Asia Pacific Formic Acid Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

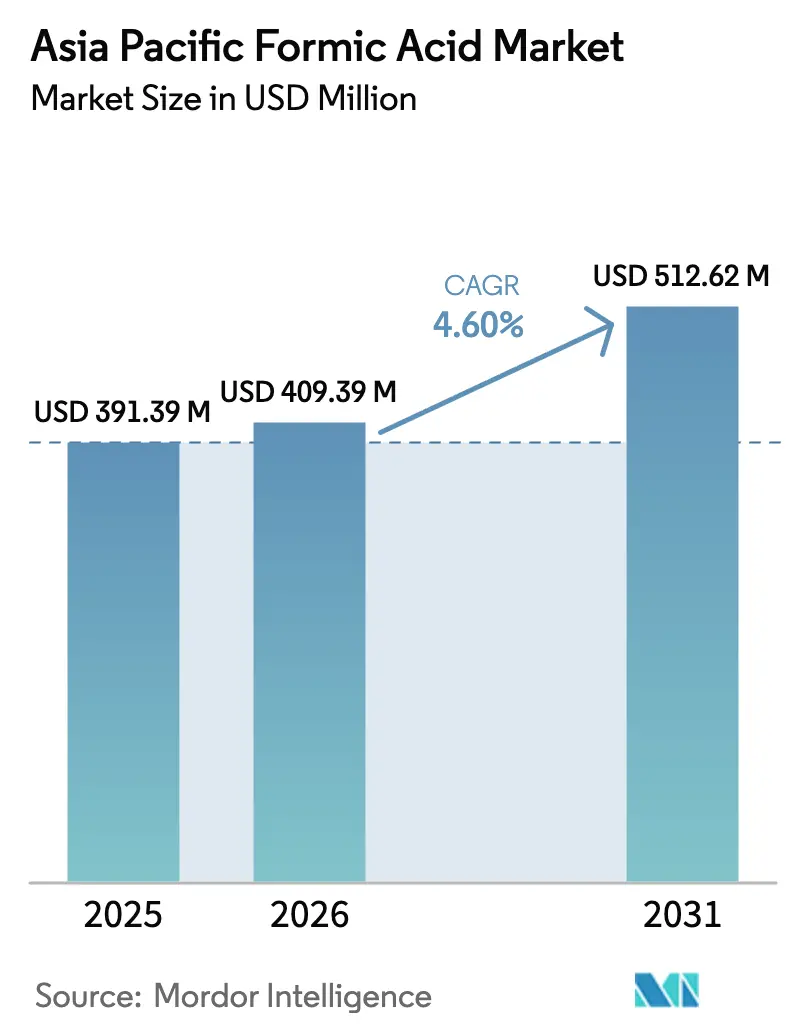

| Base Year Market Size (2025) | USD 391.39 Million |

| Market Size (2026) | USD 409.39 Million |

| Market Size (2031) | USD 512.62 Million |

| Growth Rate (2026 - 2031) | 4.60% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific Formic Acid Market Analysis by Mordor Intelligence

The Asia Pacific Formic Acid Market size was valued at USD 391.39 million in 2025 and is estimated to grow from USD 409.39 million in 2026 to reach USD 512.62 million by 2031, at a CAGR of 4.60% during the forecast period (2026-2031). This trajectory reflects the steady rise of diversified applications across livestock nutrition, leather processing, rubber coagulation, and emerging energy-carrier uses in Japan. China remains the volume anchor, yet its share is edging lower as Indonesia scales latex and oleochemical capacities and India readies policy-backed chemical investments. Feed-acidifier demand is growing in lockstep with a regional livestock boom, while leather and textile producers upgrade to higher-margin exports that rely on 85-90% technical-grade formic acid for consistent pH control. Methanol feedstock volatility and early-stage substitution by wood vinegar and propionic acid temper upside potential, but integrated producers such as BASF and Luxi Chemical continue to widen cost advantages through Verbund synergies and captive methanol. Japan’s pilot projects positioning formic acid as a liquid hydrogen carrier suggest a long-tail technology-led demand stream that could lift volumes beyond 2030 once catalyst costs fall and electrochemical routes mature.

Key Report Takeaways

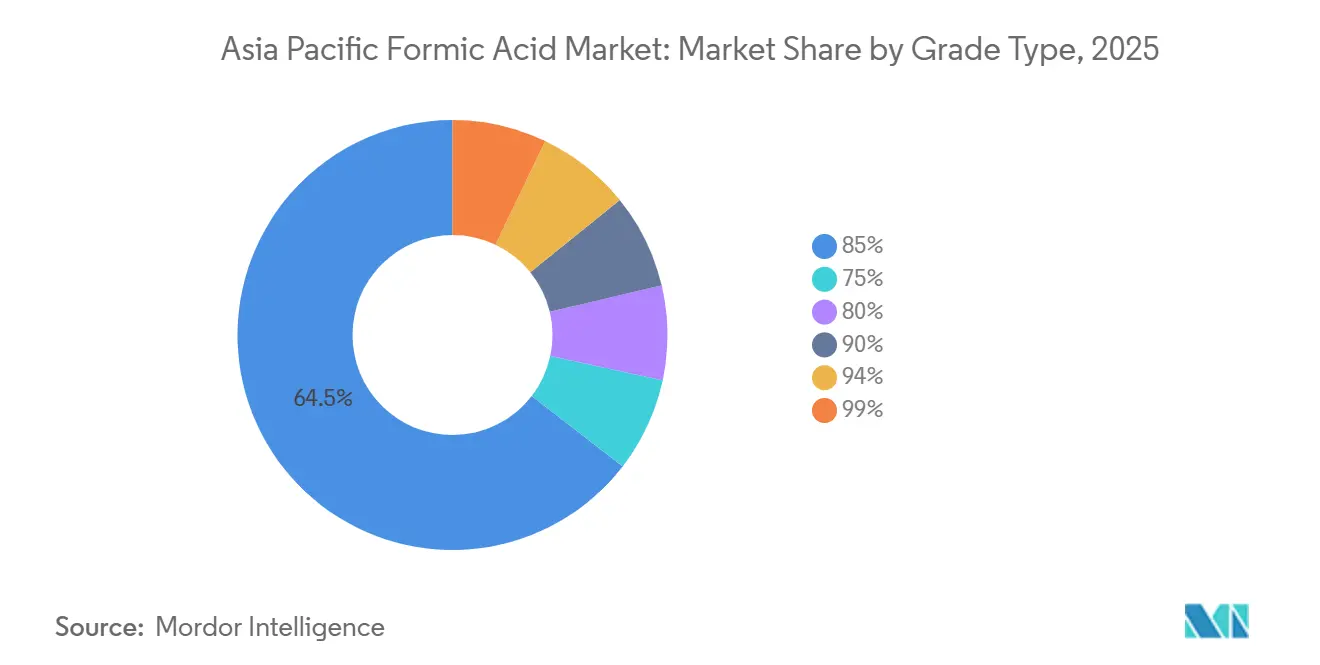

- By grade type, the 85% segment led with 64.51% revenue share in 2025 and is expanding at a 4.08% CAGR to 2031.

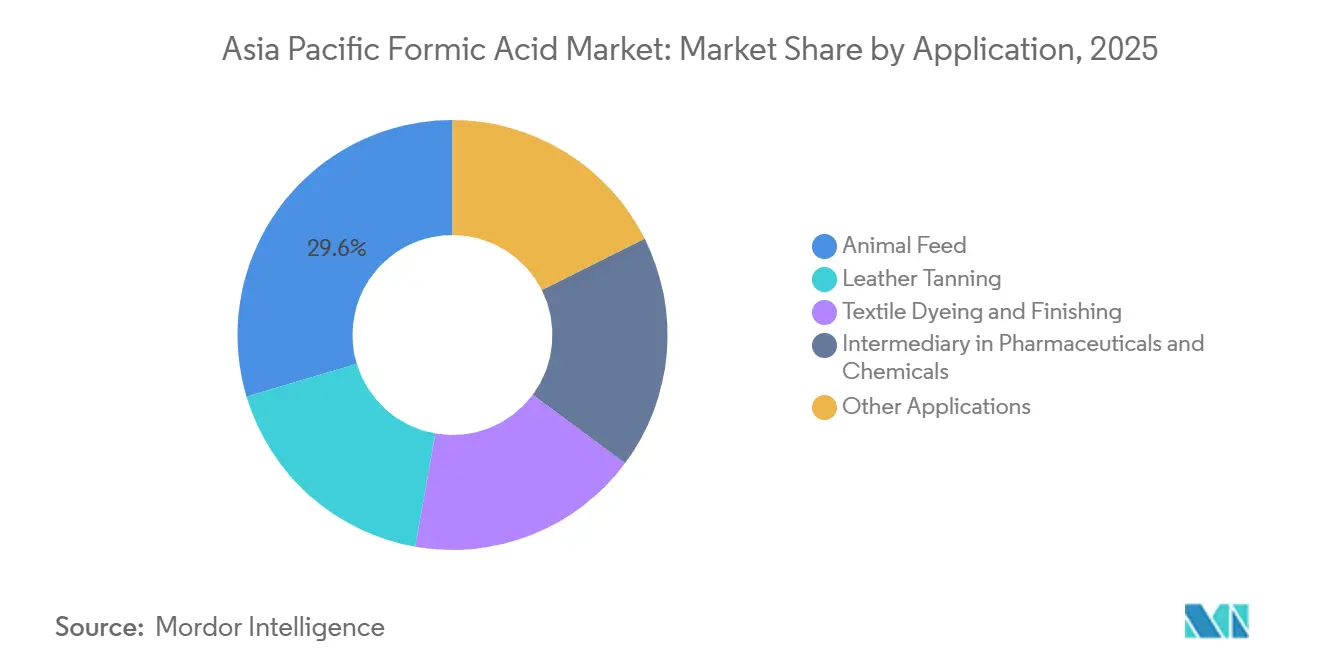

- By application, animal feed accounted for 29.63% of the Asia Pacific formic acid market share in 2025 and is advancing at a 4.13% CAGR through 2031.

- By geography, China held 64.43% of regional demand in 2025; Indonesia is set to post the quickest rise at 5.11% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Asia representing one of the more structurally developed among them. The global report on formic acid market by Mordor Intelligence reflects how these regional layers combine into a single system.

Asia Pacific Formic Acid Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Livestock Boom Driving Demand for Feed and Silage Acidifiers | +1.2% | China, India, Indonesia, Thailand, Vietnam | Medium term (2-4 years) |

| Leather and Textile Capacity Additions in China-India-ASEAN | +0.9% | China, India, Vietnam, Bangladesh, Pakistan | Short term (≤ 2 years) |

| Surging Rubber/Latex Chemical Consumption in Southeast Asia | +0.7% | Thailand, Indonesia, Malaysia, Vietnam | Medium term (2-4 years) |

| Pilot Projects Using Formic Acid as Liquid H₂-Carrier Fuel | +0.4% | Japan, South Korea | Long term (≥ 4 years) |

| Make-In-India Incentives for Domestic Capacity Expansion | +0.5% | India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Livestock Boom Driving Demand for Feed and Silage Acidifiers

Asia Pacific livestock output is forecast to deliver 54% of incremental global agricultural growth by 2034, and India alone is projected to supply nearly 40% of that expansion. Protein-rich diets in lower-middle-income countries are raising average feed intensity, compelling integrators to adopt formic acid to curb pathogenic load and reduce antibiotic use. China’s pivot toward pork and poultry sustains per-ton acidifier demand even as herd efficiency rises. Large Indian feed mills now specify organic-acid blends that include formic acid to meet export-oriented biosafety standards issued in 2025. Regional supply remains tight because GNFC and RCF operate modest capacities, allowing Chinese and Malaysian exporters to fill the gap. Supply chain managers report that price sensitivity has eased for high-purity grades as integrators link acidifier use to measurable reductions in mortality and feed conversion.

Leather and Textile Capacity Additions in China-India-ASEAN

Asian leather hubs are upgrading to premium finished goods destined for Europe and North America, prompting tanneries to standardize on 85–90% technical-grade formic acid for pickling and chrome masking[1]Chemtradeasia, “Formic Acid Technical Data Sheet,” chemtradeasia.com . Environmental regulations introduced in China and India in 2025 mandated lower effluent chromium and sulfate thresholds, driving substitution away from sulfuric toward formic acid. Seasonal maintenance at East Asian formic acid units coincided with the 2025 leather production surge, causing localized tightness that lifted spot prices 8% quarter-on-quarter. Textile dyeing units in Bangladesh and Vietnam expanded capacity for reactive dyes, favoring formic acid in the fixation bath to comply with the ZDHC Roadmap to Zero chemicals list. Stakeholders indicate that demand elasticity is limited because quality-conscious buyers penalize pH drift that leads to leather grain swelling or dye shade variability.

Surging Rubber/Latex Chemical Consumption in Southeast Asia

Thailand, Indonesia, and Vietnam deliver 80% of world natural rubber, and formic acid retains 95% usage in latex coagulation thanks to fast reaction time and low residue. Indonesia’s palm-oil boom adds a second consumption leg because oleochemical plants convert fatty-acid by-products using formic-acid-catalyzed esterification. However, field trials in 2025 confirmed that 10% wood vinegar achieves comparable coagulation on smallholder estates, launching a price-sensitive substitution trend. Indonesia’s rubber processors therefore alternate between formic acid and locally sourced wood vinegar, producing quarterly demand swings of up to 15%. Despite volatility, aggregate consumption still grows because latex output is forecast to climb 4% annually through 2031 as tire plants in Vietnam and Malaysia scale.

Pilot Projects Using Formic Acid as Liquid H₂-Carrier Fuel

Japan’s AIST and the University of Tsukuba unveiled a direct CO₂-to-formic-acid synthesis in late 2024 that quadruples reaction rates versus aqueous pathways, cutting process steps and cost. Kanazawa University later demonstrated a porous catalyst layer that lifts direct formic acid fuel-cell power density by 25%. These advances strengthen formic acid’s credentials as a liquid organic hydrogen carrier that can be stored at ambient conditions, sidestepping compressed-gas infrastructure. Demonstration rigs installed at two Japanese municipal bus depots recorded 2,000 hours of operation during 2025-2026 with stable performance. Commercial uptake remains long-tail but migrates the chemical from commodity status toward a specialty energy vector, supporting a technology premium for ultra-pure 94% and 99% grades.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Substitution by Cheaper Organic Acids in Feed and Tanning | -0.6% | Global, with acute impact in China, India, Southeast Asia | Short term (≤ 2 years) |

| Volatile Methanol/CO Feedstock Costs | -0.8% | China, India, Malaysia, Japan | Short term (≤ 2 years) |

| Rising Compliance Costs for Corrosive-Chemical Handling | -0.4% | China, India, Japan, South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Substitution by Cheaper Organic Acids in Feed and Tanning

Propionic and acetic acids undercut formic acid by 10–15% per ton when sourced from integrated Verbund sites able to amortize fixed costs. Large feed integrators in China began trialing propionic-dominant blends in 2025 to lower cost of gain, and Bangladeshi tanners have shifted to dual-acid pickling systems that use acetic acid for bulk pH adjustment with formic acid finishing. Wood vinegar’s field validation as a latex coagulant in Thailand and Indonesia adds another substitution lever at the smallholder level. If raw-material spreads widen further, substitution could accelerate, capping premium-grade growth despite rising end-market volumes.

Volatile Methanol/CO Feedstock Costs

Methanol comprises roughly half of variable costs, and Q4 2024 price spikes forced Luxi Chemical to idle part of its 300,000 MT/y line to stabilize the local market, as disclosed in its December investor note[2]Luxi Chemical, “Investor Update Q4 2024,” luxichemical.com . BASF’s Zhanjiang Verbund, commissioned in 2025, channels methanol into Oxo-alcohols first, tightening merchant availability for standalone formic acid plants. Smaller producers lacking captive methanol hedge via quarterly contracts indexed to coal-based production costs in China, yet margin compression persists. Feedstock price volatility moves directly to customer invoices, triggering inventory drawdowns at Southeast Asian rubber processors and Indian leather clusters.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade Type: Technical Grades Dominate Industrial Applications

The 85% grade commanded 64.51% of the Asia Pacific formic acid market in 2025, and it is projected to grow at a 4.08% CAGR through 2031 as key consuming clusters widen capacity. Integrated giants can switch purity levels mid-run, but 85% remains the sweet spot between yield, corrosion control, and pH stability demanded by tanners, dyers, and rubber processors. Demand resilience is strengthened because leather exporters in China and Vietnam receive higher unit prices for softer, fuller grain finished with consistent formic-acid pickling. BASF’s June 2025 launch of low-product-carbon-footprint 85% grade created a template for sustainability-driven procurement that may carve out a premium micro-segment over the next three years.

Purity bands at 75% and 80% serve price-sensitive rubber coagulation and commodity textile lines, but substitution by wood vinegar and blended acids is shaving share. High-purity 90%, 94%, and 99% grades fulfill electronics cleaning, pharmaceutical intermediates, and hydrogen-storage pilot demands in Japan and South Korea, yet volumes remain comparatively small. Growth visibility is rising as Japanese fuel-cell developers specify 94% purity for direct formic acid fuel-cell anodes, expecting niche commercialization post-2030. With Luxi Chemical bringing a 400,000 MT/y line onstream by 2027, supply security for premium grades improves, though sustainability credentials rather than capacity alone will shape buyer choice in export-driven belts.

By Application: Animal Feed Leads Amid Biosecurity Pressures

Animal feed held 29.63% of regional demand in 2025 and is projected to climb at a 4.13% CAGR, buoyed by expanding poultry and swine herds and regulatory curbs on prophylactic antibiotics. Formic acid’s dual role as preservative and gut-acidifier enhances feed conversion ratios, offering a quantifiable return on inclusion that encourages adoption even when input prices firm. China’s efficiency gains offset some volume, yet higher-value pork diets and integrator-level biosecurity standards protect per-ton usage. India’s protein transition, with per-capita meat consumption rising toward 6 kg by 2031, underpins sustained acidifier pull; local supply gaps ensure continued imports from Malaysia and China.

Leather tanning grows marginally, driven by ASEAN and South Asian capacity additions aimed at premium footwear and upholstery segments. Textile dyeing is expanding because Bangladesh and India push vertical integration to secure higher garment export margins; formic acid is preferred in dye fixation baths that comply with ZDHC chemical management protocols. Pharmaceutical and specialty-chemical intermediates add incremental tonnage in Japan, South Korea, and China’s fine-chemical clusters, supporting premium-purity requirements. Rubber coagulation remains a cornerstone but faces substitution headwinds, while potassium-formate de-icing and industrial cleaning plateau at low single-digit growth.

Geography Analysis

China retained a commanding 64.43% share of the Asia Pacific formic acid market in 2025 thanks to integrated capacity exceeding 550,000 MT/y across Luxi Chemical, Feicheng Acid Chemicals, Wanhua, and BASF’s 50,000 MT Nanjing unit. Luxi’s 400,000 MT/y brownfield expansion, scheduled for 2027 start-up, will raise its global share toward 30% and extend China’s export surplus. Domestic consumption still expands on the back of feed, leather, and textile sectors, yet overcapacity positions China as the region’s swing exporter. Methanol price spikes in late 2024 prompted supply throttling, underscoring the chain’s exposure to upstream energy swings.

Indonesia is the fastest-growing node, posting a 5.11% CAGR through 2031 as latex processors increase integration and palm-oil downstreamers scale oleochemicals. Supply fragmentation persists; domestic traders rely on spot cargoes from China, with landed prices varying 15-20% quarter-to-quarter, complicating long-term contracting.

India’s demand is supported by GNFC’s 12,705 MT/y and RCF’s 10,000 MT/y plants, yet still imported over half its requirement. The GNFC-INEOS acetic acid project exemplifies capital rotation into higher-margin acids, implying limited near-term expansion for domestic formic acid. Japan and South Korea together account for a smaller share, with technology-led pull from electronic, pharmaceutical, and hydrogen-carrier projects. Malaysia serves as a trading hub, funneling imports to Vietnam, the Philippines, and Thailand, where on-the-ground consumption rises but infrastructure and regulatory heterogeneity deter local production investment.

Mordor Intelligence provides coverage of the formic acid market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to Saudi Arabia incorporating local coverage and market participation, as required.

Competitive Landscape

The Asia Pacific formic acid market is moderately consolidated. Strategic actions trend toward vertical integration and sustainability branding. Luxi Chemical bundles captive methanol and CO off-gas streams, lowering variable costs and widening export price elasticity. BASF stitched an MoU with UPC Technology in 2024 to secure Oxo-alcohol offtake, indirectly constricting merchant methanol pools for third-party formic acid plants. Perstorp’s upstream-by-product valorization into calcium formate broadens its leather-chemical bundle aimed at Indian and Vietnamese tanners. Emerging disruptors include Japanese fuel-cell consortia that demand ultra-low-impurity 94% grades, carving a niche that mid-scale Korean producers such as Lotte Fine Chemical intend to address.

M&A appetite stays constrained because green-field Verbund economics outperform asset roll-ups, and antitrust regulators have sharpened scrutiny. Instead, technology partnerships flourish: Korea Institute of Energy Research published a biomass-to-formic-acid route in 2025 that captures CO₂ as carbonic acid, highlighting carbon-negative credentials. Producers now weigh life-cycle carbon metrics alongside traditional cost curves when positioning future investments.

Asia Pacific Formic Acid Industry Leaders

Gujarat Narmada Valley Fertilizers & Chemicals Limited

BASF

Luxi Group

Eastman Chemical Company

Chongqing Chuandong Chemical (Group) Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BASF launched low-PCF (Product Carbon Footprint) formic acid in eAuction platform in China. This initiative aimed to support industrial buyers in the region in achieving their sustainability objectives, particularly Scope 3 emissions targets, by offering transparent, lower-carbon chemical solutions for applications such as plastics, pharmaceuticals, and coatings.

- November 2024: Japan's National Institute of Advanced Industrial Science and Technology (AIST) and the University of Tsukuba jointly announced a significant advancement in carbon capture and utilization. They developed an iridium catalyst system capable of synthesizing formic acid directly from CO₂ using a supercritical solvent, which increased the formation rates of formic acid by four times compared to previous methods.

Asia Pacific Formic Acid Market Report Scope

Formic acid, or methanoic acid, is the simplest form of carboxylic acid with a pungent odor. Due to its antibacterial properties, it is used in the animal feed and silage industry as an additive and an intermediary in the pharmaceutical industry. The product is also used in other industries like leather, tanning, dyes, and textiles.

The formic acid market is segmented by grade type, application, and geography. By grade type, the market is segmented into 75%, 80%, 85%, 90%, 94%, and 99%. By application, the market is segmented into animal feed, leather tanning, textile dyeing and finishing, intermediary in pharmaceuticals and chemicals, and other applications. The report also covers the market size and forecasts for formic acid across 8 major countries in the Asia Pacific region. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| 85% |

| 75% |

| 80% |

| 90% |

| 94% |

| 99% |

| Animal Feed |

| Leather Tanning |

| Textile Dyeing and Finishing |

| Intermediary in Pharmaceuticals and Chemicals |

| Other Applications |

| China |

| India |

| Japan |

| South Korea |

| Indonesia |

| Thailand |

| Malaysia |

| Vietnam |

| Rest of Asia Pacific |

| By Grade Type | 85% |

| 75% | |

| 80% | |

| 90% | |

| 94% | |

| 99% | |

| By Application | Animal Feed |

| Leather Tanning | |

| Textile Dyeing and Finishing | |

| Intermediary in Pharmaceuticals and Chemicals | |

| Other Applications | |

| By Geography | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Malaysia | |

| Vietnam | |

| Rest of Asia Pacific |

Key Questions Answered in the Report

What is the current value of the Asia Pacific formic acid market?

The market is valued at USD 409.39 million in 2026 and is forecast to reach USD 512.62 million by 2031.

Which application segment consumes the most formic acid in Asia Pacific?

Animal feed leads demand, holding 29.63% share in 2025 and growing at a 4.13% CAGR.

Why is Indonesia the fastest-growing national market?

Rising rubber and palm-oil processing, coupled with oleochemical investment, drive Indonesian demand at a 5.11% CAGR through 2031.

How does methanol pricing affect formic acid producers?

Methanol accounts for up to 50% of variable costs, so price spikes compress producer margins and can trigger temporary output cuts.

Page last updated on: