Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 14.15 Billion |

| Market Size (2026) | USD 14.57 Billion |

| Market Size (2031) | USD 16.85 Billion |

| Growth Rate (2026 - 2031) | 2.95% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Home Appliances Market Analysis by Mordor Intelligence

The France home appliances market size is projected to expand from USD 14.15 billion in 2025 and USD 14.57 billion in 2026 to USD 16.85 billion by 2031, registering a CAGR of 2.95% between 2026 to 2031. The pace of growth reflects policy-driven replacement and premiumization instead of volume-led expansion, with regulations shaping product choices and procurement patterns [1]Directorate-General for Energy, “Ecodesign and Energy Labelling Framework,” European Union, eur-lex.europa.eu. Structural headwinds from housing and inflation in 2025 receded in 2026 as incentives and efficiency rules renewed upgrade cycles for major appliances. Supply-side friction persists because of tariffs on low-cost imports and component tightness that favor established manufacturers with resilient sourcing. Retail dynamics continue to shift toward omnichannel journeys where installation services and after-sales care decide the final point of sale.

Key Report Takeaways

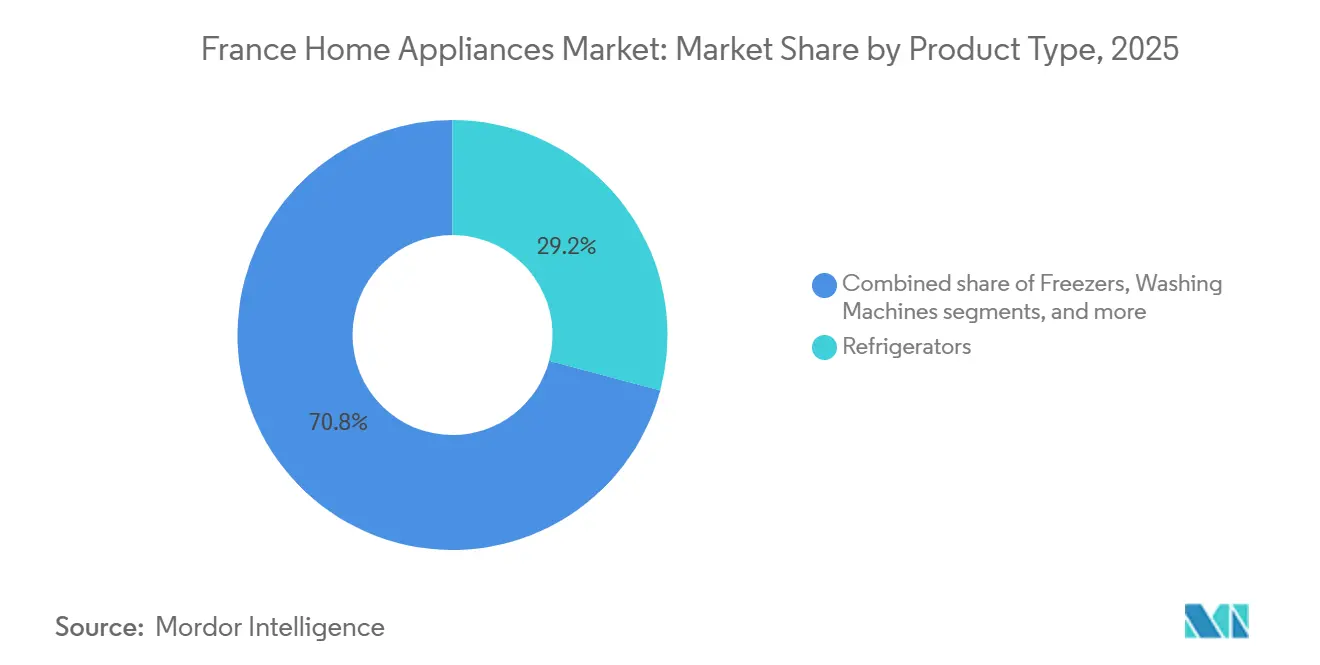

- By product type, refrigerators led with 29.16% of the France home appliances market share in 2025, while air fryers recorded the fastest projected growth at a 4.21% CAGR through 2031.

- By distribution channel, multi-brand stores held 46.72% of the France home appliances market share in 2025, while online recorded the highest projected CAGR at 4.74% through 2031.

- By geography, Île-de-France accounted for 21.84% of the France home appliances market share in 2025, while the Provence-Alpes-Côte d’Azur is forecasted as the fastest-growing region at a 3.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Home Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-efficiency regulations accelerating replacement demand | +0.7% | National, with early gains in Paris, Lyon, and Marseille metropolitan areas | Short term (≤ 2 years) |

| E-commerce and omnichannel convenience fueling purchases | +0.5% | Global, strongest in Île-de-France and urban centers above 100,000 population | Medium term (2-4 years) |

| Refurbished-appliance boom under France's Anti-Waste Law | +0.3% | National | Medium term (2-4 years) |

| Heat-wave induced surge in residential cooling demand | +0.4% | PACA, Nouvelle-Aquitaine, Occitanie; spill-over to Île-de-France | Short term (≤ 2 years) |

| Government heat-pump incentives lifting hybrid appliance sales | +0.6% | National, with early gains in owner-occupied housing markets | Medium term (2-4 years) |

| Smart-home interoperability standards (e.g., Matter) spurring connected-appliance uptake | +0.4% | APAC core, spill-over to Western Europe (France, Germany, UK) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Energy-Efficiency Regulations Accelerating Replacement Demand

France’s rental restrictions on low-performing properties continue to compress decision windows for landlords, which lifts near-term replacement of large appliances aligned with higher efficiency grades [2]Policy Team, “MaPrimeRénov’ 2025 Guidance and RGE Requirements,” Service-Public.fr, service-public.fr. The new EU Ecodesign and energy labeling updates reinforce design targets and practical repair rules that favor efficient refrigerators and heat-pump-based solutions for domestic heating and cooling. National policy signals around the repairability index and spare parts availability also push buyers toward brands with documented durability and upgrade paths [3]Legal Directorate, “Repairability and Durability Index Rules Under AGEC,” Légifrance, legifrance.gouv.fr.. A parallel reform pipeline for building performance certificates creates compliance pressure that flows directly into appliance replacement timelines. Installed base realities still matter since gas systems remain widespread in French housing, and policy shifts continue to pivot owners toward electrified alternatives supported by appliance-grade controls and monitoring.

E-Commerce and Omnichannel Convenience Fueling Purchases

Digital discovery and checkout keep gaining ground as shoppers compare models, energy labels, and delivery promises before completing transactions online or in-store. Retailers that bundle installation, warranty, and service plans convert higher-value baskets more reliably, and this shapes how premium refrigeration, dishwashers, and built-in ovens move through the France home appliances market. Brand-owned direct channels surface for flagship launches, pairing first-party data with controlled logistics for white goods and connected kitchen suites. Click-and-collect helps bridge last-mile constraints on bulky products while preserving service quality around delivery windows and setup. Clear pricing of delivery and installation fees remains a trust drive that reduces cart abandonment and anchors loyalty in a hybrid shopping model.

Refurbished-Appliance Boom Under France's Anti-Waste Law

The AGEC framework and public-procurement quotas for reconditioned equipment are expanding the secondary channel for major appliances and small domestic devices. The repair bonus and spare parts obligations are reshaping ownership costs, which supports refurbished purchases for budget-sensitive households and institutions. Collection and refurbishment partnerships between retailers and ecosystem actors increase the flow of used units suitable for a second life, which sustains scale for certified repairers and refurbishers. Manufacturers with established refurbishment programs and published durability data can carry brand trust into the reconditioned channel. Awareness and service-network density still shape outcomes since access to qualified repairers influences the practical utility of bonuses and the speed of refurbishment cycles.

Heat-Wave Induced Surge in Residential Cooling Demand

Successive hot summers and regional heat events are reshaping household priorities toward cooling-ready solutions that complement winter heating. Air-to-air and air-to-water heat pumps that provide both heating and cooling are gaining policy support and consumer interest, which lifts crossover demand for hybrid comfort systems within the France home appliances market. Appliance buyers weigh energy labels, refrigerant profiles, and controllability as they navigate higher summer peaks and indoor air comfort considerations. Regional disparities in cooling penetration and grid readiness drive uneven adoption, with southern regions advancing faster than the northwest. Incentive design and installer availability influence the pace of household conversion, which can defer some installations into subsequent fiscal periods.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inflation-driven squeeze on discretionary spending | -0.8% | National, with acute pressure on households in E/F/G DPE-rated properties | Short term (≤ 2 years) |

| Semiconductor/component shortages are lengthening product lead-times | -0.4% | Global supply chains affect premium smart appliance availability in France | Short term (≤ 2 years) |

| Housing-market slowdown dampening first-time appliance purchases | -0.6% | National, concentrated in Paris and secondary cities, with stalled construction permits | Medium term (2-4 years) |

| Mandatory long repairability periods are delaying replacements | -0.3% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Inflation-Driven Squeeze on Discretionary Spending

Elevated prices and financing costs have delayed some upgrade cycles for non-essential appliances such as dryers and countertop devices. Household budgets in lower energy-performance homes feel higher energy burdens, which reduces headroom for premium purchases. Consumers gravitate to models with strong durability scores or loyalty-linked service programs that lower the total cost of ownership. Promotions and buy-now-pay-later options help with smooth demand but do not fully offset macro pressure. This restraint narrows the market for mid-tier SKUs while supporting entry-level value and top-tier connected products that promise measurable savings.

Semiconductor/Component Shortages Lengthening Product Lead-Times

Embedded electronics and controls continue to face tight supply, and this limits availability for advanced connected appliances and high-spec refrigeration. Longer lead times channel demand toward readily available models or to brands with diversified sourcing footprints. Manufacturers are adding regional capacity and smart factories to cushion volatility in critical components. Retailers prioritize inventory for faster-moving SKUs, which can defer niche launches or limit customization options. The France home appliances market absorbs these frictions through omnichannel allocation and staggered release schedules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Air Fryers Redefine Countertop Economics

Refrigerators commanded 29.16% of France’s 2025 home appliance revenue, and air fryers are the fastest riser with a 4.21% CAGR through 2031, which sets the tone for a mixed cycle of anchor categories and high-velocity countertop devices. Refrigeration continues to premiumize with connected control, food preservation sensors, and modular designs that align with energy labeling and interoperability expectations. Flagship cooling lines emphasize freshness, cameras, and app-driven optimization to reduce waste and improve convenience. For the countertop set, air fryers benefit from convenience and health positioning that compress cook times and energy use for small batches. This barbell pattern supports both value-driven countertop wins and steady demand for core kitchen anchors in the France home appliances market.

The France home appliances industry also sees differentiated replacement cycles, as washing machines and dishwashers hold long lifespans under repairability rules, while premium tiers add features that justify upgrades. Built-in ovens and cooking systems gain share in urban kitchens where space and design drive choices, and connectivity helps with guided cooking and safety. Cooling and air treatment categories expand when heat events intensify, and hybrid HVAC aligns with broader building standards and subsidies. Across major appliances, brands emphasize efficiency, smart scheduling, and remote diagnostics to reduce lifetime costs and service downtime. These product attributes reinforce the upgrade case even as budgets remain tight in parts of the France home appliances market.

By Distribution Channel: Online Claws Share, Yet Installation Services Anchor Offline

Multi-brand stores held 46.72% of 2025 revenue, and online is the fastest-growing route with a 4.74% CAGR to 2031, underscoring a hybrid path for complex purchases and last-mile service. Offline channels maintain strength in built-in appliances that require certified installation and in-home service coordination. Retail service plans and extended warranties assure buyers that repairs and spare parts will be readily available under the Anti-Waste for a Circular Economy Law (Loi AGEC) framework. Direct-to-consumer pilots for premium refrigerators and laundry lines bring first-party relationships into focus for replenishment and firmware updates. Clear disclosure of delivery timing and installation fees helps resolve trust barriers that have historically slowed white-goods e-commerce in the France home appliances market.

The France home appliances industry benefits from click-and-collect and showrooming that cut delivery risk for large SKUs while keeping selection and price transparency online. Exclusive brand boutiques showcase top-tier cooling and cooking systems and convert high-intent buyers who want a hands-on demo before purchase. Marketplaces retain an edge in small domestic appliances where standard parcel delivery works, and installation is not required. Retailers and brands are refining returns and take-back flows to meet environmental targets while maintaining customer satisfaction. These shifts point to an allocation model where channel roles are defined by service intensity and the complexity of the product being sold in the France home appliances market.

Geography Analysis

Île-de-France holds the largest revenue contribution with a 21.84% share in 2025, which aligns with the premium mix and early adoption of connectivity in large-city households, while the Provence-Alpes-Côte d’Azur is forecasted to grow at 3.15% CAGR through 2031. Smart meter coverage and tariff tools improve the use case for connected controls in cooling and refrigeration, which heightens interest in integrated suites. Buyers in the region tend to evaluate food preservation, noise, and space efficiency in built-ins and narrow-depth refrigeration. Retail showrooms for flagship brands support trials and conversions at higher price points. The France home appliances market is shaped by these metro dynamics as they set trends for features and service expectations.

In the south, climate-driven demand is shifting category priorities as households plan for more frequent hot summers. Cooling-capable systems and efficient refrigerators rise in consideration sets as owners balance comfort, energy use, and policy incentives. Local installer availability and RGE certification throughput guide installation timing for heat pumps and connected controls. Retailers respond with inventory and service capacity tuned to seasonal peaks. These conditions reinforce a durable regional tilt that favors climate-resilient categories within the France home appliances market.

Secondary cities and the broader “rest of France” cohort rely on practical efficiency, durable construction, and accessible service networks that align with AGEC repairability rules. Take-back and refurbishment access varies by locality, and stronger networks enable more second-life outcomes that delay new purchases for value-seeking households. Where construction and household formation are steady, white goods follow, with built-in adoption tied to kitchen renovations and modular designs. Policy consistency across regions sustains common energy-labeling expectations for appliance choices. That regulatory baseline supports steady progress toward efficient and connected units in the France home appliances market.

Regulatory Landscape

France home appliances demand and product design are shaped by the EU Ecodesign and Energy Labelling framework, alongside national circular-economy rules under the Anti-Waste for a Circular Economy (AGEC) law. A key shift is the rollout of the Durability Index (Environmental Code Article L. 541-9-2, implemented by Decree No 2024-316), which expands beyond repairability by adding reliability and, where relevant, software and hardware upgradability requirements. The transition applied from 8 January 2025 for televisions and 8 April 2025 for washing machines, with the score displayed close to the price and supported by potential administrative fines under Article L. 541-9-4-1.

Energy-efficiency policy also tightened following France's transposition of EU Directive 2023/1791 through Law No 2025-391 (30 April 2025), Ordinance No 2025-979 (14 October 2025), and Decree No 2025-1382 (29 December 2025). The related energy-efficiency framework, including requirements that influence procurement criteria and operational energy-management practices, entered into force on 1 January 2026. It reinforces replacement cycles toward higher-efficiency appliances and tightens compliance across labeling, documentation, and product information obligations for producers and importers.

Competitive Landscape

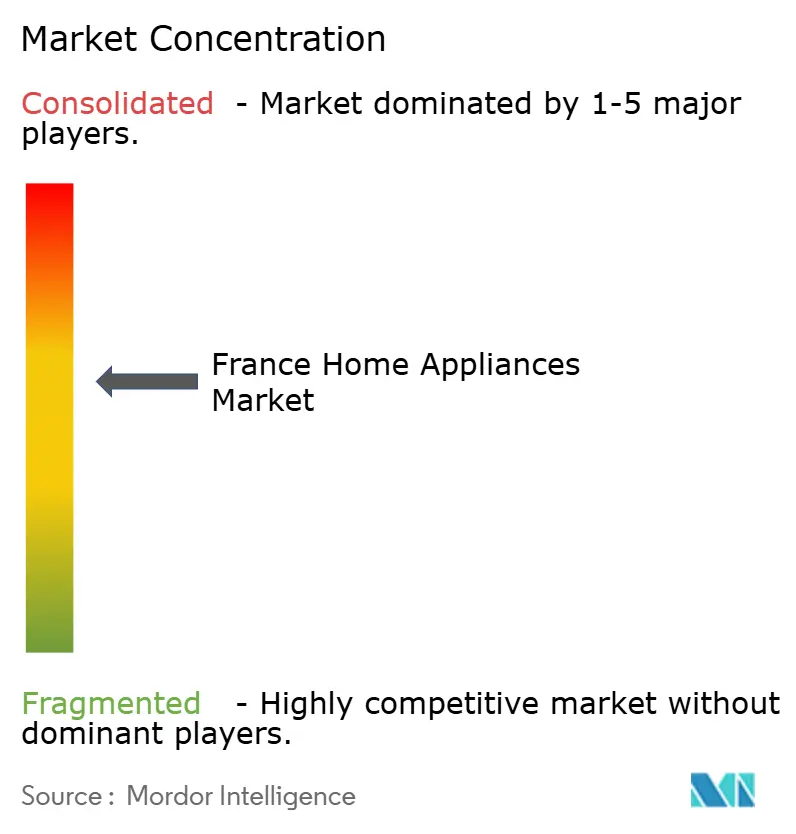

The France home appliances market exhibits medium concentration, with the top five players collectively holding a major market share. Established incumbents and consolidating rivals shape a mid-concentration field where brand scale, research and development, and service infrastructure decide share protection. BSH reported steady turnover momentum and continued investment in manufacturing and connected platforms for flagship cooling and kitchen lines[4]Corporate Media, “Annual Highlights and Production Footprint,” BSH Group, bsh-group.com. Whirlpool streamlined its European footprint by contributing major appliances to a joint venture with Arçelik, while keeping strategic focus on the Americas and select premium lines. Electrolux sharpened its premium emphasis in Europe with AEG branding and product updates on sustainability and care. Asian leaders extend presence through value-led models and progressive connectivity, which intensifies price and feature competition in the France home appliances market.

Strategic moves highlight a push toward robotics, smart kitchens, and regionally diverse production footprints. BSH announced a strategic partnership with robotics expertise to explore novel built-in service concepts, extending the kitchen beyond traditional categories. BSH also opened a refrigerator factory in Monterrey to reinforce North American capacity and resilience in the supply chain for premium formats. Miele refreshed its MasterCool line with advanced freshness, remote viewing, and flexible compartments that showcase premium preservation. Samsung and other brands continue to bring connected refrigerators and AI-assisted features to market through global newsroom announcements, which raises consumer expectations around integration.

Local and global players are also leaning into professional-premium adjacencies that influence high-end residential choices within the France home appliances market. Groupe SEB expanded its professional and premium cookware portfolio with acquisitions that carry design language and brand halos into affluent home kitchens. SharkNinja delivered double-digit growth with strong execution in outdoor cooking, beverage systems, and air purification, which illustrates crossover innovation from small domestic appliances. Beko’s sustainability recognition and extended European scale position it for value-to-mid premium gains as energy and durability needs evolve. Alongside product moves, EU repairability and eco-design rules enforce continuous improvements in durability and transparency that favor brands with deep engineering and service capabilities.

France Home Appliances Industry Leaders

Groupe SEB

BSH Hausgeräte GmbH

Whirlpool Corporation

Electrolux AB

Haier Europe

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Circular-economy compliance is opening room for differentiated offerings and services centered on durability, spare-parts availability, and certified refurbishment. The move from a Repairability Index to a Durability Index (out of 10, incorporating repairability plus reliability and updateability criteria) elevates the value of modular design, documented maintenance, and longer software support windows. Fee eco-modulation mechanisms in the household EEE chain also create financial incentives and penalties tied to repairability performance and recycled content, which supports bundling of longer-life propositions such as extended parts availability, remote diagnostics, and service plans. It also creates scale potential for trade-in, take-back, and reconditioning pathways that align with AGEC information requirements and WEEE obligations.

France-focused investments suggest ongoing momentum behind local production, automation, and capacity for small domestic and kitchen-adjacent appliances. In June 2026, Newell Brands announced a EUR 40 million planned investment for its French operations focused on advanced manufacturing automation and new production line capabilities, and in May 2026 RATIONAL opened an expansion of its Wittenheim plant, doubling production space for iVario Pro equipment. Together with policy-driven emphasis on efficiency and durability information at point of sale, these actions create clearer channels for suppliers and retailers to convert compliance into consumer-facing value, including trusted scoring, installed support networks, and more streamlined repair and refurbishment logistics.

Recent Industry Developments

- July 2026: Amica S.A. acquired rights to use the Sauter brand in France, strengthening its position in the European cooking appliance segment. The move leverages an established French brand name to broaden route-to-market options in built-in cooking and adjacent categories.

- March 2026: Cafom Group acquired Brandt Group brands (Brandt, Sauter, De Dietrich, Vedette) for EUR 18.6 million and announced reindustrialization intentions supported by production partnerships in France. The acquisition reshapes brand ownership and creates new levers for product relaunches and channel negotiations in major appliances.

- January 2025: Groupe SEB acquired La Brigade de Buyer to reinforce its Professional and Premium segment and extend its chef-led brand portfolio. The deal strengthens its positioning in premium kitchen ecosystems that influence high-end consumer purchasing across cookware and small kitchen appliances.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of home appliances sold in France for household use, including both major appliances and small appliances, tracked across typical retail and online channels.

Scope exclusions: We exclude non-household industrial equipment, spare parts sold as standalone items, and extended warranties or service-only contracts that are not bundled with an appliance sale.

Segmentation Overview

- By Product

- Major Home Appliances

- Refrigerators

- Freezers

- Washing Machines

- Dishwashers

- Ovens (Incl. Combi & Microwave)

- Air Conditioners

- Other Major Home Appliances

- Small Home Appliances

- Coffee Makers

- Food Processors

- Grills & Roasters

- Electric Kettles

- Juicers & Blenders

- Air Fryers

- Vacuum Cleaners

- Electric Rice Cookers

- Toasters

- Counter-top Ovens

- Other Small Home Appliances

- Major Home Appliances

- By Distribution Channel

- Multi-Brand Stores

- Exclusive Brand Outlets

- Online

- Other Distribution Channels

- By Geography

- Île-de-France

- Auvergne-Rhône-Alpes

- Provence-Alpes-Côte d’Azur

- Rest of France

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by setting clean boundaries for what counts as a home appliance sale in France, and then building a fact base that can be checked from multiple angles. We rely on public sources such as INSEE for household and macro indicators, Eurostat for trade and price signals, French customs trade statistics for import and export direction, and official EU policy pages on Ecodesign and Energy Labelling that influence replacement cycles.

We also review company filings, investor presentations, retailer announcements, and reputable press to map distribution trends such as online share changes, promotions, and premiumization patterns. Where needed, paid database subscriptions for company financials and intelligence, patent databases, and shipment-level trade data are used to fill gaps around supplier exposure and product innovation timing. The sources listed here are illustrative only, and many additional public references are used during data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work is used to test the desk assumptions with people who see pricing, channel mix, and demand changes in real time, including manufacturers, distributors, retailers, and service ecosystem participants. Interviews and structured surveys also help confirm which appliance categories are rising or slowing in France, and what is driving it, such as energy efficiency upgrades, replacement timing, and promotion intensity across regions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 15% | |

| Mid tier: 45% | Functional/Unit leaders: 37% | |

| Smaller Players: 18% | Managers: 48% |

Market-Sizing & Forecasting

Sizing is built using a top-down demand pool reconstruction for France, where household base, replacement behavior, and category penetration are translated into annual unit demand and then converted to value using price ladders by appliance type. Once the market total is formed, it is corroborated with selective bottom-up checks, such as supplier revenue exposure to France, sampled price points across channels, and volume sense-checks from trade flows, and then adjustments are made where mismatches persist.

Key model inputs include household count and housing turnover, replacement cycles for large appliances, share shift between offline and online channels, promotional intensity that moves average selling prices, and energy efficiency driven upgrades that change mix. To forecast, we use scenario analysis supported by simple regression checks on household spend signals and price inflation indicators, and the assumptions are refined based on what interviewees expect for replacement demand and premium feature adoption. When bottom-up evidence is incomplete for smaller categories, gaps are handled through ratio-based allocation using observed category shares and verified price bands, followed by a second pass to keep totals consistent.

Data Validation & Update Cycle

Validation happens in layers, starting with internal consistency checks so that category totals align with channel totals and implied pricing stays realistic. Outputs are then compared with independent signals, including trade direction, major promotional cycles, and any policy shifts that could move replacement demand, and anomalies are flagged for deeper review.

Before sign-off, the model is reviewed by another analyst and key assumptions are revisited when variances cannot be explained by documented drivers. The report is refreshed annually, and interim updates are made when a material event changes pricing, demand, or channel structure. Right before delivery, a final data pass is done so clients receive the most current view available at that time.

Mordor Intelligence's France Home Appliances Market Market Size Versus Other Published Estimates

Published market sizes for France home appliances do not always match because each study draws its own boundary for what counts as the market, which year is used as the base, and how prices are treated across major and small appliances.

By tracking category level unit demand and channel weighted ASPs, and then refreshing the inclusion rules around major versus small appliances, Mordor Intelligence keeps the 2025 value anchored to a clear France-only consumption scope, while some sources mix in broader retail definitions or different base-year pricing patterns.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 14.15 B (2025) | |

| Global Consultancy A | USD 16.34 B (2024) | Uses a different base year and a faster growth path, and the scope is typically framed around retail market value with channel definitions that can inflate pricing effects versus a category-mix approach. |

| Industry Publisher B | USD 8.70 B (2023) | Starts from an earlier base year and appears to apply a narrower product boundary or different category grouping, which can leave out parts of small appliances and understate replacement-driven value. |

The spread mainly comes from base-year choice and what is counted inside the home appliance basket, and those two decisions can move totals quickly when prices and mix are changing. Using transparent unit, price, and channel checks makes the estimate easier to follow and repeat, and it also helps keep the forecast tied to realistic replacement and upgrade behavior in France.

Key Questions Answered in the Report

What is the current size and growth outlook for the France home appliances market?

The France home appliances market size is estimated to reach USD 14.57 billion in 2026 and is projected to reach USD 16.85 billion by 2031 at a 2.95% CAGR for 2026–2031.

Which product categories are leading and growing fastest in France?

Refrigerators led with 29.16% revenue share in 2025, while air fryers are projected as the fastest-growing product with a 4.21% CAGR through 2031.

How are channels evolving for appliance sales in France?

Multi-brand stores held 46.72% of 2025 revenue, while online is the fastest-growing route at a 4.74% projected CAGR through 2031, indicating a durable hybrid model for delivery and installation.

Which region contributes most to France’s appliance demand?

Île-de-France accounted for 21.84% of 2025 revenue, supported by premium built-ins and higher connected adoption in metropolitan households.

What policy factors most influence appliance purchases in France?

Ecodesign and repairability rules, MaPrimeRénov’ incentives, and building performance standards guide replacement toward efficient and connected units while extending lifespans through repair.

How are brands competing in premium and connected segments?

Leading brands expand R&D, smart platforms, and service programs, with examples including BSH’s factory expansion and Miele’s MasterCool refresh, while others optimize portfolios and invest in regional manufacturing.

Page last updated on: