GCC And Africa ICT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

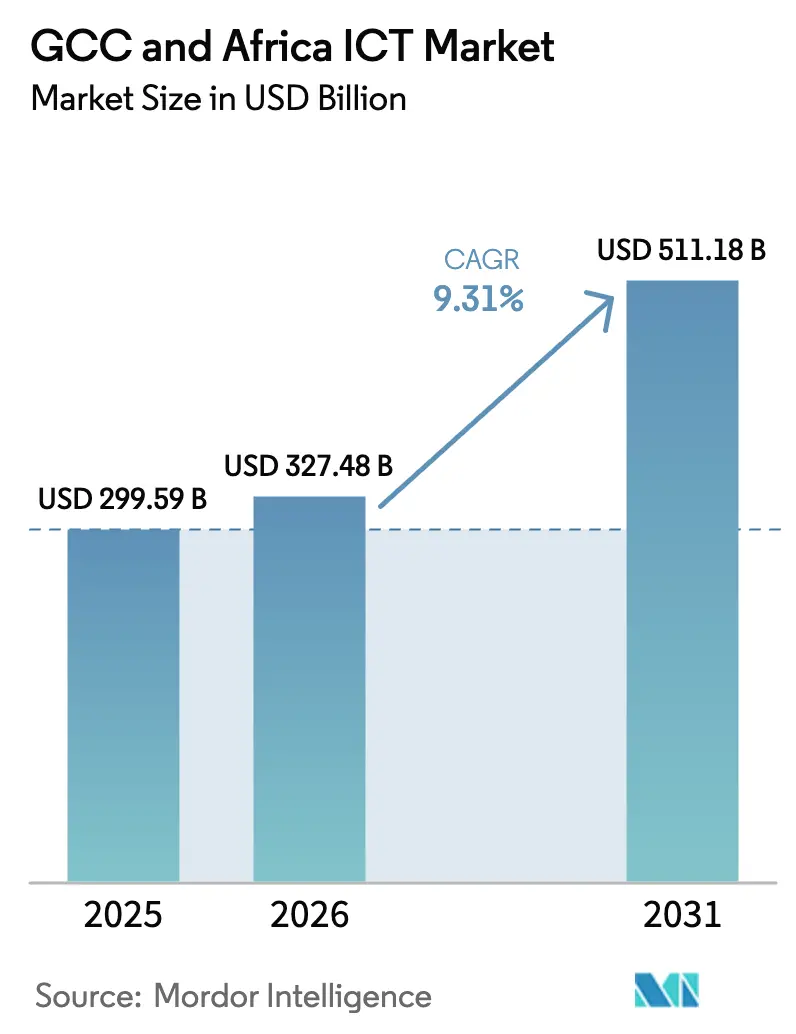

| Base Year Market Size (2025) | USD 299.59 Billion |

| Market Size (2026) | USD 327.48 Billion |

| Market Size (2031) | USD 511.18 Billion |

| Growth Rate (2026 - 2031) | 9.31% CAGR |

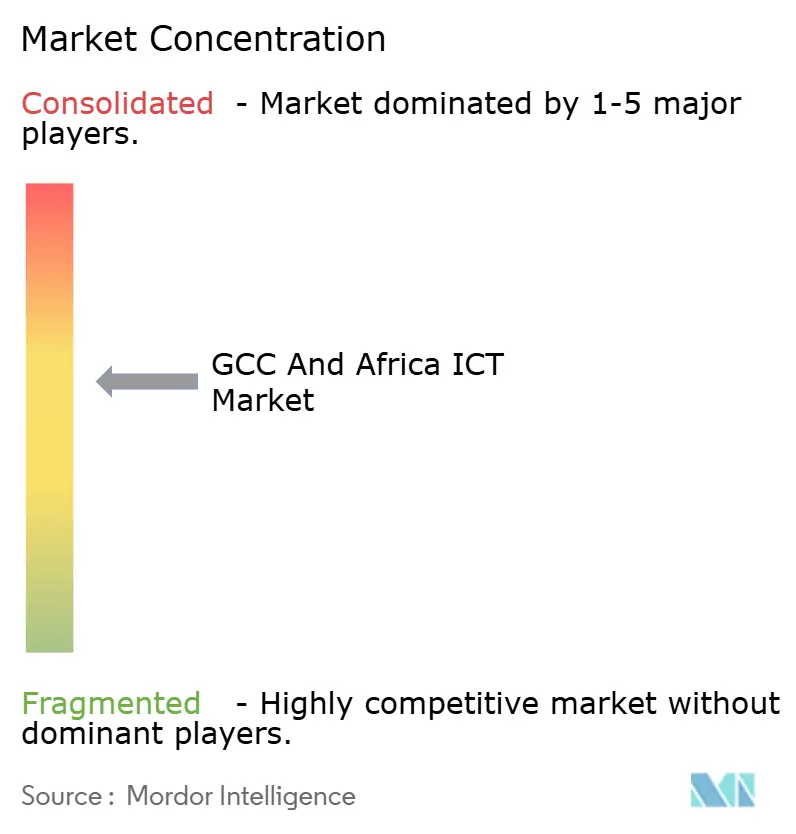

| Market Concentration | Medium |

Major Players-And-Africa-ICT-Market-ML.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC And Africa ICT Market Analysis by Mordor Intelligence

The GCC and Africa ICT market size is expected to grow from USD 299.59 billion in 2025 to USD 327.48 billion in 2026 and is forecast to reach USD 511.18 billion by 2031 at 9.31% CAGR over 2026-2031. Structural demand for advanced connectivity, cloud migration, and public–private digital initiatives drives this growth, while sovereign wealth funds have deployed more than USD 40 billion into regional gaming and technology ventures to accelerate diversification. Government programs such as Saudi Arabia’s USD 37.5 billion ICT infrastructure allocation and the UAE’s AI-2071 vision have created a stable pipeline of large projects that shield the sector from macroeconomic volatility. Fintech adoption, mobile money penetration, and youthful demographics underpin rapid expansion in key African markets, especially Nigeria, where mobile payments reached 51% of the adult population in 2024. Together, these factors sustain double-digit demand for managed services, cloud platforms, and localized software across the GCC and Africa ICT market.

Key Report Takeaways

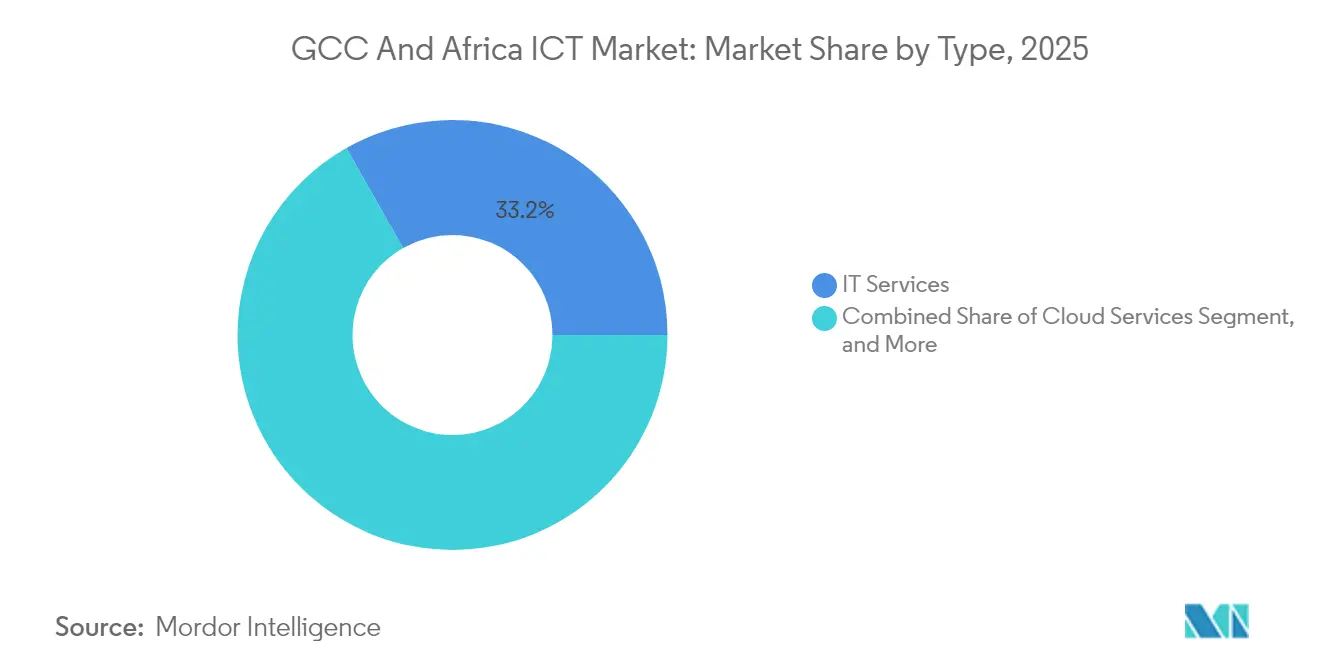

- By type, IT Services captured 33.22% of GCC and Africa ICT market share in 2025, while Cloud Services is projected to record the highest CAGR at 9.62% through 2031.

- By enterprise size, Large Enterprises accounted for 61.15% of GCC and Africa ICT market size in 2025; the SME segment is forecast to expand at a 9.74% CAGR to 2031.

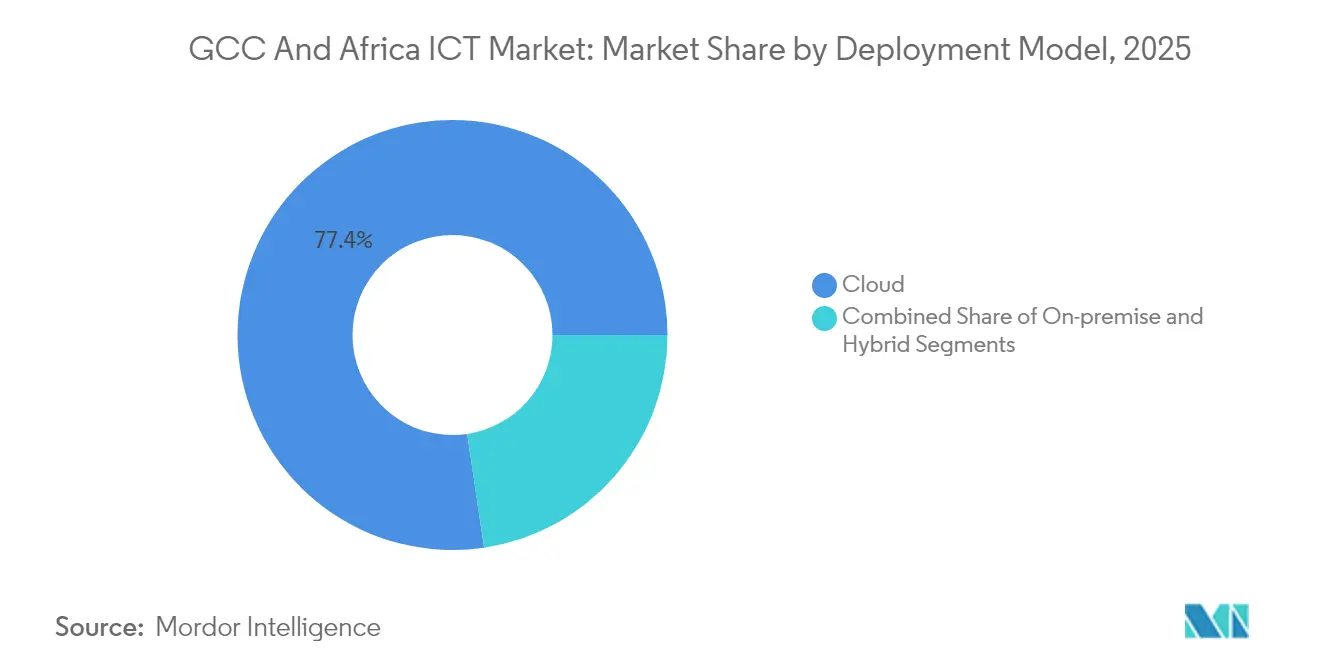

- By deployment model, cloud solutions represented 77.35% of GCC and Africa ICT market size in 2025, whereas hybrid deployments are advancing at a 10.08% CAGR during the same horizon.

- By end-user vertical, Government and Public Administration led with 20.78% revenue share in 2025; Gaming and Esports is expected to grow at a 10.35% CAGR through 2031.

- By country, Saudi Arabia held the largest single-country share at 18.05% in 2025, and Nigeria is predicted to post the fastest 10.22% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC And Africa ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Events-driven automation demand | +2.1% | GCC financial hubs; African urban centers | Medium term (2–4 years) |

| Government policies and PPP initiatives | +2.8% | Saudi Arabia, UAE, Nigeria, South Africa, Egypt | Long term (≥ 4 years) |

| Rising industrial digital transformation | +1.9% | UAE and South Africa manufacturing clusters | Medium term (2–4 years) |

| Rapid cloud and data-center expansion | +2.3% | GCC core; North and East Africa spillover | Short term (≤ 2 years) |

| Greener renewable-powered facilities | +0.7% | UAE, Saudi Arabia, Morocco, South Africa | Long term (≥ 4 years) |

| Surge in fintech and low-latency requirements | +1.6% | Nigeria, Kenya, UAE, Saudi Arabia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ongoing Events-Driven Automation Demand

Large infrastructure undertakings such as Saudi Arabia’s USD 500 billion NEOM smart-city program require frictionless, automated operations for utilities, security, and transportion. The UAE’s Mohammed bin Rashid Innovation Fund has deployed USD 2 billion to automate 90% of federal services, which compresses service-delivery times and raises citizen adoption. Nigeria’s automated clearing network processed over 2 billion transactions in 2024, cutting settlement periods from days to hours. In banking, intelligent KYC and AML platforms now reduce compliance costs by up to 40%, generating immediate productivity gains that reinforce automation’s pull on the GCC and Africa ICT market.

Government Policies and PPP Initiatives

Digital-first strategies codified in the UAE’s Digital Government Strategy 2025 require every ministry to migrate core workloads to the cloud, triggering USD 1.36 billion in public–private investments. Saudi Arabia’s National Industrial Development and Logistics Program channels USD 20 billion into PPP technology projects that embed 4.0 capabilities across factories and ports. Egypt has partnered with private carriers to extend fiber to 95% population coverage by 2030, an approach replicated by several African peers that lack upfront capital. Such frameworks lower fiscal burdens, accelerate knowledge transfer, and enlarge the addressable base for the GCC and Africa ICT market.

Rising Digital Transformation in Industries

The UAE’s Industrial Strategy 2031 targets USD 300 billion in output by embedding IoT and analytics into production lines; Emirates Steel has already achieved 15% energy savings from sensor-driven optimization In South Africa, 68% of manufacturers used predictive maintenance tools in 2024, narrowing unplanned downtime. Nigeria’s Dangote Group committed USD 2.5 billion to digitize supply chains, sidestepping chronic logistics bottlenecks. Government subsidies such as Saudi Arabia’s 50% grant for projects above USD 10 million compress payback periods, keeping industrial digitalization on a steep trajectory inside the GCC and Africa ICT market.

Rapid Cloud and Data-Center Expansion

Amazon Web Services has earmarked USD 5 billion for new regions in Saudi Arabia and the UAE, ensuring local availability zones that satisfy sovereignty mandates. Microsoft Azure expanded services to 18 African nations through marketplace partnerships, improving latency for enterprise workloads and enabling compliance with emerging data-residency rules. Regional data-center spend reached USD 3.49 billion in 2024 and is forecast to double by 2030 as carriers and OTT platforms chase edge capacity. This infrastructure boom underpins multicloud growth and pushes the GCC and Africa ICT market toward service-centric revenue streams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent skills deficit and expatriate need | −1.8% | GCC tech roles; Sub-Saharan Africa | Long term (≥ 4 years) |

| Cyber-security and data-sovereignty hurdles | −1.2% | GCC finance hubs; African public sector | Medium term (2–4 years) |

| Oil-price-linked IT-budget volatility | −0.9% | Hydrocarbon economies | Short term (≤ 2 years) |

| Regulatory fragmentation in Africa | −0.7% | Cross-border operators | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Skills Deficit and Expatriate Reliance

Saudi Arabia identified a 40% shortfall in cybersecurity talent, prompting the USD 500 million Saudi Cybersecurity Institute to train 10,000 specialists by 2030. South Africa’s sector education authority lists 70,000 open ICT roles, and 60% of firms still depend on expatriates for advanced positions. Nigeria has partnered with Microsoft to train 5 million citizens by 2025, yet inconsistent power supply and limited broadband slow progress. Across the UAE, 80% of senior technical posts are foreign-filled despite USD 1 billion in local upskilling funds, signaling a long-tail talent drag on the GCC and Africa ICT market.

Cyber-Security and Data-Sovereignty Hurdles

The UAE logged a 250% surge in cyberattacks on banks during 2024, compelling the Central Bank to tighten security standards that add 15–20% to deployment costs. Saudi Arabia’s National Cybersecurity Authority now requires Essential Cybersecurity Controls certification before vendors can sign public contracts, extending procurement cycles. Nigeria records 18,000 daily cyber-intrusion attempts, stretching limited defensive budgets and delaying digital rollouts. Divergent data-localization rules between GCC monarchies and African states complicate multi-country architectures, adding compliance overhead that tempers growth in the GCC and Africa ICT market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Services Retain Dominance while Cloud Scales Rapidly

IT Services held 33.22% of GCC and Africa ICT market share in 2025, reflecting entrenched demand for managed support amid ongoing skill shortages. Strong annuity revenue from outsourcing and maintenance stabilizes cash flows, even when capex cycles pause. Cloud Services, although smaller in absolute terms, is expanding at a 9.62% CAGR as public-sector cloud-first mandates and enterprise ERP migrations converge. The segment is set to add USD 46.3 billion to GCC and Africa ICT market size by 2031. Hardware revenues are flat because commoditized computing and falling unit prices erode margins, but security appliances remain an exception, benefiting from heightened risk awareness. Communication Services receive a lift from 5G rollouts; Saudi Telecom Company reached 85% population coverage, creating fresh opportunities in IoT and edge workloads. Overall, as workloads shift upward in the technology stack, advisory, implementation, and subscription-based delivery models command premium valuations in the GCC and Africa ICT market.

By Enterprise Size: SMEs Advance despite Large-Enterprise Scale

Large Enterprises controlled 61.15% of spending in 2025 owing to complex, multi-vendor estates that require end-to-end service bundles. Many added secure connectivity, sovereign clouds, and AI governance to existing contracts, thereby deepening wallet share for integrators. In contrast, SMEs are posting a 9.74% CAGR through 2031 as affordable SaaS and fintech platforms override earlier adoption barriers. Saudi Arabia’s Monsha’at agency earmarked USD 3.2 billion for SME digital support, pushing cloud penetration among firms with fewer than 250 staff to 78%. In Africa, mobile-first finance lowers entry costs; Kenya’s M-Pesa processed more than USD 50 billion in annual value, demonstrating how fintech ecosystems trigger platform uptake. As enterprise software vendors roll out tiered pricing and turnkey bundles, SME spending will inject steady incremental demand into the GCC and Africa ICT market.

By Deployment Model: Cloud Dominates while Hybrid Gains Momentum

Cloud captured 77.35% of 2025 spending as enterprises migrated non-sensitive workloads for cost and agility advantages, embedding a services-centric revenue bias into the GCC and Africa ICT market size. Growing maturity around cloud security frameworks widens the use-case set, but data localization statutes and industry regulations force many agencies to adopt hybrid architectures. Hybrid deployments are rising at 10.08% CAGR; the Saudi Data and AI Authority mandates hybrid stacks for agencies handling personal data, effectively institutionalizing multi-cloud procurement. On-premise estates persist in capital-intensive utilities and core banking, yet their share continues to recede. Edge computing driven by IoT and 5G pushes micro-data-center adoption, reinforcing hybrid’s role as a bridge between public cloud scale and localized processing demands across the GCC and Africa ICT market.

By End-User Vertical: Government Leads while Gaming Accelerates

Government and Public Administration delivered 20.78% of 2025 revenue, anchored by smart-city and e-government programs across the GCC. Dubai’s digital initiative alone processed 90% of services online by 2024. The sector continues to anchor first-mover adoption of AI, identity platforms, and blockchain registries. Gaming and Esports, although currently a niche, expands at 10.35% CAGR on the back of Saudi Arabia’s USD 38 billion strategy to build a global gaming hub. BFSI sustains modernization via open-banking APIs and real-time payment rails, whereas Energy and Utilities integrate AI-driven asset monitoring to hold down OPEX. Tele-health and electronic medical records lift Healthcare, particularly in Nigeria where the National Health Insurance Scheme digitized services for 200 million citizens. As retailers embrace omni-channel and last-mile logistics technology, end-vertical diversification will buffer cyclical shocks and sustain the GCC and Africa ICT market growth trajectory.

Geography Analysis

The GCC states account for the majority of topline value owing to sustained capital expenditure in infrastructure and government digital services. Saudi Arabia committed USD 37.5 billion to national ICT programs in 2024, a figure that underpins regional leadership and deepens local capacity. The UAE’s liberal ownership framework attracts hyperscalers and global software vendors seeking regional headquarters, while Qatar channels hydrocarbon surpluses into 5G and smart-stadium development. Kuwait and Bahrain nurture fintech sandboxes that expedite licensing, giving them specialized roles within the wider GCC and Africa ICT market.

African markets deliver volume growth and user-base expansion. Nigeria received USD 520 million in disclosed technology investment during 2024, driven by record mobile-money volumes and venture capital interest. South Africa remains the continent’s software and data-center nexus, but growth is constrained by power-grid instability that raises operating costs. Egypt’s New Administrative Capital and subsea cable landings strengthen its ambition to operate as a regional ICT bridgehead.

Cross-regional flows are intensifying. Mubadala’s USD 400 million Africa Tech Fund and Saudi Arabia’s equity stakes in African e-commerce platforms exemplify how GCC capital meets African innovation.These reciprocal investments stimulate joint ventures, unify standards, and unlock economies of scale, effectively knitting two high-potential regions into a contiguous opportunity set for the GCC and Africa ICT market.

Competitive Landscape

Competition is moderate and increasingly partnership-driven. Microsoft’s USD 1.5 billion investment in UAE-based G42 gives the U.S. firm cultural proximity and compliance leverage in sensitive AI workloads.[1]Microsoft Corporation, “Microsoft and G42 Form Strategic Partnership,” blogs.microsoft.com Oracle, IBM, and AWS compete for sovereign-cloud contracts, often pairing with incumbent telcos such as Emirates Telecommunications Group or Saudi Telecom Company to secure data-center real estate and in-country licensing. Local champions benefit from customer intimacy and Arabic localization but still rely on global partners for advanced tooling, making ecosystem alignment a critical success factor across the GCC and Africa ICT market.

Vertical specialization now differentiates contenders. Islamic fintech, Arabic natural-language processing, and cross-border payment hubs require nuanced regulatory fluency, favoring hybrid operating models that blend local equity with international IP. Cybersecurity service providers see white-space opportunity as statutory frameworks tighten; demand for managed detection and response outpaces indigenous supply, opening room for niche entrants. Edge-computing and colocation vendors battle for first-mover advantage near 5G base-stations, where low latency supports gaming, telemedicine, and industrial IoT.

Strategic moves in 2024–2025 reflect scaling intent. IBM used AWS Marketplace to open access in 18 African countries, reducing go-to-market friction, while Cisco announced a USD 1 billion AI fund focusing on regional startups. Telecom operators diversify into cloud resell and fintech, broadening revenue angles beyond pure connectivity. The net effect is a competitive environment that rewards collaborative portfolios and compliance acuity, positioning the GCC and Africa ICT market for accelerated yet disciplined expansion.

GCC And Africa ICT Industry Leaders

Microsoft Corporation

HP Inc.

SAP SE

Alphabet Inc. (Google LLC)

International Business Machines Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: MTN Group earmarked USD 300 million through 2027 to upgrade Cameroon’s 5G network and construct edge data centers for regional traffic aggregation.

- December 2024: Microsoft and NVIDIA created a USD 30 million fund for African AI startups in healthcare, agriculture, and finance, bundling cloud credits and mentorship programs.

- November 2024: Oracle and Google Cloud deepened their alliance to offer joint AI analytics stacks with in-region data residency across the Middle East and Africa.

- October 2024: IBM broadened availability of AI and hybrid-cloud solutions to 18 African markets via AWS Marketplace integration.

GCC And Africa ICT Market Report Scope

The ICT market in the GCC and Africa is defined based on the revenues generated from the integration and adoption of different information and communications technologies (ICT), such as big data, mobility, storage, outsourcing, and cloud computing, among others, in various end-user industries across the GCC and Africa. The analysis is based on the market insights captured through secondary research and primaries. The study also covers the major factors impacting the growth of the market in terms of drivers and restraints.

The ICT market in the GCC and Africa is segmented by technology (big data analytics, mobility and telecom, cloud computing, storage, business process outsourcing, other technologies), component (hardware/devices, software and services, communication and connectivity), end-user industry (oil, gas, and utilities, travel and hospitality, healthcare, financial services, manufacturing and construction, other end-user industries), and region/country (GCC [Saudi Arabia, United Arab Emirates, Qatar, Oman, Kuwait, Bahrain], Africa [Egypt, South Africa, Nigeria, Rest of Africa]). The report offers the market forecasts and size in value terms in USD for all the above segments.

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | Managed Services |

| Business Process Services | |

| Business Consulting Services | |

| Cloud Services | |

| IT Infrastructure | |

| IT Security | |

| Communication Services |

| Small and Medium Enterprises |

| Large Enterprises |

| On-premise |

| Cloud |

| Hybrid |

| Government and Public Administration |

| BFSI |

| Energy and Utilities |

| Retail, E-commerce and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| (Up/Mid/Down-stream) |

| Gaming and Esports |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Oman |

| Kuwait |

| Bahrain |

| Egypt |

| South Africa |

| Nigeria |

| By Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | Managed Services | |

| Business Process Services | ||

| Business Consulting Services | ||

| Cloud Services | ||

| IT Infrastructure | ||

| IT Security | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By Deployment Model | On-premise | |

| Cloud | ||

| Hybrid | ||

| By End-user Industry Vertical | Government and Public Administration | |

| BFSI | ||

| Energy and Utilities | ||

| Retail, E-commerce and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| (Up/Mid/Down-stream) | ||

| Gaming and Esports | ||

| By Country | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Oman | ||

| Kuwait | ||

| Bahrain | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

Key Questions Answered in the Report

How large is the GCC and Africa ICT market in 2026?

The sector is valued at USD 327.48 billion for 2026 and is projected to reach USD 511.18 billion by 2031.

Which segment grows fastest in regional ICT spending?

Cloud Services leads with a 9.62% CAGR through 2031, fueled by multiple government cloud-first mandates.

Why is Nigeria considered a high-growth ICT country?

Fintech penetration, youthful demographics, and a 10.22% forecast CAGR make Nigeria the region’s quickest-expanding market.

What drives the switch to hybrid cloud architectures?

Data-sovereignty rules and latency-sensitive apps compel agencies to balance public-cloud scalability with localized processing.

Which vertical shows the highest future CAGR?

Gaming and Esports is expected to grow at 10.35% through 2031 due to heavy sovereign-wealth-fund backing.

How are skills shortages being addressed?

Initiatives like Saudi Arabia’s USD 500 million cybersecurity institute and Microsoft-backed training pledges aim to close specialist gaps over the next decade.

Page last updated on: