Garlic Market Size and Share

Garlic Market Analysis by Mordor Intelligence

The garlic market size is projected to expand from USD 21.17 billion in 2025 and USD 22.40 billion in 2026 to USD 29.69 billion by 2031, registering a CAGR of 5.80% between 2026 to 2031. Growing consumer interest in cardiovascular and metabolic wellness, rising penetration of aged garlic extract in supplements, and the rapid uptake of dehydrated and fermented formats across foodservice channels are shaping near-term revenue momentum. Large buyers are hedging against fresh-crop price swings by locking in multi-year contracts for granulated and black garlic, while the commercialization of tissue-culture seeds lifts yields in emerging production belts. Regulatory vigilance on sulfur dioxide residues increases compliance costs but also encourages exporters to adopt controlled-atmosphere storage and natural sprout inhibitors. Investment in blockchain traceability is beginning to earn retail premiums, particularly in high-income markets where provenance, pesticide history, and cold-chain integrity drive consumer trust.

Key Report Takeaways

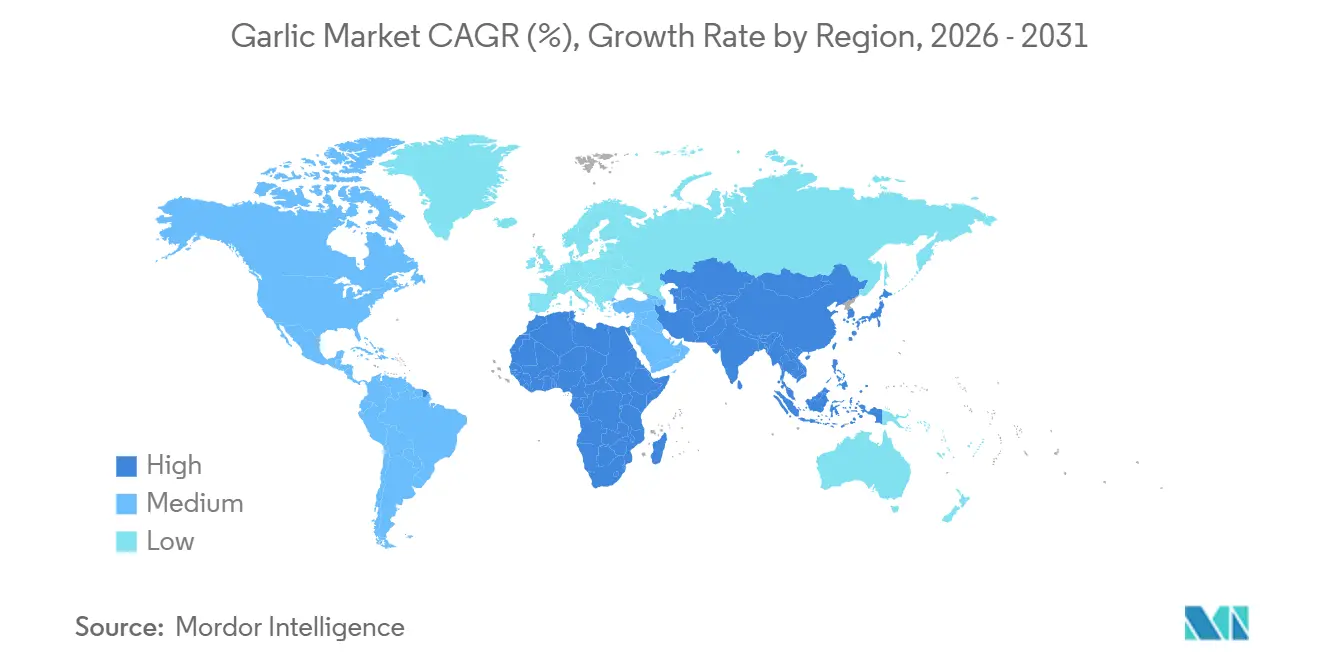

- By geography, the Asia-Pacific region led with 55.2% of the garlic market share in 2025. Africa is forecast to post the fastest regional expansion, at a 6.8% CAGR, through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Garlic Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health-driven culinary demand surge | +1.2% | Global, peak adoption in North America and Europe | Medium term (2-4 years) |

| Expanding pharmaceutical and nutraceutical usage | +1.5% | North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Rising popularity of processed formats in foodservice | +0.9% | North America, Europe, and Middle East | Short term (≤ 2 years) |

| Fermentation technology unlocking premium black garlic exports | +0.7% | China, South Korea, and North America | Medium term (2-4 years) |

| Blockchain traceability premiums in specialty retail | +0.4% | North America and Europe | Long term (≥ 4 years) |

| Tissue-culture seed commercialization in emerging growers | +0.8% | India, Indonesia, Egypt, and South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health-Driven Culinary Demand Surge

Clinical evidence linking garlic’s organosulfur compounds to reduced low-density lipoprotein cholesterol and systolic blood pressure has elevated the bulb from a flavor enhancer to a functional staple [1]Source: National Center for Complementary and Integrative Health, “Garlic,” nccih.nih.gov. Retailers report steady unit growth as aging consumers fold garlic into heart-healthy diets. Restaurateurs and meal-kit brands highlight garlic-forward dishes, nudging per-capita intake upward. Provenance labels that signal organic or heirloom varieties command price premiums and attract consumers seeking transparency. The momentum amplifies baseline volume across both fresh and processed channels, giving producers an incentive to document cultivation practices and secure third-party certifications.

Expanding Pharmaceutical and Nutraceutical Usage

Aged garlic extract rich in S-allylcysteine migrated from niche supplement to core ingredient in mainstream cardiovascular and immune formulations, validated by 2025 peer-reviewed trials that show superior bioavailability after thermal aging [2]Source: Applied Sciences, “Influence of Thermal Processing on Black Garlic,” mdpi.com. Large buyers, such as NOW Health Group, specify International Organization for Standardization (ISO) and Good Manufacturing Practice (GMP) credentials, driving vertical integration from tissue-culture seed to solvent-free extraction. Buyers reward suppliers who can furnish batch-level chromatograms that verify the sulfur profile and absence of residue, thereby widening margins for compliant processors. Rising regulatory scrutiny on health claims in the United States and European Union further differentiates suppliers with clinical dossiers.

Rising Popularity of Processed Formats in Foodservice

Commercial kitchens shift to dehydrated, minced, and granulated garlic as hourly wages for seasonal pickers rise in California. Dehydrated supply removes prep labor, improves shelf stability, and smooths flavor across multi-unit chains. OFI reported granulated-garlic shortages in 2024, prompting long-term supply contracts that lock growers into processor pipelines [3]Source: OFI Investor Relations, “Q2 2025 Earnings Report,” ofi.com. The movement compresses fresh-bulb volume but lifts unit values for processors who secure dehydration capacity adjacent to production zones. Export flows benefit as dehydrated garlic faces fewer quarantine inspections than fresh bulbs.

Fermentation Technology Unlocking Premium Black Garlic Exports

Turnkey fermenters automate multi-stage temperature and humidity cycles, cutting processing time from 30 days to 22 days while preserving S-allylcysteine levels. Chinese equipment suppliers offer modular units that handle batches ranging from 30 kilograms to 2,000 kilograms, lowering entry barriers for mid-tier processors in South Korea and Australia. Black garlic retails at three to five times the price of fresh garlic bulbs and enjoys a shelf life of over 18 months, which underpins export programs into high-income markets. Premium positioning aligns with consumer interest in fermented superfoods, providing processors with a buffer against fluctuations in commodity prices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Weather-driven price and yield volatility | -0.6% | China, India, and California | Short term (≤ 2 years) |

| Rising labor shortages and mechanization gaps | -0.5% | North America, Europe, and China | Medium term (2-4 years) |

| Sulfur-dioxide residue phytosanitary rejections | -0.3% | China export lanes to North America and Europe | Medium term (2-4 years) |

| Growing acceptance of low-odor allium substitutes | -0.2% | North America and Europe convenience segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Weather-Driven Price and Yield Volatility

Chinese weather shocks reduced 2024 output and increased global prices, allowing Indian exporters to capture market share. California acreage suffered from white rot across 22,000 acres, resulting in a reduction in 2023 production. Such swings force processors to hold higher safety stocks or chase spot cargoes at elevated rates. Climate variability narrows optimal harvest windows, raising the risk of undersized bulbs or post-harvest losses. Growers answer with precision irrigation and crop monitoring, yet capital outlay constrains smallholders.

Rising Labor Shortages and Mechanization Gaps

Garlic remains hand-planted and hand-harvested because bruising undermines fresh-market grades. Seasonal worker shortages intensify as wages rise, and mechanized harvesters remain cost-prohibitive for small-scale farms. Production shifts toward dehydration-friendly cultivars that tolerate mechanical handling, but this reduces the availability of jumbo fresh bulbs, which are prized in export lanes. Prolonged shortages could cap output growth in high-wage regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

The Asia-Pacific region led with 55.2% share of the garlic market in 2025, supported by China’s output and integrated dehydration lines that supply the global garlic market. India stepped in as a swing exporter during Chinese weather disruptions, underscoring the interdependence of the regional garlic market. Indonesia remains import-dependent, with 564.1 thousand metric tons of inflows in 2023. Tissue-culture adoption could increase domestic output and reduce reliance on Chinese supply. Vietnam and Thailand operate as re-export hubs, arbitraging tariff gaps inside Southeast Asia.

Africa registers the fastest expansion at 6.8% CAGR. Egypt shipped 21,965 metric tons between January and August 2024, leveraging proximity to European ports and looser congestion at the Suez corridor. South Africa’s urbanizing middle class boosts per capita intake, and cold-chain investments improve year-round availability. Funding for irrigation and tissue-culture labs will determine whether the region translates hectare expansion into sustained export competitiveness.

North America remains consumption-heavy yet production-light. United States acreage declined as white rot and wage inflation pressured Californian growers, prompting importers to source more from Mexico and Spain. The Department of Commerce reaffirmed anti-dumping duties for Chinese transshipments through third countries, prompting tighter origin documentation and increasing landed costs. Canada’s 24.2 thousand metric tons import volume shows persistent demand, while Mexico balances domestic consumption with shipments northward during price spikes.

Competitive Landscape

Fresh garlic remains fragmented among thousands of smallholders across China and India, yet value-added sub-segments are concentrated. Christopher Ranch cultivates more than 45,350 metric tons annually and commands a strong brand presence in United States supermarkets. Shandong Liancheng and Jining Fenduni dominate dehydrated export lanes, leveraging low-cost Chinese feedstock and scale dehydration capacity to hold cost leadership positions. Zhengzhou Wenming Machinery sells fermentation equipment that underpins smaller entrants in Australia and South Korea, shifting margin capture toward technology providers.

Strategy polarization defines competition. Commodity-oriented exporters compete on price and shipment reliability. Differentiated players chase premiums via organic certification, blockchain traceability, and clinical validation of bioactive content. Patent filings covering two-stage humidity curves for black garlic fermentation increased between 2022 and 2025, indicating rapid innovation and potential for licensing revenue. Investments in tissue-culture propagation laboratories extend beyond seed sales into royalty streams on proprietary genetics.

Regional challengers gain traction. Egyptian exporters can leverage shorter freight times to the European Union, thereby undercutting Chinese transit times. Indian labs supplying virus-free seed capture value by contracting acreage in Indonesia and East Africa, effectively exporting technology. Mid-tier processors in North America import bulbs from Argentina and convert them into granulated powder near foodservice hubs, offsetting high labor costs through automation. The collective share of the top five processors in value-added formats signals a moderately concentrated premium tier.

Recent Industry Developments

- January 2025: The Department of Agriculture (DA) in Manila declared the implementation of a PHP 3 billion (USD 53.7 million) cold storage project to minimize post-harvest losses and maintain a stable supply for vegetables, high-value crops, including garlic.

- January 2025: Indonesia's Ministry of Trade has accelerated the import of 35,600 metric tons of garlic to stabilize retail prices ahead of Ramadan, with 21,000 metric tons scheduled to arrive in March 2025 and 14,600 metric tons in April 2025. This strategic procurement underscores how import-dependent markets buffer domestic shortfalls through coordinated government intervention.

- November 2024: Malaysia's government committed RM 12 million (USD 2.69 million) for 2025 to expand and modernize the onion supply chain, targeting 30% self-sufficiency by 2030 through infrastructure investments in irrigation, storage, and drying facilities, alongside technical assistance and training for growers.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global garlic market as the value generated from fresh, semi-processed, and fully processed garlic traded through formal and informal channels across households, foodservice, nutraceutical, and industrial ingredient uses. Value is expressed in constant 2025 US dollars at the producer-to-first-buyer level.

Scope exclusion: ornamental garlic varieties grown solely for landscaping are not considered.

Segmentation Overview

- By Geography

- North America

- United States

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Canada

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Mexico

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- United States

- Europe

- Spain

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Ukraine

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- France

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- United Kingdom

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Russia

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Spain

- Asia-Pacific

- China

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- India

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Indonesia

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Vietnam

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Myanmar

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- South Korea

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- China

- South America

- Brazil

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Argentina

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Brazil

- Middle East

- Iran

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Turkey

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Iran

- Africa

- Egypt

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- South Africa

- Production Analysis (Area Harvested, Yield, and Production Volume)

- Consumption Analysis (Consumption Value and Volume)

- Import Market Analysis (Import Value, Volume, and Key Supplying Markets)

- Export Market Analysis (Export Value, Volume, and Key Destination Markets)

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- List of Key Players

- Logistics and Infrastructure

- Seasonality Analysis

- Egypt

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed growers in Shandong, exporters in Gujarat, bulk buyers in Rotterdam, and supplement formulators in California. These conversations validated informal trade volumes, average peel loss, and emerging price premiums for organic bulbs.

Desk Research

We began by mapping production, trade, and price patterns using open datasets such as FAOSTAT, UN Comtrade, and ITC-Trade Map. We then overlaid them with regional farm census updates and USDA GAIN notes to capture weather and policy shifts. National horticulture boards, the European Spice Association, and peer-reviewed journals on allicin yield trends helped us refine quality adjustments. Company 10-Ks and customs filings, accessed via D&B Hoovers and Dow Jones Factiva, completed the desk evidence pool. This list is illustrative; many other public and subscription sources informed the work.

Market-Sizing & Forecasting

A hybrid top-down build (global harvest volume × utilization matrix × weighted farm-gate price) set the baseline, which was then cross-checked with sampled supplier roll-ups and channel checks for processed forms. Key variables include sown area, yield per hectare, bulb-to-processed conversion ratios, cold-chain expansion pace, freight rates, and supplement penetration in major consumer markets. Forecasts rely on multivariate regression linking these drivers with five-year moving averages and scenario analysis for climate volatility. Gaps in county-level data were bridged through regional averages agreed upon during primary interviews.

Data Validation & Update Cycle

Before sign-off, outputs pass a three-layer analyst review where divergences over +/-5% versus external indicators trigger re-checks. Models refresh annually, while significant events such as export bans prompt interim updates, ensuring clients receive the latest view.

Why Mordor's Garlic Baseline Commands Reliability

Published figures frequently diverge because firms pick different product mixes, price points, and refresh cadences. By anchoring our model to full-spectrum utilization and the latest 2025 harvest data, Mordor minimizes these gaps for decision-makers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 38.15 B (2025) | Mordor Intelligence | - |

| USD 2.84 B (2024) | Regional Consultancy A | Focus only on dehydrated formats; excludes fresh and informal trade |

| USD 21.59 B (2023) | Global Consultancy B | Omits Africa & MEA volumes and relies on retail scanner data, not farm output |

The comparison shows that narrower scopes or dated baselines compress the market picture, whereas Mordor's disciplined variable set and yearly refresh offer a balanced, transparent reference point.

Key Questions Answered in the Report

What is the projected global revenue for the garlic market in 2031?

The garlic market will reach USD 29.69 billion by 2031, rising at a 5.80% CAGR.

Which region led global sales in 2025?

In 2025, Asia-Pacific held 55.2% of revenue due to China's dominant production base.

Why are processed garlic formats gaining share?

Dehydrated and minced products cut kitchen labor, lower spoilage, and face lighter border inspections than fresh bulbs.

How are nutraceutical trends influencing demand?

Mainstream cardiovascular and immune supplements now specify aged garlic extract rich in S-allylcysteine, driving an 8.7% CAGR in the pharmaceutical channel through 2031.

What technology reduces black garlic fermentation time?

Automated fermenters with programmable humidity and temperature profiles shorten cycles from 30 days to 22 days while retaining bioactive strength.

Which factor most threatens short term supply stability?

Weather variability in China, India, and California causes abrupt yield swings that ripple through global prices.

Page last updated on: