Africa Data Center Networking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

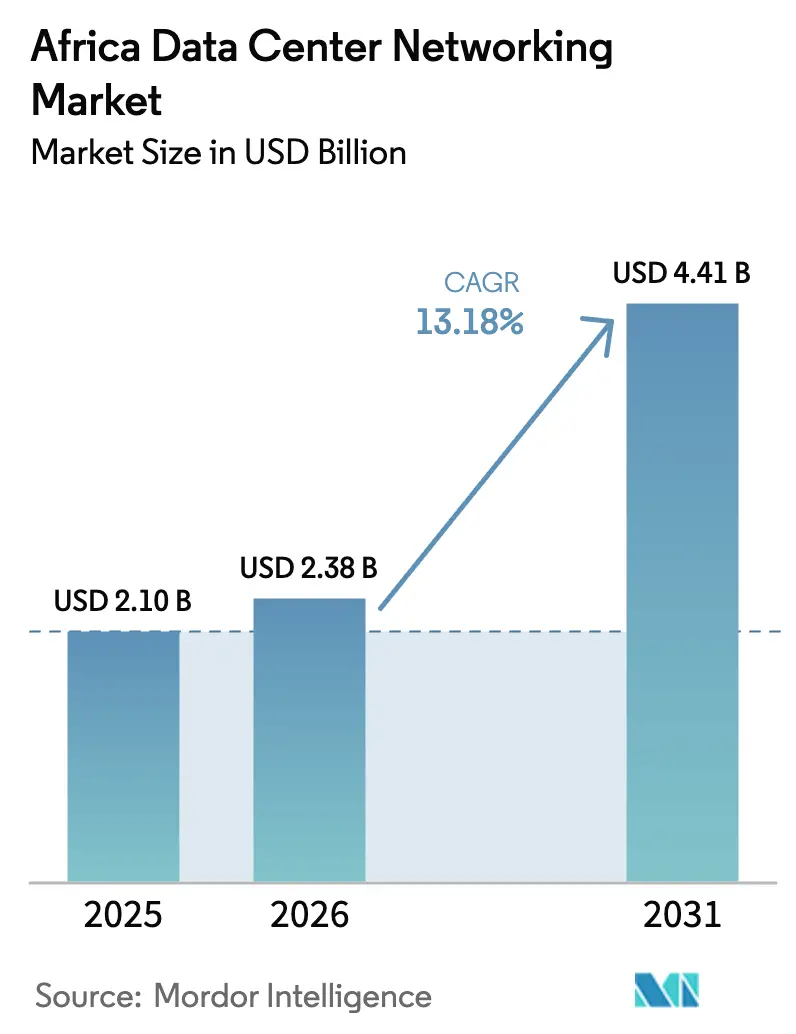

| Base Year Market Size (2025) | USD 2.1 Billion |

| Market Size (2026) | USD 2.38 Billion |

| Market Size (2031) | USD 4.41 Billion |

| Growth Rate (2026 - 2031) | 13.18% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Africa Data Center Networking Market Analysis by Mordor Intelligence

The Africa data center networking market size is expected to grow from USD 2.1 billion in 2025 to USD 2.38 billion in 2026 and is forecast to reach USD 4.41 billion by 2031 at 13.18% CAGR over 2026-2031. Continuous cloud region launches, AI workload demands, and national data-sovereignty rules are the main catalysts behind this vigorous trajectory. Extensive subsea-cable projects deliver fresh international bandwidth that feeds hyperscaler entry, while local carriers and colocation operators upgrade switching fabrics to 50-100 GbE architectures to cope with rising east-west traffic. Government incentives, especially in South Africa, Nigeria, Kenya, and Egypt, steer investments toward sustainable designs that blend renewable power with liquid-cooling topologies. At the same time, widespread adoption of white-box hardware trims capital outlays by up to 70%, giving domestic integrators room to compete with global brands. Skills shortages, power-grid instability, and complex import duties persist as restraining factors, yet they are spurring demand for managed services and modular micro-sites that tolerate volatile utility conditions.

Key Report Takeaways

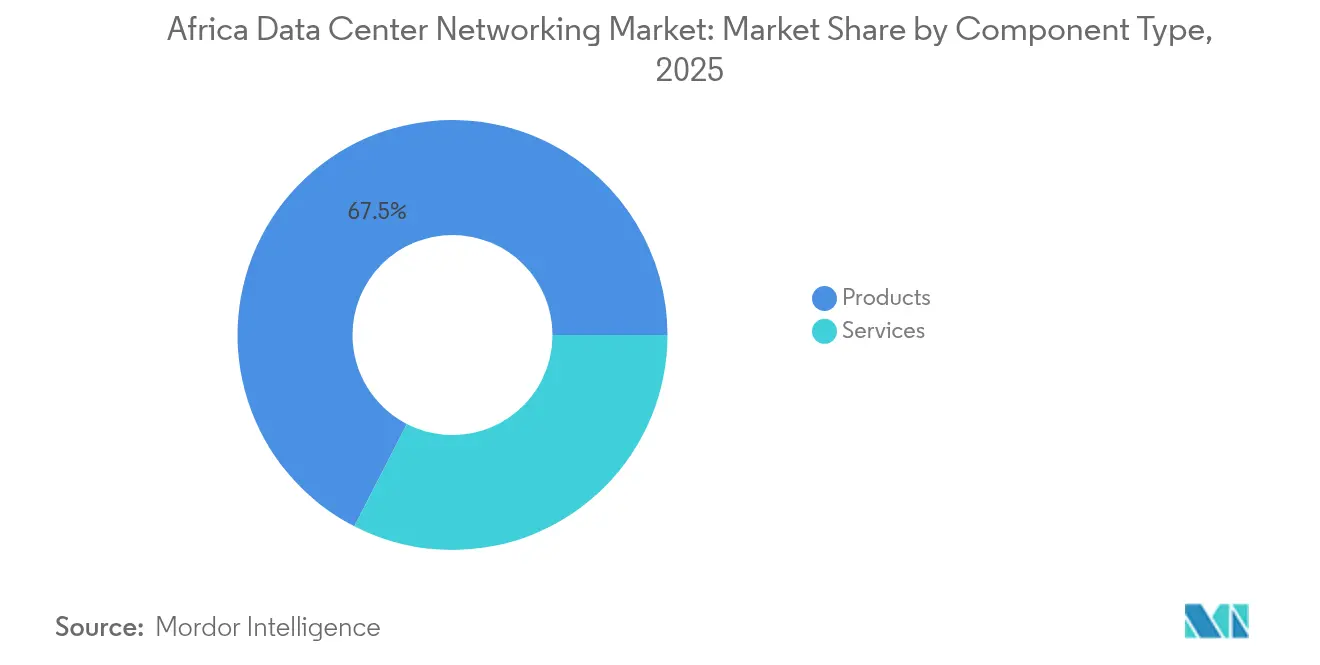

- By component, products led with 67.45% of the Africa data center networking market share in 2025, while services are projected to expand at a 14.08% CAGR to 2031.

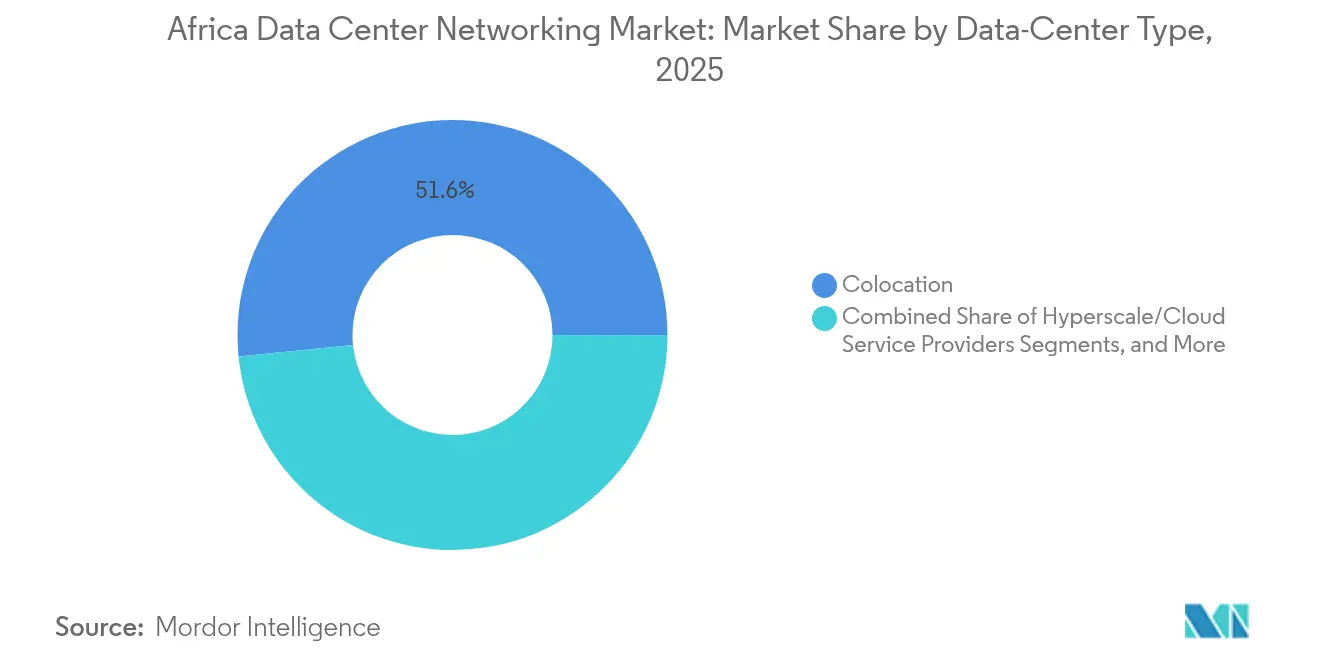

- By data-center type, colocation held 51.60% of the Africa data center networking market share in 2025; hyperscalers are set to grow at a 15.02% CAGR through 2031.

- By bandwidth, 50-100 GbE accounted for 37.55% share of the Africa data center networking market size in 2025, and >100 GbE is advancing at a 15.92% CAGR to 2031.

- By end-user, IT and telecommunications captured 32.65% share of the Africa data center networking market size in 2025, while government and defense are posting the fastest 14.72% CAGR to 2031.

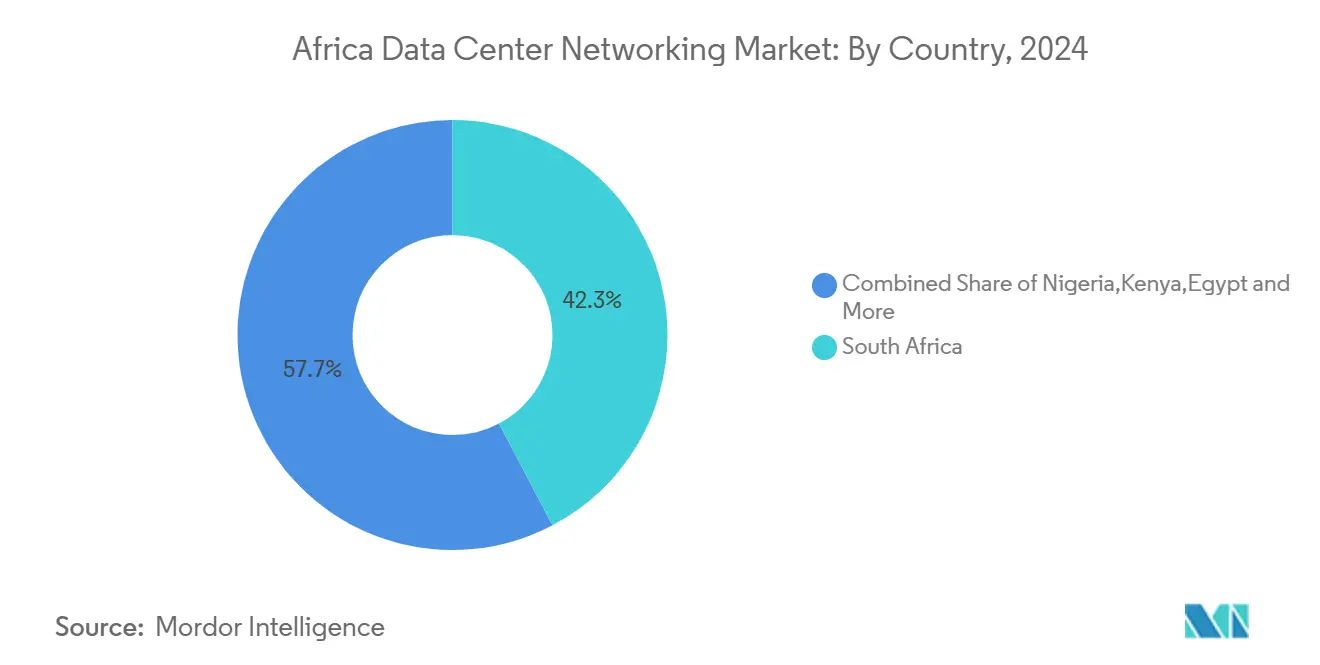

- By geography, South Africa commanded 41.85% of the Africa data center networking market share in 2025; Kenya is on track for the strongest 13.76% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global valuation is built by aggregating outputs from multiple regions, with Africa forming one of the important contributors. Mordor Intelligence's global data center networking market size report represents that cumulative total.

Africa Data Center Networking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of hyperscale and cloud deployments | +2.8% | South Africa, Nigeria, Kenya | Medium term (2-4 years) |

| Rising cyber-attack surface and compliance mandates | +1.9% | South Africa, Nigeria | Short term (≤ 2 years) |

| Surge in mobile data traffic and OTT content | +2.1% | Nigeria, Kenya, Egypt | Medium term (2-4 years) |

| Government-backed national data-residency policies | +1.7% | Morocco, South Africa, Nigeria | Long term (≥ 4 years) |

| Sub-sea cable landings enabling low-latency peering | +1.4% | West and East African coastal regions | Medium term (2-4 years) |

| Adoption of white-box/open networking to cut TCO | +1.6% | Cost-sensitive markets across Sub-Saharan Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Hyperscale and Cloud Deployments

Hyperscalers are reshaping the Africa data center networking market as Microsoft, Google, and Amazon Web Services commit fresh capital for sovereign cloud zones. Microsoft’s USD 298 million South African program delivers AI-ready fabrics built around 25 GbE leaf and 100 GbE spine layers that support large-language-model training. Google’s Johannesburg cloud region, live since early 2024, shows latency reductions of 80 milliseconds compared with Amsterdam routes, prompting regional SaaS firms to migrate workloads. Each new cloud availability zone triggers parallel investments in carrier-neutral meet-me rooms, dark-fiber routes, and open-bridged 400G optical uplinks that feed the new campuses. In Senegal, AWS partners with Sonatel to deliver sub-5 millisecond services for fintech workloads, underlining how sovereign cloud regions spur a multiplier effect on switching, routing, and interconnection spending.[1]Ecofin Agency, “AWS Partners with Sonatel for Senegal Cloud Zone,” ecofinagency.com

Rising Cyber-Attack Surface and Compliance Mandates

Tighter privacy statutes increase capital allocation toward secure switching fabrics and micro-segmented leaf layers. South Africa’s POPIA forces enterprises to deploy next-generation firewalls, zero-trust overlays, and telemetry-rich routers able to export flow data for audit trails.[2]Baker McKenzie, “South Africa National Data and Cloud Policy,” bakermckenzie.comBanks in Nigeria and South Africa are early adopters of secure SD-WAN, illustrated by African Bank’s Fortinet rollout that halved WAN expense while meeting PCI DSS rules. Compliance extends beyond finance as healthcare and public-sector clouds must maintain encrypted east-west pathways and demonstrate deterministic data-residency enforcement. Demand therefore migrates toward intent-based fabrics with embedded crypto engines and AI-driven anomaly detection that shortens mean-time-to-detect from hours to minutes.

Surge in Mobile Data Traffic and OTT Content

Sub-Saharan broadband users doubled between 2019 and 2023, forcing carriers to backhaul petabytes of video and gaming traffic through coastal landing stations[3]Baker McKenzie, “South Africa National Data and Cloud Policy,” bakermckenzie.com. The 2Africa cable introduces 180 Tbit/s of design capacity that plugs directly into new Egyptian and Kenyan carrier-hotels, accelerating orders for 50/100 GbE top-of-rack switches in peering rooms. Google’s Equiano cable has already cut consumer broadband prices by 14% in Togo and doubled average speeds, proving that fresh subsea supply converts rapidly into data-center port demand. Operators now interconnect with content platforms through Ethernet virtual-private networks that offload 40% of video streams onto local caches, trimming international transit costs and enhancing user experience.

Government-Backed National Data-Residency Policies

Localisation rules continue to anchor traffic within borders, effectively guaranteeing baseline demand for switching gear, firewalls, and intelligent load balancers. South Africa’s National Data and Cloud Policy obliges agencies to host sensitive workloads on in-country systems that pass FIPS-valid encryption standards. Niger’s USD 14.3 million Tier III public datacenter and Morocco’s Digital Morocco 2030 plan illustrate how public funding catalyses private co-investment. Sovereignty requirements also influence topology, steering networks toward geo-redundant metro clusters rather than offshore replication targets, which intensifies purchase volumes for dual-core routers, cross-metro DWDM links, and synchronous replication fabrics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating network complexity in multi-cloud fabric | -1.2% | Large enterprises across Africa | Medium term (2-4 years) |

| Scarcity of skilled DC networking professionals | -1.8% | Sub-Saharan Africa | Long term (≥ 4 years) |

| Power-grid instability affecting facility uptime | -1.3% | Nigeria, Kenya, Ghana, parts of Southern Africa | Short term (≤ 2 years) |

| Import-tariff complexities inflating hardware costs | -1.0% | Economies with high customs duties (e.g., Nigeria, Tanzania) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Network Complexity in Multi-Cloud Fabric

African enterprises adopting multi-cloud strategies face inconsistent performance, tool sprawl, and higher operational costs. A South African retail bank needed five different control planes to secure traffic across two local clouds and one European zone, resulting in configuration drift and extended change windows. Limited in-house expertise pushes organisations toward managed overlay networks that raise opex even while solving skill gaps. The situation delays the adoption of software-defined fabrics and stalls the migration of latency-sensitive apps such as digital trading platforms.

Scarcity of Skilled DC Networking Professionals

Demand for CCIE-, JNCIE-, and HCIE-level engineers far exceeds supply. Across the region, fewer than 4,000 professionals possess hands-on experience with large-scale leaf-spine deployments, according to African Union digital-skills data. This deficit forces many projects to import contractors from Europe or the Middle East, adding 12–20% to overall project cost and extending roll-out schedules. The talent shortfall particularly hampers white-box switching adoption because those platforms depend on Linux command-line fluency and DevOps tooling unfamiliar to most local engineers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Products Dominate Despite Services Acceleration

Products retained 67.45% of the Africa data center networking market share in 2025, as every facility still requires a baseline of physical switches, routers, and optical transport gear. Ethernet switches remain the largest revenue contributor because leaf-spine designs rely on high-port-density TOR units coupled with low-latency spine blocks. Routing continues to find purchase within campus cores, internet gateways, and data-center interconnects that link metro nodes to subsea landing stations. Security appliances and ADCs are gaining momentum as zero-trust and SSL offload proliferate.

Services are scaling faster at a 14.08% CAGR through 2031 as enterprises aim to bridge operational skill deficiencies. Installation and integration engagements are the first port of call for hyperscaler newcomers that want assured time-to-market. Managed network services deliver continuous operations support, freeing local IT teams to focus on application enablement. Training and consulting lines are growing because large multinationals attempt to build regional centres of excellence that can eventually own leaf-spine operations internally. Support and maintenance revenues likewise climb as SLA-sensitive sectors such as finance and healthcare demand four-nines uptime.

By End-User: IT and Telecommunications Lead, Government Accelerates

IT and telecommunications players accounted for 32.65% of the Africa data center networking market size in 2025 as they deploy dense fabrics to host customer VMs, OTT caches, and 5G core functions. Telcos are refreshing edge aggregation sites from 10 GbE to 25 GbE in preparation for ultra-reliable low-latency traffic while also investing in segment routing to control inter-city paths. Cloud-native ISPs embrace white-box units running SONiC, which lowers capital spending by 40% relative to branded stacks and shortens lead times amid global supply constraints.

Government and defence workloads exhibit the swiftest growth at 14.72% CAGR. National clouds, e-health repositories, and smart-city telemetry demand encrypted 100 GbE links across redundant availability zones. Ministries adopt private access service edges that place inspection functions inside the core rather than at the perimeter, which changes traffic flow patterns and increases east-west bandwidth needs. Defence agencies also prioritise on-premise AI inference to analyse drone footage, thereby driving requests for GPU-aware network topologies.

By Data-Center Type: Colocation Dominates, Hyperscalers Surge

Colocation facilities represented 51.60% of Africa data center networking market share in 2025, reflecting the strong preference for opex models that avoid large upfront capital commitments. Neutral sites such as Teraco Johannesburg enable enterprises to reach multiple subsea cables and cloud on-ramps through a single cross-connect, which lowers latency and simplifies redundancy planning. Dense cross-connect fabrics require high-availability spine layers with dual supervisors and real-time telemetry to track port-to-port performance.

Hyperscalers are the fastest-growing category at 15.02% CAGR as Microsoft, Google, and Oracle continue their multi-billion-dollar buildouts. Their campuses opt for 100 GbE and 400 GbE optical uplinks wired in Clos-4 topologies optimised for AI clusters. Procurement teams tend to select merchant-silicon switches in fixed 32-port form factors, which accelerates port rollout and aligns with the hyperscaler philosophy of horizontal scale. The hyperscaler wave is also elevating demand for campus dark-fiber routes because organisations require diverse paths to ensure sub-5-millisecond round-trip times between metros.

By Bandwidth: 50-100 GbE Leads, Greater than 100 GbE Accelerates

50-100 GbE links held 37.55% share of the Africa data center networking market size in 2025. This sweet-spot range offers a cost-performance balance for mixed workloads ranging from virtual desktop infrastructure to basic AI inference. Enterprises upgrading from 10 GbE find that 25 GbE disassembled breakout features allow gradual migration without forklift replacements.

Bandwidth above 100 GbE will rise at a 15.92% CAGR through 2031, driven by AI training farms, real-time analytics, and latency-sensitive fintech services. Afrihost’s Mellanox-based network delivers 400G uplinks across metro fibre rings, saving 20% on optics thanks to QSFP-DD standardisation. Optical transponder suppliers expect volume shipments of 800G coherent pluggables by 2027, which should usher in spine upgrades that further push the Africa data center networking market adoption of high-speed lanes.

Geography Analysis

South Africa maintained 41.85% of the Africa data center networking market share in 2025, thanks to its robust submarine-cable endpoints and mature power grid. International firms favour Johannesburg and Cape Town for primary and disaster-recovery nodes because the two metros already host extensive cloud on-ramps, carrier hotels, and internet exchanges. Government policy reinforces this position, with the Digital Transformation Infrastructure Roadmap promising expedited permits for new data-hall expansions.

Kenya is the fastest-growing national market at 13.76% CAGR through 2031. The Microsoft-G42 geothermal campus south of Nairobi improves sustainability metrics and introduces 100 GbE leaf layers pre-wired for 400G spine upgrades. Nairobi’s two new neutral IXPs encourage local content caching, cutting backhaul costs by 35% and boosting demand for TOR switch ports. Kenya’s special economic zone concessions waive import duties on optics and fibre, which improves project IRRs and accelerates new market entrants.

Nigeria, Egypt, and Morocco round out the second tier of expansion. Lagos-area facilities now connect directly to Equiano and 2Africa, pushing average latency to Western Europe below 120 milliseconds, while Cairo leverages its junction position between Mediterranean and Red Sea routes to attract serving points for North African OTT subscriptions. Morocco’s Digital Morocco 2030 blueprint targets data-center energy intensity under 1.3 PUE by prioritising renewable power purchase agreements, leading to pilot projects with liquid-cooled racks that require specialised manifolded topologies. Elsewhere, emerging hubs such as Dakar and Abidjan rely on Public–Private Partnerships to finance Tier III designs that seed connectivity and gradually grow regional share of the Africa data center networking market.

Coverage of the data center networking market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for South America, Middle East, and Asia, alongside detailed country-level intelligence for South Africa, Nigeria, Chile, Brazil, Saudi Arabia, and Malaysia, each shaped by local operating conditions.

Competitive Landscape

Competition centres on balancing performance, price, and operational simplicity. Cisco, Huawei, and Juniper continue to win complex financial-sector refreshes due to fully-featured operating systems and long support life-cycles, yet their dominance is eroding where cost sensitivity reigns. White-box vendors shipping Broadcom Trident-based fixed switches claim 30–70% capex savings, an advantage that resonates with local ISPs. Mellanox scored several headline deals by bundling Cumulus Linux with 100 GbE TORs, illustrating the appetite for merchant-silicon plus open-source NOS.

Software-defined networking has become a key differentiator. Vendors that embed closed-loop telemetry and offer single-panel orchestration are viewed favourably because many African operators lack large NetOps teams. Security integration is another battleground, with Fortinet and Palo Alto offering fabric-wide micro-segmentation that aligns with POPIA and GDPR equivalency rules. Meanwhile, optical-layer suppliers such as Ciena and Infinera position coherent-plug transponders as an economical method for metro DCI expansion.

Partnership strategies are also shaping standings in the Africa data center networking market. Nokia aligns with Liquid Intelligent Technologies to target pan-regional fibre plus cloud stack bundles, while HPE’s acquisition of Silver Peak gives it an SD-WAN beachhead. Investors such as IDC, IFC, and KKR continue to back neutral facilities, providing follow-on capital that indirectly fuels switching and routing sales. As competitive intensity builds, end-users increasingly weigh vendor ability to supply local spares, deliver 24×7 multilingual support, and train in-house staff, factors that can override headline equipment pricing.

Africa Data Center Networking Industry Leaders

-

Huawei Technologies Co., Ltd.

-

Cisco Systems, Inc.

-

Hewlett Packard Enterprise Company

-

Arista Networks, Inc.

-

Juniper Networks, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Raxio Group secured USD 100 million from IFC to expand its carrier-neutral platform across Sub-Saharan Africa, funding multiple Tier III builds and bolstering open peering ecosystems.

- May 2025: Mauritania inaugurated a EUR 15 million Tier III facility in Nouakchott, enhancing regional connectivity and local cloud hosting capacity.

- March 2025: Microsoft committed USD 298 million for additional South African cloud and AI capacity, including a new campus in Centurion.

- March 2025: Google opened its Johannesburg cloud region following a R2.5 billion outlay, providing low-latency access across the continent.

- February 2025: PAIX Data Centres began construction of a new facility in Dakar to expand West African interconnection options

- January 2025: KKR and Gulf Data Hub announced a USD 5 billion partnership to grow capacity across MENA, including planned sites in Egypt and Morocco

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Africa data-center networking market as all switching, routing, SAN, ADC, SDN controllers, and related support services that sit inside colocation, hyperscale/cloud, and edge or micro-data centers across South Africa, Nigeria, Kenya, Egypt, Morocco, and the wider Rest-of-Africa cluster.

Equipment used purely for campus or branch LANs and consumer-grade networking falls outside this scope.

Segmentation Overview

-

By Component

-

Products

- Ethernet Switches

- Routers

- Storage Area Network (SAN)

- Application Delivery Controllers (ADC)

- Network Security Appliances

- Software-Defined Networking (SDN) Controllers

- Optical Interconnects

-

Services

- Installation and Integration

- Training and Consulting

- Support and Maintenance

- Managed Network Services

-

Products

-

By End-User

- IT and Telecommunications

- Banking, Financial Services and Insurance (BFSI)

- Government and Defense

- Media and Entertainment

- Healthcare and Life Sciences

- Manufacturing and Industrial

- Other End-Users

-

By Data-Center Type

- Colocation

- Hyperscalers/Cloud Service Providers

- Edge/Micro Data Centers

-

By Bandwidth

- Less Than or equals to 10 GbE

- 25–40 GbE

- 50–100 GbE

- Greater than 100 GbE

-

By Country

- South Africa

- Nigeria

- Kenya

- Egypt

- Morocco

- Rest of Africa

Detailed Research Methodology and Data Validation

Primary Research

We then interview switch OEM sales heads, local systems integrators, facility operators in Johannesburg, Lagos, and Nairobi, and cloud architects serving BFSI and government clients. The exchanges clarify white-box adoption, port-speed migration, service attach rates, and discounting practices, allowing us to challenge desk findings and refine regional weightings.

Desk Research

Mordor analysts first gather publicly available anchor data, telecom regulator traffic statistics, national data-center registries, customs import codes for HS 8517 gear, African Peering & Interconnection Forum white papers, and publications from bodies such as AFCOM, GSMA, and the Africa Data Centres Association. Company 10-Ks, prospectuses, and investor decks add shipment mixes and regional ASP cues, while paid sources including D&B Hoovers and Dow Jones Factiva supply hard revenue splits and tender notices. These sources shape initial volume-value ratios and reveal capex run-rates across facilities. The sources listed are illustrative; many others inform granular checks and gap filling.

Market-Sizing & Forecasting

A top-down model converts installed and planned IT-load (MW) plus rack additions into addressable port counts, applying observed port-per-rack ratios and a mix of <=10 GbE, 25-40 GbE, 50-100 GbE, and >100 GbE. Select bottom-up checks, supplier shipment roll-ups, and sampled ASP × volume test and recalibrate totals. Key variables include new submarine cable landings, hyperscale capex announcements, data traffic per smartphone, average switch ASP erosion, and local currency swings. Forecasts run on multivariate regression with scenario analysis, letting port-speed share shifts and energy-cost elasticity steer CAGR projections. Missing bottom-up datapoints (e.g., private OEM invoices) are bridged through weighted regional proxies validated during expert calls.

Data Validation & Update Cycle

Outputs pass variance and outlier screens, followed by peer review within the Africa ICT desk. Models refresh annually; mid-cycle updates trigger when facility pipelines or regulatory moves materially change demand.

Why Mordor's Africa Data Center Networking Baseline Proves Reliable

Published estimates often diverge because firms apply different geographic cuts, include adjacent LAN gear, or extrapolate global trends without local interviews.

Key Gap Drivers: other studies may fold Middle-East revenues into Africa, assume uniform switch ASP declines, or use conservative rack growth aligned to power-grid constraints that no longer hold after new renewable projects. Mordor's base case reflects only in-data-center hardware and services inside African borders, factors hyperscale capex already committed through 2027, and benefits from annual field calls that capture rapid 400 GbE roll-outs.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.10 B (2025) | Mordor Intelligence | - |

| USD 1.20 B (2024) | Regional Consultancy A | Excludes edge/micro sites and services revenues |

| USD 3.41 B (2024) | Global Consultancy B | Combines Middle East with Africa and includes campus networking |

Taken together, the comparison shows that when scope and variables are aligned, Mordor's figure sits between aggressive regional roll-ups and narrower equipment-only audits, giving decision-makers a balanced, transparent baseline they can trace to clear public metrics and repeatable steps.

Key Questions Answered in the Report

What is the current size of the Africa data center networking market?

The Africa data center networking market size at USD 2.38 billion in 2026 and is projected to reach USD 4.41 billion by 2031.

Which segment holds the largest share in the Africa data center networking market?

Products, primarily Ethernet switches and routers, captured 67.45% of market share in 2025.

Which bandwidth category is growing the fastest?

Links above 100 GbE are expanding at a 15.92% CAGR because AI and hyperscale workloads need higher throughput.

Why is South Africa the dominant geography?

South Africa controls 41.85% of 2025 revenue thanks to extensive subsea cable landings, established carrier hotels, and supportive government policy.

How are skills shortages affecting growth?

Limited availability of advanced network engineers raises deployment costs and delays projects, subtracting an estimated 1.8% from forecast CAGR.

What opportunities do white-box vendors have in Africa?

White-box switches can reduce capex by up to 70% and align with open-source operating systems, making them attractive in price-sensitive markets.

Page last updated on: