Beta Glucan And Fucoidan Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

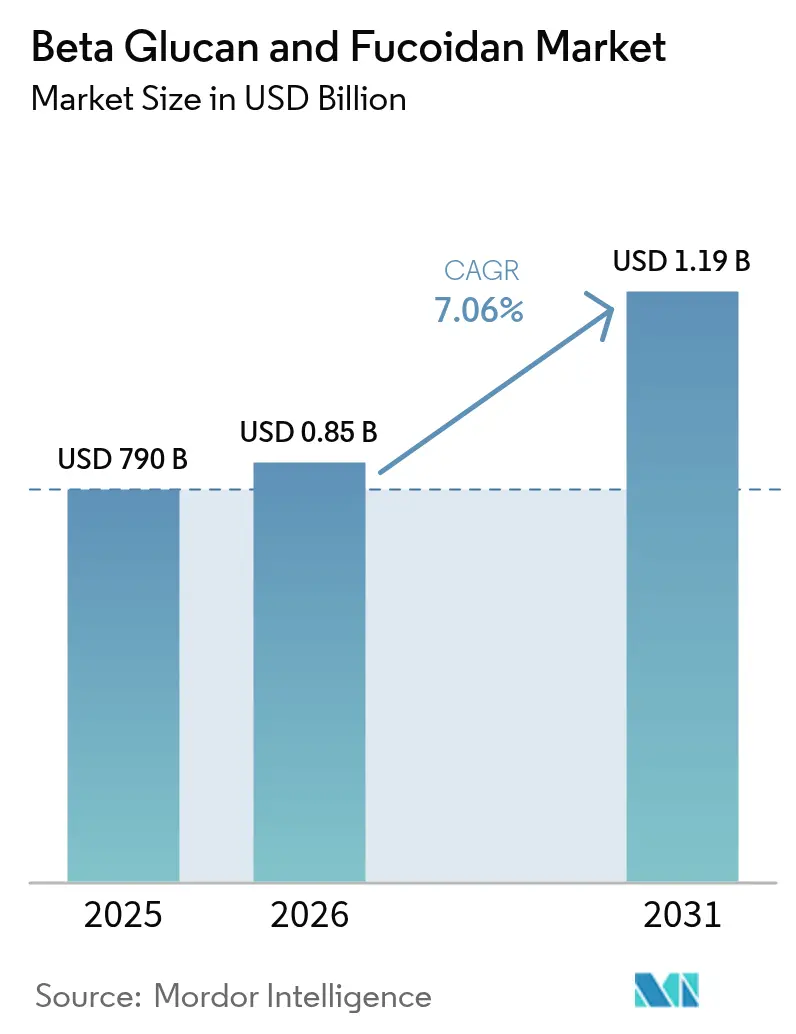

| Market Size (2026) | USD 0.85 Billion |

| Market Size (2031) | USD 1.19 Billion |

| Growth Rate (2026 - 2031) | 7.06% CAGR |

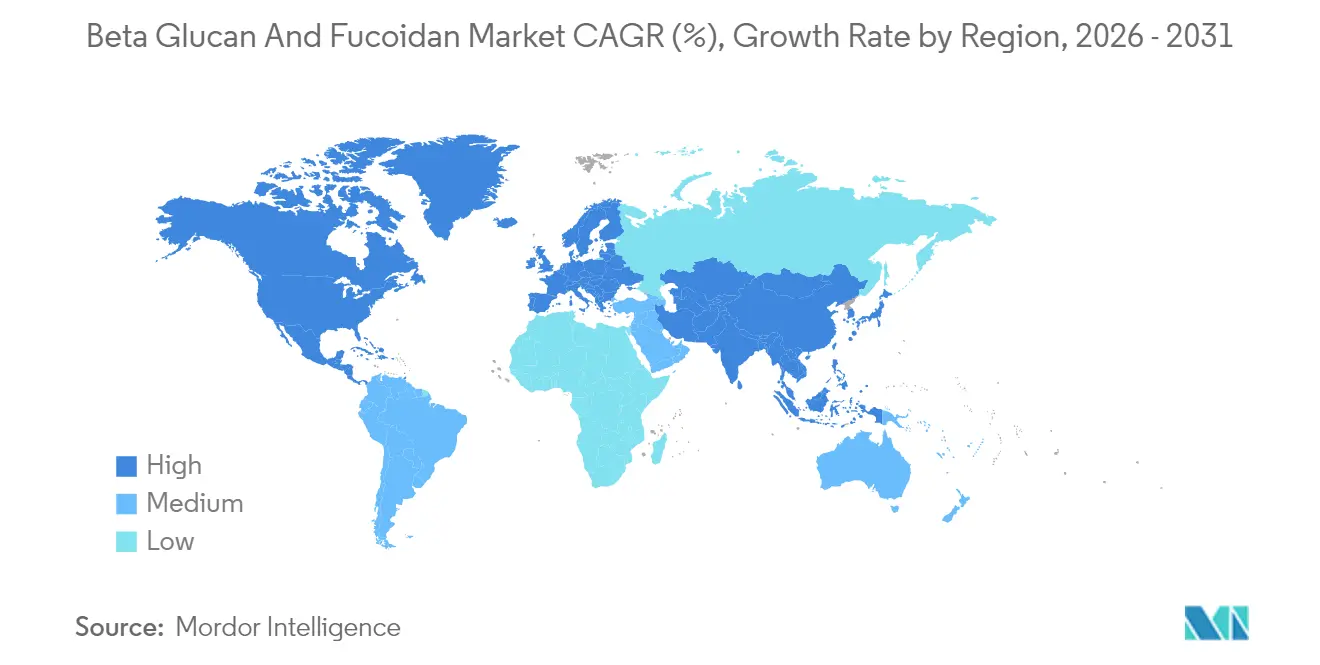

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

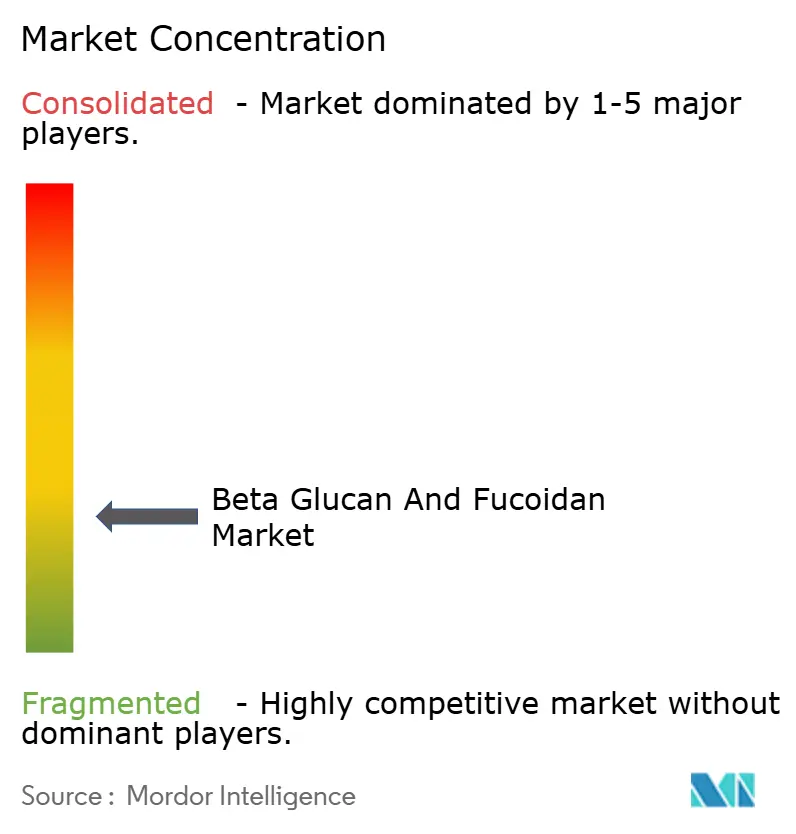

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Beta Glucan And Fucoidan Market Analysis by Mordor Intelligence

The beta-glucan and fucoidan market size is expected to grow from USD 790 million in 2025 to USD 845.77 million in 2026 and is forecast to reach USD 1.19 billion by 2031 at 7.06% CAGR over 2026-2031. Heightened pharmaceutical demand for immunomodulatory polysaccharides, stricter clean-label standards in packaged foods, and consumers’ readiness to pay for clinically proven immune-support supplements jointly sustain this growth path. Beta-glucan, supplied from yeast, mushrooms, oats, barley, and algae, maintained the lion’s share in recent years, while fucoidan, derived chiefly from brown seaweed, is scaling swiftly on the back of cosmetics and oncology-support uses. Food makers reformulating for natural fiber content, supplement brands bundling immune-support actives, and pharmaceutical formulators seeking wound-healing and adjuvant cancer therapies are simultaneously expanding addressable demand. Competitive pressure from alternative fibers persists, yet the beta-glucan and fucoidan market continues to secure shelf space because published clinical evidence helps brands substantiate performance claims. Supply-side advances in extraction technologies further improve purity, consistency, and application flexibility, reinforcing suppliers’ pricing power despite volatile raw-material costs.

Key Report Takeaways

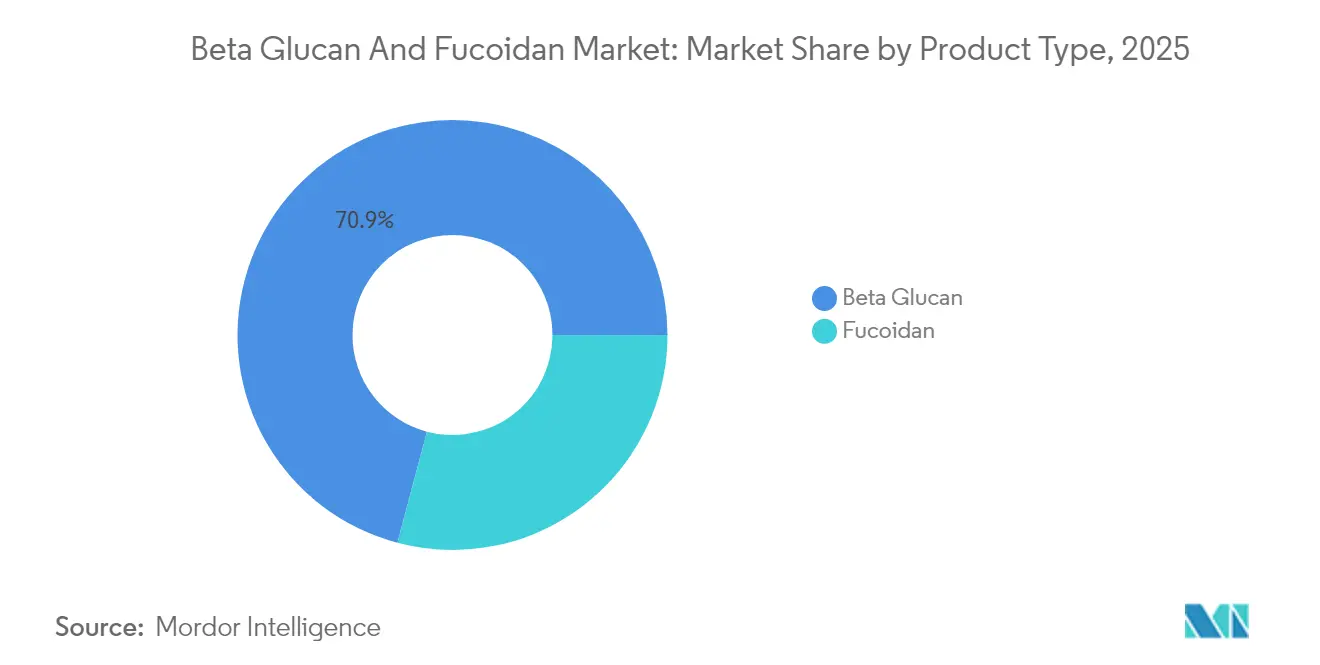

- By product type, beta-glucan commanded 70.88% of the beta-glucan and fucoidan market share in 2025. Fucoidan is forecast to post the fastest growth, registering an 7.78% CAGR through 2031.

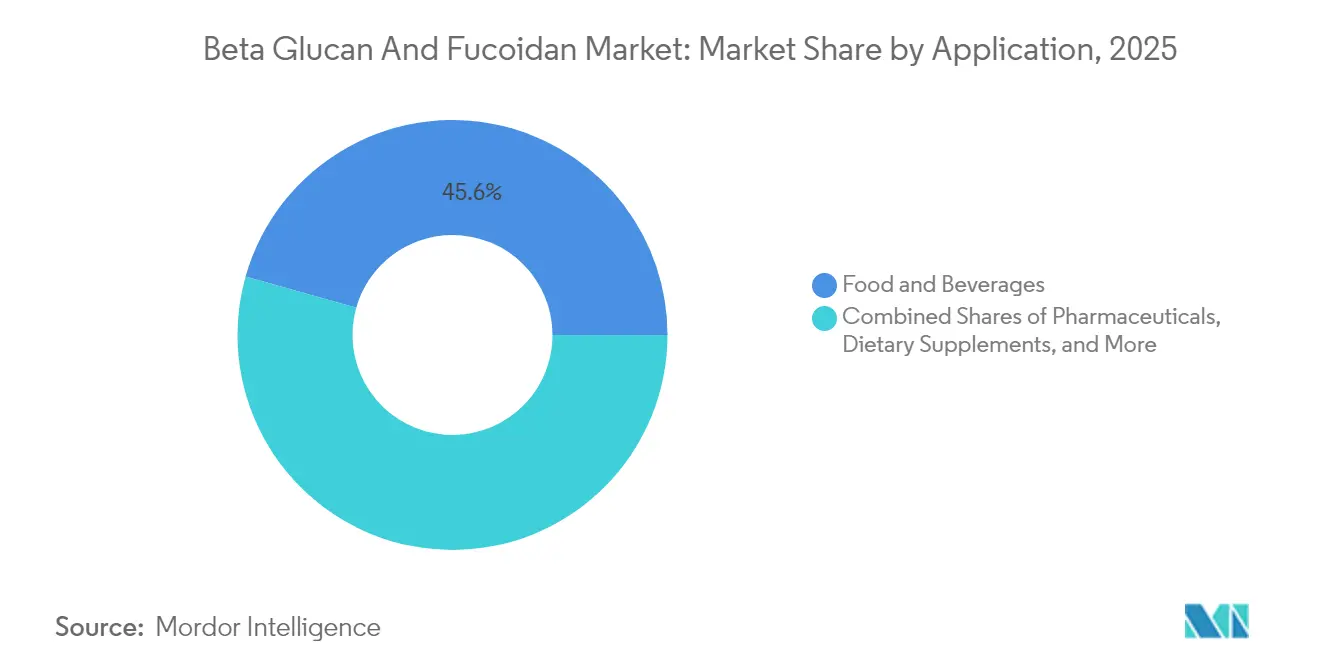

- By application, food and beverages captured 45.62% of the beta-glucan and fucoidan market size in 2025. Dietary supplements are projected to expand at a 9.12% CAGR between 2026 and 2031.

- By geography, Europe led with 34.35% market share in 2025, while Asia-Pacific is expected to accelerate at a 9.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Beta Glucan And Fucoidan Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing immune-health supplement spending | +1.4% | Global, with concentration in North America and Europe | Short term (≤ 2 years) |

| Expansion in food and beverage sector for clean-label, fortified products | +1.2% | Europe, North America, Asia Pacific urban centers | Medium term (2-4 years) |

| Growth in cosmetics and personal care | +0.9% | Europe, Asia-Pacific (Japan, South Korea) | Medium term (2-4 years) |

| Advancements in extraction and production technologies | +0.8% | Global, led by Europe and North America R&D hubs | Long term (≥ 4 years) |

| Increasing research and development investments from manufacturers | +0.7% | North America, Europe, China | Long term (≥ 4 years) |

| Rising pharmaceutical procurement for immunomodulatory applications | +1.0% | North America, Europe, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing immune-health supplement spending

Demand for immune-support supplements surged after the 2020-2023 pandemic, positioning beta-glucan and fucoidan as science-backed options that rival traditional vitamin C or zinc. Yeast-derived beta-glucan standardized to 70–85% purity dominates e-commerce and specialty retail because published clinical trials link consistent daily intake to reduced upper respiratory infection incidence. Fucoidan products, often combined with astaxanthin or curcumin, appeal to consumers seeking marine-sourced bioactives, yet U.S. regulatory ambiguity around structure-function claims keeps distribution skewed toward online channels. Personalized nutrition platforms that tailor formulations based on microbiome analysis rely on batch-specific certificates of analysis, prompting suppliers to upgrade analytical capabilities. Subscription models for monthly beta-glucan deliveries gain traction in urban markets, where convenience, perceived efficacy, and transparent sourcing justify premium pricing.

Expansion in Food and Beverage Sector for Clean-Label, Fortified Products

Food manufacturers are modifying product formulations to align with clean-label requirements by substituting synthetic emulsifiers and stabilizers with functional fibers like beta-glucan, which offer both textural advantages and health benefits. Oat beta-glucan, authorized by the European Food Safety Authority (EFSA) for cholesterol-reduction claims at a daily intake of 3 grams, is being added to breakfast cereals, yogurt, and plant-based milk alternatives, helping brands differentiate in competitive markets[1]Source: EFSA Panel, “Scientific Opinion on the Substantiation of Health Claims Related to Beta-Glucans from Oats and Barley,” EFSA Journal, efsa.europa.eu. Soluble beta-glucan from barley is increasingly used in beverage applications, where its viscosity-enhancing properties facilitate sugar reduction without affecting mouthfeel. In bakery applications, insoluble beta-glucan is utilized to enhance dietary fiber content while preserving dough extensibility, catering to consumer demand for high-fiber bread that maintains its taste and texture. Fucoidan remains underutilized in food applications due to its seaweed-derived flavor profile and limited Generally Recognized as Safe (GRAS) affirmation in the United States. Nevertheless, Japanese and Korean food companies have effectively incorporated low-molecular-weight fucoidan into functional beverages and instant soups. In Europe, the regulatory process for novel food ingredients requires pre-market authorization, creating challenges for smaller seaweed processors but ensuring that approved ingredients gain credibility with risk-averse multinational brands.

Growth in Cosmetics and Personal Care

Fucoidan’s documented capacity to stimulate fibroblast proliferation and inhibit matrix metalloproteinase activity underpins its role as a premium anti-aging active. European beauty brands introduced marine-active serums in 2024, citing clinical data showing enhanced skin elasticity and reduced transepidermal water loss. Yeast and mushroom beta-glucan appear in moisturizers and post-procedure products due to their immunomodulatory impact on Langerhans cells and ability to accelerate wound healing. Clean-beauty trends favor naturally derived polysaccharides over synthetic polymers, and Asian brands lead commercialization by embedding low-molecular-weight fucoidan in sheet masks. Regulatory frameworks vary—EU Cosmetic Regulation requires detailed safety files, while several Southeast Asian markets allow quicker entry, giving established suppliers with toxicological dossiers a clear edge.

Advancements in Extraction and Production Technologies

Enzymatic extraction now replaces acid-alkali processes for fucoidan, generating higher-purity fractions with lower environmental impact. Supercritical CO₂ extraction, though capital-heavy, yields solvent-free beta glucan suited to organic products. Membrane filtration enables precise fucoidan fractionation, tailoring sulfation patterns to cosmetic or pharmaceutical specs. Yeast-fermentation lines are optimized via strain engineering to produce cell walls richer in 1,3/1,6-linked beta glucan, trimming downstream costs. Pilot-scale precision-fermentation projects aim to synthesize fucoidan analogs without seaweed inputs, offering a potential supply-chain disruptor if unit economics improve. Suppliers that pair structural characterization tools such as NMR with robust QA protocols win contracts from pharma buyers demanding batch-to-batch consistency.

Restraint Impact Analysis*

| Restraints | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility | -1.1% | Global, with acute impact in Asia-Pacific seaweed supply | Short term (≤ 2 years) |

| Stringent food safety, labeling, and health claim regulations | -0.9% | Europe, North America | Medium term (2-4 years) |

| Competition from alternative functional fibers and immune-health ingredients | -0.7% | Global, particularly cost-sensitive food applications | Medium term (2-4 years) |

| High production expenses for purification and standardization processes | -0.8% | Global, affecting smaller processors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Food Safety, Labeling, and Health-Claim Regulations

EU Novel Foods rules impose multi-year approval cycles for new fucoidan sources, favoring incumbents with existing dossiers and deterring smaller entrants. EFSA’s high evidentiary bar compels suppliers to fund expensive clinical work if they seek disease-reduction claims, weeding out anecdotal submissions. In the United States, FDA oversight of structure-function claims under DSHEA places a compliance burden on marketers who must police downstream retailers’ language or risk warning letters[2]Source: U.S. FDA, “FDA Allows Whole Oat Foods to Make Health Claim on Reducing the Risk of Heart Disease,” fda.gov. Gluten-free certification becomes tricky for barley-derived beta-glucan, which may contain trace gluten despite purification. Emerging traceability mandates necessitate digital supply-chain systems that many small processors cannot yet afford.

Raw-Material Price Volatility

Brown seaweed harvests experience cyclical variability due to factors such as ocean-temperature fluctuations, coastal pollution, and competing demand from alginate and carrageenan processors. Fucoidan suppliers that do not have vertically integrated seaweed cultivation face margin pressures when spot prices for Laminaria and Fucus biomass rise, as seen in 2024 following reduced harvests in China's coastal provinces. Yeast-fermentation substrates for beta glucan production are connected to grain commodity markets, with molasses and corn steep liquor prices impacted by ethanol demand and shifts in agricultural policies. Smaller ingredient suppliers lacking long-term supply agreements with seaweed farmers or yeast producers face procurement challenges, restricting their ability to fulfill multi-year contracts with food and pharmaceutical buyers. Climate-related disruptions, including marine heatwaves and changes in nutrient upwelling patterns, threaten the sustainability of wild seaweed harvests. This has driven investment in land-based aquaculture systems, which enable controlled production but require substantial capital investment and technical expertise. Furthermore, currency fluctuations in seaweed-exporting nations such as Japan and South Korea add pricing uncertainties for European and North American buyers, particularly when contracts are denominated in local currencies without hedging mechanisms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Yeast and Oat Sources Anchor Beta Glucan Dominance

Beta glucan held 70.88% of the market share in 2025, driven by its regulatory approval, diverse sourcing, and broad applications in food, pharmaceuticals, and supplements. Yeast-derived beta glucan dominates supplements due to its immune-activating properties, while oat and barley beta glucan are preferred in cholesterol-reducing food products. Mushroom-derived beta glucan appeals to plant-based consumers, and soluble and insoluble fractions are used in beverages, dairy, and high-fiber snacks for their functional benefits.

Fucoidan is expected to grow at an 7.78% CAGR from 2026 to 2031, supported by its anti-inflammatory and anti-coagulant properties. Derived from brown seaweed, it offers application-specific grades for cosmetics, pharmaceuticals, and functional foods. Low-molecular-weight fucoidan is gaining traction in supplements, while high-molecular-weight forms are used in wound care and drug delivery. Regulatory challenges and high production costs limit its adoption in price-sensitive markets.

By Application: Dietary Supplements Outpace Food Fortification

Food and beverages captured 45.62% of the beta-glucan and fucoidan market size in 2025, anchored by oat beta-glucan’s cholesterol-reduction halo in cereals, granola bars, and plant-based yogurts. Bakeries prize beta-glucan’s water-binding capacity for shelf-life extension, while beverage formulators rely on soluble variants for mouthfeel in low-sugar drinks. Fucoidan’s sea-savory notes curb Western uptake, but Japanese instant soups show consumers accept the flavor when paired with umami profiles.

Dietary supplements are advancing at a 9.12% CAGR, leveraging e-commerce to tout clinical evidence. Combination products marry beta-glucan with vitamin D or zinc for synergistic immune support, while fucoidan supplements, though niche, grow as oncology and cardiovascular data accumulate. Owing to the rising consumption of dietary supplements, the use of beta-glucan in various supplements is increasing. According to the Council for Responsible Nutrition data from 2023, dietary supplement usage among adults in the United States was 74%. Pharmaceutical demand rises for wound-care dressings and immunomodulatory adjuncts, and cosmetics use fucoidan-rich serums to meet clean-beauty expectations. Emerging animal-nutrition lines integrate beta-glucan to meet antibiotic-reduction mandates in aquaculture and pet segments.

Geography Analysis

Europe held 34.35% of the market share in 2025, driven by a robust oat-processing infrastructure in Scandinavia, strict Novel Foods regulations that benefit incumbents with pre-market authorization, and EFSA-approved health claims that allow premium pricing for beta-glucan-fortified products. Finland and Sweden are home to major oat mills supplying food-grade beta-glucan to breakfast cereal manufacturers and bakery ingredient distributors across the European Union. Germany and the United Kingdom are key markets for dietary supplements, where consumer awareness of beta-glucan's cholesterol-management benefits sustains consistent demand for encapsulated yeast-derived formulations. France and Italy are experiencing increased interest in clean-label bakery products featuring beta-glucan as a natural fiber source, though regulatory compliance costs and labeling challenges limit smaller regional brands. The Netherlands acts as a logistics hub for seaweed-derived fucoidan imports from Asia, with Dutch cosmetic companies leading in marine-active formulations utilizing fucoidan's anti-aging properties.

The Asia-Pacific region is expected to grow at a CAGR of 9.96% from 2026 to 2031, driven by China's expansion of yeast-fermentation capacity, Japan's advancements in fucoidan research, and Australia's focus on sustainable seaweed aquaculture. China's dietary supplement market is growing rapidly, supported by rising disposable incomes and greater health awareness among urban consumers, with yeast beta glucan positioned as a premium immune-support ingredient. Japan's pharmaceutical and cosmetic industries have been at the forefront of fucoidan applications, leveraging extensive research into brown seaweed bioactives and strong consumer acceptance of marine-sourced ingredients. South Korea's beauty brands are incorporating low-molecular-weight fucoidan into sheet masks and essence formulations, capitalizing on the K-beauty trend and consumer willingness to pay premium prices for scientifically validated actives. Australia's seaweed aquaculture sector is attracting investments from ingredient suppliers seeking sustainable fucoidan sources that align with environmental, social, and governance (ESG) criteria demanded by European and North American buyers. India's growing supplement market presents opportunities for cost-effective beta glucan formulations, though regulatory uncertainty around health claims and limited consumer awareness hinder short-term growth.

North America shows consistent demand for oat and barley beta glucan in breakfast cereals, functional beverages, and bakery products, with the United States accounting for the majority of regional consumption. Canada's natural health product regulations permit structure-function claims for beta glucan supplements, creating a supportive environment for dietary supplement brands. In Mexico, a growing middle class and rising health awareness are driving demand for fortified foods and immune-support supplements, though price sensitivity favors lower-cost beta glucan sources over premium fucoidan formulations. South America and the Middle East remain emerging markets, with Brazil and Argentina showing localized interest in immune-support supplements. Meanwhile, Saudi Arabia and the United Arab Emirates are importing halal-certified beta glucan ingredients for regional food manufacturers.

Competitive Landscape

The global beta-glucan and fucoidan market is characterized by fragmentation, reflecting a diverse landscape of ingredient suppliers, contract manufacturers, and vertically integrated food conglomerates. Established players mitigate raw-material volatility through long-term supply agreements with yeast producers and seaweed farmers. In contrast, smaller entrants focus on niche areas such as organic certification, non-GMO verification, or proprietary extraction technologies. Vertical integration is gaining traction, with seaweed processors acquiring downstream cosmetic brands to enhance margins and control product positioning. Similarly, yeast-fermentation companies are collaborating with dietary supplement marketers to co-develop branded ingredients that command premium pricing. Growth opportunities exist in areas such as pharmaceutical-grade fucoidan for drug-delivery applications, precision-fermented polysaccharides that address seaweed supply constraints, and personalized nutrition platforms that customize beta-glucan dosing based on individual microbiome profiles.

Technology adoption plays a critical role in distinguishing market leaders from competitors. Advanced analytical tools enable suppliers to provide batch-specific certificates of analysis, molecular-weight profiling, and bioactivity assays, which support premium pricing in pharmaceutical and cosmetic markets. Patent portfolios covering innovative extraction methods, formulation technologies, and therapeutic applications create significant barriers to entry and generate licensing revenue streams, particularly for multinational ingredient companies with dedicated intellectual property teams. Smaller players are finding success by focusing on sustainability certifications, transparent supply-chain documentation, and direct-to-consumer brands that bypass traditional retail channels.

Regulatory expertise remains a key competitive advantage. Established suppliers are better equipped to navigate complex regulatory frameworks, including EFSA health-claim dossiers, FDA GRAS affirmations, and Novel Foods authorizations, compared to regional entrants with limited regulatory resources. Emerging disruptors, such as precision-fermentation startups, are developing microbial platforms to produce fucoidan-like polysaccharides without relying on seaweed harvesting. However, the commercial viability of these innovations depends on achieving cost parity with traditional extraction methods.

Beta Glucan And Fucoidan Industry Leaders

Lantmännen

Kerry Group plc

The Merck Group

Kemin Industries

DSM-Firmenich

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Tate & Lyle announced a strategic partnership with BioHarvest to develop next-generation plant-based ingredients using botanical synthesis technology, enabling sustainable production of non-GMO plant-derived ingredients without traditional agricultural constraints. The collaboration aims to create more affordable and accessible ingredients for the food and beverage industry.

- November 2024: Tate & Lyle completed the USD 1.8 billion acquisition of CP Kelco, creating a leading global specialty food and beverage solutions business with enhanced capabilities in pectin and nature-based ingredients. The merger positions the combined entity to better serve consumer demands for healthier and sustainable food options.

- October 2024: Lesaffre acquired a 70% stake in Biorigin, a Brazilian company specializing in yeast-derived products for human and animal nutrition, enhancing production processes and expanding the supply of yeast derivatives, including beta-glucans.

- October 2023: Baneo, a producer of functional fibre ingredients, launched its first barley beta-glucan ingredient, Orafti B-Fit. The product claims to be used in foods like breakfast cereals, bread, baked goods, dairy alternatives, and pasta.

Global Beta Glucan And Fucoidan Market Report Scope

Fucoidan is a long-chain sulfated polysaccharide found in various species of brown algae. Commercially available fucoidan is commonly extracted from the seaweed species Fucus vesiculosus, Cladosiphon okamuranus, Laminaria japonica, and Undaria pinnatifida. Beta-glucans (beta-glucans) comprise a group of β-D-glucose polysaccharides naturally occurring in the cell walls of cereals, bacteria, and fungi, with significantly differing physicochemical properties dependent on the source.

The beta-glucan and fucoidan market is segmented into product type, application, and geography. By Product type, the market is segmented into beta-glucan and fucoidan. Beta-glucan is further segmented into the soluble and insoluble categories. On the basis of application, the market is segmented by food and beverages, pharmaceuticals, dietary supplements, cosmetics and personal care, and others. The market is segmented by geography into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Beta Glucan | Soluble |

| Insoluble | |

| Fucoidan |

| Food and Beverages |

| Pharmaceuticals |

| Dietary Supplements |

| Cosmetics and Personal Care |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| Product Type | Beta Glucan | Soluble |

| Insoluble | ||

| Fucoidan | ||

| Application | Food and Beverages | |

| Pharmaceuticals | ||

| Dietary Supplements | ||

| Cosmetics and Personal Care | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the beta glucan and fucoidan market?

The beta glucan and fucoidan market size reached USD 845.77 million in 2026 and is projected to rise to USD 1.19 billion by 2031.

Which product type dominates sales?

Beta glucan held 70.88% of global share in 2025, driven by its regulatory status and broad application reach.

Which application is growing the fastest?

Dietary supplements are forecast to grow at a 9.12% CAGR as post-pandemic immune-health spending persists.

Which region is expected to expand most rapidly?

Asia-Pacific is poised for a 9.96% CAGR through 2031, led by China, Japan, and Australia.

Page last updated on: