Chile Fruits And Vegetables Market Analysis by Mordor Intelligence

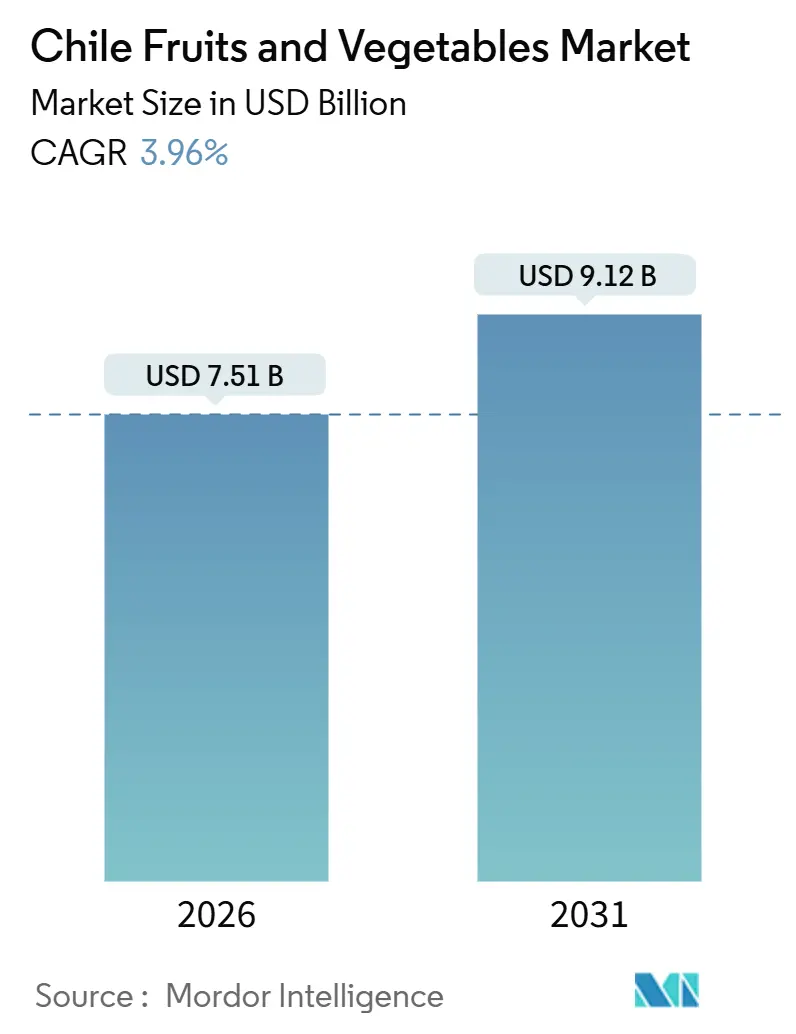

The Chile fruits and vegetables market size stands at USD 7.51 billion in 2026 and is projected to reach USD 9.12 billion by 2031, registering a 3.96% CAGR during 2026-2031. A decisive shift from wine-grape monoculture toward export-oriented cherries and blueberries, rising urban incomes, and strong plant-forward dietary trends are steering demand. Export volumes for cherries reached 401,203 metric tons in the 2024-2025 season, while domestic consumption increased due to the adoption of flexitarianism among millennials in Santiago, Valparaíso, and Concepción. Central Chile continues to dominate output, owing to its irrigated valleys and proximity to ports. Southern Chile is gaining traction as growers chase cooler microclimates and lower land costs to extend the export calendar. Government irrigation subsidies, precision agriculture rollouts, and a United States systems approach that eliminates costly fumigation have reduced operating risks and improved quality premiums. Persistent megadrought, labor shortages, port congestion, and residue-related shipment rejections remain headwinds that temper the medium-term outlook.

Key Report Takeaways

- By type, fruits accounted for 57% of the Chile fruits and vegetables market size in 2025 and are forecast to grow at a 3.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Chile Fruits And Vegetables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising vegan and flexitarian population | +0.4% | National with early gains in Santiago, Valparaíso, and Concepción | Medium term (2-4 years) |

| Expansion of export-oriented orchards | +0.8% | Asia-Pacific focus with spillover to North America and Europe | Long term (≥ 4 years) |

| Government irrigation subsidies and water-efficiency tech adoption | +0.5% | Central and Northern Chile | Medium term (2-4 years) |

| United States-Chile systems approach reducing fumigation costs for grapes | +0.3% | North America, with secondary benefits in Europe | Short term (≤ 2 years) |

| Retail and e-commerce push for fresh-cut convenience stock keeping unit (SKUs) | +0.3% | National, concentrated in urban Santiago and Valparaíso | Short term (≤ 2 years) |

| Varietal renewal boosting post-harvest quality | +0.4% | Global, strongest in Asia-Pacific and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Vegan and Flexitarian Population

Domestic per-capita consumption of fresh produce in Chile climbed 8% between 2019 and 2025, driven by a documented shift toward plant-based diets among urban consumers aged 25 to 40. Survey data from the Chilean Ministry of Health indicated that 22% of Santiago residents identified as flexitarian in 2025, up from 14% in 2020, reflecting heightened awareness of cardiovascular health and environmental sustainability [1]Source: Chilean Ministry of Health, “National Dietary Survey 2025,” minsal.cl. This behavioral pivot is amplifying demand for ready-to-eat salad kits, pre-cut vegetable trays, and organic berries in supermarket chains such as Jumbo and Walmart Chile. Retailers are responding by dedicating 15% to 20% of fresh-produce floor space to plant-based meal solutions, a category that generated USD 340 million in sales across Chile in 2024. The trend is particularly pronounced in Santiago, where disposable incomes exceed the national average by 28%, enabling premium pricing for organic and locally sourced vegetables.

Expansion of Export-Oriented Orchards

Growers converted 8,200 hectares of vineyard land and idle pasture to cherry and blueberry orchards in 2024 and 2025, targeting counter-seasonal export windows into China, where Chilean fruit commands a 40% premium over domestic alternatives during the Lunar New Year period. According to United States Department of Agriculture, Chile exported 401,203 metric tons of cherries in the 2024-2025 season, with 91% of the shipments going to China, generating FOB revenues of USD 1.8 billion. Blueberry shipments reached 134,000 metric tons in the same season, a 12% increase year-on-year, as late-season varieties such as Ventura and Cargo extended the harvest calendar into April and captured premium pricing in North American and European markets. The rapid expansion is straining cold-chain infrastructure, with reefer container shortages at Valparaíso port delaying shipments by up to 9 days during the peak harvest months of December and January.

Government Irrigation Subsidies and Water-Efficiency Tech Adoption

Chile's National Irrigation Commission (CNR), operating under the Ministry of Agriculture, allocated USD 43 million in 2024 and USD 49 million in 2025 to co-finance drip irrigation systems, pivot installations, and soil moisture sensors for smallholder and mid-sized growers. Chile's economic development agency launched a parallel program in 2024 to subsidize precision-agriculture platforms that integrate satellite imagery, weather forecasts, and real-time soil data to optimize irrigation scheduling. Early adopters in O'Higgins and Maule regions reported water savings of 18% to 25% and yield improvements of 12% for table grapes and stone fruits. The Chilean Association of Fruit Exporters (ASOEX) estimates that 14,000 hectares of orchards and vegetable fields adopted drip or micro-sprinkler systems in 2024, up from 9,800 hectares in 2023, as growers sought to mitigate rising water-trucking costs that exceeded USD 50 per cubic meter in peak summer months.

United States Chile Systems Approach Reducing Fumigation Costs for Grapes

The United States Department of Agriculture's Animal and Plant Health Inspection Service (USDA APHIS) approved Chile's system approach for table grapes in December 2023, eliminating the requirement for methyl bromide fumigation at United States ports of entry. This regulatory shift reduced post-harvest treatment costs by USD 0.08 to USD 0.12 per kilogram and cut spoilage losses by 6% to 8%, as fumigation-induced stem browning and berry softening were eliminated. The systems approach mandates orchard-level monitoring for Mediterranean fruit fly, packing-house sanitation protocols, and traceability systems that link each carton to its source block. Compliance costs average USD 0.03 per kilogram, a fraction of the fumigation expense. The approach has been extended to stone fruits and kiwifruit, with approval from the United States Department of Agriculture's Animal and Plant Health Inspection Service (USDA APHIS) granted in March 2025.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Megadrought-induced water scarcity in Central Valley | −0.6% | Central Chile with spillover to Northern valleys | Long term (≥ 4 years) |

| Rising labor costs and seasonal labor shortages | −0.5% | National, acute in Central and Southern zones | Medium term (2-4 years) |

| Logistics bottlenecks at San Antonio and Valparaíso ports | −0.3% | National, affecting all exporters | Short term (≤ 2 years) |

| Pesticide-residue alerts triggering shipment rejections | −0.3% | Global, with the highest impact in Europe and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Megadrought-Induced Water Scarcity in Central Valley

Central Chile has experienced a 30% reduction in surface water availability since 2019, as the megadrought, now in its 15th consecutive year, has depleted reservoirs and snowpack in the Andes. The Maule River basin recorded flows 42% below the 30-year average in 2024, forcing growers to drill wells exceeding 200 meters in depth and truck water at costs surpassing USD 50 per cubic meter during peak summer months [2]Source: World Bank, “Chile Economic Outlook 2024,” worldbank.org . The Chilean Water Directorate (DGA) issued 1,240 water rights suspensions in the O'Higgins and Maule regions in 2024, affecting 18,600 hectares of orchards and vegetable fields, as priority allocation shifted to urban consumption and hydropower generation. Growers responded by investing in drip irrigation, soil moisture sensors, and deficit irrigation protocols that reduce water application by 20% to 30% while maintaining acceptable yields.

Rising Labor Costs and Seasonal Labor Shortages

Chile raised its monthly minimum wage to USD 475 in January 2025, a 7% nominal increase that elevated labor costs for harvest-intensive crops such as table grapes, cherries, and asparagus. Seasonal agricultural employment in Chile totaled 420,000 workers during the 2024-2025 harvest season, a 6% decrease from 447,000 in the 2019-2020 season, as younger workers migrated to urban service sectors and construction, which offer year-round contracts and higher wages. Hortifrut deployed 18 autonomous berry-harvesting platforms in its Maule blueberry fields in 2024, achieving picking rates of 25 kilograms per hour compared to 12 kilograms for manual labor. The company announced plans to expand robotic coverage to 40% of its Chilean acreage by 2027. Mechanical harvesting remains unsuitable for delicate stone fruits and premium table grapes, where hand-picking preserves stem integrity and minimizes bruising.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Fruits Dominate Amid Berry and Cherry Export Surge

By type, fruits accounted for 57% of the Chile fruits and vegetables market size in 2025 and are forecast to grow at a 3.8% CAGR through 2031. According to the United States Department of Agriculture (USDA), berries and table grapes capitalize on counter-seasonal export windows into Asia, North America, and Europe. Cherry exports reached 401,203 metric tons in the 2024-2025 season, generating FOB revenues of USD 1.8 billion, with 91% of volumes shipped to China during the December-to-February window [3]Source: USDA Foreign Agricultural Service, “Chile Stone Fruit Annual Report 2025,” fas.usda.gov .

Blueberries contributed 134,000 metric tons, a 12% year-on-year increase, as late-season varieties such as Ventura and Cargo extended the harvest calendar into April and captured premium pricing when competing Southern Hemisphere suppliers exited the market. Table grapes, apples, and kiwifruit, along with seedless grape varieties, are gaining market share as the United States' Chilean systems approach eliminates methyl bromide fumigation costs and reduces spoilage by 6% to 8%. Avocados, citrus, and walnuts contributed smaller volumes but are expanding in Northern Chile, where arid conditions reduce fungal pressure and enable lower pesticide application rates.

Geography Analysis

Central Chile, encompassing the O'Higgins, Maule, and Ñuble regions, benefits from established irrigation infrastructure, proximity to Santiago's wholesale markets, and access to the San Antonio and Valparaíso export terminals. The region produced 78% of Chile's table grapes, 64% of stone fruits, and 52% of apples in 2024, capitalizing on Mediterranean microclimates that provide optimal chill hours and heat accumulation for deciduous crops. The Chilean Water Directorate (DGA) issued 1,240 water-rights suspensions in O'Higgins and Maule in 2024, affecting 18,600 hectares, and constraining production growth to 1.8% annually through 2031.

Southern Chile, spanning Biobío, La Araucanía, and Los Lagos, is the fastest-growing region as growers exploit cooler microclimates, lower land costs averaging USD 12,000 per hectare, and higher annual rainfall exceeding 1,200 millimeters. The region expanded cherry acreage by 1,800 hectares in 2024 and 2025, targeting late-season varieties that ripen in February and March, when Chinese demand peaks and competing suppliers have exited the market. Blueberry plantings reached 6,200 hectares in 2025, up from 4,800 hectares in 2022, with late-season cultivars such as Cargo and Atlas generating FOB prices 18% higher than mid-season fruit.

Northern Chile, encompassing Atacama, Coquimbo, and Valparaíso, specializes in table grapes, citrus, avocados, and walnuts that utilize arid conditions to minimize fungal pressure and reduce pesticide dependency. The region produced 22% of Chile's table grapes in 2024, with early-season varieties such as Sugraone and Crimson Seedless capturing premium pricing in November and December before Central Chile volumes arrive. Water scarcity remains acute, with the Elqui and Limarí river basins recording flows 38% below the 30-year average in 2024, prompting investments in desalination and wastewater-recycling projects that cost USD 1.20 to USD 1.50 per cubic meter.

Regulatory Landscape

Chile's fruits and vegetables sector is regulated primarily through the Servicio Agricola y Ganadero (SAG), the national authority empowered under Law 18.755 to certify phytosanitary compliance for domestic circulation and exports. For export horticultural products, SAG operates an official control framework that includes sampling, investigations, and response protocols when importing countries notify non-compliance (for example, under the official control system established in 2021), which directly affects exporters facing residue-related alerts and shipment rejections.

Market access is shaped more by phytosanitary requirements and trade rules than by border protection. Chile applies a largely flat 6% MFN tariff across almost all tariff lines, while extensive FTAs shift competition toward non-tariff compliance. In February 2025, the EU-Chile Advanced Framework Agreement entered into provisional application, and in June 2026 SAG issued Res. Exenta No. 1006/2026 expanding a Mediterranean fruit fly quarantine area tied to China export requirements after detections in the Metropolitan Region, increasing the operational importance of origin-specific eligibility and traceability for fruit exporters.

Value Chain Analysis

The value chain spans input suppliers (nurseries, agrochemicals, irrigation and sensor vendors), growers concentrated in irrigated valleys of Central Chile with expansion in the south, and a packing and cold-chain layer that conditions product for long-haul exports. Exporters and marketer-packer groups consolidate volumes, coordinate compliance with SAG phytosanitary certification and importing-country protocols, and route shipments through key gateways such as Valparaiso and San Antonio, while domestic volumes flow to wholesale markets and modern retail, including fresh-cut and convenience produce formats in major cities.

Cold-chain capacity and port logistics are critical cost and quality levers, especially in peak months when reefer containers and terminal throughput become binding constraints. Operational disruptions have highlighted fragility in the export leg, including the 2024-2025 season incident involving the Maersk Saltoro delay that stranded more than 1,300 containers of cherries for China during a key demand window, reinforcing the need for stronger risk management in scheduling, insurance, and contingency routing. At the farm level, irrigation and water-management investments supported by CNR co-financing, alongside mechanization pilots such as Hortifrut's autonomous berry-harvesting platforms, increasingly connect production decisions to labor availability, water scarcity, and export-quality specifications.

Competitive Landscape

The Chilean fruits and vegetables market in 2025 is characterized by producers, importers, exporters, and other players holding significant shares, reflecting the dominance of mid-sized family operations and cooperative structures that aggregate smallholder output for export. Dispersion creates white-space opportunities for vertically integrated players that can control cold-chain logistics, secure long-term retail contracts, and invest in varietal innovation. Leading players are expanding robotic coverage to 40% of their Chilean acreage by 2027, a move that signals the sector's pivot toward mechanization as labor costs rise.

Unifrutti Traders acquired Verfrut in January 2024, integrating 2,400 hectares of stone-fruit orchards and securing long-term supply agreements with Walmart Chile and Costco. This acquisition demonstrates how consolidation is being driven by retailers' demand for year-round supply and traceability. Smaller exporters, such as Exportadora Subsole, Prize Export, and Greenvic, are carving out niches in organic certification, late-season varieties, and direct-to-consumer e-commerce, thereby bypassing traditional wholesale channels to capture higher margins.

Technology adoption is accelerating, with 14,000 hectares of orchards and vegetable fields adopting drip or micro-sprinkler systems in 2024, up from 9,800 hectares in 2023, supported by CLP 42 billion (USD 43 million) in government subsidies. The Chilean Association of Fruit Exporters (ASOEX) filed 14 varietal patents in 2024, covering late-season cherries, low-chill peaches, and extended-shelf-life blueberries, signaling the sector's shift toward intellectual-property-driven differentiation.

Market Opportunities and Future Outlook

Opportunities center on strengthening quality and compliance systems for export-driven fruits (cherries, blueberries, grapes), while building resilience in water use and post-harvest performance. Government-backed programs provide concrete adoption channels at scale: the National Irrigation Commission (CNR) allocated USD 49 million in 2025 to co-finance drip irrigation, pivots, and sensors, and precision-agriculture support programs have reported measurable water savings (18% to 25%) among early adopters in O'Higgins and Maule. Separately, export protocols such as the USDA APHIS systems approach (approved for table grapes in December 2023 and extended to stone fruits and kiwifruit in March 2025) reduce reliance on costly fumigation and increase the value of traceability, orchard monitoring, and packhouse sanitation capabilities.

Export-market development and technology translation into commercial operations also create room for differentiation in perishability management and logistics. In 2026, public research and innovation bodies expanded sector tools that can be integrated into commercial packing and export workflows, including INIA's May 2026 digital report to predict post-harvest behavior and quality in blueberry exports and CIREN-FIA's July 2026 AI platform for real-time biomass and soil monitoring, relevant to broader farm decision support and resource efficiency. With fruit exports in the 2025/2026 season totaling USD 7.35 billion FOB (September 2025 to April 2026) and cherries, grapes, and blueberries representing 71.6% of export value, investments that reduce transit losses, improve compliance consistency, and extend harvest windows in Southern Chile align directly with where value concentration and operational constraints are most visible.

Recent Industry Developments

- May 2026: Ferrero Hazelnut Company announced a USD 94 million investment to build a new hazelnut shelling plant in Cunco, La Araucania Region. The project expands in-country processing capacity, supporting higher value capture and tighter quality control for Chilean nut supply chains that sit adjacent to the broader fruit export ecosystem.

- October 2025: Peru, Mexico, and Chile launched the Global Grape Group (GGG), bringing leading table grape exporters into a coordinated alliance to support consumption and market access through joint promotion. The initiative reflects a more organized, category-level approach to demand creation in key import markets, which can influence pricing power and shelf visibility for Chilean grapes.

- January 2024: Unifrutti Traders acquired Verfrut, adding approximately 2,400 hectares of stone-fruit orchards and strengthening integrated supply for major retail customers. The deal reinforced consolidation in export-oriented fruit, improving scale in sourcing and packing while raising competitive pressure on smaller exporters to differentiate through certification, varieties, or channel strategy.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the market covers the value of fruits and vegetables in Chile, expressed in USD, and anchored in how supply and demand move through production, domestic consumption, imports, exports, and wholesale pricing.

Scope exclusions: It does not count downstream packaged food processing and retail service margins beyond the produce value itself.

Segmentation Overview

- Type

- Vegetables

- Potatoes

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis

- Tomatoes

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis

- Onions

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis

- Potatoes

- Fruits

- Grapes

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis

- Apples

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis

- Blueberries

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis

- Cherries

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis

- Avocados

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis

- Kiwi

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis

- Grapes

- Vegetables

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building a fact base on Chile crop output, trade flows, and price direction, then aligning definitions so the value series stays consistent year to year. Public sources such as FAOSTAT, UN Comtrade, the Chilean national statistics office, the Chilean agriculture ministry and its supporting agencies, and customs and port statistics were used to map volumes and seasonality.

We also reviewed company annual reports and investor presentations for operating footprint clues, alongside trade association releases and reputed press for shifts in planted area, water availability, and export logistics. For hard-to-find cross checks, we used paid subscriptions that support company financials and news intelligence, plus shipment-level trade data and patent databases when relevant to post-harvest handling and packaging. This list is not exhaustive, and other sources were also referred to for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on confirming what the desk numbers cannot fully explain, especially how export windows, grade-outs, and wholesale price formation change by season and by crop. We spoke with stakeholders across the value chain in Chile, including growers, exporters, importers, wholesalers, distributors, and large produce buyers, and then used these views to validate assumptions and close data gaps for the market.

To keep the model realistic, responses were compared across different company scales and job roles, and conflicting inputs were followed up until one consistent market story was reached.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 13% | |

| Mid tier: 54% | Functional/Unit leaders: 38% | |

| Smaller Players: 16% | Managers: 49% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where production and trade data reconstruct the available supply pool for Chile. That supply pool is then aligned with domestic consumption and export demand, and priced using wholesale trend lines to arrive at value. After shaping the totals, we check them with selective bottom-up approximations such as sampled crop volumes multiplied by typical wholesale prices, plus channel checks on how much volume moves through key wholesale routes.

Inputs that matter in this market include production volumes in metric tons, export and import values and volumes, wholesale price trends by major produce groups, yield and planted area direction, and logistics conditions that affect shipped volumes and realized prices. Forecasting uses scenario analysis, where experts helped set ranges for weather and water constraints, export demand strength, and price normalization, and then a central case was chosen when signals lined up.

If a bottom-up cross check had missing coverage for smaller crops or informal routes, we filled gaps using ratio-based scaling from the most stable series, then re-tested the final value against the full set of trade and price indicators.

Data Validation & Update Cycle

Validation is done in steps so one number is not accepted without checks from at least two independent angles. Outputs are compared against trade values, production movements, and price direction, and major variances are reviewed to confirm they are explainable. For example, a price spike without a volume drop is questioned.

Before sign-off, the model and assumptions undergo analyst reviews, and follow-up calls are triggered if a key input changes or an interview indicates a material shift. Reports are refreshed annually, with interim updates when major events occur, and a final pre-delivery scan is completed so clients receive the latest view.

Mordor Intelligence's Chile Fruits and Vegetables Market Sizing Compared With Other Published Estimates

Published market values for Chile fruits and vegetables often do not match because the market boundary is not set the same way, and the time base can also shift across reports. Differences also come from which price level is used, how imports and exports are treated, and how quickly assumptions are refreshed when harvest or logistics conditions change.

Export and import value series, production volume trends, and wholesale price movements are the signals that tie the estimate back to what is physically grown and traded in Chile, which is how Mordor Intelligence arrives at USD 7.51 B (2026) for the market under the stated scope.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.51 B (2026) | |

| Global Consultancy A | USD 1.82 B (2025) | Uses a smaller stated base year and a scope that explicitly mixes fresh with processed and frozen forms, and it may be closer to a narrower demand pool measured through select channels rather than a full production plus trade aligned value. |

| Data Publisher B | USD 4.23 B (2024) | Uses an earlier base year and a different segmentation lens (organic vs non-organic emphasis), and the pricing and coverage approach appears less anchored to combined production, trade, and wholesale price checks, which can shift the implied market total. |

The table shows that most gaps come from scope boundaries and the year and price anchors used in the model. When the value is built from consistent volume signals and matched with price trends, the final number becomes easier to trace and to repeat for future updates.

Key Questions Answered in the Report

What is the current and projected value of the Chile fruits and vegetables market?

The Chile fruits and vegetables market size is USD 7.51 billion in 2026 and is projected to reach USD 9.12 billion by 2031.

Which crop category leads sales?

Fruits hold 57% of the value of 2025, led by export-ready cherries, blueberries, and table grapes.

Which region in Chile is growing the fastest in terms of produce production?

Southern Chile is growing, driven by late-season cherry and blueberry plantings.

What technological trends are shaping competitiveness?

Precision irrigation, varietal renewal, and robotic harvesters help manage water scarcity, labor costs, and post-harvest quality.

Who is the market leader among exporters?

Producers, importers, and exporters such as Garces Fruit stand out with significant shares and substantial investments in automation and varietal research and development.

Page last updated on: