Gas Separation Membrane Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 2.06 Billion |

| Market Size (2030) | USD 2.63 Billion |

| Growth Rate (2025 - 2030) | 5.00% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gas Separation Membrane Market Analysis by Mordor Intelligence

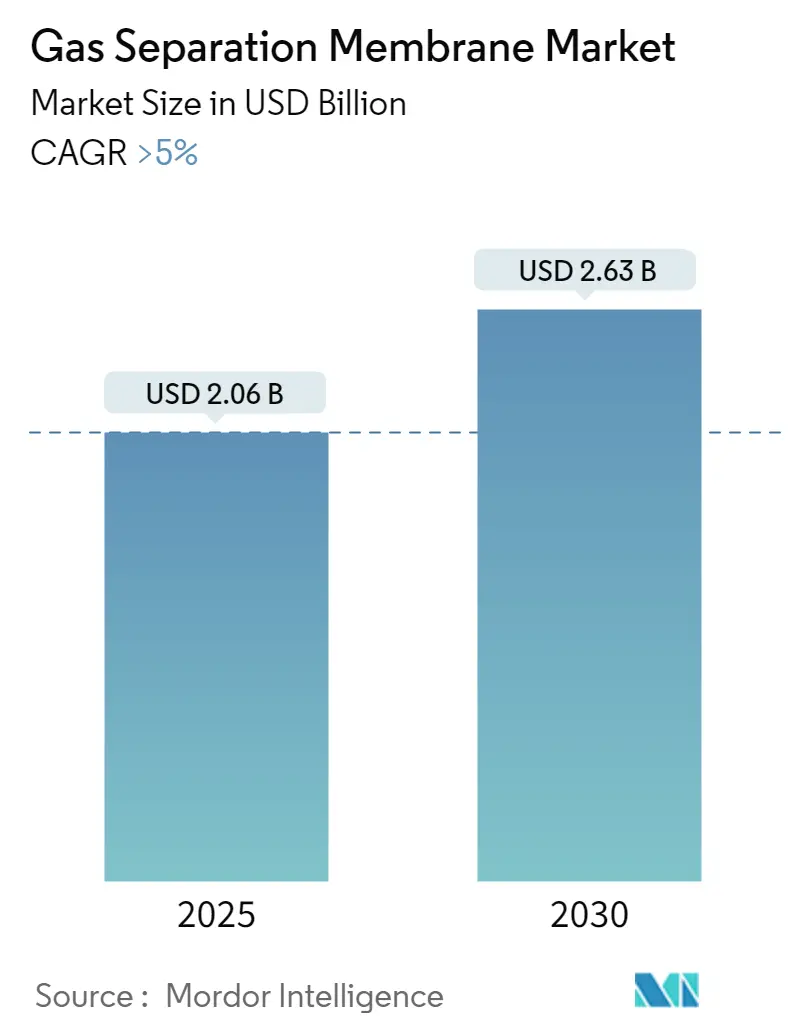

The Gas Separation Membrane Market size is estimated at USD 2.06 billion in 2025, and is expected to reach USD 2.63 billion by 2030, at a CAGR of greater than 5% during the forecast period (2025-2030).

The gas separation membrane industry is experiencing significant transformation driven by evolving energy sector dynamics and technological advancements. The United States' dry natural gas production has shown remarkable growth, exceeding 100 billion cubic feet per day (Bcf/d) in late 2022, highlighting the increasing demand for gas membrane separation technologies. This surge in production has been accompanied by substantial investments in pipeline infrastructure, particularly in regions like the Haynesville and Permian basins. The expansion of LNG export capabilities and the growing focus on natural gas as a transition fuel have created new opportunities for separation membrane technologies in gas processing applications.

The industry landscape is being reshaped by significant technological innovations in the membrane separation materials market. Research institutions and manufacturers are increasingly focusing on developing advanced membrane materials with enhanced selectivity and durability. The emergence of mixed matrix membranes (MMMs) represents a significant breakthrough, combining the processing advantages of polymeric membranes with the superior separation properties of inorganic materials. These developments are particularly relevant for applications in natural gas sweetening and carbon capture, where membrane technology offers advantages over traditional separation methods in terms of energy efficiency and operational flexibility.

The chemical and petrochemical sectors continue to drive substantial demand for gas separation membranes. According to recent industry data, Europe's LNG import capacity expanded significantly in 2022 and is anticipated to increase by a third by the end of 2024, as countries add new LNG regasification plants and expand existing import terminals. This expansion has created new opportunities for membrane-based gas separation technologies in LNG processing and purification applications. The industry is witnessing increased adoption of membrane technology in various chemical processing applications, particularly in hydrogen recovery and nitrogen generation.

The market is experiencing a notable shift toward sustainable and energy-efficient separation technologies. Major industry players are investing in research and development to improve membrane performance while reducing energy consumption. In January 2023, significant advancements were made in the development of all-carbon carbon dioxide separation membranes, demonstrating high durability in harsh environments. This innovation has particular significance for natural gas production emissions reduction. The industry is also seeing increased integration of membrane technology with other separation processes, creating hybrid systems that offer improved efficiency and flexibility in gas separation membrane market applications.

Global Gas Separation Membrane Market Trends and Insights

Increasing Demand for Membranes in Carbon Dioxide Separation Processes

The growing need for carbon dioxide separation across various industrial applications is driving significant demand for gas separation membranes. Gas separation membranes work on the principle of selective permeation across the membrane surface, where synthetic membranes of polymers and ceramic materials such as polyamides and cellulose acetate can effectively separate gas mixtures. These separation membranes are particularly valuable in natural gas processing, where CO2 is commonly found and must be removed to meet pipeline specifications or other application-specific requirements. The membrane gas separation process has gained considerable traction as it can operate in industry-supported continuous systems, unlike traditional systems such as adsorption and absorption, allowing simultaneous mixed gas supply and clean gas discharge.

The expansion of natural gas infrastructure and processing facilities is further propelling the demand for gas separation membranes. According to recent developments, FERC approved two significant projects in 2022 that will connect to LNG terminals in Louisiana, including the Evangeline Pass Expansion Project, which includes 13.1 miles of new pipeline to supply natural gas. Additionally, another capacity expansion plan of 0.5 Bcf/d was approved to transport US natural gas through a pipeline to the Energia Costa Azul LNG export project in Baja, California, Mexico. These infrastructure developments, coupled with the increasing focus on clean energy processing, are creating substantial opportunities for membrane-based gas separation technologies in carbon dioxide removal applications.

Strict Government Norms for GHG Emissions

Governments worldwide are implementing increasingly stringent policies and regulatory measures to combat the rise in greenhouse gas emissions associated with global warming and climate change. The United States Environmental Protection Agency (EPA) has established legal authority to monitor and regulate greenhouse gas emissions under the Clean Air Act, with specific controls for emissions from power plants under Section 111. The European Union has set aggressive climate change targets, making them legally enforceable with a commitment to cut carbon emissions by at least 55% by 2030 compared to 1990 levels, while the European Parliament is pushing for an even higher reduction objective of 60%.

The implementation of new climate initiatives and international cooperation is further strengthening the regulatory framework for GHG emissions control. In November 2022, at the United Nations Climate Change Conference (COP27), the United States launched the Net Zero Governments Initiative, calling on governments to achieve net zero emissions from their operations by 2050. This initiative has gained support from numerous countries, including Australia, Austria, Belgium, Canada, Cyprus, Finland, France, Germany, Ireland, Israel, Japan, South Korea, Lithuania, the Netherlands, New Zealand, Singapore, Switzerland, and the United Kingdom. These commitments are driving industries to adopt more efficient gas separation technologies, particularly membrane-based solutions, to meet their emission reduction targets and comply with regulatory requirements.

Segment Analysis

Polyimide and Polyaramide Segment in Gas Separation Membrane Market

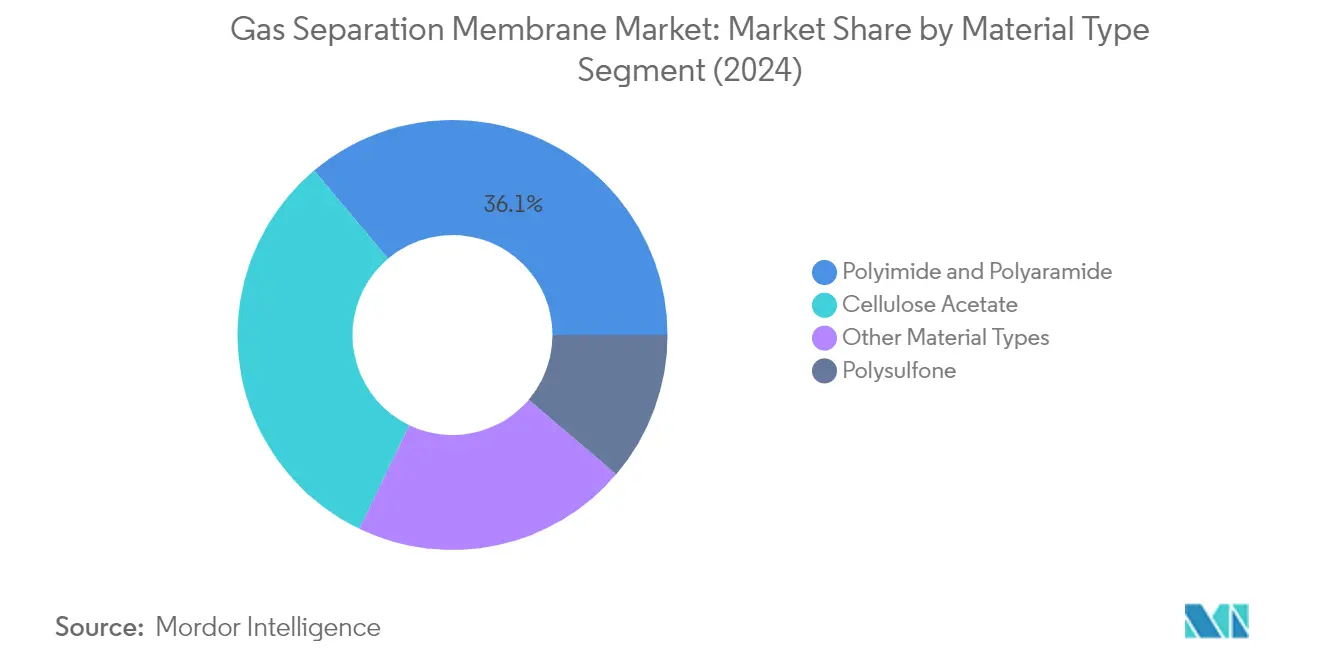

The Polyimide and Polyaramide segment dominates the gas separation membrane market, holding approximately 36% market share in 2024. This segment's leadership position is attributed to the superior physicochemical properties of these membrane separation materials, including excellent thermal stability, chemical resistance, and processability. Polyimide membranes are particularly effective in carbon dioxide collection as they can remove hydrogen sulfide and water in a single step, offering lower capital expenses compared to traditional approaches. The segment's growth is driven by increasing demand in applications like hydrogen recovery from natural gas and refinery off-gases, especially in cases where waste gas contains more than 50% hydrogen. Additionally, polyaramide membranes are gaining traction in various demanding applications such as removing carbon dioxide from natural gas, greenhouse gas-producing sources, and oxygen enrichment from air, due to their high thermal and mechanical stability combined with excellent film-forming capabilities.

Remaining Segments in Material Type

The other significant segments in the gas separation membrane market include Cellulose Acetate, Polysulfone, and Other Material Types. Cellulose Acetate membranes are valued for their excellent film-forming properties, high chemical and mechanical stability, and eco-friendly nature. Polysulfone membranes, while offering lower selectivity compared to other materials, remain commercially viable due to their inexpensive manufacturing costs and widespread availability. The Other Material Types segment includes innovative materials like Polydimethylsiloxane (PDMS), polyurethane, and inorganic membrane materials, which are increasingly being developed for specialized applications requiring specific performance characteristics such as high temperature resistance or enhanced gas permeability.

Segment Analysis: Application

Nitrogen Generation and Oxygen Enrichment Segment in Gas Separation Membrane Market

The nitrogen generation and oxygen enrichment segment dominates the gas separation membrane market, accounting for approximately 52% of the total market share in 2024. This significant market position is driven by extensive applications across multiple industries, particularly in steel manufacturing where modern basic oxygen steelmaking consumes almost 2 tons of oxygen per ton of steel. The segment's dominance is further strengthened by its critical role in the healthcare sector, where oxygen concentrators have seen substantial demand for patient care. The technology's ability to provide a cost-efficient, safer, and more convenient oxygen supply compared to traditional cryogenic tanks or pressurized cylinders has made it particularly attractive for pharmaceutical production, glass manufacturing, and water treatment applications. Additionally, the segment benefits from the increasing adoption in aerospace applications, where membrane gas separation is used to provide nitrogen-rich gases for fuel tank safety and oxygen-enriched air for high-altitude pilot support.

Carbon Dioxide Removal Segment in Gas Separation Membrane Market

The carbon dioxide removal segment is emerging as the fastest-growing application in the gas separation membrane market, projected to grow at a robust rate from 2024 to 2029. This exceptional growth is primarily driven by increasing environmental regulations and the rising focus on carbon capture and storage (CCUS) technologies. The segment's growth is supported by significant technological advancements in membrane materials and designs, making them more efficient and cost-effective compared to traditional CO2 removal methods. The implementation of carbon capture projects globally, particularly in regions like the United States and Canada, which together account for 65% of annual capture capacity, is further accelerating segment growth. The expansion of membrane technology in hybrid processes, where membranes are integrated with existing carbon capture systems, demonstrates the versatility and growing acceptance of this technology in industrial applications.

Remaining Segments in Gas Separation Membrane Market Applications

The other significant segments in the gas separation membrane market include hydrogen recovery, hydrogen sulfide removal, and various other specialized applications. The hydrogen recovery segment plays a crucial role in refinery operations and petrochemical processes, particularly in hydro-treating operations for producing low-sulfur fuels. The hydrogen sulfide removal segment is essential for natural gas processing and pipeline safety, while other applications encompass areas such as VOC removal, gas dehydration, and LPG recovery. These segments collectively contribute to the market's diversity and demonstrate the versatility of gas membrane technology in addressing various gas separation challenges across different industries. The continued development of new membrane materials and technologies is expected to further enhance the capabilities and applications of these segments in the coming years.

Geography Analysis

Gas Separation Membrane Market in Asia-Pacific

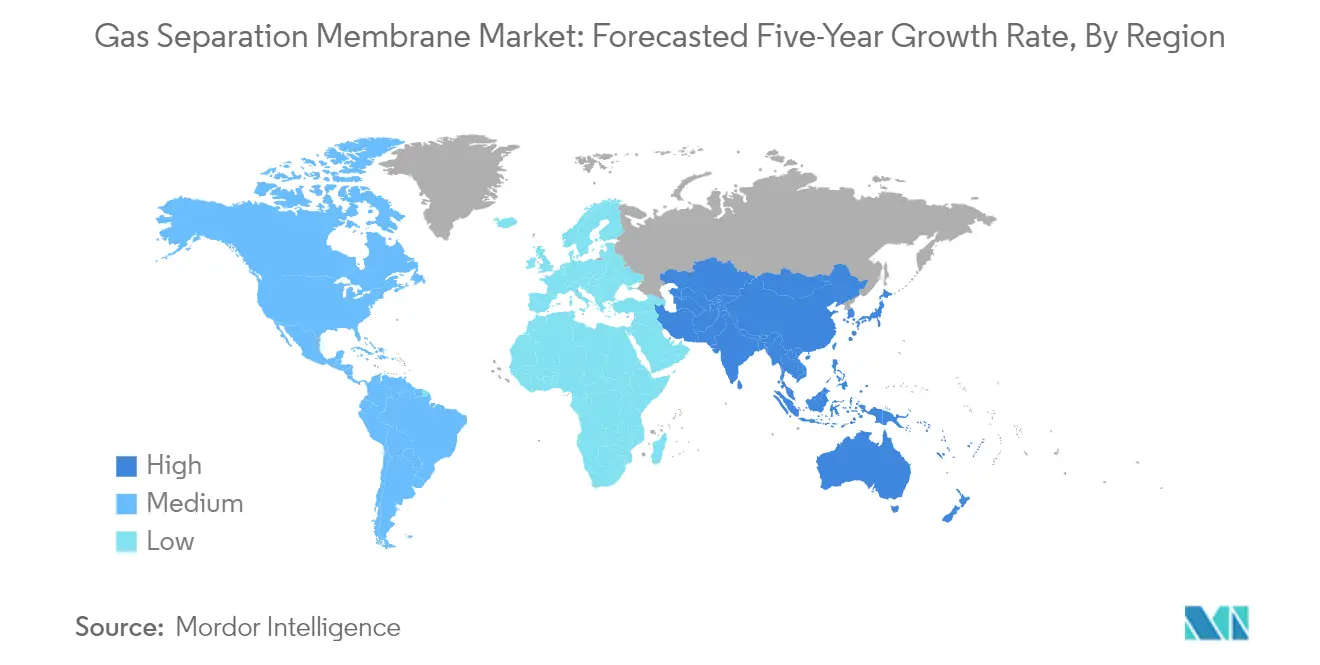

The Asia-Pacific region represents a dominant force in the global gas separation membrane market, driven by robust industrial development and increasing environmental regulations. Countries like China, India, Japan, and South Korea are making significant investments in chemical processing, power generation, and healthcare infrastructure. The region's growth is supported by rising demand for clean energy solutions, particularly in natural gas processing and carbon capture applications. The presence of major manufacturing facilities and ongoing technological advancements further strengthens the market position of this region.

Gas Separation Membrane Market in China

China leads the Asia-Pacific gas separation membrane market with approximately 51% market share in 2024. The country's dominance is attributed to its extensive chemical manufacturing base and increasing focus on environmental protection measures. The robust growth of industrial development has significantly increased the country's energy needs, particularly in sectors like steel, cement, and petrochemicals. China's commitment to reducing carbon emissions has led to increased adoption of membrane technology in various applications. The country's healthcare sector, being the second-largest globally, further drives demand through applications in medical gas separation and purification processes.

Gas Separation Membrane Market Growth Trajectory in China

China is projected to maintain its position as the fastest-growing market in the Asia-Pacific region with an expected growth rate of approximately 7% during 2024-2029. The country's aggressive environmental policies and substantial investments in clean energy technologies are driving this growth. China's commitment to achieving carbon neutrality has spurred increased adoption of gas separation membranes in carbon capture and storage applications. The expansion of the country's chemical industry, coupled with growing healthcare infrastructure investments, continues to create new opportunities for market growth. Additionally, the government's support for technological innovation in the membrane separation materials market further accelerates market development.

Gas Separation Membrane Market in North America

North America maintains a significant position in the gas separation membrane industry, characterized by advanced technological adoption and stringent environmental regulations. The region's market is primarily driven by the United States, Canada, and Mexico, with substantial applications in natural gas processing, carbon capture, and healthcare sectors. The presence of major industry players and continuous research and development activities further strengthens the region's market position. The region's focus on reducing greenhouse gas emissions and increasing adoption of clean energy solutions continues to drive market growth.

Gas Separation Membrane Market in United States

The United States dominates the North American market with approximately 73% market share in 2024. The country's leadership position is supported by its well-established chemical manufacturing industry and presence of top chemical product manufacturers. The nation's robust healthcare infrastructure and increasing focus on environmental protection drive substantial demand for gas separation membranes. The country's extensive natural gas processing operations and growing emphasis on carbon capture technologies further boost market growth. The presence of major research institutions and continuous technological innovations strengthens the United States' market position.

Gas Separation Membrane Market Growth Trajectory in United States

The United States is expected to maintain its position as the fastest-growing market in North America with a projected growth rate of approximately 6% during 2024-2029. The country's growth is driven by increasing investments in clean energy technologies and stringent environmental regulations. The expanding chemical industry and growing focus on hydrogen recovery applications create new opportunities for market expansion. The country's leadership in technological innovation and strong focus on research and development activities in membrane technology continue to drive market growth. Additionally, the growing healthcare sector and increasing demand for medical gas separation applications further support market expansion.

Gas Separation Membrane Market in Europe

Europe represents a mature market for gas separation membranes, with a strong focus on environmental sustainability and technological innovation. The region's market is driven by countries including Germany, United Kingdom, Italy, and France, each contributing significantly to market development. The region's stringent environmental regulations and commitment to reducing carbon emissions create substantial opportunities for market growth. The presence of major manufacturing facilities and continuous research activities in membrane technology further strengthens the market position. The Europe oil and gas separation market is particularly influenced by these factors, driving demand for advanced membrane technologies.

Gas Separation Membrane Market in Germany

Germany leads the European gas separation membrane market, driven by its strong industrial base and commitment to environmental protection. The country's leadership in chemical manufacturing and continuous technological innovations strengthens its market position. Germany's focus on reducing greenhouse gas emissions and increasing adoption of clean energy solutions drives substantial demand for gas separation membranes. The presence of major industry players and robust research infrastructure further supports market growth. The country's well-developed healthcare sector also contributes significantly to market expansion.

Gas Separation Membrane Market Growth Trajectory in Germany

Germany maintains its position as the fastest-growing market in Europe, driven by increasing investments in clean energy technologies and stringent environmental regulations. The country's growth is supported by continuous technological innovations and strong research activities in membrane technology. Germany's commitment to achieving carbon neutrality creates new opportunities for market expansion. The country's robust chemical industry and growing focus on hydrogen applications further drive market growth. Additionally, the well-established healthcare infrastructure continues to create steady demand for the gas separation membrane market segment.

Gas Separation Membrane Market in South America

The South American gas separation membrane market demonstrates significant growth potential, with Brazil and Argentina being key contributors to market development. Brazil emerges as both the largest and fastest-growing market in the region, driven by its extensive oil and gas operations and growing chemical industry. The region's increasing focus on environmental protection and growing industrial base creates new opportunities for market expansion. The presence of major manufacturing facilities and continuous investments in infrastructure development further strengthen the market position. The region's growing healthcare sector and increasing adoption of clean energy solutions contribute significantly to market growth.

Gas Separation Membrane Market in Middle East & Africa

The Middle East & Africa region presents substantial growth opportunities in the gas separation membrane market, with Saudi Arabia and South Africa playing crucial roles in market development. Saudi Arabia emerges as both the largest and fastest-growing market in the region, supported by its extensive oil and gas operations and growing chemical industry. The region's increasing focus on environmental protection and substantial investments in infrastructure development create new opportunities for market expansion. The presence of major manufacturing facilities and growing adoption of clean energy solutions further strengthen the market position. The region's developing healthcare sector and increasing industrial activities contribute significantly to market growth.

Competitive Landscape

Top Companies in Gas Separation Membrane Market

The gas separation membrane market is characterized by continuous product innovation focused on improving membrane performance and efficiency. Companies are investing heavily in research and development to create advanced membrane materials with enhanced selectivity and permeability, particularly for applications in carbon dioxide separation and hydrogen recovery. Operational agility is demonstrated through vertical integration strategies and the development of comprehensive solution portfolios that combine membrane technology with complementary gas separation systems. Strategic partnerships and collaborations, particularly between gas separation membrane suppliers and engineering firms, are becoming increasingly common to strengthen market positions and expand application capabilities. Geographic expansion efforts are primarily focused on high-growth regions in Asia-Pacific, where increasing industrial activity and environmental regulations are driving demand for gas separation solutions.

Consolidated Market Led By Global Players

The gas separation membrane market structure is dominated by large multinational corporations and industrial gas companies that possess extensive technological capabilities and global distribution networks. These major players, including Air Liquide, Air Products, and Linde, leverage their broad product portfolios and strong financial positions to maintain market leadership. The market also includes specialized membrane technology companies that focus on developing innovative solutions for specific applications, though their market share remains relatively smaller compared to the industry giants.

The membrane market demonstrates moderate consolidation, with established players controlling significant market share through their proprietary technologies and patent portfolios. Merger and acquisition activities are primarily driven by the need to acquire innovative membrane technologies and expand geographical presence. Companies are particularly interested in acquiring smaller technology firms that have developed breakthrough membrane materials or novel manufacturing processes, as evidenced by recent strategic moves in the industry.

Innovation and Integration Drive Future Success

Success in the membrane industry increasingly depends on developing cost-effective solutions that address specific industry challenges while meeting stringent environmental regulations. Companies must focus on creating membranes with improved durability and performance, particularly for high-temperature and high-pressure applications. The ability to offer integrated solutions that combine membrane technology with other separation technologies is becoming crucial, as end-users seek comprehensive gas separation solutions that optimize operational efficiency.

Market participants need to establish strong relationships with end-users in key industries such as oil and gas, chemical processing, and hydrogen production to maintain a competitive advantage. The threat of substitution from alternative gas separation technologies like pressure swing adsorption remains a consideration, particularly in applications requiring very high purity levels. Regulatory developments, especially those related to carbon capture and hydrogen infrastructure, are expected to significantly influence market dynamics and create new opportunities for membrane technology providers. Companies that can demonstrate the environmental benefits and operational efficiency of their membrane solutions while maintaining cost competitiveness will be better positioned for future growth in the gas separation membrane market.

Gas Separation Membrane Industry Leaders

UBE Corporation

Air Products and Chemicals, Inc.

Air Liquide Advanced Seperations

DIC CORPORATION

FUJIFILM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2023: UBE Corporation announced the expansion of its polyimide hollow fiber production facilities at its UBE Chemical Factory and gas separation membrane module production facilities at its Sakai Factory to meet the rapidly increasing demand for gas separation chambers, especially CO2 separation membranes. The two new facilities, which will increase the production capacity by around 1.8 times, are planned to go into operation in the first half of FY 2025.

- January 2022: Toray Industries Inc. developed a polymeric separation membrane module for selective or efficient hydrogen removal from mixtures of gases that contain hydrogen. The CO2 emissions of hydrogen treatment processes and the number of modules needed are more than halved with this new module.

Global Gas Separation Membrane Market Report Scope

Gas separation membranes separate gas mixtures into their individual components based on differences in their molecular size, shape, and solubility. These membranes are made of polymers, ceramics, or other materials with specific properties that enable the selective transportation of certain gases while blocking others.

The gas separation membrane market is segmented by material type, application, and geography. By material type, the market is segmented into polyimide and polyaramid, polysulfone, cellulose acetate, and other material types (nanostructured membrane). By application, the market is segmented into nitrogen generation and oxygen enrichment, hydrogen recovery, carbon dioxide removal, hydrogen sulfide removal, and other applications (carbonation). The report also covers the market sizes and forecasts for the gas separation membrane market in 27 countries across different regions. For each segment, the market size and forecasts are provided in terms of revenue (USD).

| Polyimide and Polyamide |

| Polysulfone |

| Cellulose Acetate |

| Other Material Types (Nanostructured Membrane) |

| Nitrogen Generation and Oxygen Enrichment |

| Hydrogen Recovery |

| Carbon Dioxide Removal |

| Removal of Hydrogen Sulphide |

| Other Applications (Carbonation) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Turkey | |

| Russia | |

| NORDIC | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Nigeria | |

| Qatar | |

| Egypt | |

| UAE | |

| Rest of Middle East and Africa |

| Material Type | Polyimide and Polyamide | |

| Polysulfone | ||

| Cellulose Acetate | ||

| Other Material Types (Nanostructured Membrane) | ||

| Application | Nitrogen Generation and Oxygen Enrichment | |

| Hydrogen Recovery | ||

| Carbon Dioxide Removal | ||

| Removal of Hydrogen Sulphide | ||

| Other Applications (Carbonation) | ||

| Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Turkey | ||

| Russia | ||

| NORDIC | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Nigeria | ||

| Qatar | ||

| Egypt | ||

| UAE | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the Gas Separation Membrane Market?

The Gas Separation Membrane Market size is expected to reach USD 2.06 billion in 2025 and grow at a CAGR of greater than 5% to reach USD 2.63 billion by 2030.

What is the current Gas Separation Membrane Market size?

In 2025, the Gas Separation Membrane Market size is expected to reach USD 2.06 billion.

Who are the key players in Gas Separation Membrane Market?

UBE Corporation, Air Products and Chemicals, Inc., Air Liquide Advanced Seperations, DIC CORPORATION and FUJIFILM Corporation are the major companies operating in the Gas Separation Membrane Market.

Which is the fastest growing region in Gas Separation Membrane Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Gas Separation Membrane Market?

In 2025, the Asia Pacific accounts for the largest market share in Gas Separation Membrane Market.

What years does this Gas Separation Membrane Market cover, and what was the market size in 2024?

In 2024, the Gas Separation Membrane Market size was estimated at USD 1.96 billion. The report covers the Gas Separation Membrane Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Gas Separation Membrane Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: