Germany Green Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

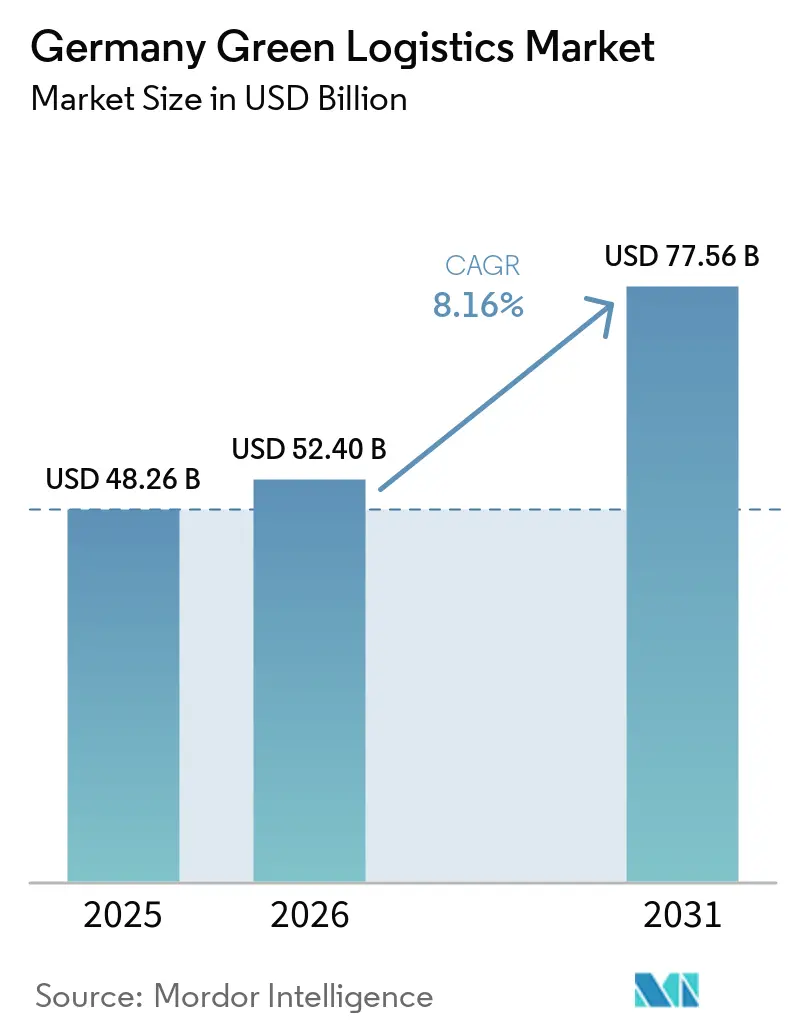

| Base Year Market Size (2025) | USD 48.26 Billion |

| Market Size (2026) | USD 52.40 Billion |

| Market Size (2031) | USD 77.56 Billion |

| Growth Rate (2026 - 2031) | 8.16% CAGR |

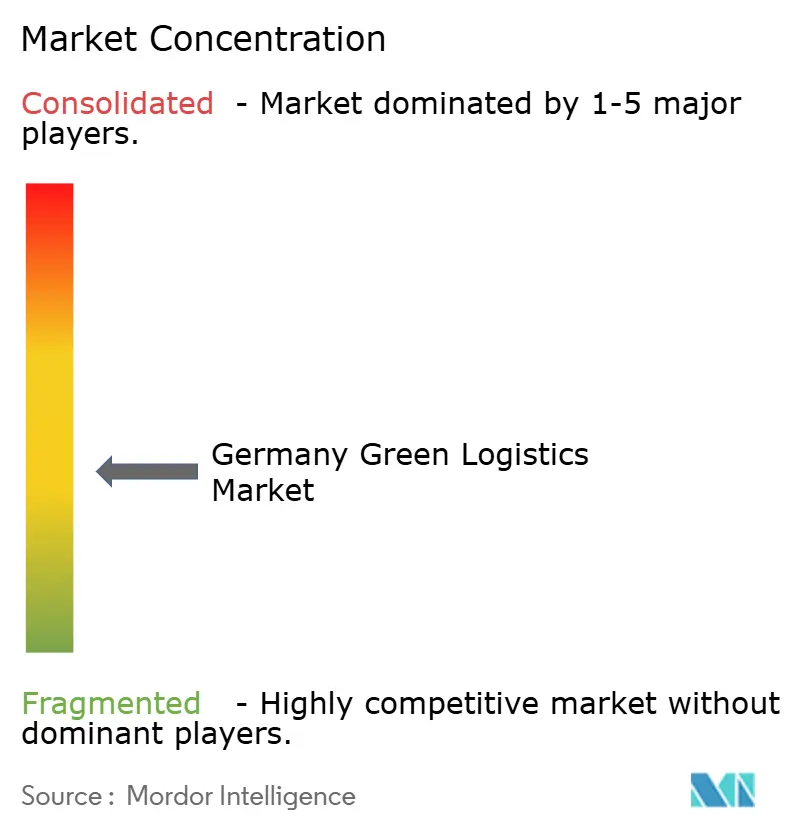

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Green Logistics Market Analysis by Mordor Intelligence

The Germany green logistics market size was valued at USD 48.26 billion in 2025 and is forecast to reach USD 52.40 billion in 2026 and USD 77.56 billion by 2031 at 8.16% CAGR from 2026 to 2031.

Tighter freight decarbonization rules, wider use of electric delivery fleets, and stronger shipper demand for measurable emissions cuts in transport contracts are shaping growth. The Germany green logistics market is also moving beyond vehicle replacement, as operators add carbon reporting tools, support for sustainable packaging, and energy upgrades across warehouse networks to stay relevant in bids and long-term contracts. Large logistics groups remain better placed to fund these changes, which gives them an edge in electrification, renewable power sourcing, and digital emissions tracking. At the same time, the Germany green logistics market still faces constraints from high fleet conversion costs, slower build-out of corridor charging and hydrogen infrastructure, and rail network disruptions that have held back the pace of the modal shift. Market opportunities remain strongest where operators can combine low-emission transport with verified reporting, flexible decarbonization products, and site-level energy efficiency improvements supported by official policy and customer commitments.

Key Report Takeaways

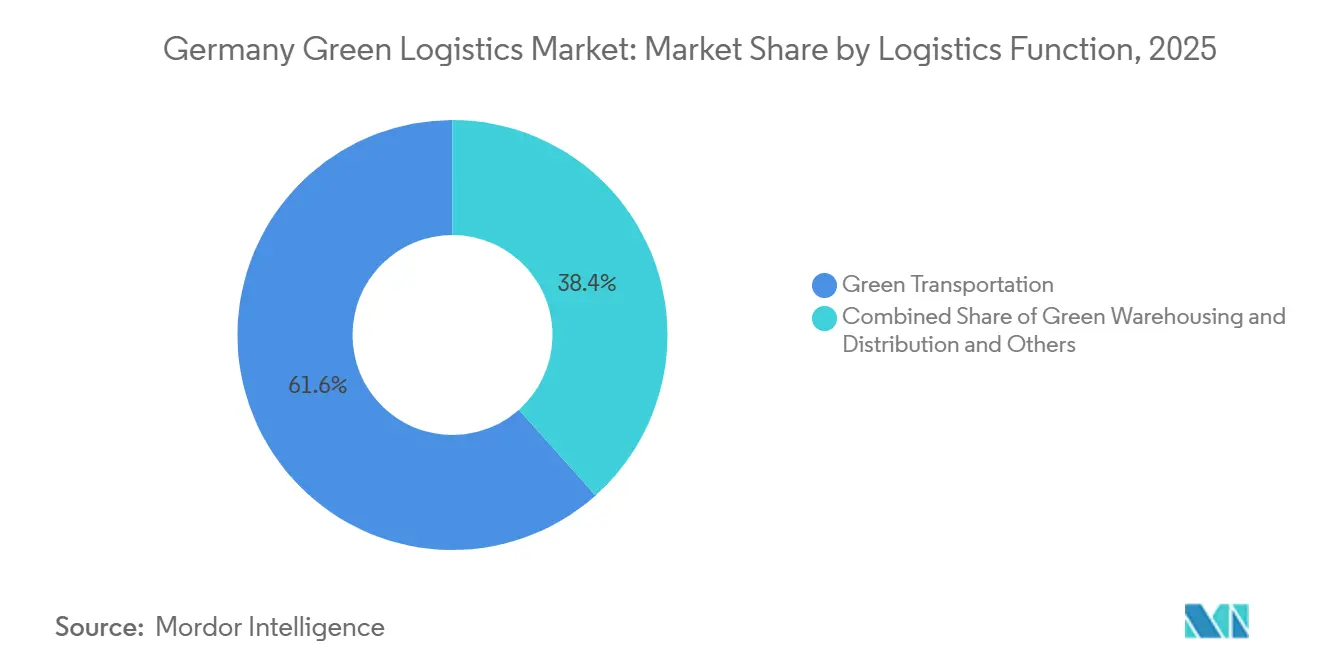

- By logistics function, green transportation accounted for 61.58% of the Germany green logistics market size in 2025, while green value-added services and others are projected to grow at 12.75% CAGR through 2031.

- By fuel and energy type, electric-powered logistics accounted for 47.80% of the Germany green logistics market share in 2025, while hydrogen-powered logistics is forecast to expand at 15.11% CAGR through 2031.

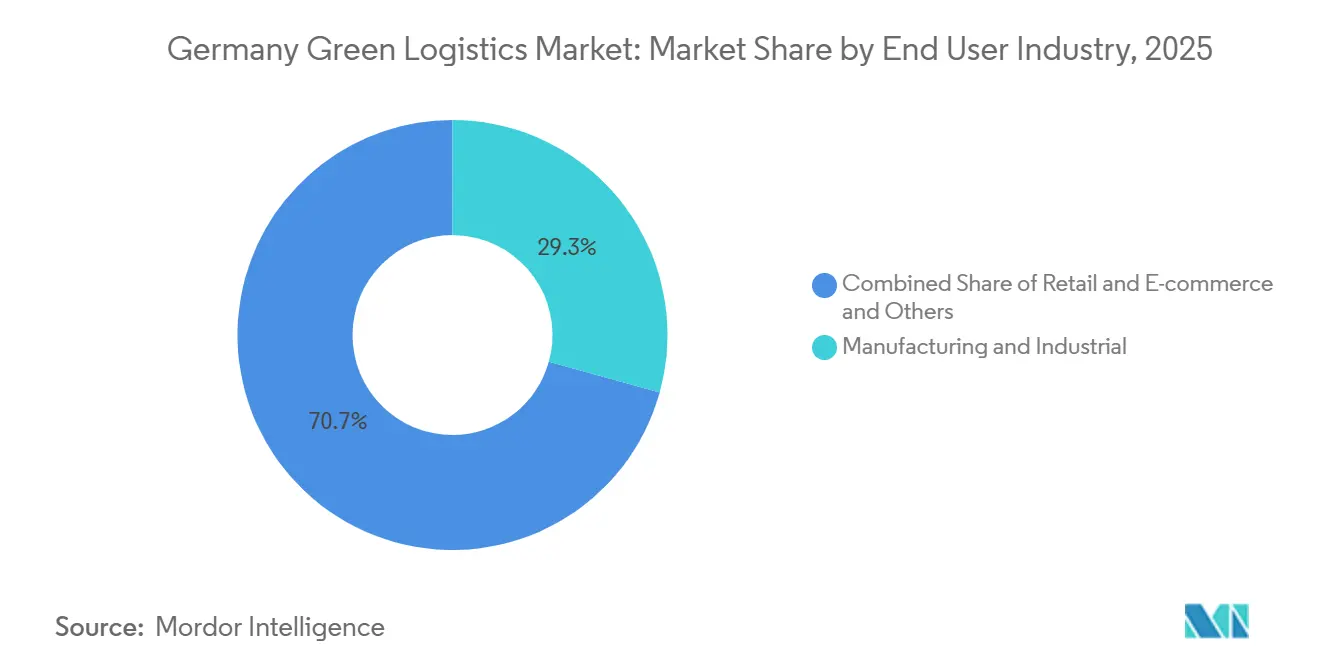

- By end-user industry, manufacturing and industrial captured 29.31% of the Germany green logistics market share in 2025, while retail and e-commerce are set to record the highest growth at 13.58% CAGR through 2031.

- By region, North Rhine-Westphalia represented 31.82% of Germany green logistics market size in 2025, while the Rest of States segment is projected to advance at 10.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Green Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Pressure On Freight Decarbonization And Reporting | +2.2% | Global, with the EU and Germany leading | Short term (≤ 2 years) |

| Fleet Electrification In Urban And Short-Haul Lanes | +1.8% | North Rhine-Westphalia, Bavaria, Baden-Württemberg | Medium term (2-4 years) |

| Rising Customer Demand For Low-Carbon Logistics Procurement | +1.4% | National, with a concentration in major industrial clusters | Medium term (2-4 years) |

| Intermodal Shift From Road To Rail And Inland Waterways | +0.8% | Rhine corridor, North Rhine-Westphalia, Hamburg hinterland | Long term (≥ 4 years) |

| Carbon-Aware Routing And Network Optimization Software | +0.7% | National, with early gains in Frankfurt, Hamburg, Munich | Short term (≤ 2 years) |

| Green Warehouse Retrofits And Energy Management Systems | +0.6% | National, with concentration in Ruhr, Rhine-Main, and Bavaria logistics hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Pressure on Freight Decarbonization and Reporting

Regulatory pressure now shapes daily operating choices across the Germany green logistics market. The EU heavy-duty vehicle CO2 framework keeps truck decarbonization on a fixed path, and FuelEU Maritime has applied a fuel greenhouse gas intensity reduction requirement for maritime transport since January 2025. Large shippers also need more detailed emissions data from logistics partners, which makes carbon reporting part of normal commercial qualification rather than a side service. This is pushing carriers to invest in measurement systems, auditable processes, and service offers that can support customer reporting obligations. The Germany green logistics market is therefore being shaped by compliance readiness as much as by physical transport assets.

Fleet Electrification in Urban and Short-Haul Lanes

Fleet electrification in city delivery and short-haul transport has moved into a visible scale in the Germany green logistics market. DHL Group expanded its electric fleet in Germany to 35,000 vehicles after adding 2,400 Ford Pro e-vans in July 2025, and the company said this supports zero-emission delivery across one-third of German postcodes[1]Source: International Post Corporation, “Milestone, 2,400 Ford Pro E-Vans Strengthen The Electric Delivery Fleet Of Deutsche Post And DHL In Germany,” International Post Corporation, ipc. be. Hermes Germany reached emission-free parcel delivery across more than 80 German city centers by the end of Q1 2026, with around 1,960 electric vehicles in service. These moves are raising the standard for urban logistics service quality in low-emission zones and dense delivery districts. They also widen the gap between large operators that can scale fleet conversion and smaller carriers that still rely on conventional assets.

Rising Customer Demand for Low-Carbon Logistics Procurement

Customer demand for lower-emission freight services is becoming more concrete in the Germany green logistics market. DHL Freight launched GoGreen Plus Flex in March 2026 and offers road freight customers fixed reduction tiers of 10%, 30%, and 80%, which shows that decarbonization is being sold as a defined commercial product rather than a general pledge. This kind of offer makes sustainability easier to compare inside procurement reviews, because customers can link service choice to a stated emissions outcome. Demand is also spreading beyond heavy industry, since retail and e-commerce customers increasingly want delivery and packaging choices that support their public climate commitments. The Germany green logistics market is therefore seeing demand growth not only from regulation but also from buyers seeking measurable, contract-ready emissions-reduction options.

Intermodal Shift from Road to Rail and Inland Waterways

Intermodal development remains an important long-term support for the Germany green logistics market. CargoBeamer took over terminal operations in Kaldenkirchen in April 2026 and began expansion work, expected to increase capacity to 200,000 units by 2027. That expansion matters because it adds semi-trailer rail-handling capacity in a key Rhine-Ruhr corridor where congestion and decarbonization pressures are both high. Intermodal assets also give operators another path to emissions reduction when direct fleet replacement is slower than expected. As this network develops, the Germany green logistics market should gain more options for combining road flexibility with lower-emission line-haul movement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Intensity Of Zero-Emission Fleets And Charging Infrastructure | -1.8% | National, with a pronounced impact on SME carriers in rural and suburban corridors | Short term (≤ 2 years) |

| Limited Hydrogen And High-Power Charging Availability On Freight Corridors | -0.7% | National, with hydrogen availability concentrated in the Rhine-Neckar and Düsseldorf regions | Medium term (2-4 years) |

| Higher Operational Complexity From Mixed-Fleet Transition And Payload Penalties | -0.5% | National, affecting operators across all fleet segments | Medium term (2-4 years) |

| Slow Payback For Sustainability Upgrades In Low-Margin Logistics Contracts | -0.4% | National, with a disproportionate impact on contract logistics and FTL operators | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Intensity of Zero-Emission Fleets and Charging Infrastructure

High upfront costs remain the clearest brake on wider adoption in the Germany green logistics market. Hellmann, DSV, and other operators benefited from the German federal KsNI support framework, and Hellmann linked its e-mobility rollout to that subsidy support before the program ended in 2025[2]Source: Hellmann Worldwide Logistics, “Best Practice In E-Mobility, Federal And State Government Officials Visit Hellmann,” Presseportal, presseportal.de. Dachser also stated in 2025 that vehicle acquisition costs remained high and public charging infrastructure for trucks was still scarce, even as the company expanded its electric fleet. This cost gap favors larger operators that can spread investment across bigger networks and longer contract books. Smaller carriers, therefore, face a slower transition path, even as customer demand for low-emission services rises.

Limited Hydrogen and High-Power Charging Availability on Freight Corridors

Infrastructure limits continue to slow long-distance decarbonization in the Germany green logistics market. In early 2026, commercially viable hydrogen pricing of EUR 8/kg (USD 8.8/kg) for heavy-duty trucking was available only in the Dusseldorf and Rhine-Neckar regions through the Hylane and H2 MOBILITY offer. That narrow regional availability shows how small the practical hydrogen network still is for national freight use. The same issue affects high-power charging because corridor coverage has not yet kept pace with the needs of large, long-haul truck fleets. As a result, urban and short-haul routes are moving faster, while long-distance trunk operations still depend heavily on future infrastructure build-out.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Logistics Function: Green Transportation Holds The Core Spend While Value-added Services Rise Faster

Green transportation accounted for 61.58% share in 2025, indicating that freight movement still accounts for the majority of spending in the Germany green logistics market size. This segment includes road, rail, air, and sea activity, and road electrification and intermodal rail projects are drawing much of the current operational attention. Green value-added services and others are projected to record the fastest growth at 12.75% CAGR through 2031, reflecting stronger demand for emissions data management, sustainable packaging support, and verification services. That shift shows that customers increasingly value proof, measurement, and process support alongside the transport task itself. In the Germany green logistics market, service design is changing: advisory and reporting work is becoming a paid add-on rather than a bundled extra.

Green warehousing and distribution sits between these two poles and is gaining relevance as operators upgrade site energy systems and local power generation. FIEGE expanded its photovoltaic system in Greven-Reckenfeld in 2025 to around 3,000 kWp, with annual generation of up to 2.4 GWh[3]Source: FIEGE Logistics, “FIEGE Expands PV System In Greven-Reckenfeld,” FIEGE Logistics, fiege.com. That kind of site investment lowers operating emissions and supports more resilient energy use in warehouses. The Germany green logistics industry is therefore moving from a transport-only transition to a broader operating model that includes data, facilities, and energy management within the service package.

By Fuel / Energy Type: Electric Solutions Lead Current Scale While Hydrogen Targets Heavy-Duty Growth

Electric-powered logistics accounted for 47.80% of Germany green logistics market share in 2025, making it the largest energy pathway. The lead comes from stronger deployment of battery-electric vans, trucks, and cargo bikes in urban delivery and short-haul distribution, where route predictability is better. Hydrogen-powered logistics is forecast to expand at a 15.11% CAGR through 2031, but it starts from a smaller base and still depends on progress in corridor infrastructure. This means the segment profile is split between mature urban electrification and an early-stage long-haul hydrogen build-out. The Germany green logistics market is therefore growing on a dual track, with battery-electric assets scaling now and hydrogen remaining more selective.

Biofuel-based logistics offers a practical middle ground for operators seeking lower emissions without immediate full-fleet replacement. CEVA Logistics said it operated more than 550 HVO100 and B100-powered trucks in Europe by the end of 2025 and was targeting 1,450 low-carbon fleet vehicles by year-end. This path suits operators that face long routes, asset constraints, or slower access to charging. The Germany green logistics industry still carries execution risk in electric logistics because battery supply, grid readiness, and capital discipline matter as much as demand growth.

By End-user Industry: Manufacturing Leads Current Demand While Retail And E-commerce Scale Faster

Manufacturing and industrial accounted for 29.31% of the market in 2025, making it the largest end-user group in the Germany green logistics market share. Germany’s industrial base in automotive, machinery, and chemicals supports that position because procurement standards increasingly require cleaner transport and greater emissions visibility. MAN Truck and Bus launched electric inbound logistics tenders for around 40 routes beginning in early 2025, and selected carriers started battery-electric operations on 8 of those routes. This shows how industrial customers are pushing logistics changes through formal sourcing decisions. It also explains why manufacturing remains the anchor customer group in the Germany green logistics market.

Retail and e-commerce are projected to grow at 13.58% CAGR through 2031 and are the fastest-growing end-user segments. The rise comes from expanding fulfillment activity and stronger pressure on consumer-facing brands to show lower-emission delivery options. That trend supports last-mile electrification, carbon-labeled transport products, and packaging changes that can be communicated clearly to end customers. Other end-user groups, such as healthcare, food and beverages, and chemicals, also matter. Still, their green logistics choices are shaped more by cost sensitivity, handling requirements, and sector-specific compliance needs. The Germany green logistics market is therefore broadening across end users, even though the spending base remains concentrated in industrial freight.

Geography Analysis

North Rhine-Westphalia held a 31.82% share in 2025, giving it the largest regional share in the Germany green logistics market size. The state benefits from dense industrial activity, deep warehousing, inland waterway links, and major freight corridors that support both road and intermodal operations. Kaldenkirchen adds to that role, as CargoBeamer began terminal expansion there in 2026 to increase capacity to 200,000 units by 2027[4]Source: CargoBeamer, “CargoBeamer Assumes Terminal Operations In Kaldenkirchen And Advances Expansion,” CargoBeamer, cargobeamer.com. FIEGE’s expanded photovoltaic installation in Greven-Reckenfeld also shows that North Rhine-Westphalia remains an active location for warehouse energy upgrades. These factors keep the region central to the operating base of the Germany green logistics market.

Bavaria and Baden-Wurttemberg form the next major regional cluster because both states combine large industrial demand with high-value logistics networks. Automotive and manufacturing flows support Bavaria, while Baden-Wurttemberg benefits from its supplier base and cross-border freight links. In January 2025, DB Schenker deployed 10 MAN eTGX electric trucks across 10 German locations and planned to integrate 100 eTGX trucks into its fleet by 2026, underscoring how large operators are spreading decarbonization assets across core logistics regions. This means the Germany green logistics market is still building first in regions where infrastructure, industrial demand, and operator scale already overlap.

The Rest of States segment is forecast to grow at a 10.46% CAGR through 2031, making it the fastest-growing geography in the Germany green logistics market share profile. Growth there is supported by lower current penetration, new logistics park development, and the spread of green warehousing beyond the traditional core hubs. Regional expansion also reflects the need to find lower-cost sites as operators add energy systems, charging assets, and newer buildings with better environmental performance. Over time, this should make Germany's green logistics market's national footprint less concentrated, even if the largest current volumes remain anchored in the main industrial states.

Competitive Landscape

The Germany green logistics market is moderately concentrated, with DHL Group, DSV, including DB Schenker, Kuehne+Nagel, Dachser, and Deutsche Bahn standing out through the scale of their sustainability programs and network assets. DSV completed its acquisition of DB Schenker in April 2025 for EUR 14.3 billion (USD 15.7 billion), further strengthening the market's top tier and combining two significant logistics platforms under one owner. Larger operators are also better placed to fund electric fleets, renewable power contracts, sustainable fuels, and reporting tools simultaneously. This matters because customers increasingly compare not only service quality, but also the credibility of decarbonization delivery. The Germany green logistics market, therefore, gives scale players a clear advantage in both operational transition and customer assurance.

Strategic moves in 2025 and 2026 show that market leaders are pushing on several fronts at once. DHL Freight introduced GoGreen Plus Flex in March 2026, turning emissions reduction into a priced transport option with three defined reduction tiers. Kuehne+Nagel and Hapag-Lloyd signed a joint sustainable ocean freight agreement in May 2026, which linked certified waste-based marine fuels to customer shipments on the East Asia to North Europe trade lane. DSV also worked with Microsoft, United Airlines, and Phillips 66 in April 2026 to unlock 11 million gallons of sustainable aviation fuel. These actions show that the Germany green logistics market is becoming more competitive in fuel sourcing, product design, and data-backed emissions reduction.

Challengers still have room to grow, especially by leveraging service innovation to offset their smaller physical scale. GEODIS received a CDP A rating in 2025, which strengthens its position in sustainability-led tendering and supports its credibility with multinational shippers. Kuehne+Nagel also reinforced its climate program in 2025 with upgraded science-based targets and a push toward 100% renewable electricity for all Contract Logistics sites. The Germany green logistics market still leaves open space in long-haul hydrogen and other less mature decarbonization niches, because no single operator has yet established a decisive operating lead there.

Germany Green Logistics Industry Leaders

DHL Group

DSV A/S (including DB Schenker)

Kuehne+Nagel

Dachser Group SE & Co. KG

Deutsche Bahn AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Kuehne+Nagel and Hapag-Lloyd signed their first joint sustainable ocean freight agreement, covering approximately 3,300 TEU on the East Asia-to-North Europe trade lane through certified waste-based Sustainable Marine Fuels (SMF), targeting avoidance of approximately 2,979 tons of CO₂ e emissions on a well-to-wake basis.

- April 2026: DSV, in collaboration with Microsoft, United Airlines, and Phillips 66, unlocked approximately 11 million gallons of Sustainable Aviation Fuel (SAF), expected to reduce lifecycle GHG emissions by approximately 100,000 tons CO₂ e compared to conventional jet fuel.

- March 2026: DHL Freight launched the GoGreen Plus Flex service, offering shippers three tiers of GHG reduction (10%, 30%, and 80% well-to-wheel) at variable pricing across all core road freight products. The commercial rollout extends DHL Freight's sustainability products beyond premium customers to businesses of all sizes.

- February 2026: Hapag-Lloyd and DSV signed a two-year Ship Green framework agreement for 18,000 tons CO₂ e of emission reductions via second-generation biofuels, with contracted delivery starting in 2026.

Germany Green Logistics Market Report Scope

| Green Transportation | Road |

| Air | |

| Sea and Inland Waterways | |

| Rail | |

| Green Warehousing & Distribution | |

| Green Value-added Services and Others |

| Electric-Powered Logistics |

| Biofuel-Based Logistics |

| Hydrogen-Powered Logistics |

| Others |

| Retail & E-commerce |

| Manufacturing & Industrial |

| Automotive |

| Healthcare & Pharmaceuticals |

| Food & Beverages |

| Chemicals & Hazardous Materials |

| Others |

| North Rhine-Westphalia |

| Bavaria (Bayern) |

| Baden-Wurttemberg |

| Rest of States |

| By Logistics Function | Green Transportation | Road |

| Air | ||

| Sea and Inland Waterways | ||

| Rail | ||

| Green Warehousing & Distribution | ||

| Green Value-added Services and Others | ||

| By Fuel / Energy Type | Electric-Powered Logistics | |

| Biofuel-Based Logistics | ||

| Hydrogen-Powered Logistics | ||

| Others | ||

| By End-user Industry | Retail & E-commerce | |

| Manufacturing & Industrial | ||

| Automotive | ||

| Healthcare & Pharmaceuticals | ||

| Food & Beverages | ||

| Chemicals & Hazardous Materials | ||

| Others | ||

| By Region | North Rhine-Westphalia | |

| Bavaria (Bayern) | ||

| Baden-Wurttemberg | ||

| Rest of States |

Key Questions Answered in the Report

What is the current size of the Germany green logistics market?

The Germany green logistics market was valued at USD 48.26 billion in 2025 and is forecast to reach USD 77.56 billion by 2031 at an 8.16% CAGR from 2026 to 2031.

Which logistics function leads the spending on green logistics in Germany?

Green Transportation led with a 61.58% share in 2025, indicating that transport activity still accounts for the majority of current spending.

Which fuel type is growing fastest in Germany green logistics?

Hydrogen-Powered Logistics is projected to grow the fastest at 15.11% CAGR through 2031, although electric-powered logistics still holds the largest current share at 47.80%.

Which end-user group drives the most demand for green logistics in Germany?

Manufacturing and Industrial led with 29.31% share in 2025, supported by Germany’s industrial freight base and stronger procurement requirements for lower-emission transport.

Which German region leads green logistics activity?

North Rhine-Westphalia held the largest regional share at 31.82% in 2025 because of its dense industrial base, freight corridors, and logistics infrastructure.

What is the main challenge slowing wider adoption of green logistics in Germany?

The biggest constraint remains the high capital intensity of zero-emission fleets and related infrastructure, especially for smaller carriers that cannot spread investment as easily as large operators.

Page last updated on: