Future-proof Pharma Labels Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

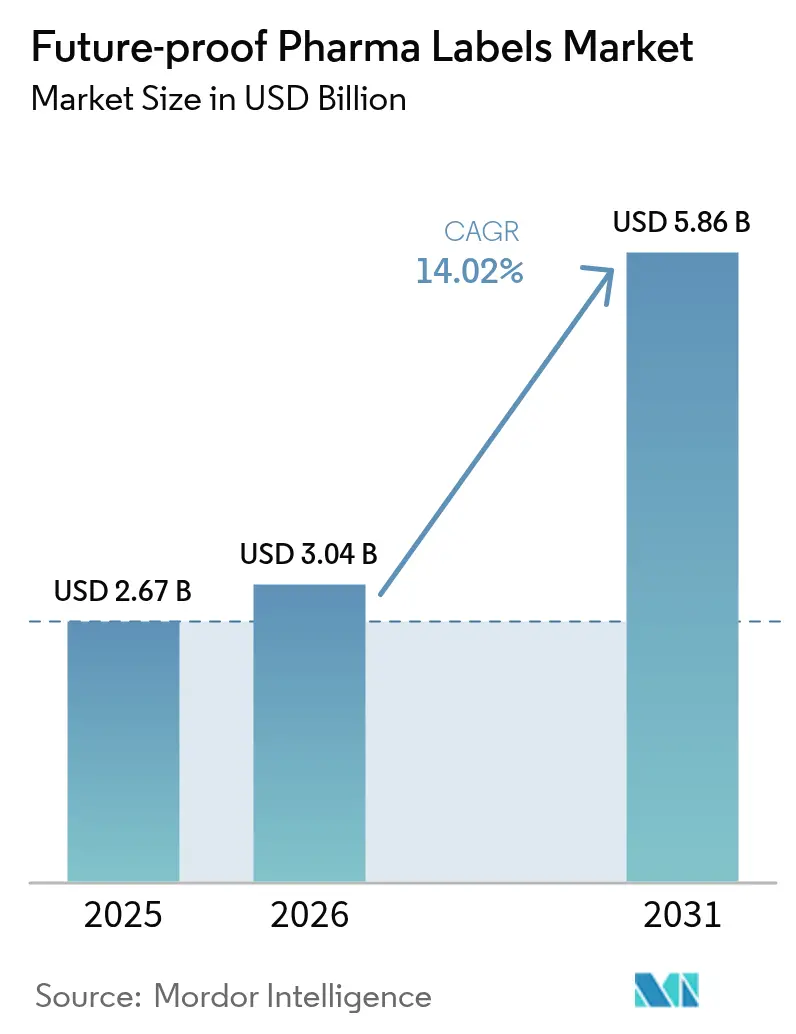

| Market Size (2026) | USD 3.04 Billion |

| Market Size (2031) | USD 5.86 Billion |

| Growth Rate (2026 - 2031) | 14.02% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Future-proof Pharma Labels Market Analysis by Mordor Intelligence

Future-proof Pharma Labels market size in 2026 is estimated at USD 3.04 billion, growing from 2025 value of USD 2.67 billion with 2031 projections showing USD 5.86 billion, growing at 14.02% CAGR over 2026-2031. This expansion is driven by serialization deadlines in major jurisdictions, surging e–commerce–driven counterfeiting risks, and the widening adoption of hospital automation platforms that rely on RFID-enabled primary packs. Heightened biologics output, especially temperature-sensitive mRNA vaccines and monoclonal antibodies, further elevates demand for sensor-embedded labels that verify cold-chain integrity. In parallel, falling unit costs for flexible NFC and ultra-thin RFID inlays are easing budget constraints that once limited the uptake of smart labels to premium therapies. Competitive intensity centers on suppliers who can blend material science know-how with electronics integration while navigating complex validation audits under FDA 21 CFR Part 820 and analogous EU quality rules.[1]U.S. Food and Drug Administration, “Drug Supply Chain Security Act (DSCSA),” FDA, fda.gov

Key Report Takeaways

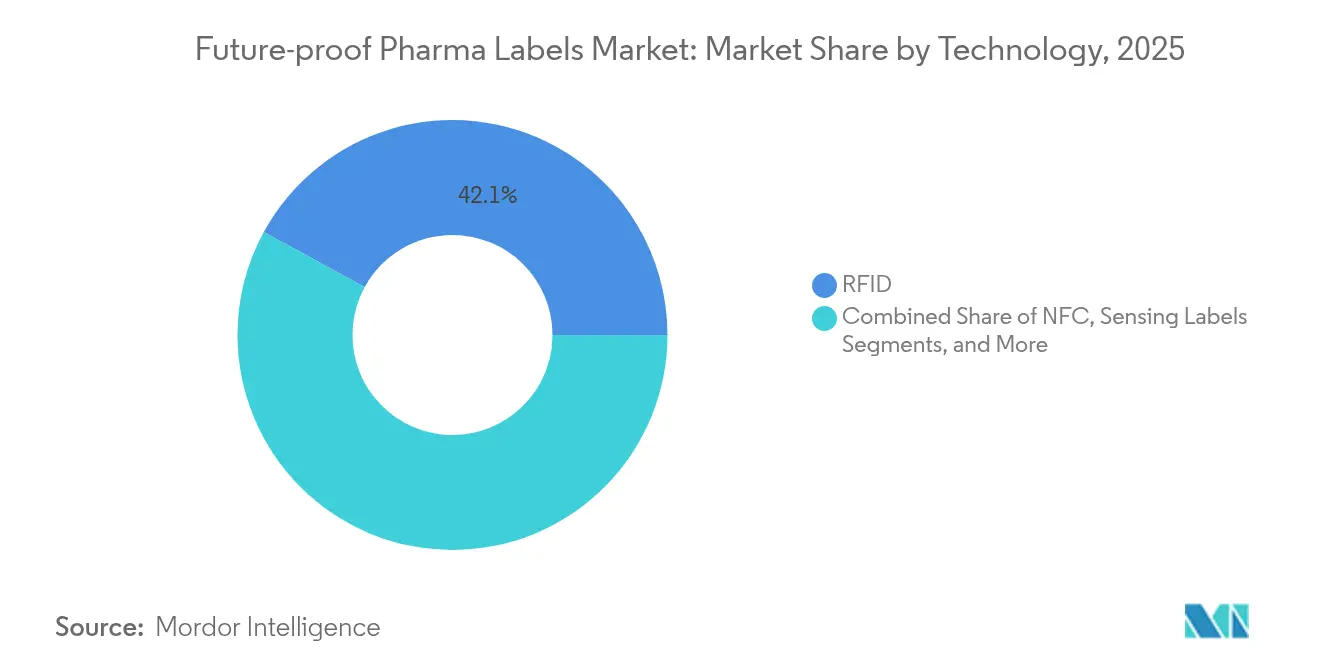

- By technology, RFID captured 42.05% of the Future-proof Pharma Labels market share in 2025, Sensing labels are advancing at a 15.08% CAGR between 2026-2031.

- By packaging type, blister packs held 32.10% revenue share in 2025; syringes and vials are forecast to expand at a 16.12% CAGR between 2026-2031.

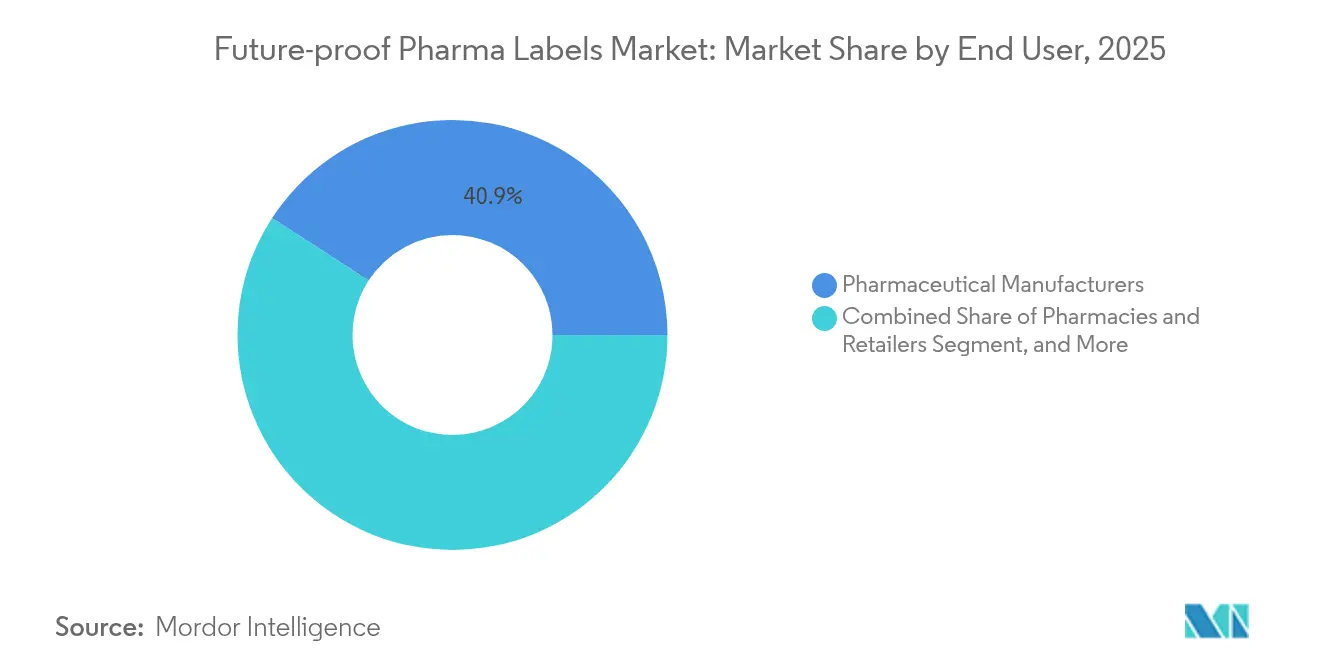

- By end user, pharmaceutical manufacturers captured 40.85% of the Future-proof Pharma Labels market size in 2025, while Contract Manufacturing Organizations (CMOs) are projected to record the highest CAGR at 16.35% through 2031.

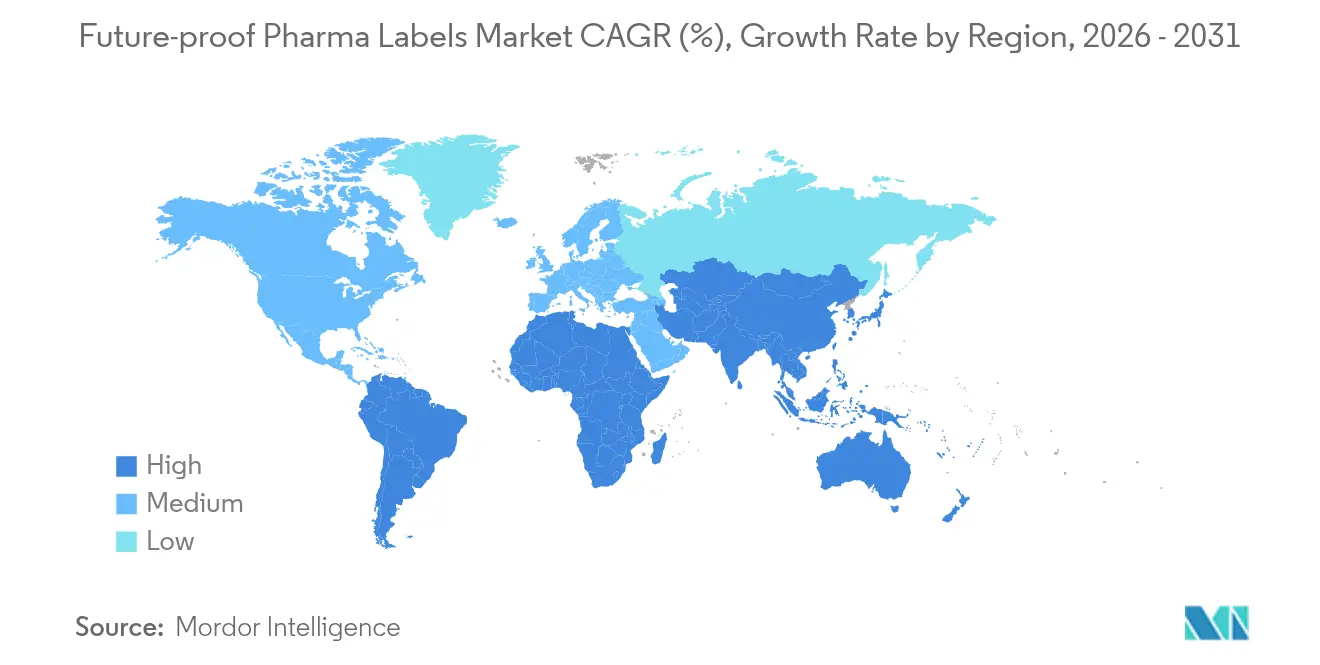

- By geography, North America led with 36.40% of the Future-proof Pharma Labels market share in 2025; Asia-Pacific is set to grow at a 15.02% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Future-proof Pharma Labels Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Serialization mandates reaching final compliance 2027-30 | +4.2% | North America and EU; spill-over to APAC | Medium term (2-4 years) |

| E-commerce counterfeit escalation | +3.1% | Global; highest in emerging markets | Short term (≤2 years) |

| Hospital RFID automation for crash carts and med rooms | +2.8% | North America and EU core; growing APAC | Medium term (2-4 years) |

| Temperature-sensitive biologics need sensor labels | +2.4% | Global; led by North America and EU | Long term (≥4 years) |

| Low-cost flexible NFC ICs enable unit-level rollout | +1.1% | APAC fabs; global use | Long term (≥4 years) |

| Blockchain-linked digital birth certificates | +0.6% | North America and EU premium lines | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Serialization mandates reaching final compliance 2027-30

Unit-level serialization rules under the U.S. DSCSA move from lot-level requirements to mandatory unique product identifiers in November 2027, compelling every prescription drug package to carry a machine-readable code that supports verification, tracing, and electronic data exchange. The EU’s Falsified Medicines Directive follows a parallel path, with member-state extensions converging during the same horizon, leaving manufacturers no option but to retrofit or rebuild labeling lines on a global scale. Because wholesalers and dispensers must confirm codes before shipment or dispense, network effects accelerate adoption beyond the factory gate. Companies are consequently prioritizing “future-proof” platforms that also accommodate upcoming blockchain or IoT extensions, avoiding stranded investments.

Escalating pharma e-commerce counterfeits

Roughly 10% of medicines sold globally are estimated to be counterfeit, a risk magnified by direct-to-consumer web channels that bypass traditional visual inspection points. Smartphone-tappable NFC or dual-frequency labels enable patients to instantly confirm authenticity, shifting the verification responsibility to the end user. Emerging-market regulators are beginning to endorse such consumer-level authentication, propelling near-term demand in India, Southeast Asia, and parts of Africa.

Hospital demand for RFID-based crash-cart and med-room automation

North American hospitals are increasingly deploying RFID platforms, such as KitCheck, which has already processed more than 325 million injectable units across 900 sites, enabling real-time inventory and expiry management. Because these workflows require tags that survive sterilization, high-speed filling, and repeated handling, pharmaceutical suppliers are integrating RFID at the primary packaging stage rather than relying on downstream re-labeling. Compliance with 21 CFR Part 820 quality-system regulations extends to label-component validation, creating another layer of supplier qualification that advantages incumbents with established audit histories.

Rise of temperature-sensitive biologics requiring sensor labels

Messenger RNA vaccines, CAR-T cell therapies, and monoclonal antibodies must remain within narrow temperature windows; excursions can silently degrade efficacy. Smart labels embedding irreversible time-temperature indicators or digital sensors provide a verifiable chain-of-custody record, satisfying Good Distribution Practice logs and reducing costly product losses. Pharmaceutical companies view these labels as both a compliance tool and a brand-differentiation lever in competitive biologic segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Absence of dose-ID performance standards across NFC/RFID bands | -2.1% | Global multi-jurisdiction supply chains | Short term (≤2 years) |

| Unit-level tag cost > 1% of COGS for emerging-market generics | -1.8% | India, China, Southeast Asia | Medium term (2-4 years) |

| Read-range interference from metals and liquids in small vials | -1.3% | Global; primary packs | Medium term (2-4 years) |

| Skilled-labor shortage for label-data integration at CMOs | -0.9% | Major CMO hubs worldwide | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Absence of dose-ID performance standards across NFC/RFID bands

Interoperability hurdles arise because different regions allocate varying frequency windows for RFID and specify divergent data-format rules. Multinationals, therefore, juggle multiple tag designs, eroding economies of scale and complicating validation regimes. Pharma labeling struggles with interoperability and reliability due to inconsistent dose-identification standards across NFC and RFID frequency bands. The absence of unified benchmarks extends validation cycles, diminishes cross-vendor compatibility, and introduces regulatory hurdles in global deployments. Consequently, the adoption of smart labels, particularly for high-assurance real-time authentication, faces significant delays.

Unit-level tag cost > 1% of COGS for generics in emerging markets

In high-volume, low-margin generic segments, a single RFID or NFC inlay may still account for more than 1% of the finished-dose cost, limiting adoption to minimum-compliance tags rather than advanced sensor or blockchain-ready variants. Flexible, ultra-thin ICs from vendors such as PragmatIC are narrowing that gap but have yet to reach mass-production yields sufficient for price points below USD 0.03. When the cost of NFC/RFID tags surpasses 1% of the unit's cost of goods sold (COGS) for low-margin generics, adopting smart labels becomes economically unfeasible. Manufacturers in emerging markets face intense pricing pressures, making it challenging to justify the added costs of serialization technologies. This situation hinders scalability, limits the reach of digital traceability, and reinforces the reliance on traditional barcoding methods for compliance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: RFID holds scale while sensor labels surge

RFID represented 42.05% of the Future-proof Pharma Labels market share in 2025, buoyed by legacy infrastructure inside hospital cabinets and wholesale depots. The tag’s proven read-rate in metallic crash carts and its compatibility with warehouse conveyors sustain its dominance. Sensing labels, however, are projected to post a 15.08% CAGR through 2031 as biologic makers request continuous temperature and humidity monitoring. Hybrid tags, which combine UHF for bulk reads and NFC for consumer taps, address omnichannel logistics while reducing SKUs. Schreiner Group’s collaboration with PragmatIC enabled the development of an ultra-thin RFID inlay that conforms to 6 mm-radius vials, thereby solving the historical antenna-coil challenge.

In practice, pharma clients want technology stacks that evolve with regulation, so suppliers are bundling firmware-updatable chips that can store blockchain pointers or IoT sensor payloads. Because North American hospitals often specify KitCheck-validated tags, global producers are standardizing on the same chip family to simplify validation audits, further reinforcing the Future-proof Pharma Labels market.

By Packaging Type: Biologics propel syringe and vial innovation

Blister packs retained 32.10% of the revenue in 2025, as oral solids still dominate prescription volume. Yet syringes and vials outpace every other format with a 16.12% CAGR as injectables expand in oncology, immunology, and vaccine portfolios. Smart-label fitment on curved glass requires flexible antenna substrates and pharmaceutical-grade adhesives. Suppliers now laminate 12-μm aluminum antennae between PET layers to survive lyophilization and gamma sterilization.

Secondary cartons are gradually incorporating dual-frequency tags that trigger e-leaflet downloads, aligning with EU eco-design proposals and reducing the use of paper inserts. The Future-proof Pharma Labels market size for syringe applications is forecast to surpass the blister value by 2029, illustrating how format-specific innovation reconfigures the revenue mix. Pharma cold-chain providers also apply pallet-level RFID tags to cryogenic shippers, enabling gate-reader confirmation when containers leave fill-finish sites. Such tertiary-unit adoption pushes the Future-proof Pharma Labels market beyond primary drug packs into broader logistics assets.

By End User: CMOs accelerate fastest amid outsourcing boom

Pharmaceutical manufacturers controlled 40.85% of the Future-proof Pharma Labels market size in 2025, safeguarding critical IP and QA oversight for high-value brands. Nevertheless, CMOs are scaling fastest at a 16.35% CAGR because brand owners outsource the production of vaccines, biosimilars, and niche or orphan drugs that require flexible lines. To win contracts, CMOs embed configurable print-apply stations and cloud links that stream EPCIS events to sponsor dashboards. Hospitals and health systems add demand pull by mandating RFID-ready packs in tenders, particularly for crash cart injectables.

As a result, many CMOs reverse-integrate label-conversion shops to ensure available capacity during surge campaigns, a lesson learned from COVID-19 vaccine scale-ups, thereby expanding their footprint in the Future-proof Pharma Labels market. Retail pharmacies remain slower adopters; however, rising mail-order volumes prompt chains to pilot consumer-tap NFC programs for high-risk medicines. Clinical-trial sponsors leverage smart labels to monitor kit returns and reveal patient dosing adherence, using data to support adaptive-trial designs that shorten development cycles.

Geography Analysis

North America retained 36.40% of the Future-proof Pharma Labels market share in 2025, buoyed by DSCSA enforcement checkpoints and widespread RFID hospital automation. State boards of pharmacy increasingly require machine-readable identifiers on narcotics, making compliance non-negotiable. Canada mirrors many U.S. protocols, so cross-border manufacturers often deploy a single North American label spec. Europe follows with sizable revenue but variable speed: Scandinavian states achieve near-full FMD digitalization, whereas Southern Europe still stabilizes data hub connections. The European Medicines Verification System nonetheless underpins steady orders for serialized 2D codes and, increasingly, dual-frequency smart tags that overlay on top of legacy DataMatrix squares.

The Asia-Pacific is the fastest-growing region, with a 15.02% CAGR through 2031, driven by the burgeoning contract-manufacturing ecosystems in India and China. Indian converters invest in automated linerless lines suited to smart-label lamination, while Chinese flexible-electronics fabs supply low-cost NFC chips to global packagers. Governments in South Korea and Japan ratify local track-and-trace mandates, extending regional pull. Southeast Asian health ministries are piloting smartphone-based authentication to combat rampant antibiotic counterfeiting, signaling future purchase orders that will broaden the Future-proof Pharma Labels market.

The Middle East and Africa register lower absolute dollars but post vibrant pockets. Saudi Arabia’s track-and-trace portal, Tatmeen, drives RFID adoption among importers, and South Africa’s private hospital chains demand tamper-evident RFID labels on oncology injectables. Latin America exhibits a gradual adoption, led by Brazil’s SNCM serialization law, although currency volatility tempers immediate volume. Collectively, emerging-market regulatory momentum ensures that the Future-proof Pharma Labels market penetrates every continent before 2030.

Competitive Landscape

The Future-proof Pharma Labels market remains moderately fragmented, with the five largest converters accounting for roughly 45% of global revenue. Avery Dennison leverages its global PET liner recycling program to attract environmentally driven pharmaceutical brands. CCL Industries scales its Checkpoint division’s RFID module into folded-leaflet labels for oncology vials, underscoring cross-business.

Zebra Technologies concentrates on printer-encoder ecosystems, bundling cloud firmware that supports electronic pedigree uploads. The Schreiner Group differentiates itself through ultra-high-speed digital late-stage customization, which programs EPCs hours before shipment, thereby shaving CMO lead times. Emerging players, such as PragmatIC, supply wafer-scale flexible ICs that reduce tag-inlay thickness to below 100 µm and trim antenna costs.[3]Labels & Labeling, “Schreiner MediPharm launches robust RFID labels,” Labels & Labeling, labelsandlabeling.com

Blockchain integrators, such as Chronicled, partner with label vendors to embed cryptographic hashes in NFC memory blocks, creating a digital birth certificate that remains intact throughout the product’s lifespan. Material-science expertise stays critical: converters must tune acrylic adhesives that pass USP <661.1> extractables limits and withstand autoclaves. Customers also award contracts based on FDA 21 CFR Part 820 audit histories, elevating incumbents with certified quality records. Consequently, suppliers able to fuse electronics, adhesives, and validation services stand to capture growing slices of the Future-proof Pharma Labels market.

Future-proof Pharma Labels Industry Leaders

Schreiner Group GmbH & Co. KG

Avery Dennison Corporation

CCL Industries Inc.

Zebra Technologies Corporation

UPM Adhesive Materials

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Schreiner MediPharm released KitCheck-optimized RFID labels supporting 325 million injections across 900 hospitals.

- July 2025: Avery Dennison introduced RFID-enabled in-mold label profiles targeting reusable pharma containers.

- May 2025: Schreiner MediPharm expanded Late-Stage Customization to cover RFID and NFC formats for just-in-time runs.

- April 2024: Schreiner MediPharm began stocking semi-finished RFID labels for rapid personalization, cutting CMO lead time from weeks to days.

Global Future-proof Pharma Labels Market Report Scope

The Future-Proof Pharma Labels Market Report is Segmented by Technology (RFID, NFC, Sensing Labels, Dual-Frequency/Hybrid, Others), Packaging Type (Blister Packs, Syringes and Vials, Bottles, Cartons and Kits, Secondary and Tertiary Logistics Units), End User (Pharmaceutical Manufacturers, Contract Manufacturing Organizations (CMOs), Hospitals and Health Systems, Pharmacies and Retailers, Clinical-Trial Sponsors), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| RFID |

| NFC |

| Sensing Labels |

| Dual-Frequency / Hybrid |

| Others |

| Blister Packs |

| Syringes and Vials |

| Bottles |

| Cartons and Kits |

| Secondary and Tertiary Logistics Units |

| Pharmaceutical Manufacturers |

| Contract Manufacturing Organizations (CMOs) |

| Hospitals and Health Systems |

| Pharmacies and Retailers |

| Clinical-Trial Sponsors |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Technology | RFID | ||

| NFC | |||

| Sensing Labels | |||

| Dual-Frequency / Hybrid | |||

| Others | |||

| By Packaging Type | Blister Packs | ||

| Syringes and Vials | |||

| Bottles | |||

| Cartons and Kits | |||

| Secondary and Tertiary Logistics Units | |||

| By End User | Pharmaceutical Manufacturers | ||

| Contract Manufacturing Organizations (CMOs) | |||

| Hospitals and Health Systems | |||

| Pharmacies and Retailers | |||

| Clinical-Trial Sponsors | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What growth rate does the Future-proof Pharma Labels market expect between 2026 and 2031?

The market is forecast to expand at a 14.02% CAGR, rising from USD 3.04 billion in 2026 to USD 5.86 billion by 2031.

Why are syringes and vials adopting smart labels faster than blister packs?

Biologic injectables require cold-chain tracking and hospital RFID compatibility, pushing syringes and vials to a 16.12% CAGR versus slower growth for mature oral-solid blister packs.

How do serialization mandates influence purchasing decisions?

Imminent DSCSA and EU FMD deadlines make smart labels a compliance necessity, accelerating unit-level adoption across manufacturing and distribution.

Which region will see the fastest expansion of smart pharma labels?

Asia-Pacific leads with a 15.02% CAGR due to expanding CMO capacity and new country-level traceability rules.

What technology trend could lower tag costs for generics?

Flexible ultra-thin ICs produced on plastic substrates promise sub-USD 0.03 unit costs, enabling affordable RFID or NFC for high-volume generics.

How are hospitals driving demand for RFID labels?

Systems like KitCheck automate crash-cart inventory, so hospitals increasingly require RFID-ready primary packs to streamline replenishment and cut medication errors.

Page last updated on: