Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

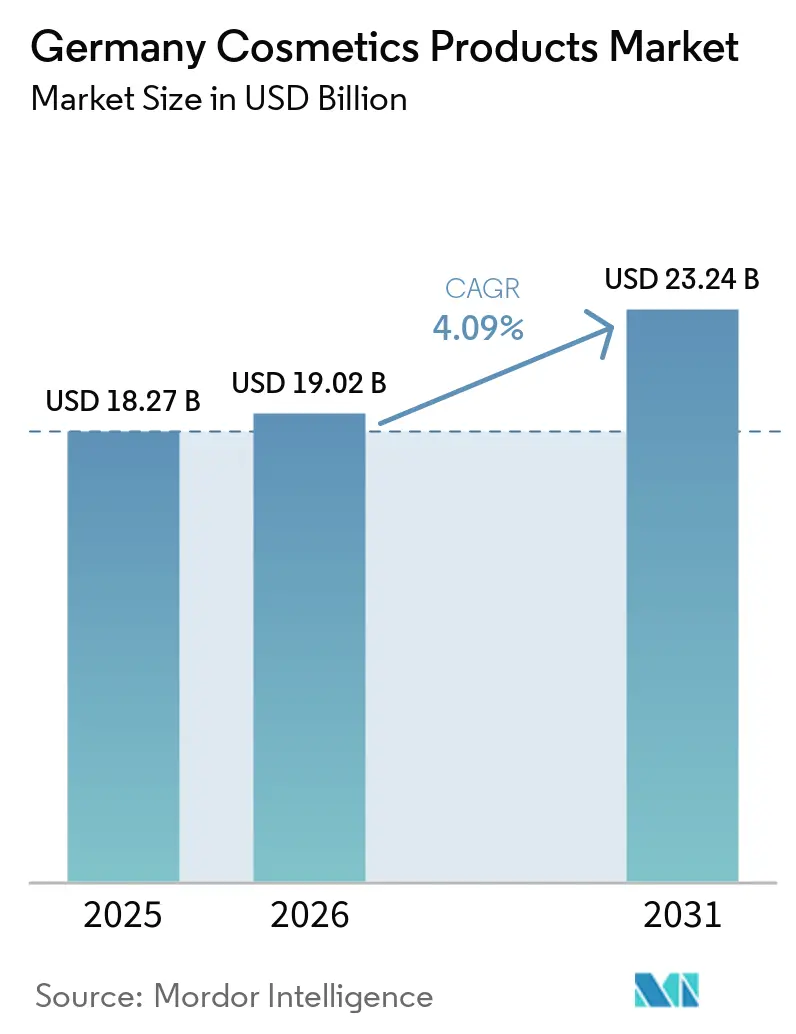

| Base Year Market Size (2025) | USD 18.27 Billion |

| Market Size (2026) | USD 19.02 Billion |

| Market Size (2031) | USD 23.24 Billion |

| Growth Rate (2026 - 2031) | 4.09% CAGR |

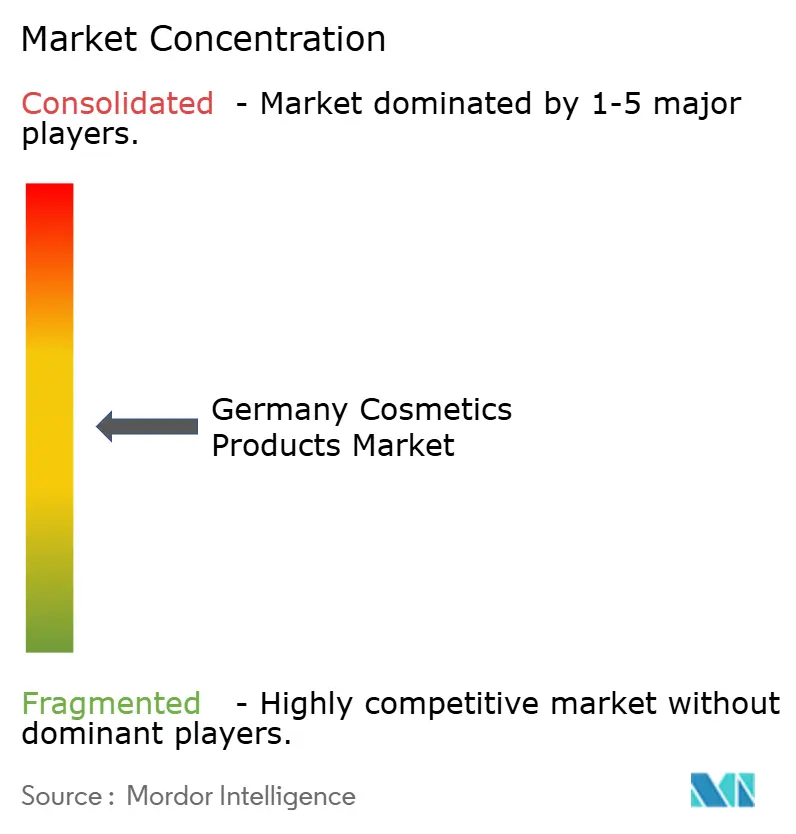

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Germany Cosmetics Products Market Analysis by Mordor Intelligence

The Germany cosmetics products market size in 2026 is estimated at USD 19.02 billion, growing from 2025 value of USD 18.27 billion with 2031 projections showing USD 23.24 billion, growing at 4.09% CAGR over 2026-2031. There's a noticeable tilt towards premium formulations, a digital-first approach to distribution, and a demand for ingredient transparency. Local players are adeptly navigating tighter EU chemical restrictions. As consumers become more health-conscious, there's a heightened interest in probiotic and microbiome-friendly products, especially those that bolster skin hydration and barrier function. Premium brands are leveraging clinically validated ingredients, refillable packaging, and endorsements from dermatologists. In contrast, mass brands are focusing on depth through private labels and competitive pricing to maintain their volume. Notable growth areas include lip and nail makeup, natural and organic products, and AI-driven personalization. However, challenges like supply-chain volatility and impending bans on PFAS and microplastics are driving up compliance costs. To counteract the rise of private labels, brands are increasingly adopting strategies centered around omnichannel ecosystems, epigenetic skin diagnostics, and consolidating in the prestige dermocosmetics space.

Key Report Takeaways

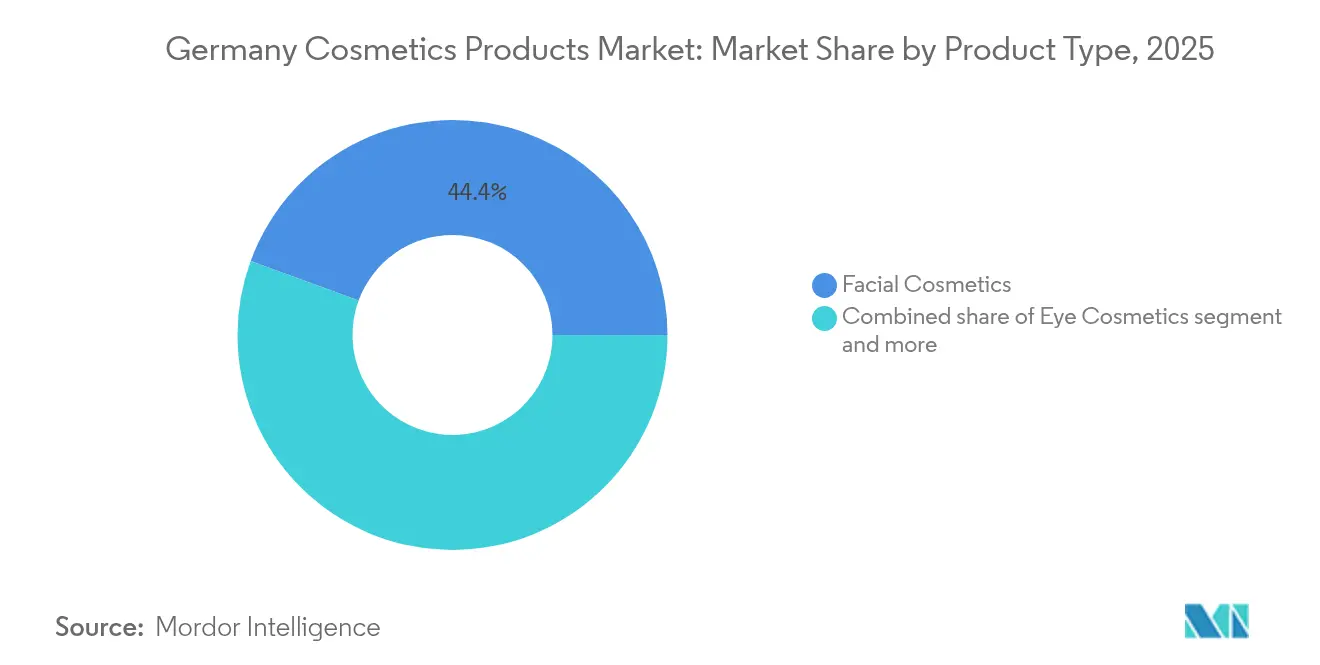

- By product type, facial cosmetics led with 44.40% of Germany's cosmetics products market share in 2025, whereas lip and nail makeup is forecast to advance at a 4.66% CAGR through 2031.

- By category, mass products held 61.70% of 2025 revenue, while premium products are projected to grow at a 5.07% CAGR to 2031.

- By ingredient type, conventional and synthetic inputs commanded 72.35% of 2025 sales, yet natural and organic offerings will expand at a 4.97% CAGR over the forecast window.

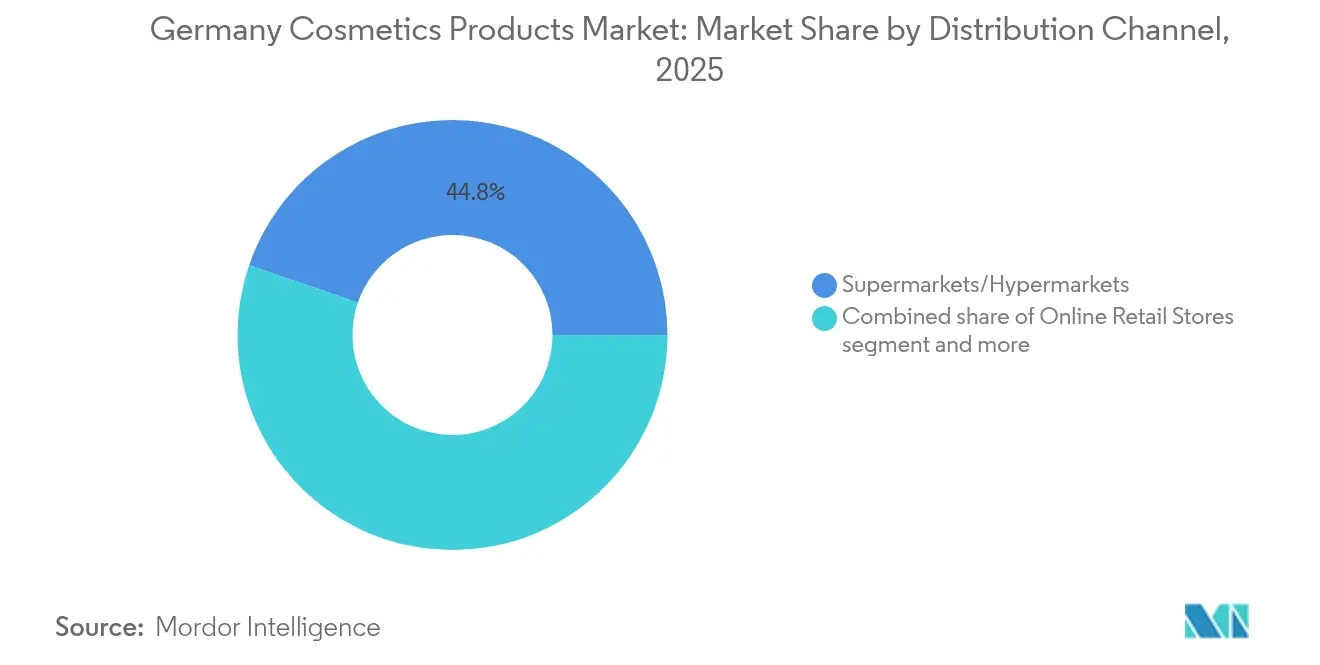

- By distribution channel, supermarkets and hypermarkets captured 44.75% of the 2025 value, but online retail is set to post a 5.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Cosmetics Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Social media influence boosting market demand | +0.6% | Germany | Short term (≤ 2 years) |

| Clean and organic beauty demand among Millennials and Gen Z | +0.7% | Germany, particularly urban centers (Berlin, Munich, Hamburg) | Medium term (2-4 years) |

| Technological advancements in product formulations | +0.5% | Germany, with R and D hubs in Hamburg and Düsseldorf | Long term (≥ 4 years) |

| Premiumisation of German beauty routines | +0.6% | Germany, strongest in metropolitan areas | Medium term (2-4 years) |

| AI-powered personalization boosting demand | +0.4% | Germany, early adoption in e-commerce channels | Short term (≤ 2 years) |

| Increasing disposable income driving market expansion | +0.5% | Germany | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Social media influence boosting the market

Beauty brands are increasingly leveraging platform-native content to streamline product discovery processes and elevate niche brands that lack a presence in traditional retail channels. According to Meta, the focus of influencer partnerships is shifting towards micro-tier creators, who have follower counts ranging from 10,000 to 50,000. These micro-influencers deliver a significantly higher engagement rate of 6.7%, compared to the 1.9% achieved by celebrity endorsements. This makes them a highly cost-effective option for premium brands to promote their products. This evolving trend benefits agile market entrants capable of rapidly adapting their product formulations based on real-time consumer feedback, thereby challenging established players to accelerate their product launch timelines. Additionally, the growing number of internet users is driving increased social media engagement. For instance, in 2024, an impressive 94% of Germany's population is reported to be internet users, according to data from the World Bank[1]Source: World Bank, " Individuals using the Internet", worldbank.org.

Clean and organic beauty demand among millennials and gen Z

Millennials and Gen Z are fueling the growth of Germany's cosmetics market, with a pronounced demand for clean and organic beauty products. These younger demographics prioritize cosmetics made from natural, non-toxic, and sustainably sourced ingredients, underscoring their commitment to environmental and health issues. They're not just conscious consumers; they're also willing to pay a premium for cosmetics that are cruelty-free, eco-friendly, and ethically produced, aligning with their values of wellness and sustainability. In 2024, data from Statistisches Bundesamt revealed that 38.13 million Germans aged 21-39 were driving this trend [2]Source: Statistisches Bundesamt, " Population by age groups", destatis.de. This demographic is also at the forefront of market innovation, urging companies to roll out personalized and multifunctional organic skincare solutions tailored to specific concerns, be it sensitive skin or anti-aging. Furthermore, German consumers under 35 are particularly discerning, willing to pay extra for products devoid of parabens, sulfates, and synthetic fragrances, especially when backed by third-party certifications like NATRUE or Ecocert. In a move underscoring the industry's shift towards transparency, Beiersdorf's Eucerin and L'Oréal's Garnier both introduced EcoBeautyScore labels in July 2025. These labels, offering A-to-E environmental ratings akin to France's Nutri-Score for food, set a new standard in the market.

Technological advancements in product formulations

Innovation in active ingredients is increasingly centered on anti-glycation peptides and epigenetic modulators, which target cellular aging pathways beyond surface hydration. In 2024, Beiersdorf introduced its Q10 Dual Action Serum, incorporating Glycostop, a novel anti-glycation ingredient derived from natural amino-hydroxyl-pyranone (NAHP). The company claims the product achieves a 27% reduction in advanced glycation end-products after 8 weeks of use. At Cosmet'Agora 2025, BASF presented 14 new cosmetic actives, including bio-fermented squalane with 98% purity and encapsulated retinoids that reduce irritation by 40% compared to conventional formulations. Symrise reported double-digit growth in its Cosmetic Ingredients division for fiscal 2024, driven by increased demand for microbiome-friendly preservatives and sensory modulators that improve texture without silicones. These advancements add complexity to formulations, favoring vertically integrated manufacturers with in-house research and development over contract fillers, while enabling premium pricing to offset rising raw material costs.

Premiumisation of German beauty routines

German consumers, influenced by dermatologist-endorsed routines on social media, are consolidating their SKU counts while simultaneously increasing their per-unit spending. In fiscal 2023/24, Douglas's premium beauty sales surged by 9.2%, outpacing its mass segment by a notable 4.1 percentage points. This uptick was driven by a noticeable shift in shopper preferences towards serums priced above EUR 50 and clinical-grade sunscreens. Meanwhile, Henkel's premium hair-care line, led by Schwarzkopf Professional, boasted a 6.9% organic growth in fiscal 2024, in stark contrast to its stagnating mass brands. Distribution channels are also feeling the impact of this trend: specialty perfumeries and pharmacies now account for 68% of premium transactions, while supermarkets continue to dominate the mass market. Refillable packaging is gaining traction as a tool for premiumization. In 2024, Beiersdorf introduced refill stations for Nivea body lotions in 50 dm stores, and the initiative saw a commendable 19% repurchase rate among those who tried it. This wave of premiumization not only shields brands from the encroachment of private labels but also tightens their focus to a more affluent customer base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU microplastics and PFAS ingredient bans | -0.3% | Germany, aligned with EU-wide regulations | Medium term (2-4 years) |

| Consumer concerns about chemical ingredients | -0.2% | Germany, particularly among Millennials and Gen Z | Short term (≤ 2 years) |

| Rising concerns over counterfeit products | -0.3% | Germany, highest seizure rates in OECD | Short term (≤ 2 years) |

| Ingredient and packaging supply-chain volatility | -0.4% | Germany | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU microplastics and PFAS ingredient bans

In 2024, the European Chemicals Agency introduced restrictions on microplastics. Rinse-off products containing polyethylene and polypropylene beads will be prohibited by October 2027, with leave-on cosmetics facing a ban by 2029. Concurrently, the EU is addressing per- and polyfluoroalkyl substances (PFAS) in items such as waterproof mascaras and long-wear foundations, with implementation set for 2027. Reformulating these products entails significant costs: replacing PFAS with bio-derived film-formers requires 18-24 months of stability testing and regulatory updates, costing major brands approximately EUR 40 million. Henkel disclosed in its 2024 report that it allocated EUR 22 million to reformulate Fa deodorants and Schauma shampoos ahead of the microplastics deadline. Smaller brands, without in-house toxicology teams, face greater compliance challenges, potentially leading to exits or acquisitions. Additionally, the bans reduce product differentiation; without PFAS, waterproof mascaras may experience a 30-40% decline in wear-time, eroding the distinctiveness of a premium category.

Consumer concerns about chemical ingredients

Ingredient skepticism is expanding beyond niche wellness communities and gaining traction among mainstream consumers, primarily due to the widespread dissemination of toxicology studies and the influence of "clean beauty" advocates on social media. A 2024 survey conducted by the European Commission highlighted that 63% of German consumers now actively avoid products containing synthetic fragrances, parabens, or phthalates, a notable rise from 51% in 2022 [3]Source: European Commission, "Autumn 2025 Economic Forecast" europa.eu. This shift reflects a growing awareness and concern about product ingredients. Paradoxically, this heightened ingredient anxiety has also driven increased interest in chemist-founded brands. These brands, despite utilizing synthetic actives, emphasize transparency in communicating their safety profiles. This trend underscores the importance of consumer education, suggesting that providing clear and accurate information about ingredient safety may be a more effective approach than the outright elimination of synthetic components.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Facial Cosmetics Lead, Lip and Nail Accelerate

Lip and nail makeup products will register the fastest expansion at 4.66% CAGR from 2026 to 2031, outpacing facial cosmetics despite the latter's commanding 44.40% share in 2025. The increasing demand for lip and nail products is primarily attributed to Gen Z consumers, who favor bold and trend-driven color cosmetics. These products typically have a rapid turnover cycle of 6-8 weeks, fueled by social media virality that accelerates product lifecycles. This dynamic encourages impulse purchases, particularly in the lip and nail categories. On the other hand, facial cosmetics, supported by products like anti-aging serums and SPF moisturizers, continue to benefit from favorable demographic trends, ensuring steady growth.

Eye cosmetics occupy an intermediate position in the market. While sales of traditional products like mascara and eyeliner have stabilized, there is a growing consumer preference for semi-permanent solutions such as lash extensions and microblading. These alternatives reduce the need for daily makeup application, signaling a shift in consumer behavior. In the facial cosmetics segment, Beiersdorf's Q10 Dual Action Serum exemplifies the industry's move toward multifunctional formulations. This product, which combines anti-glycation peptides with hyaluronic acid, demonstrates the ability to command premium price points ranging from EUR 30 to EUR 50. However, the lip and nail segment faces potential challenges due to the European Union's PFAS ban. This regulation is expected to disproportionately impact long-wear lip formulations, potentially slowing the segment's growth trajectory after 2027. The adoption of bio-based film-formers that can deliver comparable performance will be critical to mitigating this impact and sustaining growth in the segment.

By Category: Premium Gains Share as Mass Defends Volume

Germany's premium cosmetics segment is projected to grow at a CAGR of approximately 5.07% through 2031, narrowing the revenue gap with mass-market offerings. In 2025, mass-market products represented about 61.70% of the total cosmetics revenue. This trend towards premiumization indicates a shift in consumer focus from quantity to quality. There's a rising appetite for high-performance, technologically advanced, and experience-centric products. Key drivers of this growth include increasing disposable incomes, particularly in metropolitan and affluent areas, enabling consumers to spend more on premium beauty items. Millennials and Gen Z, who place a high value on self-care and wellness, are at the forefront of this shift, actively seeking products with innovative formulations, personalized touches, and enhanced sensory experiences.

While mass-market products continue to dominate, bolstered by private-label penetration and widespread availability in drugstores, the premium segment's growth is notably concentrated in metropolitan hubs like Berlin, Munich, and Hamburg, where household incomes are higher. In contrast, mass products hold sway in smaller cities and rural areas. Although the divide between mass and premium segments is likely to endure, there's a notable trend towards hybrid models, blending premium ingredients with mass-market packaging.

By Ingredient Type: Natural and Organic Gain Despite Synthetic Dominance

In 2025, conventional and synthetic ingredients contributed to 72.35% of the total revenue. However, natural and organic formulations are projected to grow at a compound annual growth rate (CAGR) of 4.97%, primarily fueled by the increasing demand from Millennials and Gen Z consumers. These demographics are particularly drawn to COSMOS-certified and vegan-labeled products, reflecting a shift in consumer preferences toward sustainability and ethical sourcing. In July 2025, Beiersdorf and L'Oréal launched EcoBeautyScore labels, which assign environmental ratings ranging from A to E. This initiative aims to institutionalize transparency within the industry while encouraging companies lagging in sustainability efforts to reformulate their products.

Synthetic ingredients maintain their dominance due to their stability and effectiveness, especially in active-driven products like anti-aging serums and sunscreens. BASF's encapsulated retinoids, highlighted at Cosmet'Agora 2025, boast a 40% reduction in irritation compared to natural counterparts, making them a premium choice for dermocosmetics. Meanwhile, Symrise experienced double-digit growth in 2024, thanks to their microbiome-friendly synthetic preservatives, which excel in broad-spectrum antimicrobial activity over natural alternatives. The distinction between natural and synthetic is becoming less clear: for instance, bio-fermented squalane, produced from sugarcane through synthetic biology, meets COSMOS's natural classification, yet boasts a 98% purity level that's hard to achieve from traditional sources like shark liver or olive.

By Distribution Channel: Online Retail Surges as Supermarkets Hold Ground

In 2025, supermarkets and hypermarkets accounted for 44.75% of the distribution market share, maintaining their dominance in the mass-market segment. However, online retail stores are projected to grow at a compound annual growth rate (CAGR) of 5.31%, making them the fastest-growing distribution channel. This growth is primarily driven by advancements in AI-powered diagnostics and virtual try-on tools, which have significantly reduced return rates by enhancing the online shopping experience. A notable example is Beiersdorf's O.W.N platform, which operates exclusively online. The platform has demonstrated the potential of digital channels to command premium pricing by achieving an average transaction value of EUR 150. This success is attributed to its innovative approach of bundling epigenetic skin analysis with customized serums, catering to consumers seeking personalized skincare solutions.

Specialty stores, particularly perfumeries and pharmacy chains, continue to play a crucial role as discovery hubs for premium brands that rely on in-person consultations to engage customers effectively. These stores provide a tactile and personalized shopping experience, which is essential for high-end products. On the other hand, supermarkets and hypermarkets are defending their market share by expanding their private-label offerings. For instance, dm-drogerie has increased its private-label penetration, while Rossmann introduced e.l.f. Cosmetics in 2024, catering to mass-market consumers seeking affordable yet quality products. These strategies offer shoppers the convenience of one-stop shopping while providing cost-effective alternatives to branded products. The distribution channel landscape is becoming increasingly polarized. Online platforms and specialty stores are capitalizing on the trend of premiumization, attracting consumers willing to pay a premium for quality and personalization. In contrast, supermarkets and hypermarkets are solidifying their position by focusing on mass-market volume. This evolving dynamic has left mid-tier department stores vulnerable, as they struggle to compete with the distinct value propositions offered by both premium and mass-market channels.

Geography Analysis

Germany's cosmetics market, while embedded in the broader European regulatory and competitive landscape, demonstrates distinctive consumer behaviors. These behaviors are heavily influenced by a retail environment dominated by drugstores and a strong inclination toward dermocosmetic brands. Premiumization trends are particularly evident in metropolitan areas such as Berlin, Munich, and Hamburg. In these cities, high-income households significantly contribute to the growth of specialty perfumeries and the increasing adoption of niche fragrances. Conversely, rural regions and smaller cities exhibit varying consumption patterns, reflecting a more diverse market dynamic.

As the largest economy in the European Union, Germany plays a pivotal role in shaping regulatory trends that often extend their influence across neighboring markets. For instance, the European Chemicals Agency has finalized restrictions on microplastics, which are scheduled for implementation in 2027, alongside the anticipated ban on PFAS. Additionally, Germany's status as the OECD nation with the highest share of global counterfeit-goods seizures underscores the ongoing enforcement challenges. These challenges undermine consumer confidence in online marketplaces, particularly for high-value products such as premium fragrances and anti-aging serums, where authenticity is a critical concern.

Cross-border shopping is on the rise, with German consumers turning to French and Italian e-commerce platforms to discover niche brands absent from their domestic market. Simultaneously, Eastern European tourists are boosting in-store sales at perfumeries in Berlin and Munich. However, the landscape isn't without challenges. Skills shortages and high energy costs, both highlighted by the European Commission, are stifling manufacturing productivity. This limitation hampers brands' ability to absorb wage-driven cost inflation without denting their profit margins. Germany's strategic position at the heart of the EU has established it as a logistics nexus for continent-wide distribution. Yet, with 88% of EU FMCG manufacturers citing sourcing challenges in 2024, supply-chain volatility is causing delays in product launches and tightening inventory cycles. The confluence of stringent regulations, discerning consumers, and a fragmented retail scene casts Germany as a dual-edged sword: a fertile ground for clean-beauty innovations and a cautionary tale of compliance costs that could sideline smaller players.

Competitive Landscape

In Germany's cosmetics market, competition is structured yet moderately concentrated. Multinational corporations and domestic manufacturers play a pivotal role in shaping the market landscape by leveraging extensive research capabilities and introducing innovative products. Prominent players such as Beiersdorf AG, L'Oréal S.A., Coty Inc., The Procter and Gamble Company, and Unilever have established a strong foothold through their strategically located manufacturing facilities and research centers within Germany, enabling them to cater effectively to local and regional demand.

Technological integration across the value chain serves as a critical factor in differentiating competitors within the market. Companies are increasingly adopting artificial intelligence systems to deliver personalized product offerings, conducting advanced research on ingredients to enhance product efficacy, and developing comprehensive digital engagement platforms to strengthen consumer relationships. These technological advancements not only aim to improve customer retention rates but also focus on optimizing operational efficiency, thereby providing a competitive edge.

The market offers significant strategic opportunities in areas such as the development of sustainable packaging solutions, the integration of personalized beauty technologies, and the creation of specialized product formulations tailored to diverse consumer demographics. Emerging players are gaining traction by utilizing direct-to-consumer distribution models and implementing targeted digital marketing strategies. The competitive landscape is undergoing a systematic transformation, with a strong emphasis on environmental sustainability initiatives, the enhancement of digital infrastructure, and the validation of products through scientific research. Leading market participants demonstrate their success by effectively balancing investments in innovation with operational optimization, ensuring compliance with regulatory standards, and addressing the evolving preferences and needs of consumers.

Germany Cosmetics Products Industry Leaders

-

Beiersdorf AG

-

L'Oréal S.A.

-

Unilever PLC

-

The Procter and Gamble Company

-

Coty Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Beiersdorf, L'Oréal, and Coty have introduced the EcoBeautyScore labeling system across their European portfolios, assigning environmental ratings ranging from A to E. This initiative, similar to the Nutri-Score system used in the food industry, aims to establish sustainability transparency within the beauty market. The move may compel competitors to adopt comparable frameworks or risk facing consumer backlash.

- January 2025: e.l.f. Beauty launched its "e.l.f. von zehn" campaign in Germany, highlighting its affordable, high-performance products through a playful approach to beauty. The campaign featured products such as the Power Grip Primer and Glow Reviver Lip Oil.

- September 2024: Beiersdorf introduced its first epigenetic serum under the Eucerin brand, incorporating the company's patented skin-specific age clock technology. The technology utilizes an algorithm based on epigenetic patterns to measure the skin's biological age.

Germany Cosmetics Products Market Report Scope

Beauty and personal care products encompass a wide array of items used to enhance appearance, hygiene, and overall well-being. The demand for Germany Beauty And Personal Care Products is increasing as consumers prioritize premium skincare, wellness-focused formulations, and sustainable beauty solutions.

The market studied is segmented by product type, category, ingredient type, and distribution channel. By product type, the market is segmented into personal care products and cosmetic and make-up products. The personal care products segment is further segmented into hair care products, skincare products, bath & shower, oral care products, men’s grooming products, deodorants & antiperspirants, and perfumes and fragrances. The cosmetics/make-up products segment is further segmented into facial cosmetics, eye cosmetic products, and lip and nail makeup products. By category, the market studied is segmented into premium and mass products. By ingredient type, the market is segmented into natural & organic, and conventional/synthetic. By distribution channel, the market is segmented into specialist retail stores, supermarkets/hypermarkets, online retail channels, and other distribution channels. The market sizing has been done in value terms in USD for all the abovementioned segments.

By Product Type

| Facial Cosmetics |

| Eye Cosmetics |

| Lip and Nail Make-up Products |

By Category

| Premium Products |

| Mass Products |

By Ingredient Type

| Natural and Organic |

| Conventional/Synthetic |

By Distribution Channel

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Online Retail Stores |

| Other Channels |

| By Product Type | Facial Cosmetics |

| Eye Cosmetics | |

| Lip and Nail Make-up Products | |

| By Category | Premium Products |

| Mass Products | |

| By Ingredient Type | Natural and Organic |

| Conventional/Synthetic | |

| By Distribution Channel | Specialty Stores |

| Supermarkets/Hypermarkets | |

| Online Retail Stores | |

| Other Channels |

Key Questions Answered in the Report

What is the projected value of the Germany cosmetics products market in 2031?

The market is forecast to reach USD 23.24 billion by 2031.

Which product category is expanding fastest toward 2031?

Lip and nail makeup is expected to post a 4.66% CAGR, making it the fastest-growing segment.

How large is the premium share relative to mass products?

Mass items still generated 61.70% of 2025 revenue, but premium lines are expanding at a 5.07% CAGR and steadily closing the gap.

Which retail channel will grow quickest?

Online retail is predicted to rise at a 5.31% CAGR, the fastest among all channels.

Page last updated on: