Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 6.97 Billion |

| Market Size (2026) | USD 7.31 Billion |

| Market Size (2031) | USD 9.43 Billion |

| Growth Rate (2026 - 2031) | 5.23% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Generator Sets Market Analysis by Mordor Intelligence

The Europe Generator Sets Market size is projected to be USD 6.97 billion in 2025, USD 7.31 billion in 2026, and reach USD 9.43 billion by 2031, growing at a CAGR of 5.23% from 2026 to 2031.

Heightened blackout risk across the continent, the hyperscale build-out of data centers, and stricter corporate uptime mandates are converging to keep the Europe Generator Sets market firmly on a growth path. Diesel remains the workhorse, but dual-fuel and hybrid sets are gaining favor as firms pursue Scope 1 decarbonization without jeopardizing resilience. Mid-range units between 75 and 375 kVA dominate commercial demand, while megawatt-class sets aligned with modular N+1 data-center architectures are the fastest climbers. Fragmentation persists, yet the top four OEMs are progressively differentiating through EU Stage V compliance, hydrogen-ready designs, and digital monitoring suites that turn standby assets into revenue-earning grid participants.

Key Report Takeaways

- By capacity, 75 to 375 kVA units captured 34.9% of the Europe Generator Sets market share in 2025, whereas the 750 to 2,000 kVA class is expected to expand at a 6.64% CAGR through 2031.

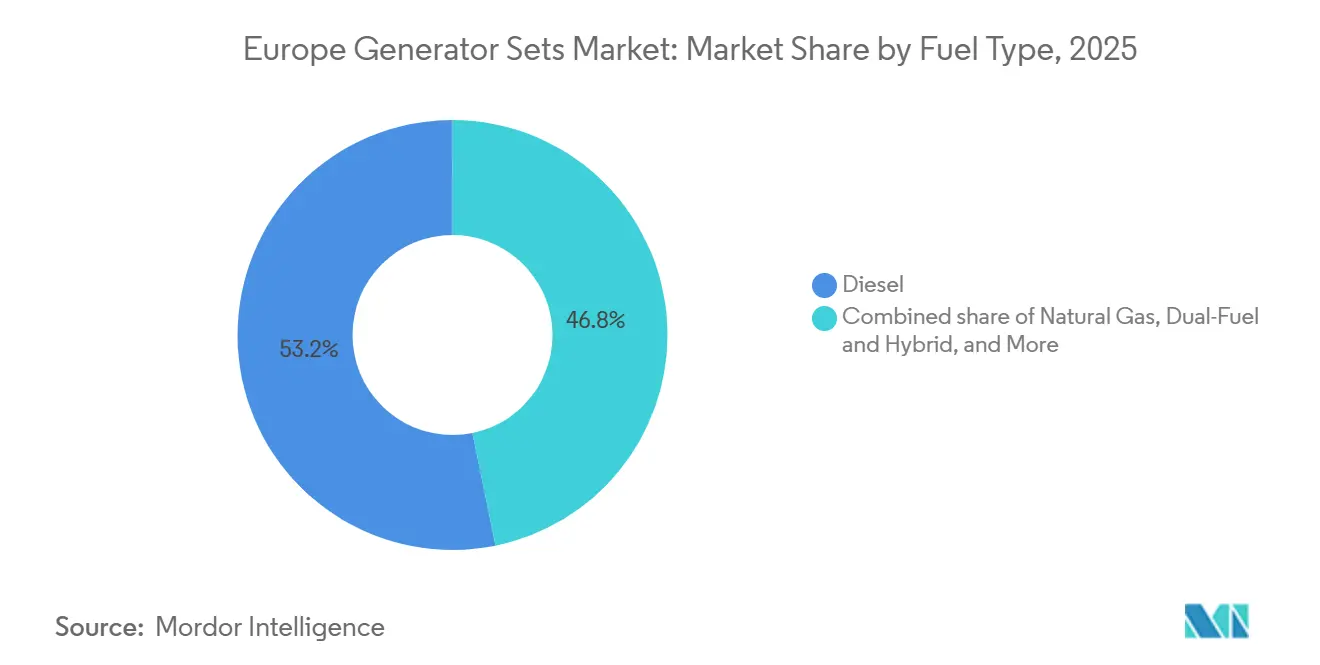

- By fuel type, diesel held a 53.2% slice of the Europe Generator Sets market in 2025, while dual-fuel and hybrid units is expected to grow at CAGR at 7.22%.

- By application, standby power contributed 44.6% of 2025 revenue; micro-grid and hybrid support is projected to grow at a 7.45% CAGR to 2031.

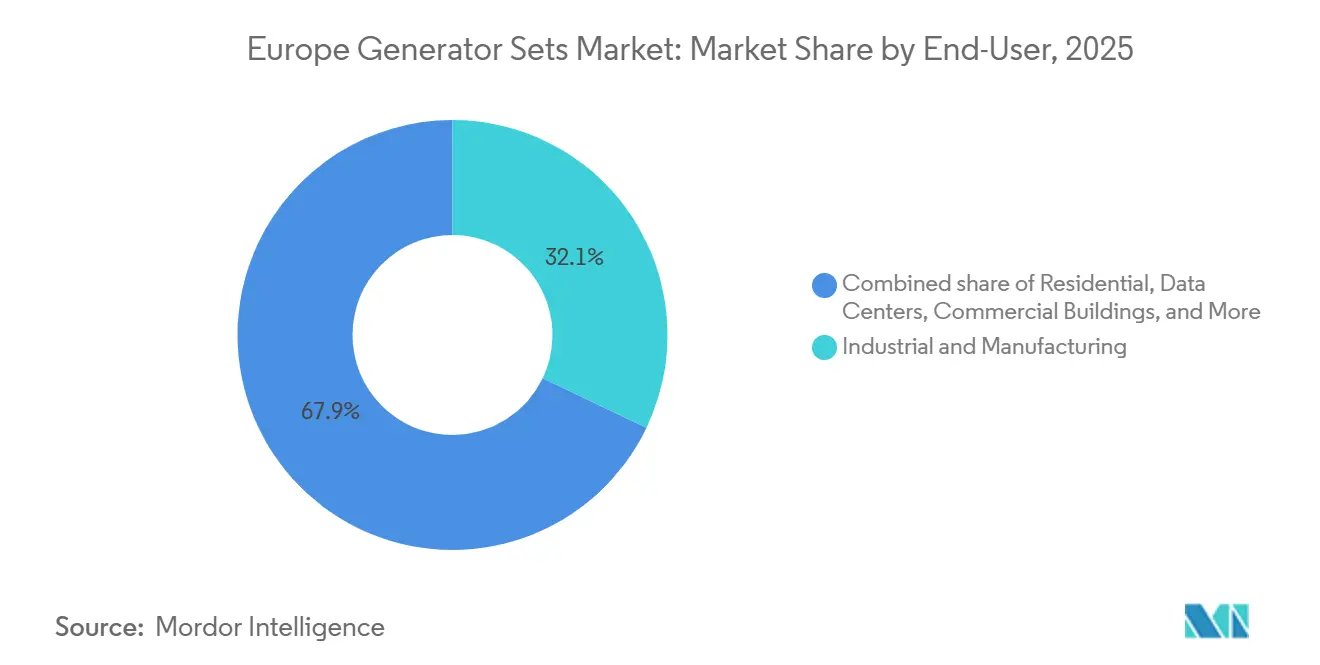

- By end-user, industrial and manufacturing sites accounted for 32.1% of revenue in 2025, yet data centers is projected to grow at a 6.96% CAGR to 2031.

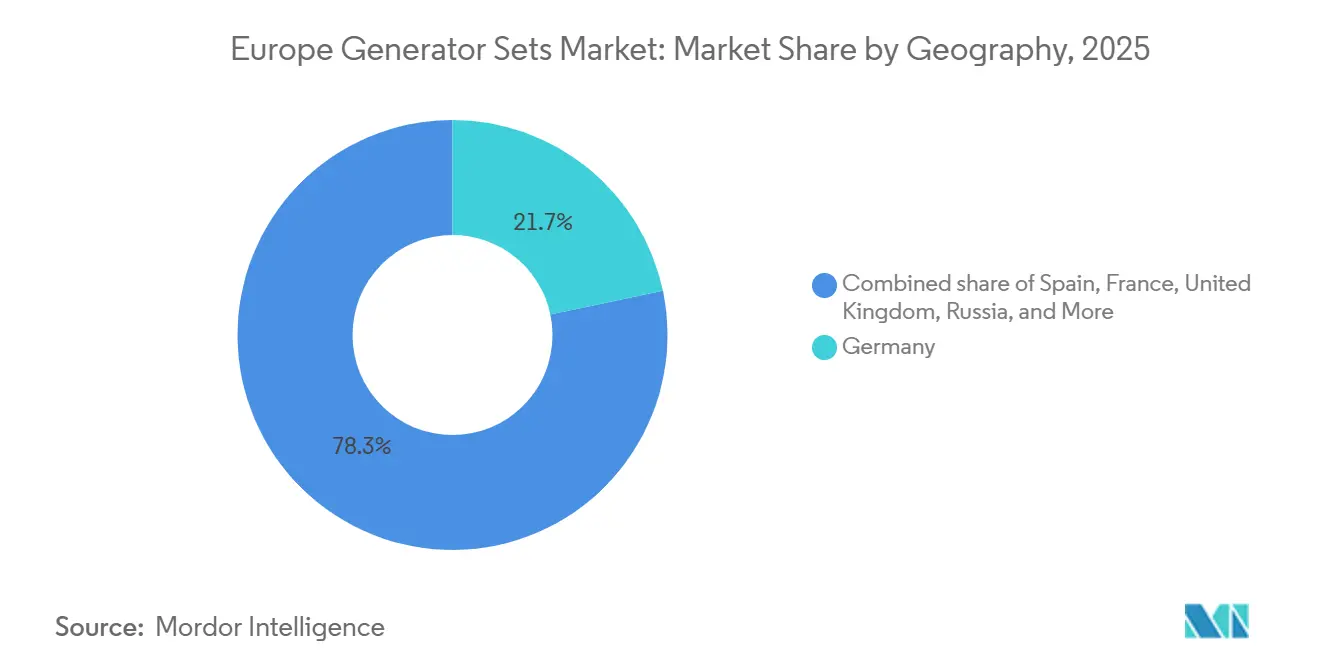

- By geography, Germany led with a 21.7% share in 2025, while Spain is projected to grow the fastest at a 6.43% CAGR to 2031.

- Cummins, Caterpillar, Rolls-Royce Power Systems, and Generac jointly secured about 40% of sales in 2025, underscoring a moderately concentrated arena.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Generator Sets Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for reliable backup power in data centers & healthcare | 1.20% | Germany, Netherlands, Ireland, Spain, France | Medium term (2-4 years) |

| Construction boom & infrastructure upgrades across Europe | 0.80% | Spain, Poland, Germany, UK, Nordics | Medium term (2-4 years) |

| Aging grid infrastructure & climate-driven outages | 0.90% | Iberian Peninsula, Italy, Eastern Europe | Short term (≤ 2 years) |

| Hybrid diesel-solar microgrids on islands & mine sites | 0.50% | Greek islands, Balearic Islands, Nordic mining regions | Long term (≥ 4 years) |

| Corporate sustainability targets boosting gas & biofuel gensets | 0.70% | Germany, UK, France, Netherlands, Nordics | Medium term (2-4 years) |

| Commercial launch of hydrogen-ready generator engines | 0.40% | Germany, Netherlands, UK, Nordics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Reliable Back-Up Power in Data Centers & Healthcare

Hyperscalers have more than 20 GW of new European capacity on the drawing board, and every megawatt requires a proportional slice of standby generation. Microsoft’s USD 10 billion Sines campus alone will rely on 1.2 GW of backup, while Google’s German cloud expansion locks in gas or diesel redundancy under Tier III rules. Hospitals are following suit, upgrading to dual 375 kVA architectures with sub-10-second transfer switches to meet IEC 60364-7-710 standards. Biofuel pilots such as EcoDataCenter’s 48-unit HVO100 deployment in Sweden highlight that resilience and decarbonization can coexist. As testing frequency moves from annual to monthly, remote monitoring platforms like Mobile Link are shifting maintenance from reactive to predictive, thereby trimming unplanned downtime and extending service life.[1]Generac, "Mobile Link Remote Monitoring Platform," generac.com

Construction Boom & Infrastructure Upgrades Across Europe

Nearly USD 11 billion in Connecting Europe Facility grants is funneling into rail, port, and highway projects that need mobile power at every stage.[2]European Commission, “Connecting Europe Facility Transport Funding,” europa.eu Rental fleets supplied 24/7 sites such as Sizewell C and Crossrail with Stage V sets ranging from 30 to 1,250 kVA, pushing utilization to a multi-year high.[3]Aggreko, “Hybrid BESS-Genset Rental Fleet,” aggreko.com Renewable build-outs also rent gensets for commissioning and grid-synchronization, a process lengthened by the 2025 heatwave that derated thermal assets across Southern Europe. Containerized solar rigs are creeping in for daylight loads, yet concrete curing, tunneling, and overnight HVAC still rest on diesel reliability.

Aging Grid Infrastructure & Climate-Driven Outages

ENTSO-E counted 18 continent-wide low-wind days in 2025, double the 2024 figure, exposing 55% of the system to elevated blackout risk.[4]ENTSO-E, “European Resource Adequacy Assessment 2025,” entsoe.eu The Spain-Portugal outage in April 2025 cut power to 2.3 million customers for eight hours and galvanized utilities to accelerate reinforcement spending. Until Germany’s USD 123 billion HVDC rollout is complete in 2030, industrial belts will continue to lean on on-site generation for voltage stability. Italy’s aging 380 kV spine, with four in ten transformers past design life, similarly sustains genset demand among pharma and auto clusters.

Hybrid Diesel-Solar Micro-Grids on Islands & Mine Sites

Islands from Tilos to Mallorca and remote Nordic mines are blending 500 kVA diesel sets with megawatt-scale solar and battery strings. The result is a 40-60% reduction in fuel use, 99% uptime during winter low-irradiance weeks, and new frequency-regulation revenue streams that shorten payback to under a decade. Control complexity remains the hurdle; advanced power-management software must sync inverter-based renewables with rotating-mass generators to avoid damaging voltage excursions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Stage V/VI emission norms heighten CAPEX & OPEX | -0.60% | EU-wide, notably Germany, France, Italy | Short term (≤ 2 years) |

| Grid reliability improvements curb standby demand | -0.40% | UK, Germany, France, Netherlands | Medium term (2-4 years) |

| Battery storage cost plunge (< EUR 233/kWh) challenges small diesel sets | -0.50% | Germany, UK, Netherlands, Nordics | Medium term (2-4 years) |

| EU Carbon Border Adjustment Mechanism raises export costs | -0.30% | Eastern Europe exporters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EU Stage V/VI Emission Norms Heighten CAPEX & OPEX

Since 2024, every generator above 560 kW must meet particulate limits of 0.015 g/kWh and NOx of 2.0 g/kWh, forcing OEMs to bolt on SCR, DPF, and EGR systems that add USD 5,816.03–17,448.08 per unit. Operators incur 3-5% more fuel burn for filter regeneration and urea dosing, nudging the total cost of ownership higher. Proposed Stage VI rules may drop NOx to 1.5 g/kWh and introduce on-board diagnostics, stacking another USD 9,305.64 onto list prices and stretching payback for small sets.

Grid Reliability Improvements Curb Standby Demand

Germany’s transmission overhaul aims to cut annual outage minutes from 18 to 12 by 2030, while the UK’s program will add 4,000 km of new cabling to absorb 50 GW of offshore wind. As SAIDI scores improve, commercial buildings with low outage costs may rethink new standby purchases. Yet gains are uneven; Eastern European grids still record more than an hour of annual downtime, so the overall drag on the Europe Generator Sets market is limited.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Capacity: Mid-Range Units Dominate, Megawatt Class Accelerates

Mid-range 75 to 375 kVA models held 34.9% of Europe Generator Sets market share in 2025, reflecting their fit for commercial buildings and midsize industries. They balance price and footprint, retailing between USD 29080.13 and USD 93056.40 with enclosure and ATS included. The Europe Generator Sets market size for the 750 to 2,000 kVA bracket is projected to expand at a 6.64% CAGR, fuelled by data-center modularity that strings 1,500 kVA sets in N+1 arrays. Above 2 MW, uptake is niche but lucrative, hinging on gas engines that double as CHP units and earn ETS credits.

Containerized designs are cutting installation from six weeks to ten days, a boon for rental firms whose utilization hit 78% in 2025. Under 75 kVA, growth stalls as rooftop solar plus batteries undercut diesel on price in high-tariff markets. Between 375 and 750 kVA, demand trails the headline CAGR as improved grid performance reduces perceived risk among large retail chains.

By Fuel Type: Diesel Dominance Erodes, Dual-Fuel Gains

Diesel still powered 53.2% of sets shipped in 2025, underscoring its 43 MJ kg energy density and cold-weather reliability. Nevertheless, dual-fuel and hybrid offerings are forecast to post a 7.22% CAGR to 2031 as operators pursue 40% CO₂ cuts when switching to gas. The Europe Generator Sets market size tied to natural-gas models rose in tandem, now at 18% of new installs, helped by biogas credit schemes. Hydrogen-ready engines remain below 2% but signal future direction as pipelines materialize.

Biofuel blends led by HVO100 are keeping legacy fleets relevant; Cummins and Rolls-Royce warranties now cover 100% HVO with negligible derating. Longer term, cost parity between gas and diesel plus carbon-pricing trajectories will tilt the mix further toward gaseous and renewable fuels.

By Application: Standby Prevails, Microgrids Surge

Standby duty captured 44.6% of 2025 revenue, cementing its place as the backbone of data-center and hospital resilience strategies. Yet micro-grid and hybrid support is the fastest riser at a 7.45% CAGR, as island grids and mines stitch together solar, storage, and diesel for 60% fuel savings. The Europe Generator Sets market share attributable to rental and temporary power climbed on the back of record equipment utilization during weather-delayed megaprojects.

Prime and continuous applications hold steady at 28%, serving off-grid telecom and mining. Peak-shaving represents a slim 12% but offers rapid paybacks where time-of-use tariffs exceed EUR 0.17 kWh. Battery-assisted hybrids are now standard in urban construction, quieting job sites by 15 dB and trimming diesel burn by half.

By End-User: Industrial Leads, Data Centers Accelerate

Industrial and manufacturing facilities controlled 32.1% of 2025 turnover, driven by high outage costs and stringent quality controls. The Europe Generator Sets market is, however, seeing the fastest CAGR, 6.96%, among data centers, where AI workloads push rack densities beyond 30 kW and mandate megawatt-scale redundant power. Commercial buildings followed at 18%, propelled by tenancy lease clauses and insurer requirements.

Healthcare’s 9% share inches upward as post-pandemic audits tighten life-safety tolerances. Residential demand is marginal and slipping as home batteries proliferate. Utilities, mining, and oil-and-gas together form a steady 21% slice, each with bespoke certification requirements such as ATEX zones or black-start capability.

Geography Analysis

Germany anchored 21.7% of 2025 revenue, underpinned by a USD 123 billion grid overhaul and a surge in hyperscale data-center builds. The Europe Generator Sets market size linked to Spain is smaller but expanding at a 6.43% CAGR, buoyed by Amazon’s USD 39.20 billion cloud roadmap and Balearic Island microgrid mandates. The United Kingdom, at 16%, is midway through a USD 134.03 billion transmission upgrade that, until complete, keeps standby sets in demand for industrial estates.

France holds 14% as it refurbishes its nuclear fleet and layers in 23 GW of renewables, yet industrial clusters still specify dual-fuel sets to hedge against reactor outages. Italy’s 11% share stems from an aging high-voltage backbone that prompted 12 unplanned shutdowns in 2025, doubling the prior year’s tally. Nordic nations together command 13%; their low-carbon grids still suffer congestion, so data-center developers deploy HVO-fueled standby fleets to maintain Tier III uptime.

Russia’s position slipped to 4% amid supply-chain sanctions, while the Rest of Europe, including Poland and the Czech Republic, absorbed relocated assembly lines that skirt CBAM steel levies. These shifts collectively illustrate how policy, investment, and climate geography weave distinct demand tapestries inside the wider Europe Generator Sets market.

Competitive Landscape

The Europe Generator Sets industry remains moderately concentrated. Cummins, Caterpillar, Rolls-Royce Power Systems, and Generac collectively seized roughly 40% of 2025 shipments, leveraging broad portfolios and in-house engine platforms. Each is fast-tracking hydrogen-ready engines and Stage V conforming exhaust packages while embedding telematics such as Cummins’ PowerCommand Cloud to monetize after-sales analytics.

Regional specialists, HIMOINSA, Pramac, FG Wilson, and SDMO, fill lead-time niches with agile production and rental-optimized skids. Aggreko differentiates through a 150-unit hybrid BESS-plus-genset fleet that halves diesel consumption for construction clients restricted by urban noise caps. Battery integrators such as Tesla Energy and Fluence nibble at the sub-75 kVA perimeter, displacing small diesel sets in markets where feed-in tariffs and storage subsidies converge.

Cost pressure from CBAM is catalyzing onshoring: Caterpillar’s Northern Ireland expansion adds 50,000 engines a year, while Rolls-Royce is retrofitting rental fleets for HVO100 to safeguard utilization ahead of 2030 net-zero checkpoints. The next competitive battleground lies in grid-interactive capabilities, with OEMs trialing fast-ramp dispatch modes that let standby fleets earn USD 58.16-93.06 MWh in ancillary-service markets.

Europe Generator Sets Industry Leaders

-

Caterpillar Inc.

-

Cummins Inc

-

Rolls-Royce Power Systems (MTU)

-

Kohler / SDMO

-

Aggreko plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Generac Holdings, Inc. announced the launch of its SD1250 and SD1500 diesel generators, designed to provide reliable and efficient power for high-demand applications. These generators, powered by the Perkins 5012 46-liter engine, address a key need in the industrial market by offering enhanced fuel efficiency, lower emissions, and a compact design.

- April 2025: Caterpillar launched the XQ20, a compact 20 kVA Tier-4-Final-compliant mobile genset designed for construction, emergency backup, and event power across Europe. Featuring a high-efficiency engine, low noise output, extended maintenance intervals, and advanced telematics, it supports European rental fleets and flexible onsite power requirements.

- February 2025: Rolls-Royce introduced upgraded MTU Series 1600 generator sets for the 50 Hz market, offering up to 40% more power (590–996 kVA) and compatibility with HVO fuel for up to 90% CO₂ reduction. These units cater to European data centers, healthcare facilities, and commercial buildings requiring sustainable, high-density backup power.

- October 2024: French manufacturer Baudouin unveiled a new diesel genset line for data centers, delivering 2000–5250 kVA outputs using M33/M55 platforms. Fully type-tested for Tier III/IV compliance, these gensets enhance Europe’s access to integrated, high-capacity, HVO-compatible backup power solutions amid rising demand from hyperscale and colocation facilities.

Europe Generator Sets Market Report Scope

An engine generator is a device that combines an electrical generator and an engine into a single piece of equipment. This combination is also known as an engine-generator set (gen-set). The machine is often taken for granted, and the combined device is called a generator.

The Europe generator sets market is segmented by capacity, fuel type, application, end user, and geography. By capacity, the market is divided into below 75 KVA, 75 to 375 KVA, 375 to 750 KVA, 750 to 2,000 KVA, and above 2,000 KVA. By fuel type, the market is segmented into diesel, natural gas, dual-fuel and hybrid, renewable/bio-fuel, and others. By application, the market is segmented into standby power, prime/continuous power, peak-shaving, rental/temporary power, micro-grid, and hybrid support. By end-user, the market is segmented into residential, commercial buildings, industrial and manufacturing, data centers, healthcare facilities, oil and gas, utilities and power, and mining and construction. The report also covers the market size and forecasts for the European generator sets market across major countries (Germany, the United Kingdom, France, Italy, Spain, the Nordic Countries, Russia, and the rest of Europe). For each segment, the market sizing and forecasts have been done based on revenue (USD billion).

By Capacity

| Below 75 kVA |

| 75 to 375 kVA |

| 375 to 750 kVA |

| 750 to 2,000 kVA |

| Above 2,000 kVA |

By Fuel Type

| Diesel |

| Natural Gas |

| Dual-Fuel and Hybrid |

| Renewable/Bio-fuel |

| Others |

By Application

| Standby Power |

| Prime/Continuous Power |

| Peak-Shaving |

| Rental/Temporary Power |

| Micro-grid and Hybrid Support |

By End-User

| Residential |

| Commercial Buildings |

| Industrial and Manufacturing |

| Data Centers |

| Healthcare Facilities |

| Oil and Gas |

| Utilities and Power |

| Mining and Construction |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| NORDIC Countries |

| Russia |

| Rest of Europe |

| By Capacity | Below 75 kVA |

| 75 to 375 kVA | |

| 375 to 750 kVA | |

| 750 to 2,000 kVA | |

| Above 2,000 kVA | |

| By Fuel Type | Diesel |

| Natural Gas | |

| Dual-Fuel and Hybrid | |

| Renewable/Bio-fuel | |

| Others | |

| By Application | Standby Power |

| Prime/Continuous Power | |

| Peak-Shaving | |

| Rental/Temporary Power | |

| Micro-grid and Hybrid Support | |

| By End-User | Residential |

| Commercial Buildings | |

| Industrial and Manufacturing | |

| Data Centers | |

| Healthcare Facilities | |

| Oil and Gas | |

| Utilities and Power | |

| Mining and Construction | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe Generator Sets market in 2026?

The Europe Generator Sets market size is valued at USD 7.31 billion in 2026, on track to reach USD 9.43 billion by 2031.

Which capacity segment is growing fastest?

Units rated between 750 and 2,000 kVA are forecast to grow at a 6.64% CAGR, driven by data-center N+1 architectures.

Are diesel gensets losing market share?

Diesel still holds 53.2% of shipments but dual-fuel and hybrid models post the quickest gains at 7.22% CAGR as firms seek lower emissions.

Why is Spain the fastest-growing country market?

Spain's 6.43% CAGR stems from hyperscale cloud investments and island microgrid programs mandating backup during multi-day renewable lulls.

What impact do EU Stage V rules have on genset costs?

After-treatment hardware adds EUR 5,000-15,000 per unit and lifts fuel use by up to 5%, lengthening payback for small sets.

When will hydrogen-ready generators become mainstream?

Commercial launches began in 2025, but widespread uptake awaits pipeline and storage infrastructure, likely post-2030 in core Northern markets.

Page last updated on: