Brazil Fruits And Vegetables Market Analysis by Mordor Intelligence

The Brazil fruits and vegetables market size is expected to grow from USD 30.0 billion in 2025 to USD 31.42 billion in 2026 and is forecast to reach USD 39.59 billion by 2031 at 4.74% CAGR over 2026-2031. The market expansion is attributed to urbanization, heightened health consciousness, and sustained production enabled by diverse agro-climatic conditions. Strategic investments in irrigation systems, cold chain infrastructure, and digital farming technologies are enhancing productivity and minimizing post-harvest losses. The favorable exchange rates maintain export margins despite fluctuating transportation costs. Processing companies are implementing vertical integration strategies to secure raw material supply and optimize profit margins, which is transforming supply chain dynamics. Producers are deploying cost-reduction technologies and diversifying market presence due to input price volatility and uncertain trade policies.

Key Report Takeaways

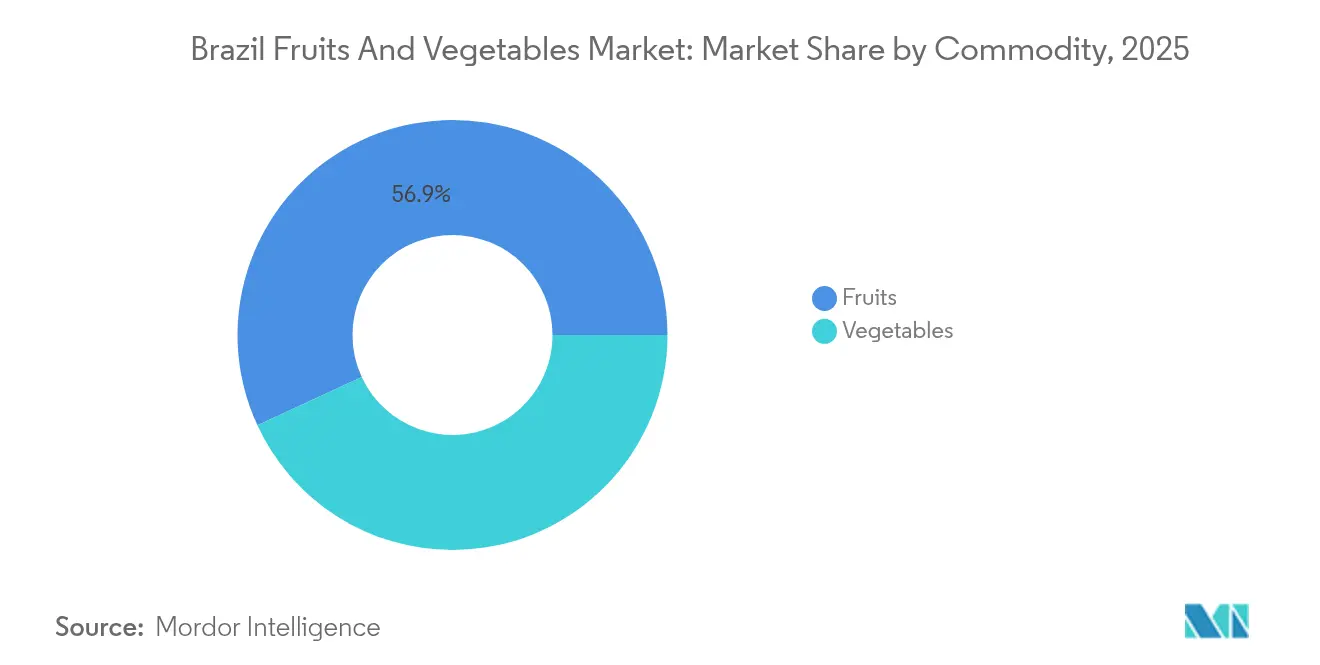

- By commodity, fruits accounted for 56.90% of the Brazil fruits and vegetables market share in 2025, whereas vegetables are projected to post a 4.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Fruits And Vegetables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging fruit-juice export contracts | +0.8% | Northeast Brazil, and São Paulo citrus belt | Medium term (2-4 years) |

| Accelerating domestic demand for fresh-cut fruits and vegetables | +0.6% | Southeast urban corridors | Short term (≤ 2 years) |

| Diverse agro-climatic zones enabling year-round output | +0.5% | Nationwide | Long term (≥ 4 years) |

| Government credit lines for horticulture tech | +0.4% | National family-farming areas | Medium term (2-4 years) |

| Expansion of drip-irrigation in semi-arid Northeast | +0.3% | Bahia and Pernambuco | Long term (≥ 4 years) |

| Ag-e-commerce platforms linking growers to institutional buyers | +0.2% | Southeast and South peri-urban belts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Fruit-Juice Export Contracts

Orange juice processors secured new multiyear contracts at premium prices, supported by a 36% increase in 2025-26 orange production to 314.6 million boxes. Export demand remained stable after the August 2025 United States tariff implementation, as juice concentrates and essential oils received exemptions. Processors invested in disease-resistant citrus varieties to protect against greening disease, which affects 50% of groves in São Paulo and Minas Gerais[1]HF Brasil, “From Sweet to Sour: U.S. Tariff Shake-Up Hits Brazil's Juice and Fruit Trade,” hfbrasil.org.br. Asian and Middle Eastern buyers established binding off-take agreements, expanding beyond traditional North American markets. The industry's vertical integration expanded, exemplified by Louis Dreyfus Company's 2024 retail brand launch. These developments provided the Brazil fruits and vegetables market with protection against commodity price fluctuations and international policy changes.

Accelerating Domestic Demand for Fresh-Cut Fruits and Vegetables

The Brazil fruits and vegetables market is experiencing growth due to changing consumer preferences and operational improvements. Urban households and institutional kitchens prefer washed, sliced, and ready-to-cook products that reduce preparation time and provide a nine-day shelf life under cold storage[2]Revista Verde de Agroecologia e Desenvolvimento Sustentável, “Avaliação das principais causas de perdas pós-colheita de hortaliças,” gvaa.com.br. Processing facilities near São Paulo operate double shifts, while new facilities in Minas Gerais serve interior cities. Restaurants and catering services are transitioning to value-added packages, reducing labor costs by up to 20% and increasing demand for leafy greens and root vegetables. Cold-chain improvements, supported by concessional loans, reduce post-harvest losses from previous levels of 35-40%. Medium-sized cooperatives are implementing audit compliance software to meet standardized good-manufacturing practices and food safety regulations. These market developments expand the customer base and strengthen relationships between processors and institutional buyers.

Diverse Agro-Climatic Zones Enabling Year-Round Output

Brazil's diverse geography, spanning from the equatorial Amazon to temperate Rio Grande do Sul, creates complementary growing seasons that reduce seasonal supply gaps. The Southeast region produces 51% of the country's fruit volume, while the Northeast accounts for 24%. This geographical distribution provides a natural buffer when one region experiences drought or frost. The country's varied climate enables counter-seasonal exports to Northern Hemisphere markets, allowing exporters to fulfill contracts despite weather challenges. Brazilian producers implement crop rotation to maintain soil health, meeting sustainability standards that earn premium prices in European and Japanese markets. The Plano Safra program supports climate-smart farming practices, including mulching, cover crops, and micro-irrigation, which enhance yields and reduce carbon emissions. These factors strengthen Brazil's position as a reliable supplier, particularly during global supply chain uncertainties.

Government Credit Lines for Horticulture Tech

The 2025-26 Plano Safra allocates BRL 89 billion (USD 16.5 billion) for family farms, representing a 55% increase and reducing interest rates to 2-3% for certified horticulture operations[3]Governo Federal, “Plano Safra 2025/2026,” gov.br. The program provides low-interest loans for drip irrigation systems, precision sprayers, and post-harvest cooling tunnels, making these technologies accessible to small growers. BNDES has distributed BRL 1.7 billion (USD 315 million) for these upgrades, with disbursement rates increasing by 12% in H1 2025[4]BNDES, “BNDES’s Rural Credit Program has approved R$ 1.7 billion since its creation,” bndes.gov.br. The mechanization helps address rural labor shortages, while improved yields enable equipment cost recovery within five harvests for high-value crops such as grapes and melons. The program includes subsidized insurance with credit packages to protect growers from weather-related risks and ensure stable loan repayment. This initiative reduces the productivity gap between smallholder farmers and large export-oriented estates by improving access to agricultural technology.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inadequate refrigerated logistics and rural roads | -0.7% | National; highest in Northeast | Medium term (2-4 years) |

| High volatility in fertilizer and diesel prices | -0.5% | Nationwide | Short term (≤ 2 years) |

| Labor shortages from rural-urban migration | -0.4% | Southeast and South | Long term (≥ 4 years) |

| Europe deforestation-traceability compliance costs | -0.3% | Amazon fringe exporters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Inadequate Refrigerated Logistics and Rural Roads

Brazil's cold storage facilities are primarily located in coastal population centers, while agricultural production clusters are situated hundreds of kilometers inland. The poor condition of feeder roads increases transit time, and with only 12% of farm-gate trucks equipped with refrigeration, farmers must either accept lower prices or risk product spoilage during peak seasons. While government freight corridors prioritize bulk grain transportation, perishable goods compete for limited cold-chain capacity. Private investment concentrates in high-volume citrus production regions, creating regional disparities that limit market access for small-scale farmers in the Northeast. The Brazil fruits and vegetables market continues to lose 18% of annual production before reaching retail outlets due to inadequate specialized logistics infrastructure.

Labor Shortages from Rural-Urban Migration

The migration of young adults from farms to service sector jobs in Rio de Janeiro and São Paulo has reduced the availability of seasonal workers needed for labor-intensive crops such as tomatoes and strawberries. This labor shortage has led to increased wages, raising production costs, while mechanization remains challenging for delicate fruit harvesting. Although cooperatives have implemented training programs to improve worker productivity, the demographic shift continues. The constrained labor market affects growth strategies, especially for vegetable processors who require steady raw material supplies. The Brazil fruits and vegetables market faces ongoing labor availability challenges until harvesting automation technology improves.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Commodity: Fruits Lead Value While Vegetables Drive Growth

Fruits dominated the market, accounting for 56.90% of the Brazil fruits and vegetables market share in 2025 through established citrus, mango, and grape supply chains that combine favorable climate conditions with extensive research investment. Citrus processors maintain price stability through long-term contracts, while banana production meets domestic demand with a consistent year-round supply. Tropical fruits, particularly mango and papaya, have capitalized on export opportunities during Northern Hemisphere off-seasons, generating higher unit revenue and increasing the market size at the farm level.

The vegetable segment, though smaller in value share, demonstrates the strongest growth potential with a projected 4.93% CAGR through 2031. According to the Food and Agriculture Organization, tomato production reached 4.1 million metric tons in 2023, supporting processing centers that produce sauces and ready-to-cook products for urban retail markets. Potato production benefits from coordinated planting schedules across three regions, ensuring a continuous supply for food service customers. Onion and garlic production, concentrated among family farms in the South and Northeast regions, benefits from the National Program for the Strengthening of Family Farming (PRONAF) extended credit programs, strengthening smallholder operations. The expansion of fresh-cut vegetable processing adds value to the segment and increases its contribution to the overall Brazil fruits and vegetables market size.

Geography Analysis

The Southeast region holds 45.80% of the Brazil fruits and vegetables market share in 2025, driven by juice-concentrate facilities in São Paulo and greenhouse expansion in Minas Gerais. The region's extensive highway network and proximity to 45 million consumers reduce delivery times, resulting in higher profit margins compared to national averages. The region's innovation hubs host agricultural technology startups, accelerating the implementation of sensors, drones, and data analytics to improve yields and reduce pesticide usage.

The Northeast region is projected to grow at a 5.04% CAGR during 2026-2031. The Petrolina-Juazeiro irrigation center utilizes São Francisco River water through drip irrigation systems to produce high-brix mangoes, seedless grapes, and melons with extended shelf life. The region's proximity to European and North American markets reduces freight time by up to four days compared to Andean competitors. In 2025, public-private initiatives that installed 420 megawatts of solar power have reduced energy costs at packing facilities, improving regional competitiveness.

South Brazil's agricultural sector comprises small and medium-sized family farms that operate through cooperatives. The region's rolling terrain and mild climate support diverse production, including soybeans, corn, wheat, tobacco, dairy, fruits, and vegetables. While traditionally strong in grain production, the region faces challenges from extreme weather events that affect soybean yields and economic stability. The temperate climate enables specialized crop production through cooperative networks. In Paraná, ADM's nutrient facility has increased local input supply by 40%. Rio Grande do Sul benefits from lower night temperatures, which enhance apple and berry color development while reducing tropical pest exposure. The region's rail connections to São Paulo help stabilize delivery costs despite diesel price fluctuations throughout growing seasons.

Recent Industry Developments

- July 2025: The Brazil government launched Plano Safra 2025-26 with BRL 516.2 billion (USD 95.04 billion) in credit, emphasizing low-carbon farm practices and irrigation upgrades for fruits and vegetables.

- June 2025: The Brazilian Agricultural Research Corporation (EMBRAPA) introduced two early-season orange varieties, Kawatta and Majorca, to overcome the limitations of traditional early oranges such as Hamlin. These varieties deliver enhanced juice quality in terms of flavor and color, increased yields, and reduced production cycles.

- November 2024: Brazil received approval to export table grapes to China after the Brazilian Ministry of Agriculture and Livestock (Mapa) and Chinese customs authorities established a new protocol. The agreement specifies that only registered orchards, packing facilities, and cold treatment facilities meeting good agricultural practice standards can participate in the export program.

Brazil Fruits And Vegetables Market Report Scope

The Brazilian fruits and vegetables market is segmented by type (fruits and vegetables). The report includes production (volume), consumption (volume and value), import (volume and value), export (volume and value), and price trend analysis. Price analysis covering the top 10 fruits and vegetables across Brazil has also been included. The report offers market size and forecast in terms of value in USD million and volume in metric tons for the above-mentioned segments.

By Commodity (Production Analysis (Volume), Consumption Analysis (Volume and Value), Import Analysis (Volume and Value), Export Analysis (Volume and Value), and Price Trend Analysis)

| Fruits | Citrus (Orange, Lemon, Lime,Tangerines, mandarins, and clementines) |

| Banana | |

| Watermelon | |

| Grapes | |

| Pineapples | |

| Mango | |

| Apple | |

| Papayas | |

| Other Fruits (Cantaloupes and other melons, Avocados, Peaches and nectarines, Strawberries, etc,) | |

| Vegetables | Tomato |

| Potato | |

| Onion and Shallots | |

| Garlic | |

| Brassicas | |

| Other Vegetables (Leafy Greens, Carrot, Beans, Eggplant, etc.) |

| By Commodity (Production Analysis (Volume), Consumption Analysis (Volume and Value), Import Analysis (Volume and Value), Export Analysis (Volume and Value), and Price Trend Analysis) | Fruits | Citrus (Orange, Lemon, Lime,Tangerines, mandarins, and clementines) |

| Banana | ||

| Watermelon | ||

| Grapes | ||

| Pineapples | ||

| Mango | ||

| Apple | ||

| Papayas | ||

| Other Fruits (Cantaloupes and other melons, Avocados, Peaches and nectarines, Strawberries, etc,) | ||

| Vegetables | Tomato | |

| Potato | ||

| Onion and Shallots | ||

| Garlic | ||

| Brassicas | ||

| Other Vegetables (Leafy Greens, Carrot, Beans, Eggplant, etc.) | ||

Key Questions Answered in the Report

How large is the Brazil fruits and vegetables market in 2026?

The value is USD 31.42 billion, with projections of USD 39.59 billion by 2031 at a 4.74% CAGR.

Which commodity group leads sales?

Fruits supply 56.90% of total 2025 spending, anchored by citrus, mango, and grape exports.

What is the fastest-growing segment?

Vegetables are on track for a 4.93% CAGR as fresh-cut demand rises in urban centers.

How are producers financing technology upgrades?

Plano Safra loans and BNDES credit supply subsidized rates as low as 2%, encouraging drip irrigation, cold storage, and precision equipment.

What risks could slow future growth?

Logistics bottlenecks, volatile fertilizer prices, and stringent EU deforestation rules pose downside threats to export margins.

Page last updated on: