Capsicum Market Size and Share

Capsicum Market Analysis by Mordor Intelligence

The capsicum market size was valued at USD 45.90 billion in 2025 and estimated to grow from USD 48.20 billion in 2026 to reach USD 61.30 billion by 2031, at a CAGR of 4.93% during the forecast period (2026-2031). Production economics are shifting as growers adopt greenhouse automation and robotics that cut labor costs by up to 40% while delivering premium, year-round fruit. Retailers reward this reliability with price premiums, tilting competitive advantage away from low-wage open-field regions toward capital-intensive controlled environments. Demand for capsaicinoid-rich chili cultivars in nutraceutical extraction is rising, prompting seed breeders to release hybrids that favor biochemical yield over cosmetic traits. Investments in desert greenhouses across the Middle East and in high-tech facilities in North America signal that access to capital and technology now matters more than acreage scale when capturing share in the capsicum market.

Key Report Takeaways

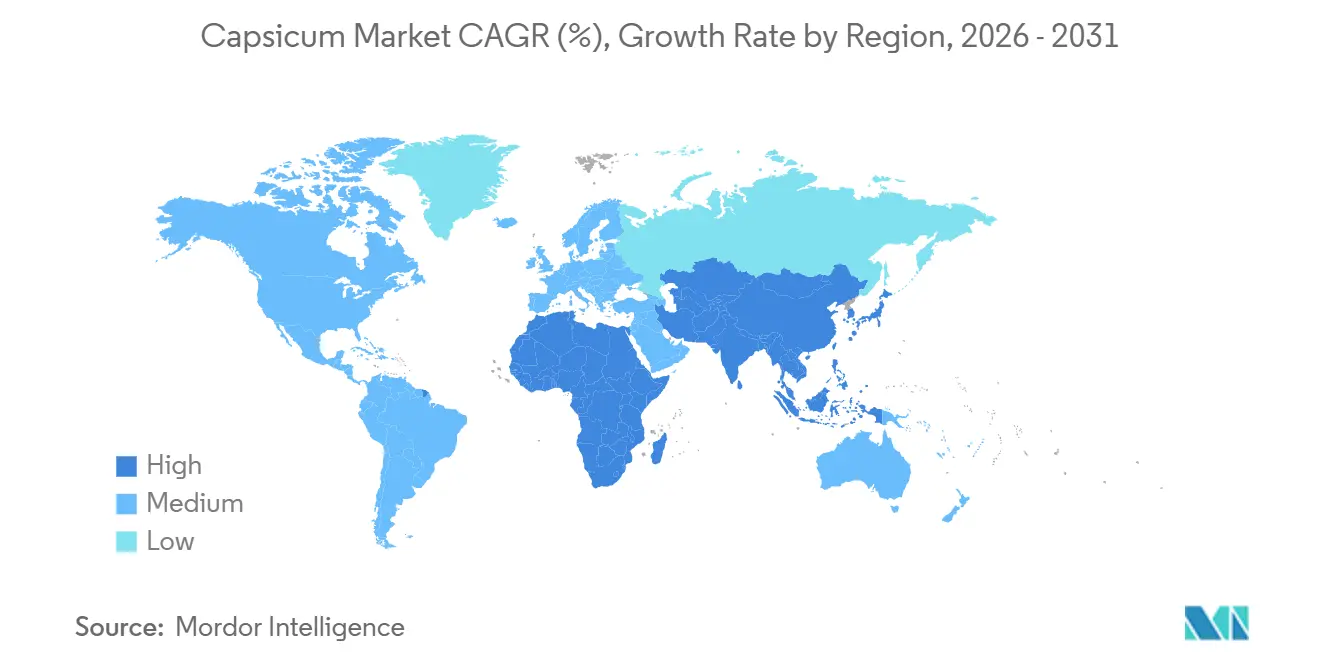

- By geography, Asia-Pacific led with 42.8% of the capsicum market size in 2025, and the Middle East is projected to log the fastest regional CAGR of 8.4% by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Capsicum Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advancements in labor-saving protected cultivation | +1.2% | North America, Western Europe, and the Middle East | Medium term (2-4 years) |

| Increasing demand from nutraceutical extractors | +0.6% | North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Growth of controlled-environment farming clusters | +1.0% | Middle East, Mexico, China, and India | Medium term (2-4 years) |

| Government incentives for greenhouse development | +0.5% | Canada, Europe, and the Middle East | Short term (≤ 2 years) |

| Adoption of blockchain-based produce traceability | +0.4% | India, China, United Arab Emirates, and Europe | Long term (≥ 4 years) |

| Surge in cross-border e-commerce for fresh produce | +0.5% | China, Vietnam, and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Advancements in Labor-Saving Protected Cultivation

Robotics and high-wire growing systems have reduced labor costs by 30% to 40% in greenhouse capsicum, facilitating year-round production of premium-grade produce. These premium grades achieve retail price premiums of 20% to 35% compared to field-grown alternatives. In November 2024, Ontario Plants Propagation inaugurated a USD 75 million propagation greenhouse in Glencoe, incorporating robotic growing techniques and advanced biosecurity measures. This facility supplies tomato, cucumber, and pepper starter plants across Canada and the United States, with plans for three additional 13-acre phases. Automated pollination drones and vision-guided harvesting arms further reduce reliance on seasonal labor, a significant advantage amid tightening labor supply caused by immigration restrictions and wage inflation in North America and Western Europe. Protected cultivation also extends growing seasons in northern regions, enabling Canadian and Dutch growers to compete with Mexican and Spanish imports during winter months when open-field production ceases. The adoption of automation is driving industry consolidation, as smaller growers often lack the capital to upgrade legacy structures with robotic systems, leaving mid-market players at risk of margin compression.

Increasing Demand from Nutraceutical Extractors

Capsaicinoid and carotenoid extraction contracts encourage growers to cultivate higher-value hot-pepper varieties. Pharmaceutical and supplement manufacturers offer premiums of 40% to 60% over fresh-market prices for capsicum with verified capsaicinoid concentrations exceeding 50,000 Scoville Heat Units. Nutraceutical demand for capsaicinoid extracts, used in pain-relief topicals, weight-management supplements, and anti-inflammatory formulations, grew by 12% annually between 2024 and 2025. This growth is driven by clinical evidence linking capsaicin to benefits in metabolic health and chronic pain management. Greenhouse systems provide precise control over stress factors such as water deficit and nutrient restriction, which enhance capsaicinoid synthesis. These systems enable contract growers to meet pharmaceutical-grade specifications that open-field production cannot consistently achieve. India and Mexico are emerging as key sourcing hubs for nutraceutical extractors, offering low production costs, expanding greenhouse infrastructure, and proximity to Active Pharmaceutical Ingredient (API) manufacturing clusters.

Government Incentives for Greenhouse Development

Carbon-credit-linked subsidies reduce capital costs for closed-loop greenhouses, driving acreage expansion in regions that recognize horticulture as a climate-mitigation strategy. In April 2023, British Columbia introduced a point-of-sale carbon tax exemption for commercial greenhouse growers, reducing the cost of natural gas and propane used for heating and CO₂ production by 80%. This policy change improved cash flow for pepper, tomato, and cucumber producers in the province. The exemption replaced a reimbursement-based relief grant, facilitating the adoption of energy-efficient heating systems and combined heat and power units that qualify for additional provincial incentives. In the European Union, member states provide investment grants covering 30% to 50% of greenhouse construction costs through rural development programs, contingent on meeting energy-efficiency and water-recycling standards aligned with the European Green Deal. These subsidies primarily benefit larger operators capable of managing application complexities and co-financing requirements, further widening the competitive gap between well-capitalized greenhouse companies and underfunded open-field growers.

Growth of Controlled-Environment Farming Clusters

New mega-greenhouse parks in desert and temperate regions are increasing global supply and addressing seasonality gaps. Pure Harvest Smart Farms operates climate-controlled facilities in the United Arab Emirates, producing tomatoes, peppers, and cucumbers year-round while using 90% less water compared to open-field systems. This approach aligns with Gulf food security priorities under national diversification strategies. Saudi Arabia's Vision 2030 framework has allocated USD 3.2 billion to agricultural infrastructure through 2025, focusing on protected horticulture projects to reduce import dependency and promote rural employment [1]Source: Vision 2030, “Agriculture and Food Security,” vision2030.gov.sa . Controlled-environment clusters further support vertical integration by enabling growers to co-locate packing, cooling, and logistics facilities, thereby shortening supply-chain lead times and minimizing post-harvest losses.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Thrips-borne Tomato spotted wilt virus outbreaks | -0.8% | North America, South America, and Mediterranean Europe | Short term (≤ 2 years) |

| Escalating greenhouse energy costs | -0.6% | Northern Europe, Canada, and Russia | Medium term (2-4 years) |

| Increasing maximum residue-limit enforcement | -0.4% | Europe, Asia-Pacific, and North America | Medium term (2-4 years) |

| Water-stress-driven yield volatility | -0.3% | South America, Southern Europe, Africa, and India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Maximum Residue-Limit Enforcement

Stricter Maximum Residue Limit (MRL) checks at European ports have resulted in shipment rejections and higher compliance costs. The European Food Safety Authority's (EFSA) Rapid Alert System for Food and Feed recorded 47 rejections of pepper imports in 2024 and 2025 due to pesticide residues exceeding European Union limits, with most cases originating from Turkey, Egypt, and India [2]Source: European Food Safety Authority, “Rapid Alert System for Food and Feed,” ec.europa.eu. European Union Regulation 396/2005 establishes Maximum Residue Limits (MRLs) that are often 10 to 50 times lower than Codex Alimentarius standards, creating significant compliance challenges. Exporters are required to implement expensive residue-testing programs and adopt integrated pest management practices to reduce synthetic pesticide use. Rejected shipments lead to additional costs, including demurrage fees, disposal expenses, and reputational damage. This can pose a risk to long-term supply contracts. Consequently, exporters are compelled to redirect shipments to less-restrictive markets in the Middle East and Asia, often at discounted prices. In 2025, Japan also tightened Maximum Residue Limit (MRL) enforcement for capsicum imports, mandating pre-shipment certificates of analysis and traceability documentation, which increased export logistics costs by 5 to 8%.

Water-Stress-Driven Yield Volatility

Drought cycles in major production regions have resulted in unpredictable open-field pepper yields. In 2024, Chile and Peru experienced yield reductions of 20 to 30% due to prolonged water shortages in the Atacama and coastal valleys, compelling growers to leave land fallow or shift to crops requiring less water. Similarly, Spain's Almería region, which accounts for 40% of Europe's winter pepper supply, faced irrigation restrictions in 2024 and 2025 as reservoir levels dropped below 30% capacity. Regional authorities prioritized urban and tourism water needs, limiting allocations for agriculture. Open-field pepper cultivation, which requires 600 to 800 mm of water per growing season, remains highly susceptible to climate variability, particularly in semi-arid areas lacking irrigation infrastructure or groundwater reserves. While greenhouse systems with closed-loop water recycling can reduce water consumption by 70 to 90%, the high capital investment required makes them inaccessible for many growers in water-stressed developing regions. In India, erratic monsoon patterns in Maharashtra and Karnataka led to pepper yield declines of 15 to 20% in 2024, tightening domestic supply and driving retail prices up by 25 to 35% in urban markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

Asia-Pacific accounted for 42.8% of revenue in 2025, driven by China's domestic greenhouse clusters in Shandong and Liaoning provinces, which supply urban retail markets, and Vietnam's export-oriented open-field production, which shipped USD 1.3 billion in 2024, rising to USD 1.5 billion in 2025 [3]Source: USDA ERS, “Vegetable and Pulses Data Products,” ers.usda.gov . The region is projected to grow moderately, aligning with the global average. China's greenhouse sector is expanding significantly, while India's open-field production is stagnating due to water stress and fragmented supply chains. In 2025, Japan implemented stricter enforcement of Maximum Residue Limits (MRLs) for capsicum imports, requiring pre-shipment certificates and traceability documentation. This development benefits Vietnamese and Chinese exporters with advanced digital infrastructure, rather than smaller suppliers in Indonesia and Thailand.

The Middle East is the fastest-growing region, with a projected CAGR of 8.4% by 2031. Growth is driven by investments in desert greenhouse parks in the United Arab Emirates and Saudi Arabia, aligned with national food-security strategies under Saudi Vision 2030, which allocated USD 3.2 billion to agricultural infrastructure through 2025. Western Asia's growth is supported by greenhouse expansion in Iran and Jordan, where subsidized energy and government co-financing reduce capital barriers. However, geopolitical instability and sanctions limit access to technology and hinder diversification of export markets. In Africa, growth is led by Kenya and Egypt, which supply European winter markets with open-field peppers. However, these producers face increasing competition from Spanish and Dutch greenhouse operations offering superior shelf life and traceability.

North America's growth is constrained by high energy costs in Canadian greenhouses and labor shortages in the United States' open-field operations. Meanwhile, Mexico's greenhouse sector benefits from Inter-American Development Bank financing and proximity to the United States retail markets. In Russia, growth remains limited due to minimal investment in greenhouse production and reliance on imports from Turkey and China. Domestic production is concentrated in low-tech open-field systems near Moscow and St. Petersburg. In Oceania, Australia's greenhouse sector primarily serves domestic retail markets and niche export opportunities to Singapore and Hong Kong. However, high labor costs and electricity prices limit its competitiveness against Asian imports.

Competitive Landscape

The capsicum market stakeholders include producers, importers, exporters, among others. Chinese provincial enterprises anchor volume segments, leveraging economies of scale and government-backed credit lines to expand greenhouse acreage rapidly. North American firms such as NatureSweet invest heavily in proprietary genetics and eco-label certifications that secure shelf space in premium chains. Spice conglomerates, led by McCormick, have carved out integrated procurement systems that bundle volume contracts and forward hedging to stabilize input costs.

Technology partnerships proliferate: sensor platform providers collaborate with seed companies to marry phenotyping data with breeding objectives, enhancing varietal performance under resource-efficient greenhouse regimes. Strategic thrusts concentrate on vertical integration and digitization. Producers acquiring downstream processing units capture greater value from demand for oleoresin and dried spice, insulating themselves from fresh-price oscillations. Blockchain pilot projects in South America demonstrate how small cooperatives can leapfrog traceability requirements and access high-margin export channels.

Joint ventures between European retailers and North African growers secure winter supply windows, illustrating how geography-driven partnerships counteract energy-price disparities. Competition is further shaped by access to skilled labor and agronomic advisory services that optimize yield ceilings for each microclimate. Mergers and acquisitions activity intensifies as mid-tier farms seek scale economies in energy and compliance overheads. Financial investors favor operations with demonstrated ESG (Environmental, Social, and Governance) metrics and renewable-energy integration, anticipating stricter disclosure rules in major importing regions.

Recent Industry Developments

- July 2025: The United States Department of Agriculture (USDA) implemented the Supplemental Disaster Relief Program, allocating USD 16.09 billion of the total USD 30.78 billion funding to support producers for crop losses, including capsicum due to disasters, with Stage 1 focusing on indemnified losses from existing crop-insurance claims.

- March 2025: Oasthouse Ventures announced plans to build the largest greenhouse facility in the United States in Virginia, representing a USD 1.1 billion investment that will create 118 jobs and inject significant capital into domestic food security infrastructure. The project targets completion in 2026 and aims to reduce reliance on imported produce through advanced sustainable farming practices.

- April 2024: Gardin Agritech and Bayer Crop Science expanded their collaboration on water management optimization in pepper cultivation, achieving 25% water usage reduction without yield compromise through advanced phenotyping technologies and real-time plant-health monitoring systems.

Global Capsicum Market Report Scope

Calcium is an essential mineral and alkaline earth metal (symbol Ca, atomic number 20) necessary for developing strong bones and teeth, as well as supporting nerve function, muscle contraction, and blood clotting. The Capsicum Market Report is Segmented by Geography (North America, Europe, and More). The Report Includes Production Analysis (Volume), Consumption Analysis (Value and Volume), Import Analysis (Value and Volume), Export Analysis (Value and Volume), Wholesale Price Trend Analysis and Forecast, List of Key Players, Regulatory Framework, Logistics and Infrastructure, and Seasonality Analysis. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

| North America | United States | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Canada | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Mexico | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Europe | Spain | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Germany | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Italy | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Netherlands | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Russia | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Asia-Pacific | China | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| India | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistic and Infrastructure | ||

| Seasonality Analysis | ||

| Japan | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Vietnam | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Indonesia | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| South America | Brazil | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Chile | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Argentina | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Peru | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Middle East | Saudi Arabia | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Turkey | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Iran | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| United Arab Emirates | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Africa | South Africa | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Nigeria | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Egypt | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Kenya | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| By Geography | North America | United States | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Canada | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Mexico | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Europe | Spain | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Germany | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Italy | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Netherlands | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Russia | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Asia-Pacific | China | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| India | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistic and Infrastructure | |||

| Seasonality Analysis | |||

| Japan | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Vietnam | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Indonesia | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| South America | Brazil | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Chile | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Argentina | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Peru | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Middle East | Saudi Arabia | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Turkey | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Iran | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| United Arab Emirates | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Africa | South Africa | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Nigeria | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Egypt | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Kenya | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

Key Questions Answered in the Report

How large is the capcium market in 2026 and what growth is projected?

The capsicum market size is USD 48.20 billion in 2026, and projected grow with 4.93% CAGR by 2031.

Why are Middle Eastern countries investing heavily in greenhouse pepper production?

Subsidized energy, scarce water, and national food security mandates drive desert greenhouse projects that cut water use by up to 90% and secure local food supply.

How does blockchain affect capsicum exports?

Blockchain traceability enables exporters to verify residue test results and origin data, unlocking 15% to 25% premiums in European and Middle Eastern markets.

What are the main risks facing open-field pepper growers?

Key threats include thrips-borne Tomato Spotted Wilt Virus, water-stress-driven yield swings, and stricter enforcement of pesticide residue limits at major import ports.

Page last updated on: