater contracts, leaving smaller facilities exposed to tariff hikes and reputational scrutiny. As the 1.5 PUE threshold takes effect in 2027, WUE transparency will become a key factor in customer site selection.

Expansion Of Hyperscale Facilities In Frankfurt And Berlin Regions

Planned and installed hyperscale capacity in Frankfurt and Berlin surpasses 1,800 MW, making these metros the epicenter of Germany data center water consumption market growth.[2]Bitkom, “Rechenzentren in Deutschland,” bitkom.org AWS alone has earmarked EUR 7.8 billion (USD 8.81 billion) for its Brandenburg sovereign-cloud campus. Such projects intensify pressure on already stressed aquifers, prompting municipalities to link new permits to proof of non-potable sourcing or district-heating off-take deals. This dynamic accelerates partnerships with wastewater utilities. NTT DATA’s Spandau sites will supply 8 MW of heat to Berlin’s Gartenfeld district, thereby reducing the net cooling water requirements.

Adoption Of Closed-Loop Liquid Cooling To Lower Operating Costs

Closed-loop direct-to-chip and immersion systems reduce cooling energy by up to 70% and minimize evaporation, making them particularly attractive in areas where industrial electricity prices average EUR 0.25 kWh. Rittal’s 1 MW rack-format module circulates 40-50°C coolant, achieving sub-1.1 PUE while capturing heat compatible with district networks. Although retrofit costs reach EUR 500 kW, payback falls below four years when operators monetize waste heat at EUR 50 MWh. Early adopters are primarily hyperscale operators that can spread capital over large footprints.

Advancements In AI-Based Cooling Control Systems: Reducing Water Waste

AI-driven platforms from Schneider Electric, Siemens, and Vertiv optimize tower cycles, chilled-water flow, and economization modes in real-time, trimming water use by 5-15% while meeting thermal targets.[3]Schneider Electric, “Water-free cooling designs for data centers,” se.com Digital Realty’s deployment prevented 78 million gallons of annual waste across four German sites after anomaly detection flagged leaks. These savings accrue quickly in hybrid cooling plants, helping legacy halls meet pending WUE reporting benchmarks without requiring wholesale equipment replacement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Availability of Reclaimed Water Infrastructure | -1.8% | Inland metros (Munich, Stuttgart) | Long term (≥ 4 years) |

| Regulatory Uncertainty Around Liquid Immersion Coolants | -1.2% | National | Short term (≤ 2 years) |

| High Capital Expenditure for On-Site Water Treatment Systems | -1.6% | National | Medium term (2-4 years) |

| Growing Public Scrutiny Over Industrial Water Withdrawals In Drought Zones | -1.4% | Berlin-Brandenburg, Lower Rhine | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Availability Of Reclaimed Water Infrastructure

Only a fraction of Germany’s 9 billion m³ of yearly wastewater output is treated to industrial-reuse grade, leaving operators in inland metropolitan areas dependent on potable supplies or costly on-site reverse-osmosis plants. EU Regulation 2020/741 establishes uniform quality standards, but federal implementation has lagged, resulting in uneven access and prolonged payback periods for municipal upgrades. Medium facilities (5-20 MW) are hardest hit because their scale cannot absorb EUR 500-800 m³-day treatment costs, yet they still fall under WUE disclosure rules.

Regulatory Uncertainty Around Liquid Immersion Coolants

Dielectric fluids reside in a gray zone under both Germany’s Chemical Safety Act and the EU F-gas phase-out, leaving operators without clear containment and disposal rules. Pending guidance stalls investment: STULZ forecasts immersion in new builds at 15% by 2030, but cautions that harmonized permitting must be in place by 2026 to capture retrofit demand. Smaller colocation sites defer adoption until compliance pathways and insurance provisions become standardized.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cooling Method: Structural Shift Toward Liquid Solutions

Liquid immersion and direct-to-chip technologies are enabling the cooling of high-density racks that air systems struggle to cool. Air cooling still commanded 65.62% of the revenue in 2025, but its share will contract as AI training pushes rack loads beyond 100 kW. The Germany data center water consumption market size for direct-to-chip solutions will expand alongside district-heating integration that monetizes 40-50°C waste heat. Two-phase immersion, championed by the January 2025 STULZ-Asperitas alliance, removes pumps and slashes parasitic power, positioning it as the premium choice for GPU clusters. Air-liquid hybrids remain viable options for multi-tenant halls where heterogeneous workloads necessitate flexible thermal zones.

The Germany data center water consumption market continues to witness differential paybacks. Immersion installations cost EUR 800-1,200 kW, roughly double that of air systems, yet energy savings and heat-reuse revenue shorten the ROI to three to four years in regions paying more than EUR 0.20 kWh. Retrofit complexity favors direct-to-chip over full immersion because existing chilled-water plants can be repurposed, easing downtime for live colocation floors.

By Facility Size: Hyperscale Dominance Intensifies

Hyperscale campuses exceeding 50 MW are growing at an annual rate of 12.08%, led by AWS's Brandenburg and Microsoft Azure's Frankfurt builds. The Germany data center water consumption market share of medium sites stood at 41.12% in 2025, but their growth lags hyperscale because reclaimed-water infrastructure and heat-reuse off-takes scale more efficiently at mega-campuses. Small edge nodes with a capacity under 5 MW remain primarily air-cooled and face limited WUE exposure; yet, they collectively must report once their capacity exceeds 300 kW.

Large-scale operators are caught between the disadvantages of scale and regulatory obligations. Without access to municipal tertiary treatment networks, many will rely on potable water and absorb escalating tariffs. Hyperscale players offset water risk by funding on-site treatment and rainwater capture; Colt Data Centre Services now incorporates both features in its 63 MW Frankfurt and 54 MW Berlin builds.

By Operator Type: Cloud Platforms Expand Faster Than Colocation

The Germany data center water consumption market is shifting toward vertically integrated hyperscale clouds, now the fastest-expanding operator tier at 12.32% CAGR. Colocation retains plurality at 51.10% but confronts tenant heterogeneity that slows the adoption of single-mode liquid solutions. Enterprise facilities are contracting as banks, automakers, and public agencies migrate workloads; yet, their legacy chilled-water plants still drive notable potable water demand. Edge deployments grow from a small base but remain water-light, mainly using direct air or closed-loop liquid coils.

Hyperscale clouds leverage their purchasing power to negotiate contracts for recycled water and invest in zero-water cooling prototypes, as Microsoft’s 2024 pledge demonstrates. Colocation providers risk margin compression if tenants resist green-premium pricing, pushing them to adopt AI control platforms to improve WUE without major capex.

By Water Source Type: Reclaimed Water Adoption Accelerates

Reclaimed and wastewater supplies are forecast to grow at a 12.36% CAGR, yet infrastructure gaps leave potable sources with a 70.88% share in 2025. The Germany data center water consumption market size tied to reclaimed sources is constrained by the limited number of tertiary treatment plants feeding industrial zones. Coastal cities piloting seawater exchangers illustrate alternative pathways, but environmental approvals lengthen rollout timelines.

Operators with early access to reclaimed pipelines gain a strategic advantage. NTT DATA’s Berlin deal with ENGIE eliminates evaporative losses while generating revenue, demonstrating the appeal of the closed-loop model. Inland sites in Munich and Stuttgart must weigh the costs of drilling private wells against rising public opposition and groundwater taxes. Rainwater capture remains marginal because Germany’s precipitation cannot sustain multi-MW loads.

Geography Analysis

Frankfurt Rhine-Main and Berlin-Brandenburg concentrate over 65% of planned capacity through 2030, anchoring the Germany data center water consumption market trajectory. Frankfurt’s role as Europe’s largest exchange hub remains a key location preference despite impending caps on potable withdrawals. New permits are increasingly contingent on non-potable sourcing or heat-reuse commitments, effectively integrating water strategy into site economics.

Berlin-Brandenburg’s drought profile magnifies scrutiny. DIW Berlin recorded conflicts among agriculture, residents, and data centers after 2024’s record-low groundwater levels. Schwarz Digits’ EUR 11 billion Lübbenau campus positions waste heat as a social utility to deflect criticism, yet its success depends on district heating uptake by 2028. Southern metros like Munich benefit from Alpine aquifers but impose withdrawal taxes to discourage excessive use, while Hamburg tests seawater cooling, which could set a precedent for freshwater-free operations.

Regional policy divergence creates siting arbitrage. Northern states subsidize heat-reuse networks, making reclaimed projects financially attractive. Operators trade fiber latency against water security; thus far, connectivity wins, confirming the structural magnetism of Frankfurt and Berlin. Unless new long-haul routes or regional cloud hubs emerge, inland scarcity will intensify competition for reclaimed resources.

Mordor Intelligence tracks the data center water consumption market across other major regions such as Europe, North America, and South America, with additional country-level coverage spanning Netherlands, Spain, Canada, Chile, United States, and Mexico, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

The Germany data center water consumption market shows moderate fragmentation. Established HVAC majors Rittal, STULZ, and Munters have retooled their portfolios toward high-density liquid cooling, bundling hardware with water-quality monitoring and leak detection capabilities. Water-chemistry leaders Ecolab and Veolia pivot from tower chemicals to closed-loop treatment analytics, positioning themselves as WUE compliance partners. Immersion specialists LiquidStack, Iceotope, and Asetek court GPU clusters with dielectric suites tuned for low GWP, though regulatory gray zones hinder scale.

Solution delivery is consolidating. Customers prefer single contracts that cover cooling equipment, water treatment, and heat-reuse tie-ins, encouraging alliances like STULZ-Asperitas. Technotrans targets retrofit niches with bolt-on liquid kits that minimize downtime. AI-based optimization software from Schneider Electric and Siemens ensures recurring revenue, locking in customers through data-driven performance guarantees.

Barriers to entry rise with each new regulation. Vendors must field regulatory affairs teams to navigate chemical safety, fire codes, and EU F-gas compliance, favoring capitalized incumbents. Market participants able to guarantee a sub-1.2 PUE, low WUE, and heat-reuse delivery will secure hyperscale design wins, leaving smaller equipment makers to focus on edge and retrofit opportunities.

Germany Data Center Water Consumption Industry Leaders

Ecolab Inc.

Veolia Environnement SA

Pentair plc

SPX Technologies Inc.

Baltimore Aircoil Company Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Veolia agreed with Mainova to build a tertiary-treated reclaimed-water pipeline for Frankfurt’s data-center corridor, scheduled for service in 2027 and expected to displace 3 million m³ of potable water annually.

- June 2025: Rittal commissioned Germany’s first liquid-cooled hall rated at 1 MW per rack on a Frankfurt campus, using a sealed water loop and dry coolers to achieve zero evaporative loss.

- April 2025: ENGIE Deutschland and NTT DATA finalized a deal to pipe 8 MW of waste heat from Spandau data centers into Berlin’s Gartenfeld district, reducing freshwater demand through closed-loop cooling.

- January 2025: STULZ and Asperitas signed a cooperation agreement to integrate two-phase immersion cooling into modular data center designs for racks above 150 kW, targeting water-neutral operation.

Germany Data Center Water Consumption Market Report Scope

The Germany Data Center Water Consumption Market Report is Segmented by Cooling Method (Air Cooling, Water Cooling (Chilled Water), Liquid Immersion Cooling, Direct-To-Chip Liquid Cooling), Facility Size (Small (Up To 5 MW), Medium (5-20 MW), Large (20-50 MW), Hyperscale (Above 50 MW)), Operator Type (Colocation Providers, Hyperscale Clouds, Enterprise/Internal Data Centers, Edge/Modular Data Centers), Water Source Type (Municipal Potable Water, Reclaimed/Wastewater, On-Site Groundwater, Captured Rainwater), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Air Cooling |

| Water Cooling (Chilled Water) |

| Liquid Immersion Cooling |

| Direct-to-Chip Liquid Cooling |

| Small (Up to 5 MW) |

| Medium (5 – 20 MW) |

| Large (20 – 50 MW) |

| Hyperscale (Above 50 MW) |

| Colocation Providers |

| Hyperscale Clouds |

| Enterprise/Internal Data Centers |

| Edge/Modular Data Centers |

| Municipal Potable Water |

| Reclaimed/Wastewater |

| On-Site Groundwater |

| Captured Rainwater |

| By Cooling Method | Air Cooling |

| Water Cooling (Chilled Water) | |

| Liquid Immersion Cooling | |

| Direct-to-Chip Liquid Cooling | |

| By Facility Size | Small (Up to 5 MW) |

| Medium (5 – 20 MW) | |

| Large (20 – 50 MW) | |

| Hyperscale (Above 50 MW) | |

| By Operator Type | Colocation Providers |

| Hyperscale Clouds | |

| Enterprise/Internal Data Centers | |

| Edge/Modular Data Centers | |

| By Water Source Type | Municipal Potable Water |

| Reclaimed/Wastewater | |

| On-Site Groundwater | |

| Captured Rainwater |

Key Questions Answered in the Report

How large is the Germany data center water consumption market in 2026?

It is valued at USD 153.29 billion liters and is projected to reach USD 265.64 billion liters by 2031.

Which cooling technology is growing fastest in German facilities?

Liquid immersion cooling is advancing at a 12.21% CAGR as AI workloads push rack densities beyond air-cooling limits.

Why are hyperscale campuses concentrating in Frankfurt and Berlin?

Both metros offer dense fiber interconnects and renewable-power access, even though their aquifers face stress, driving demand for reclaimed water and heat-reuse projects.

What regulatory metrics must German data centers track?

Operators must report Power Usage Effectiveness, Water Usage Effectiveness and Energy Reuse Factor under the Energy Efficiency Act.

How are operators reducing freshwater withdrawals?

Strategies include closed-loop liquid cooling, reclaimed-water sourcing, AI optimization software and monetizing waste heat through district-heating networks.

What is the main barrier to wider adoption of immersion cooling?

Uncertainty over dielectric fluid containment and disposal rules under German chemical and fire-safety regulations slows large-scale rollouts.

Page last updated on: