Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.90 Billion |

| Market Size (2026) | USD 4.14 Billion |

| Market Size (2031) | USD 5.56 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Feed Premix Market Analysis by Mordor Intelligence

The GCC feed premix market size was valued at USD 3.90 billion in 2025 and estimated to grow from USD 4.14 billion in 2026 to reach USD 5.56 billion by 2031, at a CAGR of 6.12% during the forecast period (2026-2031). That sustained growth reflects a policy shift that converts premix inclusion from a discretionary cost into a compliance-driven requirement, especially in Saudi Arabia and the United Arab Emirates. Demand acceleration is reinforced by poultry and aquaculture integration programs, digital ration-formulation platforms, and sovereign fund investments that expand local blending capacity. Conversely, margin pressure stems from heavy reliance on imported micro-ingredients, volatile maritime freight, and an underdeveloped cold chain for liquid premixes. Competitive intensity remains moderate, yet opportunities persist in niche segments such as camel-specific blends and clean-label antioxidant formulations.

Key Report Takeaways

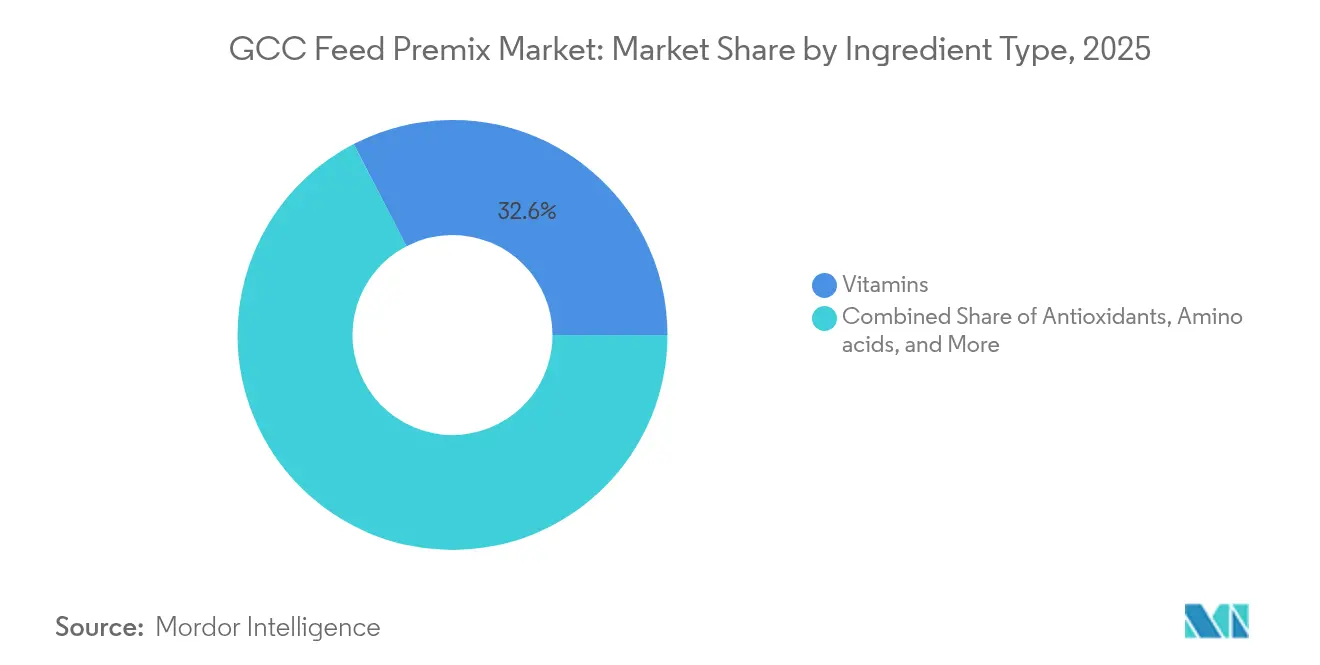

- By ingredient type, vitamins led with a 32.60% of GCC feed premix market share in 2025, while antioxidants are projected to rise at a 9.25% CAGR to 2031.

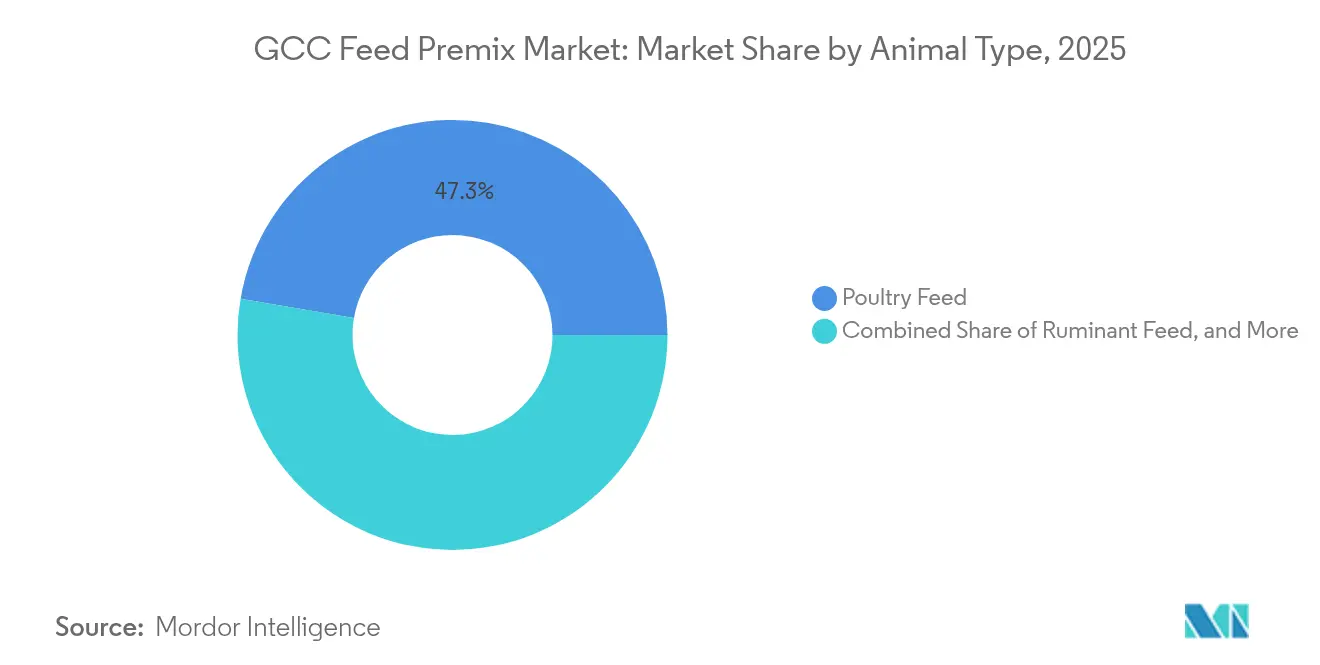

- By animal type, poultry feed accounted for 47.30% of the GCC feed premix market size in 2025 and is projected to expand at an 7.85% CAGR through 2031.

- By geography, Saudi Arabia held a 44.60% revenue share in 2025, while the United Arab Emirates recorded the fastest 7.12% CAGR from 2025 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Feed Premix Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding domestic poultry integration programs | +1.40% | Saudi Arabia, United Arab Emirates, and Qatar | Long term (≥ 4 years) |

| Rapid aquaculture build-outs along the Red Sea coast | +1.10% | Saudi Arabia, Oman, and United Arab Emirates | Medium term (2-4 years) |

| Mandatory fortification rules for compound feed | +1.60% | Saudi Arabia, United Arab Emirates, and Kuwait | Short term (≤ 2 years) |

| Sovereign food-security funds investing in premix plants | +0.90% | Saudi Arabia, United Arab Emirates, and Qatar | Medium term (2-4 years) |

| Digitized ration-formulation platforms adopted by medium farms | +0.70% | United Arab Emirates, Saudi Arabia, Kuwait, and Bahrain | Medium term (2-4 years) |

| Growing demand for antibiotic-free animal protein | +0.80% | United Arab Emirates, Saudi Arabia, and Qatar | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Domestic Poultry Integration Programs

Large, vertically integrated poultry producers are rewriting procurement norms by locking in multi-year premix contracts rather than making spot purchases. The SAR 17 billion (USD 4.5 billion) Vision 2030 allocation pushes broiler self-sufficiency toward 90% by 2030, cementing a stable and sizable offtake base for premix suppliers [1]Vision 2030 Program, “National Transformation Plan Documents,” vision2030.gov.sa. Tanmiah Food Company runs 15 fully owned complexes and sources standardized vitamin-mineral blends to protect feed-conversion ratios across 120 million birds annually. GCC-wide additive specifications, published in 2024, harmonize vitamin tolerances, enabling cross-border shipments without requiring re-testing [2]GSO Secretariat, “Feed Additive Standard GSO 1395:2024,” gso.org.sa . The integration wave lowers blender price volatility while raising anticipations for on-site nutrition services, rapid quality control feedback, and documented traceability. Bahraini and Omani smallholders, lacking scale for direct deals, increasingly rely on toll-blended premixes shipped from Saudi and Emirati plants, further centralizing technical know-how.

Rapid Aquaculture Build-Outs Along the Red Sea Coast

Marine farming projects are generating a second pillar of growth for the GCC feed premix market. NEOM’s Topian initiative aims to target 80,000 metric tons of seafood by 2030 and already specifies premixes with 30% higher phosphorus, elevated omega-3 content, and astaxanthin for enhanced pigmentation. Oman crossed 5,000 metric tons of farmed output in 2024, signaling a regional pivot to shrimp and finfish. Nutreco’s Skretting unit leverages micro-encapsulation that stabilizes vitamin C in saltwater, a capability terrestrial blenders cannot easily replicate. Fragmented oversight remains a hurdle, and residue limits differ between Saudi Arabia’s National Center for Fisheries and the United Arab Emirates’ Ministry of Climate Change and Environment, forcing suppliers to maintain multiple formulations. As marine volumes rise, technical differentiation rather than price becomes the decisive competitive factor.

Mandatory Fortification Rules for Compound Feed

Circular 4418 from Saudi Arabia’s Ministry of Environment, Water, and Agriculture compels minimum vitamin A (10,000 IU/kg), vitamin D3 (2,000 IU/kg), selenium, and zinc across all commercial feed, with the United Arab Emirates enforcing analogous audits and fines reaching AED 500,000 (USD 136,000). Low-cost mineral-only blends have largely vanished, making premix adoption universal, even among backyard farmers. Compliance costs are driving consolidation, as mills with a capacity of less than 50,000 metric tons outsource premix sourcing to Tier 1 suppliers. Although GCC standards are harmonized, enforcement rigor varies across the region. Saudi audits are quarterly, while Kuwaiti inspections occur annually, encouraging strategic product flows that exploit lighter regimes.

Growing Demand for Antibiotic-Free Animal Protein

Retail chains, including Carrefour UAE, have pledged that 60% of their fresh poultry will be antibiotic-free by 2026, while Almarai aims to eliminate the use of medically important antibiotics by 2027. Reformulations add USD 0.08/kg to premix cost but unlock the European Union's export channels with strict residue thresholds. Suppliers with portfolios in essential oils, probiotics, and enzymes gain, whereas commodity blenders dependent on tylosin face structural decline. Regulatory draft rules from Abu Dhabi restrict colistin and fluoroquinolones, aligning with WHO guidance and accelerating the shift to clean-label additives. Divergent policies across GCC states widen compliance complexity but solidify demand for differentiated functional blends.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High dependency on imported micro-ingredients | -1.20% | All GCC countries | Short term (≤ 2 years) |

| Volatile maritime freight costs | -0.90% | Saudi Arabia, United Arab Emirates, Oman, Kuwait, Qatar, and Bahrain | Short term (≤ 2 years) |

| Limited cold chain for vitamin-enriched liquid premixes | -0.60% | Oman, Bahrain, Kuwait, and Qatar | Medium term (2-4 years) |

| Fragmented farm structure in Oman and Bahrain | -0.50% | Oman, Bahrain, and Kuwait | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Dependency on Imported Micro-Ingredients

Roughly 92% of vitamins and amino acids originate from China, Germany, and France, creating supply chain exposure to plant shutdowns and currency fluctuations. DSM-Firmenich’s vitamin-A turnaround in Switzerland reduced global output 15% in 2024, spiking spot prices 28%. Adisseo’s Dubai hub saw methionine lead times extend to 90 days after Red Sea disruptions. Local blenders lack leverage for long-term contracts and carry thin inventories to manage cash, amplifying price shocks. Saudi and Emirati initiatives to develop domestic vitamin synthesis remain exploratory until they become operational, and dependence will continue to restrain margin expansion.

Limited Cold Chain for Vitamin-Enriched Liquid Premixes

Liquid blends require temperatures of 2–8 °C throughout transit, however, only 37% of Oman’s fleet and 42% of Bahrain’s trucks provide active cooling. Dry powders have 20% lower vitamin stability, necessitating higher inclusion rates and increasing costs. UAE coverage is better in urban Emirates but drops to 55% in outlying areas. Nutreco’s chilled line in Saudi Arabia’s Eastern Province experienced uptake below target because the price premium outweighed the benefits of bioavailability gains. Without regulatory cold-chain mandates, logistics providers prioritize pharma and perishables, leaving feed additives underserved.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Antioxidants Surge Amid Clean-Label Push

Antioxidants are projected to grow with a 9.25% CAGR to 2031, outpacing the trajectory for the broader GCC feed premix market. Vitamins still controlled 32.60% of GCC feed premix market share in 2025, owing to fortification mandates in Saudi Arabia and the United Arab Emirates. Natural tocopherols and rosemary extract now replace ethoxyquin in poultry diets to satisfy retailer pledges on clean labeling, while amino acids post stable gains tied to poultry expansion, yet remain vulnerable to import price swings. Minerals maintain their baseline relevance because Gulf Cooperation Council standards establish non-negotiable limits for selenium and zinc.

Product repositioning is widening the margin gap between commodity and functional blends. Carrefour UAE’s antibiotic-free requirement accelerates demand for plant-derived antioxidants that also bolster shelf life. Aresco’s multi-enzyme launch demonstrated a 4% feed-conversion improvement in broiler trials, a result that enables integrators to absorb higher inclusion prices. Antibiotic premixes shrink as Almarai phases out tylosin by 2027, creating a structural contraction in that sub-segment. Suppliers that pair R&D capability with agile blending lines are best positioned to capitalize on this ingredient pivot and achieve sustained premium pricing.

By Animal Type: Aquaculture Premixes Command Premium Margins

Poultry retained 47.30% of the GCC feed premix market size in 2025 and expanded at an 7.85% CAGR, driven by Vision 2030's push for Saudi broiler self-sufficiency to reach 90%. Long-term supply contracts from Tanmiah and other integrators provide forecast visibility, yet they also require suppliers to provide on-site nutritionists and 24-hour quality support. Ruminant demand, concentrated in Saudi dairy herds, stays steady but is capped by water-use limits that curb herd growth. Camel and equine blends carve out niche positions in the United Arab Emirates and Oman, where selenium-fortified formulas fetch 35% price premiums over standard ruminant mixes.

NEOM’s Topian project and Oman’s shrimp farms require phosphorus levels 30% above terrestrial norms and specialized omega-3 inputs, driving the fastest revenue growth and the widest gross margins in the portfolio. The segment’s technical moat deters generalist blenders who lack expertise in marine nutrients, helping Nutreco’s Skretting unit defend premium pricing. As marine output scales, suppliers able to deliver micro-encapsulated vitamins that withstand saltwater conditions will consolidate share, leaving commodity producers to compete on price in poultry and dairy sub-markets.

Geography Analysis

Saudi Arabia led with 44.60% of 2025 revenue, anchored by the poultry and livestock investment that locks in steady offtake for higher-grade vitamin blends. Compliance audits are conducted quarterly, compelling mills to adopt standardized premixes and rewarding domestic specialists, such as Arasco, that can provide documented traceability. Export-oriented producers also require halal-certified nutrient inputs, deepening the technical service moat against low-cost importers.

The United Arab Emirates is projected to post the fastest 7.12% CAGR to 2031, propelled by aquaculture projects along the Red Sea coast and the addition of 12,000 dairy cattle in 2024 . IFFCO’s new Sharjah line targets marine premix demand and shortens lead times compared to imports, reinforcing Dubai’s role as the GCC feed premix logistics hub. Qatar benefits from a 12% cut in vitamin landed costs after opening its Hamad Port micro-ingredient terminal, though volume remains concentrated among three integrators.

Oman’s rising growth reflects increased shrimp and finfish output, which offsets fragmented poultry demand. Kuwait grows but relies on imported complete feed, limiting stand-alone premix sales. Bahrain lags at because its farm base is small and distributor exits increase last-mile costs. These southern markets tap re-exports from Dubai and Dammam, so regional hubs capture value even when local consumption stays modest.

Regulatory Landscape

Feed premixes in the GCC operate under national feed laws and an increasingly harmonized Gulf Cooperation Council framework. One recent anchor is the GCC Standardization Organization (GSO) adoption of GSO 2813:2026 (approved 30 April 2026), which sets permissible and prohibited feed raw materials and additives. This tightens the specification baseline that premix blenders must meet to support multi-country trade.

Saudi Arabia applies mandatory product controls through the Saudi Food and Drug Authority (SFDA). It classifies premix as mixtures of feed additives with carriers (distinct from compound feed) and requires registration before market entry. In the United Arab Emirates, the Ministry of Climate Change and Environment (MOCCAE) requires import approval for manufactured animal feed and feed additives, renewed every five years, supported by documentation such as a Certificate of Analysis and declarations related to pork derivatives, alongside compliance with mycotoxin limits referenced to UAE/GSO requirements.

Value Chain Analysis

The GCC feed premix value chain starts with global sourcing of micro-ingredients (vitamins, amino acids, trace minerals, antioxidants, and functional additives). Inputs then move through inbound shipping into regional logistics hubs, followed by local blending and packaging (bags, totes, or liquid systems where available), before distribution to compound feed mills and integrated poultry, dairy, and aquaculture producers. Saudi Arabia and the United Arab Emirates anchor regional blending and re-export activity, while smaller markets are often served via cross-border shipments and distributor networks.

Two bottlenecks shape both cost and service levels. First, high reliance on seaborne imports exposes premix inputs to geopolitical and maritime disruption, with Red Sea route volatility adding transit time and freight surcharges. This encourages buyers to shift toward longer lead-time planning and, where working capital allows, higher safety stocks. Second, registration and licensing requirements, led by SFDA rules for additives and premixes, create compliance steps that tend to favor larger suppliers with established documentation, quality systems, and the ability to reformulate for differing inspection regimes across GCC markets.

Competitive Landscape

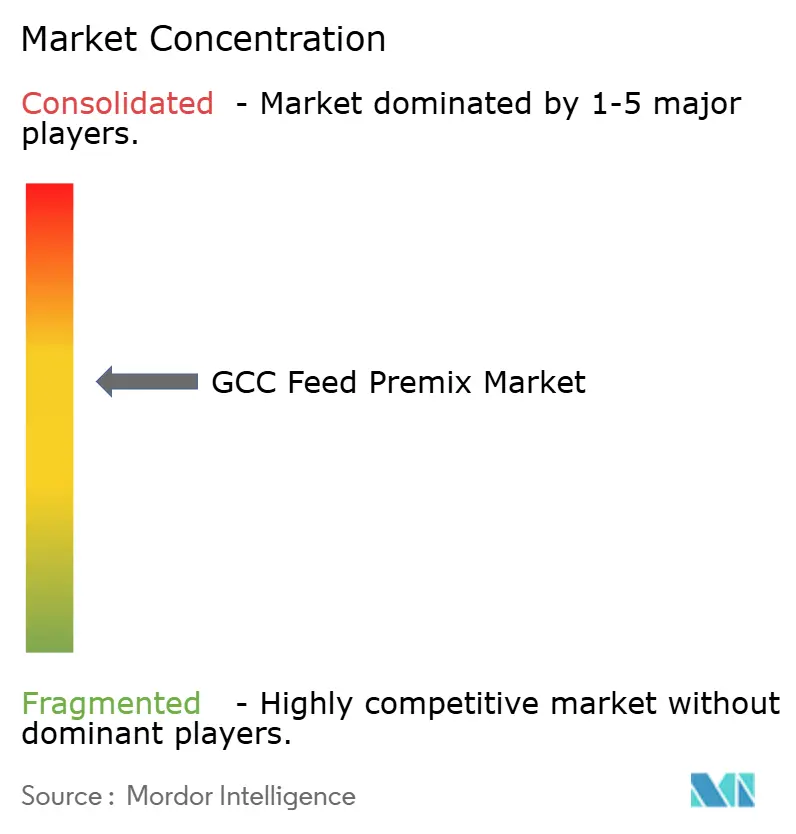

A moderate concentration prevails, with the top five players controlling a significant share of the revenue, yet strategy divergence is widening. Archer Daniels Midland Company and Cargill, Incorporated utilize global sourcing to aggressively price commodity vitamin blends, whereas Arasco and IFFCO Animal Nutrition compete on technical field support and custom batch turnaround. Nutreco defends a premium niche through patents on micro-encapsulated nutrients that resist saltwater degradation, a differentiator vital for aquafeed.

State-backed entrants in Saudi Arabia and the United Arab Emirates distort pricing by accessing subsidized capital, undercutting established players by up to 12% on vitamins while accepting lower margins to capture volume. This forces incumbents to pivot toward R&D-intensive products such as antibiotic-free and organic lines, areas where formulation complexity shields price. Digital procurement platforms accelerate the shift. Arasco’s API linkages now deliver custom premixes within five days, a speed that multinational traders struggle to match.

Regulatory variability shapes geographic tactics. Saudi Arabia’s stringent quarterly audits raise compliance costs but ensure premium pricing, while Kuwait’s annual inspections invite lower-spec imports that squeeze margins. Suppliers with cross-border quality labs arbitrage these gaps by batching compliant inventory in high-regulation markets and redistributing overage to lighter-regulated neighbors. Intellectual property, local service capability, and digital integration therefore emerge as the decisive levers for maintaining or expanding GCC feed premix market share in an environment where raw-material cost advantage alone no longer guarantees sustained leadership.

GCC Feed Premix Industry Leaders

Adisseo

Nutreco N.V.

IFFCO Animal Nutrition

Archer Daniels Midland Company

Arasco Feed

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Aquaculture-specific premixes and alternative protein inputs are creating formulation whitespace as Red Sea and coastal build-outs raise the need for marine nutrient performance, including stability in saline conditions, phosphorus management, and pigmentation packages. A concrete 2026 signal is the Saudi Industrial Investment Group (SIIG) and Unibio International joint venture announcement (March 2026) to build a 50,000-tonne single-cell protein plant in Al Jubail for aquaculture, poultry, and livestock feed. This supports new premix concepts focused on digestibility, amino-acid balancing, and functional health additives paired with novel protein substrates.

Supply-chain resilience and logistics-linked differentiation are increasingly becoming commercial levers alongside formulation. DP World and Al Dahra signed an MoU (May 2026) to develop integrated agricultural logistics across the GCC, including storage, transport, and cold chain infrastructure, aligning with the market need highlighted by limited temperature-controlled distribution for liquid and sensitive vitamin systems. Alongside this, feed and milling investments in Saudi Arabia, including Modern Mills Companys USD 40 million feed-milling project in Al-Jumum (approved December 2024, publicized March 2025) and Fourth Milling Companys USD 71 million expansion in Al-Kharj (announced May 2025), expand the industrial feed asset base that can adopt standardized, compliance-ready premixes and structured supplier service models such as QA support, traceability, and digital ration formulation.

Recent Industry Developments

- May 2026: Adisseo highlighted, in its Q1 2026 update, actions to manage Middle East logistics and energy-market volatility through its distribution footprint and localized manufacturing network. The communication reinforces how supply continuity and lead-time reliability have become competitive differentiators for premix and additive suppliers serving GCC customers exposed to freight disruption.

- May 2025: Fourth Milling Company announced a USD 71 million expansion in Al-Kharj, including a new 240 tons/day feed mill targeted for operation in the second half of 2026. Larger domestic feed output increases throughput-driven demand for standardized vitamin-mineral premixes and supports longer-term supply contracting by integrators and mills.

- May 2024: The United Arab Emirates issued Administrative Decision No. 6/2024 banning the import, circulation, and registration of colistin (polymyxin E) in premixes in the veterinary sector. This regulatory shift accelerated reformulation toward non-antibiotic performance and health solutions, lifting the importance of enzymes, probiotics, and other functional premix components in poultry and other food-animal diets.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of commercially sold feed premixes used in animal feed in GCC countries. These premixes are formulated blends of micro-ingredients such as vitamins, minerals, amino acids, antioxidants, and related additives.

Scope exclusions: It excludes complete compound feed, on-farm mixing that is not sold as a premix, and non-feed uses of these ingredients.

Segmentation Overview

- By Ingredient Type

- Antibiotics

- Vitamins

- Antioxidants

- Amino Acids

- Minerals

- Other Ingredient Types

- By Animal Type

- Ruminant Feed

- Poultry Feed

- Aquaculture Feed

- Others

- By Geography

- Saudi Arabia

- United Arab Emirates

- Oman

- Kuwait

- Bahrain

- Qatar

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the demand context for premixes and to anchor country-level assumptions before any sizing math was finalized. We reviewed official agriculture and livestock statistics, import and customs releases, and food safety or feed control notices from GCC regulators, since premix supply chains are strongly import linked for micro-ingredients.

To keep the model consistent, we also referenced public sources such as FAOSTAT-style livestock production series, trade and customs portals, and association publications for poultry, dairy, and aquaculture. We added peer-reviewed animal nutrition journals that describe inclusion rates and typical formulation changes. Company annual reports, investor presentations, and reputable press were then used to sanity check capacity announcements and distribution footprints. For company financials, patent lookups, and shipment-level trade signals where available, we used selected paid subscriptions. These examples are not exhaustive, and many other public sources were used for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work focused on building realistic inclusion-rate ranges, tracking pricing movement, and quantifying the split between dry and liquid premixes across the GCC. We interviewed premix blenders, distributors, large feed mills, and farm-integrator procurement teams in Saudi Arabia, the UAE, and other GCC countries, then re-checked outliers when desk signals and field inputs did not align.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 18% | |

| Mid tier: 42% | Functional/Unit leaders: 23% | |

| Smaller Players: 21% | Managers: 59% |

Market-Sizing & Forecasting

Sizing started with a top-down build that reconstructed the addressable premix spend from GCC livestock and aquaculture output, feed production patterns, and typical premix inclusion rates by species and production system. Once that demand pool was formed, average premix price levels were applied by ingredient mix and form (dry versus liquid), and totals were allocated across GCC countries based on production intensity and import dependence.

To keep the estimate grounded, we ran selective bottom-up checks using supplier and blender revenue indications, distributor channel checks, and sampled price per ton times estimated volumes for major species. Key inputs tracked included poultry and dairy expansion plans, aquaculture feed growth, shifts toward performance and gut-health additives, micro-ingredient import values and seasonality, and currency timing for USD conversions. Forecasts were built using scenario analysis tied to changes in protein demand, local food security programs, and premix specification tightening. We reviewed scenarios with interview feedback before finalizing the CAGR path. Where bottom-up signals were incomplete for smaller countries, we filled gaps using peer country intensity ratios, then rechecked against trade and feed output proxies.

Data Validation & Update Cycle

Each step was validated through triangulation across demand indicators, trade signals, and field feedback, and outliers were investigated instead of being averaged away. Variance checks were run at the country level and at the ingredient-mix level, followed by an internal analyst review to ensure assumptions were consistent with the market story and the math.

The report is refreshed annually, and interim adjustments are made when material events occur, such as sudden pricing swings in vitamins and amino acids, major policy changes, or large capacity announcements. Before delivery, a final update pass is completed so the numbers reflect the most recent public releases and interview confirmations.

Mordor Intelligence's Gcc Feed Premixes Market Sizing Compared With Other Published Estimates

Different published values for GCC feed premixes typically come from how each study draws the boundary between premixes and broader feed additives, and from whether the estimates are built from demand-side inclusion logic or from a narrower set of supplier revenues. Timing also matters because micro-ingredient prices can move quickly, which changes the USD value even if volumes stay stable.

Import value signals for key micro-ingredients, combined with species-level feed output checks, are the evidence points that keep Mordor Intelligence's estimate tied to premix consumption in GCC feed programs, rather than to a limited set of reported company sales. Other figures can also shift based on whether antibiotics and certain functional additives are counted inside premixes, how dry versus liquid pricing is treated, and whether currency conversion uses an average-year rate or a point-in-time rate.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.90 B (2025) | |

| Global Consultancy A | USD 1.20 B (2024) | Uses a smaller counted basket that looks closer to premix supplier revenues and does not clearly reconcile the number to GCC feed output and inclusion-rate demand pools, which can understate cross-border distribution volumes. |

| Industry Publisher B | USD 1.21 B (2025) | Appears to treat the market closer to feed additives and premix blends sold through select channels, with limited visibility on how import-linked micro-ingredient pricing and form mix (dry versus liquid) are normalized across GCC countries. |

Across the three values, the spread mainly follows scope boundaries and the strength of demand-side checks used to convert animal production into premix spend. By keeping variables explicit, such as inclusion rates, form mix, and import-priced ingredient baskets, the final estimate stays easier to trace and repeat when assumptions are refreshed.

Key Questions Answered in the Report

How large is the GCC feed premix market in 2026 ?

The GCC feed premix market size is USD 4.14 billion in 2026.

Which ingredient category is growing fastest?

Antioxidants expand at a 9.25% CAGR through 2031 as retailers shift toward clean-label meat that avoids synthetic preservatives.

Why are aquaculture premixes gaining momentum?

Red Sea projects such as NEOM’s Topian plan require specialized omega-3-rich formulations, driving aquaculture premixes at the highest segment growth rate in the bloc.

What is the main supply-chain risk for GCC blenders?

92% of vitamins and amino acids are imported, exposing blenders to price swings from global plant outages and volatile freight rates.

Page last updated on: