Gulf Cooperation Council Frozen Bakery Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

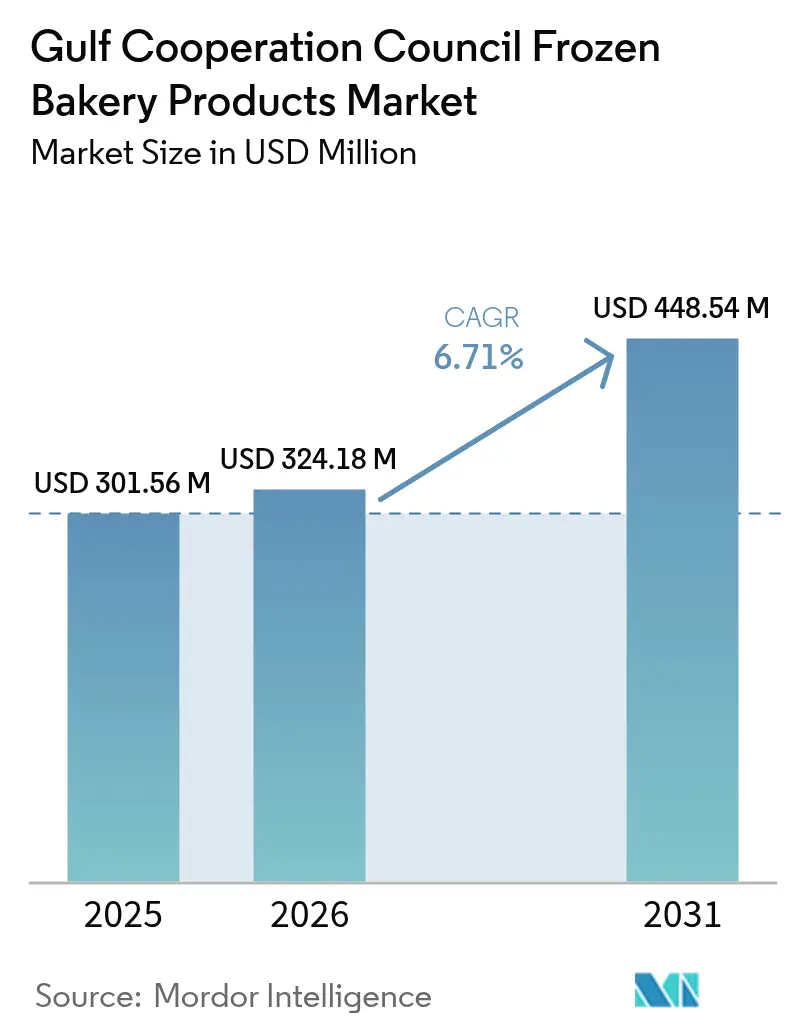

| Base Year Market Size (2025) | USD 301.56 Million |

| Market Size (2026) | USD 324.18 Million |

| Market Size (2031) | USD 448.54 Million |

| Growth Rate (2026 - 2031) | 6.71% CAGR |

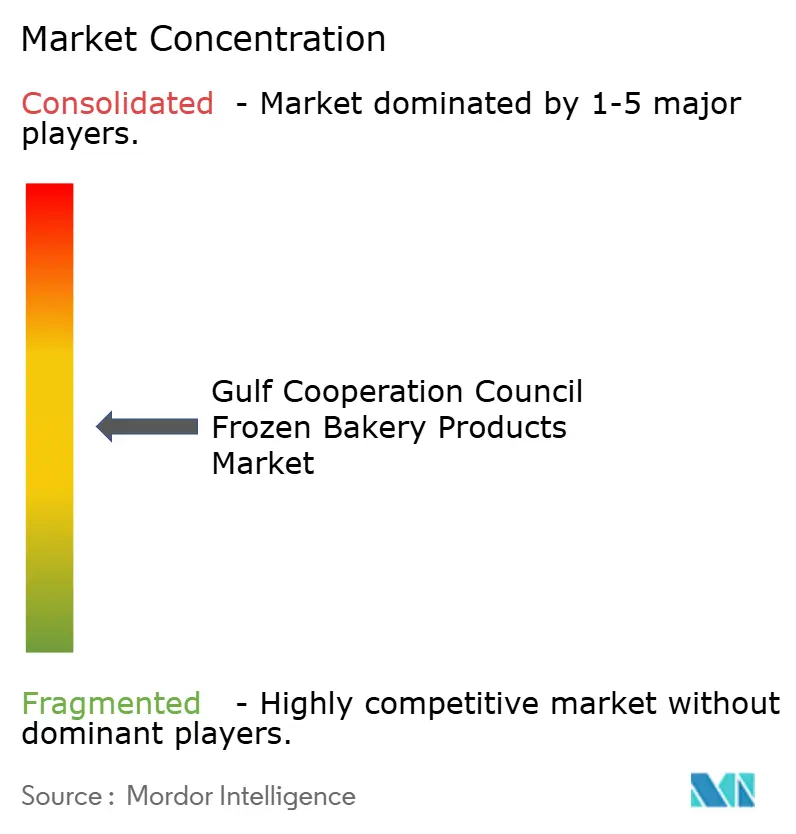

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Gulf Cooperation Council Frozen Bakery Products Market Analysis by Mordor Intelligence

The Gulf Cooperation Council Frozen Bakery Products Market size was valued at USD 301.56 million in 2025 and is estimated to grow from USD 324.18 million in 2026 to reach USD 448.54 million by 2031, at a CAGR of 6.71% during the forecast period (2026-2031). Demand is rising as hotels, cafés, and dark-kitchen aggregators focus on labor-efficient formats to reduce waste and speed up service. National food-security initiatives in Saudi Arabia and the UAE are subsidizing cold-chain capacities, which lower entry barriers for local manufacturers and improve last-mile delivery integrity. Regulatory measures, such as GSO 2483's trans fat elimination and the introduction of front-of-pack labeling, are driving reformulations that favor established players with strong in-house research and development capabilities. Furthermore, increasing tourism and the revival of large-scale events like Riyadh Season are elevating breakfast buffet standards, pushing premium viennoiserie into mainstream consumption. These factors collectively indicate a significant shift in the GCC market from traditional artisan baking to industrial freeze-thaw solutions.

Key Report Takeaways

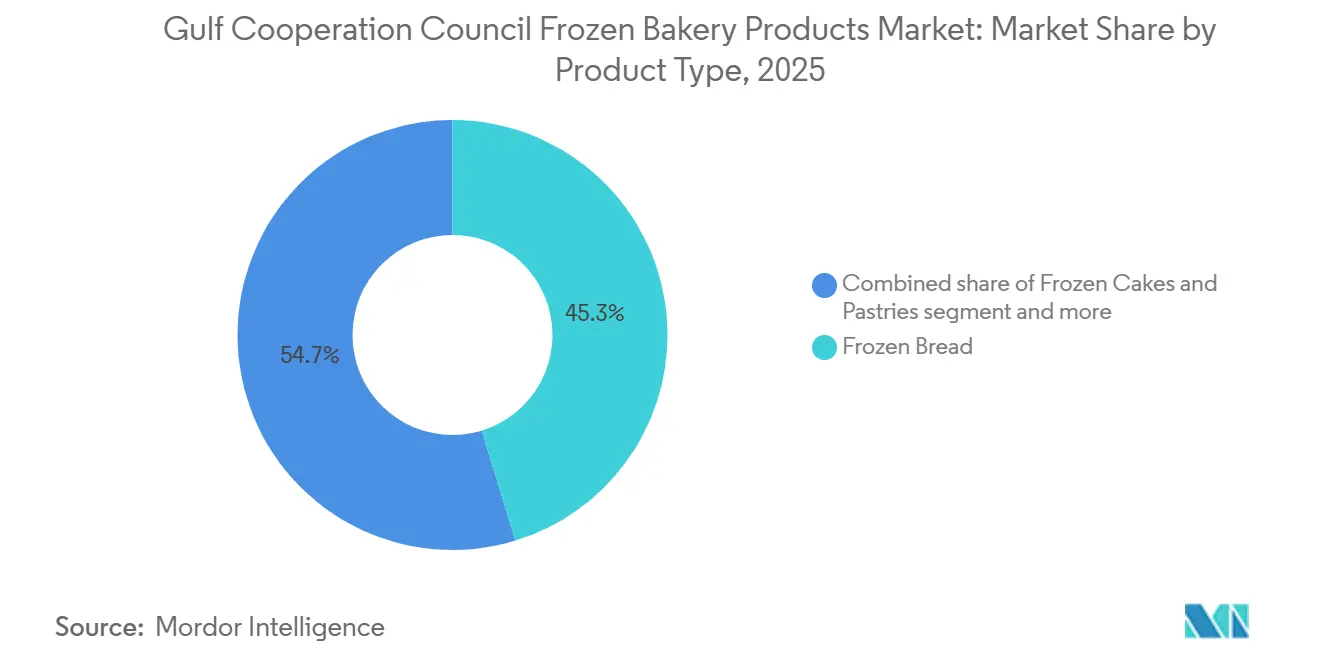

- By product type, frozen bread captured 45.28% GCC frozen bakery products market share in 2025, while frozen cakes and pastries are forecast to advance at a 6.87% CAGR through 2031.

- By category, conventional items retained 92.35% share of the GCC frozen bakery products market size in 2025, while free-from SKUs are projected to expand at a 7.71% CAGR between 2026-2031.

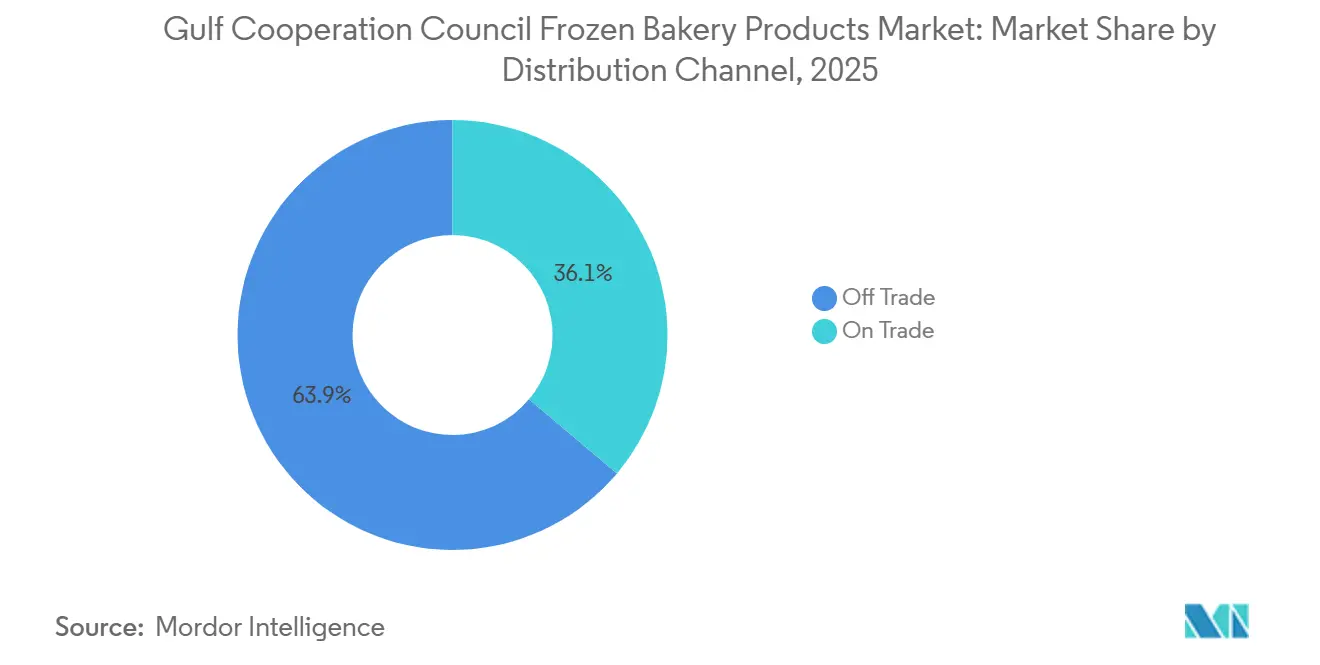

- By distribution channel, off-trade outlets held 63.87% share of the GCC frozen bakery products market size in 2025, while on-trade demand is growing at a 7.02% CAGR through 2031.

- By geography, Saudi Arabia led with 40.46% revenue share in 2025, while the UAE is accelerating at a 7.28% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Gulf Cooperation Council Frozen Bakery Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for convenient, ready-to-eat options amid busy lifestyles | +1.2% | UAE, Saudi Arabia, Qatar (urban centers: Dubai, Riyadh, Doha) | Short term (≤ 2 years) |

| Expansion of food-service chains across the GCC | +1.4% | Saudi Arabia, UAE, Kuwait (QSR and café clusters in Jeddah, Dubai, Kuwait City) | Medium term (2-4 years) |

| Growth in tourism driving demand for viennoiserie in hospitality | +1.1% | UAE, Saudi Arabia, Oman (hotel corridors: Dubai, Riyadh, Muscat) | Medium term (2-4 years) |

| Increased adoption of blast-freezing technology in in-store bakeries | +0.9% | UAE, Saudi Arabia (hypermarket chains: Carrefour, LuLu, Panda) | Long term (≥ 4 years) |

| National food-security plans mandating cold-chain investments | +1.3% | Saudi Arabia, UAE, Oman (government-led infrastructure projects) | Long term (≥ 4 years) |

| Surge in dark-kitchen aggregators sourcing frozen dough | +0.8% | UAE, Saudi Arabia, Kuwait (delivery-only brands in Dubai, Riyadh, Kuwait City) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising demand for convenient, ready-to-eat options amid busy lifestyles

In Dubai, Riyadh, and Doha, urbanization and the increase in dual-income households have reduced the time available for meal preparation. For instance, in 2024, women constituted 22.4% of the labor force in the United Arab Emirates, according to the World Bank[1]Source: World Bank, "Labor force, female (% of total labor force) - United Arab Emirates", worldbank.org. Consequently, consumers are gravitating toward frozen bakery products that provide café-quality results with minimal effort. This trend is particularly prominent among expatriate communities, which represent a substantial portion of the UAE's population. According to the Embassy of India, the Indian expatriate community is the largest ethnic group in the UAE, making up approximately 35% of the population in 2025[2]Source: Embassy of India, "Indian Community in UAE", indembassyuae.gov.in. Furthermore, younger Saudi nationals are joining the workforce in line with the Vision 2030 employment targets. Retailers are responding by expanding their frozen bakery offerings. For example, Laura Bakery in Sharjah features 20 frozen croissant SKUs, ranging from 30 to 120 grams, including regional flavors such as zaatar and cheese. This trend extends beyond retail; corporate catering and airline lounges are increasingly adopting frozen viennoiserie. This approach ensures consistent quality across various service points while reducing reliance on labor, a critical benefit in markets where skilled pastry chefs command high wages and work-visa quotas restrict hiring.

Expansion of food-service chains across the GCC

In 2024-2025, quick-service restaurants and café chains pursued aggressive expansion across the GCC. Americana Group, which operates franchises like KFC, Pizza Hut, and Costa Coffee, reduced its net new store openings from an anticipated 150-160 to 110-120 units due to underperforming outlets in Saudi Arabia. This adjustment reflects a strategic shift from expanding its footprint to improving same-store productivity. For example, by utilizing frozen pizza crusts and pre-portioned dough balls, a Pizza Hut outlet can now function with 40% less back-of-house space, enabling faster service and a smaller kitchen footprint. In September 2024, Mondelez International executives highlighted the growing global adoption of "freeze-and-thaw models." This method involves shipping finished cakes and pastries frozen, thawing them during transit, and presenting them fresh in-store. They identified this as a strategic opportunity in Saudi Arabia, where the company already distributes packaged croissants through its Chipita acquisition. For frozen bakery suppliers, the takeaway is clear: securing long-term contracts with multi-unit operators requires not only product quality but also supply-chain reliability, cold-chain traceability, and the ability to customize formulations for halal certification and local taste preferences.

Growth in tourism driving demand for viennoiserie in hospitality

Tourism in the UAE and Saudi Arabia has experienced a strong recovery, driven by major events such as Expo 2020's legacy projects, Jeddah's Formula 1 races, and the Riyadh Season festivals. These developments have not only increased hotel occupancy rates but also enhanced breakfast buffet standards, where the presentation of viennoiseries significantly impacts guest satisfaction scores. For instance, the Dubai Department of Economy and Tourism reported that Dubai welcomed 17.55 million overnight visitors between January and November 2025, reflecting a 5% rise compared to the same period in 2024[3]Source: Dubai Department of Economy and Tourism, "In-depth Research & Data Insights on Dubai's Economy", dubaidet.gov.ae. In January 2026, Oman's Salalah Mills Company launched a USD 65 million frozen bakery plant featuring 10 production lines and a 1,836-pallet refrigerated storage facility. This initiative, aimed at serving hotels, airlines, and catering companies across the GCC, highlights a strategic focus on Muscat's tourism growth, supported by Oman Vision 2040, to sustain demand for high-margin viennoiseries. Suppliers like Délifrance and Classic Fine Foods are already tapping into this trend by offering mini butter croissants in bulk packs designed for hotel buffets. Their product descriptions emphasize premium features such as AOC butter provenance and extended lamination times. The key takeaway: hospitality procurement is increasingly prioritizing freeze-thaw stability and portion consistency over cost, creating a market segment that remains unaffected by retail price competition.

Increased adoption of blast-freezing technology in in-store bakeries

Hypermarket chains such as Carrefour, LuLu, and Panda have enhanced their in-store bakeries by incorporating blast-freezing units. This enables them to produce items like croissants, muffins, and cookies in centralized commissaries, freeze them at -18°C, and distribute them to branches for final proofing and baking. This approach reduces labor costs by 30-40% compared to traditional scratch baking while retaining the aroma and visual appeal that drive impulse purchases. In the GCC, labor economics are a key driver of this trend: skilled bakers earn monthly salaries exceeding USD 2,000, and retail bakeries experience turnover rates of over 40% annually. As a result, centralized production and frozen distribution offer a more stable operating model. Additionally, the adoption of this technology creates a competitive barrier for smaller bakeries. Without blast-freezing capabilities, they cannot match the cost efficiency or consistency of larger chains, accelerating consolidation in favor of businesses with the resources to invest in cold-chain infrastructure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inconsistent cold-chain infrastructure leading to spoilage risks | -0.7% | Kuwait, Oman, Bahrain (secondary cities and rural distribution routes) | Short term (≤ 2 years) |

| Urban millennials shifting preference to fresh artisan bread | -0.5% | UAE, Saudi Arabia (Dubai, Riyadh, Jeddah affluent districts) | Medium term (2-4 years) |

| Mandates on salt- and trans-fat reformulation | -0.4% | Saudi Arabia, UAE, Kuwait (GSO 2483 compliance across all GCC states) | Long term (≥ 4 years) |

| Fluctuating refrigerated freight rates | -0.6% | All GCC states (import-dependent markets with 80-90% food imports) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Inconsistent cold-chain infrastructure leading to spoilage risks

Although national food-security mandates are in place, cold-chain infrastructure remains inconsistent outside primary urban corridors. This issue is particularly evident in Kuwait's interior governorates, Oman's Dhofar region, and Bahrain's rural areas, where refrigerated warehousing is limited, and last-mile delivery often depends on non-temperature-controlled vehicles. According to the Food and Agriculture Organization (FAO), inadequate cold chains account for 14% of global food loss. In the GCC, where summer ambient temperatures exceed 45°C, temperature excursions during distribution can make frozen bakery products unsalable within hours. The region's reliance on imports exacerbates this risk, as frozen bakery products often pass through 3-4 temperature zones (origin country, port, bonded warehouse, distributor, retailer) before reaching consumers, with each handoff increasing the likelihood of spoilage. To mitigate this, suppliers are over-engineering packaging by using thicker poly bags, vacuum-sealing, and nitrogen flushing. However, these measures increase landed costs by 8-12%, squeezing margins in a price-sensitive retail segment.

Urban millennials shifting preference to fresh artisan bread

Affluent millennials in Dubai, Riyadh, and Jeddah are increasingly favoring artisan bakeries that provide same-day sourdough, gluten-free loaves, and organic ingredients. They perceive frozen bakery products as inferior, even when taste profiles are comparable. This preference shift stems from growing health awareness, the visual appeal of artisan bread on social media, and a willingness to pay 2-3 times more for perceived authenticity. Laura Bakery in Sharjah and other boutique operators have successfully leveraged this trend by offering frozen croissants alongside freshly baked sourdough. This approach allows them to cater to both segments while positioning frozen products as a convenient option rather than a premium one. The hesitation is most evident in the 'free-from' category, where consumers seeking gluten-free or clean-label products distrust frozen formats, assuming fresh alternatives are healthier despite identical nutritional profiles. The strategic response involves premiumizing frozen offerings with transparent sourcing claims, enhancing packaging to convey artisan credentials, and targeting older demographics (35+) and expatriate families who are less influenced by artisan trends.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Institutional Bread Dominates, Viennoiserie Premiumizes

In 2025, the frozen bread segment led the GCC frozen bakery products market, accounting for 45.28% of the market share. Schools, hospitals, and catering firms have standardized products like baguettes, burger buns, and Arabic flatbreads to ensure consistent portion sizes. Hypermarkets are replicating freshness by baking goods in-store. By leveraging blast-freezer supply chains, they have reduced nightly preparation labor by one-third. Pizza crusts are gaining momentum due to the rise of dark kitchens, with par-baked bases enabling quick 12-minute oven cycles during peak delivery times. While muffins and cookies remain popular as impulse purchases at petrol marts, they contribute minimally to revenue. Specialty breads like focaccia cater to niche hotel menus but have not significantly influenced the overall trends in the GCC frozen bakery products market.

Frozen cakes and pastries are projected to grow at a rate of 6.87% through 2031, driven by hotel buffets that require buttery croissants and pain au chocolat with minimal on-site preparation. Almarai’s dominant 82.4% share of the croissant market in Saudi Arabia highlights the significant barriers to entry created by scale and research and development expertise. Salalah Mills is capitalizing on its 80-ton daily production capacity, focusing on exporting laminated dough to support Muscat’s growing tourism sector. Suppliers are differentiating themselves by promoting AOC butter origins or offering vegan recipes with quinoa to capture premiums in the free-from market. As labor shortages intensify, operators are increasingly outsourcing the complex lamination process, positioning viennoiserie as the premium growth driver in the GCC frozen bakery products market.

By Category: Conventional Still Rules, Free-From Gains Traction

In 2025, conventional SKUs accounted for 92.35% of the GCC frozen bakery products market, driven by consumer preference for familiar items like wheat-based croissants, flatbreads, and puff pastries. Retailers prioritize these conventional lines due to their high turnover rates, rotating weekly without requiring shopper education. Standardized halal certification further strengthens their position, simplifying the process for grocers and eliminating the need for SKU-by-SKU verification. Price-sensitive mainstream households favor value packs, ensuring consistent sales of six or more croissants through chest freezers. This trend supports the volume stability of the GCC frozen bakery products market.

Although "free-from" offerings represent only 7.65% of the market by value, they are projected to grow at a 7.71% CAGR through 2031. Expatriate consumers, influenced by UAE's Nutri-Mark labels that highlight fat and sugar content, are increasingly opting for gluten-free crusts and dairy-free brownies. Délifrance’s vegan croissant, which claims a 50% lower environmental footprint, targets eco-conscious millennials. However, the use of gluten-free rice or almond flours raises production costs by up to 60%, restricting distribution to upscale grocers and five-star hotels. Suppliers capable of achieving freeze-thaw stability without relying on gums or artificial emulsifiers are well-positioned to secure a competitive niche in the GCC frozen bakery products market.

By Distribution Channel: Off-Trade Holds Scale, On-Trade Accelerates

In 2025, off-trade venues, including hypermarkets, supermarkets, convenience stores, and e-commerce, accounted for 63.87% of the GCC frozen bakery products market. Carrefour and LuLu, two leading players, dedicate over 10 linear meters to frozen bakery sections and frequently offer BOGO promotions on croissants to attract customers. Online grocery shopping expanded in 2024, with platforms like Noon guaranteeing 24-hour frozen delivery to urban areas in the UAE and Saudi Arabia. Specialist bakeries are combining retail and foodservice by offering frozen trays for home baking alongside fresh loaves, increasing their margins without additional labor costs.

On-trade demand, which includes HORECA, institutions, and dark kitchens, is growing at a 7.02% CAGR. This growth is primarily driven by labor-constrained hotel kitchens that rely on thaw-and-serve pastries prepared each morning. Americana Group, previously focused on rapid outlet expansion, is now prioritizing same-store efficiencies. This shift is supported by the use of frozen dough inputs, which have reduced kitchen footprints by 40%. Dark-kitchen aggregators are favoring 10- to 20-unit dough packs, which provide flexibility across multiple virtual brands and create a distinct procurement tier. Suppliers capable of ensuring 48-hour lead times and maintaining HACCP-logged cold chains are securing multi-year contracts, stabilizing cash flow in the GCC frozen bakery products market.

Geography Analysis

In 2025, Saudi Arabia, supported by Almarai's market leadership, accounted for 40.46% of the GCC's frozen bakery market. Saudi Arabia continues to serve as the primary volume driver, with Vision 2030's extensive infrastructure projects and government-backed school meal programs consistently fueling demand for frozen bread and croissants. Almarai's vertically integrated supply chain ensures strict temperature control from its facilities in Riyadh to the most remote governorates, effectively insulating the company from volatile spot freight rates. Furthermore, the market's rigorous regulations concerning halal certification and nutritional labeling create significant barriers to entry, favoring well-established incumbents like Almarai.

Although the United Arab Emirates holds a smaller share of the market, it is projected to grow at a robust compound annual growth rate (CAGR) of 7.28% through 2031. This growth is primarily driven by Dubai's high levels of consumer spending and a revitalized tourism sector. The UAE is leveraging these factors to build momentum in the premium frozen bakery segment. Luxury hotel chains are increasingly demanding butter-rich viennoiseries that can be baked to a golden perfection within minutes, significantly enhancing guest satisfaction during breakfast services. Simultaneously, retailers in Abu Dhabi and Sharjah are aligning with this trend by offering mini croissants in resealable packaging, which encourages at-home entertaining and drives higher repeat purchase rates.

Smaller GCC states are adopting differentiated strategies to strengthen their positions in the frozen bakery market. In Oman, the Khazaen Economic City plant supplies premium frozen bakery products to Muscat’s luxury resorts while also targeting export opportunities in Kuwait and Qatar. Bahrain, on the other hand, leverages its efficient logistics network to pilot innovative products such as gluten-free muffins. These products are initially tested through quick-turnaround deliveries via Talabat before being rolled out across the broader GCC region. Collectively, these targeted approaches contribute to the overall resilience and growth of the GCC's frozen bakery products market.

Regulatory Landscape

Frozen bakery products sold across GCC countries are governed by a mix of harmonized Gulf standards issued through the GCC Standardization Organization (GSO) and country-specific food control requirements covering labeling, hygiene, and border clearance. For frozen processing and handling, suppliers commonly align operations to GSO-aligned codes of practice for quick frozen foods (e.g., GSO CAC/RCP 8:2015) and hygienic practice for refrigerated packaged foods with extended shelf life (GSO CAC/RCP 46:2021), while maintaining halal compliance and food-safety systems such as HACCP and FSSC 22000 to meet buyer and regulator expectations.

At the national level, Saudi Arabia enforces food and technical requirements through the Saudi Food and Drug Authority (SFDA), including compliance with relevant technical regulations for bakery formulations such as salt limits in bread (e.g., FD 2362/2018) and GMP expectations for food establishments. In the UAE, regulated food categories can require conformity documentation for customs clearance through Ministry of Industry and Advanced Technology (MoIAT) digital processes (Certificate of Conformity or a product status statement), and UAE Cabinet Resolution No. (28) of 2024 designates mandatory technical regulations for the food and agriculture sector. This increases the importance of correct product classification between ambient, refrigerated, and frozen bakery lines for importers and local manufacturers.

Competitive Landscape

The GCC frozen bakery market exhibits moderate concentration, with regional leaders such as Almarai, IFFCO, and Sunbulah collectively hold just over significant share in Saudi Arabia. At the same time, global players like Aryzta and Dawn Foods are penetrating the market through strategic food-service contracts. The market can be categorized into three distinct strategic clusters. Vertical integrators, such as Almarai, enhance their profitability by leveraging proprietary cold chain systems and operating diverse truck fleets that cater to multiple product categories. Asset-light companies, including ID Fresh, focus on contract manufacturing to efficiently scale the production of items like paratha and pizza dough while minimizing capital investment. Premium importers, such as Délifrance, target high-end establishments like five-star hotels, where they can command premium pricing, 2 to 3 times higher than retail, for their AOC-butter croissants. Regulatory compliance with standards such as halal, HACCP, and FSSC 22000 has become a critical requirement for market entry, creating a competitive advantage for established players who already meet these stringent criteria.

Mid-sized companies are carving out niches in the free-from and premium viennoiserie segments. Companies like Grupo Bimbo, Green Corp, and Marson’s Bakery are catering to upscale cafés by offering butter-rich croissants and muffins that are perfectly portioned for airline tray services. Suppliers to cloud kitchens are driving innovation by introducing frozen pizza bases designed for quick reheating within 10 minutes, effectively serving the needs of over 30 virtual brands. These companies are also expanding their market presence by acquiring local bakeries in key locations such as Jeddah and Dubai. This strategy not only broadens their customer base but also allows them to avoid the significant capital expenditures associated with building new production facilities.

Salalah Mills’ 80-ton daily production plant exemplifies the rise of state-supported challengers in the market. Meanwhile, ingredient innovators like Puratos are providing customized solutions, such as improvers, that enable local bakers to enter the frozen bakery segment effectively. Mondelez’s focus on freeze-and-thaw cakes highlights how multinational consumer packaged goods (CPG) companies view the GCC frozen bakery market as a testing ground for global product innovations. Consequently, the competitive dynamics in this market are shaped by the ability to master freeze-thaw technology, secure long-term partnerships with HORECA (hotels, restaurants, and catering) operators, and maintain flawless compliance with regulatory standards.

Gulf Cooperation Council Frozen Bakery Products Industry Leaders

-

Sunbulah Group

-

Americana Group Inc.

-

Almarai Company

-

Switz Group

-

Agthia Group

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Capacity-led import substitution and intra-GCC supply growth remains a visible whitespace, supported by capital deployment into integrated frozen bakery manufacturing and storage. In January 2026, Salalah Mills Companys Food Development Company opened a USD 65 million (RO 25 million) bakery products plant in Khazaen Economic City, Oman, with 10 production lines and 1,836-pallet refrigerated storage. This strengthens Omans ability to supply hotels, airlines, and catering buyers across the region with consistent frozen formats and improved cold-chain integrity.

Industry consolidation and technology transfer through regional M&A is also creating a pathway for faster scale-up in industrial frozen bakery. In December 2025, BinDawood Holding Company signed an agreement to acquire 51% of UAE-based Wonder Bakery for AED 96.9 million (USD 26 million), positioning Saudi-backed ownership to expand manufacturing reach and transfer technical operations into Saudi Arabia. This comes as institutional programs, HORECA procurement, and multi-unit foodservice operators standardize frozen bread, dough, and viennoiserie for labor and waste control. Alongside these moves, front-of-pack labeling adoption and GSO 2483 trans fat elimination referenced in the market context continue to reward suppliers that can reformulate and document compliance at scale while maintaining freeze-thaw performance for premium buffet and foodservice use cases.

Recent Industry Developments

- May 2026: Almarai announced a 40% increase in bakery production capacity to 2.8 million items per day to serve peak Hajj season demand. This capacity ramp-up reflects how large-scale producers in Saudi Arabia secure high-volume institutional and travel-related consumption windows that favor standardized frozen and par-baked formats.

- March 2026: Group AMANA completed an 8,718 sqm production facility expansion for Americana Foods in the UAE, including a 24-meter-high cold store. The added cold storage and processing footprint strengthens the region's frozen-food supply resilience and supports higher SKU complexity and distribution reach across GCC trade lanes.

- December 2024: Sunbulah Group announced a strategic collaboration with Unilever Food Solutions to develop frozen bakery products tailored for the HORECA channel across the GCC. The collaboration links product development with chef-led foodservice requirements, improving supplier relevance in hotels, catering, and chain restaurants where consistent bake-off performance and standardized portioning drive procurement decisions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of frozen bakery products sold across GCC countries through retail and foodservice routes. The scope counts finished frozen bakery items, whether sold as ready-to-bake dough or as frozen finished baked goods, in USD terms.

Scope exclusions: It excludes non-frozen fresh bakery and in-store baked items sold as fresh, along with broader frozen foods outside bakery.

Segmentation Overview

-

By Product Type

- Frozen Bread

- Frozen Cakes and Pastries

- Frozen Croissants

- Frozen Dough

- Frozen Pizza Crusts

- Frozen Muffins and Cookies

- Other Frozen Bakery Products

-

By Category

- Conventional

- Free From

-

Distribution Channel

- On Trade

-

Off Trade

- Supermarkets/Hypermarkets

- Convenience Stores

- Specialist Bakeries

- Online Retail Retails

- Others

-

By Geography

- United Arab Emirates

- Saudi Arabia

- Kuwait

- Qatar

- Oman

- Bahrain

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the country coverage, align definitions, and build the first demand and supply picture for frozen bakery in the GCC. We relied on public, non-paywalled sources such as national statistics portals and customs authorities in GCC countries, UN Comtrade for trade direction checks, FAOSTAT for supporting grain and food supply context, and food standards or labeling guidance shared by official regulators.

On top of this, we reviewed company annual reports, investor presentations, and press releases to understand capacity moves, product launches, and route-to-market shifts across retail and foodservice. For extra structure, we also used paid subscriptions limited to company financials and intelligence, patent databases, and an import-export shipment-level database to sanity check flows and packaging formats. The sources mentioned here are illustrative only and not exhaustive, and many other public references were also used for data collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what is actually sold as frozen bakery in the GCC, and how pricing and channel mix behave across the year. We spoke with a mix of manufacturers, distributors, cold-chain partners, and foodservice and retail buyers across the GCC, and then used follow-up checks to confirm pack sizes, typical price bands, and how volumes shift between on-trade and off-trade.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 12% | |

| Mid tier: 44% | Functional/Unit leaders: 31% | |

| Smaller Players: 17% | Managers: 57% |

Market-Sizing & Forecasting

For sizing, we used a top-down build that starts from GCC food consumption and trade signals, and then reconstructs the frozen bakery pool using country-level splits and channel shares. The model is then corroborated using selective bottom-up approximations, mainly sampled price points by product type multiplied by implied volumes, followed by distributor and cold-chain channel checks to adjust totals where needed.

Key inputs used (illustrative) included import and re-export patterns for frozen bakery and related preparations, freezer and cold-chain expansion signals, foodservice outlet growth and tourism-led demand indicators, changes in household consumption of convenience foods, and average selling price movement by pack type (retail packs versus bulk foodservice packs). When bottom-up evidence was patchy in a smaller GCC market, we filled gaps using calibrated per-capita consumption proxies and then corrected them using interview feedback on mix and seasonality.

Forecasting was done using scenario analysis, where variables such as population growth, foodservice recovery and expansion, cold-chain capacity additions, and pricing inflation were stressed into base, conservative, and faster-growth cases. The final forward curve was selected only after primary respondents agreed the assumptions were reasonable for each country and channel.

Data Validation & Update Cycle

Estimates are triangulated by comparing the final market totals against independent signals such as trade values, category growth statements from public filings, and the implied per-capita consumption outcome. If a country result shows an unusual jump, the drivers are rechecked, and the model is reopened to confirm channel splits, currency conversion timing, and the price-volume balance.

Before sign-off, the numbers go through a multi-step analyst review, and re-contacts are triggered when a key assumption shifts, such as a major capacity addition, a cold-chain disruption, or a clear inflation swing. Reports are refreshed annually, with interim updates for material events. Before delivery, we do a final pass to ensure the latest public information and respondent feedback are reflected.

Mordor Intelligence's Gcc Countries Frozen Bakery Product Market Estimate Compared With Other Published Estimates

Published market sizes for GCC frozen bakery can look different even when they use similar words, because the boundaries behind the numbers are not always the same. In our checks, the biggest differences usually come from what is counted as frozen bakery, how on-trade versus off-trade is treated, and how pricing is normalized across GCC currencies and years.

Import and re-export direction checks, plus channel-mix validation from distributors and foodservice buyers, are the evidence that keeps Mordor Intelligence tied to finished frozen bakery sold in the GCC and avoids pulling in adjacent frozen foods or broader bakery ingredients by mistake. Other estimates can also drift when they anchor to a different base year, apply a single ASP to all packs, or do not revisit assumptions after trade flow changes or cold-chain investments.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 301.56 M (2025) | |

| Regional Consultancy A | USD 300.00 M (2024) | Uses an earlier base year and appears to round the market total, with less visibility on how on-trade bulk packs are priced versus retail packs across GCC countries. |

| Industry Portal B | USD 280.23 M (2023) | Anchors the estimate to an older point in time and applies a longer forecast window, which can undercount recent channel recovery and does not clearly separate finished frozen bakery from nearby frozen categories. |

Overall, the spread is mainly explained by year selection and by how tightly the frozen bakery boundary is applied across products and channels. By keeping the steps transparent, using trade and channel evidence as guardrails, and then cross-checking price and volume logic, the final number stays repeatable and easier to audit.

Key Questions Answered in the Report

What is the forecast value of the GCC frozen bakery products market by 2031?

It is projected to reach USD 448.54 million, growing at a 6.71% CAGR over 2026-2031.

Which product type currently leads sales?

Frozen bread leads with 45.28% share, driven by institutional demand and in-store baking programs.

Which segment is expected to grow the fastest?

Frozen cakes and pastries are set to expand at a 6.87% CAGR, fueled by hotel and café demand for premium viennoiserie.

Why are dark kitchens important to suppliers?

They procure flexible pack sizes of frozen dough, prioritize quick turnaround, and are expanding rapidly in Dubai, Riyadh, and Kuwait City.

Page last updated on: