France Data Center Water Consumption Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

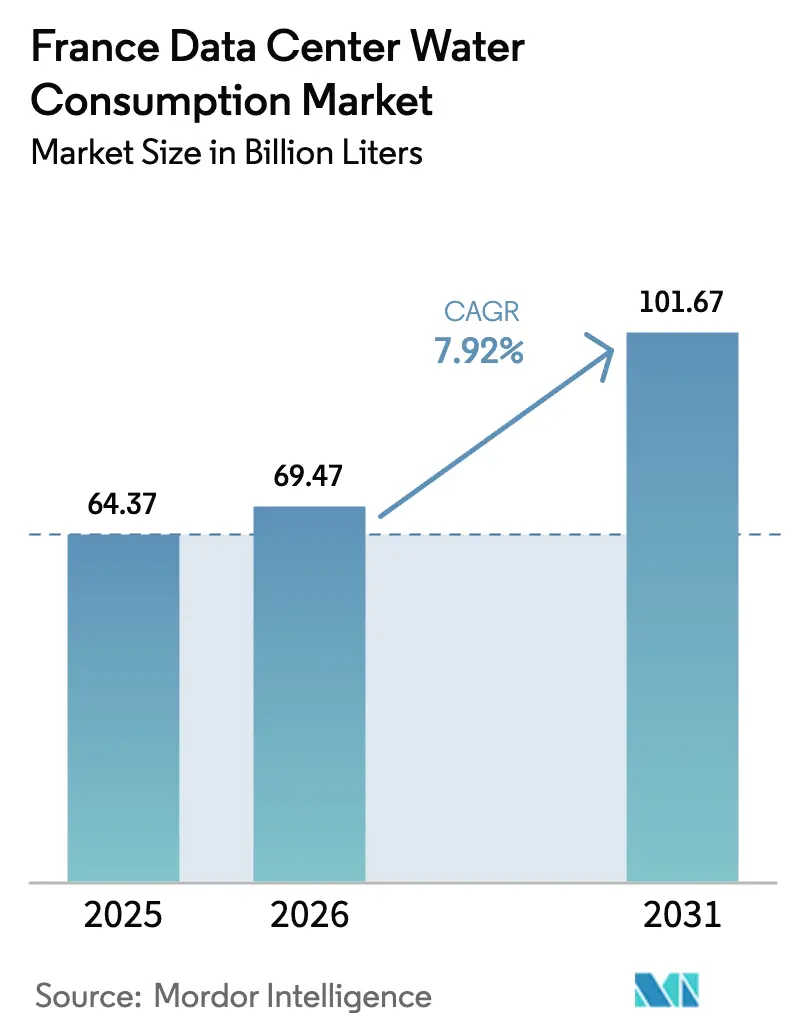

| Base Year Market Size (2025) | 64.37 Billion liters |

| Market Volume (2026) | 69.47 Billion liters |

| Market Volume (2031) | 101.67 Billion liters |

| Growth Rate (2026 - 2031) | 7.92% CAGR |

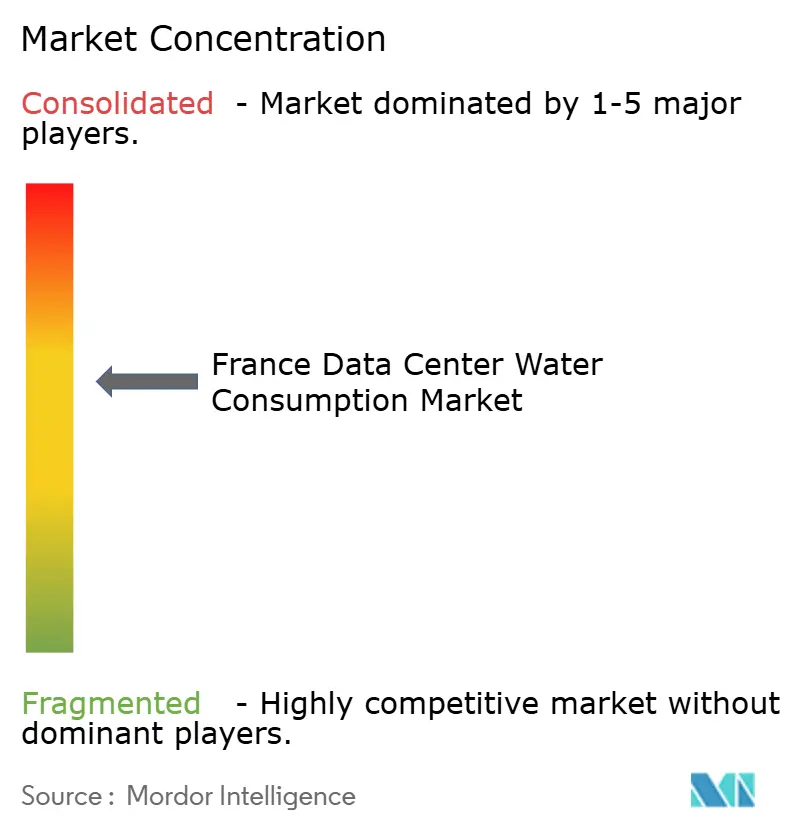

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Data Center Water Consumption Market Analysis by Mordor Intelligence

France Data Center Water Consumption Market size in 2026 is estimated at 69.47 Billion liters, growing from 2025 value of 64.37 Billion liters with 2031 projections showing 101.67 Billion liters, growing at 7.92% CAGR over 2026-2031. The growth trajectory is anchored in hyperscale build-outs around Paris, mandatory waste-heat recovery for facilities above 1 megawatt, and cloud providers’ commitments to operate water-positive campuses before 2030. Intensifying sustainability disclosure rules have transformed water efficiency from a voluntary pledge into a compliance requirement, now influencing capital allocation toward liquid immersion and direct-to-chip systems. The rapid densification of artificial intelligence and high-performance computing (HPC) racks, many of which exceed 50 kilowatts, further accelerates the pivot away from evaporative towers toward closed-loop solutions capable of capturing heat for district networks. Government retrofit grants that cover up to 40% of qualifying capital outlays shorten payback periods, while artificial-intelligence-enabled monitoring helps operators hit increasingly stringent consumption caps. Collectively, these drivers position the France data center water consumption market as a bellwether for sustainable digital infrastructure across Europe.

Key Report Takeaways

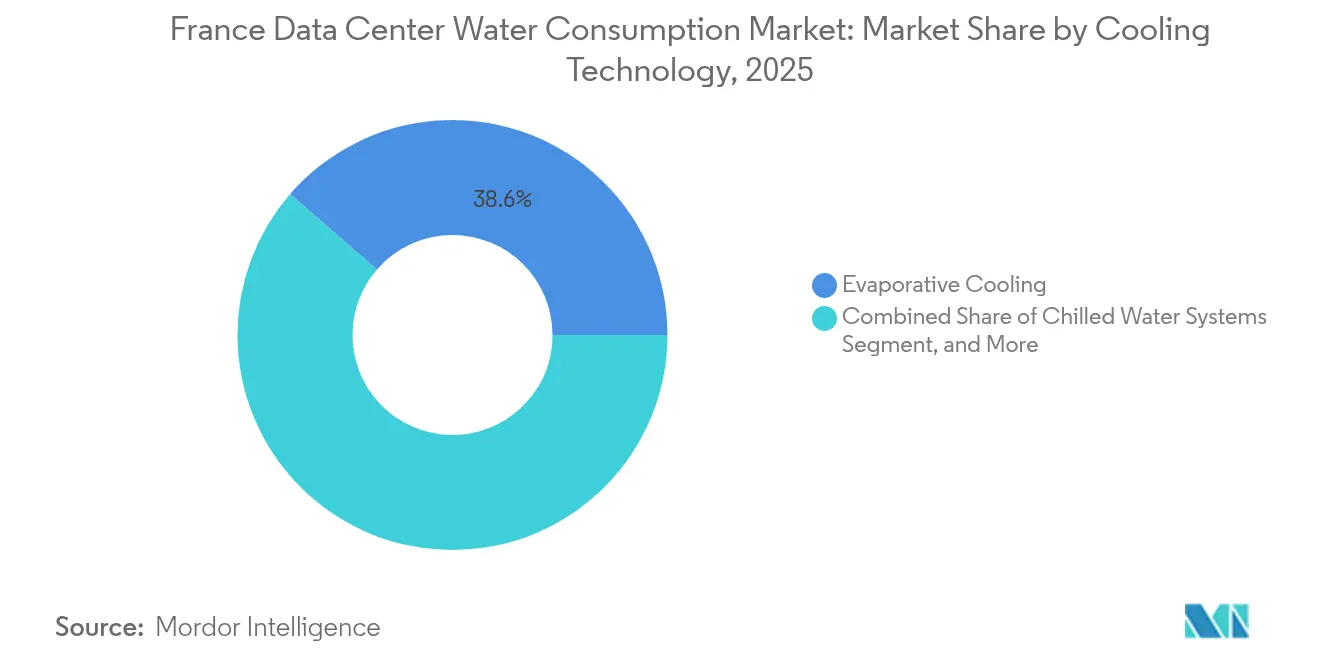

- By cooling technology, evaporative systems led with 38.62% of the France data center water consumption market share in 2025, whereas liquid immersion cooling records the fastest CAGR at 8.84% through 2031.

- By data center type, hyperscale data centers accounted for a 46.95% of the France data center water consumption market share in 2025, while edge and micro data centers are expected to expand at an 8.61% CAGR over 2026-2031.

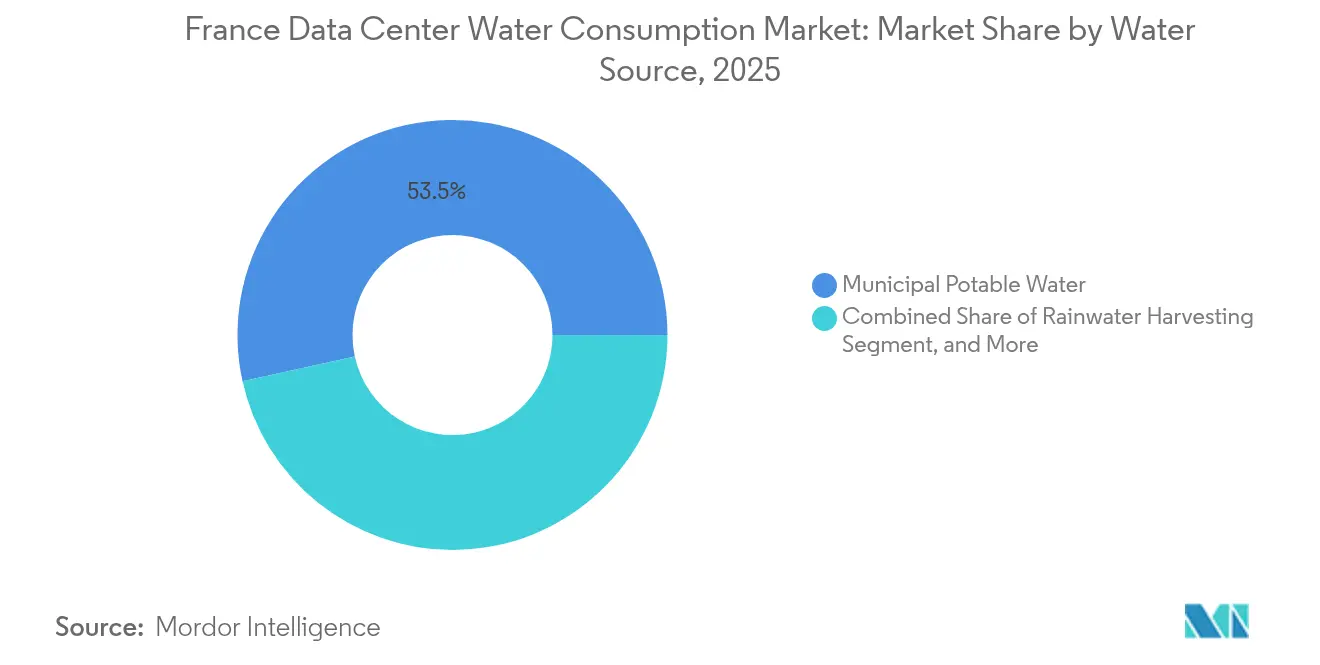

- By water source, municipal potable water supplies represented 53.45% of the France data center water consumption market share in 2025; rainwater harvesting is forecast to post an 8.48% CAGR to 2031.

- By end-user vertical, IT and telecom dominated with 42.25% of the France data center water consumption market share in 2025, whereas healthcare is projected to grow at 9.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Future direction is shaped by developments occurring across multiple countries and regions, with France contributing to the overall trajectory. The outlook on worldwide data center water consumption market reflects how these are expected to evolve collectively.

France Data Center Water Consumption Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Expansion of Hyperscale Facilities in Île-de-France | +1.8% | Île-de-France, with spillover to Marseille and Lyon metro areas | Medium term (2-4 years) |

| Government Incentives for Energy-Efficient Cooling Retrofits | +1.2% | National, with higher uptake in Paris, Lyon, Marseille | Short term (≤ 2 years) |

| Rise of Liquid Immersion Cooling Adoption | +1.5% | Global, with early deployments in hyperscale and HPC centers | Medium term (2-4 years) |

| Corporate Net-Zero Water Commitments by Cloud Providers | +1.0% | Global, concentrated in regions with hyperscale presence | Long term (≥ 4 years) |

| Deployment of AI for Real-Time Water Usage Optimization | +0.9% | Global, with faster adoption in Tier 3 and Tier 4 certified facilities | Short term (≤ 2 years) |

| Emergence of Seawater-Cooled Shoreline Data Centers | +0.6% | Coastal regions (Brittany, Provence-Alpes-Côte d'Azur) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Hyperscale Facilities in Île-de-France

Île-de-France continues to absorb the bulk of hyperscale investment, adding hundreds of megawatts of IT load each year as operators chase its robust fiber backbones and customer density. Newly enforced waste-heat recovery rules for sites exceeding 1 megawatt require a minimum 60% heat capture by 2027, prompting wholesale shifts toward liquid immersion and direct-to-chip setups that export 60 °C water to district networks.[1]Ministère de la Transition Écologique, “Green IT Initiative: Waste Heat Recovery Requirements for Data Centers,” ecologie.gouv.fr Microsoft’s 2024 pledge to eliminate potable-water use for new Azure campuses exemplifies the trend and has shortened payback periods on liquid cooling from seven years to under five. The resulting surge in liquid infrastructure orders positions Île-de-France as Europe’s proving ground for water-neutral hyperscale architecture.

Government Incentives for Energy-Efficient Cooling Retrofits

France’s National Agency for Ecological Transition reimburses up to 40% of capital spent on retrofits that cut water consumption per megawatt by at least 30%. Qualifying projects replace air-cooled chillers with adiabatic, direct-to-chip, or immersion technologies and often bundle Ecolab’s 3D TRASAR chemistry sensors to optimize tower cycles.[2]Ecolab, “3D TRASAR Technology for Cooling Tower Optimization,” ecolab.com Operators in water-stressed Mediterranean basins move the fastest because seasonal caps threaten uptime if efficiency targets are not met. These grants alter financial calculus for aging colocation sites, nudging them to accelerate replacement of evaporative towers.

Rise of Liquid Immersion Cooling Adoption

Immersion technology submerges servers in dielectric fluid, erasing the need for chillers and evaporative towers while delivering heat at district-compatible temperatures. Submer’s SmartPod racks installed at an HPC site in Lyon reached a 1.02 power-usage-effectiveness level and reclaimed 100% of waste heat for municipal networks.[3]Submer Technologies, “SmartPod Immersion Cooling Systems for Data Centers,” submer.com LiquidStack’s agreement with OVHcloud is set to slice water withdrawal by 40% on the Roubaix campus, validating capital-light retrofits over full greenfield builds. For rack densities above 50 kilowatts, immersion now offers the only path to achieving both thermal compliance and water-positive goals, positioning it as the fastest-growing solution in the France data center water consumption market.

Corporate Net-Zero Water Commitments by Cloud Providers

Amazon Web Services, Microsoft Azure, and Google Cloud aim to replenish more freshwater than they consume by 2030, aligning infrastructure roadmaps with community expectations and investor scrutiny. These pledges translate into procurement mandates that favor closed-loop equipment, greywater reuse, and rainwater capture. Google alone invested over USD 1 billion in wetland restoration and municipal upgrades tied to its French sites by 2024, creating local goodwill while diversifying water sources. Colocation providers that lag on stewardship risk losing anchor tenants as hyperscalers tighten audit criteria.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Costs of Closed-Loop Cooling Systems | -0.9% | Global, with higher impact in markets with legacy infrastructure | Medium term (2-4 years) |

| Stringent Regional Water-Withdrawal Regulations | -0.7% | France (Provence-Alpes-Côte d'Azur, Occitanie), with spillover to other water-stressed regions | Short term (≤ 2 years) |

| Limited Availability of Reclaimed Water Infrastructure | -0.5% | National, with acute gaps in suburban and rural areas | Long term (≥ 4 years) |

| Rising Public Scrutiny Over Industrial Water Usage | -0.6% | Global, with heightened sensitivity in drought-prone regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Costs of Closed-Loop Cooling Systems

Full liquid loops, heat exchangers, and redundant pumps drive upfront spend to over USD 50 million for a single hyperscale block, roughly 30% above air-cooled baselines. Smaller enterprise owners, often on five-year refresh cycles, hesitate to approve such outlays despite falling operating expenses. Although government grants offset as much as 40% of capex, sites already running efficient evaporative towers fail to meet the minimum 30% savings threshold. This gap prolongs dependence on water-intensive designs among legacy assets and hinders overall adoption rates within the France data center water consumption market.

Stringent Regional Water-Withdrawal Regulations

Water agencies in Provence-Alpes-Côte d’Azur and Occitanie now impose summer allotment caps, with surcharges climbing to EUR 5 per cubic meter (USD 5.65 per cubic meter) when drought emergencies are declared. Operators must reserve additional tank storage, negotiate contingency feeds, or throttle back expansion, which adds scheduling risk and potential cost overruns. The anticipated tightening of the EU Water Framework Directive by 2027 heightens the urgency to shift toward rainwater harvesting systems and closed-loop setups.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cooling Technology: Liquid Immersion Narrows the Gap

Evaporative towers generated the largest share of water usage in 2025, but immersion cooling’s 8.84% forecast CAGR positions it to outpace every rival technology. The France data center water consumption market size for immersion systems is expected to reach USD 20.07 billion by 2031, underscoring investor confidence in a solution that slashes water needs by up to 95%. Immersion also yields outlet temperatures of 60 °C, perfectly suited for mandated waste-heat recovery schemes, which provide it with regulatory tailwinds not available to chilled-water or hybrid solutions.

In practice, direct-to-chip plates offer a compromise for brownfield sites constrained by legacy rack formats, capturing up to 40% of waste heat while preserving serviceability. Adiabatic retrofits now qualify for state grants, driving penetration in midsize colocation facilities. Hybrid architectures, which toggle between free cooling and mechanical chillers based on ambient conditions, remain viable for enterprise campuses in temperate zones but face obsolescence when district heating partnerships require higher-grade heat output. Altogether, competitive dynamics indicate a gradual erosion of evaporative dominance, a theme mirrored in procurement pipelines across the France data center water consumption market.

By Data Center Type: Edge Capacity Gains Momentum

Hyperscale campuses still represent the lion’s share of absolute withdrawals, yet edge and micro sites lead relative growth, with an 8.61% CAGR to 2031. Their small, modular footprints typically favor sealed liquid loops or even fanless air systems, resulting in a per-megawatt water intensity close to zero. The France data center water consumption market share for edge deployments is forecast to rise from 11.35% in 2025 to 15.4% by 2031 as 5G, autonomous mobility, and real-time analytics demand sub-10 millisecond latencies.

Colocation providers juggle inter-tenant sustainability requirements, prompting the adoption of metered water dashboards and usage-based pricing. Enterprise data centers face an inflection point, retrofit or outsource. Liquid-ready racks, leak detection, and predictive maintenance platforms become decisive in retaining mission-critical loads. HPC centers, meanwhile, act as technology trailblazers, validating immersion designs that later trickle down to hyperscale builders, reinforcing the virtuous cycle within the France data center water consumption market.

By Water Source: Diversification Gains Priority

Potable utility feeds still dominate sourcing, but rainwater harvesting’s 8.48% CAGR shows a clear strategy shift. Operators in Brittany and Normandy capture rooftop runoff to cover up to 40% of cooling make-up water, aided by rainfall above 600 millimeters annually. The France data center water consumption market size for rainwater systems is projected to reach USD 7.82 billion by 2031, reflecting capital expenditure on storage tanks, filtration, and control software.

Greywater reuse is gaining momentum as municipal plants upgrade their tertiary treatment, while seawater and brackish options are finding niche adoption along the Atlantic and Mediterranean coasts. Regulatory incentives accelerate closed-loop adoption, with hyperscalers mandated to disclose liters per kilowatt-hour metrics as part of EU regulation. The resulting pivot diversifies risk and fortifies compliance readiness across the France data center water consumption market.

By End-User Vertical: Healthcare Accelerates Edge Build-Outs

IT and telecom entities retain top billing due to relentless content and cloud growth, yet healthcare’s 9.05% CAGR heralds a new set of location and cooling requirements. Real-time imaging, tele-surgery, and electronic health records operate most effectively within national borders, prompting hospital systems to install micro data centers with sealed liquid loops that prevent potable water draws.

Banking, financial services, and insurance firms modernize their trading and compliance platforms, spurring the adoption of hybrid cloud deployments. Government agencies outfit sovereign clouds under Green IT guidelines, often bundling waste-heat recovery into procurement criteria. Media, energy, e-commerce, and academia follow with workload-specific water profiles, collectively sustaining diversified demand patterns that anchor long-term resilience of the France data center water consumption market.

Geography Analysis

Île-de-France supports more than 700 megawatts of IT load and houses over 200 facilities, giving it primacy in both consumption volume and innovation cycles. Liquid immersion and direct-to-chip retrofits surge locally as operators rush to comply with the 2027 heat-recovery rule, making Paris a showcase for circular-economy data hubs. Municipal utilities actively partner in waste-heat offtake, easing grid strain and lowering community heating bills.

In Provence-Alpes-Côte d’Azur and Occitanie, drought episodes in 2022-2023 triggered withdrawal caps, prompting early rollouts of rainwater capture and AI-optimized chillers. Surcharges topping USD 5.65 per cubic meter shifted feasibility models toward closed-loop loops, and several hyperscalers postponed expansions until non-potable infrastructure was secured. Coastal corridors present opportunities for seawater-based cooling; however, impact assessments on marine ecology prolong approval times, prompting developers to explore floating or modular barge concepts.

Nationally, the EU Delegated Regulation 2024/1364 mandates uniform disclosure, making water stewardship a competitive differentiator. Operators boasting sub-0.2 liters per kilowatt-hour water-use effectiveness win preferred-supplier status with hyperscale tenants and gain access to favorable financing. As such, every region accelerates toward liquid systems and diversified sourcing, weaving a coherent narrative of rapid yet sustainable capacity escalation across the France data center water consumption market.

Analysis of the data center water consumption market by Mordor Intelligence spans multiple other regional evaluations across Europe, South America, and Asia, supported by country-level insights for Spain, United Kingdom, Brazil, United States, Canada, and Mexico, wherein local market conditions keep varying from one country to another.

Competitive Landscape

France’s supplier base blends century-old water majors with nimble cooling disruptors, creating a moderately fragmented arena. Veolia Environnement and Suez combine plant engineering, treatment chemistry, and digital twins, such as Hubgrade and Aquadvanced, to offer turnkey programs that reduce withdrawals by up to 70%. Pure-play innovators, LiquidStack, Submer Technologies, Iceotope Technologies, and Green Revolution Cooling, compete on thermodynamics and payback speed, often securing reference sites with hyperscalers aiming for zero-water loops.

Ecolab adds chemistry expertise, delivering 3D TRASAR deployments that reduce blowdown 20-30%, indirectly cutting water and chemical spend. Schneider Electric, Alfa Laval, and Pentair supply the control systems and heat exchangers that integrate with liquid setups, while Nautilus Data Technologies demonstrates seawater feasibility with its floating platforms. Strategic alliances, such as Microsoft-Iceotope, signal a paradigm shift toward liquid architectures that marry water neutrality with grid-interactive heat exports. Overall, firms that bundle treatment, monitoring, and compliance reporting into a single stack gain an edge as disclosure obligations intensify within the France data center water consumption market.

France Data Center Water Consumption Industry Leaders

Ecolab Inc.

Veolia Environnement SA

Suez SA

Xylem Inc.

SPX Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Schneider Electric and Veolia launched a joint digital-twin service that links EcoStruxure analytics with Hubgrade monitoring, delivering an additional 20% water-efficiency gain across five Parisian colocation sites in the first operational quarter.

- August 2025: OVHcloud finalized the LiquidStack immersion-cooling retrofit of its Roubaix campus, achieving a verified 45% reduction in potable-water usage while exporting 12 MW of recovered heat to the municipal district network.

- May 2025: Google completed a EUR 120 million (USD 128 million) wetland restoration near Saint-Quentin to replenish 2.5 million m³ of groundwater annually, fully offsetting the planned consumption of its forthcoming French hyperscale campus.

- March 2025: Suez introduced its Aquadvanced Data Center module and deployed the platform at an Orange facility in Marseille, enabling real-time flow optimization that is projected to cut cooling-loop potable-water draw by 25% within the first year.

France Data Center Water Consumption Market Report Scope

The France Data Center Water Consumption Market Report is Segmented by Cooling Technology (Liquid Immersion Cooling, Direct-To-Chip Liquid Cooling, Evaporative Cooling, Chilled Water Systems, Adiabatic Cooling Systems, Hybrid Cooling Solutions), Data Center Type (Hyperscale Data Centers, Colocation Data Centers, Enterprise/Corporate Data Centers, Edge/Micro Data Centers, High Performance Computing Centers), Water Source (Municipal Potable Water, Greywater/Reclaimed Water, Seawater/Brackish Water, Rainwater Harvesting, Closed-Loop Water Systems), End User Vertical (IT and Telecom, Banking Financial Services and Insurance, Government and Public Sector, Healthcare, Energy and Utilities, Media and Entertainment, E-Commerce and Retail, Research and Academia), and Geography (France). The Market Forecasts are Provided in Terms of Value (USD).

| Liquid Immersion Cooling |

| Direct-to-Chip Liquid Cooling |

| Evaporative Cooling (Cooling Towers) |

| Chilled Water Systems |

| Adiabatic Cooling Systems |

| Hybrid Cooling Solutions |

| Hyperscale Data Centers |

| Colocation Data Centers |

| Enterprise/Corporate Data Centers |

| Edge/Micro Data Centers |

| High Performance Computing Centers |

| Municipal Potable Water |

| Greywater/Reclaimed Water |

| Seawater/Brackish Water |

| Rainwater Harvesting |

| Closed-Loop Water Systems |

| IT and Telecom |

| Banking Financial Services and Insurance |

| Government and Public Sector |

| Healthcare |

| Energy and Utilities |

| Media and Entertainment |

| E-commerce and Retail |

| Research and Academia |

| By Cooling Technology | Liquid Immersion Cooling |

| Direct-to-Chip Liquid Cooling | |

| Evaporative Cooling (Cooling Towers) | |

| Chilled Water Systems | |

| Adiabatic Cooling Systems | |

| Hybrid Cooling Solutions | |

| By Data Center Type | Hyperscale Data Centers |

| Colocation Data Centers | |

| Enterprise/Corporate Data Centers | |

| Edge/Micro Data Centers | |

| High Performance Computing Centers | |

| By Water Source | Municipal Potable Water |

| Greywater/Reclaimed Water | |

| Seawater/Brackish Water | |

| Rainwater Harvesting | |

| Closed-Loop Water Systems | |

| By End User Vertical | IT and Telecom |

| Banking Financial Services and Insurance | |

| Government and Public Sector | |

| Healthcare | |

| Energy and Utilities | |

| Media and Entertainment | |

| E-commerce and Retail | |

| Research and Academia |

Key Questions Answered in the Report

How large is the France data center water consumption market in 2026?

The France data center water consumption market size is valued at USD 69.47 billion in 2026.

What CAGR is forecast for France’s data center water usage spending between 2026 and 2031?

Spending is projected to rise at an 7.92% CAGR over the 2026-2031 period.

Which cooling technology is growing the fastest in France?

Liquid immersion cooling leads growth with a 8.84% CAGR thanks to near-zero water usage and waste-heat recovery capabilities.

Why is rainwater harvesting gaining traction among French data centers?

Operators adopt rainwater systems to mitigate potable-water caps, comply with EU reporting rules, and cut utility costs, especially in high-rainfall regions.

How do government incentives support retrofit projects?

France reimburses up to 40% of qualified capital costs when retrofits reduce water consumption per megawatt by at least 30%, shortening payback timelines.

What regions outside Paris are important for future water-efficient data centers?

Provence-Alpes-Côte d’Azur, Occitanie, Brittany, and Normandy are focal points due to drought exposure, coastal cooling opportunities, or high rainfall.

Page last updated on: