GCC Architectural Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

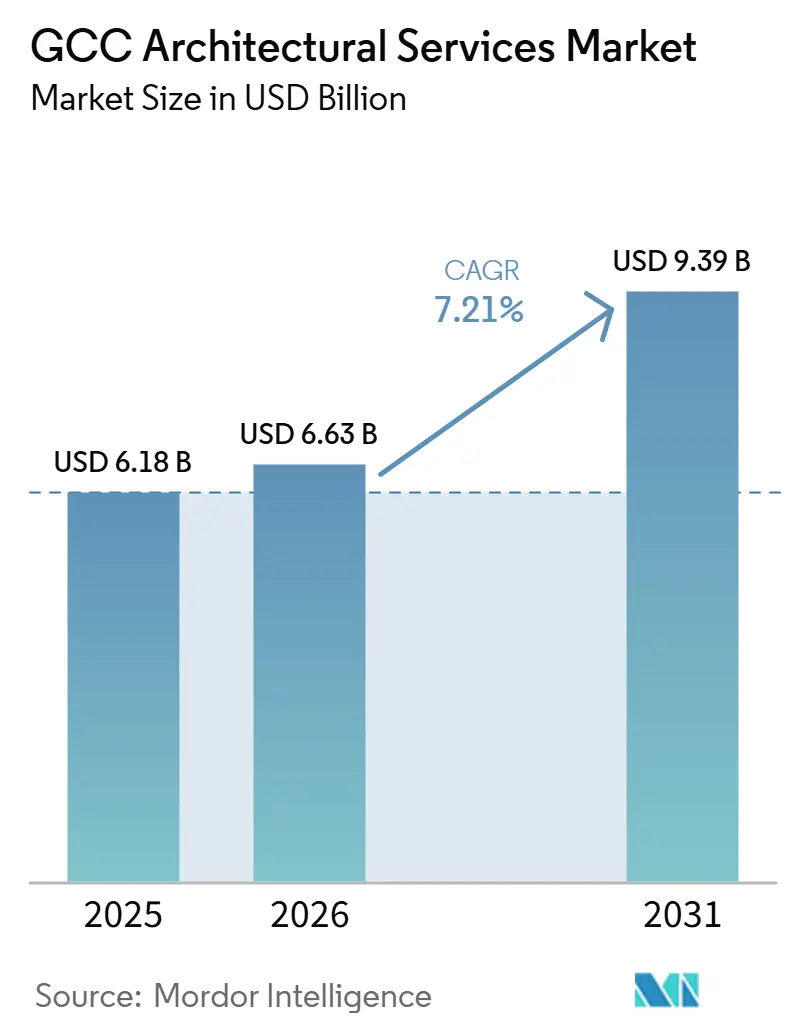

| Base Year Market Size (2025) | USD 6.18 Billion |

| Market Size (2026) | USD 6.63 Billion |

| Market Size (2031) | USD 9.39 Billion |

| Growth Rate (2026 - 2031) | 7.21% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Architectural Services Market Analysis by Mordor Intelligence

The GCC Architectural Services Market size was valued at USD 6.18 billion in 2025 and is estimated to grow from USD 6.63 billion in 2026 to reach USD 9.39 billion by 2031, at a CAGR of 7.21% during the forecast period (2026-2031).

The GCC architectural services market is being supported by sovereign investment programs, national transformation agendas, and a project pipeline that has clearly moved from planning into active delivery across several large urban, tourism, housing, and infrastructure programs. Public clients still anchor the revenue base, providing the GCC architectural services market with a durable volume floor even as private capital moves at different paces across countries and asset classes. The adoption of the Global Sustainability Assessment System (GSAS) (Gulf Standard GSO 3000:2025) is expanding the technical requirements of architectural design, making sustainability expertise a key differentiator for public and compliance-focused projects throughout the GCC. The GCC architectural services market is also broadening through renovation, retrofit, heritage-sensitive work, and infrastructure-linked building programs, thereby reducing overdependence on pure greenfield construction and creating space for specialist firms with differentiated delivery capabilities. Competition remains fragmented, and premium mandates are increasingly being awarded to joint ventures that can combine scale, local execution depth, and multidisciplinary delivery.

Key Report Takeaways

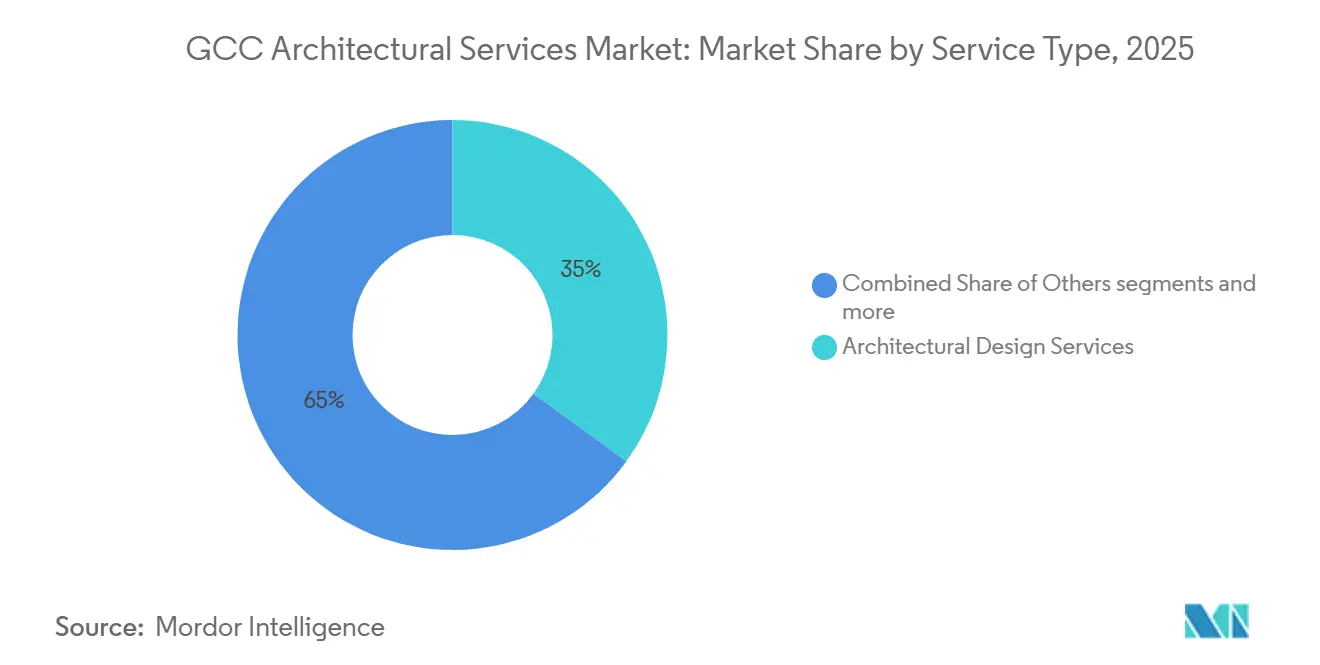

- By service type, architectural design services accounted for 35.00% of the GCC architectural services market share in 2025, while urban design and master planning services are projected to grow at a 8.90% CAGR through 2031.

- By project type, new construction accounted for 73.00% of the GCC architectural services market share in 2025, while renovation is forecast to expand at 8.80% CAGR through 2031.

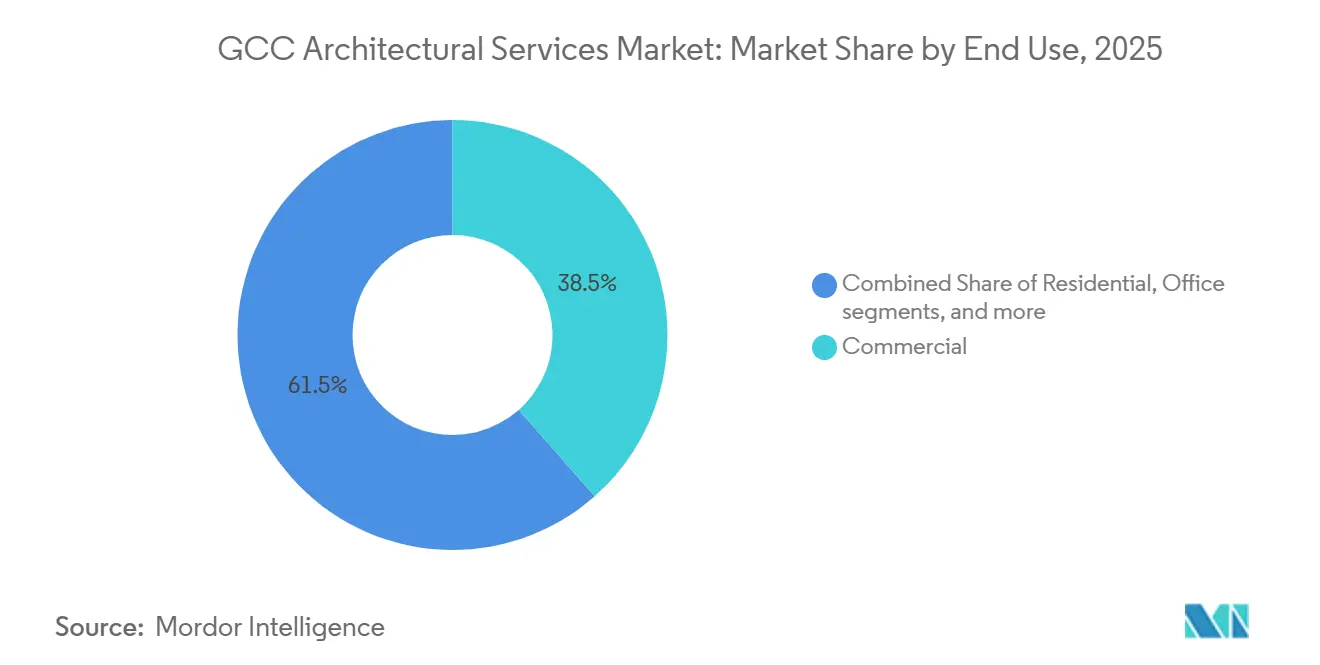

- By end use, commercial real estate accounted for 38.50% of the GCC architectural services market share in 2025, while infrastructure-linked buildings are projected to grow at a 9.60% CAGR through 2031.

- By investment source, public investment held 58.5% share of the GCC architectural services market size in 2025, while private investment is projected to advance at 8.40% CAGR through 2031.

- By geography, the United Arab Emirates captured 47.00% of the GCC architectural services market share in 2025, while Saudi Arabia is expected to post the highest CAGR at 7.90% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

GCC Architectural Services Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Giga-Project Pipeline Accelerates Demand for Architectural Services | +2.4% | Saudi Arabia and the United Arab Emirates, with secondary pull from Qatar and Kuwait | Long term (≥ 4 years) |

| Sustainability Design Mandates Increase Green Building Projects | +1.3% | GCC-wide, strongest in Abu Dhabi, Qatar, and Saudi Arabia | Medium term (2-4 years) |

| Renovation, Retrofit, and New-Build Activity Expands Design Demand | +1.0% | United Arab Emirates and Saudi Arabia | Medium term (2-4 years) |

| Digital Design and BIM Requirements Enhance Service Adoption | +0.8% | Saudi Arabia and the United Arab Emirates | Short term (≤ 2 years) |

| Hospitality and Mixed-Use Asset Repositioning Drives Architectural Demand | +0.7% | Saudi Arabia, United Arab Emirates, and Oman | Long term (≥ 4 years) |

| Public Sector Project Acceleration Boosts Design Service Demand | +0.5% | Saudi Arabia and Abu Dhabi | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Giga-Project Pipeline Accelerates Demand for Architectural Services

The GCC architectural services market continues to benefit from the simple fact that very large projects are no longer defined only by announcements; they are increasingly defined by staged execution and repeat design packages. In practical terms, this means firms are not competing for a single concept commission alone; they are often competing for work that extends into detailed design, coordination, delivery support, and later phases across the same development. Saudi Arabia remains the clearest example of this pattern. Still, the GCC architectural services market also sees it in major United Arab Emirates waterfront, residential, and urban destination projects that require long design cycles and multiple specialist teams. Large clients are also showing a stronger preference for consortia, because project scale now often exceeds the efficient reach of a single firm working alone, especially when urban design, infrastructure coordination, and public realm planning need to move together. This pattern enhances revenue visibility in the GCC architectural services market because multi-phase work tends to generate follow-on mandates rather than isolated assignments.

Sustainability Design Mandates Increase Green Building Projects

Sustainability has moved from a premium feature to a baseline design expectation in much of the GCC architectural services market. The adoption of the Global Sustainability Assessment System (GSAS) as Gulf Standard GSO 3000:2025 formalized a regional reference point for sustainable building requirements. It reduced the compliance burden across design briefs, which must now address energy, water, and material performance more directly[1]Gulf Organisation for Research and Development, “GCC Standardization Organization Adopts GSAS as Gulf Green Building Standard GSO 3000:2025,” GORD, gord.qa. This shift matters for architecture firms because performance-led design usually requires more coordination at the concept stage, more technical analysis during development, and closer integration between architecture and engineering inputs. Regulatory enforcement is also driving broader green building adoption, which supports the view that compliance will continue to direct demand toward firms that can embed sustainability from the start of the design process. In commercial terms, the GCC architectural services market benefits from regulation, which deepens service offerings, extends design tasks, and makes purely decorative or minimal-compliance designs less viable. The result is a market where sustainability qualification is steadily becoming a condition of entry for public and institutional work rather than a marginal differentiator.

Renovation, Retrofit, and New-Build Activity Expands Design Demand

The GCC architectural services market is still led by new construction. Still, renovation and retrofit work is becoming a more meaningful source of fees across mature urban locations and heritage-sensitive districts. This matters because renovation is not simply smaller new-build work; it usually requires a different design process that includes surveys, adaptation of existing structure, code alignment, and tighter coordination around live assets or preserved fabric. In the United Arab Emirates, older commercial stock and first-generation mixed-use assets are driving more repositioning briefs, while in Saudi Arabia, the emphasis on cultural identity and district renewal is supporting design work closer to conservation and adaptive reuse. The value of this shift is that it widens the addressable work mix for the GCC architectural services market and reduces dependence on a narrow set of large greenfield packages. Firms that can combine interior planning, architectural reprogramming, and digital documentation are better positioned to win these mandates, as clients increasingly seek refurbishment that supports both asset performance and tenant appeal. Over time, this part of the GCC architectural services market should remain attractive because specialized retrofit work tends to be less exposed to direct fee competition than standardized new-build assignments.

Digital Design and BIM Requirements Enhance Service Adoption

Digital delivery requirements are tightening across the GCC architectural services market, and Building Information Modeling (BIM) now functions more like a procurement threshold than a premium add-on. For architecture firms, BIM capability affects not only drawing production but also interdisciplinary coordination, revision control, phasing, and the ability to respond to complex briefs without losing time across delivery stages. This helps explain why commissioning authorities increasingly expect digital workflows from the start[2]Faisal Al-Harith et al., “Blueprint for Progress, Understanding the Driving Forces of BIM Adoption in Kingdom of Saudi Arabia Construction Industry,” PLOS One, journals.plos.org. It strengthens the GCC architectural services market by increasing the value of firms that can deliver in an organized, repeatable, and scalable manner across large projects. It also changes competitive behavior, since firms that lack mature digital processes are more likely to be screened out before pricing becomes the main evaluation factor. The effect is not uniform across all firms, but it clearly favors practices that can combine design quality with disciplined information management on multi-stakeholder projects.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competitive Tendering Compresses Architectural Service Fees | -1.2% | Saudi Arabia, the United Arab Emirates, and Qatar | Short term (≤ 2 years) |

| Shortage of Senior Multidisciplinary Talent Constrains Project Delivery | -0.8% | GCC-wide, most acute in Kuwait and Saudi Arabia | Medium term (2-4 years) |

| Uneven Regulatory Frameworks Increase Cross-Border Project Complexity | -0.5% | Cross-border corridors, especially Saudi Arabia and the United Arab Emirates | Medium term (2-4 years) |

| Developer Preference for In-House Design Limits Outsourced Services | -0.4% | United Arab Emirates and Saudi Arabia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competitive Tendering Compresses Architectural Service Fees

The GCC architectural services market remains attractive enough to attract both global and regional participants to the same tenders, which intensifies competition even when demand remains healthy. In large public and prestige-led projects, many clients can demand extensive technical capability, visual quality, and coordinated delivery while still pushing down fees through open competition. This creates the greatest pressure on mid-tier firms, because they often lack the pricing flexibility of local specialists and the balance sheet depth or global profile of the largest multinational practices. The GCC architectural services market, therefore, shows a gap between headline demand and realized profitability, since a firm can win visible work without necessarily protecting margin quality across scope changes and late design revisions. Joint ventures partly solve this problem by sharing risk and capability, but they also raise the entry bar for firms that do not already have trusted partners or a long local track record. Fee pressure does not remove opportunity, but it does make selectivity, cost discipline, and project fit more important for sustainable growth.

Shortage of Senior Multidisciplinary Talent Constrains Project Delivery

The GCC architectural services market also faces capacity constraints, as the most valuable projects increasingly require senior staff who can lead design teams, work fluently in BIM environments, and meet sustainability and coordination demands simultaneously. That combination is not easy to build quickly, especially as regional project volumes expand faster than the talent pipeline for experienced design leadership. In practice, this means firms may have demand in hand but still struggle to take on too many complex mandates at once without risking delivery quality, timeline slippage, or weaker client service. The problem is more serious in the upper end of the GCC architectural services market because mega developments, public programs, and mixed-use districts require both concept strength and organizational discipline across many workstreams. Localization requirements in some countries also add another layer, since firms need to deepen local talent benches while maintaining immediate delivery capacity on active assignments. The result is that hiring, training, and retention have become strategic growth issues rather than routine operational concerns.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Architectural Design Services Anchors Revenue While Urban Design & Master Planning Services Commands Growth

Architectural design services held 35.00% of the GCC architectural services market share in 2025, which confirms that the earliest design phase still generates the largest fee pool within the overall service mix. This lead reflects the structure of the GCC architectural services market, where major projects usually begin with concept definition, scheme development, and detailed design that then shape all downstream tasks. Architectural design also tends to remain central even when delivery models become more collaborative, because clients still want a lead design vision that can align engineering, interiors, public realm, and documentation. In revenue terms, this gives core design practices a durable role even as specialist services expand around them. The segment also benefits from the region’s preference for signature districts, branded destinations, and high-visibility civic assets, where design quality remains a client priority.

Urban design and master planning services are expected to record the highest CAGR of 8.90% through 2031, indicating that growth is becoming more place-led and program-led rather than tied solely to individual buildings. Within the GCC architectural services market size outlook, this is important because large developments increasingly need district planning, mobility integration, phasing strategy, and public realm design before vertical packages can move efficiently. That pattern is evident in major mixed-use and waterfront communities, where land use, circulation, and civic identity must be resolved well before detailed building design is finalized. The GCC architectural services market also benefits here from public clients planning at the city scale, as master planning work can directly lead to later architectural packages for the same development area. Over time, this should keep service demand balanced between firms focused on building-level design and firms that can guide broader urban transformation programs.

By Project Type: New Construction Dominates, but Renovation Approaches Structural Significance

New construction accounted for 73.00% of revenue in 2025, indicating that the GCC architectural services market still relies mainly on greenfield delivery and large-scale expansion across cities, tourism zones, housing communities, and public assets. This dominance is consistent with a region where sovereign-backed and developer-led projects are still adding new built stock at scale rather than only upgrading what already exists. The largest briefs also tend to sit in new-build formats, which supports revenue concentration in concept design, detailed package development, and multidisciplinary coordination around fresh site conditions. For many leading firms, new construction remains the clearest route into landmark mandates and long-duration client relationships. This is why the GCC architectural services market continues to favor firms that can handle multi-phase delivery and broad consultant coordination on large, fresh developments.

Renovation, however, is forecast to expand at 8.80% through 2031, suggesting a more balanced project mix over time. The rise of renovation matters because mature building stock, heritage-sensitive districts, and repositioning of older assets require design work that differs in method, staffing, and risk from standard new-build assignments. In the GCC architectural services market, renovation remains a smaller segment. Still, it can support stronger specialization because clients often need measured surveys, adaptive reuse thinking, and more careful planning around site and user constraints. This gives firms with experience in refurbishment, interior reconfiguration, and conservation-sensitive detailing a clearer position, less exposed to volume-based price competition. As this segment expands, the GCC architectural services market should see more firms build dedicated retrofit capabilities rather than treating renovation as a secondary extension of new-build practice.

By End-Use: Commercial Real Estate Leads While Infrastructure-Linked Buildings Grow Fastest

Commercial real estate accounted for 38.50% of end-use revenue in 2025, making it the largest demand center across offices, retail-led destinations, mixed-use assets, and hospitality-linked commercial projects. This lead fits the structure of the GCC architectural services market, where urban growth and destination development still rely heavily on revenue-generating built assets that need strong design identity and tenant appeal. Commercial work also offers a broad range of commissions, from shell-and-core design to public realm, interiors, façade revisions, and asset repositioning. That breadth matters because it allows firms to participate across multiple work stages and fee bands rather than relying on a single narrow design package. It also helps explain why both global and regional firms remain active in this part of the GCC architectural services market.

Infrastructure-linked buildings are projected to grow at 9.60% through 2031, making it the fastest-growing end-use segment. This area includes airports, transit hubs, logistics-related facilities, and other building programs where architecture has to respond to heavy functional demands, public movement, and systems integration. Large mixed-use and infrastructure-style projects show how building design and mobility-oriented coordination are converging on more complex briefs. Residential demand also remains relevant in the GCC architectural services market, and major villa development contracts in Dubai underscore the ongoing scale of external design opportunities in premium housing. Together, these patterns show that growth is shifting toward end uses where architecture is expected to solve both experience and operational complexity.

By Investment Source: Public Funds Underpin the Market as Private Capital Accelerates

Public investment held 58.50% of revenue in 2025, so state-backed commissioning remained the main base of the GCC architectural services market. This matters because public and sovereign-linked clients tend to support the longest project pipelines, the largest design briefs, and the clearest continuity between planning and later implementation phases. Public capital also shapes standards, as many sustainability and digital requirements first become more visible in government and strategic development projects before spreading to the private sector. In commercial terms, this provides the GCC architectural services market with a steady institutional anchor, even as private development timing shifts across real estate cycles. It also explains why firms with strong public-sector compliance and coordination experience remain well-positioned on regional shortlists.

Private investment is projected to grow at 8.40% through 2031, suggesting the next layer of expansion will come from developers, investors, and mixed-funding structures seeking external design support. The private side of the GCC architectural services market tends to move faster in some asset classes, especially in residential communities, branded destinations, and commercial repositioning projects, which respond to market opportunities rather than solely to policy scheduling. The line between public and private funding is also becoming less rigid, as many large development vehicles operate with sovereign backing but use delivery models and procurement practices closer to those of the private sector. This shift increases opportunity for firms that can work with more commercial timelines while still meeting institutional standards on complex briefs. In that sense, the GCC architectural services market should continue to be underpinned by public capital while gaining additional growth energy from private and hybrid investment channels.

Geography Analysis

The United Arab Emirates accounted for 47.00% of the GCC architectural services market share in 2025, which made it the largest country market in the region. Its lead reflects the depth of work across Dubai and Abu Dhabi, where residential, hospitality, mixed-use, and infrastructure-linked programs continue to generate a wide range of commissions. The United Arab Emirates also benefits from a mature client base that can issue briefs across concept design, interiors, supervision support, public realm planning, and asset repositioning rather than only one-off building packages. Sustainability compliance has become a stronger part of that demand mix, and Global Sustainability Assessment System (GSAS) standardization at the Gulf level reinforces a market where green design capability is increasingly expected rather than optional. The market is also expanding geographically within the country, with Ras Al Khaimah attracting more hospitality and branded-residence projects, including major design appointments tied to luxury coastal development[3]SSH Design, “SSH Appointed Lead Design Consultant on Nobu Hotel and Residences in Al Marjan, Ras Al Khaimah,” SSH Design, sshic.com.

Saudi Arabia is forecast to grow at a 7.9% CAGR through 2031, which makes it the fastest-growing geography in the GCC architectural services market. The scale of sovereign development is shaping the country’s role, the breadth of destination projects, and the rising need for architecture that responds to cultural identity as well as modern delivery requirements. Saudi Arabia also remains important because many of its major schemes are large enough to support ongoing workstreams, creating follow-on demand for design revision, coordination, and phased package development. Large appointments on projects such as The Mukaab show that Saudi briefs favor firms or teams that can combine range, scale, and execution depth. The GCC architectural services market also sees Saudi Arabia as a place where sustainability and digital delivery expectations are tightening, which supports firms with credible BIM and performance-led design capability.

Oman, Qatar, Kuwait, and Bahrain together account for the remaining regional demand, and each market offers a distinct opportunity profile for the GCC architectural services market. Oman is benefiting from quality-led office and mixed-use work, including major lead design and construction supervision roles on Muscat business park developments. Qatar and Kuwait continue to support institutional and infrastructure-related assignments, while Bahrain maintains a smaller but steady design flow in dense urban and waterfront formats. This mix matters because it gives the GCC architectural services market a broader regional base than the 2 largest countries alone, and it allows firms to build portfolios across different client types, project scales, and regulatory settings.

Competitive Landscape

The GCC architectural services market is fragmented, with numerous international, regional, and local firms competing across commercial, residential, infrastructure, hospitality, and mixed-use developments. Global firms such as AECOM, AtkinsRéalis, Jacobs, Gensler, and Skidmore, Owings & Merrill LLP participate in large and technically complex projects. In contrast, regional firms including Omrania, SSH Design, Dewan Architects + Engineers, Khatib & Alami, and KEO International Consultants maintain strong positions through local expertise, long-standing client relationships, and familiarity with regional regulatory environments. As a result, no single firm or group of firms dominates the GCC architectural services market, allowing both multinational and regional practices to compete across a broad range of project types.

Competition is increasingly centered on specialization, project experience, and collaborative delivery rather than company size alone. International firms often partner with regional specialists to combine global design expertise with local market knowledge, particularly on large-scale urban developments and government-led projects in Saudi Arabia and the United Arab Emirates. At the same time, regional firms continue to secure significant commissions through their understanding of local planning requirements, cultural considerations, and client expectations. These dynamics reinforce the fragmented nature of the GCC architectural services market by creating opportunities for firms with differentiated capabilities rather than concentrating work among only a few players.

Product differentiation is also becoming a key competitive factor. Firms with expertise in sustainable design, heritage conservation, digital design technologies, interior architecture, and integrated master planning are better positioned to compete for higher-value assignments. While established international firms remain prominent in landmark developments, regional and specialized firms continue to expand through niche expertise, local execution capabilities, and long-term client relationships. Consequently, the GCC architectural services market is expected to remain fragmented, with competition driven by technical specialization, project-specific expertise, and regional execution capabilities rather than overall market concentration.

GCC Architectural Services Industry Leaders

AECOM

AtkinsRéalis

Dar Al-Handasah Consultants

KEO International Consultants

Foster + Partners

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: ORA Developers appointed AtkinsRéalis to deliver masterplanning, infrastructure coordination, and public realm design services for BAYN, a landmark waterfront community in Ghantoot, positioned between Dubai and Abu Dhabi, extending the firm's Buildings and Places portfolio within the United Arab Emirates (UAE)'s emerging coastal development corridor.

- April 2026: SSH Design secured the lead design consultancy and construction supervision contract for Expo Valley Views at Expo City Dubai, delivering integrated architecture, interior design, structural, mechanical, electrical, and plumbing engineering, and public realm design services for a sustainable residential community aligned with the United Arab Emirates (UAE)'s Net Zero 2050 ambitions.

- February 2026: AtkinsRéalis and Futurecity formally launched a global strategic partnership, announced at MIPIM Cannes 2026, to embed cultural placemaking as a core driver of urban development across the Middle East, with priority on major projects in Saudi Arabia and the United Arab Emirates.

GCC Architectural Services Market Report Scope

The GCC Architectural Services Report is Segmented by Service Type (Architectural Design Services, Architectural Documentation & Delivery Services, and More), Project Type (New Construction, and Renovation), End-Use (Residential and More), Investment Source (Public and Private), and Geography (United Arab Emirates, Saudi Arabia, Oman, Qatar, Kuwait, and Bahrain). The Market Forecasts are Provided in Terms of Value (USD).

| Architectural Design Services |

| Architectural Documentation & Delivery Services |

| Interior Architecture & Space Planning Services |

| Urban Design & Master Planning Services |

| Others |

| New Construction |

| Renovation |

| Residential | |

| Commercial | Retail |

| Institutional | |

| Industrial and Logistics | |

| Others | |

| Infrastructure-linked Buildings |

| Public |

| Private |

| United Arab Emirates |

| Saudi Arabia |

| Oman |

| Qatar |

| Kuwait |

| Bahrain |

| By Service Type | Architectural Design Services | |

| Architectural Documentation & Delivery Services | ||

| Interior Architecture & Space Planning Services | ||

| Urban Design & Master Planning Services | ||

| Others | ||

| By Project Type | New Construction | |

| Renovation | ||

| By End-Use | Residential | |

| Commercial | Retail | |

| Institutional | ||

| Industrial and Logistics | ||

| Others | ||

| Infrastructure-linked Buildings | ||

| By Investment Source | Public | |

| Private | ||

| By Geography | United Arab Emirates | |

| Saudi Arabia | ||

| Oman | ||

| Qatar | ||

| Kuwait | ||

| Bahrain | ||

Key Questions Answered in the Report

What is the size outlook for GCC architectural services through 2031?

The GCC architectural services market is expected to grow from USD 6.18 billion in 2025 to USD 9.39 billion by 2031, at a 7.21% CAGR from 2026 to 2031.

Which country leads the regional demand for architectural services in the GCC?

The United Arab Emirates led with 47.00% of 2025 revenue, supported by broad activity across Dubai and Abu Dhabi, and by expanding destination-led projects in other emirates.

Which GCC country is growing fastest for architectural firms?

Saudi Arabia is expected to expand fastest, with a 7.90% CAGR through 2031, driven by large sovereign development projects and multi-phase urban projects.

Which service type brings in the most revenue?

Architectural design services was the largest service type in 2025, accounting for 35.00% of revenue, underscoring the importance of concept and detailed design in the project cycle.

What part of the business mix is growing fastest?

Urban design and master planning services is projected to grow fastest among service types at 8.90%, while infrastructure-linked buildings leads end-use growth at 9.60%.

What is shaping competition among firms in the region?

Competition is shaped by joint ventures, stronger BIM expectations, sustainability compliance, and the need for firms to combine local execution knowledge with multidisciplinary scale.

Page last updated on: